Poultry Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

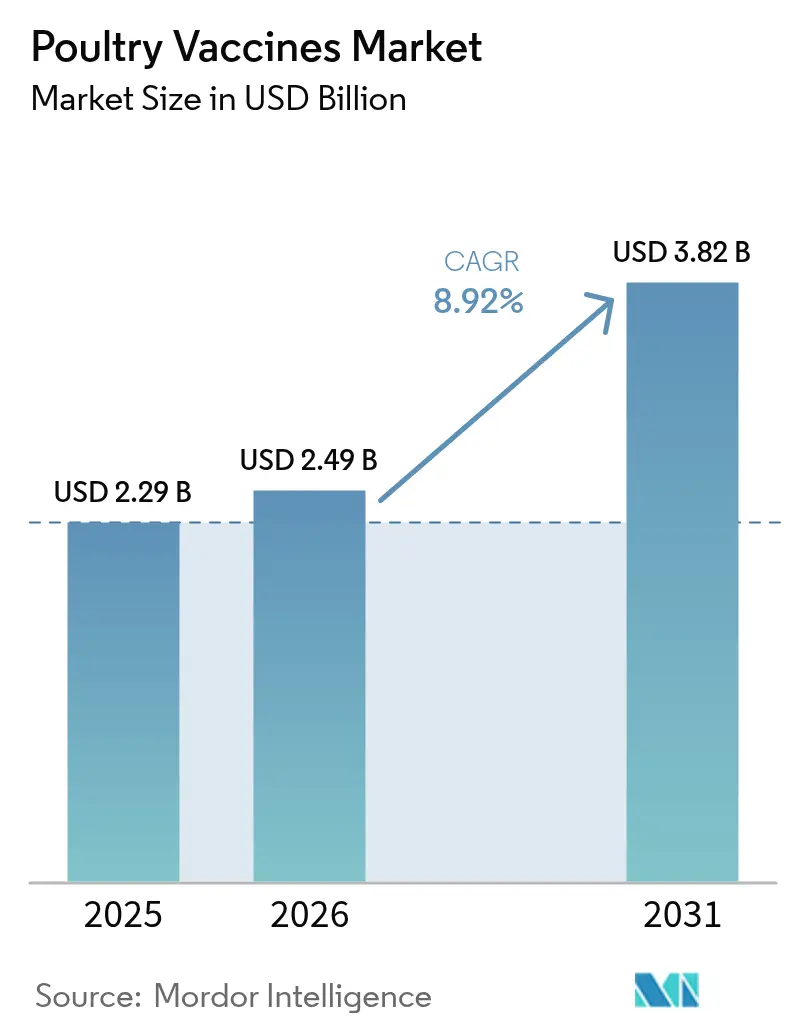

| Market Size (2026) | USD 2.49 Billion |

| Market Size (2031) | USD 3.82 Billion |

| Growth Rate (2026 - 2031) | 8.92% CAGR |

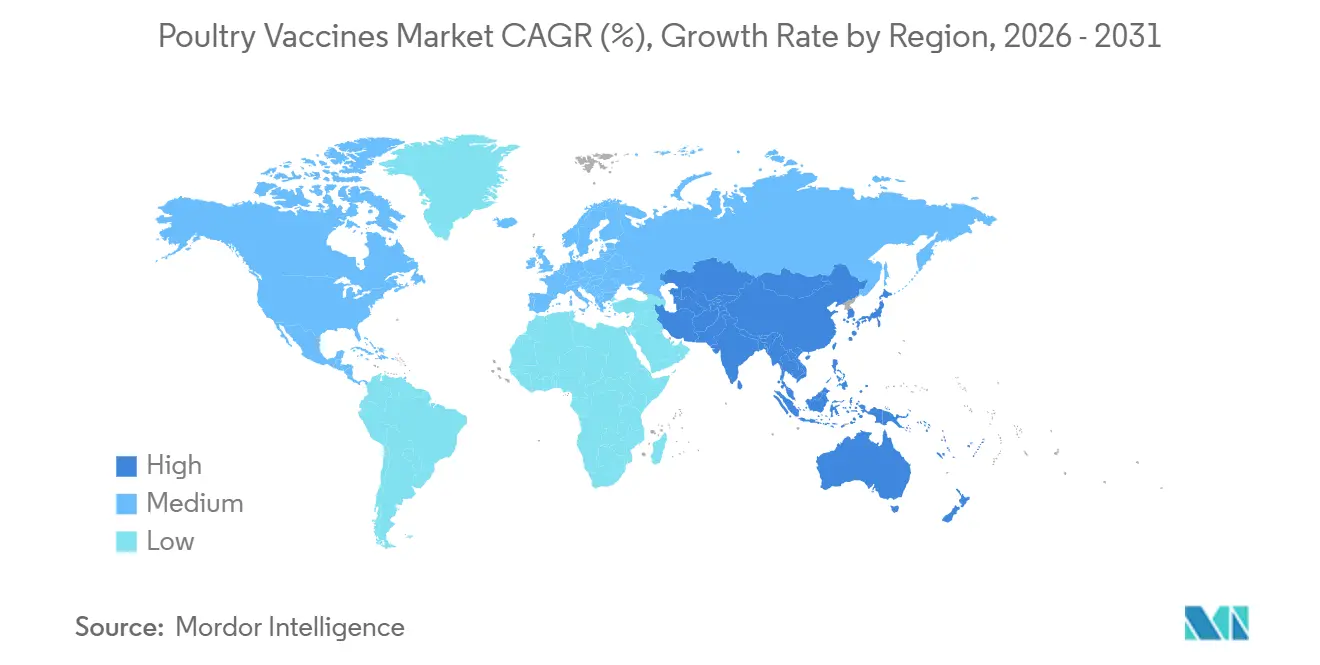

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Poultry Vaccines Market Analysis by ���ϲ�����

The Poultry Vaccines Market size is expected to grow from USD 2.29 billion in 2025 to USD 2.49 billion in 2026 and is forecast to reach USD 3.82 billion by 2031 at 8.92% CAGR over 2026-2031.

Growth rests on three pillars: tightening curbs on prophylactic antibiotics, rapid uptake of recombinant herpesvirus of turkey (HVT) constructs that bundle antigens into a single in-ovo shot, and the steady march of vertically integrated production models across Asia-Pacific. Producers are also shifting toward thermostable and lyophilized formulations that travel well in weak grid settings, while digitized ordering platforms shorten lead times and document cold-chain integrity. On the demand side, the persistent spread of H5N1 clade 2.3.4.4b and emerging infectious bronchitis variants keep vaccine pipelines full and margins resilient in a high-volume, price-sensitive business. As counterfeit doses surface in parts of Africa and Southeast Asia, regulators are rolling out serialization and QR-code verification, opening new service niches around traceability.

Key Report Takeaways

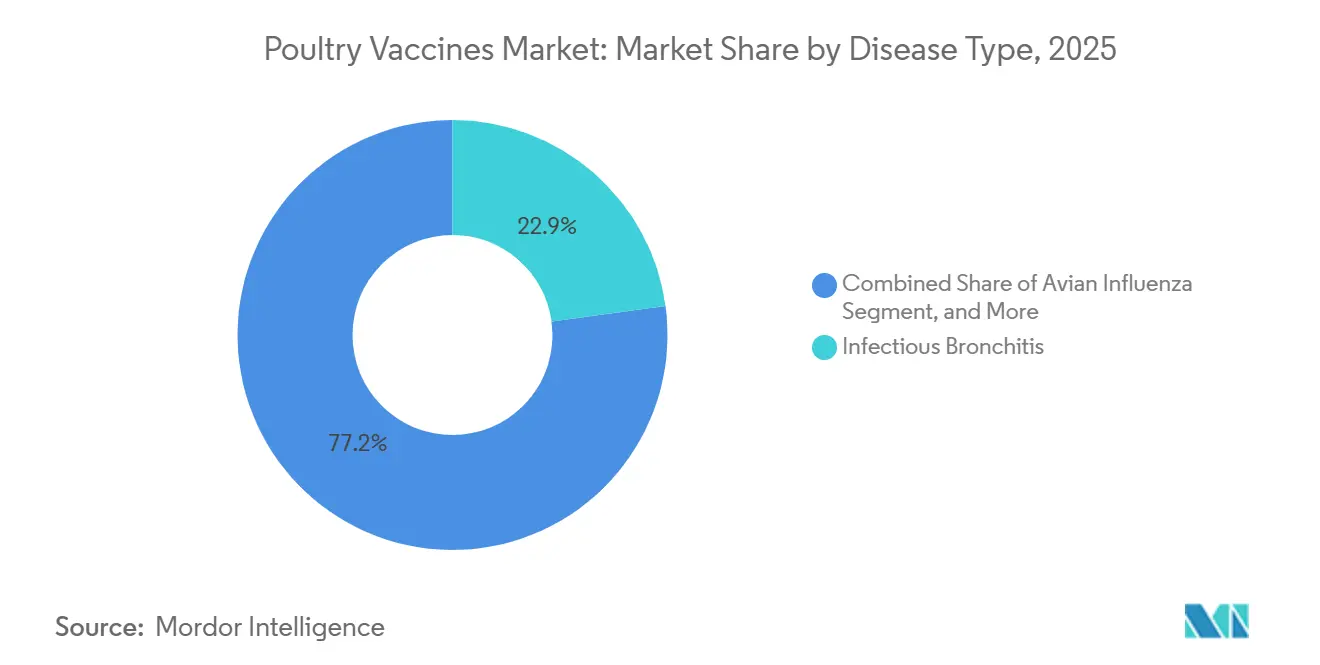

- By disease, infectious bronchitis led with 22.85% of poultry vaccine market share in 2025, while avian influenza vaccines are projected to grow at a 9.00% CAGR through 2031.

- By technology, live attenuated products held 38.40% share in 2025; recombinant and vector platforms are advancing at a 9.25% CAGR to 2031.

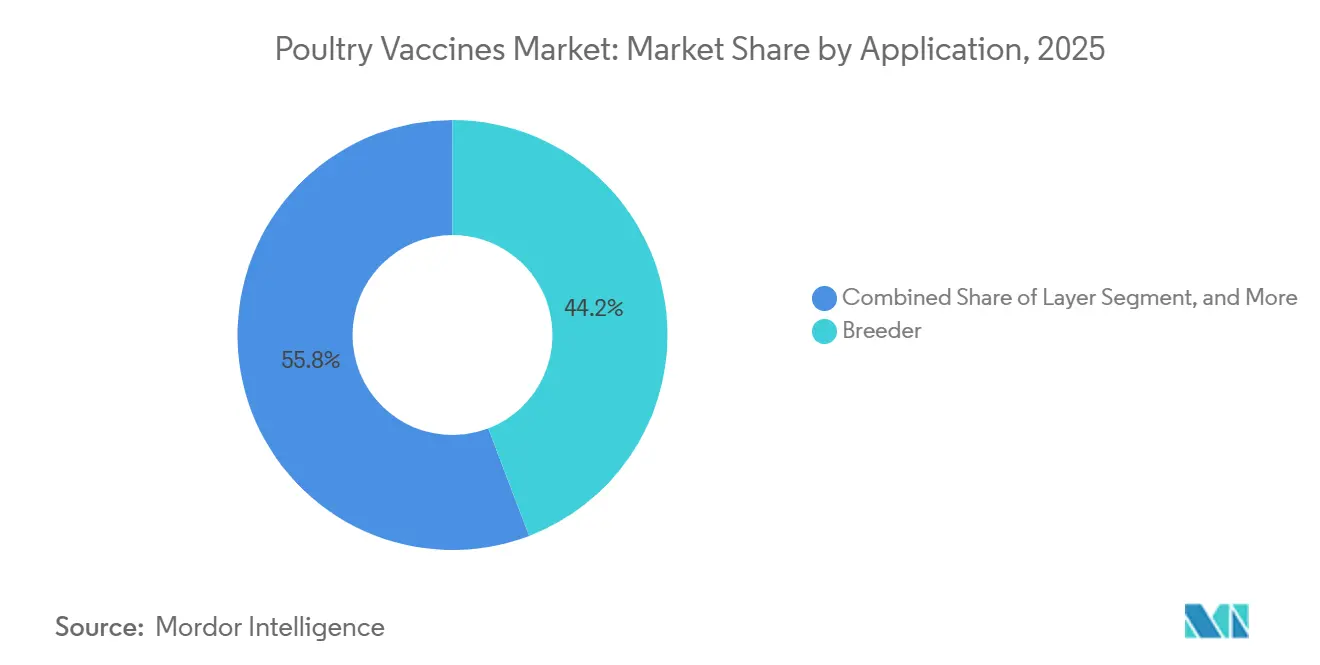

- By application, breeder-flock immunization accounted for 44.20% of 2025 revenue, whereas layer-flock programs are forecast to expand at an 8.99% CAGR over 2026-2031.

- By dosage form, liquid formulations commanded 55.46% share in 2025, yet powder and dust vaccines are expected to post a 10.78% CAGR to 2031.

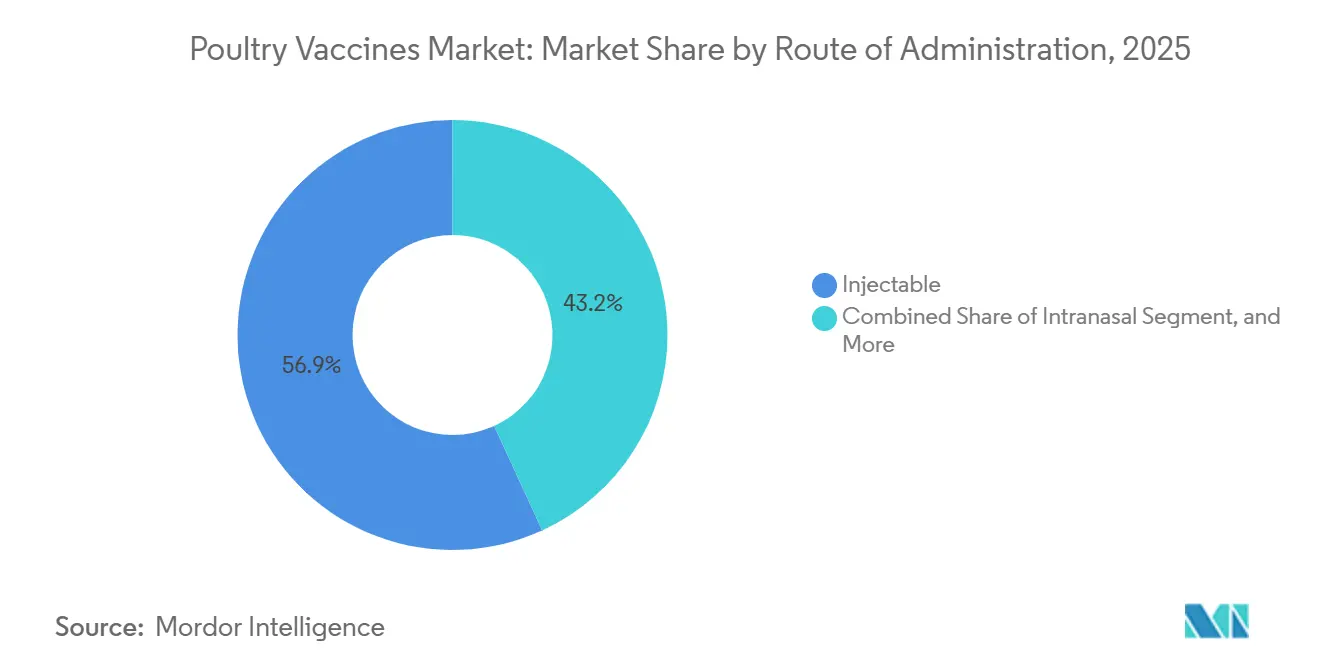

- By route of administration, injectable delivery captured 56.85% share in 2025, but intranasal administration via hatchery spray cabinets is set to climb at a 10.95% CAGR.

- By end user, poultry farms generated 67.60% of 2025 sales; veterinary clinics and hospitals are on track for a 10.22% CAGR as advisory services gain traction.

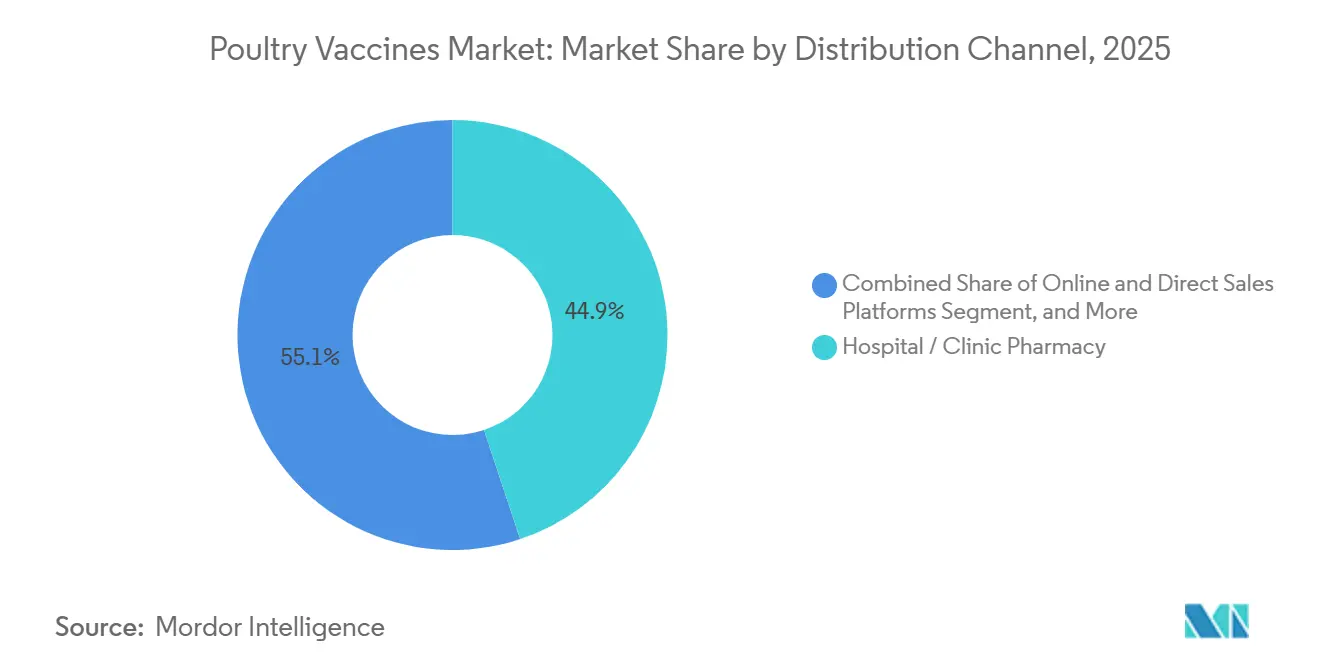

- By distribution channel, hospital pharmacies controlled 44.90% of 2025 turnover, while online and direct sales platforms are rising at an 11.90% CAGR on the back of e-procurement.

- North America held 33.50% Asia-Pacific is on an 9.48% CAGR trajectory through 2031, driven by intensifying broiler integration in ASEAN and China’s continuing shift toward preventive AI vaccination.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Poultry Vaccines Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing incidences of poultry & zoonotic diseases | +1.8% | Global, acute in Asia-Pacific & Sub-Saharan Africa | Short term (≤ 2 years) |

| Regulatory push to replace antibiotics with vaccination | +2.1% | North America, EU, spillover to Latin America | Medium term (2-4 years) |

| Rapid expansion of vertically integrated broiler operations in Asian | +1.5% | Thailand, Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Improvements in vectored & combination vaccinations | +1.3% | North America & Western Europe R&D hubs | Long term (≥ 4 years) |

| Digital procurement platforms shrinking stock-outs | +0.9% | Asia-Pacific, Middle East, Latin America | Short term (≤ 2 years) |

| GCC food-security funds accelerating breeder-flock immunization | +0.7% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Increasing Incidences of Poultry & Zoonotic Diseases

In 2024-2025, H5N1 outbreaks led to record losses in 47 countries, prompting the United States to cull over 80 million birds and Mexico, along with parts of Europe, to initiate emergency vaccination drives.[1]U.S. Food and Drug Administration, “Center for Veterinary Medicine: Antimicrobial Resistance in Veterinary Settings,” FDA, www.fda.gov Endemic Newcastle disease is causing 30%-50% mortality in backyard flocks in Indonesia, Nigeria, and Bangladesh, driving up the demand for thermostable drinking-water vaccines that circumvent cold-chain issues. Following human H5N1 cases in Cambodia and Vietnam, the World Health Organization emphasized public health measures, advocating for ring vaccinations of flocks within a 10 km radius of confirmed cases. As Marek’s disease evolves with increased virulence, producers are increasingly turning to bivalent HVT-based products. Additionally, coccidiosis continues to result in approximately USD 3 billion annually in performance losses, solidifying the role of live oocyst vaccines as a primary control method in antibiotic-free programs.

Regulatory Push to Replace Antibiotics with Vaccination

Since January 2022, the European Union has enforced a full ban on prophylactic antibiotics. This move has led to an increase in vaccine courses for clostridial and necrotic enteritis, with projections extending through 2025. In the United States, FDA Guidance 263 has not only curtailed the use of feed-grade antimicrobials but has also catalyzed a broader adoption of multivalent enteric vaccines. Meanwhile, Brazil's policy to cut colistin has driven national integrators to invest in autogenous programs targeting Salmonella and E. coli. In China, the ongoing ban on colistin has led to a 40% surge in domestic orders for inactivated doses of avian-pathogenic E. coli by 2025. This uptick is further bolstered by producers ramping up their capacity. Additionally, adherence to Codex residue limits has become a crucial requirement for exporters. This has pushed countries like Thailand, Argentina, and South Africa to intensify their focus on preventive immunization.

Rapid Expansion of Vertically Integrated Broiler Operations in ASEAN

In 2025, Thailand increased its broiler output by 12%, driven by the deployment of new hatcheries equipped with automated in-ovo units. These units administer vaccines for Marek’s, infectious bursal disease, and Newcastle disease in a single pass. Meanwhile, Indonesia attracted USD 800 million in foreign direct investment (FDI) for 2024-2025. Japanese and Korean investors have mandated hatchery immunization specifically for export lines. In Vietnam, authorities approved the establishment of eight mega-complexes in 2025. Each complex is required to have inactivated avian influenza coverage for its parent stock. The Philippines is supporting smallholder upgrade loans that include mandatory vaccinations against Newcastle disease and infectious bursal disease. Additionally, Malaysia's halal regulations have expedited the adoption of plant-based media for vaccine production.

Improvements in Vectored & Combination Vaccinations

Recombinant HVT-based multivalent platforms provide durable immunity while bypassing maternal antibody interference, a property that has prompted several producers to redesign hatchery workflow around single-shot schedules. The unspoken benefit is inventory simplification; integrators report double-digit reductions in on-farm SKU counts, indirectly improving biosecurity by reducing handling errors. Peer-reviewed trials confirm that temperature-sensitive recombinant M41-R vaccines maintain tracheal ciliary activity post challenge.[2] United States Department of Agriculture, “Highly Pathogenic Avian Influenza 2025 Response Plan,” USDA, www.usda.gov Companies are leveraging various virus vectors, such as fowl poxvirus, fowl adenovirus, Marek's disease virus, and Newcastle disease virus, for vaccine development, each withdisease challenges and reduced labor by 25% by consolidating three live-virus rounds into a single round unique benefits for targeted applications. This technological evolution is bolstering the competitive edge of firms with robust R&D in recombinant technologies, while it risks unsettling the market standing of those adhering strictly to traditional vaccine methods. Boehringer Ingelheim's Vaxxitek HVT+IBD+ND demonstrated 95% field efficacy against virulent Newcastle challenges and reduced labor by 25% by consolidating three live-virus rounds into one.

Restraint Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Counterfeit products eroding producer confidence | -0.8% | Sub-Saharan Africa, South & Southeast Asia | Short term (≤ 2 years) |

| Cold-chain expense & vaccine hesitancy among African smallholders | -0.6% | Sub-Saharan Africa, pockets in South Asia | Medium term (2-4 years) |

| Emergence of variant IBV serotypes shortening product life-cycles | -0.5% | China, Middle East, Latin America | Long term (≥ 4 years) |

| Heightened regulatory scrutiny of viral-vector vaccines in China | -0.4% | China, potential ripple in Asia-Pacific | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Counterfeit Products Eroding Producer Confidence

In 2024, the National Agency for Food and Drug Administration and Control (NAFDAC) aggressively targeted and destroyed unauthorized veterinary products, including counterfeit anthrax vaccines made of just water or sugar. These products, often found in "price-driven grey markets," were seized in states such as Kaduna, Nasarawa, and Oyo. NAFDAC emphasized the unregistered, frequently smuggled nature of these products, noting the challenges posed by porous borders. In 2024, they also confiscated significant quantities of "substandard and falsified" medicines. Meanwhile, the Kenya Veterinary Medicines Directorate (VMD) enforces stringent regulations on veterinary vaccines, such as Avian Influenza and East Coast Fever (ECF). They mandate a registration process for importers to ensure safety standards are upheld. The 15% failure rate in 2025 aligns with ongoing efforts to balance regulatory oversight between imported and locally produced vaccines, including those from the Kenya Veterinary Vaccines Production Institute (KEVEVAPI). This registry initiative is a key component of their strategic plan spanning from 2023 to 2027.

Cold-Chain Expense & Vaccine Hesitancy Among African Smallholders

In Sub-Saharan Africa, where electricity costs exceed OECD norms, maintaining doses between 2°C and 8°C adds an expense of USD 0.15-0.25 per shot. Despite receiving a 50% subsidy, surveys conducted in Uganda, Tanzania, and Mozambique revealed that only 22% of flocks were vaccinated against Newcastle disease. Farmers, having previously encountered issues with ineffective or expired vaccines, now prioritize spending their limited funds on feed or housing. While solar-powered refrigerators offer a potential solution, their high cost is a barrier. On the other hand, products derived from the thermostable I-2 strain can withstand ambient heat for up to seven days. However, they are still pending clearance due to the need for local stability dossiers.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Infectious Bronchitis Leads, Avian Influenza Surges

In 2025, vaccines for infectious bronchitis captured 22.85% of the poultry vaccine market, underscoring their importance in broiler, layer, and breeder operations. These vaccines address respiratory issues and shell-quality concerns that can impact profit margins. Meanwhile, avian influenza vaccines are projected to grow at a 9.00% compound annual growth rate (CAGR) through 2031. This surge is driven by culling costs and export bans, prompting governments in Mexico, Egypt, and Vietnam to enforce flock coverage mandates.

Newcastle disease solutions remain essential in emerging markets. Thermostable I-2 formulations facilitate mass delivery through drinking water. For Marek’s disease, day-old or in-ovo herpesvirus of turkey (HVT)-SB1 blends are employed to counteract increasing virulence. Coccidiosis vaccines are gaining traction in drug-free programs that have eliminated ionophore feed additives.

By Technology: Live Attenuated Dominates, Recombinant Platforms Accelerate

In 2025, live attenuated products held a 38.40% share of the poultry vaccine market, valued for their ability to induce strong cellular immunity and their cost-effective spray-cabinet dosing method. Recombinant vectors, particularly HVT carriers that avoid maternal-antibody interference, are on a growth trajectory with a 9.25% CAGR.

Despite their higher labor and dosage costs, inactivated vaccines play a crucial role for breeder and layer boosters, ensuring maternal antibodies are passed to chicks. Meanwhile, DNA and subunit vaccines are advancing through late-stage trials, valued for their rapid two-month antigen-update cycles that keep pace with swiftly mutating strains like H5 or GI-23.

By Application: Breeder Flocks Command Share, Layers Drive Growth

In 2025, breeder programs accounted for 44.20% of the revenue, utilizing maternal-antibody transfer to protect chicks in their crucial first three weeks. Layer flocks are anticipated to experience an 8.99% CAGR through 2031. This growth is attributed to cage-free systems extending their productive lifespan beyond 100 weeks, necessitating additional boosters.

Broiler programs are increasingly reliant on automated in-ovo injections, capable of processing up to 80,000 eggs hourly. This efficiency not only reduces labor but also enhances cost competitiveness within the 35-day cycle.

By Dosage Form: Liquid Formulations Lead, Powder Gains Traction

In 2025, liquid vaccines accounted for 55.46% of the market. Their low viscosity makes them ideal for in-ovo needles and subcutaneous applications. Powder and dust formats are projected to grow at a 10.78% CAGR. Notably, lyophilized doses can remain effective for 48 hours at ambient temperatures, a significant advantage in areas with unreliable power supply.

On-farm reconstitution of freeze-dried bricks simplifies hatchery spray routines. Additionally, while backpack aerosol powders are designed for backyard birds, there's variability in field coverage.

By Route of Administration: Injectable Dominates, Intranasal Surges

Injectables commanded a 56.85% market share in 2025, playing a crucial role for breeders and layers that require precise dosing. Intranasal sprays administered at day-old are witnessing a 10.95% CAGR. These sprays not only prevent puncture injuries but also reduce labor by 40% in hatcheries.

Automated in-ovo systems are adept at inserting antigens on embryonic day 18, seamlessly integrating transfer, candling, and dosing processes. While drinking-water and spray-house methods effectively cover broilers, they come with the risk of uneven titer gaps due to inconsistent drinking or aerosol dispersion.

By End User: Poultry Farms Dominate, Veterinary Clinics Expand

Poultry farms, encompassing integrators, contract growers, and independents, accounted for 67.60% of the 2025 market. Meanwhile, veterinary clinics and hospitals are experiencing a robust growth rate of 10.22% CAGR. This surge is largely driven by smallholders in Africa and South Asia, who are increasingly seeking comprehensive advisory visits. These visits often bundle treatments for Newcastle, infectious bursal disease, and fowl pox. While research institutes may contribute modestly to revenue, their influence is significant, shaping regulatory approvals through efficacy trials and post-market surveillance.

By Distribution Channel: Hospital Pharmacies Lead, Online Platforms Surge

In 2025, hospital pharmacies accounted for 44.90% of the market turnover. Their value lies in batch tracking and oversight by pharmacists. Online platforms are witnessing a meteoric rise, boasting an 11.90% CAGR. This growth is fueled by integrators who consolidate orders, upload Internet of Things (IoT) temperature logs, and effectively reduce stock-outs by as much as 30%. While farm-supply stores remain relevant, especially in areas with limited internet access, they are gradually losing ground. E-commerce platforms are offering broader selections and transparent pricing, making them increasingly attractive to consumers.

Geography Analysis

North America retains a 33.50% market share in 2025. USDA indemnity payouts totaling USD 1.1 billion highlight the fiscal magnitude of HPAI. Insurers have begun to model policy premiums on whether a farm participates in USDA-approved vaccination programs, effectively turning vaccines into quasi-financial instruments that influence coverage costs.

Asia is the fastest-growing region, with a 9.48% CAGR outlook for 2026-2031. China’s historic 73% avian influenza vaccination coverage has prompted local labs to develop accelerated systems for monitoring viral evolution. Those surveillance assets double as competitive intelligence, allowing regional manufacturers to iterate on vaccines ahead of global peers.

Europe, Latin America, and the Middle East each display distinct triggers for vaccine uptake, from welfare regulations to export-market access requirements. Brazil’s export-oriented producers increasingly view vaccination status as a tool to mitigate tariffs. In contrast, GCC buyers fold vaccine clauses directly into long-term feed import contracts to ensure continuity of local protein supplies.

Competitive Landscape

Major players like Zoetis, Boehringer Ingelheim, Ceva, Merck Animal Health, and Elanco dominate the poultry vaccine market, collectively accounting for about 55% of global revenues. Meanwhile, regional specialists such as Hester Biosciences, Indian Immunologicals, and Ringpu Biologicals carve out niches in price-sensitive markets, leveraging autogenous batches and on-ground field technicians. The competitive landscape is heated, particularly around patent-protected herpesvirus of turkey (HVT) vectors and the bundled in-ovo delivery hardware, both of which are crucial for hatchery operations. Notable strategic maneuvers include Zoetis securing a conditional United States license for its H5N2 killed-virus vaccine by 2025, Elanco teaming up with Medgene on a highly pathogenic avian influenza (HPAI) platform, and Ceva entering a supply agreement with breeder farms in the United Arab Emirates (UAE).

Untapped opportunities abound in developing thermostable vaccine lines for off-grid markets, creating rapid-turn deoxyribonucleic acid (DNA) vaccines tailored to emerging serotypes, and implementing blockchain serialization to combat counterfeiting. Additionally, producers are exploring plant-based media that adhere to halal standards, aiming to strengthen ties with Middle Eastern importers.

Poultry Vaccines Industry Leaders

Zoetis Inc.

Ceva Santé Animale

Boehringer Ingelheim International GmbH

Merck & Co., Inc. (Merck Animal Health / MSD)

Elanco Animal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Hester Biosciences obtained a manufacturing license for an inactivated H9N2 low-pathogenic avian-influenza vaccine for poultry.

- June 2025: Boehringer Ingelheim introduced a single-dose trivalent vaccine in India covering bursal, Newcastle, and Marek’s diseases, administered at hatchery level.

- April 2025: The USDA launched a USD 1 billion HPAI response plan, earmarking USD 100 million for vaccine innovation.

- February 2025: The USDA granted Zoetis a conditional license for an H5N2 killed-virus vaccine, opening the first US commercial channel for HPAI immunization.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the poultry vaccines market as all licensed immunological preparations sold to protect domesticated chickens, turkeys, ducks, and geese against viral, bacterial, or parasitic diseases that materially influence flock health, productivity, or trade flow. Revenues reflect ex-factory sales of commercial doses used in-ovo, spray, ocular, drinking-water, or injectable formats.

Scope Exclusion: Antibiogram test kits, feed-based coccidiostats, and unregistered autogenous blends are not considered.

Segmentation Overview

- By Disease Type

- Infectious Bronchitis

- Avian Influenza

- Newcastle Disease

- Marek's Disease

- Coccidiosis

- Egg Drop Syndrome

- Avian Encephalomyelitis

- Other Diseases

- By Technology

- Live Attenuated Vaccines

- Inactivated (Killed) Vaccines

- Recombinant / Vector Vaccines

- DNA & Sub-unit Vaccines

- Other Technologies

- By Application

- Broiler

- Layer

- Breeder

- By Dosage Form

- Liquid

- Freeze-Dried (Lyophilised)

- Powder & Dust

- By Route of Administration

- Injectable

- Intranasal

- In-Ovo

- Spray & Drinking-Water

- By End User

- Poultry Farms

- Veterinary Hospitals & Clinics

- Research Institutes

- By Distribution Channel

- Hospital / Clinic Pharmacy

- Farm Supply Stores & Cooperatives

- Online & Direct Sales Platforms

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interview vaccine technologists, integrated broiler operators, hatchery veterinarians, and regulators across North America, Europe, Asia, South America, and the Middle East. These discussions validate real-world dose prices, usage protocols, and forthcoming policy shifts, closing gaps left by public data.

Desk Research

We extract five-year trends on live-bird inventories, slaughter volumes, and outbreak alerts from open platforms such as FAOSTAT, USDA-ERS, OIE-WAHIS, Eurostat, and national veterinary bulletins. Shipment intelligence from Volza, patent counts via Questel, and manufacturer financials hosted on D&B Hoovers sharpen visibility into supply chains and innovation pace. Company 10-Ks, investor decks, International Poultry Council notes, and leading veterinary journals round out the evidence base. The sources listed are indicative; many other publications inform our analysis.

Market-Sizing & Forecasting

A top-down construct converts day-old chick placements and slaughter numbers into an annual dose pool, which is then cross-checked with selective bottom-up supplier roll-ups (average selling price multiplied by sampled volumes). Core variables, vaccination coverage %, confirmed disease incidence, average flock size, ASP progression tied to valency upgrades, and regional broiler production tonnage feed a multivariate regression model that projects demand through 2030. Country anomalies are smoothed before aggregation.

Data Validation & Update Cycle

Outputs undergo variance checks against independent price decks, trade flows, and outbreak logs, followed by senior analyst review. Models refresh every twelve months, with interim updates when notifiable disease spikes, regulatory changes, or major product launches materially shift demand.

Why Mordor's Poultry Vaccines Baseline Earns Trust

Published estimates often diverge because firms adopt different disease baskets, pricing ladders, and update cadences.

Key gap drivers include exclusion of coccidiosis biologics, sole reliance on vendor revenue splits, and frozen currency conversions, whereas Mordor's base blends epidemiological counts, rolling ASP audits, and annual refreshes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.29 B (2025) | ���ϲ����� | - |

| USD 2.54 B (2025) | Global Consultancy A | Narrower disease scope; supplier revenue roll-up only |

| USD 1.32 B (2025) | Trade Journal B | Viral vaccines only; static 2023 ASP |

| USD 2.15 B (2024) | Industry Publication C | Includes ancillary biologics; outdated flock data |

The comparison confirms that ���ϲ����� delivers the most balanced and transparent baseline, grounded in live-flock metrics, validated prices, and timely updates, giving decision-makers a dependable foundation for strategy and investment.

Key Questions Answered in the Report

How big is the poultry vaccines market?

The poultry vaccines market size is expected to reach USD 2.49 billion in 2026 and grow at a CAGR of 8.92% to reach USD 3.82 billion by 2031.

What is a common vaccine for poultry?

One common poultry vaccine is the Newcastle Disease (ND) vaccine, which is extensively utilized to safeguard against one of the most serious and economically damaging viral diseases affecting birds.

What is f1 vaccine in poultry?

The F1 vaccine for poultry is generally linked to the Newcastle Disease Virus (NDV) vaccine. This live attenuated vaccine is derived from the F strain of the Newcastle Disease virus and is commonly utilized in poultry to safeguard against Newcastle Disease, a highly contagious viral infection that impacts birds' respiratory, digestive, and nervous systems.

What are the vector vaccines for poultry?

Vector vaccines for poultry involve a harmless virus or bacterium, known as the "vector," which is genetically modified to carry genes from a specific pathogen. This allows the immune system to develop a response to the targeted disease.

Do farmers vaccinate their livestock?

Yes, farmers routinely vaccinate their livestock to safeguard against infectious diseases that could affect their health, productivity, and economic viability.

Page last updated on: