Zygomatic And Pterygoid Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 280.34 Million |

| Market Size (2031) | USD 381.59 Million |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

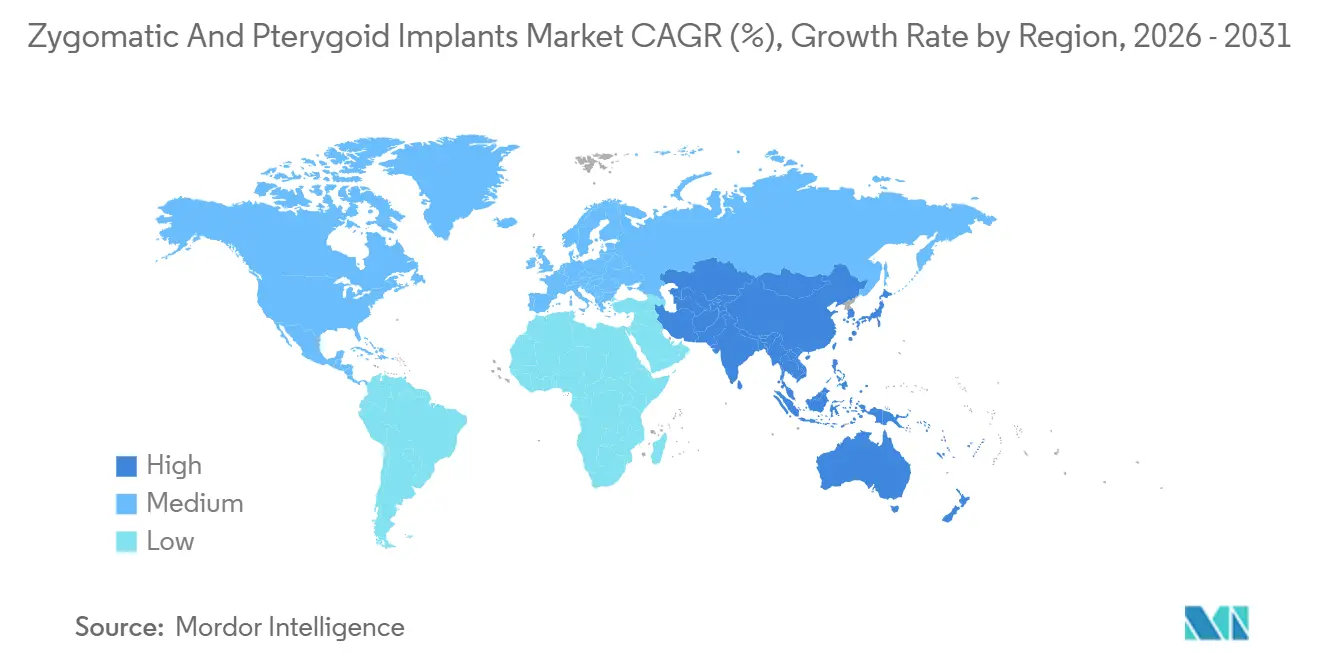

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Zygomatic And Pterygoid Implants Market Analysis by ���ϲ�����

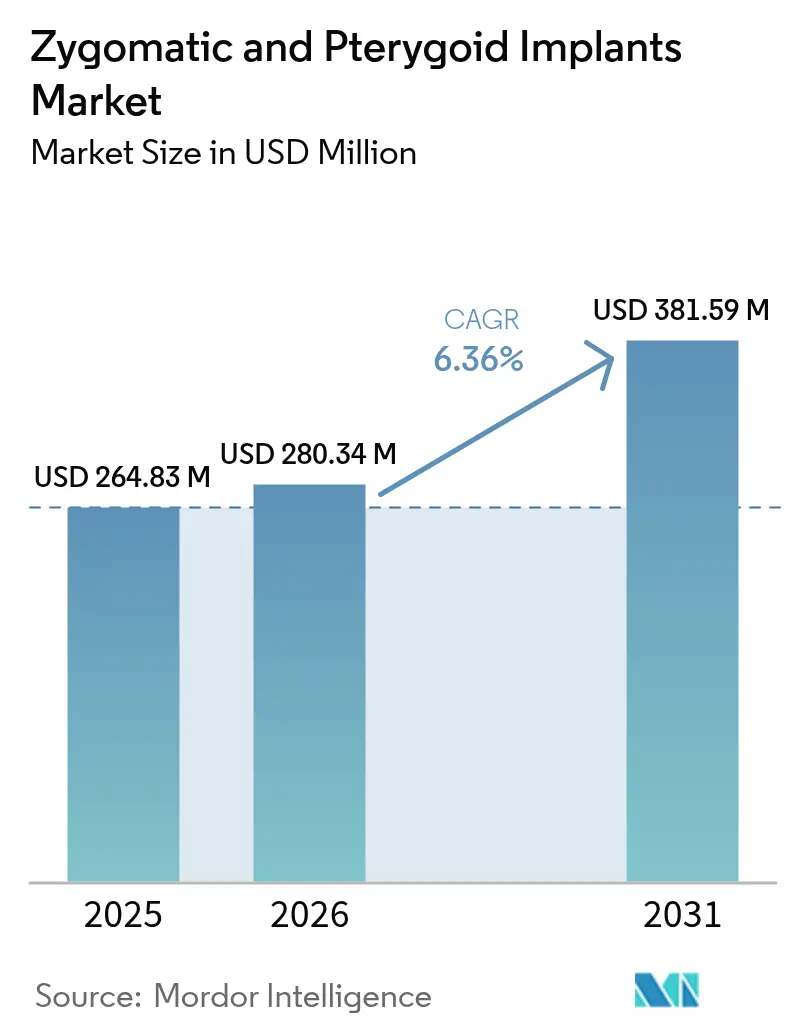

The Zygomatic And Pterygoid Implants Market size is projected to be USD 264.83 million in 2025, USD 280.34 million in 2026, and reach USD 381.59 million by 2031, growing at a CAGR of 6.36% from 2026 to 2031.

Clinical preference is shifting toward extra-maxillary anchorage solutions that bypass bone-grafting, shortening treatment timelines and expanding eligibility for patients with severe maxillary atrophy. Guidance issued by the U.S. Food and Drug Administration in 2024 placed zygomatic devices outside the streamlined endosseous pathway, highlighting their distinct biomechanical profile; nevertheless, a predicate-based route remains viable, as shown by NobelZygoma TiUltra’s 510(k) clearance in 2025. Immediate-loading protocols now dominate procedure volume because long-term survival consistently exceeds 98%, satisfying patient demand for same-day function. Digital dentistry, particularly cone-beam CT planning, CAD-CAM prosthetics, and dynamic navigation, continues to lower the learning curve, allowing more surgeons to offer complex extra-maxillary procedures.

Key Report Takeaways

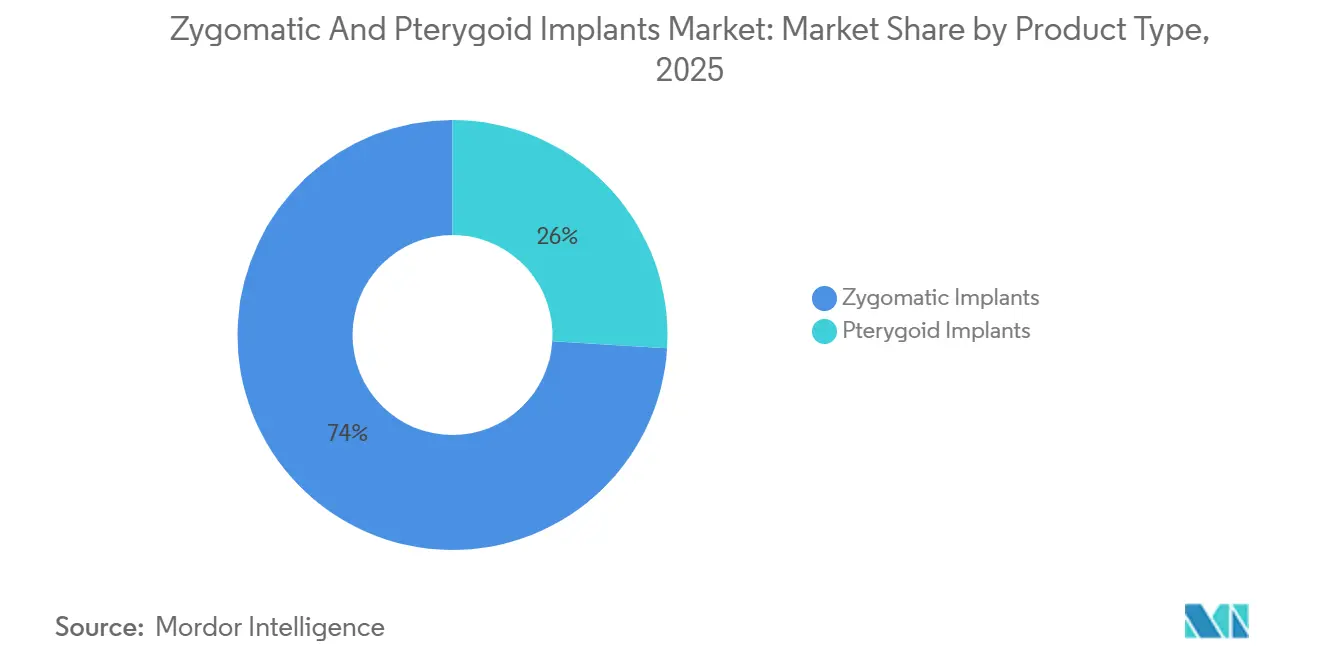

- By product type, zygomatic implants led with 74.02% of zygomatic and pterygoid implants market share in 2025 while pterygoid implants recorded the highest projected CAGR at 7.29% through 2031.

- By implant length, fixtures above 50 millimeters accounted for the fastest growth, expanding at a 9.93% CAGR between 2026-2031, whereas the 31-to-50 millimeter group retained 47.87% of the 2025 revenue.

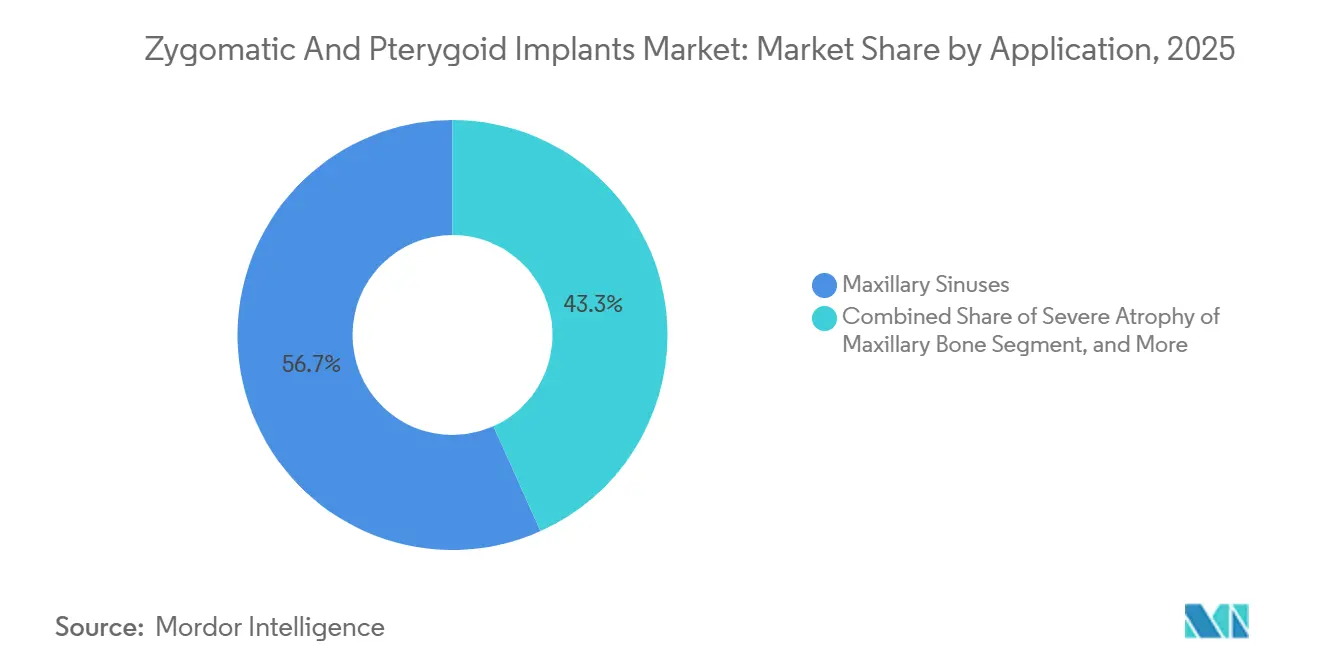

- By application, severe maxillary atrophy drove an 8.43% CAGR to 2031, overtaking the historically dominant maxillary-sinus indication, which held 56.72% of 2025 value.

- By procedure type, immediate loading accounted for 61.08% of 2025 procedures and is advancing at a 7.68% CAGR through 2031.

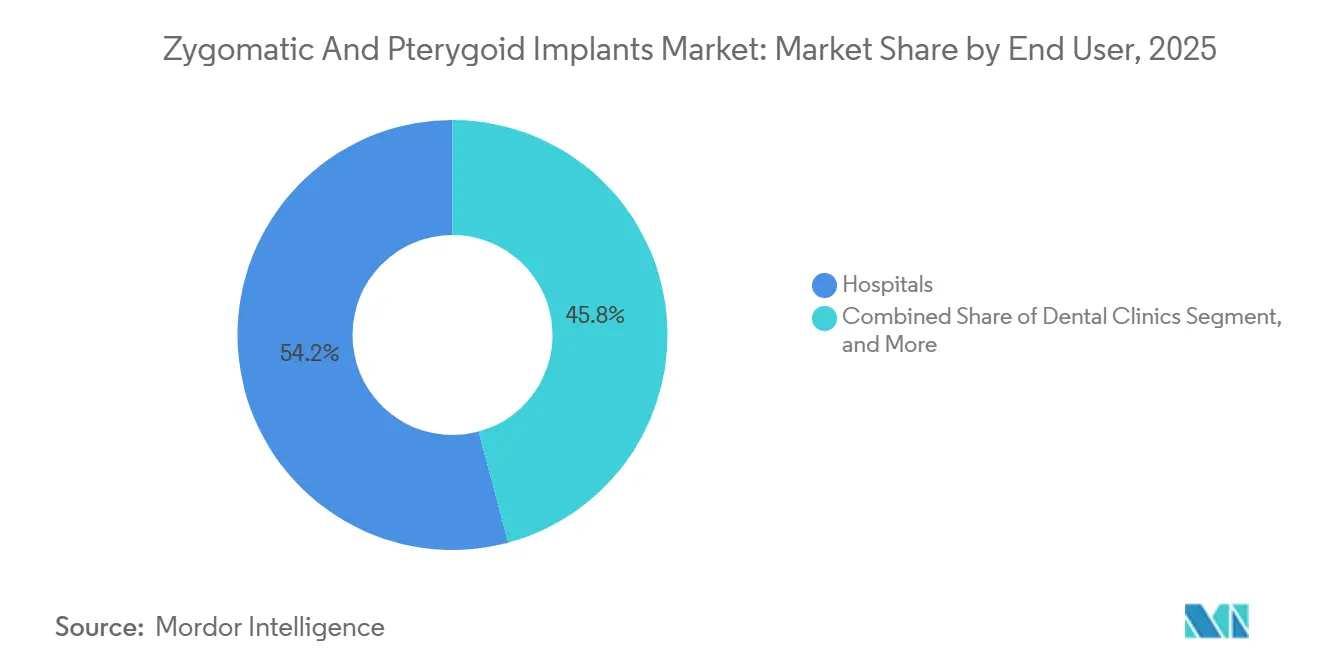

- By end user, ambulatory surgical centers are growing at 8.79% a year to 2031, narrowing the 54.18% volume lead hospitals held in 2025.

- By geography, North America retained 41.23% of 2025 value, the largest regional share, while Asia-Pacific is forecast to grow at 9.63% a year, the fastest pace worldwide.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Zygomatic And Pterygoid Implants Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Severe Maxillary Atrophy & Edentulism | +1.2% | Global, acute demand in aging North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Clinical Advantage of Graft-Less, Immediate-Loading Rehabilitation | +1.5% | Global, early uptake in North America and Western Europe, spreading to Asia-Pacific and Latin America | Medium term (2-4 years) |

| Adoption of Digital Dentistry | +0.9% | North America, Europe, high-income APAC markets | Medium term (2-4 years) |

| Quad-Zygomatic Protocols Expanding Eligible Patient Pool | +0.8% | Specialist centers in North America and Europe, gradual diffusion to APAC | Long term (≥ 4 years) |

| Dental Tourism Surge for Complex Oral Rehabilitation | +0.7% | Turkey, Spain, Hungary, Poland, Mexico, Costa Rica, Thailand, India | Short term (≤ 2 years) |

| Pilot Insurer Reimbursements for Oncologic Maxillectomy | +0.6% | United States, selected European payers | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising Prevalence of Severe Maxillary Atrophy & Edentulism

The World Health Organization noted in 2024 that severe periodontal disease affects 20% of adults, with prevalence spiking among people older than 65 and oncologic survivors.[1]World Health Organization, “Global Oral Health Status Report 2024,” WHO.int Maxillary atrophy results in vertical and horizontal bone loss, precluding the placement of conventional implants, prompting the adoption of zygomatic and pterygoid solutions that deliver fixed prostheses within weeks. Rapid execution appeals to patients managing diabetes or osteoporosis who cannot tolerate lengthy graft healing. United Nations projections show that the global population aged 65 and older will reach 1.5 billion by 2050, locking in long-term demand.

Clinical Advantage of Graft-Less, Immediate-Loading Rehabilitation

Pooled analyses published by the International Team for Implantology documented a 98.1% survival rate for immediately loaded zygomatic implants. Removing graft steps cuts operating-room time up to 40% and eliminates graft material costs. A 2024 prospective study achieved 100% survival for Straumann’s ZAGA implants over 46.5 months, validating predictable outcomes when anatomical protocols are followed.[2]Straumann, “ZAGA Zygomatic Implant System Clinical Data,” Straumann.com Economic and clinical benefits continue to push immediate loading toward mainstream dominance.

Adoption of Digital Dentistry

Cone-beam CT, CAD-CAM, and dynamic navigation have transformed planning accuracy, reducing angular deviation to under 2° and trimming average surgery time by 18 minutes. Platforms from Straumann, Nobel Biocare, and ZimVie deliver cloud-based planning with 3D-printed guides, accelerating surgeon onboarding. High equipment costs still limit penetration in price-sensitive markets, creating a digital divide between premium urban clinics and resource-constrained settings.

Quad-Zygomatic Protocols Expanding Eligible Patient Pool

Long-term cohort data showed 97.7% implant survival and 98.2% prosthetic success for quad-zygomatic cases, extending fixed rehabilitation to patients once considered untreatable. Training academies operated by Straumann and Nobel Biocare certify surgeons, and the FDA explicitly labeled NobelZygoma for quad indications in 2025, signaling regulatory confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedural & Implant Costs | -0.9% | Global, acute in emerging markets with limited coverage | Long term (≥ 4 years) |

| Steep Surgical Learning Curve & Limited Specialist Base | -1.1% | APAC, Latin America, MEA regions with sparse training infrastructure | Long term (≥ 4 years) |

| Post-Operative Sinusitis Management Burden | -0.5% | Global clinical concern | Medium term (2-4 years) |

| Regulatory Ambiguity on Extra-Maxillary Devices | -0.4% | Emerging APAC, Latin America, MEA markets | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High Procedural & Implant Costs

One arch of zygomatic rehabilitation in North America ranges from USD 15,000 to USD 40,000, 150-200% above standard implant therapy. Major insurers such as Cigna limit coverage to cancer, congenital defects, or trauma, excluding periodontal disease in most circumstances.[3]Cigna, “Medical Coverage Policy: Dental Implants,” Cigna.com Patients seek lower-cost destinations abroad, but cross-border care complicates follow-up and warranty enforcement.

Steep Surgical Learning Curve & Limited Specialist Base

Comprehensive credentialing programs require cadaver labs, live-patient mentoring, and significant tuition, restricting the global pool of trained surgeons. Operators with fewer than 20 zygomatic cases observe sinusitis in over 20% compared with 10% among high-volume surgeons. Limited expertise hampers adoption in emerging regions.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Zygomatic Dominance Anchors Full-Arch Protocols

Zygomatic implants held 74.02% of 2025 revenue, anchoring most full-arch cases and reinforcing the leadership of NobelZygoma and Straumann ZAGA. Pterygoid implants, while smaller, are expanding 7.29% a year as surgeons combine anterior zygomatic and posterior pterygoid fixation for balanced load distribution. Hybrid demand is set to keep pterygoid share climbing within the zygomatic and pterygoid implants market.

Increasing adoption of pterygoid fixtures reflects documented 95.6% six-year success and the desire to shorten cantilevers in full-arch prostheses. Ongoing training and digital guides are expected to narrow outcome gaps between the two product lines, sustaining healthy rivalry that benefits end users within the zygomatic and pterygoid implants market.

By Length of Implant: Extreme Atrophy Drives Demand for Extended Fixtures

Implants 31-50 mm accounted for 47.87% of 2025 placements, yet lengths above 50 mm are rising fastest at a 9.93% CAGR. The zygomatic and pterygoid implants market share for long fixtures is climbing as clinicians treat patients with severe bone loss or post-oncology maxillectomy. Extended lengths provide bicortical anchorage and exceed 35 N cm insertion torque, prerequisites for immediate loading in the zygomatic and pterygoid implant markets.

Longer implants, offered up to 60 mm by NobelZygoma TiUltra, suit anatomies with aggressive sinus pneumatization. Growth in this category underscores surgeons’ confidence in digital navigation to accurately traverse complex trajectories without breaching critical structures.

By Application: Severe Atrophy Gains Momentum

Maxillary-sinus indications still commanded 56.72% of 2025 revenue; however, severe atrophy cases are expanding 8.43% yearly as clinicians extend graft-less therapy to edentulous and post-trauma patients. The zygomatic and pterygoid implants market size for severe atrophy is projected to overtake sinus procedures early in the next decade.

Guidelines now encourage use in patients contraindicated for grafting because of diabetes, smoking or bisphosphonate therapy. Wider indication breadth widens the addressable patient pool and diversifies revenue streams within the zygomatic and pterygoid implants market.

By Procedure Approach: Immediate Loading Becomes Standard

Immediate loading accounted for 61.08% of 2025 procedures and is growing at 7.68% per year, with a documented 98% survival. Surgeons leverage high primary stability and digital occlusal guidance to place fixed provisional prostheses within 24 hours, elevating patient satisfaction and clinic productivity in the zygomatic and pterygoid implants market.

Delayed loading remains for low-torque or high-risk cases, but its 39% share is expected to erode as confidence in immediate-function protocols solidifies. Manufacturers continue to position surface-treated implants and multi-unit abutments expressly for same-day teeth, deepening the trend toward immediate loading.

By End User: Outpatient Settings Accelerate

Hospitals held 54.18% of 2025 cases, reflecting their capacity to manage comorbidities under general anesthesia. Ambulatory surgical centers are growing fastest, with a 8.79% CAGR, aided by increased U.S. Medicare facility fees for complex dental rehabilitation. Supportive reimbursement is enabling same-day discharge models that suit immediate-function zygomatic workflows in the zygomatic and pterygoid implants market.

Dental clinics represent a smaller yet specialized tier where office-based anesthesia is permitted and high-end imaging is available. Continuous expansion of CBCT ownership will gradually elevate clinic participation.

Geography Analysis

North America contributed 41.23% of 2025 value to the zygomatic and pterygoid implants market. Favorable oncology reimbursement, dense continuing-education networks, and high disposable incomes sustain premium adoption. U.S. private insurers cover cancer-related cases, while Canada’s provincial plans subsidize medically necessary reconstructions, creating steady volume.

Europe ranks second. Harmonized CE-marking under MDR eases multicountry rollout; Germany, France, and the United Kingdom anchor core demand, while Spain and Hungary attract cross-border patients seeking 30-50% fee reductions. Currency stability and widespread acceptance of immediate-load dentistry underpin resilient growth despite macroeconomic pressures.

Asia-Pacific is the fastest-growing territory, expanding 9.63% annually. Urban China and India generate sheer volume, whereas Japan and South Korea capture premium case values. Thailand and Singapore leverage medical tourism frameworks, promoting bundled packages that include CBCT, implant surgery, and prosthetic delivery in a single trip, strengthening regional contributions to the zygomatic and pterygoid implants market.

Middle East & Africa present concentrated demand pockets, especially among affluent populations in the Gulf Cooperation Council. Government-funded specialty centers in the United Arab Emirates and Saudi Arabia are recruiting European-trained surgeons to run digital implant suites. South America’s upswing is paced by Brazil’s large private dental sector and Argentina’s cost-competitive clinics, which are drawing Chilean clients, though currency volatility tempers momentum.

Competitive Landscape

The top five suppliers, Straumann, Nobel Biocare (Envista), Dentsply Sirona, Zimmer Biomet, and Osstem, command a significant portion of global dental-implant revenue, giving them resources to fund training academies, digital workflows, and post-market surveillance. Straumann’s ZAGA Academy and Nobel Biocare’s Zygoma Academy credential thousands of surgeons each year, locking participants into their respective ecosystems. Dentsply Sirona’s 2024 financial filing revealed USD 973 million in implant-segment sales, down year-on-year due to pricing pressure and competitive discounting.

ZimVie invested USD 26.9 million in R&D and launched the Implant Concierge workflow, signaling a pivot toward software-driven differentiation. Lower-priced Asian manufacturers such as Osstem and Noris Medical are gaining traction in price-sensitive markets, forcing incumbents to defend share with proprietary surface treatments and comprehensive warranties. Regulatory clarity arrived in August 2025 when the FDA cleared NobelZygoma TiUltra via 510(k), proving that predicate evidence can secure approval for extra-maxillary devices. Digital-native startups offering AI planning that works across implant brands may disrupt entrenched ecosystems, encouraging open-platform collaboration.

Zygomatic And Pterygoid Implants Industry Leaders

Noris Medical

S.I.N. Implant System

Southern Implants

Straumann Holding AG

IDC Implant & Dental Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Proclaim raised capital to scale its Custom-Jet Oral Health System, enrolling 700+ practices.

- January 2025: Nuvia Dental Implant Center earned 2024 recognition for its “permanent teeth in 24 hours” protocol.

- December 2024: Patient Square Capital acquired Patterson Companies for USD 4.1 billion with intentions to take the distributor private at a 49% shareholder premium.

- October 2024: FDA issued comprehensive guidelines on endosseous dental implants and abutments, defining safety-based performance criteria and streamlining 510(k) pathways.

- August 2024: Perceptive showcased the first fully automated dental procedure using AI robotics, reaching 90% cavity-detection accuracy and cutting chair time to 15 minutes.

- July 2024: Henry Schein bought abc dental AG for USD 27.5 million to deepen presence in French and German-speaking markets.

Global Zygomatic And Pterygoid Implants Market Report Scope

As per the scope of the report, zygomatic and pterygoid implants are a unique option for the upper jaw when there is significant bone loss. Zygomatic and pterygoid implants anchor in the jawbone and the bone behind the upper jaw, as opposed to normal dental implants, which do so in the jawbone.

The Zygomatic and Pterygoid Implants Market Report is Segmented by Product Type (Zygomatic Implants, Pterygoid Implants), Length of Implant (Up to 30 mm, 31-50 mm, Above 50 mm), Application (Severe Atrophy of Maxillary Bone, Maxillary Sinuses, Trauma & Other Indications), Procedure Approach (Immediate Loading, Delayed Loading), End User (Hospitals, Dental Clinics, Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Zygomatic Implants |

| Pterygoid Implants |

| Up to 30 mm |

| 31 – 50 mm |

| Above 50 mm |

| Severe Atrophy of Maxillary Bone |

| Maxillary Sinuses |

| Trauma & Other Indications |

| Immediate Loading |

| Delayed Loading |

| Hospitals |

| Dental Clinics |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Zygomatic Implants | |

| Pterygoid Implants | ||

| By Length of Implant | Up to 30 mm | |

| 31 – 50 mm | ||

| Above 50 mm | ||

| By Application | Severe Atrophy of Maxillary Bone | |

| Maxillary Sinuses | ||

| Trauma & Other Indications | ||

| By Procedure Approach | Immediate Loading | |

| Delayed Loading | ||

| By End User | Hospitals | |

| Dental Clinics | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the zygomatic and pterygoid implants market today?

The zygomatic and pterygoid implants market size was USD 0.26 billion in 2025 and is set to reach USD 0.38 billion by 2031.

Which product type dominates sales?

Zygomatic implants commanded 74.02% of 2025 revenue, maintaining leadership over pterygoid systems.

What region grows fastest through 2031?

Asia-Pacific is projected to expand at a 9.63% CAGR, outpacing all other geographies.

Why is immediate loading preferred?

Immediate loading shows 98% survival, delivers same-day teeth and cuts treatment time, driving 61.08% of 2025 procedures.

How are regulatory agencies treating these devices?

The FDA requires traditional 510(k) evidence, as shown by NobelZygoma TiUltra’s 2025 clearance, affirming predicate-based pathways.

Page last updated on: