Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 66.48 Billion |

| Market Size (2031) | USD 92.34 Billion |

| Growth Rate (2026 - 2031) | 6.79% CAGR |

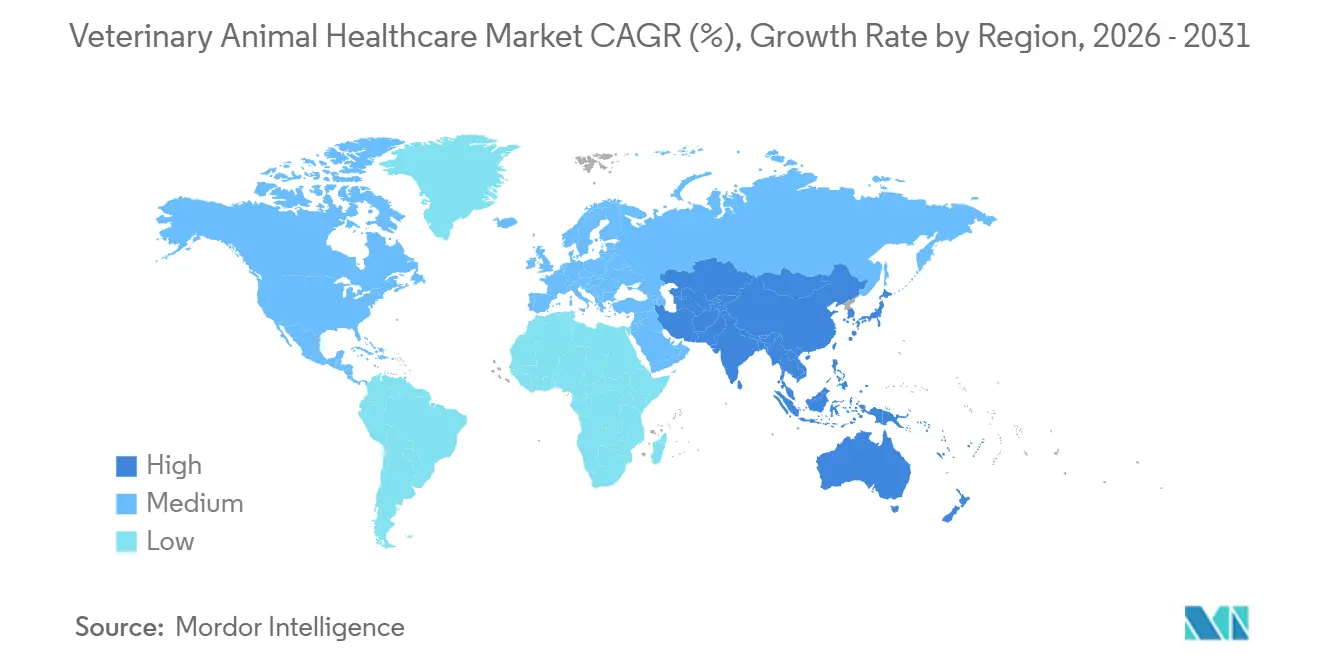

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

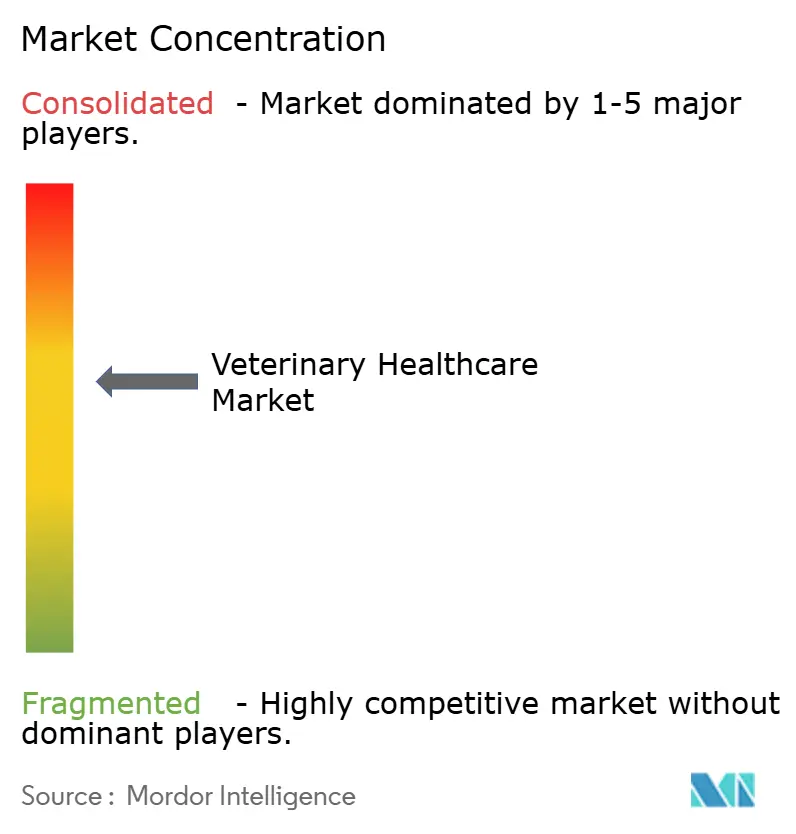

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Veterinary Animal Healthcare Market Analysis by ���ϲ�����

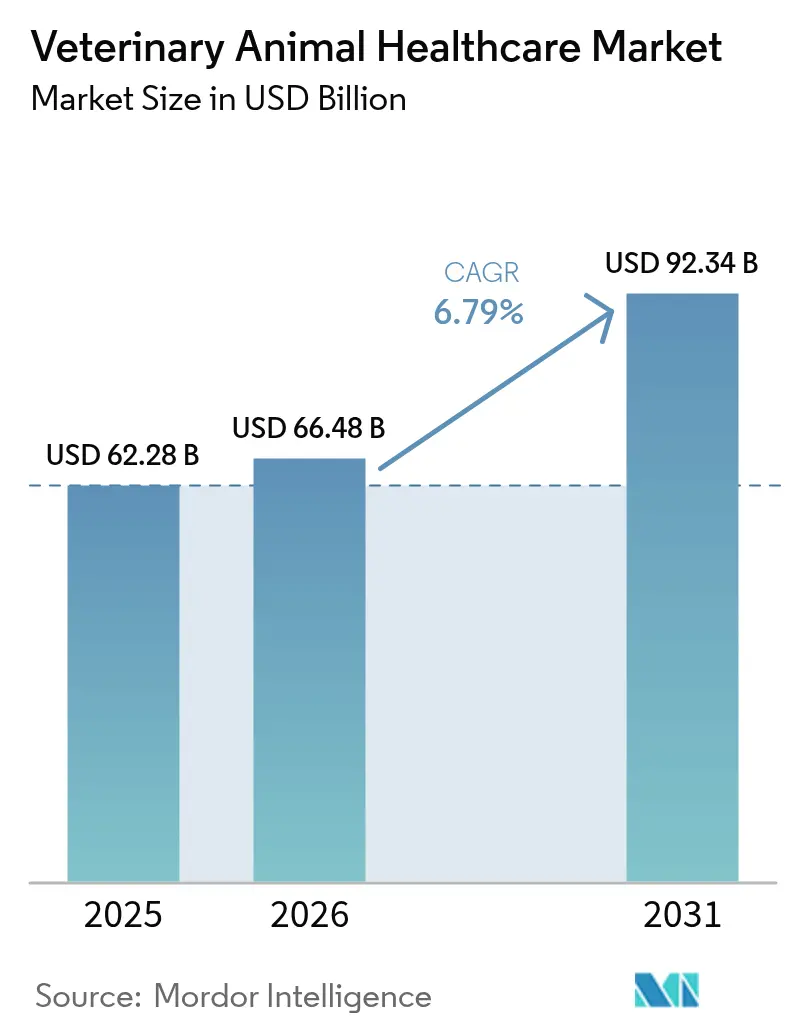

The Veterinary Animal Healthcare Market size is projected to expand from USD 62.28 billion in 2025 and USD 66.48 billion in 2026 to USD 92.34 billion by 2031, registering a CAGR of 6.79% between 2026 to 2031.

Growth is underpinned by the convergence of protein-supply security, companion-animal welfare, and rapid diagnostic innovation. Combination vaccines and monoclonal antibodies now reach commercial launch in 24–30 months, compressing historical timelines and enlarging addressable volumes for biologics. Early disease detection is gaining parity with therapeutics in capital budgets, as benchtop PCR systems and AI-augmented imaging shorten turnaround times from days to minutes. Tightening antimicrobial-stewardship rules are accelerating substitution toward narrow-spectrum drugs, probiotic feed additives, and autogenous vaccines. Meanwhile, vertical integration among corporate practice groups raises equipment-integration requirements that favor suppliers offering plug-and-play software and remote-support ecosystems.

Key Report Takeaways

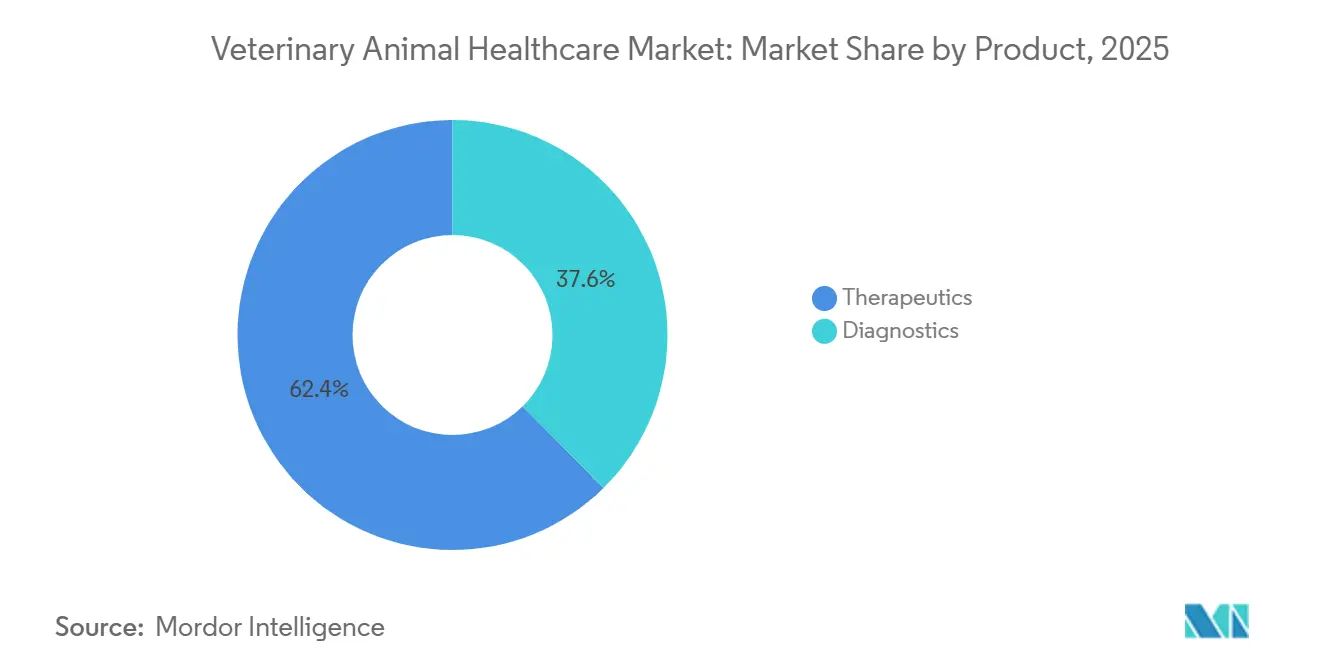

- By product, therapeutics commanded 62.4% of 2025 revenue, while diagnostics are advancing at a 7.86% CAGR to 2031, the fastest within the Veterinary Animal Healthcare Market.

- By animal type, dogs and cats led with 55.1% of 2025 revenue; poultry is expanding at a 7.12% CAGR through 2031.

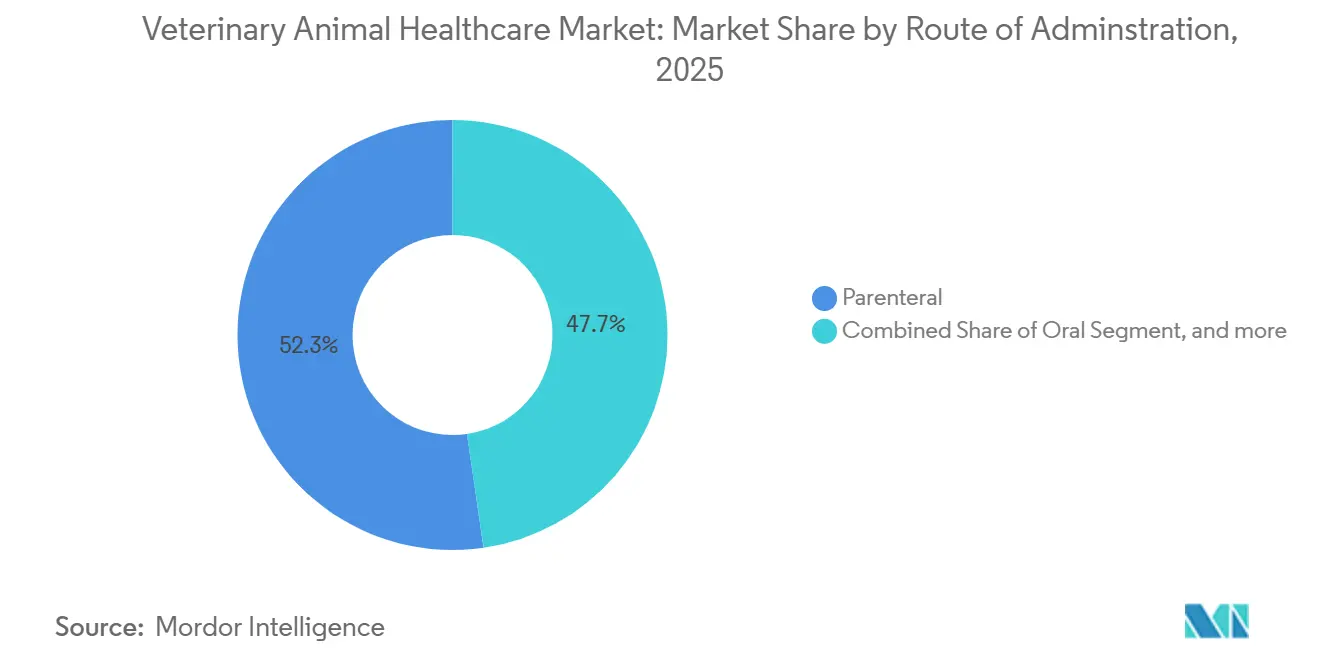

- By route of administration, parenteral delivery held 52.3% of 2025 revenue; oral formulations are projected to grow at 7.33% CAGR to 2031.

- By end user, hospitals and clinics contributed 57.7% of 2025 revenue, yet point-of-care settings are accelerating at an 8.32% CAGR through 2031.

- By geography, North America represented 45.3% of the Veterinary Animal Healthcare Market share in 2025, while Asia-Pacific is forecast to post the highest regional CAGR at 8.11% to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Animal Healthcare Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Protein-Rich Animal Products | +1.2% | Asia-Pacific core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Increasing Pet Humanization and Healthcare Spending | +1.8% | North America & Europe, emerging in urban Asia-Pacific | Long term (≥ 4 years) |

| Expanding Livestock Production in Emerging Economies | +1.1% | China, India, Vietnam, Brazil | Medium term (2-4 years) |

| Digital Transformation of Veterinary Practices | +0.9% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Tele-Medicine-Based Herd-Health Management Growth | +0.7% | North America, Australia, parts of Europe | Medium term (2-4 years) |

| AI-Enabled Early Disease-Detection Platforms | +1.0% | Global, initially concentrated in advanced markets | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising Demand for Protein-Rich Animal Products

Annual per-capita meat intake in Asia-Pacific climbed to 35 kilograms in 2025, spurring integrators to adopt real-time diagnostics against African swine fever and avian influenza, which in turn increases per-animal veterinary spend [1]FAO, “Meat Consumption Statistics 2025,” fao.org. Poultry producers in Thailand and Indonesia demonstrate mortality reductions of up to 18 percentage points after deploying autogenous vaccines. Brazil invested USD 240 million in 2025 for traceability upgrades that align with antibiotic-free import standards. Cage-free transitions in North America raise pathogen exposure, necessitating broader vaccine coverage. Gulf markets expand cold-storage capacity for halal-certified biologics, widening distribution channels for thermostable formulations.

Increasing Pet Humanization and Healthcare Spending

Average U.S. household veterinary outlay reached USD 1,480 per dog in 2025, a 22% increase versus 2020 [2]American Veterinary Medical Association, “Pet Expenditure Trends 2025,” avma.org. Pet-insurance penetration climbed to 4.2%, lowering price sensitivity for MRI, CT, and genomic screens. Urban millennials in China subscribe to preventive-care bundles that combine dental, vaccine, and parasite prophylaxis, posting 30% growth in 2025 clinic subscriptions. Specialist oncology centers installed linear accelerators for radiation therapy, expanding advanced-care capacity in California and Texas. Tele-consult platforms processed 8.5 million visits in 2025, yet several EU states still require in-person exams before prescribing.

Expanding Livestock Production in Emerging Economies

India’s dairy herd reached 145 million head in 2025 on the back of subsidy-funded artificial-insemination programs. Vietnam’s swine inventory rebounded to 28 million after biosecurity upgrades and mandatory vaccination raised per-pig veterinary spend by 40%. Brazil shipped 4.8 million metric tons of poultry in 2025 underpinned by PCR hatchery surveillance. Sub-Saharan Africa’s cattle population expands 3.1% per year, yet service coverage remains below 30%, creating scope for solar-powered vaccine fridges. China now obliges large farms to submit quarterly disease-surveillance datasets through electronic health records.

Digital Transformation of Veterinary Practices

Private-equity-backed consolidators operated 6,200 clinics in North America by 2025, standardizing protocols via cloud EHRs and telemedicine. Integrated practice-management systems auto-populate lab results from IDEXX analyzers, generating automated follow-up prompts. AI-based radiology tools achieved 94% concordance with board-certified specialists, trimming interpretation time to under 2 minutes. Australian livestock apps record GPS-tagged treatments and automate withdrawal calculations [3]Australian Veterinary Association, “Telemedicine Adoption in Rural Practices,” ava.com.au. European pilots link blockchain animal IDs to veterinary certificates for antibiotic-free claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Compliance & Approval Timelines | –0.8% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Antimicrobial-Resistance Stewardship Restrictions | –0.6% | Global, led by EU and North America | Medium term (2-4 years) |

| Cold-Chain Gaps for Critical Biologics | –0.5% | Sub-Saharan Africa, Southeast Asia, parts of Latin America | Medium term (2-4 years) |

| Alternative-Protein Diets Curb Livestock Numbers | –0.4% | North America and Western Europe | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Stringent Regulatory Compliance & Approval Timelines

Median U.S. FDA approval for novel veterinary biologics lengthened to 38 months in 2025 as five-year safety monitoring became mandatory. EMA now requires aquatic-toxicity and soil-persistence models, adding up to nine months to EU launches. A single companion-animal dossier can cost USD 5 million in preclinical work and fees, deterring niche-indication investment. China insists on in-country efficacy trials even for products approved elsewhere, fragmenting rollout strategies. Japan still lacks a conditional-approval fast-track, delaying emergency vaccines.

Antimicrobial-Resistance Stewardship Restrictions

Europe rules banning prophylactic use of medically important antimicrobials raised feed costs 18–25% as producers switched to probiotics and organic acids. U.S. sales of such drugs to food animals dropped 22% after over-the-counter access ended in 2025. North American integrators spent USD 340 million upgrading ventilation and density management to offset antibiotic reductions. Rapid susceptibility tests deliver results in six hours, guiding targeted therapy. Exporters in Brazil and Thailand must navigate differing withdrawal intervals across destination markets.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Diagnostics Outpace Therapeutics in Innovation Velocity

Therapeutics accounted for 62.4% of 2025 revenue within the Veterinary Animal Healthcare Market, anchored by combination vaccines and anti-infectives. Diagnostics are forecast to grow at 7.86% annually, supported by point-of-care immunoassays and AI-enabled imaging. Vaccines dominate therapeutic volume, with multivalent canine and bovine formulations displacing monovalent products. Pricing pressure on parasiticides arises as isoxazoline generics arrive, yet new chewable endectocides that cover flea, tick, and heartworm in one dose gain traction.

Molecular diagnostics expand as PCR unit prices fall below USD 15,000, opening mid-tier clinic adoption. Portable ultrasound and digital radiography penetrate equine and large-animal field work where ruggedness and mobility are essential. Clinical-chemistry analyzers bundled with hematology modules become standard in critical-care rooms, reducing reliance on external labs. Feed additives based on phytogenics deliver 4–7% feed-conversion gains relative to antibiotics. Anti-infective portfolios increasingly emphasize narrow-spectrum cephalosporins that meet stewardship criteria.

By Animal Type: Poultry Biosecurity Drives Fastest Expansion

Dogs and cats commanded 55.1% of 2025 revenue, reflecting high spend on preventive dentistry, orthopedic repair, and oncology. Poultry is the fastest-growing segment, advancing at 7.12% CAGR to 2031 as Asia-Pacific integrators lift biosecurity spend and deploy onsite influenza antigen tests. The Veterinary Animal Healthcare Market size for poultry is projected to expand at USD-denominated mid-single-digit billions by 2031, reflecting continuous integration investments.

Equine care remains niche, driven by performance-medicine spending in North America and Europe. Dairy operations intensify mastitis-prevention and reproductive-efficiency programs, while beef herds shrink amid drought and plant-protein consumption trends. Swine herds in China and Vietnam rebuild after ASF, driving sales of biosecure infrastructure. Aquaculture vaccines reduce antibiotic use 30% since 2023, boosting health budgets in Norwegian salmon and Southeast Asian shrimp farming. The Veterinary Animal Healthcare Market share for exotic and zoo animals remains under 2%, concentrated in accredited institutions.

By Route of Administration: Oral Gains on Palatability Breakthroughs

Parenteral formats captured 52.3% of 2025 revenue in the Veterinary Animal Healthcare Market, led by vaccines and long-acting injectables. Oral formulations are forecast to expand at a 7.33% CAGR as flavor-masking and chewable matrices increase owner compliance. Lipid-based carriers improve bioavailability for hydrophobic actives and enable once-monthly chewable antiparasitics that match injectable duration.

Topicals face competition from systemic options but retain popularity among owners wary of needles. Long-acting injectables such as moxidectin extend dosing intervals to quarterly, enhancing livestock compliance.

Intramammary and intra-articular routes serve specialized needs like mastitis and equine joint disease. Veterinary Animal Healthcare Market size growth for oral formats is reinforced by livestock drenches and in-feed nutraceuticals that avoid antimicrobial classifications.

By End User: Point-of-Care Settings Reshape Diagnostic Workflows

Hospitals and clinics generated 57.7% of 2025 revenue, yet in-house and point-of-care venues are growing fastest at 8.32% CAGR. Analyzers deliver complete blood counts in under 15 minutes, negating courier lead times and propelling Veterinary Animal Healthcare Market penetration among mobile practices. Reference labs maintain leadership in histopathology and genomic services, though turnaround gaps narrow.

Corporate consolidation standardizes procurement, privileging suppliers with integrated instrumentation and centralized support. On-farm diagnostics for pregnancy and mastitis underpin livestock decision-making. Mobile clinics equipped with handheld ultrasound and battery-powered hematology units extend veterinary reach into underserved territories. Telemedicine further blends end-user boundaries, routing triage between home care and referral centers, thereby expanding the Veterinary Animal Healthcare Market footprint.

Geography Analysis

North America accounted for 45.3% of 2025 revenue due to high per-pet spend and consolidated practice networks. Asia-Pacific is projected to grow at 8.11% CAGR, adding USD-denominated double-digit billions to the Veterinary Animal Healthcare Market size by 2031. China’s pet population exceeded 120 million dogs and cats, fueling multispecialty clinic growth. India’s dairy sector elevates veterinary input intensity, though rural coverage gaps persist, creating room for mobile and tele-health service expansion.

Europe benefits from stringent welfare rules that mandate veterinary oversight across production systems, yet stagnant companion-animal numbers temper revenue growth. The EU Farm-to-Fork strategy’s 50% antimicrobial-reduction target accelerates vaccine and probiotic adoption. Middle East and Africa present bifurcated demand: Gulf states invest in camel and equine centers, while sub-Saharan regions focus on cold-chain expansions for livestock vaccines.

South America’s export-oriented poultry and beef sectors invest in traceability and surveillance to satisfy import partners, driving Veterinary Animal Healthcare Market adoption of rapid PCR and blockchain certification. Brazil’s USD 240 million 2025 traceability outlay underscores commitment to disease-free status. Argentina and Colombia replicate Brazil’s hatchery-based PCR programs. Across regions, tele-enabled clinics and thermostable biologics emerge as common denominators of future growth

Competitive Landscape

The Veterinary Animal Healthcare Market is moderately consolidated; the top five players capture about majority of global revenue. Zoetis, Boehringer Ingelheim, and Merck Animal Health leverage integrated R&D pipelines to launch combination vaccines that reduce handling steps and improve compliance. Diagnostic specialists such as IDEXX and Heska embed AI algorithms that auto-interpret hematology and imaging results, cutting turnaround times by one-third. White-space opportunities include thermostable livestock vaccines, cloud-native telemedicine platforms, and aquaculture biologics with proprietary adjuvants.

Patent filings for machine-learning image analysis rose significantly in 2025, signaling intellectual-property stakes as point-of-care devices commoditize. Regulatory costs rise under FDA Guidance 263 and EMA pharmacovigilance extensions, pressuring smaller firms toward licensing or acquisition. Geographic portfolios diverge: companion-animal leaders prioritize China’s urban segments, whereas livestock-focused firms invest in Brazil, Vietnam, and parts of Africa where protein demand outpaces infrastructure. Practice-group consolidation raises integration barriers, cementing incumbency for vendors with seamless EHR connectivity and automated inventory replenishment.

Veterinary Animal Healthcare Industry Leaders

Zoetis Inc.

Boehringer Ingelheim International GmbH

Elanco Animal Health

Merck & Co., Inc.

IDEXX Laboratories Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Zoetis announced a pivot toward feline chronic kidney disease and companion-animal oncology, targeting the USD 3–4 billion CKD opportunity.

- December 2025: Boehringer Ingelheim secured FDA approval for the first monoclonal antibody to treat canine atopic dermatitis, opening a USD 400 million U.S. segment.

- November 2025: Zoetis acquired Veterinary Pathology Group to expand its U.K. and Ireland diagnostics footprint.

Global Veterinary Animal Healthcare Market Report Scope

As per the report's scope, veterinary animal healthcare can be defined as the science associated with diagnosing, treating, and preventing animal diseases. The increasing importance of the production of livestock animals is boosting market growth.

The veterinary animal healthcare market is segmented by product, animal type, and geography. By product, the market is segmented into therapeutics and diagnostics. By animal type, the market is segmented into dogs, cats, horses, ruminants, swine, poultry, and other animal types. By route of administration, the market is segmented into oral, parenteral, topical, and other routes. By end users, the market is segmented into veterinary hospitals & clinics, reference laboratories, point-of-care / in-house settings, and academic & research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for all the above segments.

By Product

| Therapeutics | Vaccines |

| Parasiticides | |

| Anti-Infectives | |

| Medical Feed Additives | |

| Other Therapeutics | |

| Diagnostics | Immunodiagnostic Tests |

| Molecular Diagnostics | |

| Diagnostic Imaging | |

| Clinical Chemistry | |

| Other Diagnostics |

By Animal Type

| Dogs & Cats |

| Horses |

| Ruminants |

| Swine |

| Poultry |

| Other Animal Types |

By Route of Administration

| Oral |

| Parenteral |

| Topical |

| Other Routes |

By End User

| Veterinary Hospitals & Clinics |

| Reference Laboratories |

| Point-of-Care / In-House Settings |

| Academic & Research Institutes |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Therapeutics | Vaccines |

| Parasiticides | ||

| Anti-Infectives | ||

| Medical Feed Additives | ||

| Other Therapeutics | ||

| Diagnostics | Immunodiagnostic Tests | |

| Molecular Diagnostics | ||

| Diagnostic Imaging | ||

| Clinical Chemistry | ||

| Other Diagnostics | ||

| By Animal Type | Dogs & Cats | |

| Horses | ||

| Ruminants | ||

| Swine | ||

| Poultry | ||

| Other Animal Types | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| Other Routes | ||

| By End User | Veterinary Hospitals & Clinics | |

| Reference Laboratories | ||

| Point-of-Care / In-House Settings | ||

| Academic & Research Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for global veterinary healthcare?

Revenues stand at USD 66.48 billion in 2026 and are forecast to reach USD 92.34 billion by 2031, reflecting a 6.79% CAGR.

Which product line is showing the fastest expansion?

Diagnostics leads growth at a 7.86% CAGR through 2031, driven by molecular point-of-care platforms and rapid in-clinic testing.

How does rising pet humanization affect spending?

Owners treat pets as family members, lifting average U.S. veterinary bills to USD 1,480 per household in 2024 and boosting demand for premium therapies and insurance uptake.

Why is poultry health spending accelerating?

Intensive production and biosecurity rules push poultry to a 7.12% CAGR, with mandatory vaccines and rapid pathogen screening becoming routine.

What impact do point-of-care diagnostics have on veterinary clinics?

In-house analyzers deliver results within minutes, raise case acceptance, and are propelling the fastest end-user growth segment at a 7.28% CAGR.

What key obstacles limit broader product adoption?

Lengthy regulatory approvals add up to two years per novel therapy, while equipment costs above USD 100,000 restrict access for rural and emerging-market clinics.

Page last updated on: