North America Precision Agriculture Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

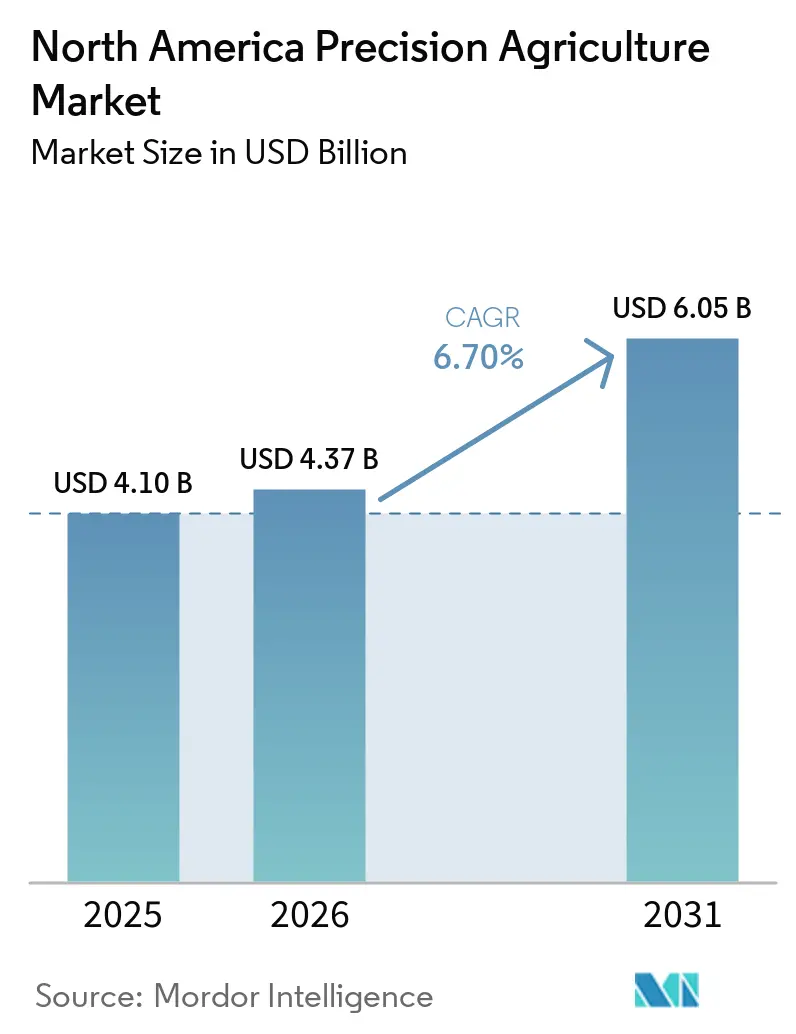

| Base Year Market Size (2025) | USD 4.10 Billion |

| Market Size (2026) | USD 4.37 Billion |

| Market Size (2031) | USD 6.05 Billion |

| Growth Rate (2026 - 2031) | 6.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

North America Precision Agriculture Market Analysis by ���ϲ�����

The North America precision agriculture market is projected to grow from USD 4.10 billion in 2025 and USD 4.37 billion in 2026 to USD 6.05 billion by 2031, registering a CAGR of 6.7% between 2026 and 2031. Federal cost-share programs, provincial subsidies, and increased carbon-credit revenues are encouraging growers to invest in variable-rate applicators, soil-microbiome diagnostics, and edge-enabled analytics. While hardware continues to dominate spending, the adoption of recurring software subscriptions is increasing as operators prioritize prescriptive insights over incremental equipment upgrades. The deployment of private 5G networks on large farms is reducing latency for autonomous fleets, and real-time irrigation scheduling is becoming critical due to worsening drought conditions in the High Plains and California’s Central Valley. Competitive intensity remains moderate, as equipment manufacturers protect proprietary data ecosystems, while software providers advocate for open Application Programming Interfaces (APIs) to enable growers to integrate cross-brand telemetry into unified dashboards.

Key Report Takeaways

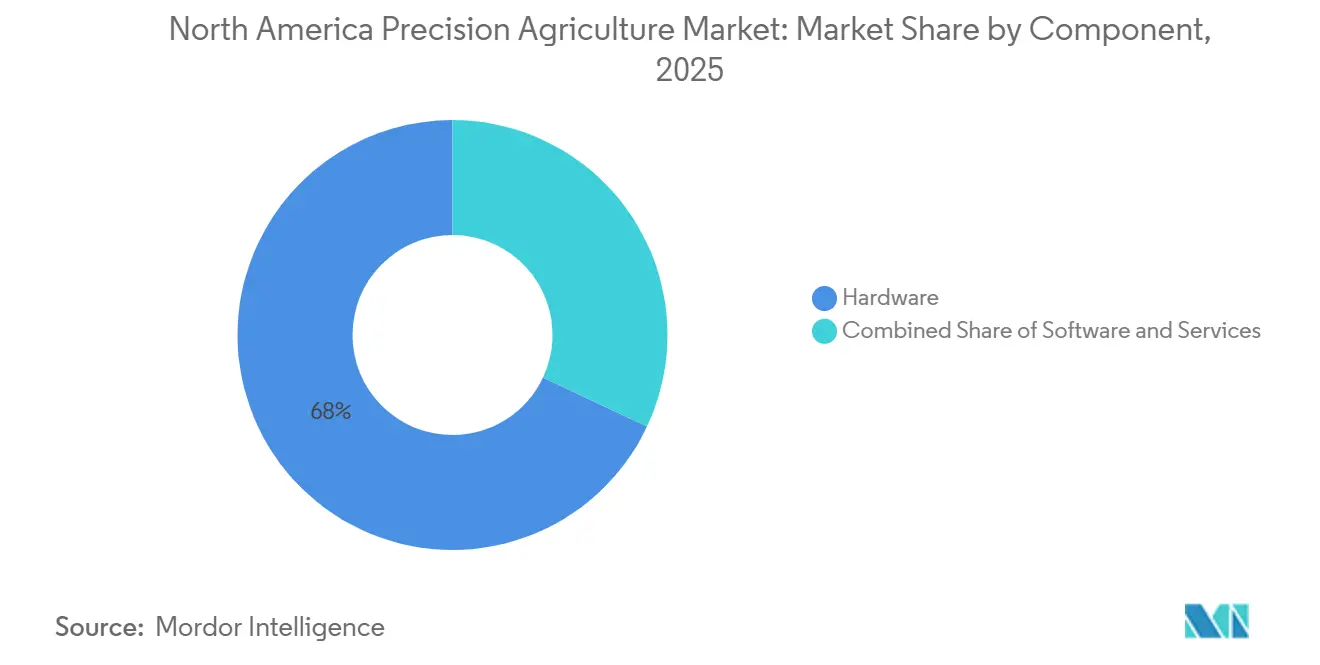

- By component, hardware accounted for the largest market share, 68.0% in the North America precision agriculture market in 2025, while the software segment market size is projected to grow at the fastest CAGR of 9.8% from 2026 to 2031.

- By technology, guidance (GPS/GNSS) systems held the largest market share, 37.5% in the North America precision agriculture market in 2025, whereas the variable-rate technology market size is projected to grow at the fastest CAGR of 10.4% from 2026 to 2031.

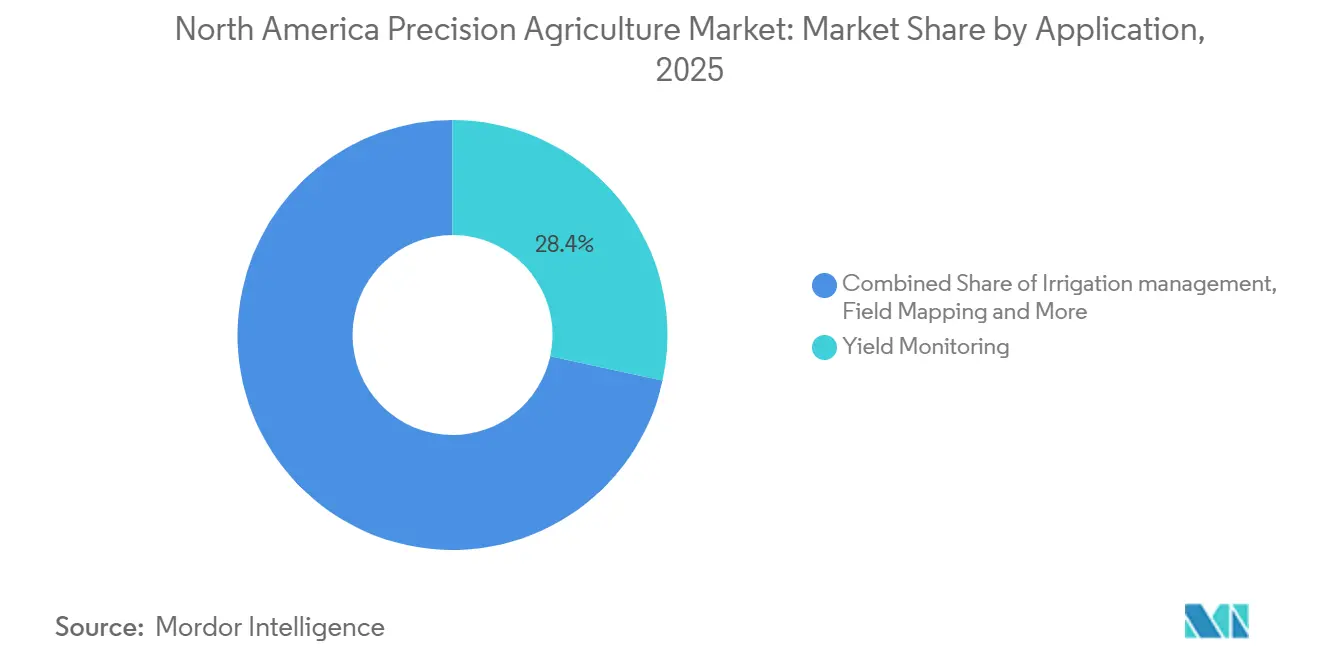

- By application, yield monitoring represented the largest market share, 28.4% in the North America precision agriculture market in 2025, while the irrigation management market size is anticipated to grow at the fastest CAGR of 11.2% from 2026 to 2031.

- By farm size, large farms (more than 1,000 acres) held the largest market share, 51.0% in the North America precision agriculture market in 2025, whereas small farms (less than 250 acres) market size is projected to grow at the fastest CAGR of 8.6% from 2026 to 2031.

- By geography, the United States accounted for the largest market share, 85.3%, in the North America precision agriculture market in 2025, while the market size for Mexico is projected to grow at the fastest CAGR of 9.5% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Precision Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Optimized variable-rate inputs lowering costs | +1.4% | United States Corn Belt, Canadian Prairies, and Mexico Bajío | Medium term (2-4 years) |

| Subsidies promoting smart equipment use | +1.2% | United States, Canada, and Mexico | Short term (≤ 2 years) |

| Increased adoption of IoT sensors, drones, and analytics | +1.3% | United States, Canada, and Mexico | Medium term (2-4 years) |

| Carbon-credit gains from precise nitrogen use | +0.9% | United States Midwest, and Western Canada | Long term (≥ 4 years) |

| Private 5G networks on large farms | +0.6% | Texas, California, Alberta, and Saskatchewan | Long term (≥ 4 years) |

| Soil-microbiome analytics enabling adaptive fertility | +0.8% | United States specialty-crop regions, and Canadian organics | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Optimized Variable-Rate Inputs Lowering Costs

Variable-rate technology enables growers to adjust seed, fertilizer, and pesticide application rates within specific micro-zones, reducing waste by 10%–15% and providing immediate cash-flow benefits [1]Source: Springer Nature, “Economic Returns to Variable-Rate Nitrogen Application in Corn Production,” Springer.com . John Deere’s ExactApply nozzle system achieved herbicide savings of up to 77% during trials conducted in Nebraska and Kansas in 2025 [2]Source: John Deere, “ExactApply Nozzle System Technical Specifications,” Deere.com . Adoption of this technology is advancing most rapidly in areas with high soil variability and existing GPS-guided tractors, particularly in regions such as Iowa, Illinois, and Saskatchewan. Dealers have reported strong sales of retrofit controllers, which can be installed on existing planters at one-third the cost of full replacements.

Subsidies Promoting Smart Equipment Use

Cost-share incentives remain significant in promoting the adoption of precision agriculture technologies across North America. In the United States, the Department of Agriculture enhanced conservation funding programs, including the Environmental Quality Incentives Program, during 2021–2023. This expansion increased financial support for precision farming tools and climate-smart practices. Similarly, in Canada, Agriculture and Agri-Food Canada launched the Agricultural Clean Technology Program in 2021, providing cost-sharing assistance for precision equipment, sensors, and energy-efficient technologies, with funding available through 2026.

Increased Adoption of IoT Sensors, Drones, and Analytics

Affordable sensors provide data on moisture levels, canopy temperature, and pest pressure through unified dashboards, enabling growers to automate time-sensitive tasks. Lindsay Corporation acquired Pessl Instruments in Jan 2025, integrating weather stations into the FieldNET pivot platform. This platform now activates irrigation based on real-time evapotranspiration data instead of fixed intervals. Farmers Edge gained subscribers for its Corvian analytics suite by combining satellite imagery with machine-learning alerts to identify nutrient stress. DroneDeploy users processed imagery over large areas, with flights supporting variable-rate seeding plans.

Carbon-Credit Gains from Precise Nitrogen Use

Quantified nitrogen-use efficiency now enables carbon offsets valued at USD 10–USD 20 per acre in voluntary markets. The Climate Action Reserve adopted Version 3.0 of the United States Nitric Acid Production Protocol in August 2025. This version introduced improved methodologies for accounting, reporting, and verifying greenhouse gas emission reductions from nitrous oxide abatement [3]Source: Climate Action Reserve, Updated United States Nitric Acid Production Protocol Provides Opportunity for Greater Positive Climate Impact, climateactionreserve.org . Yara’s Agoro Carbon Alliance reported that it has made over USD 15 million in payments to United States farmers and ranchers within its first two years of operation, under programs that support the adoption of climate-smart practices such as improved nitrogen management and soil health measures [4]Source: Agoro Carbon Alliance, “Agoro Carbon Pays $15 Million to United States Farmers & Ranchers in First Two Years”, agorocarbonalliance.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital costs for advanced technologies | −1.1% | United States small and medium farms, Canada prairies, and Mexico smallholders | Short term (≤ 2 years) |

| Data interoperability and privacy issues | −0.7% | United States, Canada, and Mexico | Medium term (2-4 years) |

| Lack of ag-tech technicians in rural areas | −0.5% | United States Great Plains, Canada rural provinces, and Mexico northern states | Medium term (2-4 years) |

| Connectivity gaps due to fragmented rural spectrum | −0.6% | Montana, Wyoming, remote Saskatchewan, and ejido communities | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Capital Costs for Advanced Technologies

Equipment costs remain high for a standard package comprising RTK receivers, drone platforms, and variable-rate controllers. This expense poses a significant challenge for small grain farms, which struggle to amortize such investments when net returns are limited. High initial investment requirements continue to be a significant barrier to the adoption of precision agriculture technologies in North America. The substantial upfront costs of advanced equipment, including GPS-guided systems, sensors, and data platforms, discourage adoption, particularly among small and mid-sized farms with limited capital access. Beyond hardware expenses, farmers also face difficulties in assessing the return on investment due to uncertainties regarding long-term economic benefits and the operational complexity of these technologies.

Data Interoperability and Privacy Issues

Many United States growers operate mixed equipment fleets. However, only a small percentage effectively achieve seamless cross-brand data exchange. This inefficiency results in additional manual hours per farm annually. The American Farm Bureau Federation reports that growers are concerned about the potential impact of yield data on land-rent negotiations or futures pricing. In 2024, the Open Ag Data Alliance introduced new Application Programming Interface (API) standards, but these standards remain voluntary and are not compatible with legacy consoles. Furthermore, Canada’s privacy law requires explicit consent for data sharing, creating additional challenges for platform consolidation.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Gains as Data Monetization Matures

Hardware captured the largest 68.0% of the North America precision agriculture market share in 2025, owing to the entrenched base of GPS receivers and drone platforms. Even so, the software market size is projected to grow at the fastest 9.8% CAGR from 2026 to 2031. The Climate Corporation gained new FieldView subscribers, with a significant portion opting to pay additional fees for variable-rate scripting and carbon-credit documentation. In 2023, Trimble announced its mixed-fleet precision agriculture strategy through a joint venture with AGCO, emphasizing integration across equipment brands and data systems. By 2024, this initiative expanded into broader multi-brand connectivity and data integration platforms, enabling telemetry interoperability across the Deere & Company, CNH Industrial N.V., and AGCO Corporation .

Service-based offerings are expanding in response to increasing operational complexity, with vendors emphasizing integrated digital platforms and remote support to minimize reliance on on-site interventions. Equipment manufacturers are incorporating telematics, connectivity, and agronomic advisory services into their offerings, aligning revenue models with performance outcomes and fostering long-term customer engagement. Additionally, advanced sensing technologies, such as hyperspectral imaging and soil analysis tools, are being integrated into broader digital ecosystems. Proprietary analytics play a key role in transforming raw data into actionable insights for effective farm management.

By Technology: Variable-Rate Systems Outpace Legacy Guidance

Guidance (GPS/GNSS) held the largest 37.5% of the North America precision agriculture market share in 2025, reflecting two decades of retrofits and factory installs. The variable-rate technology market size is projected to grow at the fastest 10.4% CAGR from 2026 to 2031. This growth is driven by the addition of prescription control over seeding, fertilization, and chemical application, which enhances returns on existing autosteer platforms. In May 2025, John Deere’s acquisition of Sentera integrated hyperspectral analytics directly into its Operations Center, eliminating a subscription layer and facilitating adoption for connected machines.

Remote sensing and analytics providers are enhancing edge computing and real-time processing capabilities, enabling quicker decision-making and reducing delays in field assessments. Interoperability solutions and retrofit technologies are improving accessibility by allowing older machinery to connect with modern precision systems, facilitating broader adoption among cost-conscious operators. While artificial intelligence-driven analytics are gaining traction for applications like crop monitoring and yield optimization, adoption remains limited to technologically advanced users due to high data requirements and implementation complexities.

By Application: Irrigation Management Surges Amid Water Scarcity

The yield monitoring segment accounts for the largest 28.4% of the North America precision agriculture market share in 2025, yet its growth is tapering because new combines now ship with factory-installed sensors at no extra charge. The irrigation management market size is projected to grow at the fastest 11.2% CAGR from 2026 to 2031. Lindsay’s FieldNET network, integrated with real-time weather and moisture data, reduced water usage during Nebraska corn trials in 2024. FarmX’s Osmo sensor achieved water savings in California nut orchards, thereby reducing pumping costs.

Applications such as crop scouting, nutrient management, and field monitoring are advancing with greater accuracy and efficiency, driven by improvements in aerial imaging and data analytics. Weather intelligence has become a critical component of operational planning, influencing activities such as spraying schedules, harvesting decisions, and overall risk management. Furthermore, growing concerns about water availability are increasing interest in irrigation-focused solutions, positioning water management technologies as a key emerging priority within precision agriculture systems.

By Farm Size: Small Operations Narrow the Adoption Gap

Large farms (more than 1,000 acres) account for the largest 51% of the North America precision agriculture market share in 2025. Their focus is shifting toward analytics subscriptions and carbon-offset documentation that derive new revenue from existing datasets. Whereas the market size of small farms (less than 250 acres) is projected to grow at the fastest 8.6% CAGR from 2026 to 2031 by clustering into cooperatives that dilute capital risk. Nebraska's PRO-AG grant subsidized the cost for shared variable-rate spreaders, leading to an increase in adoption within a short period.

The adoption of precision agriculture technologies differs based on farm size. Large farms are at the forefront, supported by greater financial resources, technical expertise, and the capacity to implement advanced systems across extensive operations. Medium-sized farms are progressively adopting these technologies by utilizing external service providers and bundled solutions, enabling efficiency improvements without substantial internal investments. Smaller farms, traditionally constrained by limited capital, are increasingly turning to simplified and service-based tools. As these technologies become more cost-effective, scalable, and user-friendly, adoption is growing across all farm sizes, reducing the disparity between large and smaller operations.

Geography Analysis

The United States accounts for the largest, 85.3% of the North America precision agriculture market share in 2025. Precision technologies, including GPS-guided equipment and variable-rate systems, are extensively adopted, particularly in the Corn Belt. Federal initiatives, such as the Environmental Quality Incentives Program, provide financial and technical support for conservation practices, such as nutrient management, thereby facilitating broader adoption in key agricultural regions. In California, specialty crop producers are increasingly adopting advanced irrigation technologies, such as soil moisture sensors and data-driven irrigation scheduling, to improve water-use efficiency amid persistent water scarcity.

The market size for Mexico is projected to grow at the fastest CAGR of 9.5% from 2026 to 2031. Research from the Inter-American Development Bank emphasizes the importance of precision irrigation and improved water management practices to mitigate water stress and boost productivity in export-oriented farming systems. Furthermore, public research institutions are actively encouraging the adoption of precision technologies, including drones and decision-support tools, particularly among smallholder and cooperative farming systems.

In Canada, the adoption of precision agriculture is steadily increasing, supported by federal programs like the Agricultural Clean Technology Program, which funds precision equipment and energy-efficient technologies. The large farm sizes in provinces such as Saskatchewan and Alberta enhance the economic feasibility of technologies like variable-rate application and automated equipment. Additionally, provincial initiatives, such as carbon offset systems, incentivize practices that lower emissions through improved input efficiency, including precision nitrogen management.

Competitive Landscape

The North America precision agriculture market is moderately concentrated in 2025. The top five companies include Deere and Company, Trimble Inc., CNH Industrial N.V., AGCO Corporation, and Topcon Corporation. Deere & Company uses connected machines to promote its Operations Center analytics, while CNH Industrial N.V. offers pay-per-acre packages that integrate guidance, telematics, and agronomy support to address capital constraints. In 2024, Deere & Company's strategic partnership with Trimble aims to standardize machine-control protocols, indicating that interoperability has transitioned from a competitive strategy to a growth driver.

Software-focused entrants target mixed fleets. The Climate Corporation and Farmers Edge process data from drones, satellites, and ground sensors via open Application Programming Interfaces (APIs), providing brand-agnostic dashboards for operators managing diverse machinery lines. Trace Genomics exemplifies domain specialization by converting soil DNA data into adaptive fertility scripts, offering capabilities that traditional dealers cannot replicate. Niche hardware manufacturers like Ag Leader Technology, Inc. and TeeJet Technologies (Spraying Systems Co.) maintain market share through retrofit compatibility and competitive pricing. For instance, TeeJet Technologies (Spraying Systems Co.)’s DynaJet nozzle is priced lower than Deere & Company’s ExactApply but has shown comparable weed control performance in independent trials.

Mergers and strategic partnerships are reshaping the market. Kubota Corporation has partnered with Agtonomy to develop autonomous narrow tractors designed to reduce labor in organic crop production, while AGCO Corporation has pre-installed 5G modems to enhance telemetry capabilities. Smaller analytics firms face margin pressures as OEMs integrate features like rate maps and pathology alerts directly into console firmware. The market is evolving, with equipment giants consolidating core platforms while agile startups focus on high-value niches such as microbiome diagnostics and carbon-credit verification.

North America Precision Agriculture Industry Leaders

Deere and Company

Trimble Inc.

CNH Industrial N.V.

AGCO Corporation

Topcon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: AGCO's Fendt brand focuses on high-speed, real-time data exchange through the FendtONE platform and PTx technologies such as vConnect|Drive to support autonomy, mixed-fleet management, and high-precision planting in its new models designed for 2026.

- June 2025: Kubota Corporation made a partnership with Agtonomy to enhance autonomous tractor solutions for specialty crops, incorporating AI-driven operations and precision farming technologies.

- May 2025: Deere & Company acquired Sentera, Inc. to incorporate aerial field scouting capabilities into its digital agriculture ecosystem. This acquisition strengthens the John Deere Operations Center by integrating high-resolution drone imagery and analytics.

North America Precision Agriculture Market Report Scope

Precision agriculture is a farming method that utilizes technologies such as GPS, sensors, and data analytics to monitor and manage variability in crop fields. This approach optimizes inputs like water, fertilizers, and pesticides, enhancing productivity, efficiency, and sustainability. The North America precision agriculture market report is segmented by component (hardware, software, and services), by technology (guidance GPS/GNSS, remote sensing, variable rate technology, and Artificial Intelligence (AI)-enabled analytics), by application (yield monitoring. field mapping, crop scouting, weather tracking and forecasting, irrigation management and inventory and labor management), by farm size (large farms (more than 1,000 acres), medium farms (250–999 acres), and small farms (less than 250 acres)), and by geography (United States, Canada, Mexico, and rest of North America). The market forecasts are provided in terms of value (USD).

| Hardware |

| Software |

| Services |

| Guidance (GPS (Global Positioning System)/GNSS (Global Navigation Satellite System)) |

| Remote Sensing |

| Variable-rate Technology |

| AI-enabled Analytics |

| Yield Monitoring |

| Field Mapping |

| Crop Scouting |

| Weather Tracking and Forecasting |

| Irrigation Management |

| Inventory and Labor Management |

| Large Farms (more than 1,000 acres) |

| Medium Farms (250-999 acres) |

| Small Farms (less than 250 acres) |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Component | Hardware |

| Software | |

| Services | |

| By Technology | Guidance (GPS (Global Positioning System)/GNSS (Global Navigation Satellite System)) |

| Remote Sensing | |

| Variable-rate Technology | |

| AI-enabled Analytics | |

| By Application | Yield Monitoring |

| Field Mapping | |

| Crop Scouting | |

| Weather Tracking and Forecasting | |

| Irrigation Management | |

| Inventory and Labor Management | |

| By Farm Size | Large Farms (more than 1,000 acres) |

| Medium Farms (250-999 acres) | |

| Small Farms (less than 250 acres) | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the forecasted value of the North America precision agriculture market by 2031?

It is projected to reach USD 6.05 billion by 2031 from USD 4.37 billion in 2026, growing at a 6.7% CAGR.

How fast will Variable-Rate Technology grow within precision agriculture across North America?

Variable-Rate Technology is anticipated to post the fastest 10.4% CAGR between 2026 and 2031.

Which farm-size segment will expand quickest?

Small Farms (less than 250 acres) are forecast to grow at the fastest 8.6% CAGR from 2026 to 2031 as costs decline.

Why is irrigation management gaining traction?

Water scarcity and government funding, such as Mexico's modernization program, are pushing irrigation management to a 11.2% CAGR from 2026 to 2031 .

Which country is set to show the highest regional growth?

Mexico will lead with the fastest 9.5% CAGR from 2026 to 2031, supported by irrigation and modernization investments.

Page last updated on: