Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

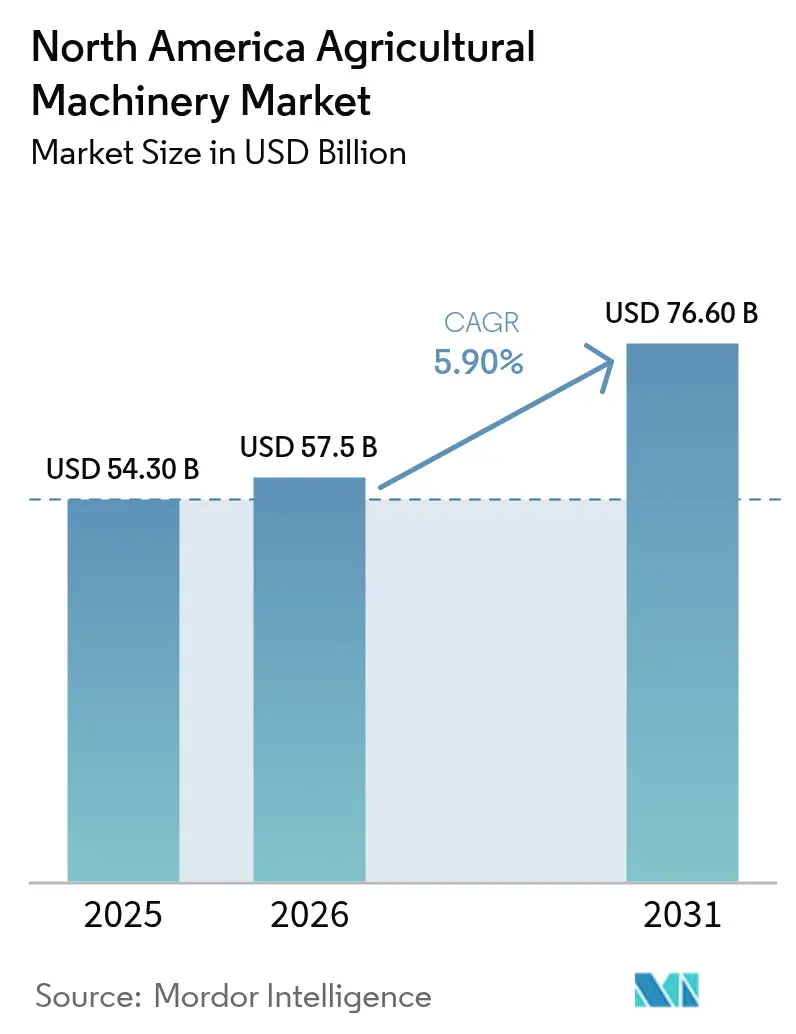

| Base Year Market Size (2025) | USD 54.30 Billion |

| Market Size (2026) | USD 57.5 Billion |

| Market Size (2031) | USD 76.60 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

North America Agricultural Machinery Market Analysis by ���ϲ�����

The North America agricultural machinery market size is projected to expand from USD 54.3 billion in 2025 and USD 57.5 billion in 2026 to USD 76.6 billion by 2031, registering a 5.90% CAGR between 2026 to 2031. Federal support, rising labor costs, and precision‑ag adoption are reshaping farm equipment demand[1]Source: USDA Economic Research Service, “Farm Income and Wealth Statistics,” ers.usda.gov. Robust payments have preserved grower liquidity even as crop prices returned to long‑term averages, while a tightening labor pool has accelerated automation in spraying, tillage, and harvesting. Precision technologies are increasingly integrated into large farms, driving demand for autosteer‑ready tractors and sensor‑equipped combines. At the same time, financing arms of major manufacturers are underwriting a majority of machinery purchases, helping producers manage higher interest rates. Together, these factors are shortening replacement cycles and lifting annual equipment sales across the North America agricultural machinery market.

Key Report Takeaways

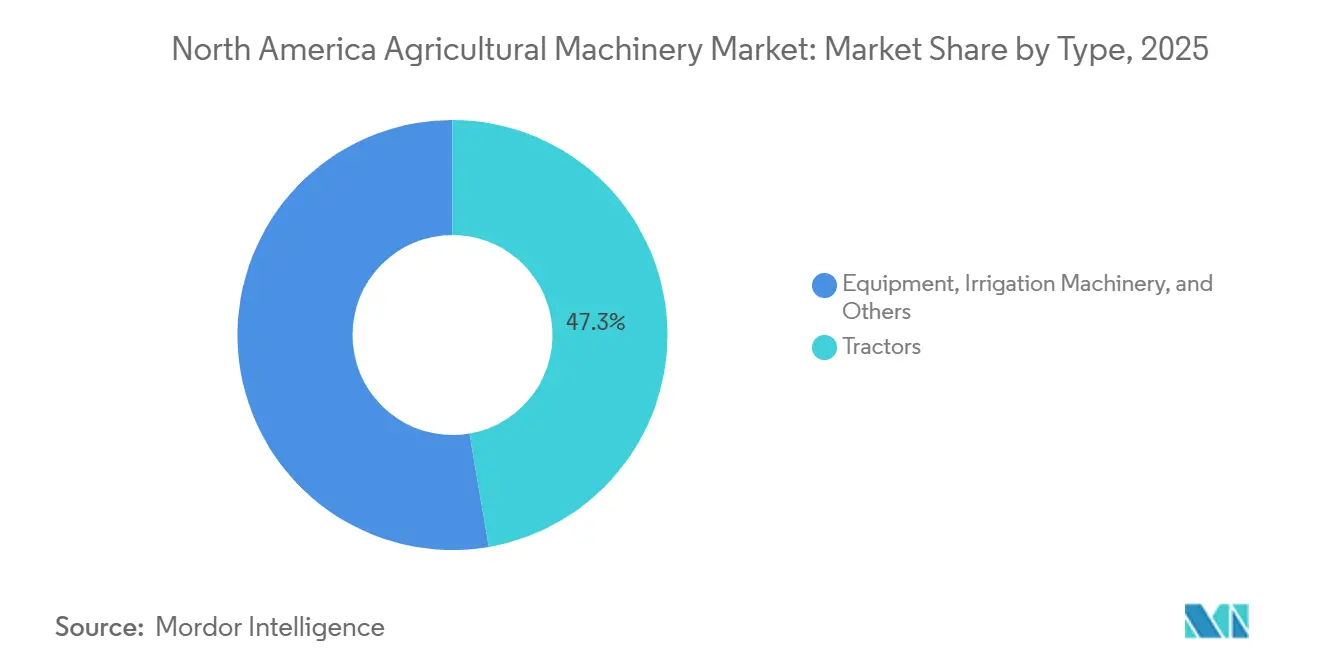

- By type, tractors accounted for a market share of 47.3% of the North America agricultural machinery market size in 2025, while irrigation machinery is projected to post the fastest 6.4% CAGR from 2026 to 2031.

- By geography, the United States accounts for 61.4% of the North America agricultural machinery market share in 2025, while Mexico is projected to grow at the fastest CAGR of 6.6% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust farm-income outlook and subsidy programs | +1.2% | United States, Canada, selective support in Mexico | Medium term (2-4 years) |

| Rising labor scarcity and wage inflation | +1.0% | United States and Canada, emerging in Mexico | Short term (≤ 2 years) |

| Precision-agriculture adoption accelerating equipment replacement | +0.9% | United States Corn Belt, Canadian prairies, pilot zones in Mexico | Medium term (2-4 years) |

| Original Equipment Manufacturer (OEM) embedded-finance boosting purchasing power | +0.7% | United States and Canada, expanding in Mexico | Short term (≤ 2 years) |

| Subscription-based machinery access models | +0.4% | United States, early trials in Canada | Long term (≥ 4 years) |

| Climate-Smart grants driving low-emission equipment | +0.5% | United States, spillover to Canada | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Robust Farm-Income Outlook and Subsidy Programs

Federal support programs continue to underpin machinery demand even as crop receipts soften. In March 2022, the Government of Canada invested in agricultural machinery innovation and technology, reinforcing the role of public funding in sustaining capital expenditure. Direct government payments, including climate-focused allocations, have provided a cushion that allowed producers to maintain investment despite lower crop prices. The Farm Bill extended crop insurance subsidies and introduced targeted grants for precision equipment that reduce nitrogen runoff, lowering the effective cost of GPS-guided planters and variable-rate spreaders. Canada mirrors this pattern through programs that stabilized income for prairie growers, while Mexico’s initiatives allocated significant funding to smallholder mechanization, disproportionately benefiting key agricultural states. Subsidy-driven liquidity compresses replacement cycles, as operators trade in older tractors for precision-ready fleets.

Rising Labor Scarcity and Wage Inflation

Agricultural labor markets have tightened sharply, with many producers ranking workforce availability as their primary constraint. Average farm wages have continued to climb, while seasonal visa processing delays have extended hiring timelines. According to the Association of Equipment Manufacturers (AEM), sales of 4WD tractors increased by 31.7%, from 3,466 units in 2022 to 4,564 in 2023, reflecting the increasing adoption of mechanization to offset labor shortages. This wage pressure disproportionately affects labor-intensive segments such as vegetable harvesting, orchard management, and livestock handling, driving adoption of autonomous tractors, robotic weeders, and self-propelled forage harvesters[2]Source: American Farm Bureau Federation, “Farm Labor Survey,” fb.org. Canada faces parallel constraints, with provinces offering incentives to attract operators during harvest, while Mexico’s rural-to-urban migration is eroding the traditional labor pool. Cooperatives are pooling capital for shared machinery fleets, making mechanization a survival imperative for mid-sized operations.

Precision-Agriculture Adoption Accelerating Equipment Replacement

Precision agriculture penetration has expanded rapidly among large farms, with autosteer systems and connected platforms becoming standard. This adoption wave compels producers to retire older equipment lacking modern architecture, as retrofitting is often cost-prohibitive compared to purchasing new units[3]Source: USDA National Agricultural Statistics Service, “Farm Computer Usage and Ownership,” nass.usda.gov. The shift is particularly pronounced in the Corn Belt, where growers use yield maps to modulate seeding density and nitrogen application, achieving input savings and yield gains. Integrated platforms from leading manufacturers aggregate data across planters, sprayers, and combines, creating ecosystem lock-in effects that favor bundled purchases. Canada’s prairie provinces, with their large field sizes, see even higher precision-agriculture uptake.

Climate-Smart Grants Driving Low-Emission Equipment

Climate-focused initiatives have allocated substantial funding for equipment upgrades that reduce greenhouse-gas emissions. Eligible investments include electric tractors, methane digesters, and precision sprayers that cut chemical use. New electric tractor models have entered vineyards, orchards, and dairy operations, supported by rebates under state and federal programs. Canada’s clean technology programs mirror this approach, disbursing funds for solar-powered irrigation pumps and electric utility vehicles. The constraint remains battery-grade semiconductor availability, as agricultural demand competes with automotive and grid-storage sectors, extending lead times for electric models. Climate-focused subsidies are bifurcating the market, creating a premium tier of low-emission equipment that commands higher prices but qualifies for grants that offset costs, making total ownership competitive with diesel alternatives for operators in carbon-credit programs.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and maintenance costs of advanced machinery | -0.8% | United States and Canada, acute in Mexico | Short term (≤ 2 years) |

| Volatile commodity prices curbing Capital Expenditure (CapEx) cycles | -0.6% | United States and Canada, moderate in Mexico | Medium term (2-4 years) |

| Interest-rate-driven credit tightening at the farm level | -0.5% | United States and Canada | Short term (≤ 2 years) |

| Battery-grade semiconductor supply constraints for e-tractors | -0.3% | United States and Canada, minimal in Mexico | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Upfront and Maintenance Costs of Advanced Machinery

The rising cost of tractors, planters, and combines has placed significant financial pressure on producers, particularly smaller operators. Modern precision equipment carries high purchase prices, while maintenance expenses add further strain through software subscriptions and premium replacement parts. For smallholders, even compact machinery can be prohibitively expensive without subsidized financing. The result is a widening technology gap between large-scale farms, which can spread costs across extensive acreage, and smaller producers, who struggle to justify investments. This dynamic concentrates market growth among larger operations that can achieve payback through efficiency gains and precision farming benefits.

Volatile Commodity Prices Curbing Capital Expenditure (CapEx) Cycles

Commodity price fluctuations continue to compress margins for row‑crop producers, curbing their ability to commit to new machinery purchases. Farmers often defer capital expenditure until futures markets stabilize above breakeven thresholds, extending the age of existing equipment fleets. In Canada, growers have postponed replacements for combines and air seeders, while in Mexico, government price supports have provided more stability for staple crops. Export‑oriented producers, however, have scaled back investments in irrigation and other systems as demand softened. The broader implication is that volatility in commodity markets introduces cyclicality into equipment replacement cycles, with producers waiting for sustained recovery before committing to multi‑year financing.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Tractors Lead while Irrigation Gains Speed

By type, tractors accounted for market share of 47.3% of the North America agricultural machinery market size in 2025. Tractors remain the backbone of crop operations, reflecting their indispensable role across diverse farming systems. According to the Association of Equipment Manufacturers (AEM), retail sales of tractors above 100 HP and 4WD tractors increased by 5.2% and 31.7% respectively from 2022 to 2023. The segment benefits from autonomous retrofits that have been tested extensively, validating real‑world uptime and reducing skepticism about driverless tillage. These innovations highlight tractors as the central hub of mechanization, integrating precision technologies that improve efficiency and productivity. Their dominance underscores how farms continue to prioritize versatile equipment capable of handling multiple tasks, while also adapting to new digital platforms that enhance connectivity and operational control.

Irrigation machinery is projected to post the fastest 6.4% CAGR from 2026 to 2031. Irrigation equipment is gaining momentum as water‑scarcity mitigation projects expand across North America, with center‑pivot conversions accelerating adoption in Mexico. This segment is anticipated to outpace other categories, driven by the need for sustainable water management and climate resilience. Precision irrigation systems are increasingly integrated with digital monitoring tools, enabling farmers to optimize water use while maintaining yields. The growth trajectory reflects how irrigation machinery is evolving from a support function into a strategic investment, positioning itself as one of the most dynamic areas of agricultural equipment demand.

Geography Analysis

The United States accounted for 61.4% of the North America agricultural machinery market in 2025. Tractors remain central to large-scale operations, with Corn Belt farms regularly upgrading fleets to stay compatible with telematics and precision systems. California specialty-crop growers continue to invest in irrigation to comply with groundwater regulations, while cotton producers in the Southern Plains adopt precision sprayers to manage herbicide resistance. Replacement-driven demand is anticipated to sustain growth, reflecting the United States market’s reliance on technology upgrades to maintain productivity and efficiency across diverse agricultural regions.

Mexico is poised to expand at a fastest 6.6% CAGR from 2026-2031. Government funding programs covering a portion of equipment costs for small cooperatives are accelerating adoption among fragmented landholdings. Sinaloa’s vegetable growers dominate tractor uptake, Jalisco’s avocado orchards invest in hillside-stable sprayers, and Sonora’s irrigated wheat farms expand combine use. Rental platforms are bridging affordability gaps for smallholders, enabling broader access to modern machinery. This dynamic positions Mexico as the fastest-growing geography in the region, with mechanization increasingly viewed as essential for competitiveness and resilience in both domestic and export-oriented agriculture.

Canada contributed a significant share of regional sales, concentrated in Saskatchewan, Alberta, and Manitoba. Large-scale air seeders dominate spring drilling in the Prairies, while dairy heartlands in Ontario and Quebec sustain demand for forage harvesters and manure spreaders. British Columbia’s berry growers prefer compact tractors with narrow wheel bases suited to specialty crops. Diverse crop profiles across provinces continue to drive steady demand for modern machinery, reinforcing Canada’s role as a stable and important contributor to the North America agricultural machinery market.

Competitive Landscape

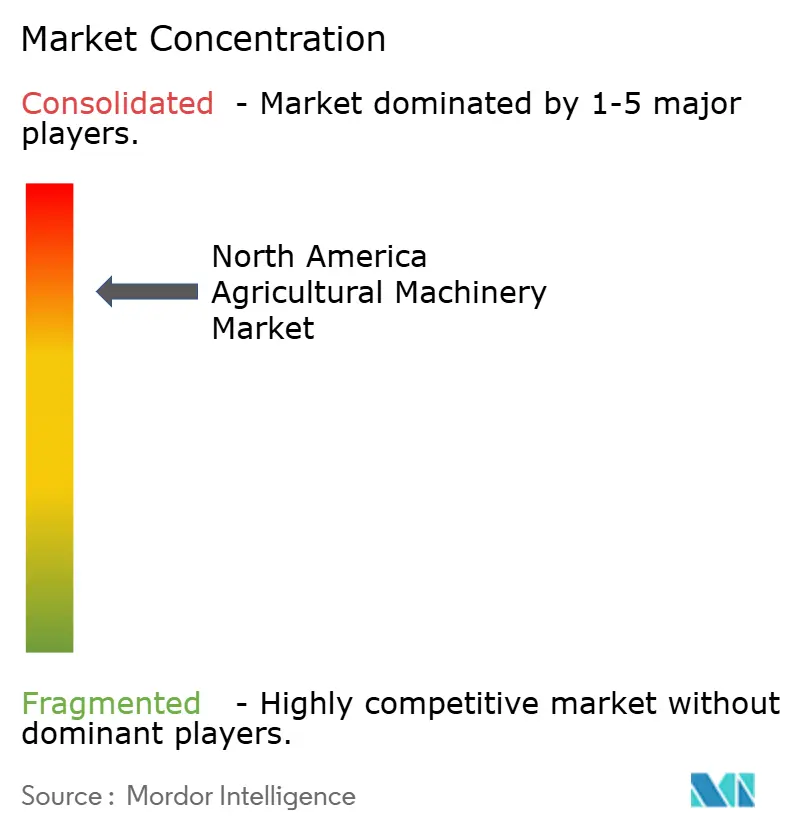

Market concentration in North America remains high in 2025, with the top five original equipment manufacturers commanding the majority of revenue. Deere & Company leads the segment, followed by CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and CLAAS KGaA mbH. Competitive focus has shifted from mechanical specifications to digital ecosystems. Deere & Company emphasizes a per‑acre software model, CNH Industrial N.V. integrates Raven autonomy, and AGCO Corporation leverages its joint venture with Trimble Inc. to deliver a mixed‑fleet open platform. In April 2025, AGCO Corporation expanded its dealer footprint with Carter Agri-Systems in Utah and the Delta Ag Equipment launch of Mississippi’s first full-line Fendt and Massey Ferguson outlet, enhancing market access for advanced machinery. These strategies highlight how digital integration, connectivity, and precision technologies now define leadership in agricultural machinery.

Smaller brands differentiate through customer intimacy and innovation. Kubota Corporation has earned strong dealer satisfaction and showcased its electric tractor lineup at major industry events. CLAAS KGaA mbH reorganized distribution in Dakota to strengthen direct touchpoints, while Butler Machinery continues to supply parts during the transition. Embedded finance strategies from leading OEMs create entry barriers for startups, but subscription‑based access models such as MachineryLink Sharing are beginning to challenge traditional ownership structures. By monetizing idle capacity, these platforms introduce new ways for producers to access advanced machinery without full capital commitments.

Innovators in field robotics and sensing increasingly partner with established OEMs to accelerate commercialization. Autonomous implement specialists integrate onto existing tractor platforms, expanding functionality and reducing adoption hurdles. Precision‑ag software companies grow revenue by offering application‑specific modules that operate across brands, running seamlessly on cab displays. This cross‑compatibility could gradually erode lock‑in effects, encouraging more open ecosystems. Partnerships with firms such as Horsch Maschinen GmbH, KUHN SAS, Bernard Krone Holding SE & Co. KG, The Toro Company, Vermeer Corporation, and J.C. Bamford Excavators Ltd. illustrate how collaboration between innovators and OEMs is reshaping the competitive landscape.

North America Agricultural Machinery Industry Leaders

Deere & Company

AGCO Corporation

CLAAS Group

Kubota Corporation

CNH Industrial N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Deere & Company unveiled comprehensive autonomous agriculture solutions at CES 2025, including fully autonomous tillage systems, and retrofit capabilities for 8 Series and 9 Series tractors with low upfront pricing and per-acre monetization models. These launches signal Deere’s intent to embed software-as-a-service revenues into core equipment sales while demonstrating field-proven fuel savings that resonate with large row-crop producers.

- January 2025: Kubota Corporation North America showcased multiple advanced equipment concepts at CES 2025, including the Agri Concept 2.0 electric tractor with autonomous functions, a Smart Autonomous Sprayer for precision chemical application. The exhibit positions Kubota as a technology challenger by pairing compact-equipment heritage with electrification and robotics aimed at mid-sized farms.

- January 2025: CLAAS and Butler Machinery announced a strategic reorganization of sales coverage in the Dakotas, with CLAAS Group establishing new dealerships to offer its full product line while Butler continues service and parts support through December 2026. The staged handover reduces customer disruption and expands CLAAS’s direct market reach at a time when growers seek multi-brand support under one roof.

North America Agricultural Machinery Market Report Scope

The agricultural machinery industry is considered a part of the machinery industry that comprises the manufacturing of machinery required to support agriculture.

The North America Agricultural Machinery Market Report is Segmented by Type (Tractor, Equipment, Irrigation Machinery, Harvesting Machinery, Haying and Forage Machinery, and Other Types) and by Geography (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD).

By Type

| Tractor | Less Than 40 HP |

| 40 to 100 HP | |

| More than 100 HP | |

| 4WD Tractors | |

| Equipment | Plows |

| Harrows | |

| Cultivators and Tillers | |

| Other Equipment | |

| Irrigation Machinery | Sprinkler |

| Drip | |

| Other Irrigation | |

| Harvesting Machinery | Combine Harvesters |

| Forage Harvesters | |

| Other Harvesting | |

| Haying and Forage Machinery | Mowers |

| Balers | |

| Other Haying and Forage | |

| Other Types |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type | Tractor | Less Than 40 HP |

| 40 to 100 HP | ||

| More than 100 HP | ||

| 4WD Tractors | ||

| Equipment | Plows | |

| Harrows | ||

| Cultivators and Tillers | ||

| Other Equipment | ||

| Irrigation Machinery | Sprinkler | |

| Drip | ||

| Other Irrigation | ||

| Harvesting Machinery | Combine Harvesters | |

| Forage Harvesters | ||

| Other Harvesting | ||

| Haying and Forage Machinery | Mowers | |

| Balers | ||

| Other Haying and Forage | ||

| Other Types | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

How large is the North America agricultural machinery market in 2026?

The market reached USD 57.5 billion in 2026 and is forecast to expand to USD 76.6 billion by 2031.

What is the anticipatedCAGR for agricultural machinery demand in North America?

The compound annual growth rate is projected at 5.9% from 2026-2031.

Which equipment type commands the largest revenue share?

Tractors held the top spot with 47.3% share in 2025, reflecting their versatility across operations.

Why is irrigation machinery growing faster than other segments?

Water-scarcity mitigation efforts, especially in Mexico under the National Water Plan 2024-2030, drive a 6.4% CAGR for irrigation equipment.

Who are the leading OEMs in the region?

Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and CLAAS Group collectively control majority of the market.

How do USDA Climate-Smart grant influence equipment purchases?

Grants subsidize low-emission machinery, effectively lowering acquisition costs and accelerating adoption of electric or fuel-efficient models.

Page last updated on: