Precision Medicine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

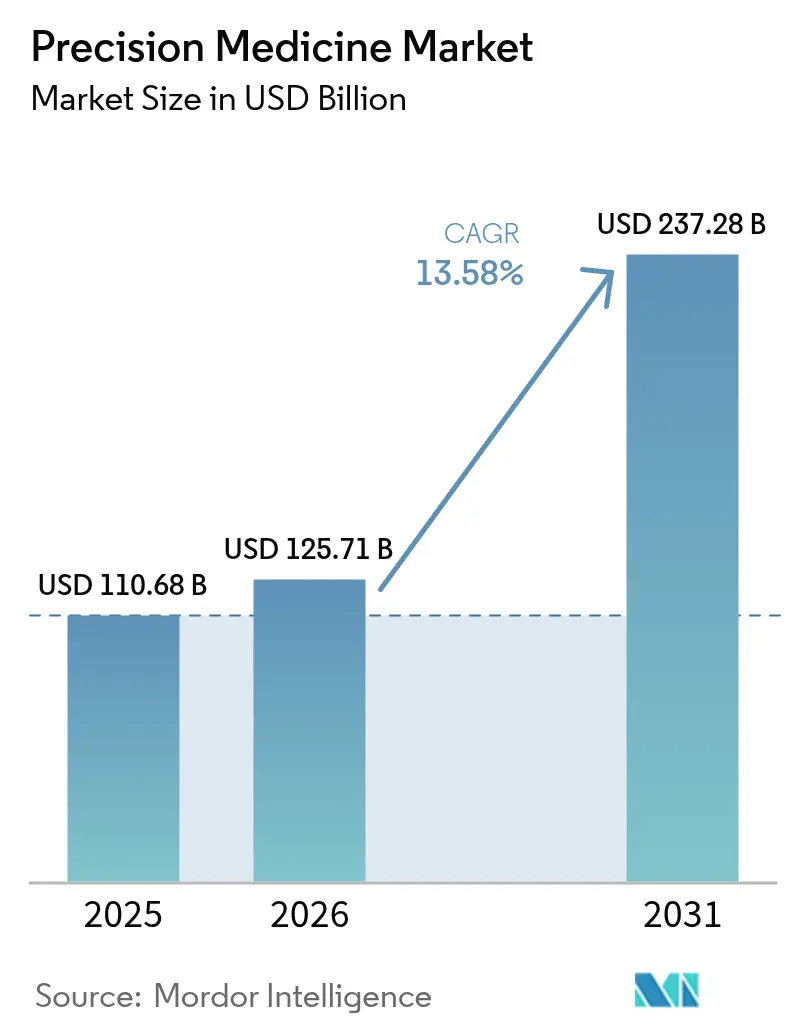

| Market Size (2026) | USD 125.71 Billion |

| Market Size (2031) | USD 237.28 Billion |

| Growth Rate (2026 - 2031) | 13.58% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Precision Medicine Market Analysis by ���ϲ�����

The Precision Medicine Market size is projected to expand from USD 110.68 billion in 2025 and USD 125.71 billion in 2026 to USD 237.28 billion by 2031, registering a CAGR of 13.58% between 2026 to 2031.

Precision biomarker approvals are accelerating because regulators now evaluate data in real time, cutting review cycles and giving drug–diagnostic pairs an earlier commercial window. Industry momentum is reinforced by national genome initiatives that lower discovery costs, by AI-driven diagnostic tools that continuously update using real-world data, and by falling oligonucleotide synthesis cycle times that enable personalized vaccines to be produced same-day. Competition is diverging between platform integrators that monetize data at scale and focused tool vendors that offer best-in-class analytics. Meanwhile, diverging data-sovereignty rules create both compliance costs and regional arbitrage opportunities.

Key Report Takeaways

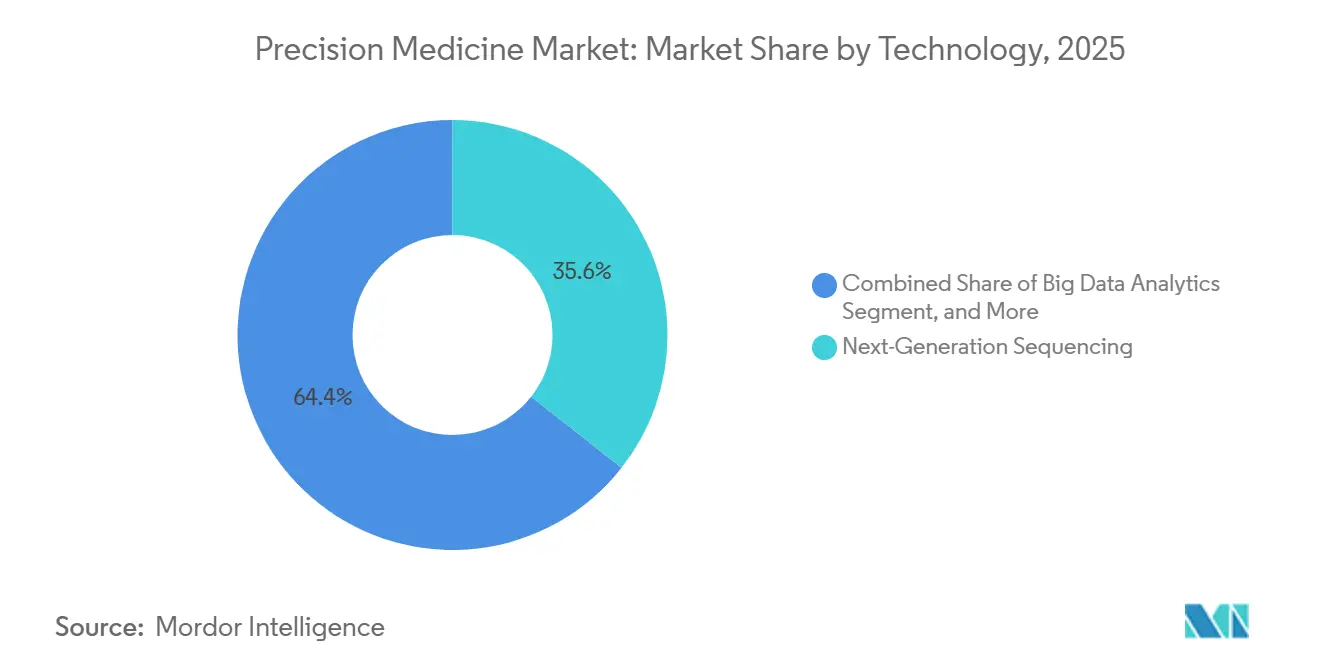

- By technology, next-generation sequencing held 35.55% of the precision medicine market share in 2025; AI and machine-learning tools are expanding at a 17.85% CAGR through 2031.

- By application, oncology led with 40.53% revenue in 2025, while rare and genetic disorders are forecast to expand at a 15.75% CAGR to 2031.

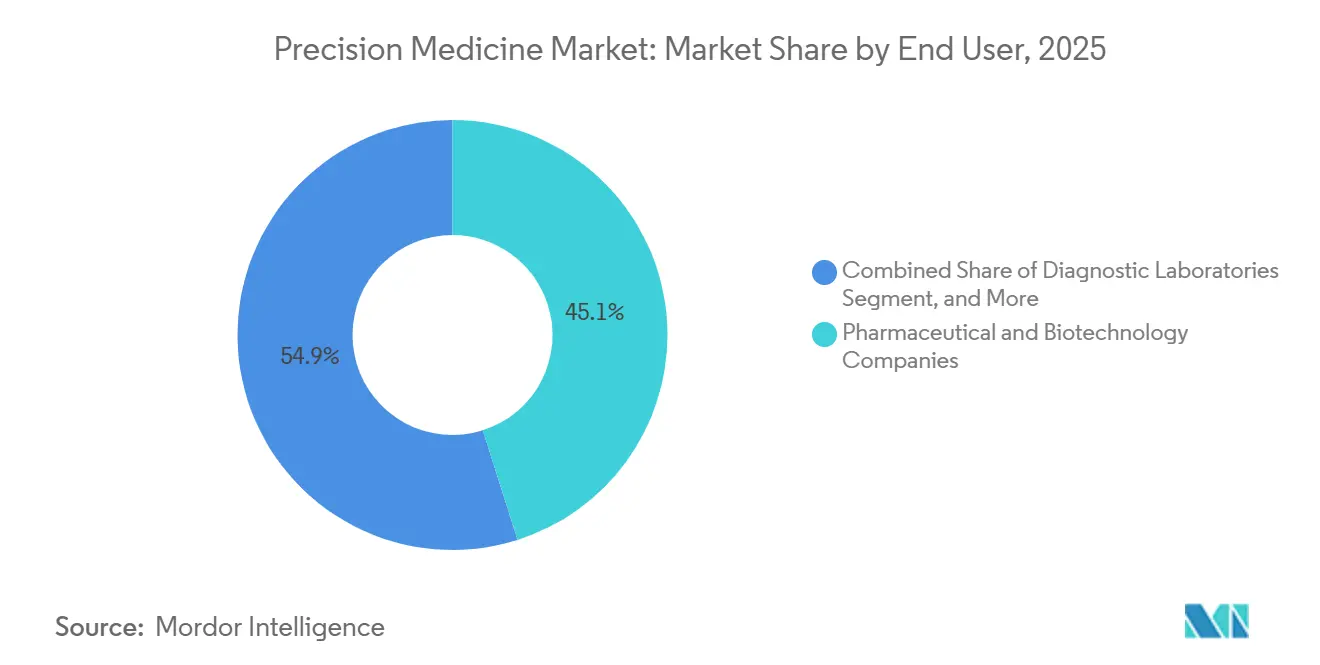

- By end user, pharmaceutical and biotechnology companies accounted for 45.15% spending in 2025; home-care settings are advancing at a 15.82% CAGR through 2031.

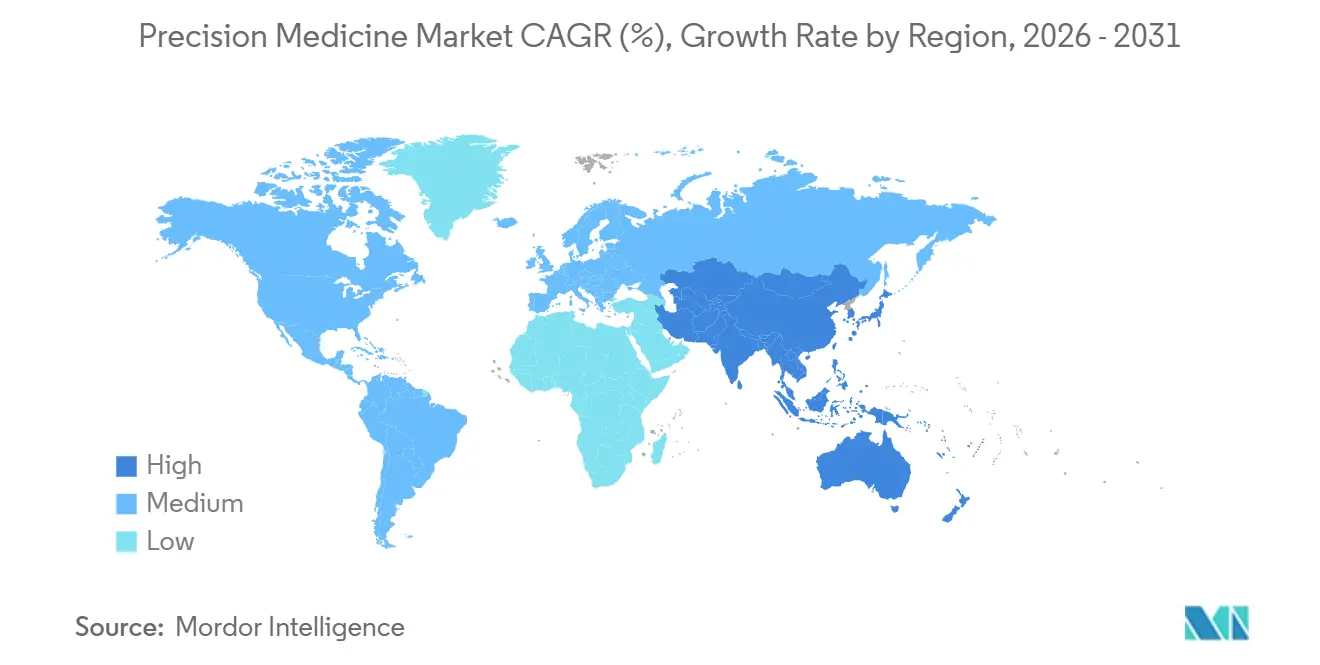

- By geography, North America accounted for 42.55% of revenue in 2025, whereas Asia-Pacific is projected to grow at a 14.72% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Precision Medicine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Genomic Initiatives Accelerating R&D Funding | +2.3% | Global, with concentration in US, UK, China, India, Japan | Medium term (2-4 years) |

| Integration of AI & Machine Learning in Genomics | +3.2% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Advancement in Cancer Biology Expanding Biomarker Pipeline | +2.7% | Global, led by US and Europe | Medium term (2-4 years) |

| Rapid Decline in Oligo-Synthesis Cycle Times Enabling Same-Day Therapies | +1.4% | North America & Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Emergence of Digital Biobanks Monetizing Multi-Ethnic Genomic Data | +1.1% | Global, early leadership in US, UK, China | Long term (≥ 4 years) |

| FDA Real-Time Oncology Review Shortening Approval Cycles | +1.9% | North America, spillover to EU & Japan | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

National Genomic Initiatives Accelerating R&D Funding

Government-backed genome programs de-risk biomarker discovery by providing large, well-phenotyped cohorts. The UK Biobank’s release of 500,000 exomes in 2024 enables drug developers to run in silico target validation before clinical investment[1].National Institutes of Health, “Researcher Workbench Usage Statistics 2025,” Allofus.nih.gov India sequenced 10,000 individuals from 99 ethnic groups, revealing 135 million variants absent from Western data sets and opening licensing avenues for South-Asian-specific therapies further diversifying the global precision medicine market opportunity. Japan enrolled 200,000 citizens to generate polygenic risk scores that will feed precision underwriting products. In the United States, the All of Us cloud workbench processed 18,500 research queries in 2025, 42% of which were from non-US scholars, demonstrating that open-access design multiplies knowledge without linear increases in cost[2]National Institutes of Health, “Researcher Workbench Usage Statistics 2025,” Allofus.nih.gov. China’s USD 9.2 billion Precision Medicine Initiative is funding provincial biobanks, making its data environment the largest outside the US.

Integration of AI & Machine Learning in Genomics

Regulatory clarity has turned adaptive algorithms into mainstream diagnostics. FDA guidance issued in January 2024 permits locked-algorithm devices to refresh their models using real-world evidence without a new 510(k), cutting maintenance costs and maintaining sensitivity above 95%. Paige AI received clearance that same year for a prostate cancer grading model that is retrained quarterly. BGI rolled out AI-based software across 300 Chinese hospitals, slashing the time to rare-disease diagnosis from 45 days to 7 days. Foundation Medicine embedded generative AI to infer tumor mutational burden from panel data, eliminating whole-exome sequencing and cutting costs by 40%. Tempus AI’s USD 6.1 billion IPO underscores investor belief in data-native platforms that integrate clinic, image, and omics layers, reinforcing confidence in scalable models across the precision medicine market.

Advancement in Cancer Biology Expanding Biomarker Pipeline

Multi-analyte diagnostics are fragmenting oncology into micro-segments with narrow but lucrative reimbursement. FDA cleared 23 companion diagnostics in 2024, 14 of which require NGS panels rather than single-gene assays. AstraZeneca’s Tagrisso gained a label extension for a mutation found in 2% of lung cancers, illustrating high-price structures achievable when cohorts are molecularly defined. Bristol Myers Squibb’s USD 4.1 billion RayzeBio buy adds radiopharmaceutical assets that bundle drug and imaging diagnostics in a single value proposition. Liquid biopsy adoption surged after Guardant’s Shield became the first blood-based colorectal screening assay for average-risk adults, expanding the testable population from 150,000 patients to 50 million asymptomatic individuals.

FDA Real-Time Oncology Review Shortening Approval Cycles

The Real-Time Oncology Review pathway cut median approval to 4.3 months in 2025, versus 10 months previously, by letting reviewers examine rolling data. Mirati used RTOR to bring adagrasib to market six months early, booking USD 180 million in first-year sales, 40% above forecasts. Novartis partnered with Illumina on a pan-cancer panel that will accompany all targeted therapies submitted under RTOR, standardizing biomarker testing at launch. The EMA mirrored the scheme with the PRIME pathway, capping review at 150 days.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Cross-Border Multi-Omics Data Regulations | -1.6% | Global, acute in EU–Asia and US–China flows | Long term (≥ 4 years) |

| High Cost & Limited Accessibility of Genetic Testing | -1.8% | Emerging markets, rural areas in developed economies | Medium term (2-4 years) |

| Shortage of Clinical Geneticists Limiting Interpretation Capacity | -1.1% | Global, most severe in US & Europe | Medium term (2-4 years) |

| Rising Cyber-attacks on Genomic Clouds Elevating Liability Risks | -0.7% | Global, heightened in North America & Europe | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Fragmented Cross-Border Multi-Omics Data Regulations

China’s 2024 Human Genetic Resources rules require foreign firms to keep Chinese genomes onshore, prompting costly duplication of infrastructure and delaying multi-country trials across the precision medicine industry. The EU’s GDPR bars transfers to non-adequate jurisdictions, making U.S. biobanks negotiate standard clauses that add legal overhead[3]European Commission, “Adequacy Decisions,” Ec.europa.eu. Illumina recorded USD 45 million in compliance outlays and eight-month launch delays in Europe during 2025. India’s 2024 Digital Personal Data Protection Act requires local storage of sensitive genomic information, compelling new data-center spending for international labs, limiting broader clinical adoption and slowing equitable expansion across the precision medicine industry.

High Cost & Limited Accessibility of Genetic Testing

Sequencing dipped to USD 600 per genome in 2025, yet clinical interpretation ranges from USD 1,200 to USD 3,000, pricing tests beyond self-pay segments in upper-middle-income economies[4]Nature Biotechnology, “Whole-Genome Sequencing Cost Analysis 2025,” Nature.com . Only 212 new clinical geneticists were certified globally in 2024, producing six-month wait times for rural U.S. patients. 23andMe’s 2025 restructuring, which cut 40% of staff, underscores the challenge of sustaining direct-to-consumer offerings when customer acquisition exceeds lifetime value. Even in rich markets, coverage gaps persist: Medicare reimburses hereditary cancer tests but excludes polygenic risk scores for cardiac disease.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: AI Reshapes Interpretation Economics

Next-generation sequencing generated 35.55% of the p recision medicine market revenue in 2025, backed by an installed base of 25,000 Illumina sequencers and aggressive low-cost bids from BGI. AI-based analytics are forecast to outgrow every other category at 17.85% CAGR, benefiting from the FDA’s streamlined change-control plan. Big-data platforms are shifting to cloud-native architectures, as illustrated by Tempus AI’s valuation and the widespread adoption of the All of Us federated workbench. Companion diagnostics remain essential but face bundling pressure that pushes revenue recognition into therapy royalty streams. Proteomics and metabolomics add orthogonal layers that raise predictive power; SomaLogic’s 7 k-protein panel reduces false positives in polygenic scoring by 30%.

By Application: Oncology Dominance Masks Rare-Disease Velocity

Oncology accounted for 40.53% of application revenue in 2025, as Medicare coverage widened and 17 biomarker-linked therapies entered the U.S. market. Rare and genetic disorders, however, exhibit the fastest growth rate at 15.75% CAGR, propelled by gene therapies such as Lyfgenia, which carries a USD 3.1 million price tag and requires confirmatory genetic testing. Neurology’s momentum rests on Alzheimer’s diagnostics bundled with amyloid-targeted drugs, while cardiology blends polygenic risk screening with pharmacogenomic dosing, now used by 15% of U.S. cardiology practices. Infectious-disease precision approaches are commercially available only for hospital-acquired infections; metabolic uses remain newborn-screening-centric, collectively reinforcing oncology’s structural dominance in the precision medicine market..

By End User: Home-Care Disruption Challenges Lab Incumbents

Pharma and biotech companies accounted for 45.15% of spending in 2025 due to mandatory companion diagnostic programs. Home-care channels are rising at 15.82% CAGR as ancestry and wellness kits bypass hospital labs. Yet 23andMe’s cost-of-customer paradox shows that scale alone does not guarantee profitability. Diagnostic laboratories fight reimbursement compression by slashing panel prices, evidenced by Labcorp’s USD 99 pharmacogenetic offer.

Geography Analysis

North America accounted for 42.55% of the precision medicine market revenue in 2025, driven by comprehensive profiling, reimbursement, and the All of Us dataset. Canada standardized coverage for 12 drug–gene pairs in 2025, speeding national adoption. Asia-Pacific, however, is predicted to deliver the fastest growth at a 14.72% CAGR, powered by China’s multibillion-dollar initiative and rapid AI rollout, which cut diagnostic turnaround from 45 days to 7 days. India’s 10,000-genome cohort introduces 135 million novel variants, while Japan’s cardiovascular focus targets insurer-backed underwriting products. Australia achieves 90% public coverage in rare disease testing but remains volume-limited by population size. Europe shows intra-regional variability: the U.K. shortened rare-disease diagnoses to 14 days under the NHS, whereas Germany still wrestles with 16 state payers. Saudi Arabia’s 100,000-genome plan leads the Middle East, while South Africa’s capability remains limited to three clinical-grade sequencing labs. South America builds slowly; Brazil covers hereditary cancer testing but not pan-omic assays.

���ϲ����� provides coverage of the precision medicine market across other key regional markets, including North America and Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to China incorporating local coverage and market participation, as required.

Competitive Landscape

The precision medicine market shows moderate concentration: the top five players held a significant share of global revenue in 2025, too low for dominance but high enough to influence standards. Illumina’s hardware edge is eroding as BGI and Element Biosciences roll out sub-USD 500 genomes that undercut legacy price points. Platform firms such as Tempus AI aggregate clinical, image, and omic data for predictive modeling, whereas specialists like Guardant Health focus on liquid biopsies that now target screening populations after Shield’s 2024 FDA clearance. AI leaders file escalating patent volumes. Illumina filed 47 machine-learning patents in 2024, up from 12 a year earlier. First-mover advantages accrue to companies obtaining Breakthrough Device designations, which cut market entry by roughly 18 months. White space remains in pharmacogenomics, where test penetration precedes actionable variants in only 1 in 10 U.S. prescriptions.

Precision Medicine Industry Leaders

Pfizer Inc.

Thermo Fisher Scientific Inc.

Novartis AG

Qiagen N.V.

Illumina Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Precision for Medicine and PathAI advanced their collaboration to automate digital-pathology analytics across global clinical trials.

- April 2025: Illumina and Tempus AI agreed to co-develop evidence packages that accelerate payer adoption of sequencing-based tests.

Global Precision Medicine Market Report Scope

As per the scope of the report, precision medicine, a combination of molecular biology techniques and systems biology, is an emerging approach to disease treatment and prevention. The market for this approach is gaining momentum as it accounts for individual variability in genes, environment, and lifestyle when developing drugs and vaccines.

The precision medicine market is segmented into technology, application, end user, and geography. By technology, the market is segmented into big data analytics, bioinformatics, next-generation sequencing (NGS), AI & machine learning, companion diagnostics, genomics, proteomics, metabolomics, epigenomics, and transcriptomics. By application, the market is segmented into oncology, neurology (CNS), immunology, cardiology, infectious diseases, respiratory, rare & genetic disorders, metabolic disorders, and other indications. By end user, the market is segmented into pharmaceutical & biotechnology companies, diagnostic laboratories, hospitals & clinics, academic & research institutes, contract research organisations, healthcare it & bioinformatics firms, and home-care settings. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Big Data Analytics |

| Bioinformatics |

| Next-Generation Sequencing (NGS) |

| AI & Machine Learning |

| Companion Diagnostics |

| Genomics |

| Proteomics |

| Metabolomics |

| Epigenomics |

| Transcriptomics |

| Oncology |

| Neurology (CNS) |

| Immunology |

| Cardiology |

| Infectious Diseases |

| Respiratory |

| Rare & Genetic Disorders |

| Metabolic Disorders |

| Other Indications |

| Pharmaceutical & Biotechnology Companies |

| Diagnostic Laboratories |

| Hospitals & Clinics |

| Academic & Research Institutes |

| Contract Research Organisations (CROs) |

| Healthcare IT & Bioinformatics Firms |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Big Data Analytics | |

| Bioinformatics | ||

| Next-Generation Sequencing (NGS) | ||

| AI & Machine Learning | ||

| Companion Diagnostics | ||

| Genomics | ||

| Proteomics | ||

| Metabolomics | ||

| Epigenomics | ||

| Transcriptomics | ||

| By Application | Oncology | |

| Neurology (CNS) | ||

| Immunology | ||

| Cardiology | ||

| Infectious Diseases | ||

| Respiratory | ||

| Rare & Genetic Disorders | ||

| Metabolic Disorders | ||

| Other Indications | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Diagnostic Laboratories | ||

| Hospitals & Clinics | ||

| Academic & Research Institutes | ||

| Contract Research Organisations (CROs) | ||

| Healthcare IT & Bioinformatics Firms | ||

| Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the precision medicine market in 2031?

It is forecast to reach USD 237.28 billion by 2031 based on a 13.58% CAGR from 2026.

Which technology segment is growing fastest within precision medicine?

AI and machine-learning tools are advancing at a 17.85% CAGR, outpacing all other technologies.

Why is Asia-Pacific considered the most dynamic region for precision medicine?

China’s USD 9.2 billion national initiative and rapid adoption of AI-enabled interpretation drive the region’s 14.72% CAGR.

How did FDA’s Real-Time Oncology Review affect drug approvals?

The pathway reduced median approval time to 4.3 months in 2025, roughly halving previous timelines.

Which application area beyond oncology shows notable growth?

Rare and genetic disorders are expanding at a 15.75% CAGR as high-value gene therapies reach market.

Page last updated on: