Subdermal Contraceptive Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

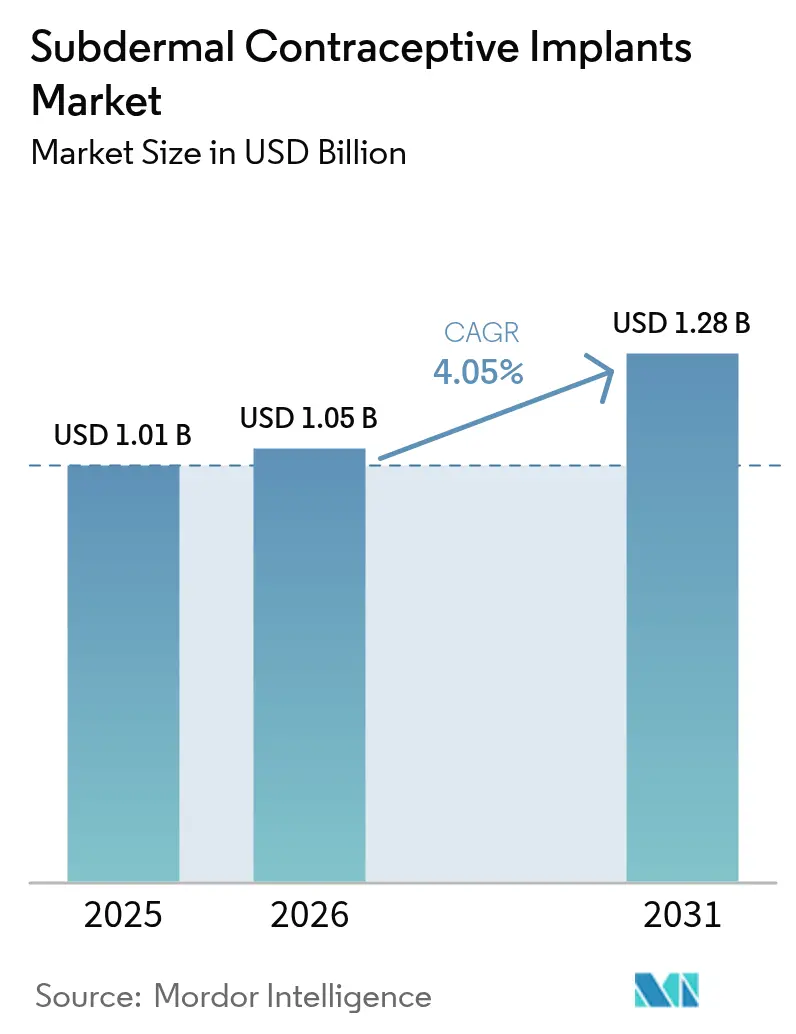

| Market Size (2026) | USD 1.05 Billion |

| Market Size (2031) | USD 1.28 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Subdermal Contraceptive Implants Market Analysis by ���ϲ�����

The Subdermal Contraceptive Implants Market size was valued at USD 1.01 billion in 2025 and is estimated to grow from USD 1.05 billion in 2026 to reach USD 1.28 billion by 2031, at a CAGR of 4.05% during the forecast period (2026-2031).

Escalating unintended pregnancy rates, widening reimbursement for long-acting reversible contraception (LARC), and steady procurement by multilateral health agencies keep baseline demand resilient even as donor-funded volumes plateau. High concentration around Organon’s Nexplanon franchise sustains premium pricing in North America, whereas double-rod levonorgestrel generics underpin large public tenders in sub-Saharan Africa and South Asia. Technology upgrades, such as ultra-thin applicators and digital insertion logs, reduce malposition risk, broadening the provider base beyond obstetricians. Patent expiry from 2027 ushers in biosimilar competition that will compress average selling prices in high-income regions but expand total user access in emerging markets.

Key Report Takeaways

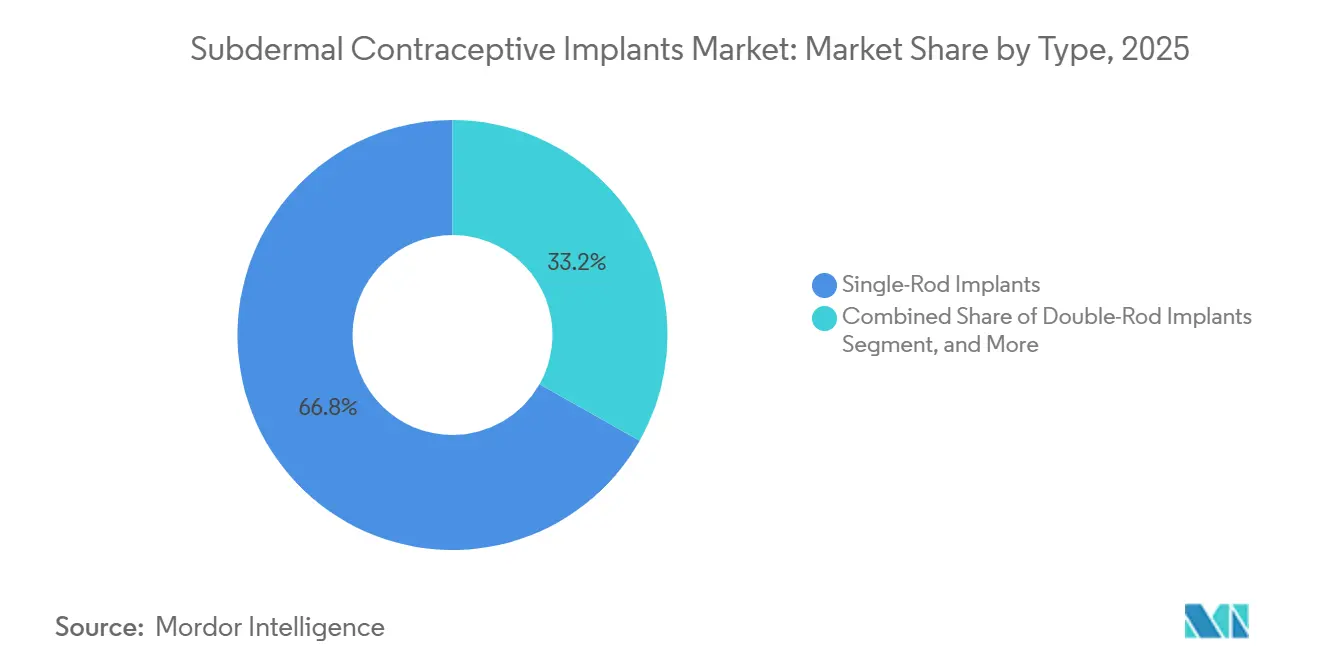

- By type, single-rod etonogestrel devices held 66.82% of the subdermal contraceptive implants market share in 2025, whereas double-rod systems are forecast to advance at a 5.09% CAGR to 2031.

- By hormone, etonogestrel commanded 70.27% revenue share in 2025, while levonorgestrel formulations are projected to post a 6.94% CAGR over 2026-2031.

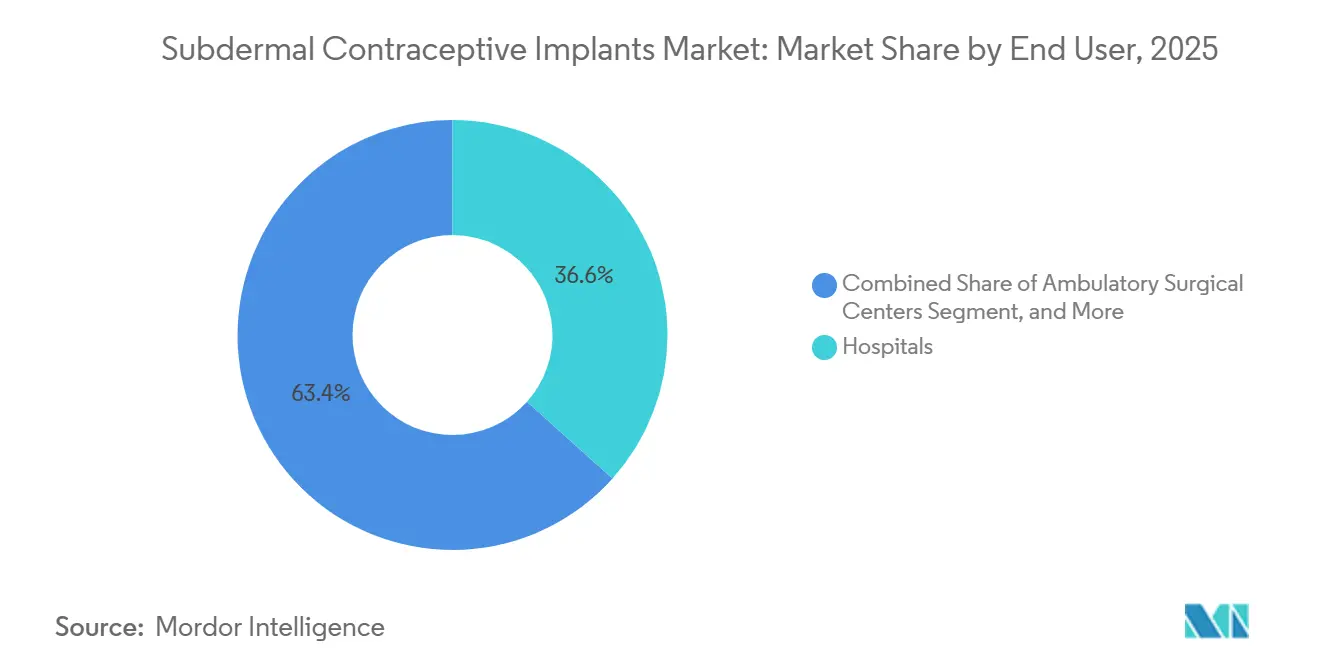

- By end user, hospitals captured 36.63% of 2025 sales, yet family-planning centers are expanding fastest at a 5.82% CAGR through 2031.

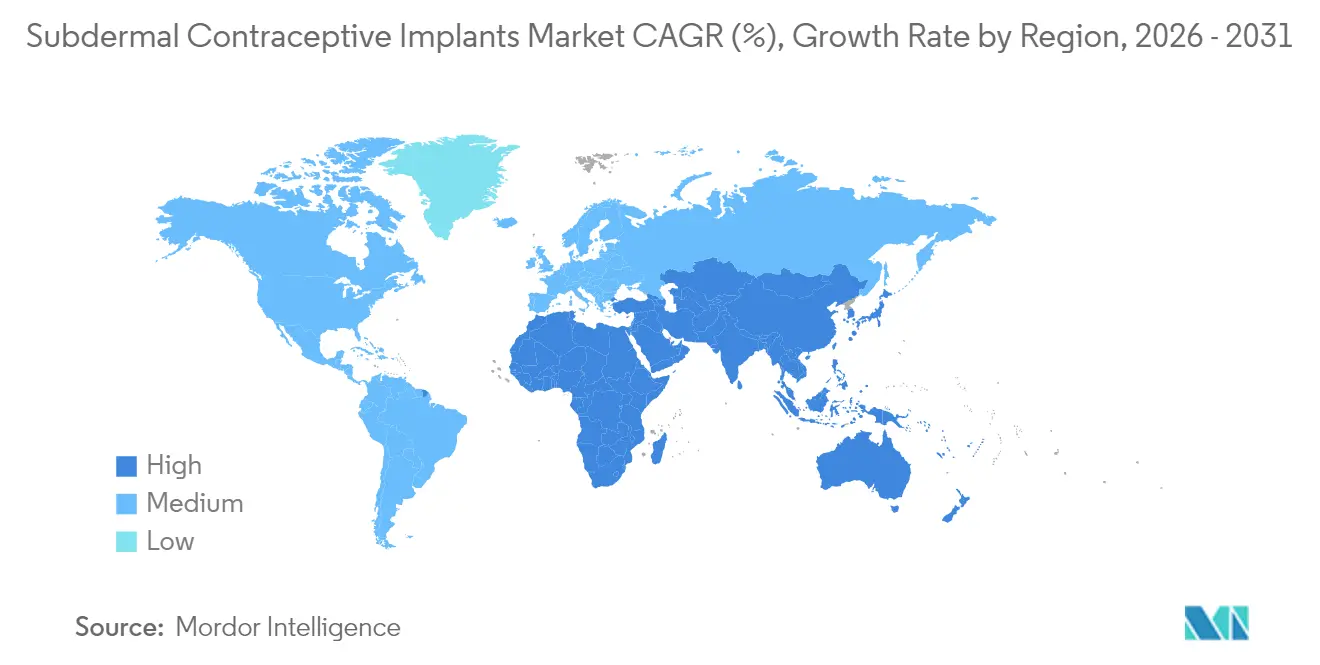

- By geography, North America led with a 45.08% revenue share in 2025; Asia-Pacific is the fastest-rising region, with a 7.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Subdermal Contraceptive Implants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Unintended Pregnancy Rates & Demand for LARC | +1.0% | Global, with acute unmet need in Sub-Saharan Africa, South Asia, and Latin America | Long term (≥ 4 years) |

| Favorable Government Family-Planning Initiatives & Subsidies | +0.8% | APAC (India, Indonesia, Philippines), Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Superior Efficacy & Cost-Effectiveness of Implants | +0.6% | Global, with highest impact in OECD markets where health-economic evaluations drive formulary inclusion | Long term (≥ 4 years) |

| Growing NGO Procurement in Emerging Markets | +0.5% | Sub-Saharan Africa, South Asia, Southeast Asia, with UNFPA and USAID-funded programs | Medium term (2-4 years) |

| Miniaturized Ultra-Thin Single-Insertion Devices | +0.4% | North America & Europe, with spillover to urban centers in APAC and Latin America | Short term (≤ 2 years) |

| Digital Insertion-Tracking Apps Boost Provider Confidence | +0.3% | North America, Western Europe, urban APAC markets with established digital health infrastructure | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rising Unintended Pregnancy Rates & Demand for LARC

Global unintended pregnancies totaled 121 million in 2024, representing 48% of all pregnancies, and 257 million women in low- and middle-income countries still lack access to modern methods.[1]United Nations Population Fund, “State of World Population 2024,” unfpa.org Long-acting reversible options already account for 21% of modern method use, up from 16% in 2019, because users prefer “set-and-forget” protection without daily adherence burdens. Ministries of health now channel up to 50% of contraceptive budgets to implants and intrauterine devices, recognizing that a single USD 15 donor-priced implant averts more pregnancies over three years than 36 cycles of oral pills costing USD 1.50 each. Uptake among adolescents and women with no prior births is rising, challenging earlier clinical norms and expanding the overall addressable pool. These dynamics underpin enduring demand for the subdermal contraceptive implants market during and beyond the forecast horizon.

Favorable Government Family-Planning Initiatives & Subsidies

India’s Mission Parivar Vikas trained 50,000 auxiliary nurse midwives and achieved 2.1 million insertions in fiscal 2024 after waiving user fees.[2]Government of India Ministry of Health and Family Welfare, “Mission Parivar Vikas Annual Report 2024,” mohfw.gov.in Indonesia’s universal health coverage reimburses USD 25 per insertion, triple the rate for injectables, to nudge providers toward LARC, resulting in 1.8 million implants procured in 2024. The Philippines secured USD 120 million in Asian Development Bank financing to distribute 1.5 million implants through rural health units, aiming to increase modern prevalence by 10 percentage points by 2028. These initiatives shorten manufacturers' payback periods and spur localized production, thereby fueling medium-term growth in the subdermal contraceptive implants market.

Superior Efficacy & Cost-Effectiveness of Implants

Subdermal implants post a Pearl Index below 0.05, far outperforming oral pills (9.0) or injectables (6.0). A 2024 cost-utility study calculated 2.8 quality-adjusted life years per 1,000 users for implants versus 1.2 for pills, supporting full reimbursement in Medicaid programs and European health systems. Immediate postpartum insertion saves USD 12,000 in avoidable pregnancy costs within 18 months, prompting 23 U.S. states to mandate coverage. These economics continue to attract payers and keep efficacy a central pillar of the subdermal contraceptive implants industry’s value proposition.

Miniaturized Ultra-Thin Single-Insertion Devices

Bayer’s Nexplanon NXT shrank applicator diameter to 2.1 millimeters and cut insertion time by one-third, slashing malposition from 1.2% to 0.3% across 15,000 post-launch procedures. Malpractice insurers in the United States now offer 15% premium discounts to clinics adopting the upgrade, widening the provider pool to nurse practitioners and physician assistants. Shanghai Dahua’s 1.8-millimeter levonorgestrel prototype under telehealth supervision aims to serve rural China by 2027, foreshadowing expanded market reach. Such design refinements lower training burdens and litigation risk, reinforcing positive sentiment for short-term adoption in the subdermal contraceptive implants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-Event Concerns & Litigation | -0.7% | North America & Europe, spillover in APAC | Medium term (2-4 years) |

| High Upfront Cost in Out-of-Pocket Markets | -0.5% | Latin America, Middle East, APAC | Long term (≥ 4 years) |

| Cold-Chain Constraints in Tropical Regions | -0.4% | Sub-Saharan Africa, Southeast Asia, tropical Latin America | Long term (≥ 4 years) |

| Religious Activist Opposition to Hormonal Contraception | -0.3% | Philippines, parts of Latin America & Africa | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Adverse-Event Concerns & Litigation

Consolidated lawsuits covering 3,200 injury claims prompted Organon and Bayer to reserve USD 150 million for settlements in 2024.[3]United States Courts, “Nexplanon Litigation Filings 2024,” uscourts.gov The U.K. regulator now requires ultrasound confirmation within 48 hours, adding USD 50 compliance cost per case. Rising malpractice premiums forced 12 U.S. states’ ambulatory centers to discontinue implant services, lengthening rural wait times to eight weeks. Although redesigned applicators cut malposition dramatically, ongoing litigation tempers provider enthusiasm and weighs on the subdermal contraceptive implants market CAGR.

High Upfront Cost in Out-of-Pocket Markets

Retail prices of USD 800-1,000 at private Latin American and Middle Eastern clinics equal up to 4 months of household income. Brazil’s 2024 household survey found 62% of women citing cost as the key barrier to switching from pills to implants. Generic alternatives at USD 50-80 remain unevenly distributed; only 15% of Mexico City pharmacies stocked them in mid-2024. Micro-finance pilots raised uptake among low-income Kenyan and Bangladeshi women to 40%, yet scale-up awaits stronger mobile-money ecosystems. Upfront affordability, therefore, caps penetration, especially outside subsidized public tenders, dampening long-term growth prospects for the subdermal contraceptive implants industry.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Double-Rod Systems Gain Ground

Double-rod levonorgestrel implants are projected to expand at a 5.09% CAGR through 2031, outpacing the overall subdermal contraceptive implants market size for this metric. These systems benefit from unit prices of USD 8-10 in donor tenders, versus USD 12-15 for single-rod generics. Shanghai Dahua’s Sino-implant (II) secured a 4.5-million-unit contract with Nigeria in 2024, demonstrating momentum in budget-constrained settings. Single-rod etonogestrel devices still dominate premium segments, maintaining 66.82% market share in 2025 owing to Organon’s entrenched training network and malpractice offsets. As biosimilars launch post-2027, price gaps between rod formats will narrow, and convenience features could re-shape the competitive hierarchy within the subdermal contraceptive implants market.

The cost-performance trade-off also influences procedural logistics: double-rod insertion requires a 4-millimeter incision and longer chair time, which mildly elevates infection risk. Yet public programs prioritize budget impact over marginal convenience, ensuring continued tender dominance. Venture-backed biodegradable polymer implants, currently under 2% share, attracted USD 45 million in 2024 funding, hinting at a future pivot toward removal-free platforms. Collectively, these factors will guide procurement decisions and sustain diversified growth avenues within the subdermal contraceptive implants industry.

By Hormone: Levonorgestrel Formulations Accelerate

Etonogestrel systems accounted for 70.27% of revenue in 2025, but levonorgestrel implants are forecast to grow at a 6.94% CAGR through 2031, surpassing overall subdermal contraceptive implants market growth. Lower API costs USD 180/kg for levonorgestrel versus USD 420 for etonogestrel, and a five-year duration bolsters their adoption in settings where follow-up access is limited. India’s Antara program alone distributed 2.1 million units in fiscal 2024 at a negotiated price of USD 6.80. Clinical efficacy remains near-equivalent; both hormones carry WHO Category 1 eligibility, though levonorgestrel shows slightly higher irregular bleeding (35% vs 28%) according to a 2024 Cochrane review.

Forthcoming etonogestrel biosimilars will compress North American price premiums, and differentiation will hinge more on applicator ergonomics and digital tracking than on hormone selection. Indonesia’s 2024 tender already shifted 60% of volumes to levonorgestrel, signaling accelerating momentum. Overall, hormone choice will continue to influence formulary decisions and shape market share trajectories within the subdermal contraceptive implants market size discussion.

By End User: Family-Planning Centers Surge

Hospitals accounted for 36.63% of revenue in 2025, leveraging immediate postpartum insertion reimbursement codes. Nonetheless, specialized family-planning centers are advancing at a 5.82% CAGR, the highest among all channels, aided by bundled payments of USD 650 that cover counseling and 12-month follow-up. These clinics report 85% 12-month continuation, compared with 68% in general OB-GYN practices, highlighting service-delivery advantages. Planned Parenthood saw a 22% jump in implant procedures across 600 U.S. centers during 2024 after adopting same-day insertion policies.

Ambulatory surgical centers and retail health outlets, while price-competitive, face liability hurdles and have only captured 15% of the 2025 volume. India’s rural sub-center model, which pays community health activists USD 12 per procedure, shifted 18% of implants out of district hospitals in 2024. Such decentralization is poised to expand geographic access and enhance the growth potential of the subdermal contraceptive implants industry across varied care settings.

Geography Analysis

North America generated 45.08% of 2025 revenue, buoyed by Medicaid expansion and commercial insurers’ removal of cost-sharing for LARC. Immediate postpartum protocols, now a Tier 1 quality metric, lifted U.S. insertions to 1.8 million in 2024, equal to 11 implants per 1,000 women of reproductive age. Patent cliffs from 2027 will invite biosimilars, likely trimming average selling prices but boosting overall subdermal contraceptive implants market size as lower out-of-pocket costs spark incremental uptake.

Asia-Pacific is the fastest-growing region, projected at a 7.13% CAGR to 2031, driven by India, Indonesia, and the Philippines, where collective demand will top 6.5 million units by 2028. China approved domestic levonorgestrel production in 2024 and targets 500,000 annual insertions by 2027, aiming to reverse a 12% drop in modern method use among rural women since 2020. Rapid urbanization, smartphone penetration, and government subsidies together accelerate market penetration, underscoring Asia-Pacific’s pivotal role in reshaping the global subdermal contraceptive implants market share landscape.

The U.K.’s flat volume of 420,000 implants in fiscal 2024 illustrates maturity. Nonetheless, litigation-driven safety mandates could create opportunities for digital insertion-tracking tools. Middle East & Africa combined accounted for 12% of 2025 volume and will grow at a 6.2% CAGR on the back of UNFPA and USAID procurement in Ethiopia, Kenya, Nigeria, and Tanzania, markets where unmet need surpasses 25%. South America, with 8% revenue share, grapples with fiscal austerity; Brazil’s public distribution fell 9% in 2024 as budgets pivoted to vaccination campaigns, underscoring macroeconomic sensitivities within the subdermal contraceptive implants industry.

Competitive Landscape

Organon anchors the competitive field with significant branded revenue from Nexplanon, which generated USD 963 million in fiscal 2024 and should cross USD 1 billion in 2025. Shanghai Dahua’s vertically integrated Sino-implant (II) controls donor-funded tenders in Africa and Southeast Asia thanks to a USD 6.50 all-in cost, whereas Indian generics players Cipla, Lupin, and HLL Lifecare supply price-sensitive programs such as India’s Antara. Bayer’s 2024 roll-out of Nexplanon NXT showcases a pivot toward applicator safety and positions the firm to defend share even as biosimilars erode price premiums.

Strategic moves extend beyond pricing. Organon is spending USD 120 million to boost Dutch production capacity by 40% ahead of Medicaid-driven demand surge. Cipla secured tentative U.S. FDA approval for a biosimilar launching post-2027, while Lupin races with a levonorgestrel file to enter by 2028. Hologic’s Bluetooth-enabled applicator pilot cut malposition to 0.1% across 8,000 cases, illustrating data-driven differentiation. A USD 45 million venture funding round for biodegradable implants reveals an innovation frontier that could sidestep removal procedures altogether. Smaller regional contenders, including Meril Life Sciences and Pregna International, leverage 48-hour delivery guarantees and on-site training to chip away at incumbent distribution advantages, particularly in geographies where cold-chain reliability remains uneven. Overall, competition centers on cost, device ergonomics, digital traceability, and manufacturing scale variables that will decide future winners in the subdermal contraceptive implants market.

Subdermal Contraceptive Implants Industry Leaders

Shanghai Dahua Pharmaceutical Co., Ltd.

Bayer AG

Organon & Co.

DKT WomanCare Global

Celanese

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mass General Brigham and MIT developed a novel long-acting contraceptive implant deliverable through tiny needles using Self-assembling Long-acting Injectable Microcrystals (SLIM) technology, potentially revolutionizing insertion procedures by eliminating surgical requirements and enhancing patient comfort.

- February 2025: FDA approved MIUDELLA, the first hormone-free copper intrauterine system in the U.S. in over 40 years, expanding LARC options and demonstrating regulatory openness to innovative contraceptive technologies that could influence implant approval pathways.

- February 2024: Organon launched "Her Plan is Her Power" global initiative with U.S. grant programs and listening tours targeting high-need communities, representing a strategic shift toward comprehensive market access programs that combine product distribution with community engagement.

Global Subdermal Contraceptive Implants Market Report Scope

Subdermal contraceptive implants refer to those implants that involve the delivery of a steroid progestin from polymer capsules or rods placed under the skin. The hormone diffuses out slowly at a stable rate, providing contraceptive effectiveness for 1-5 years.

The Subdermal Contraceptive Implants Market Report is Segmented by Type (Single-Rod Implants, Double-Rod Implants, Others), Hormone (Etonogestrel, Levonorgestrel), End User (Hospitals, Gynecology & Obstetrics Clinics, Family Planning & Reproductive Health Centers, Ambulatory Surgical Centers, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Single-Rod Implants |

| Double-Rod Implants |

| Others |

| Etonogestrel |

| Levonorgestrel |

| Hospitals |

| Gynecology & Obstetrics Clinics |

| Family Planning & Reproductive Health Centers |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Single-Rod Implants | |

| Double-Rod Implants | ||

| Others | ||

| By Hormone | Etonogestrel | |

| Levonorgestrel | ||

| By End User | Hospitals | |

| Gynecology & Obstetrics Clinics | ||

| Family Planning & Reproductive Health Centers | ||

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the subdermal contraceptive implants market by 2031?

The market is forecast to reach USD 1.28 billion by 2031.

How fast is Asia-Pacific growing in the subdermal implants space?

Asia-Pacific is expected to log a 7.13% CAGR between 2026-2031.

Which device type leads current global revenue?

Single-rod etonogestrel systems held 66.82% revenue share in 2025.

When will etonogestrel biosimilars likely enter the U.S. market?

Tentative FDA approval positions launches soon after Organon’s patent expires in Q2 2027.

Why are family-planning centers expanding faster than hospitals?

Bundled reimbursement codes and specialized counseling push their CAGR to 5.82% through 2031.

Page last updated on: