Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

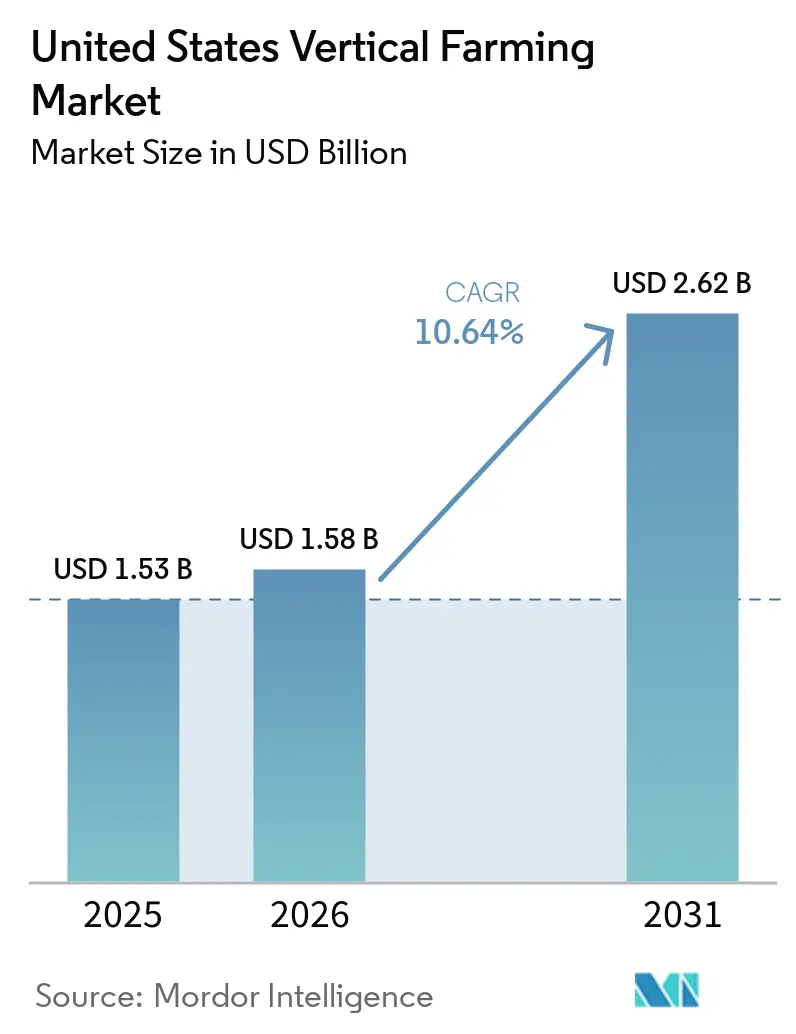

| Base Year Market Size (2025) | USD 1.53 Billion |

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.62 Billion |

| Growth Rate (2026 - 2031) | 10.64% CAGR |

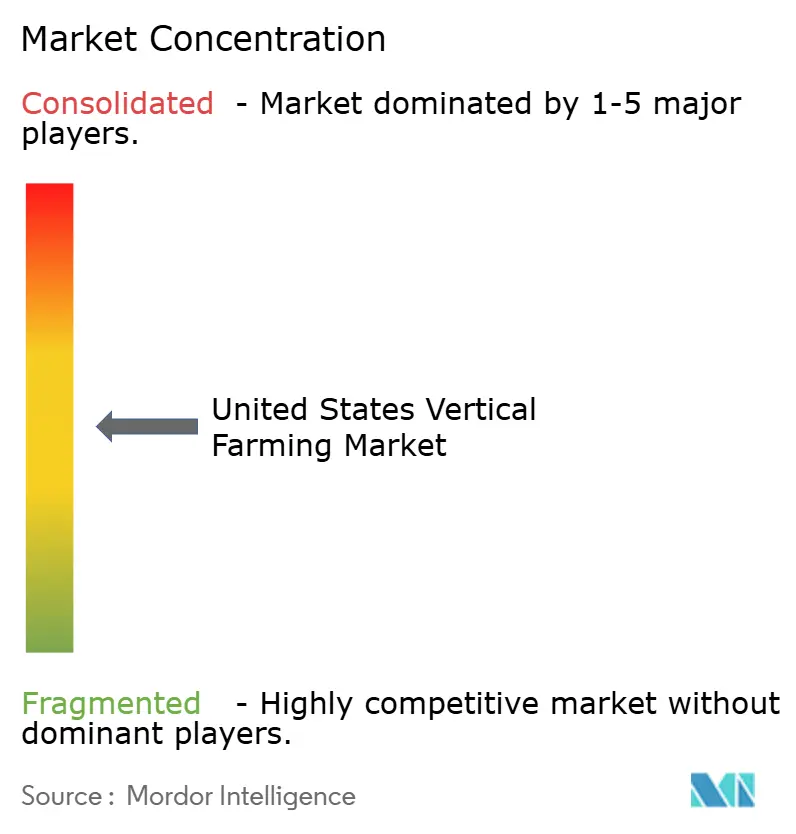

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

United States Vertical Farming Market Analysis by ���ϲ�����

The United States vertical farming market size was valued at USD 1.5 billion in 2025 and is estimated to grow from USD 1.6 billion in 2026 to reach USD 2.6 billion by 2031, at a CAGR of 10.6% during the forecast period 2026-2031. The United States vertical farming market is moving out of the 2022 to 2024 reset period, with a smaller set of operators holding better assets and stronger balance sheets. Demand for pesticide-free and locally sourced produce continues to support steady offtake, helping profitable growers preserve revenue even as funding conditions remain tight. The United States vertical farming market is also gaining support from water stress in western field agriculture, as produce buyers treat indoor hydroponics as a supply continuity option rather than a niche premium format. Renewable power contracts, microgrid arrangements, and more disciplined site selection are improving cost visibility for farms exposed to electricity swings. At the same time, artificial intelligence-assisted pollination and spectral control are expanding the crop mix into berries and other premium formats, giving the United States vertical farming market a broader revenue base than it had when leafy greens were the only proven scale category.

Key Report Takeaways

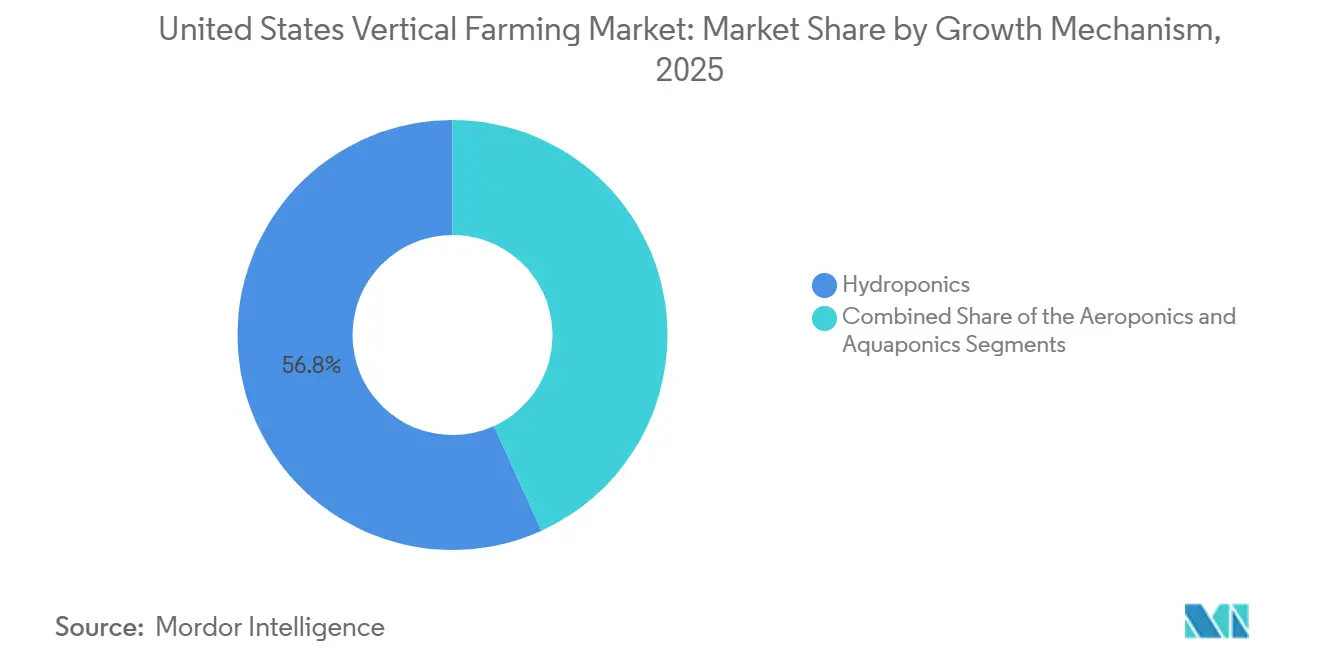

- By growth mechanism, hydroponics was the largest segment with 56.8% of the United States Vertical Farming market share in 2025, while aeroponics is the fastest segment and is projected to expand at a 16% CAGR during 2026-2031.

- By structure, building-based farms were the largest segment with 68.6% of the United States Vertical Farming market share in 2025, while shipping-container farms are the fastest segment at a 12.2% CAGR during 2026-2031.

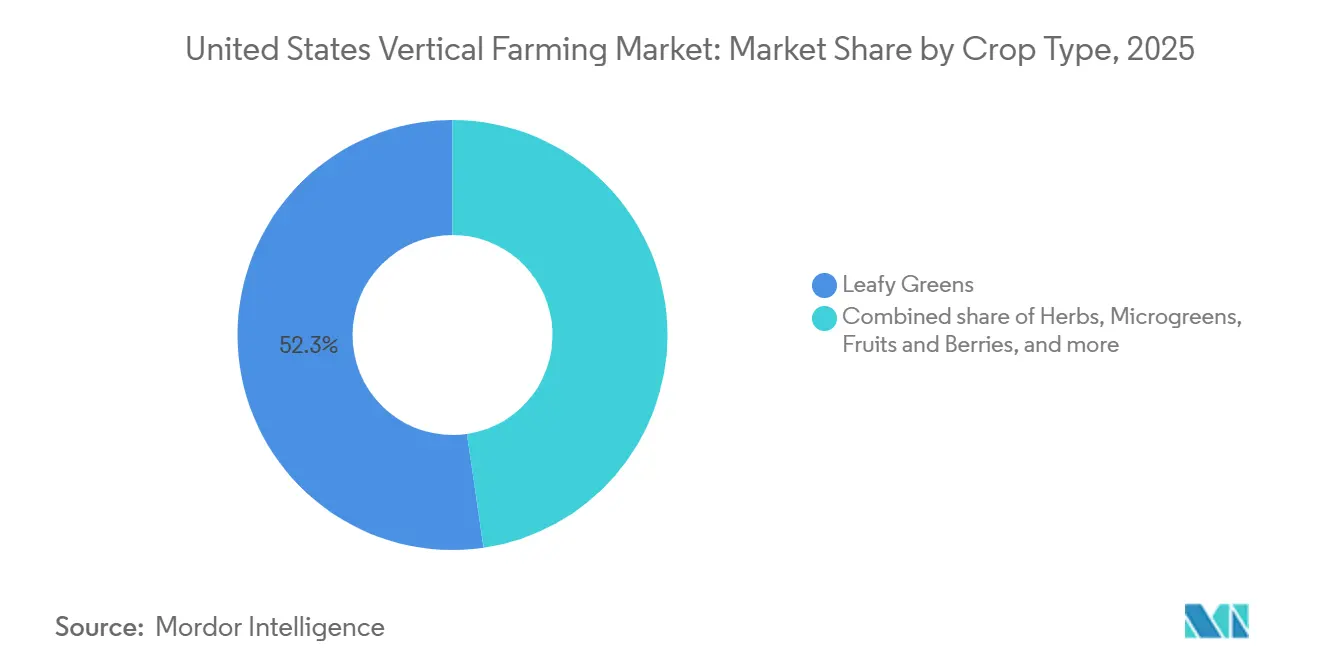

- By crop type, leafy greens were the largest segment with 52.3% share of the United States Vertical Farming market size in 2025, while fruits and berries are the fastest-growing segment at a 10.3% CAGR during 2026-2031.

- By component, hardware was the largest segment with 63.7% of the United States Vertical Farming market share in 2025, while software is the fastest segment at a 12.4% CAGR during 2026-2031.

- By end user, retail and supermarkets were the largest segment with 48% share of the United States Vertical Farming market size in 2025, while pharmaceutical and cosmetic ingredient buyers are the fastest segment at a 15% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Vertical Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Local Pesticide-Free Greens | +2.3% | National, with the strongest retail pull in the Northeast and West Coast urban corridors, where premium fresh produce turns faster | Short term (≤ 2 years) |

| Food-Mile Reduction and Same-Day Freshness | +1.5% | National, centered on large metropolitan distribution networks, where shelf-life losses carry direct margin implications | Short term (≤ 2 years) |

| Water-Efficient Production under Western Drought Pressure | +1.2% | Strongest in California, Arizona, and Colorado, with spillover demand in Texas as water security shapes sourcing decisions | Medium term (2-4 years) |

| Retailer Demand for Year-Round Supply Resilience | +1.6% | National, especially in regions exposed to weather-related field crop disruptions and variable inbound produce flows | Medium term (2-4 years) |

| Renewable Power and Microgrid Contracting Improves Economics | +0.9% | Most relevant in Texas and western states, where flexible power structures and renewable access can support indoor facilities | Long term (≥ 4 years) |

| AI Vision, Pollination, and Crop Recipes Enable Premium Fruit Crops | +1.1% | National, with early commercial concentration in New Jersey, Virginia, and California, where berry programs are moving beyond pilot scale | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Demand for Local Pesticide-Free Greens

Retail demand is anchoring the United States vertical farming market, as major grocery chains increasingly treat pesticide-free produce as a procurement standard. Indoor farms consistently meet zero-pesticide and no-herbicide requirements, outperforming field growers and many greenhouse suppliers across seasons. This alignment with retail expectations is further supported by federal initiatives, such as the USDA's January 2025 announcement of USD 14.4 million in new Urban Agriculture and Innovative Production grants, bringing total commitments since 2020 to USD 53.7 million[1]Source: United States Department of Agriculture, “USDA Announces Grants and Technical Assistance Funding for Urban Agriculture and Innovative Production,” USDA, usda.gov. These developments strengthen contract visibility, retailer relationships, and pricing discipline in packaged salads and fresh-cut categories. By reducing the risk that indoor greens are treated as discretionary products during economic downturns, the market is shifting its focus to retail category management and supply assurance. This interconnected demand pattern underscores the United States vertical farming market's growing reliance on stable retail partnerships rather than consumer novelty preferences.

Food-Mile Reduction and Same-Day Freshness

Shorter delivery distances are driving efficiency in the United States vertical farming market by addressing the significant shelf-life losses leafy greens face during long cross-country transit. Conventional produce from California and Arizona often takes 4 to 6 days to reach eastern retail networks, leaving limited time for store handling and consumer purchase. In contrast, indoor farms within 200 miles of major cities can deliver produce within 24 hours of harvest, extending retail shelf life by 5 to 7 days. A September 2025 study by Wang and coauthors highlighted that proximity sourcing reduced postharvest respiration losses by 18% to 22%, directly improving retailer margins and reducing markdowns. This shift underscores why same-day freshness is evolving from a marketing message to a contractual standard in urban distribution corridors, solidifying the case for regional indoor farming.

Water-Efficient Production under Western Drought Pressure

Water productivity is reshaping the United States vertical farming market as drought risks intensify in western states. Agronomy for Sustainable Development (2025) study highlighted that hydroponic lettuce in controlled environments achieved 140 grams of fresh weight per liter of water, compared to just 15.3 grams per liter in open-field production. Additionally, a life-cycle assessment revealed that conventional field lettuce required up to 240 liters per kilogram in California and 169 liters per kilogram in Arizona, while hydroponic systems used significantly less water[2]Source: A. Banboukian et al., “Life Cycle Water Assessment of Hydroponic versus Open-Field Lettuce in California and Arizona,” International Journal of Life Cycle Assessment, doi.org. These efficiencies are influencing buyer decisions, as water availability increasingly impacts procurement continuity and costs. Reflecting this shift, Vertical Harvest Farms secured USD 59.5 million in 2024, supported by the USDA Rural Energy for America Program, with water savings being a key driver. As irrigation risks grow, vertical farming is solidifying its role as a sustainable solution in western sourcing strategies.

AI Vision, Pollination, and Crop Recipes Enable Premium Fruit Crops

Crop diversification is transforming the United States vertical farming market as fully enclosed farms expand beyond leafy greens into berries and premium fruits. Artificial intelligence (AI)-assisted pollination and spectral crop recipes are enabling efficient management of fruiting crops that were previously uneconomical to grow at scale indoors. For instance, Oishii’s Amatelas Farm in New Jersey, launched in June 2024, demonstrates the viability of industrial-scale berry production with 237,000 square feet of indoor strawberry capacity, 50 autonomous robots, and 60 billion annual crop data points. Similarly, in September 2024, Plenty Unlimited’s partnership with Driscoll’s in Virginia integrates indoor production with a large-scale commercial berry platform, emphasizing scalability and brand value. These advancements are reshaping the revenue mix in the vertical farming market by introducing higher-value categories, such as premium fruits, which command higher prices than traditional greens. This shift not only diversifies offerings but also justifies investments in sophisticated automation and data systems, thereby driving the market's long-term growth potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crop Profitability Remains Concentrated in Leafy Greens and Herbs | -1.5% | National, with the clearest limits in mature Northeast and Midwest greens programs, where crop diversification still moves slowly | Short term (≤ 2 years) |

| Power Intensity and Electricity-Price Volatility Pressure Margins | -2.0% | Strongest in the Midwest and Northeast tariff zones, especially around Illinois, New York, and Ohio | Medium term (2-4 years) |

| Post-Bankruptcy Financing Gap Raises Cost of Capital | -1.2% | National, with the sharpest effect on mid-tier operators below USD 50 million in annual revenue | Short term (≤ 2 years) |

| State And Local Zoning, Permitting, And Interconnection Complexity | -0.8% | National, with longer delays in urban infill projects across New York, Illinois, and California | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Power Intensity and Electricity-Price Volatility Pressure Margins

Electricity is a major cost driver for the United States vertical farming market due to the reliance on energy-intensive systems like lighting, climate control, and dehumidification. In 2024, Kaiser and coauthors reported that electricity constitutes 20% to 40% of production costs, with lighting alone consuming 60% to 85% of total electricity. AGEYE's 2025 findings showed that pre-build financial models often underestimate HVAC and dehumidification costs by 30% to 50%, leading to weaker cost assumptions. A 2026 study in Nature Communications found that most vertical farms exceed the energy-intensity threshold for carbon-competitive positioning against traditional imports. While dynamic lighting can cut electricity costs by 12%, retrofitting older facilities is often unaffordable. This leaves the market vulnerable to tariff volatility, particularly in the Midwest and Northeast, highlighting the urgent need for renewable energy adoption, storage systems, and efficient technologies to stabilize costs and enhance competitiveness.

Post-Bankruptcy Financing Gap Raises Cost of Capital

The United States vertical farming market faces financing challenges, as lenders and investors remain cautious following bankruptcies and restructurings from 2022 to 2024. Stricter credit standards now burden smaller operators with tighter covenants, higher interest spreads, and limited flexibility for delays. Established players like Local Bounti, which restructured USD 197 million in debt in 2025 and raised USD 15 million in 2026, and AeroFarms, which issued and later rescinded a WARN notice after restructuring, highlight the ongoing need for financial stability. This environment favors well-capitalized buyers who can expand without incurring first-time build costs, while underfunded operators are pushed toward mergers or distressed sales. The financing gap reshapes the market, determining the pace and participants of future growth.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Growth Mechanism: Hydroponics Is the Largest, Aeroponics Is the Fastest

Hydroponics dominated the United States vertical farming market with a 56.8% share in 2025, driven by its compatibility with leafy greens, established nutrient systems, and ease of integration into existing indoor farm layouts. Its ability to deliver predictable outputs and standardized crop cycles aligns with retailer demand for crops like lettuce and spinach, which remain the top commercial products. However, the widespread adoption of hydroponics has reduced product differentiation, making operational scale, execution, and customer access more critical for success.

Aeroponics, with a projected 16% CAGR during 2026-2031, is emerging as the fastest-growing mechanism due to its efficient water usage, 70% to 95% less than hydroponics, and enhanced root-zone oxygenation, which benefits high-value, water-sensitive crops. Innovations like Local Bounti's AI-assisted hybrid system, patented in February 2026, highlight the increasing flexibility of growth methods as operators optimize throughput. While aquaponics remains a niche due to its operational complexity in managing both plant and fish biology, it serves specialized markets like institutional and pharmaceutical channels, where traceability and closed-loop production add value. Together, these mechanisms reflect a market evolving towards efficiency, innovation, and targeted applications to meet diverse demands.

By Structure: Building-Based Farms Are the Largest, Containers Are the Fastest

Building-based farms accounted for 68.6% of the 2025 market value, making them the largest structure type in the United States vertical farming market. Their ability to repurpose existing warehouse and industrial spaces for high-volume production, in addition to the dense multi-tier layouts and tighter climate control, ensures higher harvest volumes. These advantages are critical for meeting national and regional retail contracts, and the scalability of building-based formats allows operators to spread fixed costs over greater output, solidifying their central role in the market.

Meanwhile, shipping-container farms, with a projected CAGR of 12.2% during 2026-2031, are emerging as the fastest-growing structure type. Their modular and rapid-deployment capabilities make them ideal for food deserts, military locations, and institutional campuses where permanent construction is less practical. For instance, Opollo Farm’s 2025 automated cube deployment in Phoenix demonstrated how container systems can address labor and space constraints through compact, automated solutions. Warehouse-based farms, positioned between these two formats, offer more cultivation volume than containers but lower build intensity compared to purpose-designed multi-level buildings. Together, these structure types reflect a market balancing large regional hubs with smaller, modular units, driving the evolution of the United States vertical farming market toward diverse and adaptable solutions.

By Crop Type: Leafy Greens Are the Largest, Fruits and Berries Are the Fastest

Leafy greens accounted for 52.3% of the 2025 revenue, solidifying their position as the largest crop segment in the United States vertical farming market. This dominance stems from optimized short growth cycles, consistent lighting techniques, and efficient packaging formats that integrate seamlessly into retail distribution. Crops like lettuce, spinach, and arugula remain the backbone of the market due to their steady demand and ease of handling. In October 2025, Little Leaf Farms reported holding over 54% of the indoor lettuce category across more than 8,000 United States stores, underscoring the mainstream retail penetration of leafy greens, which continue to define the market's revenue foundation.

Meanwhile, fruits and berries are emerging as the fastest-growing crop segment, with a projected 10.3% CAGR from 2026 to 2031. This growth is fueled by advancements in pollination systems, improved climate control, and higher revenue per unit compared to leafy greens. Facilities like Oishii’s in New Jersey and Plenty’s Virginia berry program with Driscoll’s highlight the shift of indoor berry production from technical feasibility to commercial scalability. Additionally, herbs and microgreens contribute to market growth by supporting premium pricing and consistent demand from foodservice, specialty retail, and health-conscious consumers. For instance, 80 Acres Farms expanded its microgreens range to over 17,000 retail locations by January 2026, demonstrating the scalability of smaller-format crops and further contributing towards market growth. Together, these developments underline the diversification and growth potential of the United States vertical farming market, with leafy greens anchoring revenue and fruits, berries, and microgreens driving future expansion.

By Component: Hardware Is the Largest, Software Is the Fastest

In 2025, hardware accounted for 63.7% of the United States vertical farming market, driven by the essential upfront investment in lighting, irrigation, racking, and climate systems required to initiate crop production. These systems remain critical as they directly influence yield and unit costs, ensuring hardware retains the largest market share. However, as facilities establish their physical infrastructure, the focus is increasingly shifting toward digital control systems to enhance efficiency and reduce costs.

Software, projected to grow at a CAGR of 12.4% during 2026-2031, is becoming indispensable for advanced crop monitoring, traceability, and production planning, particularly for multi-site operators. The integration of artificial intelligence, computer vision, and enterprise software is evolving from optional to essential, enabling optimization of physical assets. Additionally, the expansion of outsourced services, such as agronomy support and system integration, reflects a shift toward prioritizing operational expertise and software over physical infrastructure alone. Together, these trends highlight the growing synergy between hardware and software, driving the evolution of the United States vertical farming market.

By End User: Retail and Supermarkets Are the Largest, Pharmaceutical and Cosmetic Buyers Are the Fastest

Retail and supermarkets, projected to account for 48% of end-user revenue in 2025, dominate the United States vertical farming market. Grocery shelves test the economics of indoor farming, as packaged salads and fresh greens rely on consistent fill rates, quality control, and shelf-life management. Retail chains drive compliance costs through demands for food-safety documentation and logistics integration but offer stable operators recurring demand, solidifying retail as the market's revenue anchor.

Meanwhile, pharmaceutical and cosmetic buyers, growing at a 15% CAGR during 2026-2031, prioritize controlled environments for purity and consistency, highlighting the value of vertical farming for sensitive applications. Foodservice, the second-largest segment, emphasizes freshness and local sourcing, while direct-to-consumer and e-commerce channels focus on premium specialty items. Together, these trends underline a diversifying end-user base, with vertical farming increasingly meeting demands for crops that traditional systems cannot reliably produce.

Geography Analysis

The Northeast dominated the United States vertical farming market in 2025. This leadership is driven by dense urban demand, short delivery routes, and a concentration of indoor farming assets in the New York, New Jersey, and Pennsylvania corridor. Key developments, such as Little Leaf Farms' greenhouse expansion in Pennsylvania and Oishii’s premium berry production in New Jersey, highlight the region's innovation. However, rising real estate costs and slower interconnection timelines are prompting a shift of new projects to less urbanized areas.

The Midwest and the South are emerging as competitive regions, leveraging cost and infrastructure advantages. The Midwest benefits from lower real estate costs and strong water access, as seen in Gotham Greens' Chicago expansion, while the South attracts large-scale investments like BrightFarms' facilities in Texas and Georgia, supported by favorable zoning and grid access. These regions are becoming vital growth hubs, balancing cost efficiencies with operational scalability.

The West, fastest CAGR during 2026-2031, driven by water scarcity and the adoption of hydroponic and aeroponic systems. States like California and Arizona lead with efficient water use, while Colorado and Washington add momentum with clean energy access and demand for premium crops. Arizona’s innovative deployments, such as Opollo Farm’s automated systems, further emphasize the region's role in shaping the future of vertical farming. Together, these regional dynamics reflect a market evolving toward resource efficiency, innovation, and interconnected growth.

Competitive Landscape

The United States vertical farming market remains moderately concentrated, with the top five operators, Little Leaf Farms, Gotham Greens, BrightFarms, Oishii, and Local Bounti, holding a significant share of the market value in 2025. However, this leadership is evolving as restructuring enables well-funded buyers to acquire assets from weaker operators at reduced costs. The 2025 merger of 80 Acres Farms and Soli Organic, creating a platform with an estimated first-year revenue of USD 200 million across 17,000 retail locations, has intensified competition. At the same time, regional greenhouse operators are challenging vertical farms by targeting premium retail shelf space with lower energy and capital requirements. This shift highlights that competitive strength now depends on cost efficiency, customer access, and crop strategy rather than farm count or capacity alone.

Technology is a critical driver of this competitive evolution, as digital systems and intellectual property enhance yield, labor efficiency, and compliance readiness. Local Bounti’s February 2026 patent for its AI-assisted hybrid growing system reflects efforts to secure technological advantages. Suppliers like Priva Holding and Argus Control Systems remain influential, as many growers rely on their systems within proprietary frameworks. The United States Food and Drug Administration (FDA), is extending the compliance date for additional traceability records under Section 204 of the Food Safety Modernization Act to July 2028 after major compliance milestones took effect in 2025[3]Source: United States Food and Drug Administration, “Requirements for Additional Traceability Records for Certain Foods, Compliance Date Extension,” Federal Register, federalregister.gov. These factors collectively strengthen the position of established players, limiting market fragmentation despite ongoing technological advancements.

Strategic moves in 2025 and 2026 further illustrate how scale players are adapting to this competitive landscape. BrightFarms is building regional hubs in Texas and Georgia to enhance retail distribution and regional coverage. Oishii’s partnership with MISUMI in March 2026 focuses on precision manufacturing for robotic cultivation, emphasizing premium fruit production and automation. Local Bounti’s capital raise in March 2026, following debt restructuring, underscores the growing importance of financial stability alongside farm expansion. Similarly, 80 Acres Farms expanded through distressed-asset acquisitions in 2025, leveraging lower build costs. These strategies collectively demonstrate that the United States vertical farming market is consolidating around regional scale, technological innovation, and disciplined capital management, driving it toward a more competitive, innovation-driven future.

United States Vertical Farming Industry Leaders

Little Leaf Farms, LLC

Gotham Greens Holdings, LLC

BrightFarms Inc.

Oishii Farm Corporation

Local Bounti Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Oishii Farm Corporation entered into a strategic partnership with MISUMI to supply precision-machined components for its robotic cultivation systems. This strengthens the United States vertical farming market by improving automation economics in premium berry production, which can support scale-up in high-value crops and expand future revenue opportunities beyond leafy greens.

- March 2026: Local Bounti secured USD 15 million in new capital to advance its growth strategy. The raise enables retail door expansion and operational efficiency investment without legacy capital-structure constraints.

- October 2025: Little Leaf Farms opened its fourth greenhouse at McAdoo, Pennsylvania, becoming the world's largest controlled environment agriculture leafy-greens producer with greater than 54% indoor lettuce market share across more than 8,000 United States stores.

United States Vertical Farming Market Report Scope

Vertical farming is an agricultural practice that involves growing crops in vertically stacked layers, typically within controlled indoor environments. This production system optimizes plant growth by regulating factors such as light, temperature, humidity, and nutrients, and commonly employs soilless cultivation techniques including hydroponics, aquaponics, and aeroponics.

The United States vertical farming market is segmented by growth mechanism (aeroponics, hydroponics, and aquaponics), by structure (building-based vertical farms, warehouse-based vertical farms, and shipping container vertical farms), by crop type (leafy greens, herbs and microgreens, fruits and berries, and flowers and ornamentals), by component (hardware, software, and others), and by end-user (retail and supermarkets, foodservice, direct-to-consumer and e-commerce, institutional and government, and pharmaceutical and cosmetic ingredient buyers). The report provides market size and forecasts in terms of value (USD) for all the aforementioned segments.

By Growth Mechanism

| Hydroponics |

| Aeroponics |

| Aquaponics |

By Structure

| Building-based Vertical Farms |

| Warehouse-based Vertical Farms |

| Shipping-Container Vertical Farms |

By Crop Type

| Leafy Greens |

| Herbs |

| Microgreens |

| Fruits and Berries |

| Flowers and Ornamentals |

By Component

| Hardware | Lighting Systems |

| HVAC and Climate Control | |

| Sensors and Monitoring | |

| Irrigation and Nutrient Delivery | |

| Racks, Trays, and Conveyance | |

| Power and Backup Systems | |

| Software | Farm Operating Systems |

| AI and Computer Vision | |

| Workflow, ERP, and Traceability | |

| Services | Design and Integration |

| Maintenance and Agronomy Support | |

| Managed Operations |

By End User

| Retail and Supermarkets |

| Foodservice |

| Direct-to-Consumer and E-commerce |

| Institutional and Government |

| Pharmaceutical and Cosmetic Ingredient Buyers |

| By Growth Mechanism | Hydroponics | |

| Aeroponics | ||

| Aquaponics | ||

| By Structure | Building-based Vertical Farms | |

| Warehouse-based Vertical Farms | ||

| Shipping-Container Vertical Farms | ||

| By Crop Type | Leafy Greens | |

| Herbs | ||

| Microgreens | ||

| Fruits and Berries | ||

| Flowers and Ornamentals | ||

| By Component | Hardware | Lighting Systems |

| HVAC and Climate Control | ||

| Sensors and Monitoring | ||

| Irrigation and Nutrient Delivery | ||

| Racks, Trays, and Conveyance | ||

| Power and Backup Systems | ||

| Software | Farm Operating Systems | |

| AI and Computer Vision | ||

| Workflow, ERP, and Traceability | ||

| Services | Design and Integration | |

| Maintenance and Agronomy Support | ||

| Managed Operations | ||

| By End User | Retail and Supermarkets | |

| Foodservice | ||

| Direct-to-Consumer and E-commerce | ||

| Institutional and Government | ||

| Pharmaceutical and Cosmetic Ingredient Buyers | ||

Key Questions Answered in the Report

What is the current size of the United States vertical farming market?

The United States vertical farming market stands at USD 1.6 billion in 2026.

Which crop category generates the most revenue in the United States?

Leafy greens are the largest crop segment, with 52.3% of revenue in 2025, because lettuce, spinach, and arugula remain the most optimized and retail-ready indoor categories.

Which growth mechanism is expanding the fastest in indoor farming across the United States?

Aeroponics is the fastest-growing mechanism, with a 16% CAGR during 2026-2031.

What is the biggest cost challenge for indoor farm operators?

Electricity is the main pressure point, with power accounting for 20% to 40% of production cost in many facilities, and lighting representing 60% to 85% of total electricity use.

Which end-user group is expanding the fastest beyond grocery retail?

Pharmaceutical and cosmetic ingredient buyers are the fastest end-user segment, with a 15% CAGR during 2026-2031, because they value controlled purity and repeatable phytochemical profiles.

Page last updated on: