Poultry Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.86 Billion |

| Market Size (2031) | USD 28.44 Billion |

| Growth Rate (2026 - 2031) | 8.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

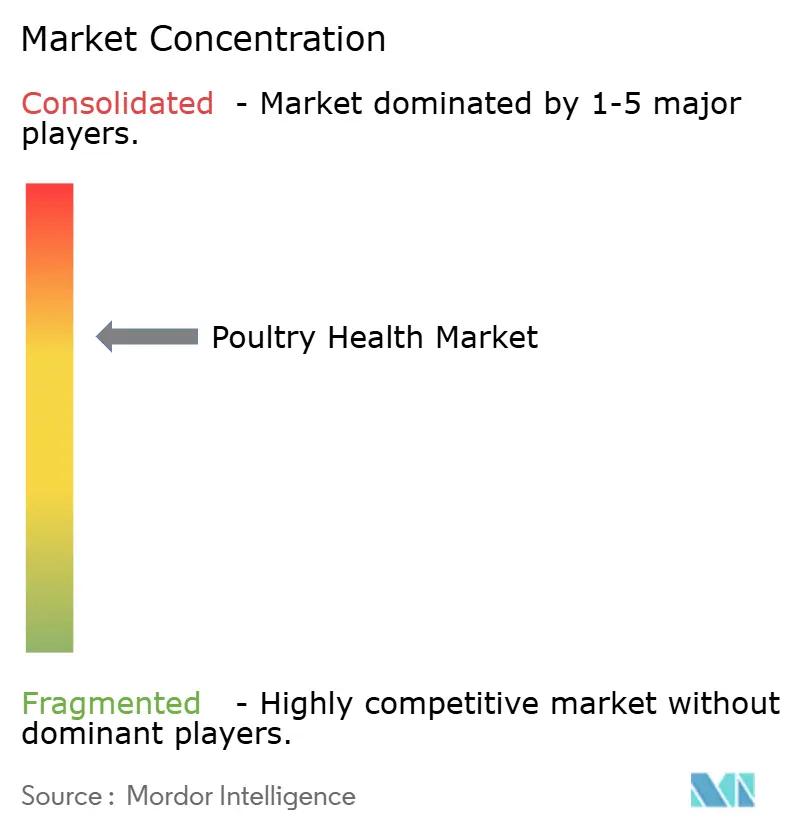

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Poultry Health Market Analysis by ���ϲ�����

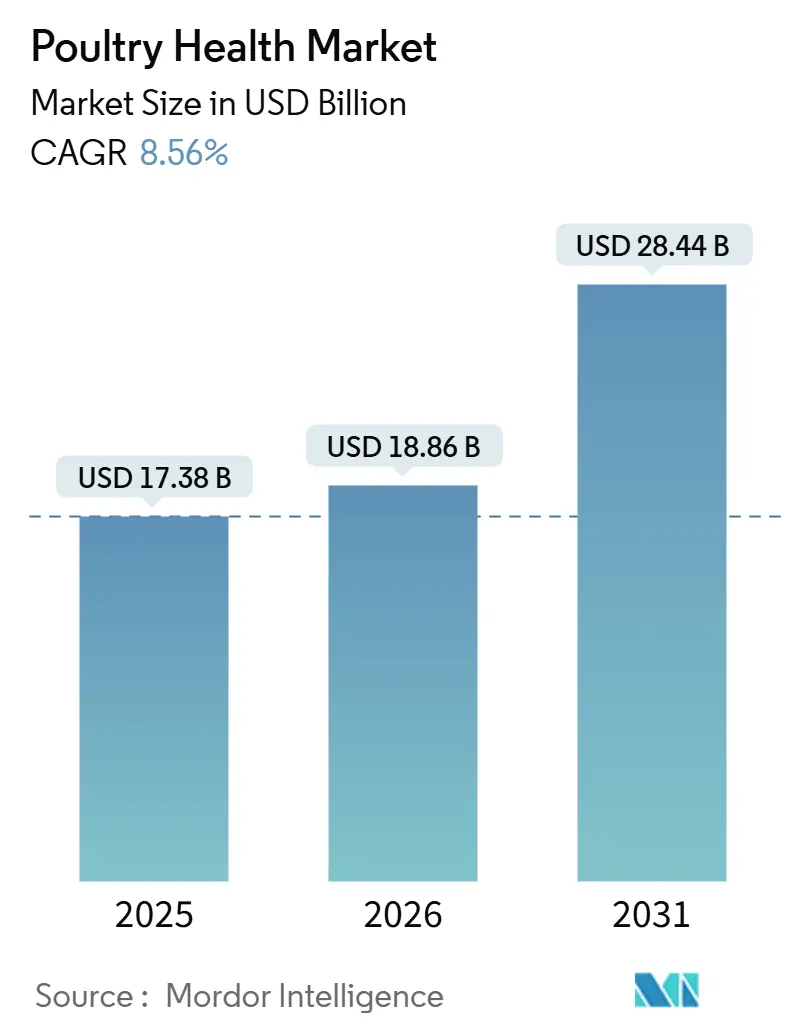

The Poultry Health Market size was valued at USD 17.38 billion in 2025 and is estimated to grow from USD 18.86 billion in 2026 to reach USD 28.44 billion by 2031, at a CAGR of 8.56% during the forecast period (2026-2031).

Demand accelerators include intensifying broiler production in Asia-Pacific, rising consumer preference for antibiotic-free chicken, and government-backed vaccination initiatives. Conditional regulatory approvals for avian-influenza vaccines in the United States and expanded cell-culture manufacturing capacity are shortening response times to future outbreaks [1]United States Department of Agriculture, “USDA Invests $1 Billion in Avian Influenza Vaccine Manufacturing,” usda.gov. Integrators are recalibrating away from curative drugs toward microbiome-driven prevention, which is lifting probiotic uptake even as vaccines remain the highest-value product class. Counterfeit biologics, raw-material bottlenecks, and integrator consolidation continue to pressure margins, yet sustained capital inflows into digital diagnostics and vector-vaccine platforms signal confidence in long-term value creation.

Key Report Takeaways

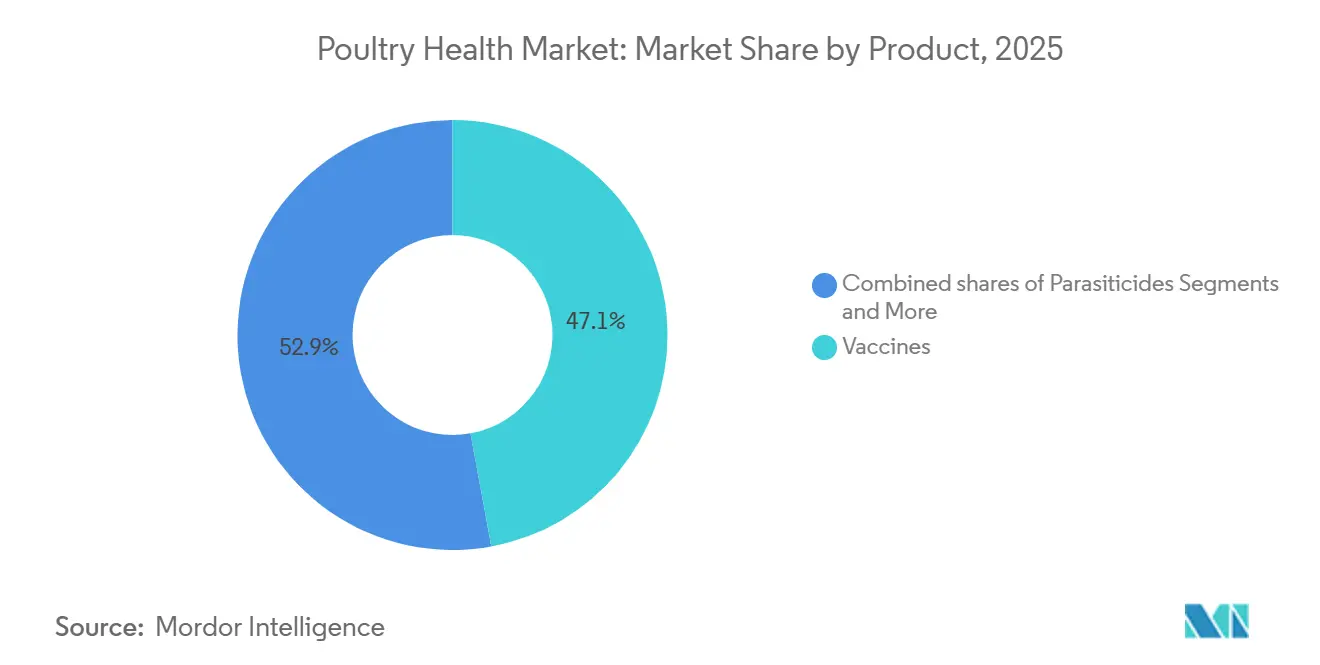

- By product type, vaccines led with 47.12% of the poultry health market share in 2025, while probiotics and prebiotics are advancing at an 8.79% CAGR to 2031.

- By animal type, broilers accounted for 63.34% share of the poultry health market size in 2025, whereas breeders are projected to expand at 8.9% CAGR between 2026 and 2031.

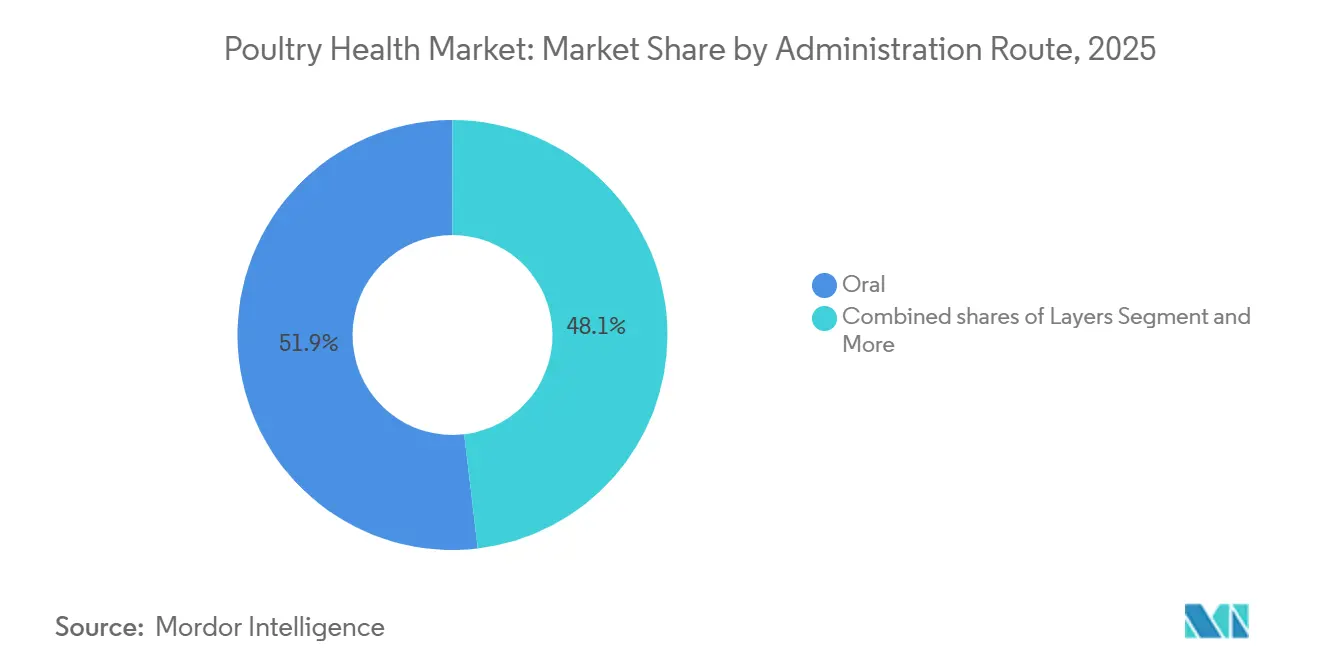

- By administration route, oral delivery captured 51.87% of 2025 revenue, and spray/aerosol is expanding at a 9.12% CAGR through 2031.

- By disease type, viral products dominated with 39.12% revenue share in 2025, yet bacterial-disease vaccines are growing at 9.67% CAGR to 2031.

- By end users, commercial poultry led with 75% of the poultry health market share in 2025, while veterinary clinics are advancing at an 9.56% CAGR to 2031.

- By geography, North America retained 39.76% revenue share in 2025, and Asia-Pacific is forecast to post a 9.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Poultry Health Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid intensification of commercial broiler production in emerging economies | +1.8% | APAC core (China, India, Vietnam), spill-over to MEA & South America | Medium term (2-4 years) |

| Expansion of government-subsidized poultry vaccination programs | +1.5% | APAC, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Growth in demand for antibiotic-free “No-ABF” value chains | +1.3% | North America & EU | Short term (≤ 2 years) |

| Acceleration of digital flock-health monitoring platforms | +0.9% | Global, led by North America & Europe | Medium term (2-4 years) |

| Development of next-gen vector vaccines targeting multiple serotypes | +0.7% | North America & EU | Long term (≥ 4 years) |

| ESG-driven retail sourcing mandates for animal-welfare certification | +0.6% | North America & EU | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rapid Intensification of Commercial Broiler Production in Emerging Economies

China processed 7.6 billion broilers in 2024, and India turned out 5.3 billion birds across the 2024-2025 cycle, compressing grow-out times and heightening pathogen pressure [2]Food and Agriculture Organization of the United Nations, “Poultry Production Statistics 2024,” fao.org. Higher stocking densities are pushing integrators toward multivalent vaccines and diagnostics that detect respiratory and enteric infections early. Brazil’s 6.9 billion chicken slaughter in 2024 required biosecure upgrades to retain market access to influenza-free importers. Argentina’s 12% capacity hike between 2023 and 2025 strained veterinary networks, exposing coverage gaps that spurred demand for turnkey immunization contracts. Vietnam and Thailand are pivoting to environmentally controlled houses, trimming mortality yet amplifying the economic cost of any outbreak, which reinforces spending on preventive biologics.

Expansion of Government-Subsidized Poultry Vaccination Programs

India’s National Animal Disease Control Programme earmarked USD 450 million in 2024 to underwrite avian-influenza and Newcastle-disease vaccines for backyard and semi-commercial flocks. Indonesia followed in 2025 with 200 million Newcastle-disease doses distributed through new cold-chain hubs. The Philippines partnered with Ceva Santé Animale to locate regional freezers that ensure potency in hot climates. African Union pilots with thermostable formulations are cutting reliance on electricity-intensive refrigeration. Subsidies are enlarging the addressable base for manufacturers and embedding routine immunization into national veterinary codes.

Growth in Demand for Antibiotic-Free “No-ABF” Value Chains

Walmart and Costco committed to 100% Better Chicken Commitment-compliant sourcing by 2026, eliminating routine antibiotics and compelling suppliers to adopt probiotics and immune-modulating feed acids. Perdue Farms reported 95% of its 2024 volume as raised without medically important antimicrobials, attributing success to Bacillus subtilis probiotics and stricter biosecurity. European Union prohibitions on prophylactic antibiotics, enforced since 2022, have catalyzed the uptake of organic acids and yeast beta-glucans. Retail premiums of USD 0.15-0.30 per pound in the United States offset higher input costs, though producers now demand verifiable efficacy data before switching health protocols.

Acceleration of Digital Flock-Health Monitoring Platforms

Tyson Foods’ 2024 IoT pilot installed acoustic sensors that identified respiratory issues 48 hours ahead of visual inspection, lowering antibiotic use by 18% and lifting average daily gain [3]Tyson Foods, “Digital Health Monitoring Initiative,” tysonfoods.com. Cobb-Vantress embedded wearable trackers in breeder houses in 2025, optimizing vaccination schedules from continuous behavioral analytics. European players employ computer vision to grade gait, preventing welfare non-compliance fines tied to lameness. Blockchain traceability demanded by Middle Eastern importers since 2025 mandates timestamped vaccination and treatment logs, further embedding digital dashboards into export supply chains.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply shortages of critical antigens for avian-influenza vaccines | -0.7% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Escalating counterfeit biologics trade in South-East Asia | -0.5% | APAC (Vietnam, Indonesia, Thailand, Philippines) | Medium term (2-4 years) |

| Regulatory delays for novel feed-additive approvals in the EU | -0.4% | EU and referencing markets | Long term (≥ 4 years) |

| Consolidation of integrators squeezing vendor margins | -0.5% | Global, led by North America & Brazil | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Supply Shortages of Critical Antigens for Avian-Influenza Vaccines

The 2024-2025 H5N1 episode forced depopulation of 168.62 million U.S. birds by April 2025, yet antigen capacity lagged because egg-based plants need 18 months to scale. A USD 1 billion USDA program launched in February 2025 is funding cell-culture lines that ramp in six months, though full output will not materialize until late 2027. Europe diverted limited doses from Brazil and India during its 2024 outbreak, underscoring trans-regional interdependence. Competition with human pandemic-influenza vaccines for the same substrates exacerbates scarcity, forcing producers into costly culling and shrinking downstream health-product consumption.

Escalating Counterfeit Biologics Trade in South-East Asia

The Philippine Bureau of Animal Industry seized 120,000 fake Newcastle-disease doses in 2024 bearing forged batch labels. Ineffective vaccines fuel outbreaks that trigger trade embargoes, eroding producer trust and driving them back to broad-spectrum antibiotics. Manufacturers are adding blockchain-verified serial numbers; Zoetis deployed the system in Thailand in 2025. Yet enforcement remains patchy, and fabricated volumes distort market-demand modeling, complicating legitimate capacity planning.

Segment Analysis

By Product Type: Probiotics Lead Growth Amid Antibiotic Restrictions

Vaccines retained a 47.12% lion’s share in 2025, anchored by compulsory Newcastle disease, infectious bronchitis, and avian-influenza immunizations. Probiotics and prebiotics are charting an 8.79% annual rise to 2031 as large retailers demand antibiotic-free birds and peer-reviewed trials show Bacillus strains cutting Salmonella counts by up to 60%. Anti-infectives are losing ground where regulators curb medically important molecules, while parasiticides sustain volume through shuttle programs that rotate ionophores with vaccines. Diagnostics is a bright spot; IDEXX’s two-hour multiplex PCR for H5, H7, and H9 is gaining traction among integrators seeking rapid flock segregation. The poultry health market size for probiotics is set to eclipse USD 4 billion by 2031 if current conversion rates persist.

Second-order effects center on fermentation expertise and field-trial validation: suppliers that can provide strain-specific data in commercial settings are capturing distribution slots once held by generic antibiotic vendors. Cross-licensing between feed-additive firms and vaccine majors is emerging as a route to bundle gut-health solutions with immunization protocols, smoothing procurement for integrators.

Note: Segment shares of all individual segments available upon report purchase

By Animal Type: Breeder Health Investments Yield Downstream Returns

Broilers delivered 63.34% revenue in 2025, reflecting annual placements exceeding 100 billion birds worldwide. Layers follow, but breeders, although fewer in headcount, are racing ahead at an 8.9% CAGR to 2031. Integrators recognize that every 1-point uptick in hatchability lifts downstream broiler volume by millions of chicks, justifying premium vaccination schedules covering Mycoplasma, ILT, and egg-drop syndrome. The poultry health market share for breeders will likely register a significant growth rate by 2031 as health budgets move upstream.

Breeder sensitivity to reproductive pathogens was highlighted when a 2024 United States metapneumovirus flare cut hatch rates 15%, costing USD 80 million in lost chicks. The fallout prompted rapid uptake of live-attenuated breeder vaccines and reinforced biosecurity audits at grandparent farms. Integrators now view breeder health as a profit-center rather than a cost line item, directing R&D toward longer-lasting, combined antigens that minimize handlings.

By Administration Route: Spray Automation Reshapes Hatchery Economics

Oral delivery remained dominant at 51.87% in 2025, yet automated spray vaccination is growing 9.12% annually as hatcheries install cabinets that immunize day-old chicks against Newcastle disease and bronchitis in under 10 seconds. In-ovo systems, counted within spray, are standard for Marek’s and coccidiosis in the United States, capturing more than 60% of hatchery volume.

Labor economics underpin the shift: a single operator with a spray cabinet can vaccinate 30,000 chicks an hour versus 3,000 by hand. Uniform coverage cuts titration failures and boosts immunity, making capex attractive for large hatcheries. Regulators are aligning; EMA guidelines issued in 2024 permit spray for certain live vaccines that were once injection-only, accelerating European adoption.

Note: Segment shares of all individual segments available upon report purchase

By Disease Type: Bacterial Vaccines Gain as Antibiotics Retreat

Viral formulations held 39.12% demand in 2025, driven by Newcastle and avian-influenza mandates. However, bacterial vaccines are sprinting ahead at 9.67% CAGR, led by autogenous Salmonella, E. coli, and Clostridium perfringens preparations. The U.S. Center for Veterinary Biologics trimmed autogenous approval times to six months in 2024, spurring regional labs to scale custom manufacturing.

Cost comparisons now favor prevention: European farms saw a notable surge in autogenous uptake after the 2022 prophylactic-antibiotic ban. This pivot is expected to lift the poultry health market size for bacterial vaccines by 2031. Parasitic and fungal segments remain niche yet present a margin upside in free-range and humid climates, respectively.

By End Users: Commercial Integrators Consolidate Purchasing

Commercial poultry operations held 75% of the poultry health market share in 2025, a lead grounded in large integrators such as Tyson Foods and Pilgrim's Pride that purchase directly from manufacturers, capturing 15-25% volume discounts and first call on limited vaccine supplies. Their dominance is expected to level off as integrators build in-house veterinary teams and, in Tyson’s case, open autogenous-vaccine plants that reduce dependence on external suppliers.

Veterinary clinics are expanding at a 9.56% CAGR through 2031, fueled by mid-sized farms in India, Brazil, and Southeast Asia that now need diagnostic testing, prescription products, and on-farm consulting not available through generic wholesalers. Backyard farmers still depend on publicly funded campaigns; India’s National Animal Disease Control Programme moved 450 million vaccine doses through local clinics in 2024, yet field audits show notable loss in potency where refrigeration is unreliable.

Geography Analysis

North America accounted for 39.76% revenue in 2025, supported by the United States’ 9 billion broiler flock and Canada’s export-oriented processors. FDA’s conditional clearance of Zoetis’ H5N1 vaccine in February 2025 lets producers vaccinate rather than depopulate, with potential savings of USD 500 million annually if endemic status emerges. High feed costs and labor scarcity temper the adoption of premium biologics, steering buyers toward solutions with tight payback metrics.

Asia-Pacific is the fastest-advancing region at 9.34% CAGR to 2031, powered by China’s 7.6 billion broiler output and India’s government-funded vaccination initiatives. Indonesia’s 200 million-dose campaign and Vietnam’s transition to commercialized barns are enlarging the poultry health market. Counterfeit threats persist, prompting firms to embed blockchain labels, yet regional scale outweighs compliance complexity.

Europe, the Middle East & Africa, and South America jointly supply the balance of global receipts. European regulation banning prophylactic antibiotics has accelerated probiotic penetration and autogenous vaccine filings, which rose significantly between 2022-2025. Brazil’s 6.9 billion-bird slaughter volume underpins vaccination spend to satisfy influenza-free importers. Argentine peso devaluation spurred a capacity hike but uncovered veterinary bottlenecks. Water-scarce GCC states import most poultry yet are investing in biosecure indoor farms, opening niches for high-efficacy vaccines that qualify under Halal ingredient audits.

Competitive Landscape

Zoetis, Merck Animal Health, Ceva Santé Animale, Boehringer Ingelheim, and Elanco captured a majority of global revenue in 2025. Zoetis commissioned a USD 389 million Suzhou biologics site in 2024 capable of 2 billion doses annually, underscoring China’s centrality to the poultry health market. Ceva’s Transmune vector platform won EMA approval in 2024, delivering multi-antigen protection in one spray, a labor-saving edge.

Smaller firms are carving diagnostics and data niches: IDEXX’s two-hour RealPCR commands premium pricing among integrators that value rapid isolation. Boehringer’s VAXXON machine-learning engine tailors antigen mixes to local epidemiology, shrinking formulation timelines to six months and offering a service moat. Merck Animal Health’s 12 patents on thermostable adjuvants and mucosal delivery aim at tropical markets deprived of a cold chain.

Integrator consolidation exerts price pressure: Tyson Foods and Pilgrim’s Pride process a significant share of U.S. broiler volume, leveraging volume to negotiate multi-year supply contracts. Vendors lacking proprietary platforms risk margin compression unless they bundle digital services or co-develop welfare-certified protocols that retailers now require.

Poultry Health Industry Leaders

Boehringer Ingelheim GmbH

Ceva Santé Animale

IDEXX Laboratories, Inc.

Zoetis Inc.

Elanco Animal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Boehringer Ingelheim rolled out a single-dose trivalent vaccine in India covering Bursa, Newcastle, and Marek’s disease, enabling hatchery-level administration.

- February 2025: Zoetis received a USDA conditional license for its H5N2 killed-virus avian-influenza vaccine labeled for chickens.

Global Poultry Health Market Report Scope

As per the scope of the report, poultry animals are domesticated birds, including ducks, chickens, turkeys, geese, quails, and other birds kept by humans. The poultry industry is one of the fastest-growing segments of livestock animals. The scope of the report emphasizes the importance of poultry animal care, for which the veterinarian is the pivotal link for the companies for the continual improvements in poultry animal health and welfare.

The poultry health market is segmented by products, animal type, administration route, disease type, end user, and geography. By product, the market is segmented into vaccines, parasiticides, anti-infectives, probiotics & prebiotics, diagnostics kits & reagents. By animal type, the market is segmented into broilers, layers, breeders, and others. By administration route, the market is segmented into oral, parenteral, topical, and spray/aerosol. By disease type, the market is segmented into viral diseases, bacterial diseases, parasitic diseases, and fungal diseases. By end users, the market is segmented into commercial poultry, backyard poultry, and veterinary clinics.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Vaccines |

| Parasiticides |

| Anti-infectives |

| Probiotics & Prebiotics |

| Diagnostics Kits & Reagents |

| Broilers |

| Layers |

| Breeders |

| Others |

| Oral |

| Parenteral |

| Topical |

| Spray / Aerosol |

| Viral Disease |

| Bacterial Diseases |

| Parasitic Diseases |

| Fungal Diseases |

| Commercial Poultry |

| Backyard Poultry |

| Veterinary clinic |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Vaccines | |

| Parasiticides | ||

| Anti-infectives | ||

| Probiotics & Prebiotics | ||

| Diagnostics Kits & Reagents | ||

| By Animal Type | Broilers | |

| Layers | ||

| Breeders | ||

| Others | ||

| By Administration Route | Oral | |

| Parenteral | ||

| Topical | ||

| Spray / Aerosol | ||

| By Disease Type | Viral Disease | |

| Bacterial Diseases | ||

| Parasitic Diseases | ||

| Fungal Diseases | ||

| By End Users | Commercial Poultry | |

| Backyard Poultry | ||

| Veterinary clinic | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the poultry health market in 2026 and what growth is expected?

The market is valued at USD 18.86 billion in 2026 and is forecast to reach USD 28.44 billion by 2031, rising at an 8.56% CAGR

Which product category is growing fastest?

Probiotics and prebiotics are expanding at 8.79% annually as producers phase out routine antibiotics in favor of gut-health modulation

Why are breeders a strategic growth segment?

Breeder health affects hatchability, chick quality, and downstream broiler yields, driving an 8.9% CAGR for this segment through 2031

What region will lead future growth?

Asia-Pacific posts the highest regional CAGR at 9.34% thanks to large-scale broiler expansion and government-funded vaccination programs

How is technology shaping poultry disease management?

Integrators deploy IoT sensors, AI analytics, and blockchain traceability to detect disease early, verify vaccination records, and optimize feed conversion.