Bahrain Cybersecurity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

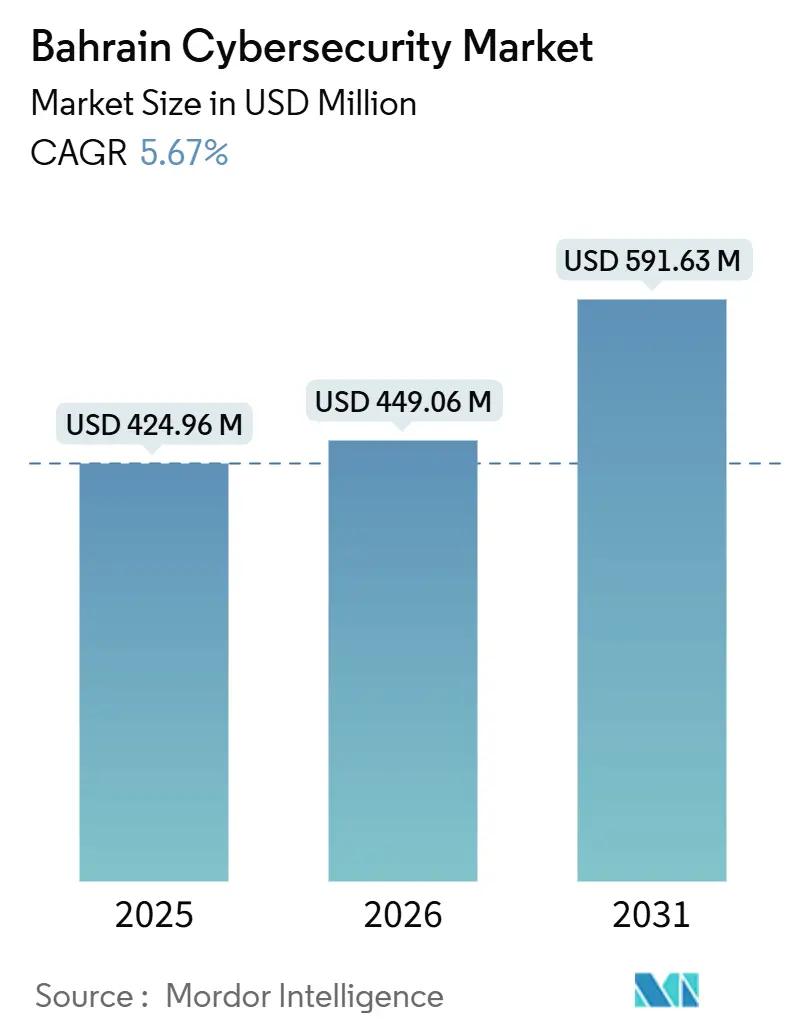

| Base Year Market Size (2025) | USD 424.96 Million |

| Market Size (2026) | USD 449.06 Million |

| Market Size (2031) | USD 591.63 Million |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

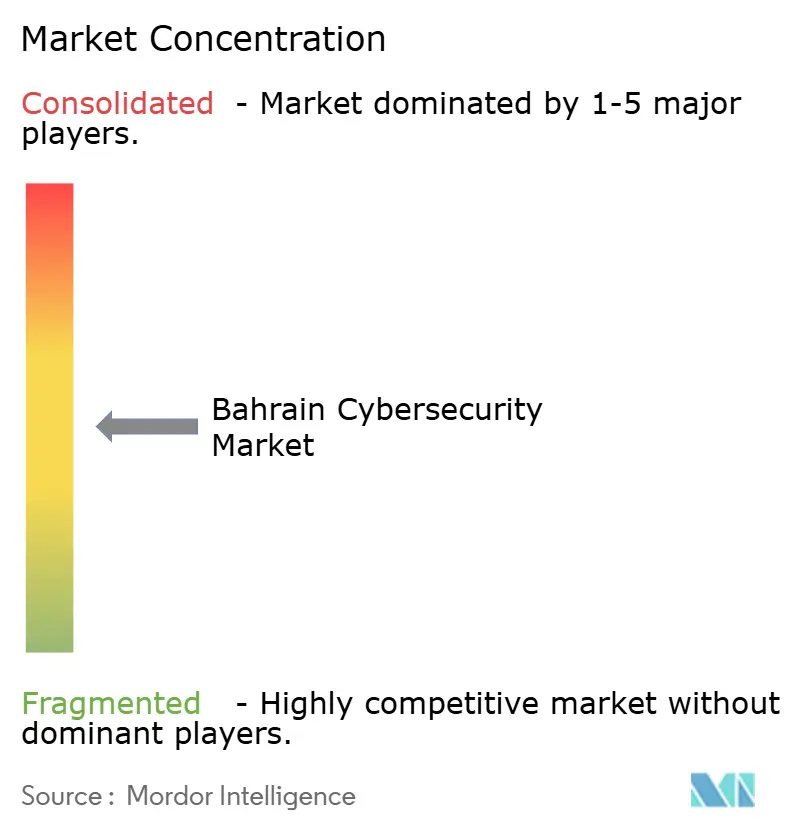

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Bahrain Cybersecurity Market Analysis by ���ϲ�����

The Bahrain Cybersecurity Market size is expected to increase from USD 424.96 million in 2025 to USD 449.06 million in 2026 and reach USD 591.63 million by 2031, growing at a CAGR of 5.67% over 2026-2031. Mandatory compliance programs in banking, utilities, and public administration continue to anchor spending, while expanding 5G coverage, a Cloud-First mandate covering 85% of government workloads, and an influx of hyperscaler infrastructure broaden the total addressable opportunity. Rising artificial-intelligence-enabled cybercrime, exemplified by Bahraini organizations accounting for 7% of regional DDoS traffic in 3Q 2025, accelerates demand for real-time threat intelligence platforms. Investments now lean toward managed detection and response because a persistent talent shortage inflates the cost of in-house operations. At the same time, quantum-safe cryptography pilots and zero-trust architectures are reshaping product roadmaps, signaling the next wave of differentiation for vendors able to prove post-quantum readiness.

Key Report Takeaways

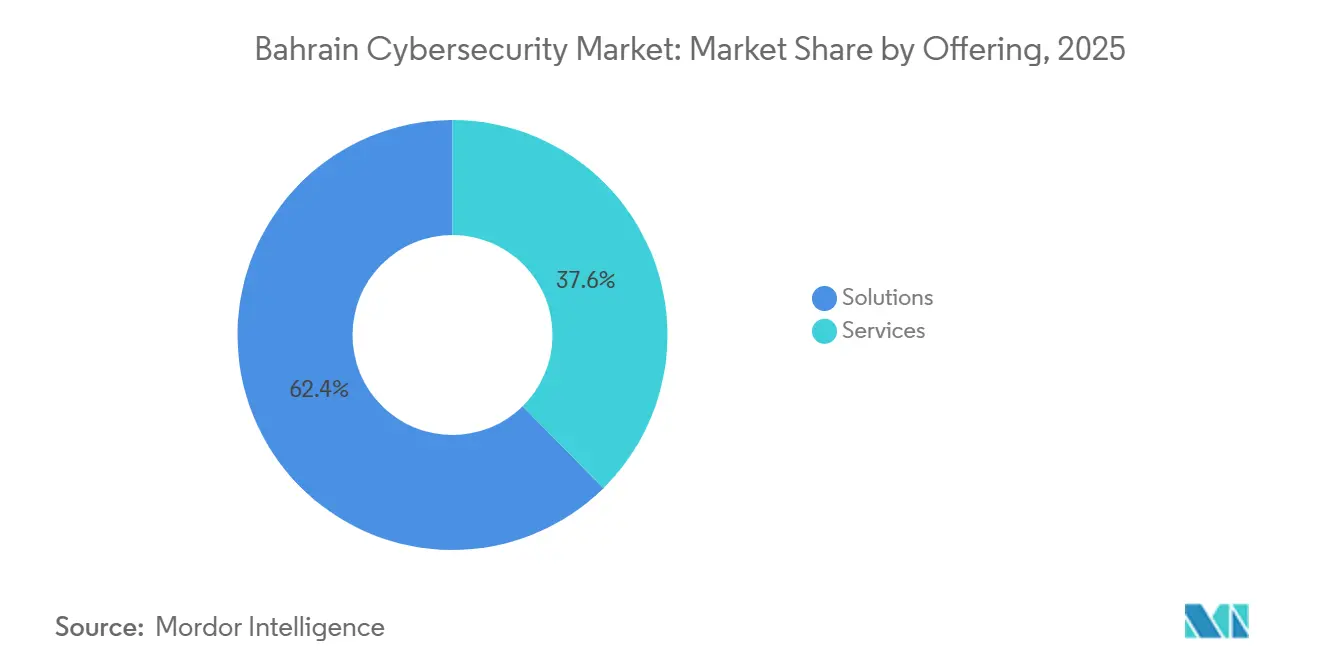

- By offering, solutions captured 62.38% of Bahrain cybersecurity market share in 2025, while services are projected to post the fastest growth at 6.23% CAGR through 2031.

- By deployment mode, on-premises security dominated with 63.43% of the Bahrain cybersecurity market size in 2025; cloud-based safeguards are forecast to expand at the same 6.23% CAGR thanks to the Cloud-First policy.

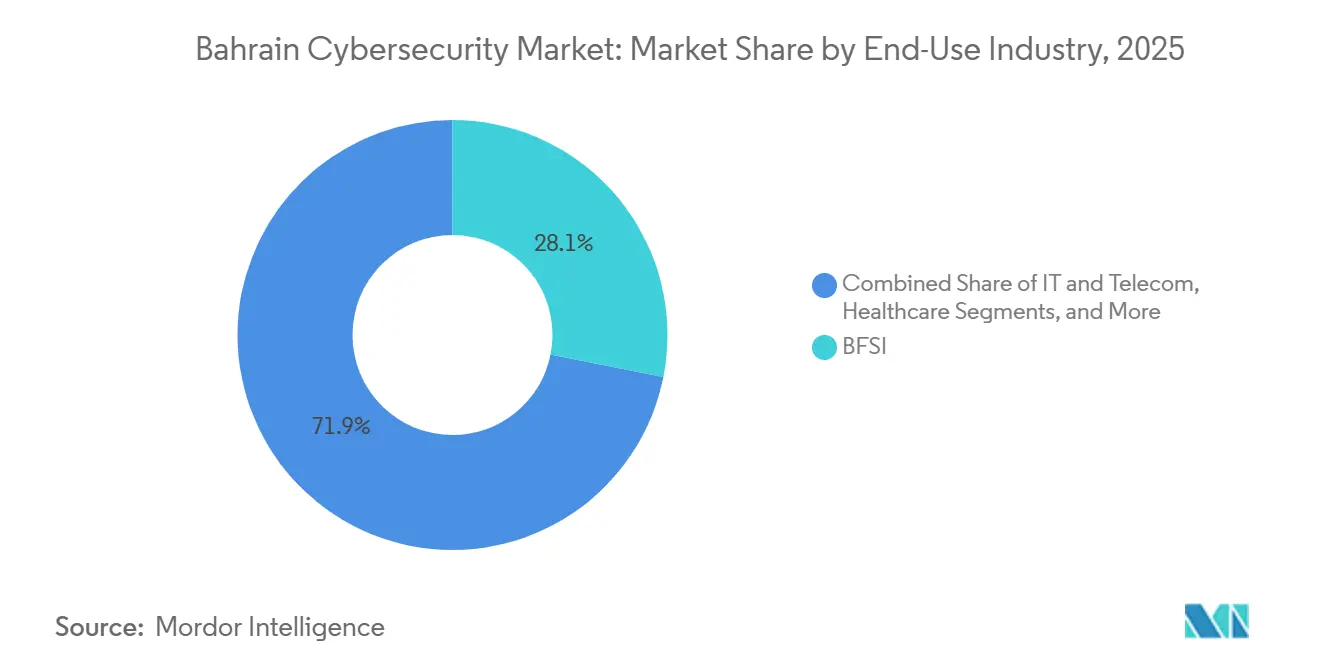

- By end-use industry, banking, financial services, and insurance led with 28.12% revenue share in 2025, whereas healthcare is set to register the highest 7.17% CAGR to 2031.

- By enterprise size, large organizations commanded 62.81% of 2025 spending, yet small and medium enterprises are on track for a 7.13% CAGR, supported by government subsidy programs.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bahrain Cybersecurity Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Digital Transformation Initiatives Across BFSI | +1.2% | National, concentrated in Manama financial district and Bahrain FinTech Bay | Medium term (2-4 years) |

| Rising Incidence of Sophisticated Cyber Threats | +1.0% | National, with spillover effects across GCC due to regional threat actor activity | Short term (≤ 2 years) |

| Government Mandates for Critical Infrastructure Protection | +0.9% | National, focused on Gas, Electricity and Oil, telecommunications, water, and government sectors | Long term (≥ 4 years) |

| Rapid Adoption of Cloud Services in Bahrain | +0.8% | National, led by government Cloud-First policy and private-sector SaaS migration | Medium term (2-4 years) |

| Accelerated Deployment of National Open Banking APIs | +0.7% | National, BFSI sector with Central Bank of Bahrain oversight | Short term (≤ 2 years) |

| Growth of Bahrain's Fintech Sandbox Participants Requiring Advanced Security | +0.5% | National, Bahrain FinTech Bay and regulatory sandbox participants | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Increasing Digital Transformation Initiatives Across BFSI

���ϲ�����less-payment ceilings rose to BHD 50 (USD 132), mobile banking adoption surged after the pandemic, and every retail bank must maintain PCI-DSS compliance, EMV chip-and-PIN controls, and geolocation-based fraud analytics.[1]Central Bank of Bahrain, “CBB Rulebook Volume 5 – Payment Card Security,” CBB.GOV.BH These rules trigger accelerated refresh cycles for identity and access management, tokenization, and API-security gateways that prevent credential leakage. Bahrain FinTech Bay’s 21 sandbox participants often lack in-house expertise, creating a niche for managed security providers able to bundle cloud-native defenses with regulatory reporting dashboards. A 2024 academic study confirmed that rapid prototyping and third-party API dependencies magnify threat exposure for early-stage fintechs, underscoring appetite for scalable, pay-as-you-grow safeguards. The driver raises baseline spending and cements banking as the anchor tenant of the Bahrain cybersecurity market.

Rising Incidence of Sophisticated Cyber Threats

Nation-state actors, hacktivists, and financially motivated groups continue to probe Bahraini infrastructure. The National Cyber Security Centre logged seven domestic ransomware victims between 2022-2026, while Dragos reported an 87% global jump in industrial ransomware attacks during 2024, 75% of which caused partial OT shutdowns. Artificial-intelligence-powered toolkits like FraudGPT lower entry barriers, enabling targeted phishing and business-email compromise campaigns. Mobile-supply-chain exploits also grow: Kaspersky uncovered the Triada Trojan on counterfeit smartphones, siphoning USD 270,000 in crypto from regional users. Such incidents compel continuous investment in extended detection and response, OT-security segmentation, and threat-intelligence subscriptions across the Bahrain cybersecurity market.

Government Mandates for Critical Infrastructure Protection

Seven sectors energy, telecommunications, water, government, healthcare, finance, and transportation must follow sector-specific controls that include 24/7 security operations centers, biannual penetration tests, and one-hour incident-report windows. Defense modernization, highlighted by a USD 500 million HIMARS buy that bundles secure C4I systems, broadens demand for ruggedized encryption and classified-network hardening. Hybrid architectures protecting both legacy on-premises assets and new cloud workloads spur uptake of cloud-access security brokers, zero-trust network access, and ISO-27001-aligned governance suites. The directive ensures a steady multi-year pipeline for vendors active in the Bahrain cybersecurity market.

Rapid Adoption of Cloud Services in Bahrain

The Cloud-First mandate migrated 85% of government workloads to hyperscale platforms by 2025, and IDC estimates cloud services will add USD 1.2 billion to Bahrain’s GDP by 2026. Amazon Web Services’ in-country region guarantees data residency, propelling platform-as-a-service revenue from USD 33.1 million in 2024 toward USD 191.7 million by 2033. Healthcare providers adopt always-on encryption and automated threat detection as described in Oracle’s 2025 GCC whitepaper, making cloud-native security a competitive differentiator.[2]Oracle Corporation, “Healthcare Cloud Security in the GCC,” ORACLE.COM Yet misconfigurations persist; Tenable found 70% of regional AI workloads exposed, with 30% harboring the critical curl vulnerability CVE-2023-38545. The migration reshapes perimeter strategies and accelerates unified exposure-management adoption across the Bahrain cybersecurity market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Cybersecurity Professionals | -0.8% | National, acute in public sector and SME segments | Long term (≥ 4 years) |

| High Initial Investment for Advanced Solutions | -0.6% | National, affects SMEs and budget-limited public bodies | Medium term (2-4 years) |

| Complex Regulatory Compliance Landscape | -0.4% | National, cross-border for multinationals | Medium term (2-4 years) |

| Fragmented Legacy Systems in Public Sector | -0.3% | National, ministries and utilities | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Shortage of Skilled Cybersecurity Professionals

The National Cyber Security Centre aims to train 20,000 citizens by 2026, yet demand for OT security architects, cloud specialists, and threat hunters already exceeds supply.[3]Kingdom of Bahrain National Cyber Security Centre, “National Cybersecurity Strategy 2025-2028,” NCSC.GOV.BH Tamkeen and SANS deliver subsidized courses, and Beyon Cyber’s memorandum with Bahrain Polytechnic adds internships, but salary competition from multinationals drains talent. Skills scarcity forces small entities to outsource operations, inflates service fees, and slows deployment of AI-driven security operations centers across the Bahrain cybersecurity market.

High Initial Investment for Advanced Security Solutions

Next-generation platforms SIEM, XDR, and integrated risk management carry steep upfront costs. While Tamkeen’s SME vouchers and Zoho One bundles soften the blow, many firms still underinsure against cyber loss. PricewaterhouseCoopers found 15% of regional breaches exceeded USD 100,000, but only one-quarter of firms planned double-digit budget hikes for 2025. Capital hurdles encourage subscription models, yet public agencies steeped in procurement cycles hesitate, tempering growth momentum in the Bahrain cybersecurity market.

Segment Analysis

By Offering: Managed Services Gain Traction Amid Skills Gap

The Bahrain cybersecurity market size for solutions stood at USD 0.27 billion in 2025, equal to 62.38% of total revenue. Compliance-driven purchases of firewalls, endpoint detection, and identity governance platforms dominated as banks, telecom operators, and ministries raced to meet stringent incident-reporting rules. Nevertheless, a chronic talent shortage and rising platform complexity prompt enterprises to reassess do-it-yourself security models.

Services revenue, forecast to expand at 6.23% CAGR, reflects this pivot. Managed detection and response centers offer predictable subscription pricing, rapid deployment, and 24-hour coverage that SMEs cannot replicate internally. Beyon Cyber’s acquisition of DTS Solution injected 60 extra specialists and broadened advisory, OT-security, and fintech-security lines, illustrating how local providers bundle expertise with platforms to lock in mid-market accounts. As a result, managed offerings are set to outpace hardware sales, reshaping channel strategies across the Bahrain cybersecurity industry.

By Deployment Mode: Cloud Security Accelerates as Government Leads Migration

On-premises controls represented 63.43% of 2025 spending because critical-infrastructure entities rely on air-gapped environments for classified systems. Yet the Cloud-First policy and the presence of an AWS region tilt new projects toward elastic security-as-a-service layers. The Bahrain cybersecurity market size tied to cloud defenses is projected to climb at 6.23% CAGR, fueled by SaaS adoption in retail and healthcare.

Ministries retain latency-sensitive OT assets in data centers while enforcing zero-trust network access for staff using Microsoft 365, whose centralized backup rolled out to 44 agencies in 2024. Sophos’ plan to open a UAE data center heightens competitive pressure, pushing Bahraini managed providers to guarantee in-country hosting. Misconfiguration and shadow-IT risks keep demand high for cloud posture-management suites.

By End-Use Industry: Healthcare Surges on EHR Rollouts and Ransomware Exposure

Banking held the largest contribution, accounting for 28.12% of Bahrain cybersecurity market share in 2025, underpinned by PCI-DSS rules and the Open Banking Framework that secures APIs against man-in-the-middle exploits. Mandatory SOC operations and tokenization engines make the sector a perennial spender.

Healthcare, while smaller today, is on course for the swiftest 7.17% CAGR after I-SEHA achieved 89% electronic-health-record penetration and a June 2025 ransomware hit exposed gaps in network segmentation. Hospitals shift imaging archives to encrypted cloud storage, adopt micro-segmentation for Internet-of-Things devices, and run tabletop drills, converting compliance need into an expanding revenue pool within the Bahrain cybersecurity market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Enterprise Size: SME Momentum Builds Through Subsidies

Large organizations contributed 62.81% of 2025 outlays, primarily on integrated risk platforms and bespoke threat intelligence feeds that exceed smaller budgets. Their established chief information security officers integrate cybersecurity into board-level planning, sustaining multi-year refresh cycles.

Conversely, the SME cohort is projected to post a 7.13% CAGR. Tamkeen’s partnership with Mastercard to digitize 2,500 businesses and Zoho’s subsidized bundles lower entry barriers, while sandbox fintechs outsource SOC functions to avoid capital shock. As managed providers craft tiered service catalogs, the Bahrain cybersecurity market welcomes a new wave of first-time SME buyers.

Geography Analysis

Manama’s financial district, Bahrain FinTech Bay, and the Digital City cluster form the geographic nucleus of demand. Tier-1 status in the ITU 2024 Global Cybersecurity Index validates the Kingdom’s mature legal and technical frameworks, encouraging multinational enterprises to anchor regional operations locally. Absence of strict data-localization rules, combined with the AWS Bahrain region, attracts foreign direct investment and stimulates cross-border data flows.[4]Information and eGovernment Authority, “Cloud-First Policy,” IGA.GOV.BH

Government policy amplifies this magnetism. The National Cybersecurity Strategy 2025-2028 prioritizes critical-infrastructure protection, capability development, and international cooperation, laying out procurement pipelines for zero-trust and quantum-safe solutions. SandboxAQ’s deployment of AQtive Guard across 60 ministries positions Bahrain as an early adopter of post-quantum encryption, showcasing regulatory agility.

Regional spillovers further benefit the Bahrain cybersecurity market. Shared GCC threat-intelligence initiatives create economies of scale for vendors, and Beyon Cyber’s expansion into Saudi Arabia and Jordan illustrates how homegrown champions leverage Bahrain’s regulatory credibility to win contracts abroad. Progress hinges on resolving the skills gap and finishing cloud migrations at slower-moving public entities.

Competitive Landscape

Global platform vendors Cisco, Fortinet, Check Point, IBM, and Microsoft maintain entrenched enterprise accounts through certified local integrators. Their dominance stems from broad portfolios validated to ISO-27001, ISO-22301, and SOC-2 standards, yet they face price pressure from sovereign-hosted newcomers.

Domestic champions carve space by coupling localization with managed services. Beyon Cyber operates the largest private SOC, augmented by its DTS Solution acquisition, and markets an Integrated Defense Platform that unifies alert triage for mid-size banks and ministries. CTM360 focuses on digital-risk protection, recently allying with Cyberani to fold brand-protection feeds into Saudi managed services, signaling cross-border ambitions.

White-space opportunities cluster around OT security, quantum-safe cryptography, and AI-governance of large language models. Fortinet’s AI-powered workspace suite and Deloitte’s Cortex XSIAM center highlight a pivot toward consolidated, automation-rich offerings, catering to clients that lack headcount for multi-vendor orchestration. The Bahrain cybersecurity market therefore rewards vendors blending unified platforms, local data centers, and workforce-development partnerships.

Bahrain Cybersecurity Industry Leaders

Cisco Systems Inc.

Fortinet Inc.

Check Point Software Technologies Ltd.

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: CTM360 partnered with Cyberani to embed brand-protection and attack-surface management into Saudi managed services.

- December 2025: SandboxAQ agreed with the National Cyber Security Centre to deploy AQtive Guard quantum-safe cryptography across 60 ministries.

- November 2025: Beyon Cyber and Bahrain Polytechnic signed an MoU to develop cybersecurity curricula and internships.

- November 2025: Paramount and the NCSC launched MITRE D3FEND training for government defenders.

Bahrain Cybersecurity Market Report Scope

The Cybersecurity Market encompasses global spending on solutions, software, and services designed to protect digital infrastructure, data, and operations across all industries, including cloud, network, endpoint, and application security; it includes enterprise, government, and SME segments but excludes physical security and pure consulting-only services, with the market evolving rapidly toward AI-driven automation, platform consolidation, and regulatory-driven transformation.

The Bahrain Cybersecurity Market Report is Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End Point Security | |

| Services | Professional Services |

| Managed Services |

| On-Premises |

| Cloud |

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How large is the Bahrain cybersecurity market in 2026?

The Bahrain cybersecurity market size is projected to reach USD 449.06 million in 2026, on its way to USD 591.63 million by 2031.

What is the growth outlook for managed security services in Bahrain?

Managed service revenue is forecast to expand at 6.23% CAGR between 2026-2031 as firms outsource security operations to offset the talent gap.

Which sector spends the most on cybersecurity in Bahrain?

Banking, financial services, and insurance led 2025 spending with 28.12% of revenue, driven by stringent Central Bank regulations.

Why is healthcare the fastest-growing vertical?

EHR rollouts, ransomware incidents, and cloud-based telemedicine demand push healthcare to a 7.17% CAGR through 2031.

How does the Cloud-First policy influence security investment?

By migrating 85% of government workloads to public cloud, the policy shifts budgets toward cloud-native controls and zero-trust network access platforms.

What challenges could slow market expansion?

A shortage of certified professionals and high upfront costs for next-generation platforms remain key headwinds.