Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

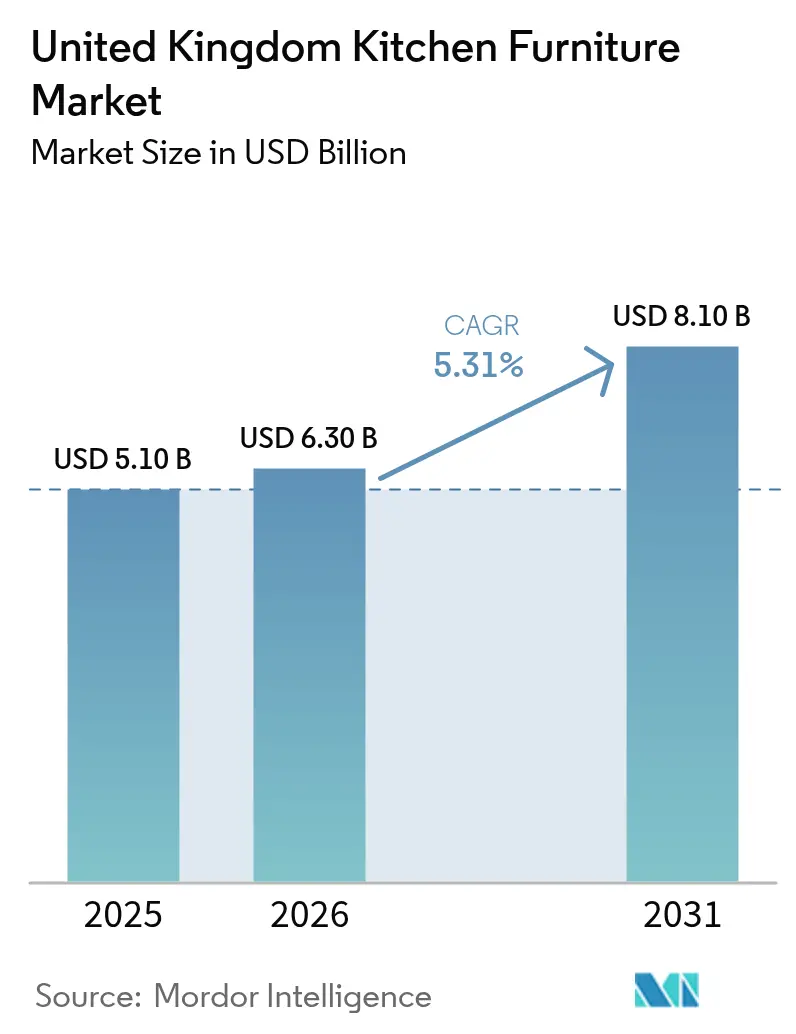

| Base Year Market Size (2025) | USD 5.10 Billion |

| Market Size (2026) | USD 6.30 Billion |

| Market Size (2031) | USD 8.10 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Kitchen Furniture Market Analysis by ���ϲ�����

The United Kingdom kitchen furniture market size is USD 5.1 billion in 2025, projected to reach USD 6.3 billion in 2026 and USD 8.1 billion by 2031, reflecting a 5.31% CAGR over the forecast period. Stabilizing property transactions after April 2025 stamp-duty threshold adjustments, including 100,440 residential completions recorded in December 2025, which marked a 5% year-on-year gain, are supporting first-fit and replacement activity, lifting installation pipelines across price tiers [1]HM Revenue & Customs, “UK Property Transactions Statistics, December 2025,” GOV.UK, gov.uk. New-home registrations rose to 115,350 units in 2025, up 11% over 2024, with growth in private-sector permits and rental-affordable programs signaling healthier site starts that translate into primary kitchen fits and supply-chain confidence for manufacturers. Repair, maintenance, and improvement spending continues to provide a floor to demand even as total construction output contracted 2.1% in the fourth quarter of 2025, since many households defer relocations but proceed with tactical kitchen refreshes that deliver visible home-value uplift. Within channels and end markets, B2B and project-led distribution is moving faster than retail because multi-family programs and social-housing frameworks systematize procurement and installation schedules, while Northern Ireland shows the fastest regional momentum in the medium term.

Key Report Takeaways

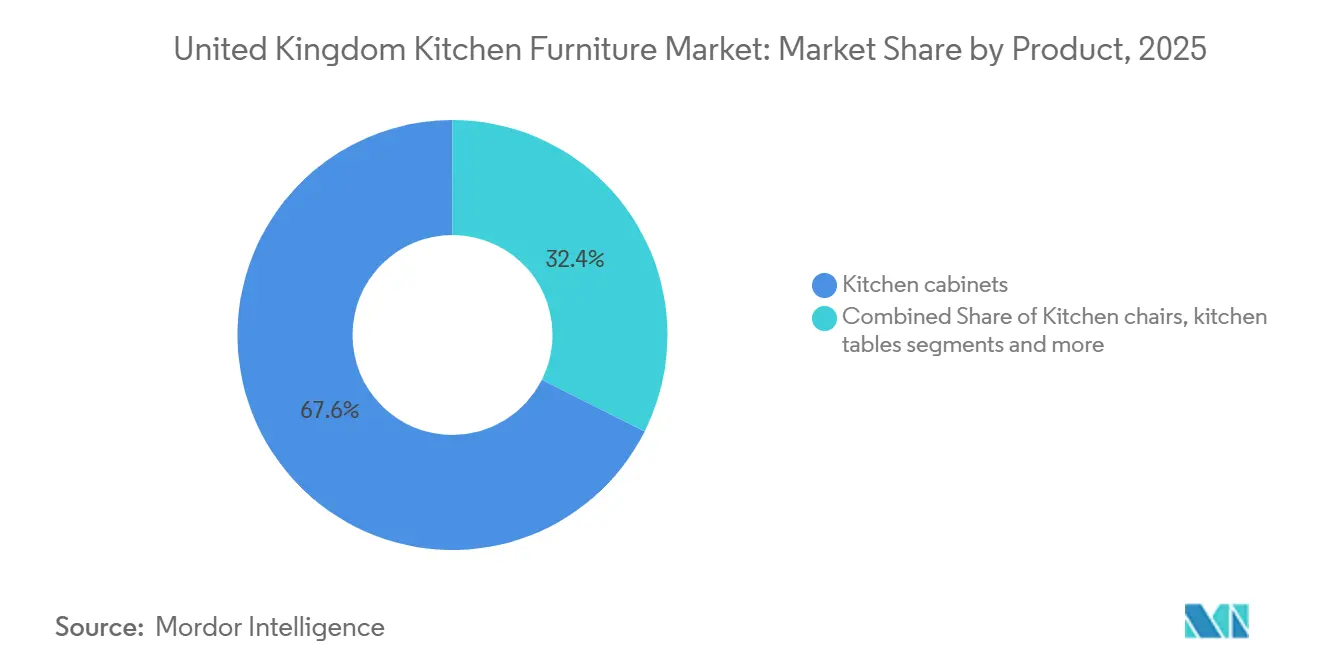

- By product, kitchen cabinets led with 67.57% revenue share in 2025, confirming structural dominance in the United Kingdom kitchen furniture market. Kitchen chairs are forecast to expand to a 6.46% CAGR by 2031, the fastest within the product set.

- By material, wood accounted for 56.92% of 2025 installations, while metal segments are projected to grow at a 7.08% CAGR to 2031.

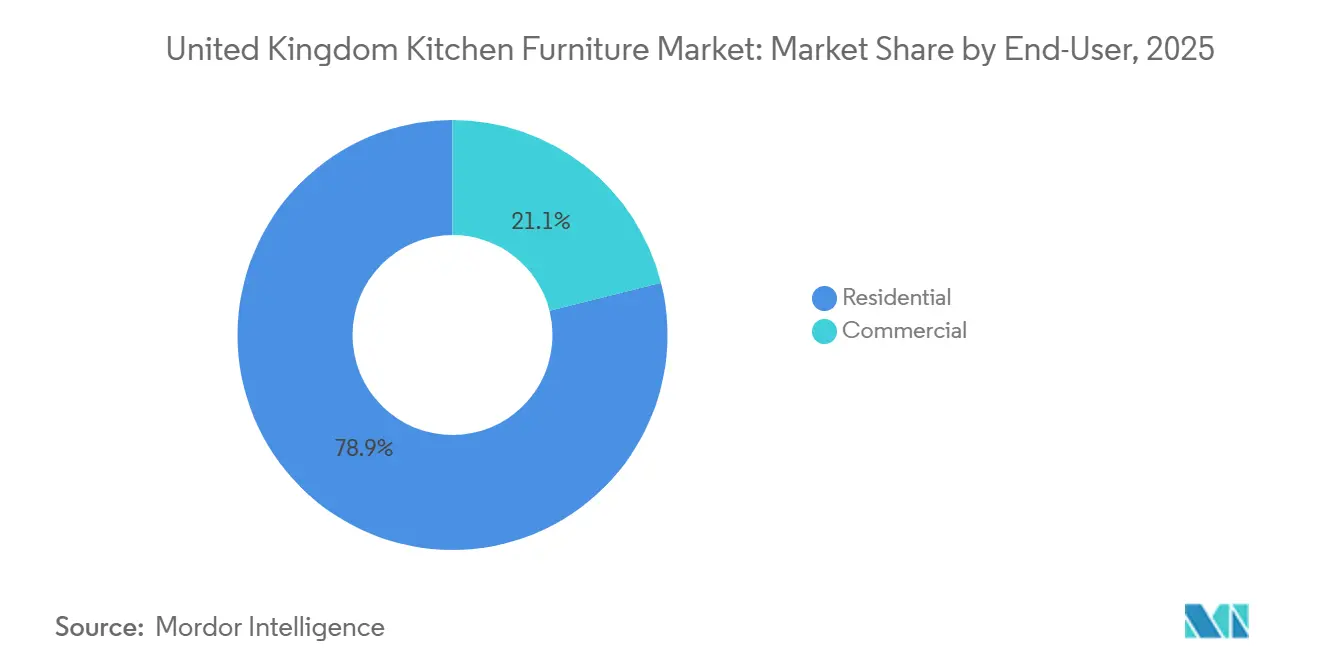

- By end-user, residential represented 78.96% of the 2025 value, and commercial is expected to grow at a CAGR of 6.56% to 2031.

- By distribution channel, B2C retail captured 80.95% of the 2025 value, while B2B project distribution is expected to post a 6.12% CAGR through 2031.

- By geography, England held 83.37% of 2025 revenue, while Northern Ireland is expected to be the fastest-growing region at a 6.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Kitchen Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stabilizing housing transactions and raising new-home registrations, re-energizing kitchen demand | +1.3% | England, Scotland, and Wales, concentrated in first-time buyer corridors | Medium term (2-4 years) |

| Resilient RMI and trade pipelines underpin core demand across price points | +1.0% | National, with strength in the Southeast, Southwest, and East Midlands | Long term (≥ 4 years) |

| Omnichannel growth raises lead capture and conversion in kitchens | +0.8% | National, with urban clusters benefiting from click-and-collect density and digital design tools | Medium term (2-4 years) |

| Value-tiered kitchen ranges and installation options expand affordability | +0.7% | National, with emphasis on price-sensitive markets such as the Northeast, Wales, and Northern Ireland | Medium term (2-4 years) |

| Build-to-Rent fit-out programs scale standardized kitchen packages | +0.5% | National, with concentration in London, Manchester, Birmingham, and Leeds, multi-family developments | Medium term (2-4 years) |

| Class MA and broader PDR conversions create incremental kitchen installations | +0.3% | England-dominant, particularly Southeast office-to-residential conversions | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Stabilizing Housing Transactions and Rising New-Home Registrations Re-Energize Kitchen Demand

Seasonally adjusted residential property completions reached 100,440 in December 2025, a 5% year-on-year increase that reflects the effect of April 2025 stamp-duty threshold changes and improved buyer sentiment as mortgage-rate pressure eased from 2024 peaks. New-home registrations increased to 115,350 units in 2025, up 11% from 2024, while private-sector permits expanded by 12% and rental-affordable programs added 10%, indicating better land-release and site-activation activity among builders [2]National House-Building Council, “New Home Registrations and Completions 2025,” NHBC, nhbc.co.uk. These pipelines replenish first-fit kitchen volumes from completions and maintain momentum in installation schedules across trade and retail channels that depend on predictable builder demand. Secondary-market turnover adds a replacement-cycle catalyst, as recent movers reconfigure layouts, often with faster project timelines than first-fit programs that follow build schedules. Together, these trends compress idle capacity for fitters and manufacturers, which supports steadier throughput in the United Kingdom kitchen furniture market.

Resilient RMI And Trade Pipelines Underpin Core Demand Across Price Points

Even with a 2.1% decline in total construction output in the fourth quarter of 2025, the repair, maintenance, and improvement segment has shown staying power, helping protect volumes in kitchen refits as households defer relocations [3]Office for National Statistics, “Consumer Price Inflation December 2025,” ONS, ons.gov.uk. Trade-focused networks that stock rigid cabinets for next-day collection maintain activity by serving installers and small builders who convert homeowner intent into scheduled work without long lead times. Industry surveys reported softer RMI volumes than in 2024, yet remained close to trend, given a committed backlog and the pull of energy-efficiency upgrades that are often bundled into kitchen projects by small and medium-sized contractors. Retail sales data pointed to a lift in January 2025, with big-ticket categories supported by promotional intensity, validating that price-elastic customers still transact when discounts and financing reduce upfront outlays. On balance, the trade channel’s ability to offer immediate availability and installed outcomes continues to stabilize throughput in the United Kingdom kitchen furniture market, even as broader housing metrics waver.

Omnichannel Growth Raises Lead Capture and Conversion in Kitchens

Online penetration across non-food retail reached the mid-30% range in early 2025, and kitchen categories now translate digital engagement into physical and installed sales through design configurators, appointment booking, and finance journeys that shorten the decision cycle. IKEA United Kingdom reports 43% online contribution to national sales and continues to broaden small-format, planned-led locations that integrate click-and-collect and in-store visualization to support end-to-end conversions. Kingfisher has highlighted kitchen demand as a bright spot in its first-half fiscal 2025/26 results, underpinned by a clear value ladder and a seamless path from web discovery to store design to delivery. Wickes’ core design-and-install channel returned to consistent growth during 2025, supported by a digital quotation tool that improved capture and handover from online browsing to fitted projects. This convergence lifts attachment rates for worktops, storage, and appliances, improving average tickets and enhancing the resilience of the United Kingdom kitchen furniture market through more reliable conversion funnels.

Value-Tiered Kitchen Ranges and Installation Options Expand Affordability

Suppliers now offer clear good-better-best options and flexible labor options that allow budget-constrained households to self-install, while time-sensitive buyers choose turnkey design and fitting. B&Q’s tiered approach, combined with a large-format store estate and digital planning tools, enables shoppers to compare specifications and price steps in a single journey, improving confidence to buy. IKEA continues to defend entry price points and offers online planning services and finance options that keep essential configurations within reach for value-tier consumers. Wickes reports steady growth in its design-and-install business as modular packages at clear price bands match the needs of first-time buyers and landlords who prioritize move-in readiness and basic durability. The plastics and polymers category is also expanding faster than wood because advanced laminates and thermofoil finishes now mimic timber at lower cost and shorter lead times, bringing contemporary styles to the broad base of value-seeking customers in the United Kingdom kitchen furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Installer and carpenter shortages extend lead times and raise install costs | -0.5% | National, acute in the Southeast and Scotland, where wage competition from commercial projects is most intense | Long term (≥ 4 years) |

| Big-ticket sensitivity to macro headwinds dampens upgrade cycles | -0.4% | National, with higher elasticity in London and the Southeast during elevated inflation | Short term (≤ 2 years) |

| Timber due diligence (UKTR) compliance adds cost and complexity | -0.2% | National, acute for importers of wood products and solid-timber door manufacturers | Medium term (2-4 years) |

| Project segment inertia, starts lag completions amid high-rise regulatory frictions | -0.2% | London-centric delays with spillovers to apartment-heavy areas | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Installer And Carpenter Shortages Extend Lead Times and Raise Install Costs

The construction labor market faces persistent gaps, with more than 140,000 vacancies and an aging workforce that implies cumulative retirements over the next decade will exceed current training inflows for key trades. CITB projects a sector hiring need of 239,300 additional workers from 2025 through 2029, underscoring the pressure on carpentry, joinery, electrical, and plumbing capacity that is integral to fitted-kitchen completion. Extended installation wait times have become common for customized work, which can discourage discretionary remodels and complicate scheduling for retailers and developers aiming to complete on fixed dates. Higher day rates for fitters increase total project costs and reduce take-up for mid-market specifications where price sensitivity is higher than in the luxury tier. Retailers and project managers explore hybrid fitting models that split self-install and professional labor, but these approaches have limits in terms of quality and safety compliance, which keeps capacity tight in the United Kingdom kitchen furniture market.

Big-Ticket Sensitivity to Macro Headwinds Dampens Upgrade Cycles

Headline inflation moderates but remains above the central bank’s target, which keeps real income under pressure and delays some large kitchen purchases that rely on unsecured finance or mortgage-linked cash-out. The base rate eased into late 2025 but remains restrictive versus the prior decade, which sustains caution and extends decision cycles for higher-spec refits. Retailers respond with promotions and financing that protect volume, yet these tactics compress margins and do not fully offset hesitancy among households with limited budget slack. Even with steady volumes at the value end, the mid-priced fitted segment can lag when consumers prioritize essential spending and defer aspirational upgrades. This dynamic creates uneven demand across tiers and channels within the United Kingdom kitchen furniture market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cabinets Anchor Value, Freestanding Gains Velocity

Kitchen cabinets accounted for 67.57% of the United Kingdom kitchen furniture market in 2025, cementing their role as the structural core that drives most project value and installer schedules across trade and retail. The configuration of wall, base, and tall units ties directly to storage, worktop area, and appliance integration, which keeps cabinet demand resilient across budget, mid-market, and premium tiers. Chairs are the fastest riser with a 6.46% CAGR through 2031, reflecting open-plan layouts that spur more frequent seating refresh cycles and higher attachment rates at checkout. Tables track steady replacement and are increasingly integrated with island seating, which shifts some demand from standalone pieces to multifunction modules that retailers bundle with core cabinet ranges. In e-commerce channels, small-format freestanding units such as carts and compact storage attract price-sensitive renters who avoid fixed installations, creating incremental attachment for online baskets.

Premiumization in rigid cabinet systems shows up in soft-close mechanisms, push-to-open hardware, and integrated lighting that now appear in mid-tier packages after component costs fell due to scale manufacturing. Flat-pack holds share where self-install is feasible, yet trade installers often prefer rigid carcasses for durability, which nudges channel mix toward depots that guarantee next-day availability. Chairs benefit from easy visual refresh, wipe-clean surfaces, and stackability that fits smaller dwellings, while renters and landlords favor impact-resistant finishes over delicate materials. Cabinet workshops that serve conservation areas and listed properties retain bespoke in-frame and Shaker demand on longer lead times, which supports a premium niche insulated from mass-market price competition. This product mix balance helps the United Kingdom kitchen furniture market absorb cyclical variations in big-ticket appetite by leaning on frequent, lower-ticket chair and accessory purchases.

By Material: Wood Dominates, Synthetics Close the Gap in Speed

Wood accounted for 56.92% of 2025 installations as consumers associate timber with longevity and warmth, even as cost and lead-time considerations shift some share to engineered options. Plastics and polymers, led by advanced laminates and thermofoil finishes, are projected to grow at a 6.81% CAGR due to improved visual realism and durability that align with budgets in value and standardized project segments. Metals and other materials remain niche in residential settings, with concentrated adoption in design-led or hospitality-inspired spaces where performance characteristics justify higher spending. In project settings that prioritize lifecycle costs and serviceability, moisture-resistant synthetic fronts reduce callbacks and simplify turnarounds after tenant changes, supporting adoption beyond purely budget-led motives. These dynamics help manufacturers balance capacity across finishing lines and diversify sourcing to manage regulatory and price risks.

United Kingdom Timber Regulation enforcement activity in 2024 and 2025 increased compliance intensity among wood-product importers, including more due diligence checks and publicized enforcement actions that elevated reputational risk and added costs to maintain legality documentation. Solid-wood programs lean harder into certified European species to reduce risk, which carries a price premium that either flows into tickets or compresses margins in competitive mid-market price bands. Laminates and thermofoil fronts offer shorter lead times and consistency, helping retailers respond to color and texture trends on an 18- to 24-month cycle. With a heavy import profile for wood products in the United Kingdom, manufacturers continue to optimize blends of certified timber and synthetics to sustain reliability while meeting specification preferences across the United Kingdom kitchen furniture market.

By End-User: Residential Drives Volume, Commercial Seeks Standardization

Residential accounted for 78.96% of the 2025 market value and mirrors the overall 4.96% CAGR through 2031, since homeowner replacement cycles, first-fit installations after purchase, and rental refreshes remain the largest and most frequent sources of demand. Within residential, owner-occupied dwellings skew to higher specification and longer cycles, while private landlords focus on robust finishes and serviceable components that meet tenancy turnover requirements. Social housing providers procure standardized, repairable kitchens through national and regional frameworks, which generate repeat volume for suppliers and ensure consistent nationwide service. Commercial and communal spaces such as office kitchenettes, co-working pantries, and student accommodation add consistent though smaller ticket volumes and favor modular designs that reduce onsite time. This end-user balance keeps installed capacity busy through varied pathways, limiting dependence on any single tenure type.

B2B frameworks in housing programs and community regeneration create predictable pipelines for residential applications at scale, which stabilize supplier utilization rates. Homes England reported higher starts and completions in fiscal 2024–25 across affordable programs, which bolsters standard-fit kitchen volume and supports factory planning for carcasses and fronts. Commercial and amenity spaces specify durable finishes and warranty terms tied to asset life, which increases the use of standardized component sets and common appliance platforms across portfolios. These purchasing patterns support the broader stability of the United Kingdom kitchen furniture market by blending homeowner-driven upgrades with scheduled deliveries in residential-led development.

By Distribution Channel: Retail Leads, Project Pipelines Scale Faster

B2C retail captured 80.9% of the 2025 value through home centers, specialty showrooms, and online direct-to-consumer platforms that match how households research, design, and finance kitchens. B2B and project channels are on a faster 6.12% growth path as developers, housing associations, and modular builders rely on framework agreements and offsite assembly to compress timelines and standardize warranty liabilities. Large-format retail footprints powered by appointment-led design flows and robust e-commerce are effective at converting browsing into paid orders for cabinets, worktops, and appliances. Online-only models capture value-seeking self-install shoppers by cutting showroom overhead and leveraging planning support to streamline purchasing, thereby expanding reach into areas with limited store density. This channel preserves access and immediacy for households while building a stable project pipeline that supports factory throughput.

B2B and project momentum benefit from clear lines of responsibility across design, supply, and installation that developers and registered providers prefer, reducing delays and rework. Affordable programs start, and completions reported by public agencies bolster these frameworks, with kitchens delivered within broader packages that align with fire safety, accessibility, and lifecycle standards. At the same time, retail formats refine price ladders and appointment booking to maintain conversion rates despite cautious consumer sentiment, enabling a steady flow in the United Kingdom kitchen furniture market through both homeowner and institutional channels.

Geography Analysis

England held 83.37% of the United Kingdom kitchen furniture market in 2025, supported by stabilized property completions late in the year after tax-threshold adjustments and by an extensive installed base that renews on predictable cycles. Registration data points to improve builder confidence outside the most constrained urban high-rise segments, helping sustain first-fit volumes within regional housebuilding corridors. Social and affordable program starts and completions also contribute to a predictable framework-led delivery that benefits standardized kitchen packages and their supply partners. Within England, the balance between secondary-market refurbishments and new-built first fits supports both trade depots that emphasize immediacy and retail showrooms that convert design appointments to orders.

Scotland and Wales maintain steady activity through a combination of refit cycles, apartment-led development in key cities, and continued spending on core home improvements, which extend demand for rigid units and durable finishes aligned with mixed-tenure profiles. A focus on resilient RMI in owner-occupied housing supports consistent ordering in trade-led channels, while compact new-built layouts in urban locations nudge the adoption of modular, space-efficient kitchen configurations. Planning frameworks for conversions under permitted development deliver additional small-unit kitchens in select locations, although these programs remain concentrated primarily in England. Suppliers serving these areas balance showroom-led consultation with regional depots that hold core inventory for short-lead projects, stabilizing install calendars throughout the year.

Northern Ireland is projected to be the fastest-growing region at a 6.26% CAGR through 2031, reflecting a higher proportional exposure to new-build activity and an active pipeline that supports primary fits alongside refit cycles in established stock. Framework-led procurement by registered providers and consistent activity in private development help distribute demand across standardized packages and retail-led upgrades. Channel strategies that combine direct-to-consumer planning with trade-focused depots reduce delivery friction, which is key for regional installers coordinating multiple small projects. These threads reinforce steady outlooks for the United Kingdom kitchen furniture market across devolved nations, even as policy and planning regimes differ by jurisdiction.

Competitive Landscape

Market is consolidated, with the top six suppliers collectively estimated to hold 80% to 85% of value through complementary channel strategies that span trade-only depots, big-box retail, manufacturer-direct showrooms, and omnichannel planning. Howdens anchors the trade channel through a dense national depot network and next-day cabinet availability, which underpin installer productivity and loyalty. Kingfisher’s B&Q highlights kitchens as a big-ticket growth area, leveraging a clear proposition ladder, store footprint, and end-to-end digital planning that supports design appointments at scale. IKEA maintains price leadership and broad online engagement, with kitchens benefiting from planning tools, finance options, and logistics coverage that shorten installation timelines [4]IKEA UK, “FY2025 Results and Price Investment,” IKEA, ikea.com.

Wren continues to operate a manufacturer-direct showroom network with vertically integrated production and a focus on experiential design and finance offers that convert foot traffic into fit orders. Magnet has transitioned under new ownership and is positioned to emphasize retail expansion and framework-led partnerships in social housing and development, strengthening its route-to-market options across consumer and B2B channels. In the long tail, private-label suppliers and independent studios compete on design differentiation and service, while German-origin brands retain a foothold in the premium tier through specification depth and consistent fit-and-finish. Online pure plays leverage content and planning support to capture self-install demand and extend geographic coverage without store-driven overhead.

Strategic investment focuses on production scaling, range refreshes, and planning-led store expansion that support a steady flow through mixed cycles. Kingfisher reports like-for-like growth in the first half of fiscal 2025/26, reflecting execution of a tiered kitchen offer and tighter online-to-store integration. IKEA’s recent results show kitchens advancing within a broader price investment program, while online share remains high, confirming the continued relevance of omnichannel in big-ticket categories. Howdens continues to invest in capacity and network improvements to sustain service levels that align with installer expectations and trade job sequencing. These moves reinforce a competitive pattern in the United Kingdom kitchen furniture market, where speed, reliability, and breadth of configuration matter as much as ticket price.

United Kingdom Kitchen Furniture Industry Leaders

Howdens Joinery Group

Wren Kitchens

B&Q (Kingfisher)

Wickes

Magnet (incl. Magnet Trade/Project)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Howdens Joinery opened 16 new depots across the United Kingdom and Ireland since December 2025, creating new jobs and expanding its trade-supply footprint to serve next-day rigid-cabinet availability for builders and installers.

- January 2026: Alteri Investors completed the acquisition of Magnet, Gower, and CIE from Nobia Group, with Magnet reporting positive like-for-like sales growth and average-order-value gains as the brand returned to quarterly profitability under new ownership.

- December 2025: Wren Kitchens executed a year-end expansion by opening multiple new showrooms and extending its small-format approach that targets high-street footfall with immersive displays and finance options.

- November 2025: Howdens Joinery announced a factory expansion program to build one of the world’s largest cabinet production lines and outlined further depot openings across Ireland in 2026 as part of its vertical-integration strategy.

United Kingdom Kitchen Furniture Market Report Scope

A complete background analysis of the United Kingdom Kitchen Furniture market, which includes an assessment of emerging trends by segments, significant changes in market dynamics, and market overview, is covered in the report. The report also features the qualitative and quantitative assessment by analysing data gathered from industry analysts and market participants across various key points in the industry's value chain. The United Kingdom Kitchen Furniture Market is segmented by product (kitchen cabinets, kitchen chairs, kitchen tables, and others), by material (wood, metal, plastic & polymer, and other materials), by end-user (residential and commercial), by distribution channel (B2C retail and B2B project), and by region (Englan, Scotland, Wales, and Northern Ireland). The report also covers the market sizes and forecasts for the United Kingdom Kitchen Furniture market in value (USD) for all the above segments.

By Product

| Kitchen Cabinets |

| Kitchen Chairs |

| Kitchen Tables |

| Other Products (trolley, cart, pantry shelves) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Project |

By Region

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Product | Kitchen Cabinets | |

| Kitchen Chairs | ||

| Kitchen Tables | ||

| Other Products (trolley, cart, pantry shelves) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Region | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the current size and expected growth of the United Kingdom kitchen furniture market?

The United Kingdom kitchen furniture market size is USD 5.1 billion in 2025 and is forecast to reach USD 8.1 billion by 2031 at a 5.31% CAGR.

Which product segment leads the United Kingdom kitchen furniture market?

Kitchen cabinets led with 67.57% revenue share in 2025, confirming cabinets as the core value driver in fitted projects.

Which region is expected to grow fastest within the United Kingdom kitchen furniture market?

Northern Ireland is projected to be the fastest-growing region with a 6.26% CAGR through 2031.

How are channels evolving in the United Kingdom kitchen furniture market?

B2C retail commanded 80.9% of value in 2025, while B2B and project distribution are expanding faster at a 46.12% CAGR due to framework-led procurement and offsite assembly.

What macro or regulatory issues could restrain demand?

Capacity constraints for installers, inflation-linked sensitivity for big-ticket items, and United Kingdom Timber Regulation compliance requirements add cost and time pressures that can temper upgrade cycles.

How is omnichannel shaping buyer behavior in the United Kingdom kitchen furniture market?

High online penetration and planning tools drive faster conversion from browsing to installed sales, with IKEA, Kingfisher, and Wickes reporting solid contributions from digital to design-to-install journeys.

Page last updated on: