Industrial And Manufacturing TIC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

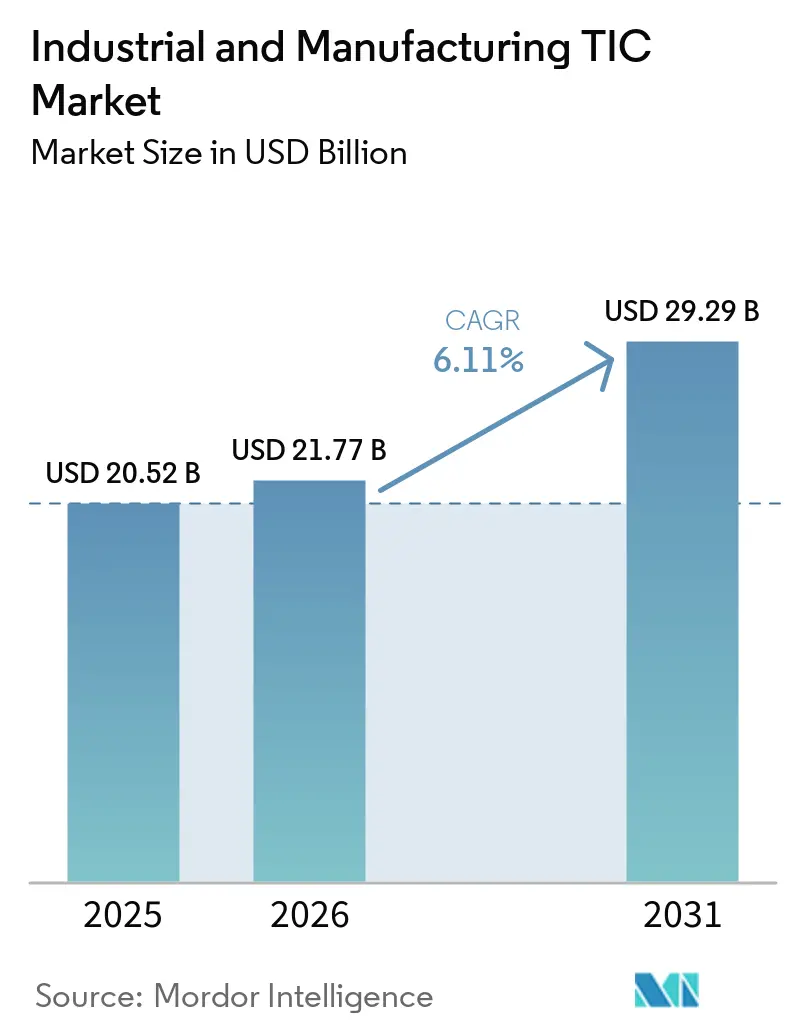

| Market Size (2026) | USD 21.77 Billion |

| Market Size (2031) | USD 29.29 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Industrial And Manufacturing TIC Market Analysis by ���ϲ�����

The industrial and manufacturing TIC Market size is expected to increase from USD 20.52 billion in 2025 to USD 21.77 billion in 2026 and reach USD 29.29 billion by 2031, growing at a CAGR of 6.11% over 2026-2031. The industrial and manufacturing TIC market is moving away from reactive compliance checks and toward technology-linked quality assurance that supports risk control and market entry. Manufacturers now use third-party testing, inspection, and certification more as a commercial safeguard than as a narrow compliance expense, as evidenced by the rise of outsourced specialty inspection work and recurring certification contracts. The industrial and manufacturing TIC market is also being reshaped by stricter national standards in Asia-Pacific, broader sustainability rules, digital product passport requirements, and expanding AI conformity needs that are pushing certification beyond legacy product safety scopes. At the same time, outsourcing is gaining structural strength because several newer regulatory frameworks reserve critical conformity assessment roles for accredited third parties, while competition remains moderate at the top, with global-scale providers operating alongside regional and specialist firms.

Key Report Takeaways

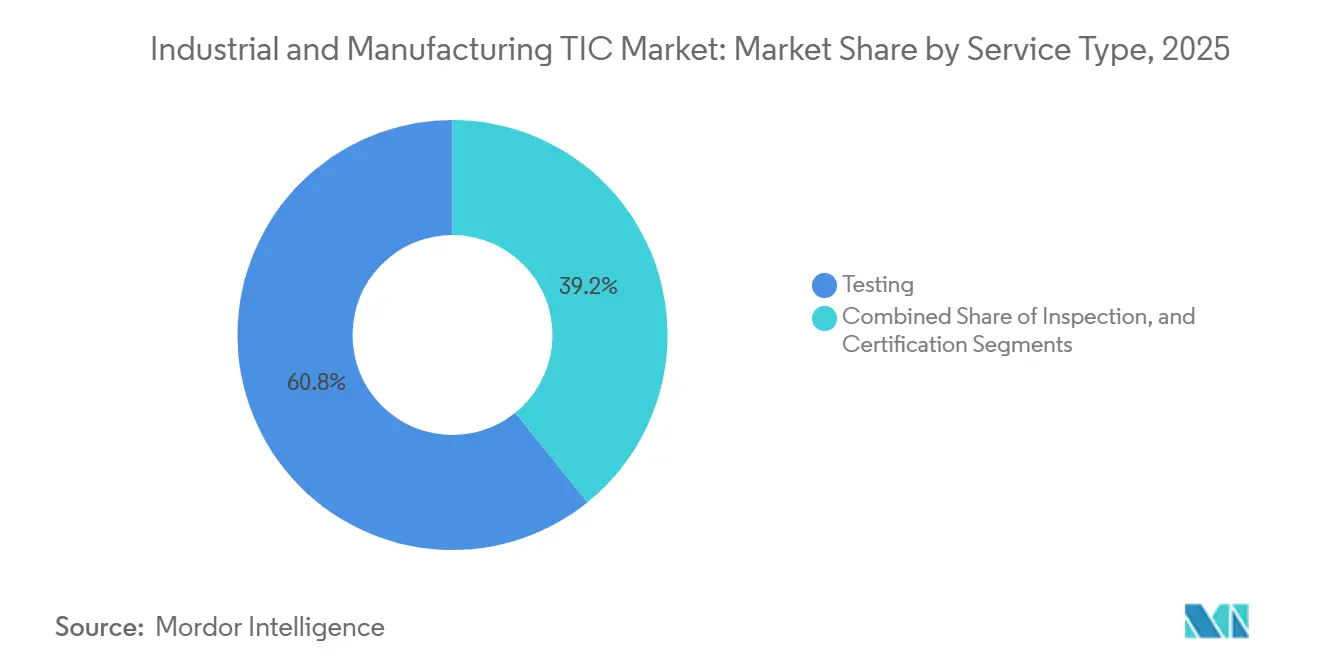

- By service type, testing led with a 60.81% share of the industrial and manufacturing TIC market in 2025, while certification is projected to record the fastest growth at a 6.25% CAGR through 2031.

- By sourcing type, outsourced services held 60.32% share of the industrial and manufacturing TIC market in 2025, and the same category is forecast to expand at the fastest 7.01% CAGR through 2031.

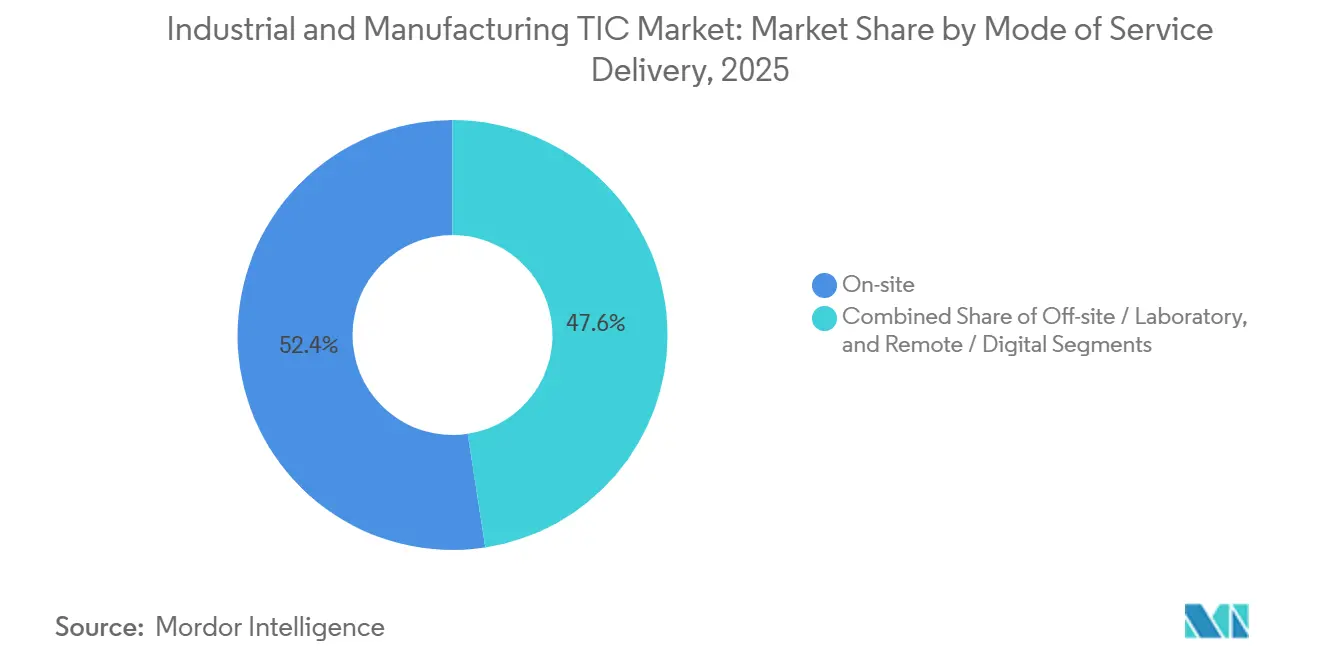

- By mode of service delivery, on-site delivery accounted for a 52.44% share of the industrial and manufacturing TIC market in 2025, while remote and digital delivery is expected to grow the fastest at a 6.66% CAGR through 2031.

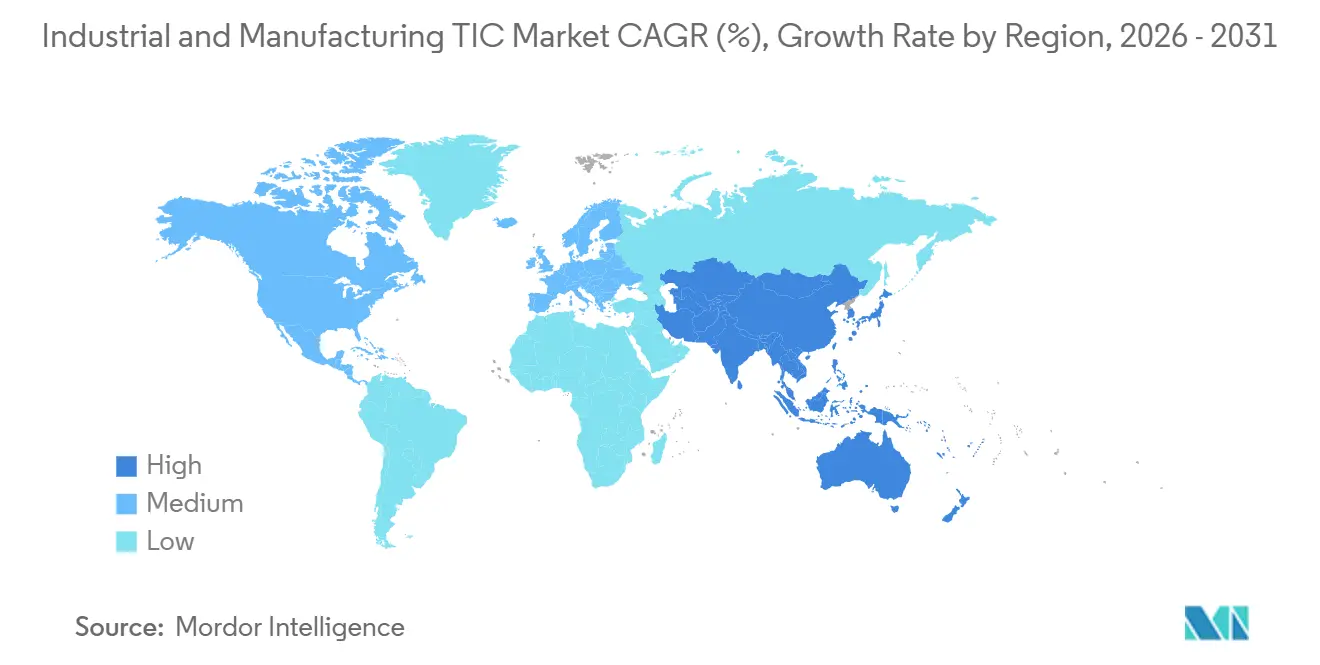

- By geography, Asia-Pacific captured 45.63% share of the industrial and manufacturing TIC market in 2025 and is also the fastest-growing regional segment with a 6.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial And Manufacturing TIC Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Global Product Safety and Process Compliance Rules | +1.7% | Global | Short term (≤ 2 years) |

| Industry 4.0 and Connected Machinery Validation Needs | +1.2% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| EU Machinery Regulation Cybersecurity and AI Conformity Burden | +0.9% | Europe is primary, North America and Asia-Pacific spill-over | Short term (≤ 2 years) |

| Rising Outsourcing of Specialist TIC by Mid-Sized Manufacturers | +0.7% | Global, with Asia-Pacific and North America leading | Medium term (2-4 years) |

| Sustainability and Circular Economy Certification Demand | +0.6% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Carbon and Product Passport Verification Demand in Industrial Supply Chains | +0.5% | Europe primary, early adoption in North America | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Tightening Global Product Safety and Process Compliance Rules

Mandatory conformity assessment has become the baseline across industrial supply chains, and that shift remains the largest structural demand driver for the industrial and manufacturing TIC market. The EU Ecodesign for Sustainable Products Regulation widened lifecycle verification expectations, while the WTO Technical Barriers to Trade framework continues to support mutual recognition arrangements that increase the value of multi-jurisdiction credentials for exporters.[1]European Parliament and Council, “Regulation (EU) 2023/1230 on Machinery,” EUR-Lex, eur-lex.europa.eu The change is visible in automotive and industrial controls, where standards such as ISO 26262 and IEC 61508 are now applied to software-heavy systems and safety functions that depend on advanced electronic control units, thereby expanding the need for independent assessment. Tier-one suppliers in Germany and Japan that once relied more heavily on internal verification now engage accredited third parties when auditors require independent confirmation for safety-integrity-level components and related documentation packages. As these obligations move from OEMs down to component suppliers, the industrial and manufacturing TIC market gains a wider customer base and a larger recurring workload. This is why certified inspection and validation services are reaching deeper into the supply chain than the original compliance buyer.

Industry 4.0 and Connected Machinery Validation Needs

The spread of IIoT sensors, autonomous robotics, and edge-computing controllers has created a validation workload that older laboratory protocols were not built to handle. Connected machinery now needs electromagnetic compatibility tests, mechanical safety checks, cybersecurity assessments, protocol interoperability reviews, and reliability validation under live operating conditions, which extends both testing time and laboratory requirements. The OPC Foundation stated in March 2026 that support for OPC UA version 1.03 will end by year-end 2026, requiring manufacturers to validate against version 1.05 to maintain certified interoperability. That kind of protocol transition creates repeat recertification demand and supports a more continuous service model inside the industrial and manufacturing TIC market. MISTRAS Group reaffirmed full-year 2026 revenue guidance of USD 730 million to USD 750 million in May 2026, while its aerospace and defense segment revenue rose 35.5% year over year in Q1 2026, which points to stronger demand for complex validation work in digitally integrated equipment. Providers that combine analytics with physical inspection are better positioned to win these budgets, as digital asset operators increasingly seek ongoing condition visibility rather than isolated test events.

EU Machinery Regulation Cybersecurity and AI Conformity Burden

The EU Machinery Regulation is increasing the workload for conformity assessment of connected and AI-enabled machinery, which is becoming an important driver of demand for the industrial and manufacturing TIC market. Regulation (EU) 2023/1230 expands the role of third-party assessment for higher-risk machinery categories and places more weight on safety, documentation, and conformity evidence for connected systems. That has pushed manufacturers to prepare technical files, risk assessments, and supporting test records earlier, which is already raising pre-compliance activity in 2026. Bureau Veritas reported that industrial products certification delivered high single-digit organic growth in Q1 2026, supported in part by strong demand in machinery and pressure vessel certification. The same direction of travel is increasing the relevance of cybersecurity testing and AI management system assurance as manufacturers try to avoid late-stage remediation and certification delays. This is widening the commercial scope of certification beyond traditional product safety and into software behavior, system updates, and connected operational risk.

Rising Outsourcing of Specialist TIC by Mid-Sized Manufacturers

Mid-sized manufacturers are outsourcing specialist TIC work faster than their larger peers because many cannot maintain multi-domain accreditation in-house at a viable cost. The industrial and manufacturing TIC market is benefiting from this shift because outsourcing converts fixed laboratory and staffing burdens into variable service contracts. SGS closed its acquisition of Applied Technical Services for USD 1.325 billion on January 13, 2026, adding 85 US facilities and 2,100 employees, thereby directly strengthening its ability to serve clients seeking a single outsourced partner. As more rules require designated accredited bodies, outsourcing moves from a cost choice to a structural compliance model.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Multi-Standard Compliance Cost for Small and Mid-Sized Manufacturers | -0.8% | Global, most acute in South America and Middle East and Africa | Medium term (2-4 years) |

| Shortage of Qualified Inspectors and Advanced Lab Talent | -0.6% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Fragmented Acceptance of Remote and Hybrid Inspections Across Accreditation Regimes | -0.4% | Global | Medium term (2-4 years) |

| Liability and Data Integrity Risk in Connected-Asset Testing | -0.3% | North America and Europe, Asia-Pacific growing | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Multi-Standard Compliance Cost for Small and Mid-Sized Manufacturers

Overlapping national and international compliance systems create a heavier burden for small and mid-sized manufacturers than for larger firms, limiting their full participation in the industrial and manufacturing TIC market. A single product sold into North America, Europe, and Asia-Pacific may still require separate certification routes, documentation, and renewal cycles, which adds both cost and delay. The self-declaration route under ISO/IEC 17050 provides only partial relief, as many regulated categories still require a designated third party. That means the highest-cost categories often remain the least flexible ones for smaller exporters. TIC providers that can bundle multi-market programs under a single contract can reduce this friction, but the underlying demand constraint still slows broader adoption across the industrial and manufacturing TIC market.

Shortage of Qualified Inspectors and Advanced Lab Talent

The shortage of skilled inspectors and advanced laboratory staff is limiting throughput in the industrial and manufacturing TIC market, and this issue cannot be solved solely through equipment spending. The US Bureau of Labor Statistics data showed more than 24,000 annual lab technician vacancies, while only 12% of current technicians said they were likely to remain in the field long term. The Government Accountability Office reported that the FDA inspector vacancy rate approached 20% across human foods inspection divisions in 2025-2026, and it also noted that new investigators often need 2-3 years of experience before they can conduct independent foreign inspections.[2]U.S. Government Accountability Office, “Drug Safety, FDA Should Implement Strategies to Retain Its Inspection Workforce,” GAO, files.gao.gov That long training curve matters because industrial metrology, quality assurance, and inspection work also depend heavily on tacit knowledge and equipment-specific judgment. Providers are investing in AI analytics, augmented guidance, and virtual training tools to improve utilization, but core field inspections still depend on experienced staff. Until that talent pipeline improves, capacity growth in the industrial and manufacturing TIC market will remain partly constrained even where demand is strong.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Anchors Revenue While Certification Captures New Ground

Testing retained a 60.81% share of the industrial and manufacturing testing, inspection, and certification (TIC) market in 2025, which kept it as the clear revenue anchor across service types. Testing covers a broad range of work, from destructive mechanical tests on structural materials to non-destructive testing of welds, electromagnetic compatibility checks on control systems, and firmware validation on connected equipment. That breadth keeps the industrial and manufacturing TIC market closely tied to testing, as nearly every product development and production stage still requires evidence that performance, safety, and reliability standards are met. Inspection remained the second-largest service type because industrial operators continue to require in-service asset integrity reviews, plant audits, and factory checks across capital-intensive sectors. Certification was smaller by revenue, but it is projected to grow at a 6.25% CAGR through 2031 as the service mix shifts toward recurring assurance programs rather than single-event validation. SGS became the first organization globally to receive ISO/IEC 42001 AI management system certification, demonstrating that AI assurance is moving toward a recurring, certifiable service line rather than remaining a one-time advisory exercise.

The certification path is widening because sustainability reporting, digital product passport frameworks, energy management systems, and AI governance requirements now create new audit scopes across manufacturing operations. Bureau Veritas stated that its industrial products certification services delivered high single-digit organic revenue growth in both full-year 2025 and Q1 2026, with railway systems assessment and pressure vessel certification among the strongest contributors. That pattern supports the view that the industrial and manufacturing TIC market is no longer driven solely by legacy safety certification, as newer assurance categories are generating fresh, recurring demand. Testing, therefore, remains the largest part of the industrial and manufacturing TIC market, while certification is steadily gaining ground as self-declaration routes narrow and formal third-party evidence becomes more valuable. This balance explains why leading providers continue to invest in both laboratory infrastructure and higher-value certification portfolios.

By Sourcing Type: Outsourcing Becomes The Default Compliance Model

Outsourced services captured 60.32% of the industrial and manufacturing testing, inspection, and certification (TIC) market share in 2025 and are forecast to grow at a 7.01% CAGR through 2031, making outsourcing the fastest-growing sourcing category. The shift is structural because several regulatory systems now require accredited third-party participation for high-risk or formal conformity outcomes. In-house TIC still matters for large manufacturers that handle high sample volumes, manage sensitive intellectual property, or operate in tightly controlled production settings such as specialty chemicals, aerospace components, and semiconductor fabrication. Even in those sectors, captive labs often focus on internal process validation while external bodies are used for final conformity submissions and recognized certification. That means the industrial and manufacturing TIC market is becoming more dependent on outsourced specialists, even where manufacturers retain some internal testing capacity.

The acceleration is strongest in Asia-Pacific, where new manufacturing capacity is coming online quickly, and in North America, where reshoring is increasing the number of standards and jurisdictions that firms must manage. SGS reinforced that direction with its January 2026 acquisition of ATS, which added a broad US industrial testing and inspection footprint, especially relevant for mid-market manufacturers seeking a single outsourced compliance partner.[3]SGS SA, “SGS Successfully Closes Applied Technical Services Acquisition,” SGS, sgs.com Providers that can bundle testing, inspection, and certification under a single framework agreement are gaining a larger role in the industrial and manufacturing TIC industry, as they simplify vendor management and reduce the burden of multi-market coordination. As a result, the industrial and manufacturing TIC market is moving toward longer-duration, more integrated outsourcing contracts rather than fragmented project-based assignments.

By Mode of Service Delivery: On-Site Leads While Remote Channels Redefine The Perimeter

On-site delivery accounted for 52.44% of the industrial and manufacturing testing, inspection, and certification (TIC) market in 2025, reflecting the physical realities of asset inspection, factory auditing, and process validation in industrial environments. Many inspections still require direct access to equipment, facilities, and operating conditions, which keeps the on-site model central to the industrial and manufacturing TIC market. Off-site and laboratory delivery remained the second-largest mode because a large part of testing work still depends on controlled environments for materials characterization, chemical analysis, and type-approval procedures. Remote and digital delivery is forecast to grow at a 6.66% CAGR through 2031, supported by continuous condition monitoring, drone-enabled visual reviews, and cloud-based data platforms. This is extending the reach of the industrial and manufacturing TIC market into more continuous, data-linked service models rather than solely site-visit-based workflows.

The remote channel is advancing more slowly than its technical potential because many accreditation systems still differ on whether remotely gathered evidence can substitute for physical verification. ILAC has issued guidance on remote assessments, but acceptance still varies across jurisdictions and inspection categories, creating commercial friction for providers and clients. When remote methods are accepted, providers can review routine condition data more quickly and reserve senior inspectors for cases that require a physical presence. That improves throughput, but it does not eliminate the need for in-person judgment in safety-critical environments. The industrial and manufacturing TIC market will therefore keep a hybrid delivery structure, with digital tools expanding the perimeter of inspection while on-site work remains indispensable.

Geography Analysis

Asia-Pacific held 45.63% of the industrial and manufacturing TIC market share in 2025 and is expected to expand at a 6.94% CAGR through 2031, making it both the largest and fastest-growing regional block. Rising domestic production, stricter national standards, and export-linked compliance needs support the industrial and manufacturing TIC market in Asia-Pacific. China continues to expand the scope of products subject to mandatory certification through the CCC system and ongoing updates to GB standards, sustaining recurring testing and certification demand. India is adding new demand through BIS certification and through production-linked incentive programs in electronics, pharmaceuticals, and advanced chemistry cells that tie manufacturing growth to formal compliance requirements. Intertek acquired the assets of a solar PV laboratory in Ahmedabad in April 2026, creating an ISO 17025-accredited facility with BIS and IECEE CB Scheme accreditations that align with India’s manufacturing and renewable build-out goals.[4]Intertek Group plc, “Intertek Strengthens Solar Assurance Leadership with Purchase of Mitsui Chemicals Solar Laboratory Assets in India,” Intertek, intertek.com

Japan provides a stable demand through its precision manufacturing and electronics base, where quality requirements and established standards frameworks continue to support formal TIC spending. South Korea is also gaining momentum as mandatory conformity assessment requirements expand for machinery and energy-related equipment, further strengthening the regional role of the industrial and manufacturing TIC market. Europe remains the most regulation-dense region, with CE marking, REACH, RoHS, and incoming machinery and cybersecurity obligations creating a structurally recurring certification cycle. Germany continues to stand out because it combines a deep engineering base with leading TIC headquarters such as DEKRA, TÜV SÜD, TÜV Rheinland, and TÜV NORD, all of which support both domestic and cross-border certification activity. North America remains a core revenue region for the industrial and manufacturing TIC market because reshoring in electronics, medical devices, and advanced industrial systems is adding multi-state and multi-standard compliance work. SGS strengthened its North American position materially through the ATS acquisition in January 2026, which raised the scale threshold for regional specialists competing in industrial testing and inspection breadth.

The Middle East, Africa, and South America still represent smaller but developing parts of the industrial and manufacturing TIC market. Saudi Arabia and the United Arab Emirates are expanding mandatory conformity systems as part of industrial diversification programs, while South Africa and Egypt are building national accreditation capacity that should gradually reduce reliance on foreign-accredited bodies. In South America, Brazil continues to expand the scope of compulsory certification through INMETRO, while Argentina’s demand for industrial safety inspections is growing alongside formal manufacturing activity. These regions offer a longer-cycle opportunity because regulatory infrastructure and accreditation networks need time to mature, but supply chain diversification and local-content policies are steadily improving the demand base for the industrial and manufacturing TIC market.

Competitive Landscape

The industrial and manufacturing TIC market shows moderate concentration at the top international tier, with SGS SA, Bureau Veritas SA, and Intertek Group plc holding strong positions through large laboratory networks, broad accreditation portfolios, and wide geographic coverage. Their advantage comes from scale, multi-country client relationships, and the ability to combine testing, inspection, and certification into framework contracts that smaller firms often cannot match. At the same time, the industrial and manufacturing TIC market still leaves room for regional providers and specialist firms, as technical depth, local approvals, and niche inspection capabilities matter across many verticals. This creates a structure where global breadth and specialized differentiation coexist rather than fully displacing one another. That balance is one reason competition remains active even though the top tier is well established.

SGS further strengthened its strategic position in 2025 and 2026 through a series of digital trust and connectivity initiatives. The company acquired Granite River Labs Services in March 2026 to deepen its validation capabilities for high-speed wired data connections for servers, chips, and industrial electronics, supporting the growing compliance needs of AI-enabling infrastructure. SGS also expanded AI assurance through its agreement with CertX and linked that offer to the NVIDIA Halos Systems Inspection Lab ecosystem, which targets automotive, robotics, and industrial automation applications that require higher conformity. Bureau Veritas signed an agreement in April 2026 to acquire Lotusworks for EUR 375 million (USD 409 million), which gives it a stronger platform in data center commissioning and semiconductor manufacturing quality assurance, two areas where complexity supports premium pricing and long-term contracts. These moves show that the industrial and manufacturing TIC market is rewarding providers that expand beyond traditional inspection capacity into higher-value digital and mission-critical assurance work.

The competitive white space sits in digital-native inspection software and in underserved industrial client groups in Asia-Pacific, the Middle East, and Africa. MISTRAS Group reaffirmed 2026 revenue guidance of USD 730 million to USD 750 million and reported an 18.7% year-over-year increase in adjusted EBITDA in Q1 2026, which indicates that specialist asset-integrity and NDT providers can still grow well where technical expertise matters more than global scale.[5]MISTRAS Group Inc., “MISTRAS Announces First Quarter 2026 Results,” MISTRAS Group, mistrasgroup.com Accreditation rules under ISO/IEC 17065 and ISO/IEC 17020 continue to act as meaningful barriers to entry because commercially accepted certification and inspection results still depend on recognized formal status. That protects incumbent positions in the industrial and manufacturing TIC market, even as software-led challengers try to automate parts of inspection workflows and improve productivity.

Industrial And Manufacturing TIC Industry Leaders

SGS SA

Bureau Veritas SA

Intertek Group plc

DEKRA SE

TÜV SÜD AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Intertek Group plc acquired the solar PV laboratory assets of Mitsui Chemicals India Pvt. Ltd. in Ahmedabad, Gujarat, creating an ISO 17025-accredited testing facility offering BIS and IECEE CB Scheme accreditations to serve the expanding Indian renewable energy manufacturing sector.

- March 2026: Bureau Veritas signed an agreement to acquire Lotusworks, a specialist in commissioning, quality assurance, and calibration for data centers and semiconductor manufacturing facilities, for an enterprise value of EUR 375 million (USD 409 million). The transaction, expected to close by summer 2026, establishes a new mission-critical platform with a combined revenue of EUR 300 million (USD 340 million).

- March 2026: SGS acquired Granite River Labs Services, a specialist in validating high-speed wired data connections for servers, chips, and industrial electronics, with over 200 experts across 9 laboratories in Asia, Europe, and the United States. The acquisition reinforces SGS's digital trust and connectivity positioning for AI-enabling infrastructure.

- March 2026: Eastman announced that its Kingsport, Tennessee, facility achieved ISO 59014 certification from SCS Global Services for its methanolysis recycling technology, covering sustainability and traceability in secondary material recovery, signaling a widening secondary-material certification market.

Global Industrial And Manufacturing TIC Market Report Scope

The Industrial and Manufacturing Testing, Inspection, and Certification (TIC) market comprises services that evaluate, verify, and certify the quality, safety, reliability, performance, and regulatory compliance of industrial products, manufacturing processes, equipment, facilities, and management systems. These services help manufacturers, industrial operators, suppliers, and asset owners ensure adherence to applicable industry standards, technical specifications, environmental regulations, and safety requirements throughout the product and asset lifecycle.

The Industrial and Manufacturing TIC Report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House, and Outsourced), Mode of Service Delivery (On-Site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Testing | |

| Inspection | ||

| Certification | ||

| By Sourcing Type | In-house | |

| Outsourced | ||

| By Mode of Service Delivery | On-site | |

| Off-site / Laboratory | ||

| Remote / Digital | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size outlook for the industrial and manufacturing TIC market?

The industrial and manufacturing TIC market reached USD 20.52 billion in 2025, is estimated at USD 21.77 billion in 2026, and is forecast to reach USD 29.29 billion by 2031 at a 6.11% CAGR.

Which service type leads revenue in industrial and manufacturing TIC?

Testing led the industrial and manufacturing TIC market in 2025 with a 60.81% share because it remains essential across materials qualification, process validation, and final product compliance.

Which segment is growing the fastest in industrial and manufacturing TIC services?

Certification is the fastest-growing service type with a 6.25% CAGR through 2031, supported by sustainability rules, digital product passport needs, and AI-related conformity requirements.

Why is outsourcing gaining ground in this field?

Outsourced services held 60.32% of the market in 2025 and are projected to grow at a 7.01% CAGR because many manufacturers cannot sustain multi-domain accredited capabilities in-house.

Which region offers the strongest growth opportunity through 2031?

Asia-Pacific is both the largest region, with a 45.63% share in 2025, and the fastest-growing one, with a 6.94% CAGR through 2031, supported by stricter standards and expanding manufacturing output.

How are digital technologies changing TIC delivery models?

Remote and digital delivery is projected to grow at a 6.66% CAGR as connected sensors, drones, and cloud platforms extend inspection reach, even though on-site work still leads with a 52.44% share in 2025.

Page last updated on: