Specialty Pharmaceuticals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

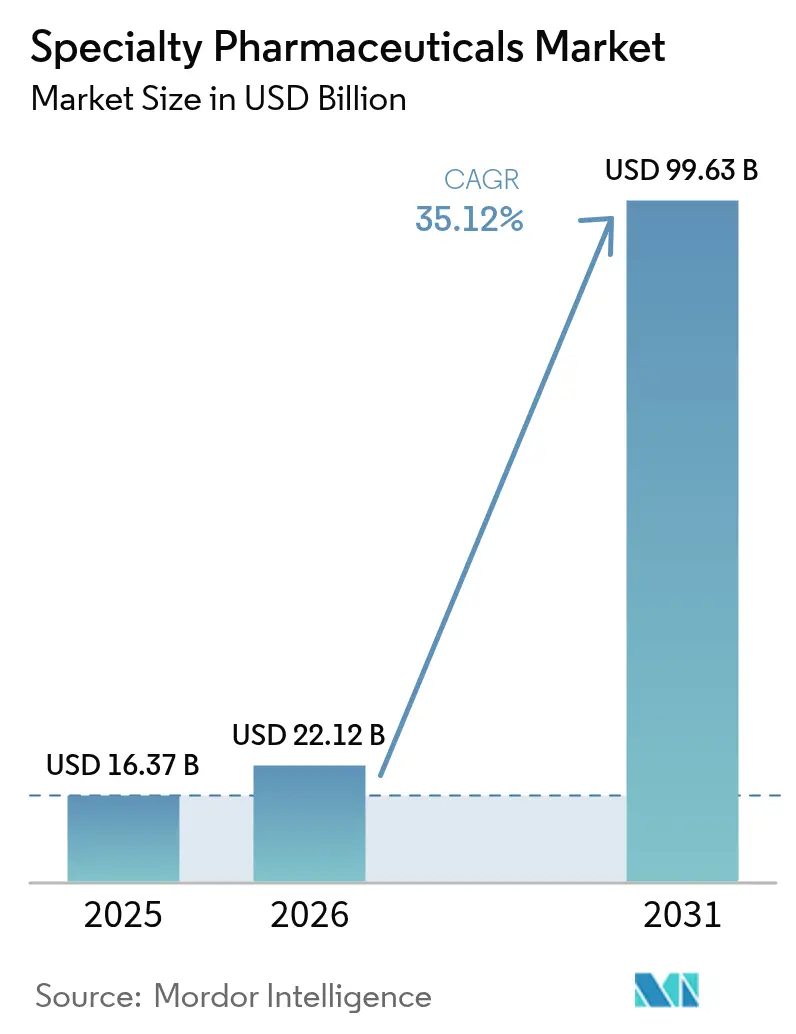

| Market Size (2026) | USD 22.12 Billion |

| Market Size (2031) | USD 99.63 Billion |

| Growth Rate (2026 - 2031) | 35.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Specialty Pharmaceuticals Market Analysis by ���ϲ�����

The specialty pharmaceuticals market size was valued at USD 16.37 billion in 2025 and estimated to grow from USD 22.12 billion in 2026 to reach USD 99.63 billion by 2031, at a CAGR of 35.12% during the forecast period (2026-2031). Robust demand for high-complexity therapies, the protection of launch-phase pricing power under the Inflation Reduction Act, and rapid biologics innovation together underpin this steep curve. Checkpoint inhibitor label expansions, orphan-drug designations, and priority-review vouchers are shortening commercialization cycles, while integrated specialty-pharmacy networks improve patient onboarding and adherence. Capital flows into manufacturing led by GLP-1 capacity expansions, CAR-T contract development, and facility retrofits for ultra-cold storage signal sustained interest in new modalities. Payer constraints are tightening, yet outcomes-based agreements and indication-specific pricing carve-outs remain viable access routes for breakthrough assets.

Key Report Takeaways

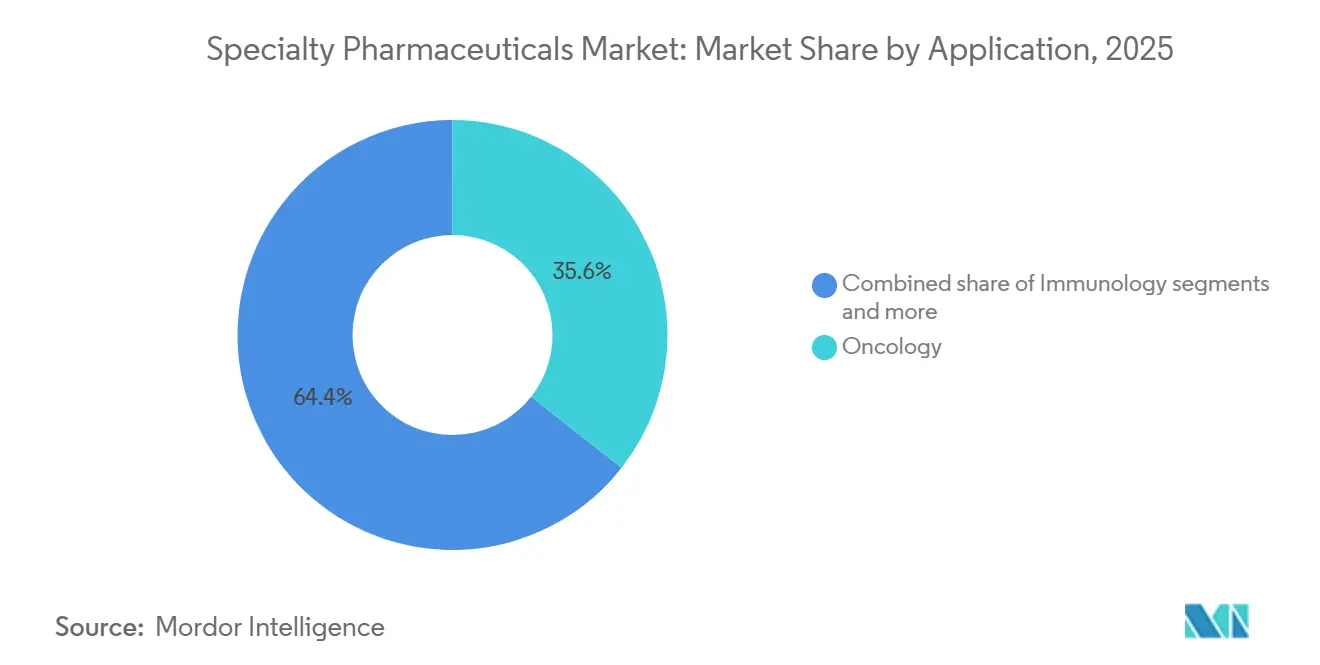

- By application, oncology led with 35.55% of the specialty pharmaceuticals market share in 2025. Rare and orphan disorders are projected to expand at a 36.85% CAGR through 2031.

- By drug class, biologics accounted for 60.53% of the specialty pharmaceutical market in 2025. Gene and cell therapies are advancing at a 37.75% CAGR between 2026-2031.

- By mode of administration, injectables and parenterals accounted for 76.15% of the specialty pharmaceuticals market size in 2025. Intravitreal delivery is growing at a 36.82% CAGR to 2031.

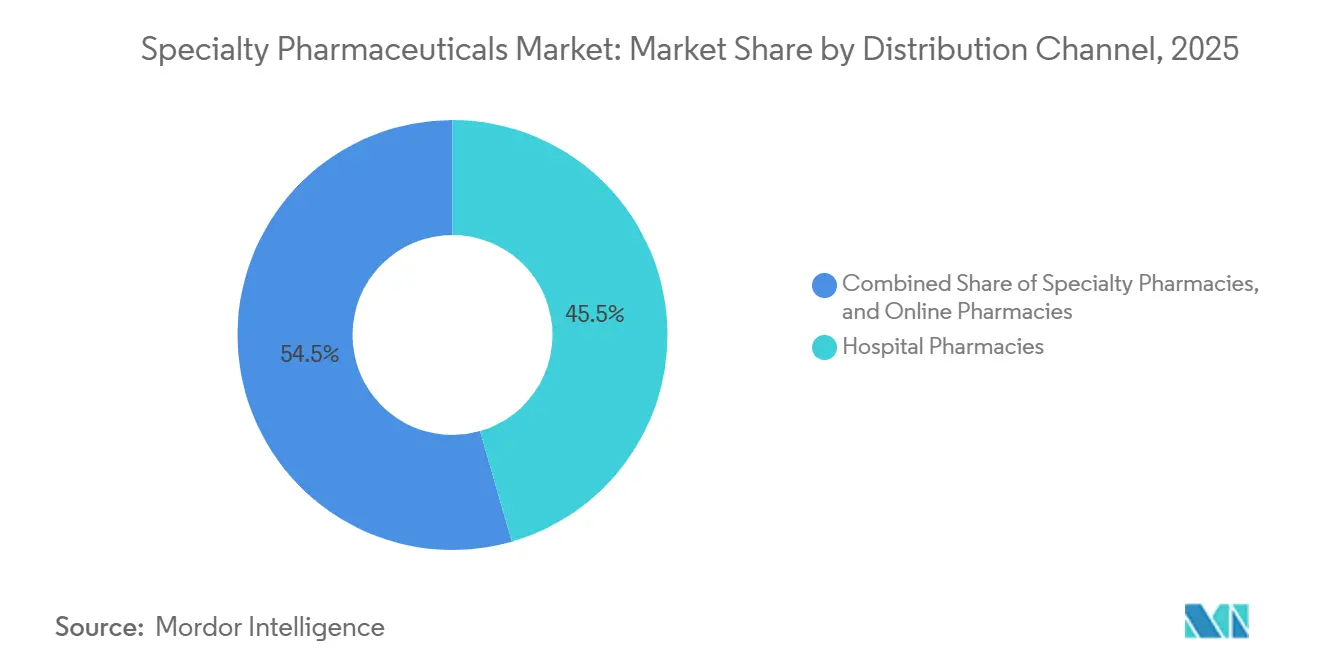

- By distribution channel, hospital pharmacies accounted for 45.52% of revenue in 2025. Online pharmacies are forecast to climb at a 37.12% CAGR through 2031.

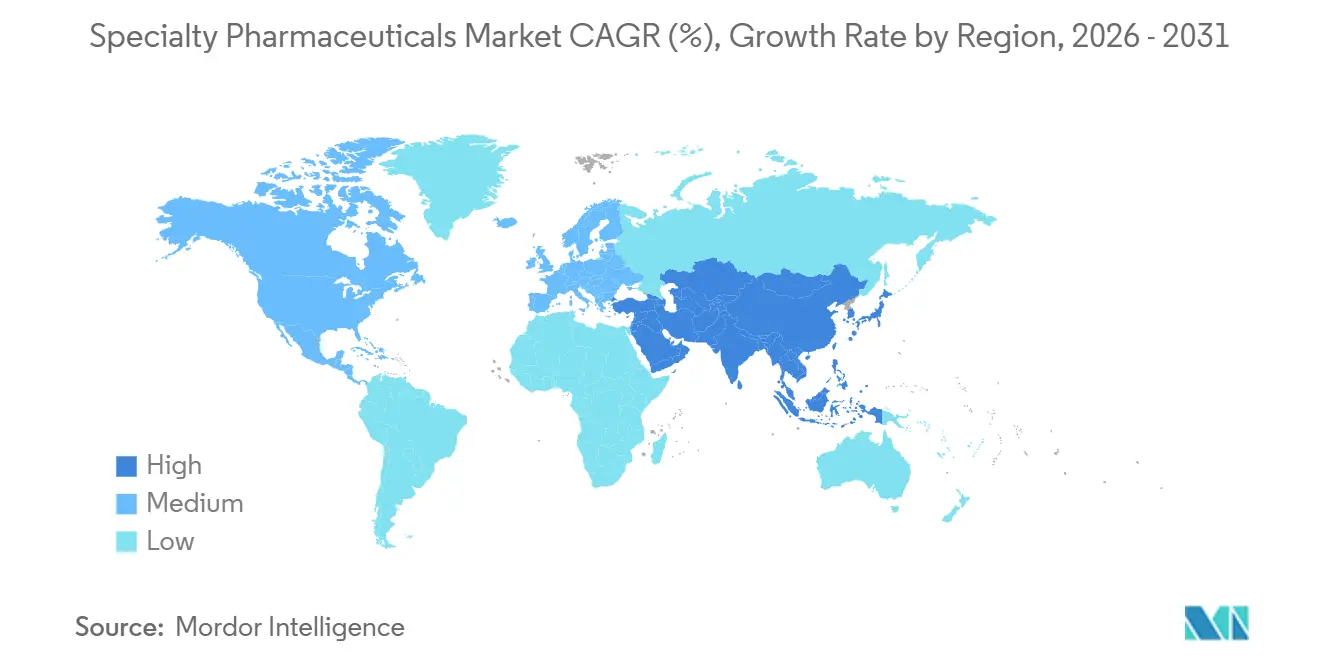

- By geography, North America retained leadership with a 46.62% share in 2025, but Asia-Pacific will post the fastest CAGR of 36.22% through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Specialty Pharmaceuticals Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic & Rare Diseases | +8.2% | Global, with concentration in North America and Europe due to advanced diagnostics | Long term (≥ 4 years) |

| Rapid Expansion of Biologics & Biosimilars Pipeline | +9.5% | Global, APAC gaining share via India and China manufacturing scale-up | Medium term (2-4 years) |

| Growth of Integrated Specialty-Pharmacy Networks | +6.8% | North America core, early adoption in Western Europe | Medium term (2-4 years) |

| Orphan-Drug Priority Review Voucher Arbitrage | +4.1% | United States, with spillover to EU via regulatory harmonization | Short term (≤ 2 years) |

| Pay-for-Performance Contracts Unlocking Niche Access | +6.6% | North America and select EU markets (Germany, UK, Italy) | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising Prevalence of Chronic & Rare Diseases

More than 300 million people live with one of roughly 5,500 recognized rare diseases, yet diagnostic rates remain under 50% in many low- and middle-income countries[1]World Health Organization, “ICD-11 for Mortality and Morbidity Statistics,” who.int.Next-generation sequencing now costs well below USD 1,000 per genome, enabling earlier identification of monogenic disorders and widening the treatment pool for enzyme-replacement and gene therapies. Chronic disease incidence is also climbing; six in ten U.S. adults live with at least one chronic condition, intensifying demand for long-term oncology, immunology, and endocrine regimens. In 2024, the FDA granted 46 orphan-drug designations, including gene therapies targeting Angelman syndrome and pregnancy complications, underscoring sustained sponsor interest in ultra-rare indications[2]U.S. Food and Drug Administration, “Orphan Drug Designations and Approvals,” fda.gov . Accelerated-approval corridors, relied on for 72% of 2025 novel approvals, enable faster market entry but place post-marketing evidence burdens on manufacturers.

Rapid Expansion of Biologics & Biosimilars Pipeline

Seven orphan biologics cleared FDA review in 2024, headlined by the first engineered T-cell receptor therapy and a gene-edited treatment for leukodystrophy. Biosimilars are catching up; U.S. adalimumab analogs captured over 90% penetration by Q4 2024, eroding a USD 21 billion franchise. Europe’s prescribing quotas accelerate similar uptake, although interchangeable rules differ by country, complicating pan-European launches. China approved 82 innovative biologics in 2024, while CDMO majors are racing to open vector suites that reduce lead times from 18 months to near 12 months. Autologous CAR-T manufacture still needs 22-28 days per patient, pressuring innovators to develop off-the-shelf allogeneic platforms.

Growth of Integrated Specialty-Pharmacy Networks

Cardinal Health’s purchase of Specialty Networks typifies the vertical-integration push that merges dispensing, data, and patient support inside one entity. Health-system-owned specialty pharmacies now account for one-quarter of accredited U.S. locations, helping hospitals keep high-cost infused therapies in-house and skirt manufacturer 340B shipment limits. Outcomes-based deals are easier to execute within integrated networks; Zolgensma’s five-year installment model ties payment to motor milestone achievement, and CMS is piloting multi-state risk-pooling for one-time gene therapies. Still, disparate electronic health record systems and non-standardized real-world-evidence formats slow payer assessments of long-term efficacy.

Orphan-Drug Incentives & Favorable Reimbursement

Priority review vouchers sold for USD 100-150 million each through 2024, subsidizing the development of ultra-rare therapies. BioMarin and CSL Behring used voucher proceeds to offset the USD 2.9-3.5 million list prices for their hemophilia gene therapies. The sunset of the U.S. program eliminates this liquidity, while Europe lacks a similar voucher, driving sponsors to secure U.S. exclusivity first, then pursue EMA approval. Japan’s Sakigake pathway offers advice and priority review but lacks a tradable instrument, limiting its financial appeal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Treatment Costs & Payer Cost-Containment | -7.3% | Global, acute in U.S. due to IRA negotiation, Europe via HTA fragmentation | Medium term (2-4 years) |

| Complex Cold-Chain & Handling Logistics | -4.9% | Global, most pronounced in APAC and MEA due to infrastructure gaps | Long term (≥ 4 years) |

| Fragmented Real-World-Evidence Standards Slowing Uptake | -3.2% | Global, with divergence between FDA, EMA, and APAC regulatory frameworks | Long term (≥ 4 years) |

| Sustainability Pressure on Single-Use Delivery Devices | -2.8% | Europe core (EU MDR compliance), expanding to North America via ESG investor mandates | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Escalating Treatment Costs & Payer Cost-Containment

Medicare’s first round of negotiated prices delivered mean discounts of 79%, slashing Enbrel to USD 2,355 and Imbruvica to USD 9,319 per month. Without out-of-pocket caps at USD 2,000 from 2025, plans and manufacturers shoulder greater cost, accelerating formulary exclusions and step-therapy rules. Private PBMs now require metformin trials before GLP-1 coverage, and UnitedHealthcare excluded Zepbound in favor of Wegovy to leverage higher rebates[3]Reuters, “PBMs Tighten GLP-1 Coverage,” reuters.com . Gene-therapy pricing remains contentious; Casgevy’s USD 2.2 million tag faces scrutiny over 20-year durability, yet pivotal data cover only 31 patients. International reference pricing in Germany and other EU markets further compresses launch-year margins.

Complex Cold-Chain & Handling Logistics

Gene-therapy vials shipped at -80 °C incur 15-20% temperature deviations that trigger costly product loss. Treatment centers must install bespoke freezers, limiting Zynteglo and Roctavian access to ~40 U.S. sites. Roche’s Vabysmo permits only 24 hours at room temperature post-refrigeration; breaches require disposal, inflating waste. Dry-ice logistics contribute to a 15 million-ton carbon footprint, drawing ESG scrutiny. Smart containers with GPS and deviation alerts are rolling out, yet hospital inventory systems seldom integrate automatically, delaying dosing. EU Medical Device Regulation now demands lifecycle assessments for single-use injectors, adding compliance cost without delivering reusable alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Oncology Dominance Meets Rare-Disease Acceleration

Oncology retained 35.55% of the specialty pharmaceuticals market share in 2025, driven by checkpoint inhibitors, antibody-drug conjugates, and CAR-T therapies. Rare-disease therapies, while smaller, are set to grow at a 36.85% CAGR through 2031 as the FDA fast-tracks ultra-orphan candidates. The specialty pharmaceuticals market size for oncology is projected to surpass USD 40 billion by 2031, while rare-disease revenue could multiply six-fold on the same horizon. Competitive intensity rises as new PD-1/TIGIT combinations and bispecific antibodies challenge incumbents.

Growth vectors differ. Oncology pipelines prioritize tumor-agnostic indications, whereas rare-disease sponsors focus on first-in-class gene-replacement approaches. Reimbursement hurdles diverge as well: value-based oncology contracts hinge on overall survival endpoints, while orphan therapies often face single-payer negotiations over ultra-high per-patient prices. The player mix reflects that divergence: big pharma dominates oncology, whereas venture-backed biotech maintains leadership positions in diseases with <10,000 patients globally.

By Drug Class: Biologics Lead, Gene Therapies Surge

Biologics accounted for 60.53% of the 2025 specialty pharmaceutical market, buoyed by monoclonal antibodies, fusion proteins, and recombinant enzymes. Gene and cell therapies, though <5% revenue, are set for a 37.75% CAGR to 2031 as manufacturing bottlenecks ease. Within small molecules, targeted kinase inhibitors remain entrenched but face earlier generic erosion.

Commercial dynamics favor biologics for chronic diseases, with high refill frequency sustaining revenue, while one-time gene therapies rely on payer acceptance of multi-million-dollar price tags. Manufacturing scale is the swing factor; a single 2,000-liter bioreactor run can generate USD 500 million of monoclonal antibody supply, whereas autologous cell-therapy capacity remains patient-specific. Platform advances such as CRISPR-based off-the-shelf edits could shift that calculus.

By Mode of Administration: Injectables Prevail, Intravitreal Innovations Accelerate

Injectables accounted for 76.15 of % specialty pharmaceuticals market share in 2025, reflecting the dominance of parenteral biologics[4]Roche Holding AG, “Annual Report 2024,” roche.com. Intravitreal injections, though niche, will advance at a 36.82% CAGR on the back of extended-release port systems and dual-pathway inhibitors. Oral specialty agents hold a loyal niche in oncology and immunology but are not well-suited to clinical settings that demand rapid titration and adherence monitoring.

Patient preference is reshaping formats. Subcutaneous formulations of formerly IV drugs, such as infliximab, increase at-home dosing, while ocular implants, such as refillable ranibizumab reservoirs, reduce clinic visits by 90%. Still, adverse-event monitoring requirements tether many therapies to infusions at certified centers, sustaining procedure-based revenue streams for hospitals.

By Distribution Channel: Hospital Pharmacies Lead, Online Platforms Surge

Hospital pharmacies captured 45.52% of the specialty pharmaceutical market share in 2025, driven by infusion-center dominance. Online pharmacies, predicted to expand at a 37.12% CAGR, leverage telehealth triage, home delivery, and automated prior-authorization engines to win convenience-seeking patients.

Regulatory compliance will separate winners from laggards. Risk Evaluation and Mitigation Strategies restrict the distribution of high-risk therapies, giving accredited specialty networks an advantage over pure-play e-pharmacies. Yet state-level licensure reciprocity is expanding, and Amazon Pharmacy’s national footprint, along with One Medical’s telehealth node, creates an end-to-end virtual channel that could redirect chronic injectable refills away from brick-and-mortar outlets.

Geography Analysis

North America generated 46.62% of 2025 revenue as Medicare Part D specialty spend exceeded USD 133 billion, even before IRA negotiations trimmed headline prices. The United States commands the region through higher unit prices. Keytruda exceeds USD 200,000 annually and dense infusion-center networks. Canada enforces median international pricing, delaying several gene-therapy launches, while Mexico’s social-security expansion broadens biologic access but leaves large uninsured populations exposed.

Europe trails in revenue but leads in biosimilar penetration. Germany’s early benefit assessment and AMNOG negotiations cut list prices by up to 50% within 1 year of launch. France, Italy, and Spain pursue parallel HTA reviews even under the EU’s 2025 joint-assessment regulation, extending market-access timelines by 12-18 months. The United Kingdom’s QALY-based pricing cap keeps many gene therapies in “managed access” schemes.

Asia-Pacific delivers the steepest growth trajectory at a 36.22% CAGR and could match North America’s revenue by 2031. China green-lit 82 novel therapies in 2024, and Beijing’s volume-based procurement lowers prices yet expands volumes. India’s biosimilar export boom benefits from FDA mutual inspections; Biocon and Dr. Reddy’s secure first-to-file slots for denosumab and aflibercept analogs. Japan’s Sakigake pathway speeds review, but biennial price cuts erode five-year revenue curves. Australia, South Korea, and GCC states broaden reimbursement but still negotiate aggressive risk-sharing deals, limiting upside.

Competitive Landscape

Ten manufacturers capture the majority of specialty pharmaceutical market revenue, signaling moderate concentration. AbbVie, Pfizer, Roche, Novartis, Johnson & Johnson, Eli Lilly, Novo Nordisk, Bristol Myers Squibb, Amgen, and Merck dominate oncology, immunology, and metabolic franchises. Consolidation accelerates: Amgen bought Horizon for USD 27.8 billion, acquiring Tepezza for thyroid eye disease; Pfizer paid USD 43 billion for Seagen’s antibody-drug conjugates.

Biosimilars disrupt established cash cows. Humira analogs reached 90% penetration by Q4 2024, collapsing AbbVie’s adalimumab revenue below USD 3 billion. GLP-1 capacity lags demand despite Novo Nordisk and Eli Lilly investing >USD 9 billion in new plants, opening gray-market compounding channels. Gene-therapy pioneers such as Sarepta and Vertex punch above their weight in valuation, leveraging single-asset orphan exclusivity to command multibillion-dollar revenue streams.

Strategy tilts toward digital wrap-arounds. Novo Nordisk’s connected pens transmit adherence data, Eli Lilly’s diabetes platform bundles remote coaching, and Roche’s Foundation Medicine aligns diagnostics with targeted therapy sales. Patent strategies remain aggressive; AbbVie filed >130 Humira patents, delaying biosimilars by eight years, and similar “patent thickets” shield Skyrizi and Rinvoq until late decade. ESG and MDR compliance now influence injector design and carbon accounting, elevating the bar for new entrants.

Specialty Pharmaceuticals Industry Leaders

Teva Pharmaceutical Industries Ltd.

AbbVie, Inc.

Amgen Inc.

Johnson and Johnson

Bristol-Myers Squibb Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The FDA granted breakthrough-therapy designation to Wayrilz (rilzabrutinib) for warm autoimmune hemolytic anemia

- August 2025: SERB Pharmaceuticals agreed to acquire Y-mAbs Therapeutics for USD 412 million in cash, adding Danyelza to its oncology portfolio

Global Specialty Pharmaceuticals Market Report Scope

As per the scope of the report, specialty pharmaceuticals are branded injectables, infusions, or oral medications with high cost and high complexity, with limited or exclusive availability and distribution, that are used to treat chronic or rare diseases.

The specialty pharmaceuticals market is segmented by application, drug class, mode of administration, distribution channel, and geography. By application, the market is segmented into oncology, immunology, endocrinology, infectious diseases, neurology, rare & orphan disorders, cardiovascular, and ophthalmology. By drug class, the market is segmented into biologics, small-molecule specialty drugs, gene & cell therapies, and peptide therapeutics. By mode of administration, the market is segmented into injectable/ parenteral, oral, intravitreal / ocular, and others. By distribution channel, the market is segmented into hospital pharmacies, specialty pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Oncology |

| Immunology |

| Endocrinology |

| Infectious Diseases |

| Neurology |

| Rare & Orphan Disorders |

| Cardiovascular |

| Ophthalmology |

| Biologics |

| Small-molecule specialty drugs |

| Gene & Cell Therapies |

| Peptide Therapeutics |

| Injectable/ Parenteral |

| Oral |

| Intravitreal / Ocular |

| Others |

| Hospital Pharmacies |

| Specialty Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Oncology | |

| Immunology | ||

| Endocrinology | ||

| Infectious Diseases | ||

| Neurology | ||

| Rare & Orphan Disorders | ||

| Cardiovascular | ||

| Ophthalmology | ||

| By Drug Class | Biologics | |

| Small-molecule specialty drugs | ||

| Gene & Cell Therapies | ||

| Peptide Therapeutics | ||

| By Mode of Administration | Injectable/ Parenteral | |

| Oral | ||

| Intravitreal / Ocular | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the specialty pharmaceuticals market by 2031?

It is forecast to reach USD 99.63 billion by 2031 on a 35.1% CAGR trajectory.

Which therapeutic area held the largest share in 2025?

Oncology led with 35.55% specialty pharmaceuticals market share in 2025.

How fast are gene and cell therapies expected to grow?

They are projected to expand at a 37.75% CAGR between 2026-2031.

Why are hospital pharmacies still dominant in distribution?

Many infused and injectable therapies require on-site monitoring, giving hospital pharmacies 45.52% revenue share in 2025.

Which region will grow the quickest through 2031?

Asia-Pacific, propelled by faster regulatory approvals in China and expanding biosimilar exports from India, is set to grow at a 36.22% CAGR.

Page last updated on: