Marine And Shipping TIC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.17 Billion |

| Market Size (2031) | USD 2.68 Billion |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

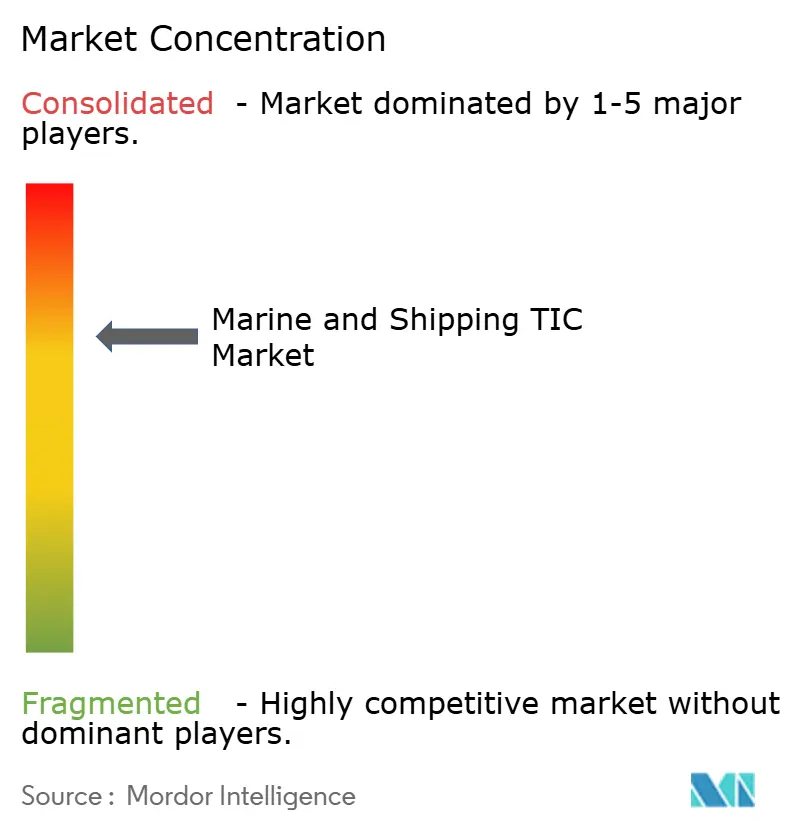

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Marine And Shipping TIC Market Analysis by ���ϲ�����

The Marine and Shipping TIC market size was valued at USD 2.08 billion in 2025 and is estimated to grow from USD 2.17 billion in 2026 to USD 2.68 billion by 2031, at a CAGR of 4.31% from 2026 to 2031. A decisive pivot from reactive compliance toward predictive risk management is reshaping demand, with decarbonization mandates, offshore wind build-outs, and the emergence of autonomous vessels rewriting survey scopes. Shipowners are commissioning ammonia, methanol, and hydrogen propulsion tests years before the International Maritime Organization’s Net-Zero Framework enters force, front-loading revenue for laboratories able to validate low-flashpoint fuels.[1]International Maritime Organization, “IMO Net-Zero Framework,” IMO.org Remote inspection platforms are shortening survey cycles and broadening the geographic reach, especially where geopolitical tensions or limited infrastructure restrict on-site access. Competitive differentiation is shifting from surveyor headcount to digital service portfolios that bundle analytics, voyage planning, and real-time condition monitoring into subscription models.

Key Report Takeaways

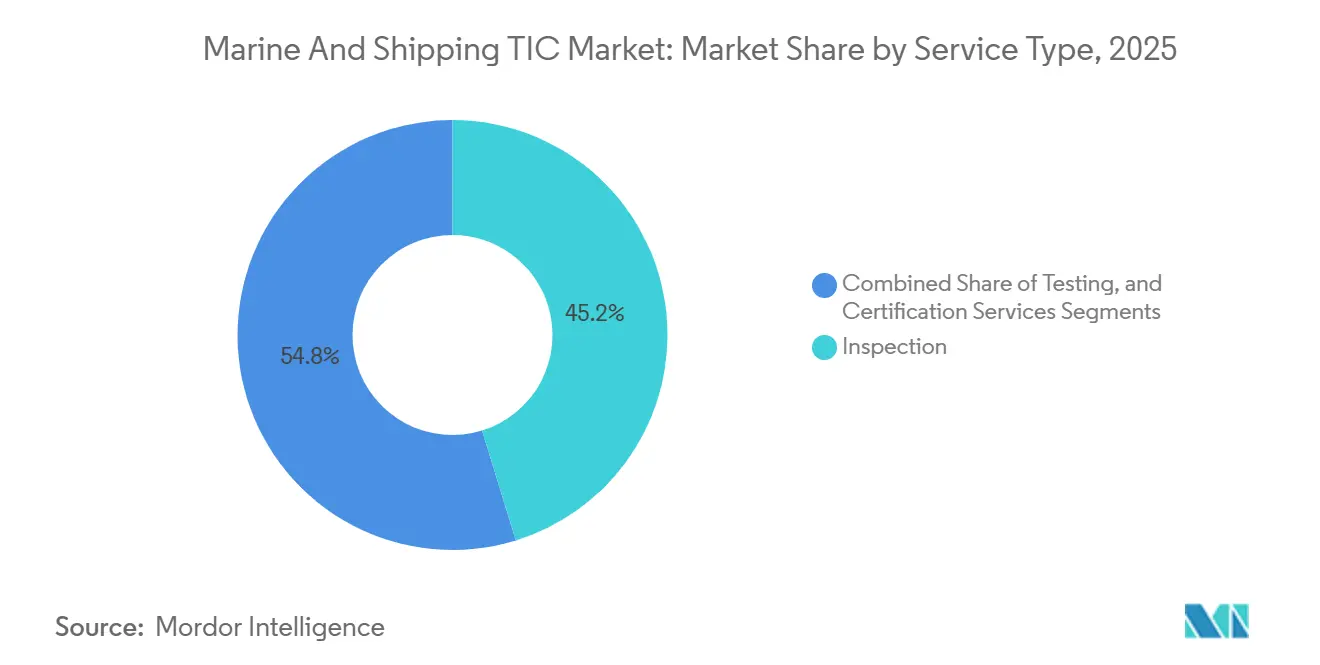

- By service type, inspection led with 45.23% of marine and shipping TIC market share in 2025, while certification is projected to register a 4.47% CAGR through 2031 as digital-twin and autonomous-navigation validations gain traction.

- By sourcing type, outsourced services accounted for 62.34% marine and shipping TIC market share in 2025 and are expected to advance at a 4.55% CAGR over 2026-2031, reflecting owners’ preference to delegate complex alternative-fuel and hull-integrity assessments.

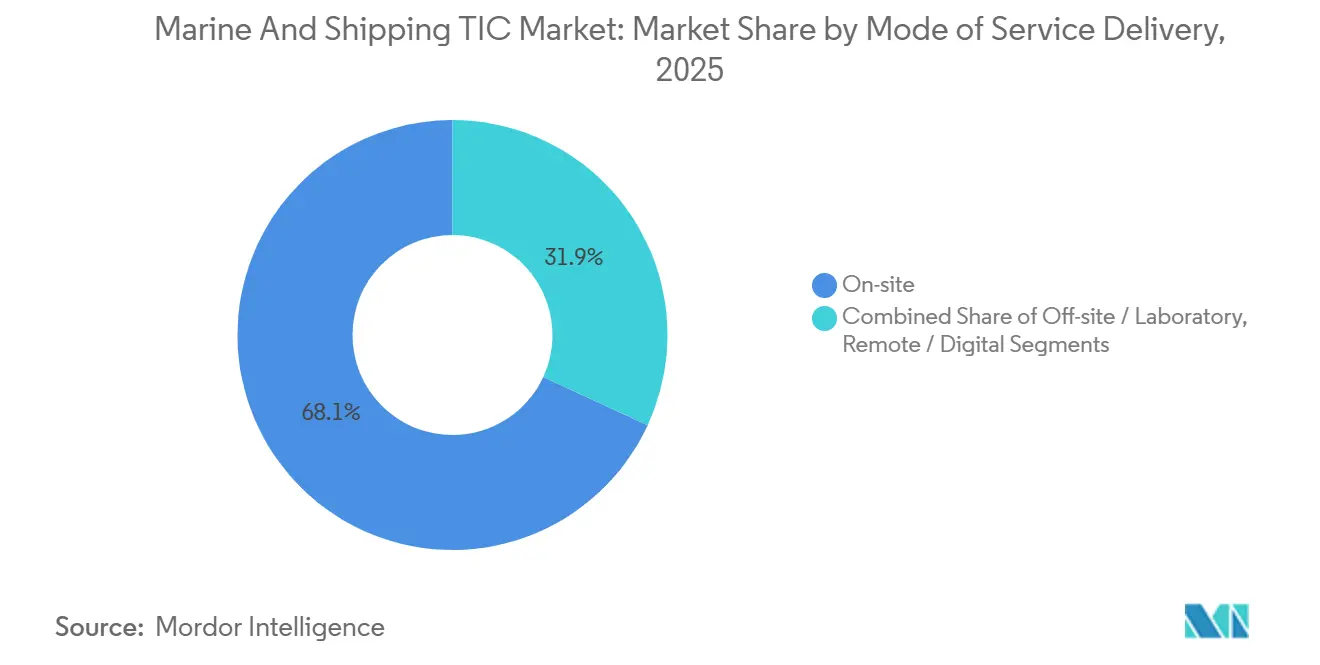

- By mode of service delivery, on-site surveys held 68.11% marine and shipping TIC market share in 2025, yet remote inspection is forecast to climb at a 5.59% CAGR to 2031, lifted by drone, crawler, and augmented-reality deployments.

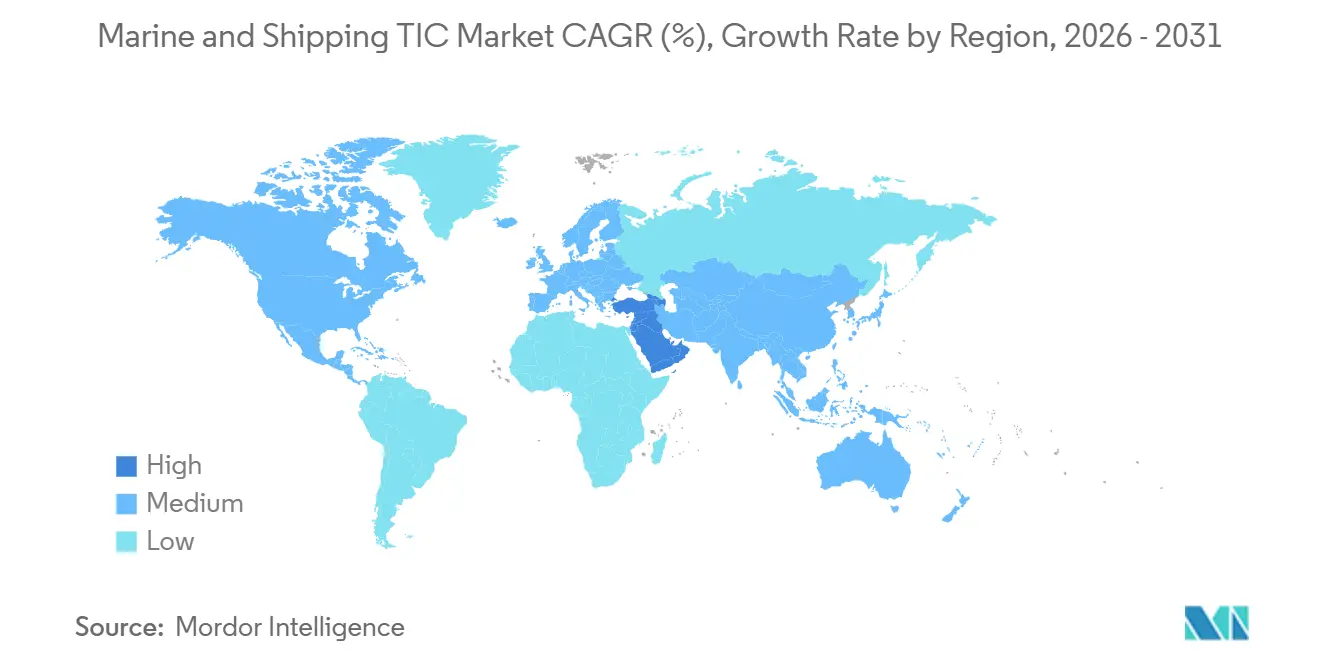

- By geography, Asia-Pacific captured 34.41% marine and shipping TIC market share in 2025, while the Middle East is poised for the fastest expansion at 5.61% through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Marine And Shipping TIC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decarbonization Mandates Driving Alternative Fuel Testing | +1.2% | Global, early uptake in Europe and Asia-Pacific | Medium term (2-4 years) |

| Accelerated Offshore Wind Installations Necessitating Marine Warranty Surveys | +0.9% | Europe, North America, Asia-Pacific offshore zones | Short term (≤ 2 years) |

| Expanding Digital Twin Adoption for Predictive Maintenance Verification | +0.7% | Global, concentrated in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growth in Autonomous Shipping Raising Certification Demand | +0.6% | Asia-Pacific (Japan, South Korea), Europe (Norway) | Long term (≥ 4 years) |

| Stricter Ballast Water Treatment Compliance Testing | +0.5% | Global, heightened enforcement in North America and Europe | Short term (≤ 2 years) |

| Insurance Premium Incentives for Verified Hull Integrity | +0.4% | Global, notable for aging fleets in Asia-Pacific and Europe | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Decarbonization Mandates Driving Alternative Fuel Testing

The International Maritime Organization has set carbon-intensity reduction milestones that escalate from 11% in 2026 to 21.5% by 2030, obligating owners to validate ammonia, methanol, and hydrogen propulsion systems before commercial deployment. DNV’s EU-funded Ammonia24 program has already issued safety guidance enabling an orderbook of 39 ammonia-fueled vessels to proceed, demonstrating how standardization accelerates capital commitments.[2]DNV, “Ammonia24 Project and Alternative Fuel Testing,” dnv.com Each alternative-fuel newbuild triggers commissioning tests, mid-term surveys, and retrofit validations, creating recurring revenue streams previously absent from diesel fleets. Lloyd’s Register complemented the shift by publishing hydrogen fuel-cell installation guidelines in 2025, giving shipyards clear reference points for ventilation, leak detection, and explosion-proof design. As goal-based standards replace prescriptive rules, classification societies are free to offer proprietary testing packages at premium rates for early adopters.

Accelerated Offshore Wind Installations Necessitating Marine Warranty Surveys

Europe’s 75 gigawatt installed offshore wind base and 380 gigawatt pipeline demand requires continuous marine warranty verification for jack-up vessels, dynamic positioning systems, and subsea cable equipment. DNV’s compliance certificates for Ørsted’s 4.2 gigawatt Hornsea 3 and 4 projects, issued in February 2026, exemplify the elevated technical rigor now applied to crane load curves and weather-window modeling. Bureau Veritas and American Bureau of Shipping issued similar approvals to heavy-lift vessels in early 2026, reinforcing a competitive race for high-margin survey work. Novel requirements such as blade-tolerance checks in 50-meter seas extend well beyond conventional cargo inspections, boosting fee potential. Bureau Veritas’s Marine and Offshore division reported EUR 1.16 billion (USD 1.24 billion) revenue in 2023, with offshore wind contributing a rising portion, underscoring the segment’s material impact on earnings.

Expanding Digital Twin Adoption for Predictive Maintenance Verification

Shipowners increasingly rely on digital twins to predict corrosion, fatigue, and machinery wear, but insurers insist on third-party validation before accepting virtual models as proof of seaworthiness. DNV’s ShipManager Hull platform installed on Saipem’s fleet required independent verification to satisfy underwriters, setting a precedent for paid digital-twin certification. Hyundai Heavy Industries earned Approval in Principle for its HiDTS ship-level digital twin, signaling shipyards’ willingness to invest in software once class notations are in place. The EU-backed TwinShip program is developing a universal zero-emission twin framework to 2028, likely seeding mandatory global standards post-2027. The market is bifurcating: large owners build proprietary twins and seek certification, while smaller operators purchase turnkey packages, favoring societies that combine software and validation under one roof.

Growth in Autonomous Shipping Raising Certification Demand

ClassNK awarded the world’s first AUTO-Nav2(All) notation to the GENBU container ship on 3 April 2026 under Japan’s MEGURI2040 initiative, confirming autonomous navigation for medium-distance coastal service. Japan’s transport ministry validated an autonomous Ro-Ro ferry in February 2026, and other flag states are studying the regulatory playbook. The IMO’s Maritime Autonomous Surface Ships code, adopted in non-mandatory form in May 2026, will become compulsory in 2032, spurring societies to create test protocols for collision-avoidance algorithms and cyber-resilience. Early movers enjoy a first-mover advantage, as builders favor partners that shorten approval lead times. Simulation labs and AI-validation benches, therefore, become strategic investments for classification societies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Qualified Marine Surveyors in Emerging Economies | -0.8% | Southeast Asia, Africa, South America | Medium term (2-4 years) |

| High Cost of Advanced Non-Destructive Testing Equipment | -0.6% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Fragmented Regulatory Framework Across Flag States | -0.4% | Global, variance among Paris MoU, Tokyo MoU, Caribbean MoU | Long term (≥ 4 years) |

| Geopolitical Tensions Impacting Cross-Border Inspection Access | -0.3% | Russia, China, Middle East | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Shortage of Qualified Marine Surveyors in Emerging Economies

Southeast Asia, Africa, and South America lack sufficient surveyors certified in alternative-fuel systems, digital twin validation, and advanced non-destructive testing. Training pipelines remain thin despite programs from the International Institute of Marine Surveying and Lloyd’s Register Maritime Academy.[3]International Institute of Marine Surveying, “Global Training Programs for Marine Surveyors,” iims.org.uk China and South Korea control more than 80% of global shipbuilding orders, yet regional workforces struggle to master IACS unified requirements, stretching approval lead times. Indian Register of Shipping relies on expatriate experts for complex inspections, raising project costs. Without mandated continuous education on AI-driven diagnostics under the STCW Convention, the skills gap persists, especially in African ports where detention rates stay elevated.

High Cost of Advanced Non-Destructive Testing Equipment

Phased-array ultrasonic scanners, acoustic-resonance crawlers, and corrosion-under-insulation sensors can cost beyond USD 500,000 per unit, a prohibitive hurdle for independent surveyors and small shipyards. Lloyd’s Register validated the ORCA hull-inspection crawler in March 2026, delivering ±0.22-millimeter accuracy through coatings yet demanding specialist operators and regular calibration. Intertek’s real-time corrosion-under-insulation service, launched in February 2026, detects 250-micron defects but is priced for large fleets, creating a two-tier diagnostic market. The EU-funded AUTOASSESS project aims to democratize autonomous aerial inspection, though commercialization is unlikely before 2028, leaving a short-term affordability gap.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Certification Gains as Digital Validation Scales

Certification accounted for the fastest expansion, with a 4.47% CAGR, reflecting owners’ need to prove autonomous navigation and alternative-fuel safety. Inspection remained the largest slice at 45.23% in 2025, anchored by statutory hull-thickness and ballast-water checks. The Marine and Shipping TIC market size for certification services is projected to grow steadily as digital twin and software validation mature. The rising uptake of ClassNK’s AUTO-Nav2 (All) notation and Bureau Veritas’s Augmented Surveyor 3D platform underscores how real-time data flows blur the boundaries between Inspection and certification. Owners increasingly bundle lab tests within integrated survey contracts, compressing administration and tilting revenue toward full-scope providers.[4]ClassNK, “AUTO-Nav2(All) Notation for GENBU Container Ship,” classnk.or.jp

Testing services expand more slowly, yet fuel-quality analysis and emissions sampling remain indispensable for compliance. Continuous monitoring subscriptions tied to drone imagery and LiDAR scans expand recurring revenue, reinforcing the structural shift from one-off reports to data-driven lifecycle assurance. As remote tools proliferate, certification’s strategic importance grows because regulators and insurers rely on class approvals to accept algorithmic or sensor-based evidence.

By Sourcing Type: Outsourced Services Dominate Amid Complexity

Outsourcing accounted for 62.34% of 2025 expenditure and are also advancing at 4.55% CAGR and will continue to rise as owners delegate ballast-water system audits, hull-integrity scans, and alternative-fuel validations to societies with global footprints. The Marine and Shipping TIC market share for outsourced engagements was well above that of in-House programs, signaling the premium placed on third-party impartiality. High equipment costs and rapid technology turnover disincentivize in-house investment, prompting even large liners to adopt hybrid models that pair onboard monitoring with external certification.

Lloyd’s Register’s integration of OTG and OneOcean illustrates the outsourcing value proposition, giving customers consolidated voyage planning and compliance tracking. Conversely, the Indian Register of Shipping leverages regional proximity and competitive fees to win orders from CMA CGM and Maersk, proving that agile challengers can secure contracts where incumbents are costlier. Insurance underwriters reinforce the outsourcing trend by mandating independent condition surveys before policy renewal, particularly on ships older than 15 years.

By Mode of Service Delivery: Remote Inspection Surges Post-Pandemic

On-site surveys commanded 68.11% in 2025, reflecting regulatory reliance on physical hull checks during drydockings. Remote inspection, however, is the fastest-growing channel, with a 5.59% CAGR to 2031, as drone, crawler, and augmented-reality platforms eliminate the need for scaffolding and confined-space entry. The Marine and Shipping TIC market size attributed to remote channels is set to grow as flag states progressively accept digital evidence in line with IMO-approved guidelines.

Lloyd’s Register’s validation of TSC Subsea’s ORCA crawler and American Bureau of Shipping’s oversight of a fully robotic FPSO tank survey show remote methods moving from pilot to routine operations. Drone-enabled visual mapping reduces survey time by roughly 40%, translating into lower off-hire costs. Yet acceptance remains patchy, with some flag administrations restricting remote eligibility to intermediate or annual inspections, compelling societies to maintain blended service portfolios.

Geography Analysis

Asia-Pacific held 34.41% of 2025 revenue, propelled by China’s 52.8% share of global shipbuilding orders and South Korea’s 28.1% orderbook leadership. ClassNK rose to first place by vessel count, and China Classification Society climbed into the top five by gross tonnage, evidencing robust regional activity.[5]Clarkson Research, “Global Shipbuilding Market Share Data,” clarksons.com Japan’s MEGURI2040 program certified four autonomous vessels in early 2026, spurring demand for novel testing frameworks. Indian Register of Shipping delivered 115 vessels since January 2025 and opened a Saudi Arabia office, extending Asia-Pacific know-how into adjacent markets. Korean Register’s revenue advanced 4% year over year to KRW 206 billion (USD 155 million) in 2025 and targets further gains in 2026, in line with rising domestic construction activity.

The Middle East is forecast to post the fastest regional CAGR at 5.61% through 2031. Saudi Arabia’s port investments and the United Arab Emirates’ logistics expansion attract classification societies seeking proximity to greenfield terminals and offshore energy projects. Survey demand also heightens when geopolitical flare-ups raise war-risk premiums in the Strait of Hormuz, intensifying calls for independent hull and machinery inspections. Indian Register of Shipping’s Riyadh branch illustrates strategic positioning to capture these opportunities.

Europe and North America exhibit below-average growth due to mature fleets, but they dominate high-margin niches such as offshore wind, marine warranty surveys, and digital-twin certifications. DNV’s Bremerhaven Offshore Wind Competence Center, with 100 engineers, and Lloyd’s Register’s Houston office underline continued investment in advanced capabilities. Africa and South America lag due to limited surveyor pools and testing infrastructure, though remote inspection and training partnerships are gradually unlocking latent potential.

Competitive Landscape

Japan's Market concentration is moderate. The top five societies, American Bureau of Shipping, DNV, ClassNK, Lloyd’s Register, and China Classification Society, hold a significant share of global revenue, yet rivalry remains intense. Lloyd’s Register’s November 2024 acquisition of OTG fused voyage-planning analytics with regulatory intelligence, while Bureau Veritas’s pending EUR 375 million (USD 401 million) purchase of Lotusworks aims to add semiconductor and data-center inspections, diversifying income streams. Digital platforms such as Bureau Veritas’s Augmented Surveyor 3D and DNV’s ShipManager Hull strengthen customer lock-in through continuous monitoring.[6]Lloyd’s Register, “OTG Acquisition and OneOcean Integration,” lr.org

Autonomous-vessel certification, offshore-wind surveys, and alternative-fuel validations represent white-space territories where early entrants command premium pricing. ClassNK’s April 2026 AUTO-Nav2 (All) notation set a high bar that competitors must match.

Smaller challengers like the Indian Register of Shipping and the Korean Register exploit cost advantages and faster turnaround to win regional contracts, pushing incumbents to innovate. The non-binding Yacht Safety and Environmental Consortium, formed in September 2024, highlights collaborative efforts to harmonize standards, yet execution speed and the breadth of digital services remain key differentiators.

Marine And Shipping TIC Industry Leaders

Bureau Veritas SA

Intertek Group plc

SGS SA

TÜV SÜD AG

DEKRA SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ClassNK awarded the first AUTO-Nav2(All) notation to the GENBU container ship, certifying autonomous navigation under Japan’s MEGURI2040 program.

- April 2026: Lloyd’s Register and Cyclus Marine signed an agreement to create a unified ship-recycling certification that prioritizes environmental and worker safety standards.

- March 2026: DNV acquired AquaCloud, enhancing its data infrastructure offerings for environmentally monitored aquaculture operations.

- June 2025: Bureau Veritas launched Augmented Surveyor 3D, combining artificial intelligence, LiDAR, and drones to automate cargo-hold inspections.

- June 2025: The Polish Register of Shipping and the China Classification Society agreed on mutual recognition of certification and joint alternative-fuel research.

Global Marine And Shipping TIC Market Report Scope

The Marine and Shipping TIC Market Report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-house, and Outsourced), Mode of Service Delivery (On-site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Testing | |

| Inspection | ||

| Certification | ||

| By Sourcing Type | In-house | |

| Outsourced | ||

| By Mode of Service Delivery | On-site | |

| Off-site / Laboratory | ||

| Remote / Digital | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Marine and Shipping TIC market size and how fast is it growing?

The Marine and Shipping TIC market size stands at USD 2.17 billion in 2026 and is forecast to reach USD 2.68 billion by 2031, growing at a 4.31% CAGR.

Which service type is expanding the quickest in Marine and Shipping TIC?

Certification services post the fastest growth, projected at a 4.47% CAGR between 2026-2031 as owners seek third-party validation for digital-twin, autonomous-navigation, and alternative-fuel applications.

Why are remote inspections gaining traction among vessel operators?

Drone, crawler, and augmented-reality tools cut survey duration by about 40%, reduce off-hire costs, and enable access where geopolitical or logistical constraints limit on-site surveys, prompting a 5.59% CAGR for remote inspection channels.

Which region offers the highest growth opportunity for TIC providers?

The Middle East is forecast to grow at 5.61% through 2031, driven by port expansion in Saudi Arabia and the United Arab Emirates and rising offshore-energy logistics demand.

How are alternative fuels influencing demand for testing and certification?

Ammonia, methanol, and hydrogen propulsion systems require new safety and performance protocols, creating recurring revenue for laboratories and classification societies as each vessel must undergo commissioning tests and periodic surveys.

Who are the leading companies in Marine and Shipping TIC and what is their combined influence?

American Bureau of Shipping, DNV, ClassNK, Lloyd's Register, and China Classification Society dominate with about 85% of global tonnage under class, giving them substantial sway over standard-setting and digital-service adoption.

Page last updated on: