Market Overview

| Study Period | 2020 - 2031 |

|---|---|

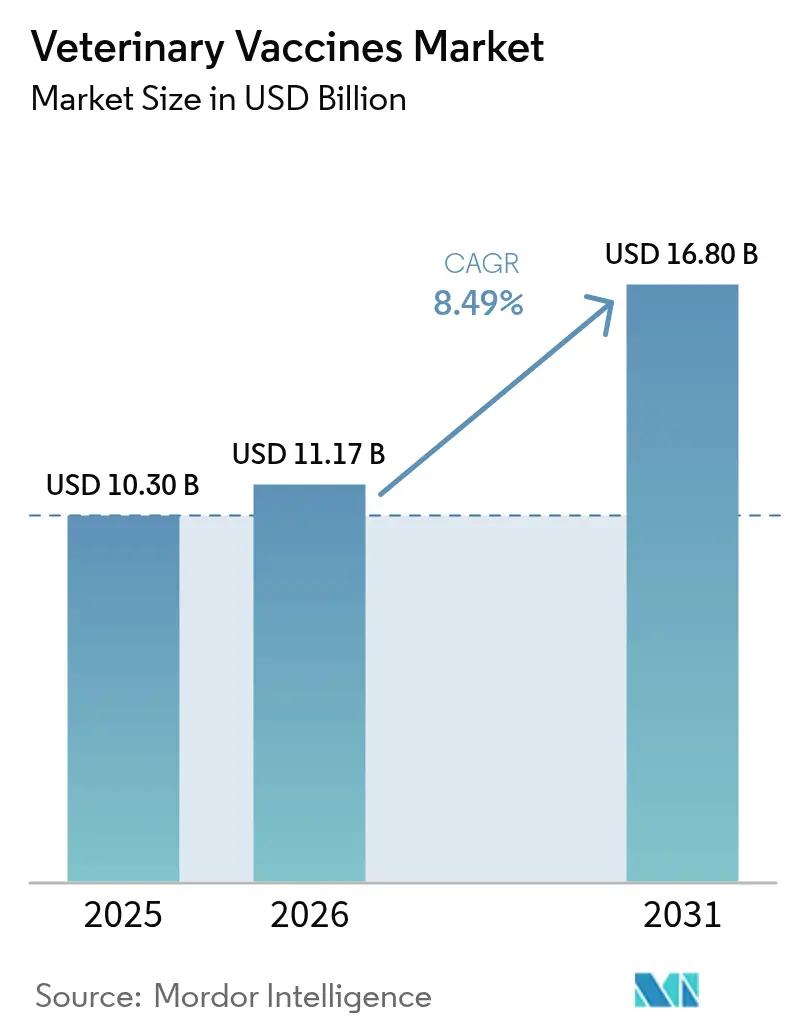

| Market Size (2026) | USD 11.17 Billion |

| Market Size (2031) | USD 16.80 Billion |

| Growth Rate (2026 - 2031) | 8.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Veterinary Vaccines Market Analysis by ���ϲ�����

The Veterinary vaccines market size was valued at USD 10.30 billion in 2025 and is estimated to grow from USD 11.17 billion in 2026 to reach USD 16.80 billion by 2031, at a CAGR of 8.49% during the forecast period (2026-2031). Heightened global awareness of antimicrobial resistance is shifting producers toward preventive immunization, while recurring waves of highly pathogenic avian influenza and African swine fever keep public agencies on permanent alert. Emergency response spending worth USD 824 million by the United States alone during 2024-2025 shows how zoonotic threats now attract budget lines once reserved for national defense. In parallel, regulatory guidance for DNA and recombinant platforms in Europe accelerates product pipelines that can be used in regions with weak cold chains[1]European Medicines Agency, “Guideline on DNA Vaccines for Veterinary Use,” ema.europa.eu . Live-animal workforce shortages temper companion-animal uptake, yet the rapid growth of e-commerce channels allows rural livestock owners to purchase vaccines without clinic visits.

Key Report Takeaways

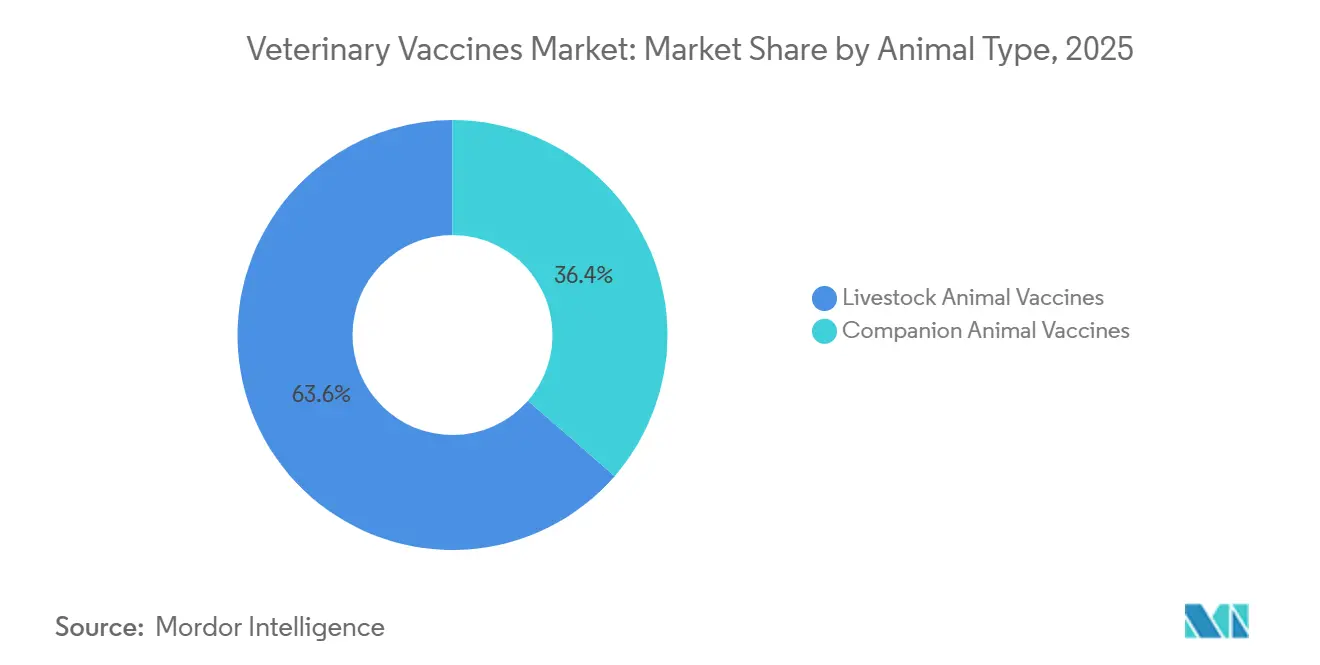

- By animal type, livestock vaccines captured 63.55% of the Veterinary vaccines market share in 2025, whereas companion-animal products expanded at a 9.85% CAGR through 2031.

- By technology, live attenuated platforms led with 50.53% revenue share in 2025, while recombinant and sub-unit candidates are projected to post a 10.75% CAGR to 2031.

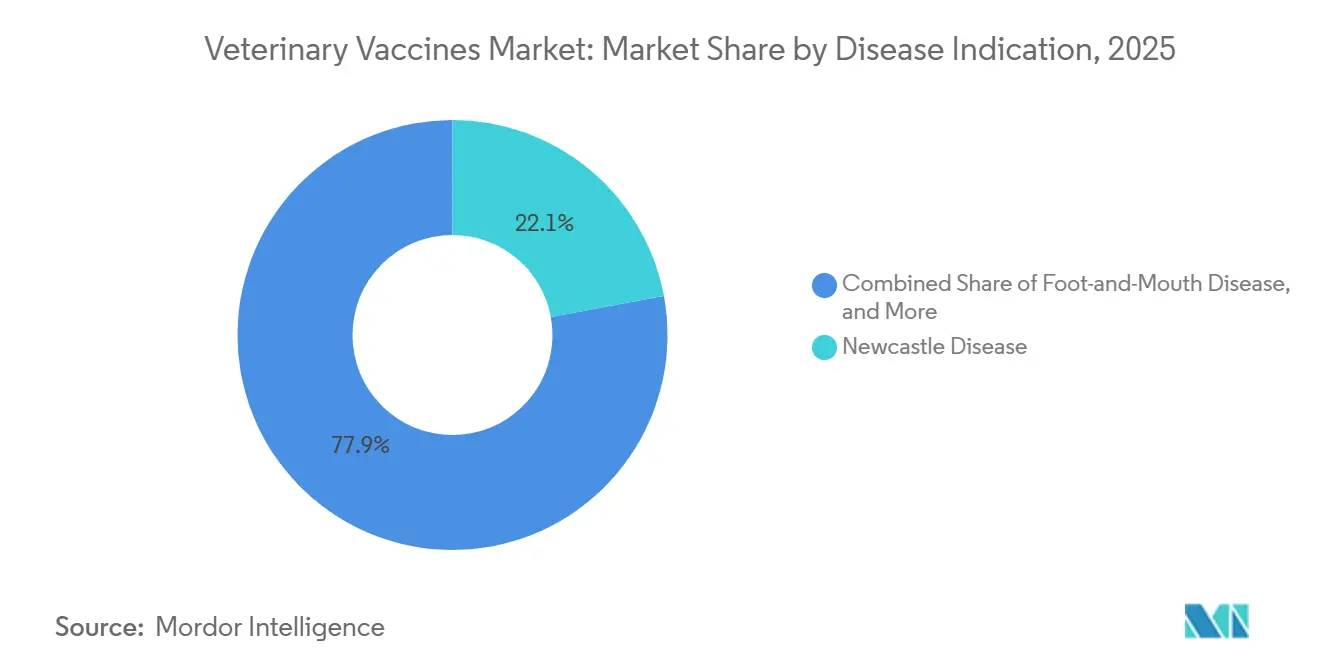

- By disease indication, Newcastle disease accounted for 22.15% in 2025, and avian influenza vaccines are set to grow at a 10.82% CAGR over 2026-2031.

- By route of administration, parenteral injection accounted for 72.52% of the market share in 2025, yet needle-free systems are expected to grow at an 11.12% CAGR through 2031.

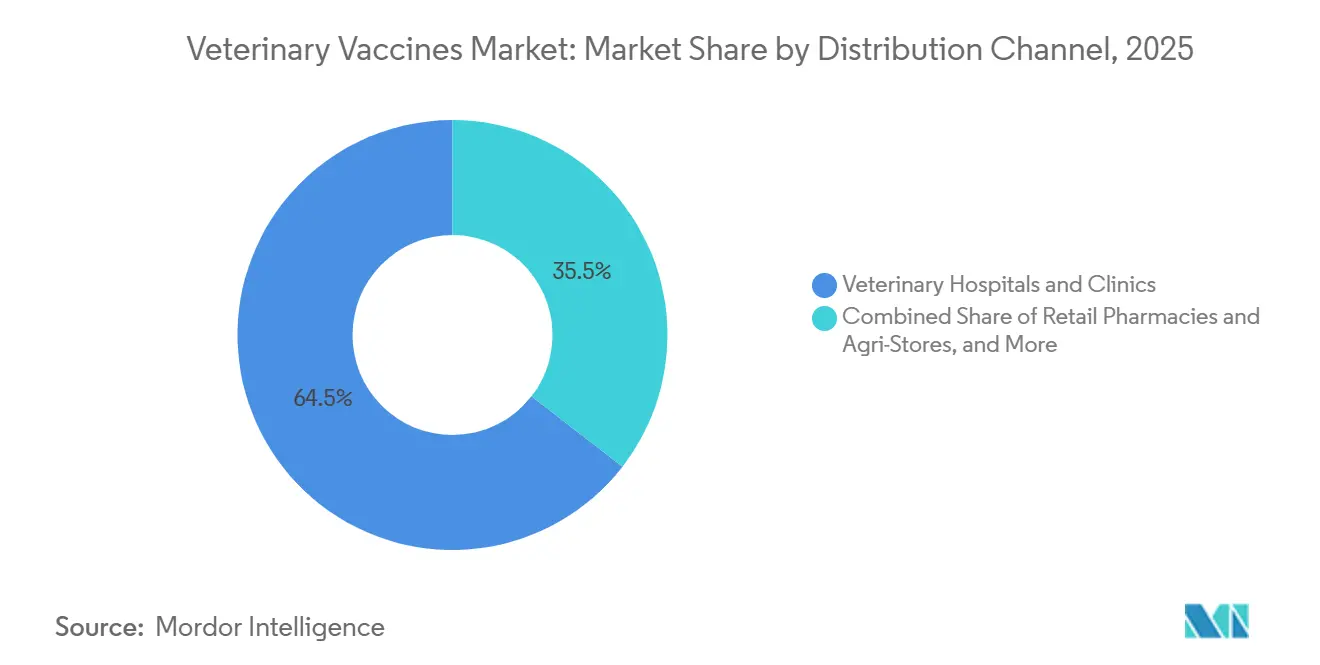

- By distribution channel, veterinary hospitals and clinics accounted for 64.54% in 2025, while online and e-commerce outlets are projected to grow at a 12.32% CAGR through 2031.

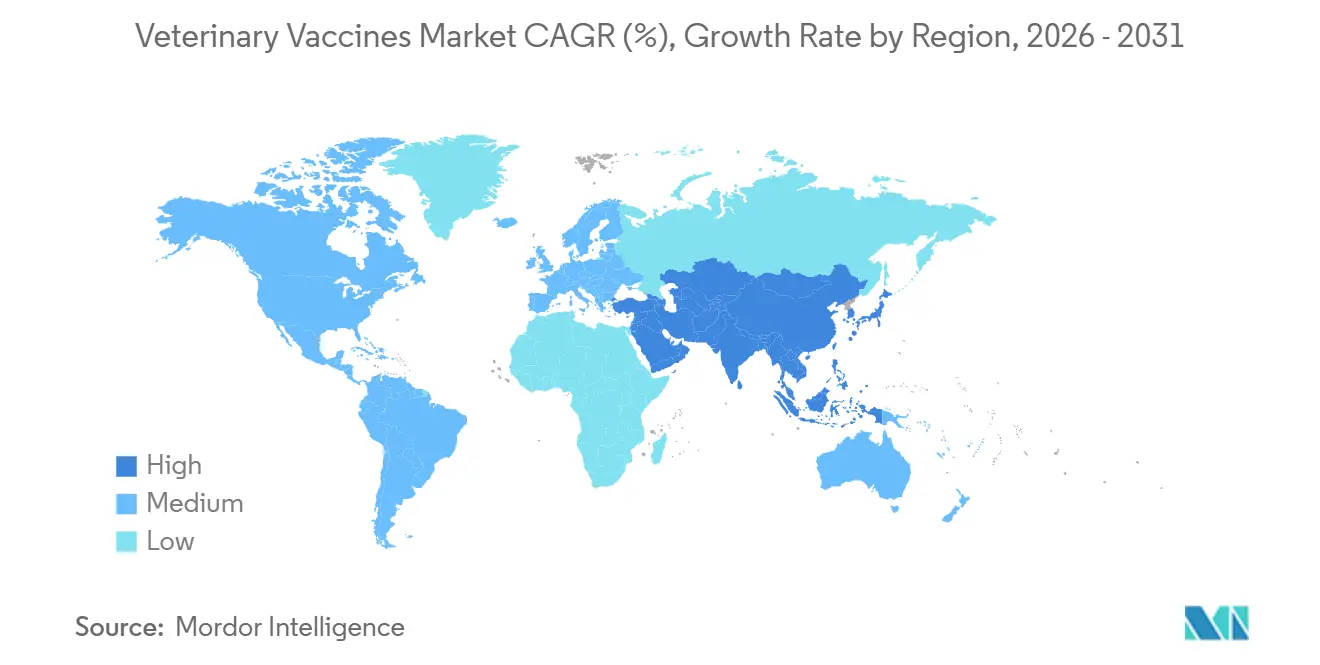

- By geography, North America dominated witha 32.62% share in 2025, whereas Asia-Pacific is forecast to record the fastest 9.72% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Transboundary Livestock Outbreaks | +2.1% | Global, with acute pressure in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Rising Companion-Animal Ownership and Spend | +1.4% | North America and Europe core, spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Government-Funded Mass-Vaccination Programs | +1.8% | Asia-Pacific, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Commercial Poultry Integration Boosting Biosecurity Demand | +1.3% | Global, led by North America and Brazil | Short term (≤ 2 years) |

| Precision-Livestock Analytics Enabling Micro-Targeted Immunization | +0.9% | North America and Europe early adopters, Asia-Pacific following | Long term (≥ 4 years) |

| Emergence of Autogenous and Thermostable Vaccines Amid AMR Curbs | +1.0% | Global, with regulatory leadership in Europe and North America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Growing Transboundary Livestock Outbreaks

Cross-border animal diseases now behave like rolling demand shocks, permanently raising baseline vaccination volumes. The World Organisation for Animal Health logged 4,782 highly pathogenic avian influenza events across 76 countries during 2024-2025, including first-ever detections in United States dairy herds that led to the cull of more than 100 million poultry[2]World Organisation for Animal Health, “Avian Influenza Situation Report 2024-2025,” woah.org. Germany confirmed its first domestic ASF case in June 2024, and the Philippines lost 15% of its swine inventory in the same period. These crises pushed the FAO and WOAH to launch a USD 500 million ASF control pathway in 2025, locking in multi-year vaccine contracts that are insensitive to price swings[3]Food and Agriculture Organization, “Progressive Control Pathway for African Swine Fever,” fao.org .

Rising Companion-Animal Ownership and Spend

United States households owned 89.7 million dogs and 73.8 million cats in 2025, yet veterinary spending declined 4% year over year as owners embraced telemedicine and online pharmacies. Many states now allow licensed practitioners to prescribe core vaccines through video consultations, enabling e-commerce platforms to dispatch rabies and distemper boosters directly to homes. However, just 57.3% of cat owners saw a veterinarian in 2025, suggesting feline coverage remains suboptimal. Manufacturers that hope to capture the 12.32% CAGR e-commerce channel must therefore invest in consumer education that explains the preventive value of timely shots.

Government-Funded Mass-Vaccination Programs

India’s Union Budget 2026 raised allocations for its Livestock Health and Disease Control scheme, which distributes free FMD and brucellosis doses to more than 500 million cattle and buffalo. The United Kingdom granted GBP 12.5 million (USD 15.8 million) to stimulate domestic vaccine research, signaling its intent to slash import reliance. In the United States, the 2024 Farm Bill earmarked USD 22.2 million for the National Animal Vaccine and Veterinary Countermeasures Bank to stockpile antigens for FMD and classical swine fever. Public orders speed procurement but expose suppliers to political budget shifts.

Commercial Poultry Integration Boosting Biosecurity Demand

United States broiler production is concentrated among fewer than 50 integrators, all of whom standardize vaccination protocols that cover billions of birds each year. Brazil exported 4.9 million metric tons of chicken meat in 2024, and export-certified flocks must receive Newcastle and infectious bursal disease shots. Demand, therefore, tracks production volume rather than disease incidence, providing predictable revenue yet increasing exposure to any single large integrator that might switch suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-Chain Gaps in Emerging Markets | -0.8% | Sub-Saharan Africa, South Asia, rural Latin America | Medium term (2-4 years) |

| Shortage of Large-Animal Veterinarians and Vaccinators | -0.6% | North America and Europe rural areas, global large-animal sectors | Long term (≥ 4 years) |

| Regulatory Bottlenecks for Novel Vector and Mrna Veterinary Vaccines | -0.5% | Global, with slower pathways in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Rising Anti-Vaccination Sentiment among Smallholders | -0.4% | Fragmented across rural communities globally | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Cold-Chain Gaps in Emerging Markets

The FAO estimates that up to 40% of livestock doses in sub-Saharan Africa lose potency before use because transport exceeds 8 °C for extended periods. Thermostable DNA formats hold promise, but national authorities often lack the capacity to evaluate stability dossiers, prolonging registration by as much as five years. Until uniform standards emerge, poor infrastructure will cap penetration in hot climates.

Shortage of Large-Animal Veterinarians and Vaccinators

Rural United States counties average 1 large-animal veterinarian per 15,000 head of cattle, limiting the pace of field vaccination. Pilot schemes that license trained laypersons have seen slow uptake due to liability concerns. Device makers see opportunity in jet injectors and microneedle patches that anyone can administer, though regulatory paths for those formats remain unclear.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Livestock Dominance Driven by Regulatory Shifts

Livestock products captured 63.55% of the Veterinary vaccines market share in 2025, and the segment is projected to grow at a 9.85% CAGR as antimicrobial resistance drives the phase-out of routine antibiotics[4]USDA Center for Veterinary Biologics, “Autogenous Biologics Licenses Issued 2024-2025,” aphis.usda.gov. Bovine programs remain buoyed by state-funded brucellosis and FMD eradication drives in India, Brazil, and several African nations. Porcine autogenous formulations, licensed on a farm-by-farm basis in the United States, let producers match viral drift faster than commercial updates. Poultry doses dominate volume terms because hatchery spray and in-ovo injection protocols deliver near-universal coverage for day-old chicks.

Companion-animal vaccines held 36.45% in 2025 but confront headwinds from longer booster intervals and telemedicine’s partial substitution for in-clinic care. Core canine rabies and distemper injections remain mandatory in most jurisdictions, anchoring a steady revenue floor, yet discretionary products such as Lyme disease boosters lose ground to antibody titre testing. Feline uptake trails canine because indoor cats are perceived as lower risk, a gap that suppliers hope to close through direct-to-consumer education.

By Technology: Recombinant Platforms Gain Share in Marker-Vaccine Strategies

Live attenuated formats owned 50.53% of revenue in 2025, reflecting decades of use in poultry and cattle. The Veterinary vaccines market for recombinant and subunit products is expected to grow rapidly, expanding at a 10.75% CAGR through 2031 as eradication campaigns demand DIVA compliance. Recombinant ASF candidates approved in Europe delete diagnostic target genes, allowing herds to prove freedom from infection and regain export access.

Inactivated doses continue to serve pregnant animals and regions wary of reversion risk, though multi-shot protocols inflate labor costs. DNA, mRNA, and VLP technologies occupy an emerging niche supported by guidelines issued in 2024, yet production expenses remain five to ten times higher than conventional lines. Wider rollout depends on manufacturing scale and streamlined approval pathways in the Asia-Pacific.

By Disease Indication: Avian Influenza Vaccines Surge Amid Zoonotic Spillover

Newcastle disease accounted for 22.15% of category revenue in 2025, driven by backyard poultry across Africa and Asia that rely on thermostable strains that require no refrigeration. Following unprecedented H5N1 transmission into United States dairy cattle, avian influenza formulations are forecast to grow at 10.82% CAGR to 2031, supported by emergency-use clearances.

PRRS remains a high-value niche for swine, costing United States producers an estimated USD 664 million each year, while rabies retains steady companion-animal demand thanks to legal mandates. FMD shots are policy-driven, with multivalent stockpiles refreshed biennially based on WOAH surveillance. The “other” category includes lumpy skin disease, which entered Europe and Asia during 2024-2025 and triggered new procurement.

By Route of Administration: Needle-Free Systems Rise in Labor-Constrained Operations

Parenteral delivery accounted for 72.52% of revenue in 2025, driven by dose accuracy and regulatory familiarity. Yet needle-free jet injectors and microneedle patches are forecast to grow at 11.12% CAGR as the livestock workforce shrinks. Swine farms appreciate reduced needle-stick injuries and no sharps waste, despite initial capital outlays.

Oral bait technology supports wildlife rabies programs and aquaculture mass immunizations, while intranasal bovine doses provide quick respiratory immunity but require frequent repeats. Spray systems remain limited to selected poultry houses because of worker exposure concerns.

By Distribution Channel: E-Commerce Disrupts Traditional Veterinary Gatekeeping

Clinics and hospitals controlled 64.54% of turnover in 2025, helped by regulations that tie prescription access to licensed veterinarians. Nonetheless, the Veterinary vaccines market now sees a strong 12.32% CAGR in online sales as several U.S. states sanction remote prescribing. Rural livestock owners, who often drive over 50 miles for veterinary care, welcome doorstep delivery.

Retail chains such as Tractor Supply recorded double-digit growth in animal health during 2024-2025, though a pending FDA rule could reclassify some over-the-counter products as prescription-only. Manufacturers must therefore invest in validated cold-chain packaging and user-friendly instructions to maintain e-commerce momentum.

Geography Analysis

North America held 32.62% of global revenue in 2025, supported by vertically integrated poultry systems that vaccinated more than 9 billion broilers during the year. Companion-animal saturation and declining clinic visits limit upside, yet emergency funding worth USD 824 million for HPAI during 2024-2025 produced a temporary spike in orders. Mexico’s expanding pork and poultry sectors promise incremental growth once cold-chain improvements roll out.

Asia-Pacific is the fastest-growing territory, registering a 9.72% CAGR to 2031. China’s hog-herd reconstruction after ASF and India’s public procurement of FMD and brucellosis vaccines underpin demand. Japan and South Korea enforce mandatory poultry vaccination to improve volume stability, while Australia and New Zealand focus on export-oriented livestock that must meet stringent health rules at destination markets.

Europe benefits from regulatory leadership, having released DNA-vaccine guidelines in 2024 and approved recombinant ASF candidates in 2025. Germany, France, and Spain dominate usage due to large animal populations, though overall herd sizes continue to shrink under environmental policy pressure. The United Kingdom’s GBP 12.5 million vaccine initiative indicates a post-Brexit drive for sovereign production.

The Middle East and Africa are catching up as FAO-backed programs subsidize doses in least-developed economies. The GCC is investing in domestic biomanufacturing, led by Saudi Arabia’s new National Center for Animal Health facility. South America grows on the back of Brazil’s poultry exports and Argentina’s fast-rising swine capacity, both of which must document vaccination for Asian buyers.

Competitive Landscape

The Veterinary vaccines market is moderately fragmented. The five largest multinationals maintain an edge through bundled diagnostics and biologics that lock in customers. Zoetis couples PRRS vaccines with PCR kits, which raises switching costs. Boehringer Ingelheim strengthened its line-up by purchasing Elanco’s United States poultry portfolio in 2024, consolidating hatchery spray systems that favor high-volume suppliers. Merck Animal Health and Ceva expand capacity through new biologics plants, ensuring buffer stock to meet sudden outbreak demand.

Regional firms carve out niches. Indian Immunologicals leverages expedited domestic approvals to underprice multinationals in public tenders, while Hester Biosciences focuses on thermostable Newcastle disease options tailored to backyard birds. European biotech startups are exploiting the EMA’s DNA-vaccine guideline to pursue niche indications, such as therapeutic oncology in pets. Despite these entrants, incumbents still hold the bulk of cold-chain assets and key opinion leader relationships that guide on-farm protocols.

White-space opportunities cluster around autogenous swine formulations, thermostable lines for hot climates and needle-free hardware that cuts labor. Success depends on navigating patchwork regulations that vary by species, pathogen and country, a complexity that tends to favor companies with dedicated regulatory affairs teams.

Veterinary Vaccines Industry Leaders

Zoetis Inc.

Merck & Co. Inc.

Virbac

Boehringer Ingelheim International GmbH

Elanco Animal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Elanco Animal Health received USDA approval for TruCan Ultra B, the first orally delivered Bordetella bronchiseptica vaccine for dogs.

- November 2025: Zoetis launched Vanguard Recombishield, a new injectable Bordetella bronchiseptica vaccine for canine respiratory protection in the United States.

Global Veterinary Vaccines Market Report Scope

As per the scope of the report, veterinary vaccines are biological preparations designed to stimulate protective immunity in animals against infectious diseases. They help prevent, control, or reduce the severity of viral, bacterial, and parasitic infections across livestock and companion species. By enhancing herd immunity and reducing pathogen transmission, veterinary vaccines support animal health, food safety, and productivity.

The veterinary vaccines market segmentation includes animal type, technology, disease indication, route of administration, distribution channel, and geography. By animal type, the market is segmented into livestock animal vaccines (bovine, porcine, poultry, and other livestock) and companion animal vaccines (canine, feline, and equine). By technology, the market is segmented into live attenuated, inactivated/killed, toxoid, recombinant/subunit, and other technologies. By disease indication, the market is segmented into foot-and-mouth disease, Newcastle disease, porcine reproductive & respiratory syndrome, rabies, brucellosis, avian influenza, canine parvovirus, and other indications. By route of administration, the market is segmented into parenteral, oral, intranasal, transdermal / needle-free, and others. By distribution channel, the market is segmented into veterinary hospitals & clinics, retail pharmacies & agri-stores, and online / e-commerce. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers the value (USD) for the above segments.

By Animal Type

| Livestock Animal Vaccines | Bovine |

| Porcine | |

| Poultry | |

| Other Livestock (Small Ruminants, Aquaculture, etc.) | |

| Companion Animal Vaccines | Canine |

| Feline | |

| Equine |

By Technology

| Live Attenuated |

| Inactivated / Killed |

| Toxoid |

| Recombinant / Sub-unit |

| Other Technologies (DNA, mRNA, VLP, etc.) |

By Disease Indication

| Foot-and-Mouth Disease (FMD) |

| Newcastle Disease |

| Porcine Reproductive & Respiratory Syndrome (PRRS) |

| Rabies |

| Brucellosis |

| Avian Influenza |

| Canine Parvovirus |

| Other Indications |

By Route of Administration

| Parenteral (Injection) |

| Oral |

| Intranasal |

| Transdermal / Needle-free |

| Other Routes |

By Distribution Channel

| Veterinary Hospitals & Clinics |

| Retail Pharmacies & Agri-Stores |

| Online / e-Commerce |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Animal Type | Livestock Animal Vaccines | Bovine |

| Porcine | ||

| Poultry | ||

| Other Livestock (Small Ruminants, Aquaculture, etc.) | ||

| Companion Animal Vaccines | Canine | |

| Feline | ||

| Equine | ||

| By Technology | Live Attenuated | |

| Inactivated / Killed | ||

| Toxoid | ||

| Recombinant / Sub-unit | ||

| Other Technologies (DNA, mRNA, VLP, etc.) | ||

| By Disease Indication | Foot-and-Mouth Disease (FMD) | |

| Newcastle Disease | ||

| Porcine Reproductive & Respiratory Syndrome (PRRS) | ||

| Rabies | ||

| Brucellosis | ||

| Avian Influenza | ||

| Canine Parvovirus | ||

| Other Indications | ||

| By Route of Administration | Parenteral (Injection) | |

| Oral | ||

| Intranasal | ||

| Transdermal / Needle-free | ||

| Other Routes | ||

| By Distribution Channel | Veterinary Hospitals & Clinics | |

| Retail Pharmacies & Agri-Stores | ||

| Online / e-Commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Veterinary vaccines market in 2026 and where is it heading?

The market is pegged at USD 11.17 billion in 2026 and is projected to reach USD 16.80 billion by 2031 at an 8.49% CAGR.

Which animal segment contributes most to revenue?

Livestock leads with 63.55% share in 2025, underpinned by poultry, swine and bovine programs.

What technology is growing fastest?

Recombinant and sub-unit platforms are forecast to advance at a 10.75% CAGR because they support DIVA strategies.

Which region will record the highest growth?

Asia-Pacific is set to expand at 9.72% CAGR through 2031, driven by China and India.

How are online channels affecting distribution?

Relaxed telemedicine rules let licensed veterinarians prescribe remotely, pushing e-commerce vaccine sales toward a 12.32% CAGR.

What is the main restraint hampering wider uptake in emerging markets?

Cold-chain gaps cause up to 40% potency loss, making thermostable innovations and infrastructure upgrades critical.

Page last updated on: