Abutment Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

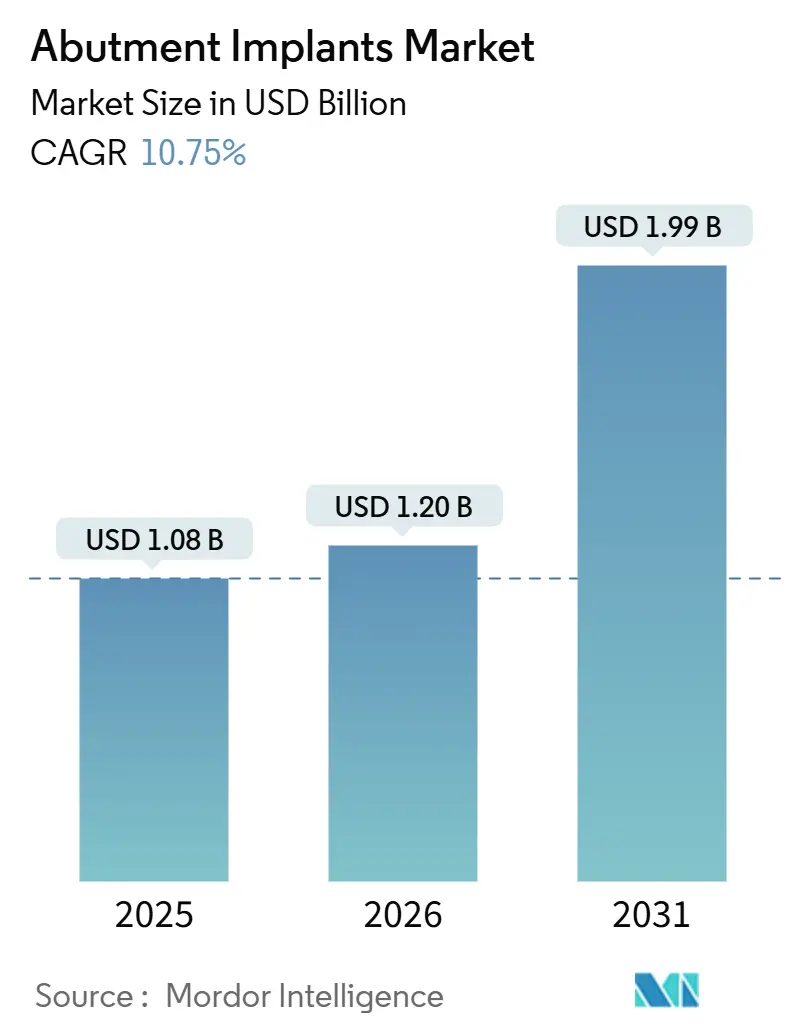

| Market Size (2026) | USD 1.20 Billion |

| Market Size (2031) | USD 1.99 Billion |

| Growth Rate (2026 - 2031) | 10.75% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Abutment Implants Market Analysis by ���ϲ�����

The Abutment Implants Market size was valued at USD 1.08 billion in 2025 and is estimated to grow from USD 1.20 billion in 2026 to reach USD 1.99 billion by 2031, at a CAGR of 10.75% during the forecast period (2026-2031).

Elevated life expectancy, the growing popularity of metal-free anterior restorations, and rapid uptake of digital dentistry are widening the patient pool while shortening treatment timelines. Leading manufacturers now prioritize vertically integrated production and proprietary software ecosystems to lock in recurrent consumable sales, yet contract laboratories are simultaneously gaining bargaining power as design authority shifts away from chairside clinicians. Raw-material inflation of 12%–18% during 2024 compressed gross margins for titanium and zirconia suppliers, further encouraging diversification into polymer‐based abutments. In parallel, AI-assisted design tools have cut custom-abutment turnaround to 48 hours, encouraging same-day prosthetic delivery that differentiates urban clinics and spurs premium pricing.

Key Report Takeaways

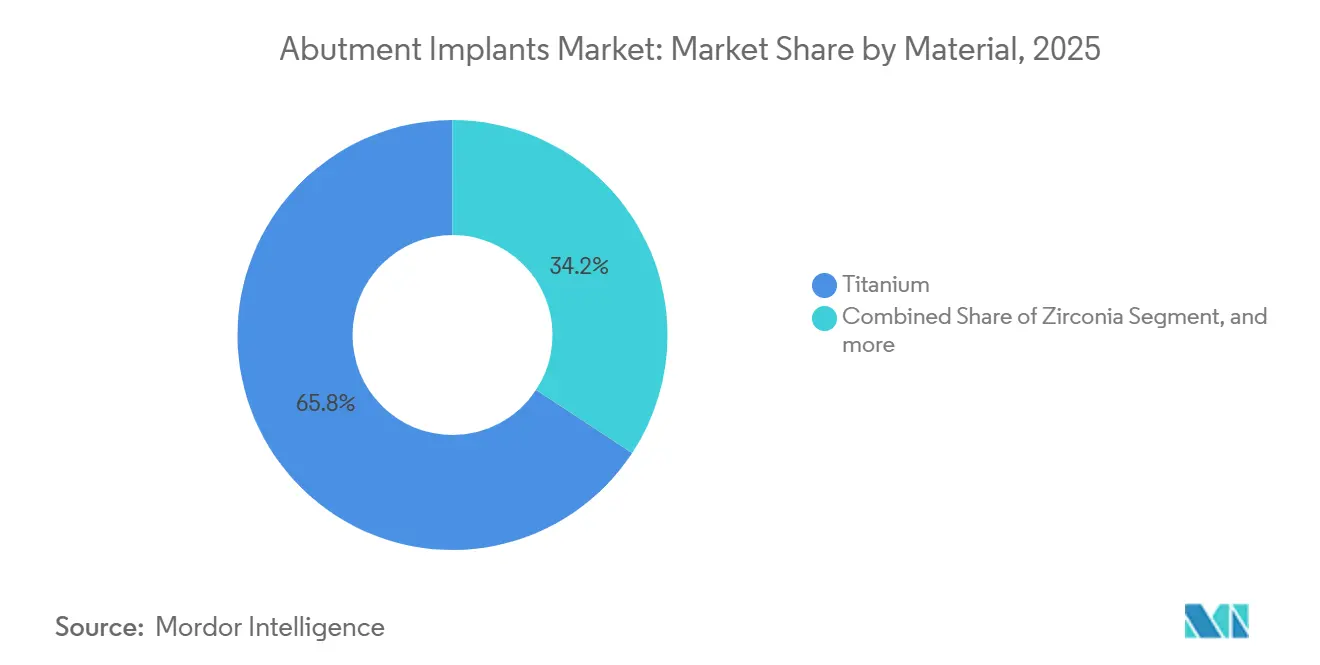

- By material, titanium led with 65.76% of abutment implants market share in 2025, whereas zirconia is set to advance at a 12.65% CAGR through 2031.

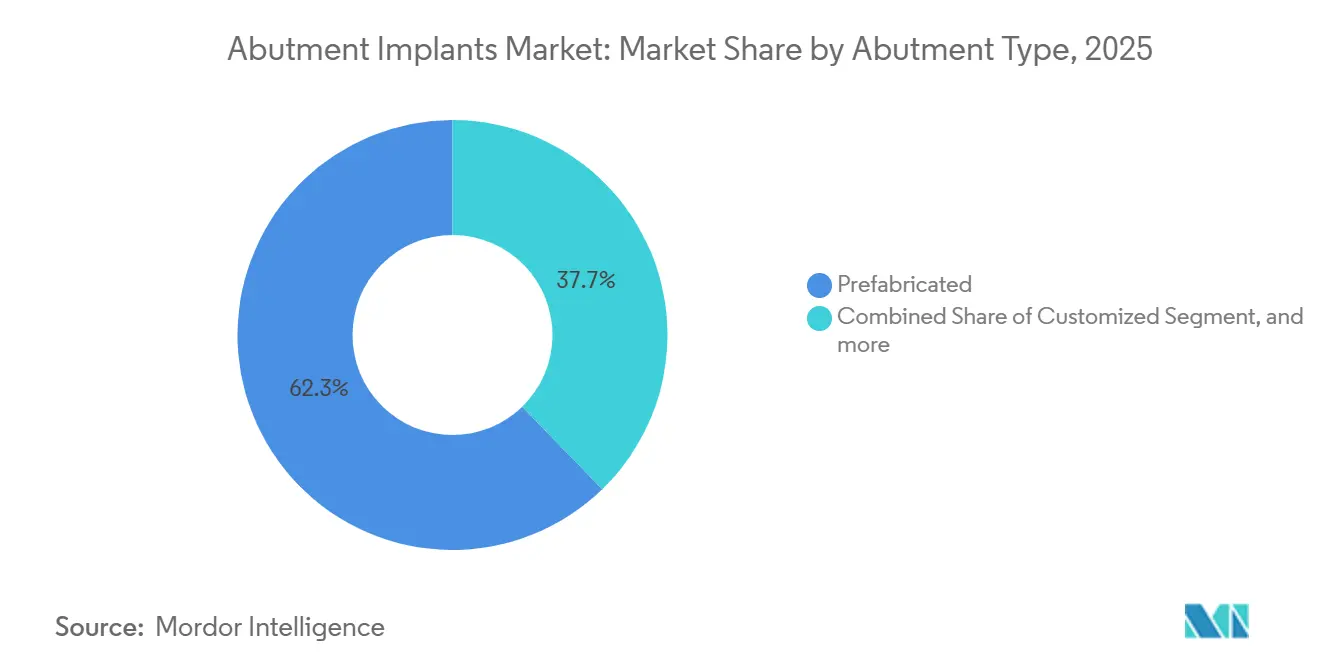

- By abutment type, prefabricated units held 62.26% share of the abutment implants market size in 2025 and customized variants are projected to grow at 13.44% CAGR to 2031.

- By end user, dental clinics captured 46.43% revenue share in 2025, while dental laboratories are forecast to expand at a 13.65% CAGR between 2026 and 2031.

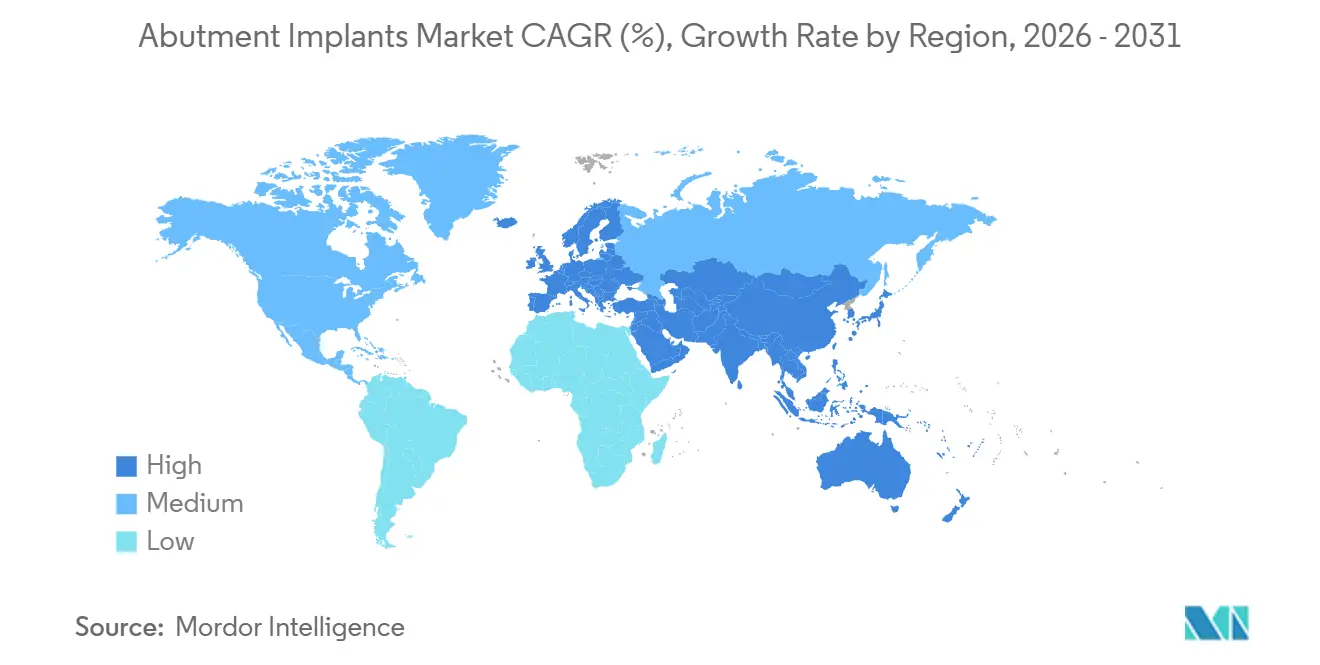

- By geography, North America dominated with 43.54% of abutment implants market share in 2025; Asia-Pacific is the fastest growing region at an 11.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Abutment Implants Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demographic Shift Toward Older Population | +2.1% | Global, with concentration in Japan, South Korea, Germany, and Italy | Long term (≥ 4 years) |

| Rising Demand For Aesthetic Restorations | +1.8% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Rapid Adoption Of Digital Dentistry Technologies | +2.4% | North America, Europe, Asia-Pacific core markets | Short term (≤ 2 years) |

| Expansion Of Insurance Coverage For Implant Procedures | +1.6% | United States (ACA expansion states), select European Union markets | Medium term (2-4 years) |

| Integration Of Artificial Intelligence In Custom Abutment Design | +1.3% | North America, Western Europe, Japan, South Korea | Short term (≤ 2 years) |

| Proliferation Of Low-Cost Polymer And PEEK Abutments In Emerging Markets | +1.2% | India, Southeast Asia, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Demographic Shift Toward Older Population

The global cohort aged 65 plus is expected to reach 1.6 billion by 2050, driving a sustained need for fixed restorations as edentulism rates remain 15%–25% in this group. China already hosts 280 million citizens aged 60 and over, while Japan’s super-aged society translates into per-capita implant use triple the world average. Older patients increasingly prefer multi-unit solutions that offer immediate function and fewer surgical visits, supporting premium pricing in the abutment implants market. Urban households earning above USD 30,000 annually further accelerate elective spending, particularly on full-arch restorations that require multiple abutments. Manufacturers respond with angulated multi-unit designs that simplify prosthesis delivery for mobility-impaired seniors.

Rising Demand for Aesthetic Restorations

Cosmetic dentistry revenue in the United States exceeded USD 18 billion in 2024, with anterior implants representing 35% of volume as patients prioritize smile esthetics. Zirconia abutments, priced 40%–60% above titanium, have gained momentum by eliminating gray metal shine through thin gingiva. Social-media influencers openly documenting smile makeovers normalize implant procedures for Millennials and Generation Z, channeling new demand into high-volume practices that negotiate bulk discounts while still growing average selling prices in the abutment implants market. Custom abutments that tailor emergence profiles now dominate anterior cases, improving papilla regeneration and soft-tissue support.

Rapid Adoption of Digital Dentistry Technologies

U.S. intraoral scanner penetration jumped from 48% in 2023 to 57% in 2024, trimming impression failures and enabling real-time abutment evaluation. Dental 3D printing, valued at USD 450.75 million in 2024, is projected to reach USD 1.12 billion by 2032, with abutment production comprising 22% of print jobs. Straumann’s iEXCEL platform integrates planning, design, and milling into a single interface, reinforcing ecosystem lock-in and securing consumable sales over the forecast period. Open-architecture rivals instead emphasize interoperability, dividing the competitive field along software-hardware alignment and influencing procurement preferences within the abutment implants market.

Expansion of Insurance Coverage for Implant Procedures

The April 2024 CMS rule allows U.S. states to add adult dental benefits to ACA plans starting in 2027, potentially covering 15–20 million new candidates for implant therapy. Private payers such as UnitedHealthcare now reimburse 50% of abutment costs after a waiting period, nudging bridge-first patients toward implant solutions. Although annual maximums still leave 60%–70% of treatment out of pocket, even partial coverage can expand the abutment implants market by 8%–12% in mature economies. Medical tourism fills reimbursement gaps elsewhere, especially in India where complete implant packages cost one-third of Western prices.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Cost And Limited Reimbursement In Developing Regions | -1.9% | India, Southeast Asia, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Insufficient Skilled Dental Implant Workforce | -1.4% | United States, United Kingdom, Germany, rural Asia-Pacific | Medium term (2-4 years) |

| Increasing Incidence Of Peri-Implant Diseases | -1.1% | Global, with higher rates in smokers and diabetic populations | Medium term (2-4 years) |

| Supply Chain And Sustainability Challenges For Titanium And Zirconia | -0.8% | Global, acute in regions dependent on single-source suppliers | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

High Treatment Cost and Limited Reimbursement in Developing Regions

Complete implant therapy costs USD 2,500–5,000 in developed markets but only USD 600–1,200 in India and Turkey, still unaffordable for vast populations earning below USD 2,000 per capita[1]World Bank, “GDP per Capita Indicators,” worldbank.org . Public schemes in Brazil and South Africa exclude implants, confining adoption to self-pay urban elites. Micro-credit options exist yet default rates of 8%–12% deter widespread rollout, constraining addressable demand for the abutment implants industry in lower-income nations.

Insufficient Skilled Dental Implant Workforce

The United States will require an extra 10,000 dentists by 2030, but specialty training pipelines graduate just 350 prosthodontists per year. Europe confronts similar shortages amid aging clinician pools and restrictive cross-border licensing. Limited expertise raises procedure costs and elongates waiting lists, slowing growth of the abutment implants market in underserved areas despite latent demand.

Segment Analysis

By Material: Zirconia Gains on Aesthetic Imperative

Zirconia will grow at a 12.65% CAGR, outpacing the broader abutment implants market as patients accept 40%–60% premiums for translucency that eliminates the gray shine of titanium in the smile zone. Titanium retained 65.76% share in 2025 due to decades of posterior load success and compatibility with the installed base. PEEK addresses low-income needs, especially in India and Southeast Asia, yet remains a niche area with scant long-term evidence. Hybrid metal-ceramic laminates aim to combine strength and esthetics but face multi-year regulatory hurdles before influencing the abutment implants market.

Titanium’s ductility still dominates screw-retained full-arch protocols by preventing fracture under torque, while zirconia thrives in anterior cementless workflows that favor soft-tissue health. Polymer uptake sits at the intersection of affordability and radiolucency advantages although limited color options confine it to non-esthetic sites. Manufacturers continue R&D into surface textures that reduce bacterial adhesion, yet any breakthrough faces strict biocompatibility trials before reshaping the abutment implants market share.

Note: Segment shares of all individual segments available upon report purchase

By Abutment Type: Customization Accelerates with Digital Workflows

Customized abutments are forecast to expand 13.44% CAGR as intraoral scanning and AI design platforms slash delivery to 48 hours, freeing clinic capital and enabling same-day smiles. Prefabricated units still held 62.26% share in 2025 because of ready inventory, lower unit cost, and simplicity in posterior cases. Multi-unit abutments, critical for All-on-4-style rehabilitations, command USD 200–400 per piece and rely on precision machining, which narrows supplier pools.

Clinicians adopt definitive abutment placement during initial surgery, shrinking the role of healing abutments, reducing total component spend per case, and raising value for high-margin custom parts. Chinese-made prefabs priced 60% below Western brands pressure loyalty in price-sensitive regions, but established players defend share with digital workflows that integrate seamlessly into practice management ecosystems across the abutment implants market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Facility: Laboratories Gain Design Authority

Dental laboratories will post a 13.65% CAGR through 2031 as design control migrates from chairside clinicians to CAD technicians who manipulate margin lines and emergence profiles. Dental clinics retained 46.43% share in 2025 as primary surgical sites but increasingly outsource design, concentrating on placement and final torque. Hospitals manage medically complex cases, while academic centers shape future product innovation rather than immediate volume.

Laboratories in tier-2 cities harness subscription AI platforms for USD 500–1,200 monthly, enabling 30–40 abutment designs per day and increasing throughput by 8x. Clinics benefit from reduced chairside adjustments, but laboratories capture a larger slice of abutment implants market revenue by selling high-precision custom pieces directly to dentists.

Geography Analysis

North America accounted for 43.54% of global revenue in 2025, driven by about 5.5 million annual placements in the United States. Consolidation of Dental Service Organizations, now controlling 64% of U.S. practice revenue, unlocks volume-rebate deals but squeezes supplier margins. The 2027 rollout of adult dental benefits under ACA could add up to 20 million eligible implant candidates, expanding multi-unit demand targeted at the Medicare-eligible segment[2]. Canada lags due to limited public reimbursement, whereas Mexican border clinics thrive on U.S. cross-border traffic, though many patients return home for restorative stages, limiting local abutment uptake.

Asia-Pacific leads growth at 11.54% CAGR as China’s 280 million seniors and India’s burgeoning middle class boost elective care spending. Japan’s implant density is triple the global average, yet mature penetration tempers incremental growth. South Korea’s >70% CAD/CAM penetration enables same-day abutments, exemplifying digital leadership. Domestic brands Osstem and MegaGen undercut Western prices by 30%–40%, prompting Straumann to open its 2026 Neodent facility in Brazil to replicate cost advantages regionally, but it still faces fierce local competition across Asia-Pacific.

Europe ranks second by value, with Germany alone placing 1.3 million implants in 2024 under a co-payment regime that covers 50% of standard prosthetics but excludes fixtures and abutments. The EU Medical Device Regulation imposes strict post-market surveillance, favoring established manufacturers who can absorb compliance costs. Eastern Europe attracts budget-minded Western Europeans for discounted treatments, yet language and quality variability limit the flow to border regions, capping gains in the abutment implants market.

The Middle East & Africa and South America remain nascent, with penetration under 5% among edentulous populations. GCC states support premium clinics but generate modest unit volumes. Brazil dominates South America; Straumann’s Brazilian plant should secure supply chain resilience and price competitiveness despite local currency swings. South African private clinics cater to regional tourists, yet political volatility deters large-scale capital investment in the abutment implants market.

Competitive Landscape

Straumann, Dentsply Sirona, Envista, and Zimmer Biomet together commanded roughly 55%–60% global revenue in 2025, reflecting moderate consolidation. Straumann posted CHF 585.5 million (USD 660 million) in implant sales in Q3 2024, driven by its iEXCEL digital ecosystem, which embeds recurring revenue streams. Dentsply Sirona suffered a slide to USD 158 million in the same quarter and wrote down USD 359 million in goodwill, underscoring the gap between digital leaders and laggards. Envista’s Nobel Biocare regained share in Europe through new launches, while Zimmer Biomet secured FDA clearance for a surface-enhanced TSV system, reducing healing time to eight weeks.

Regional challengers such as Osstem and MegaGen leverage 30%-plus price advantages in Asia-Pacific, whereas BioHorizons gains traction in North America with tapered threads optimized for soft bone. Polymer entrants focus on emerging markets where cost sensitivity is highest. Suppliers now bundle scanners, design software, milling units, and implants to create switching costs, mimicking enterprise IT models. DSOs amplify this dynamic by negotiating platform-wide deals, compelling smaller vendors to differentiate via open-architecture interoperability within the abutment implants market.

Abutment Implants Industry Leaders

Nobel Biocare

Dentsply Sirona

Straumann Group

Envista

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Kuraray Noritake Dental launched KATANA Zirconia ONE For IMPLANT, a pre-sintered zirconia block designed for use with CEREC systems.

- May 2025: Dentsply Sirona introduced the CEREC Cercon 4D Multidimensional Zirconia Abutment Block—an innovative CAD/CAM zirconia block that combines high strength with esthetics for both hybrid abutments and hybrid abutment crowns.

Global Abutment Implants Market Report Scope

As per the scope of this report, Abutment is a metal connector that a dental professional installs into the patient's dental implant for healing from dental surgery.

The Abutment Implants Market is segmented by Type (Prefabricated Abutment systems and Custom Abutment Systems) and Geography (North America, Europe, Asia-Pacific, and the Rest of the World). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Titanium |

| Zirconia |

| Peek & High-Performance Polymers |

| Hybrid/Composite Alloys |

| Prefabricated |

| Customized |

| Healing |

| Multi-Unit |

| Academic & Research Institutes |

| Dental Clinics |

| Dental Laboratories |

| Hospitals & Surgery Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Titanium | |

| Zirconia | ||

| Peek & High-Performance Polymers | ||

| Hybrid/Composite Alloys | ||

| By Abutment Type | Prefabricated | |

| Customized | ||

| Healing | ||

| Multi-Unit | ||

| By End-User Facility | Academic & Research Institutes | |

| Dental Clinics | ||

| Dental Laboratories | ||

| Hospitals & Surgery Centers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will global spending on abutment components become by 2031?

The abutment implants market size is forecast to reach USD 1.99 billion by 2031, reflecting a 10.75% CAGR from 2026.

Which material is gaining traction for anterior implant restorations?

Zirconia is expanding the fastest at a 12.65% CAGR thanks to superior esthetics and soft-tissue response.

What impact will U.S. insurance changes have on demand?

ACA adult dental coverage starting in 2027 could add up to 20 million insured candidates, enlarging the addressable patient pool for multi-unit restorations.

Why are dental laboratories growing faster than clinics?

Digital impressions and AI design tools let labs control abutment geometry and cut delivery times to 48 hours, driving a 13.65% CAGR through 2031.

Which region will see the quickest revenue growth?

Asia-Pacific leads with an 11.54% CAGR as China's aging society and India's middle class boost elective implant uptake.

How are supply-chain risks being managed by manufacturers?

Companies like Straumann are regionalizing production—e.g., a new Brazilian plant—to reduce tariff exposure and titanium price volatility.