United Kingdom Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

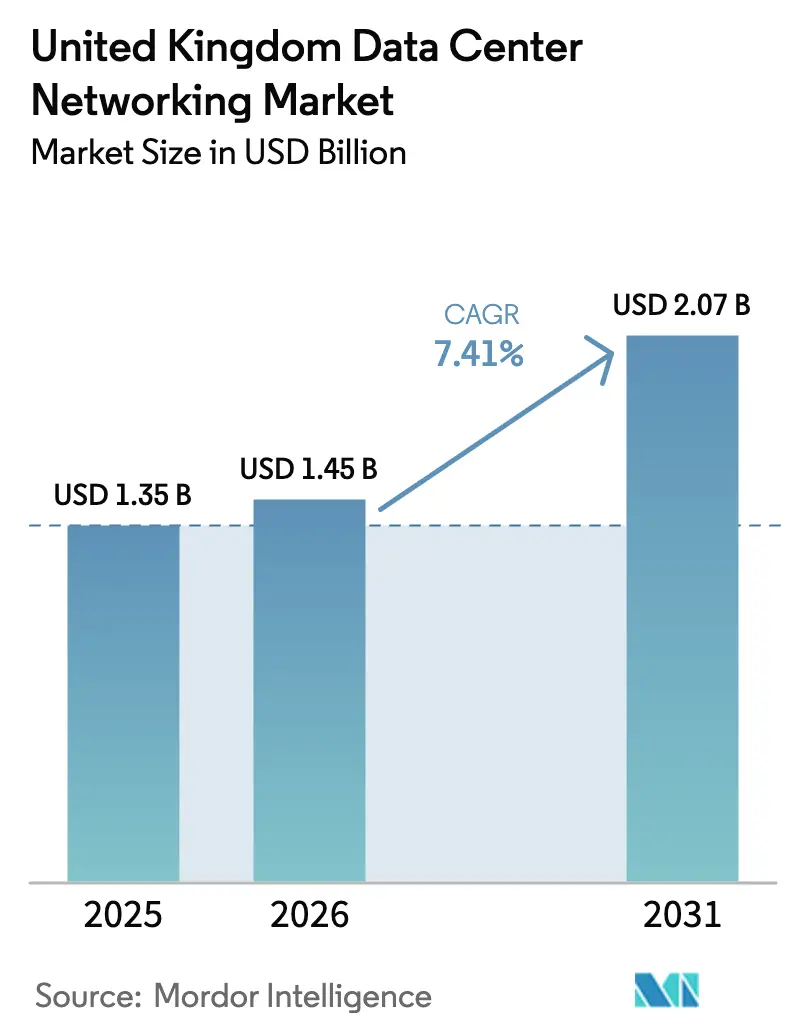

| Base Year Market Size (2025) | USD 1.35 Billion |

| Market Size (2026) | USD 1.45 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Data Center Networking Market Analysis by ���ϲ�����

The United Kingdom data center networking market size is expected to grow from USD 1.35 billion in 2025 to USD 1.45 billion in 2026 and is forecast to reach USD 2.07 billion by 2031 at 7.41% CAGR over 2026-2031. This expansion stems from the government’s Critical National Infrastructure (CNI) designation for data centers, a GBP14 billion (USD 19.21 billion) AI investment pledge, and private-sector hyperscale commitments that jointly raise expectations for resilient, high-bandwidth, low-latency fabrics. Enterprises are redesigning network topologies to support AI training clusters that push port-density limits and mandate lossless, RDMA-capable Ethernet. Power-supply constraints around London are pushing new builds toward regional hubs, which in turn accelerates demand for more energy-efficient 400G and 800G hardware. Ongoing consolidation typified by the HPE Juniper proposal signals a market tilt toward end-to-end platforms bundling switching silicon, optics, automation software, and managed services offerings.

Key Report Takeaways

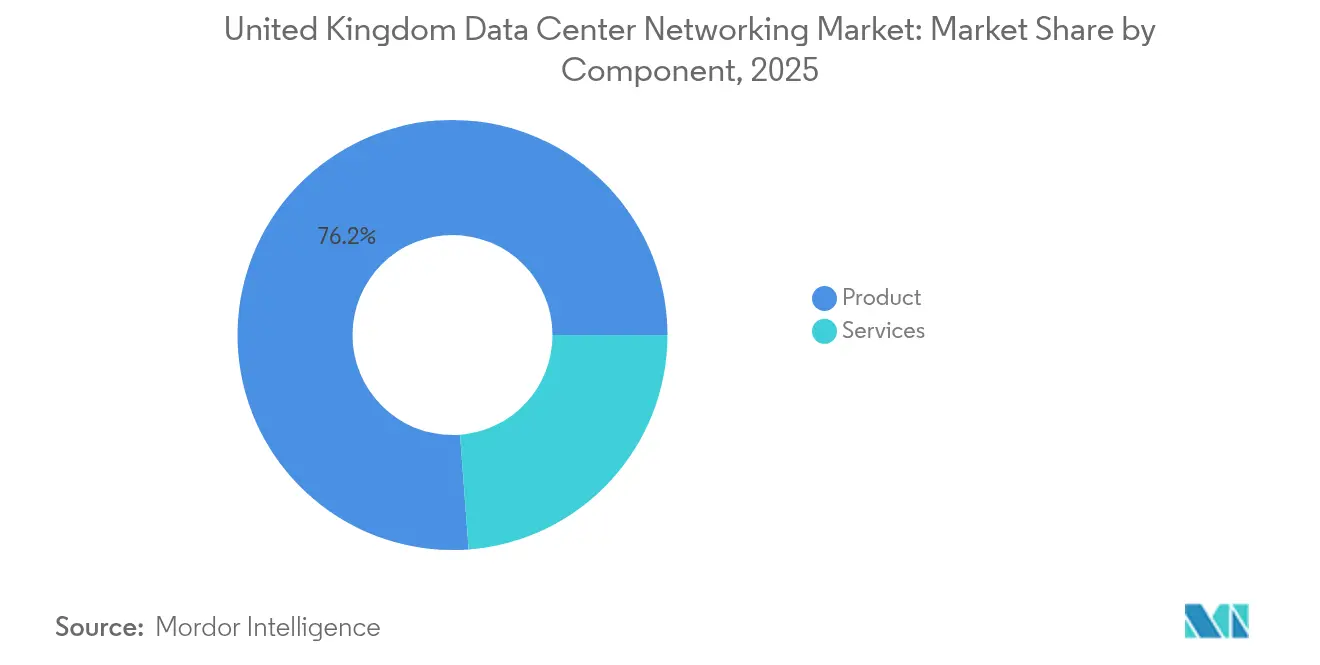

- By component, products commanded 76.20% of the United Kingdom data center networking market share in 2025, while services are projected to advance at a 7.55% CAGR to 2031.

- By end-user, IT and telecommunications led with 36.80% revenue share in 2025; manufacturing is forecast to expand at an 7.95% CAGR through 2031.

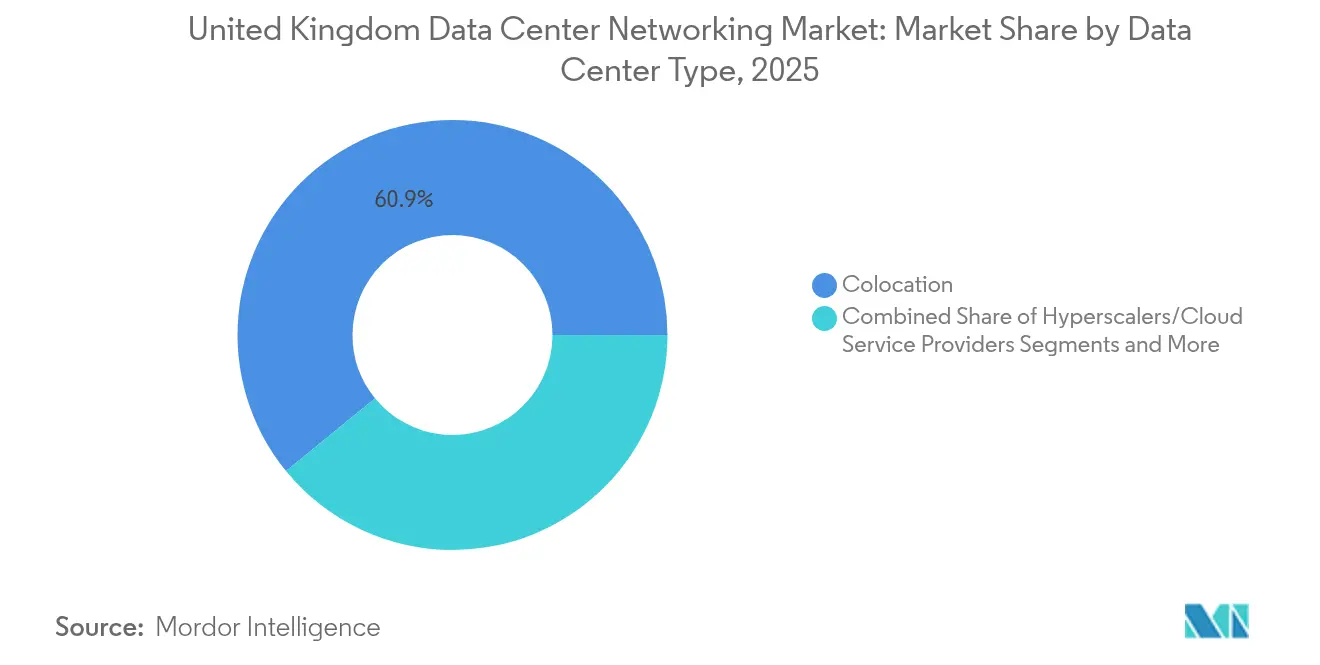

- By data-center type, colocation facilities held 60.90% of the United Kingdom data center networking market size in 2025, whereas hyperscalers are set to grow at 9.15% CAGR to 2031.

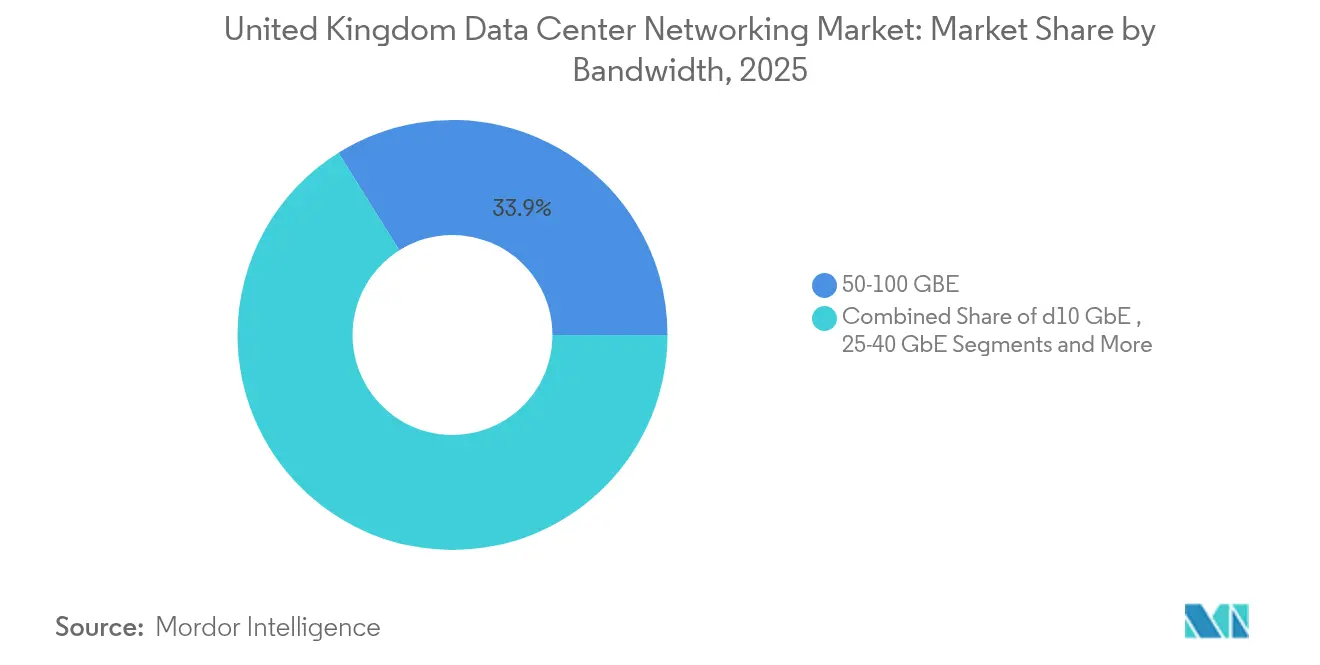

- By bandwidth, 50–100 GbE accounted for 33.90% share of the United Kingdom data center networking market size in 2025; greater than 100 GbE is poised for an 8.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Anticipated developments are shaped at a system level, with United kingdom signals feeding into a larger global picture. The outlook on global data center networking market consolidates these expectations.

United Kingdom Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI/ML and HPC driving 400/800 G upgrades | +2.1% | London, Manchester, Leeds | Medium term (2–4 years) |

| Government CNI status and GBP 14 billion AI plan | +1.8% | Nationwide; early activity in Culham, Oxfordshire | Short term (≤ 2 years) |

| Cloud and hybrid-multi-cloud traffic explosion | +1.5% | National; spill-over to emerging edge locations | Long term (≥ 4 years) |

| Sustainability push for spine-leaf architectures | +0.9% | Focus on South-East England | Medium term (2–4 years) |

| Regional edge DC build-out outside London | +0.7% | Manchester, Cardiff, Leeds, Birmingham | Long term (≥ 4 years) |

| Silicon-photonics 1.6 T Ethernet roadmap | +0.6% | Early hyperscale adoption | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Surge in AI/ML and HPC driving 400/800 G upgrades

Rising generative-AI clusters require ultra-low-latency fabrics that traditional 10/25 G links cannot sustain. NVIDIA’s Spectrum-X platform posts 1.6 × throughput gains versus prior Ethernet fabrics, while Arista’s 7060X6 AI Leaf and 7800R4 AI Spine supply up to 51.2 Tbps and 460 Tbps, respectively, to meet pod-level aggregation demand.[1]NVIDIA Corporation, “Spectrum-X Ethernet Platform,” nvidia.comMeta’s adoption of distributed 400 G switches further demonstrates hyperscalers’ shift to deeper leaf-spine tiers that shorten east-west paths and minimize tail-flow latency. Cisco’s decision to embed Silicon One ASICs inside NVIDIA’s Ethernet stack exemplifies convergence between merchant silicon and AI-centric software pipelines that enterprises now consider a prerequisite for future readiness.

Government CNI status and GBP 14 billion AI plan catalyzing spend

The September 2024 CNI designation grants data-center operators priority access to planning and security support, directly unlocking record capital pledges such as Vantage’s GBP 12 billion (USD 16.47 billion) multi-campus build and Nscale’s USD 2.5 billion sovereign AI facility. The Action Plan also inaugurates AI Growth Zones with dedicated power-allocation corridors, starting in Culham, which accelerates permit approvals that historically delayed capacity. A twentyfold expansion in public compute by 2030, including a GBP 750 million (USD 1029.15 million) Scottish supercomputer, underpins multi-year demand for 800 G interconnects across public-sector and academia workloads.

Cloud and hybrid-multi-cloud traffic explosion

Hybrid architectures intensify east-west movement between IaaS, PaaS, and on-prem environments, demanding deterministic 400 G port performance at internet exchanges and private cloud on-ramps. AWS’s GBP 8 billion (USD 10.98 billion) UK expansion, Google’s USD 1 billion Waltham Cross site, and Microsoft’s GBP 106 million (USD 145.45 million) Leeds hyperscale build all aim to keep cloud latency under 10 milliseconds for UK end-users.[2]Amazon, “Amazon’s one-of-a-kind machine ushering in the next generation of AI,” amazom.com Decommissioning of NHS data rooms following full AWS migration showcases the public sector’s role in fueling interconnect traffic, while BT’s Juniper-based cloud-native core illustrates telecom adoption of spine-leaf topologies for mass 5G offload.

Sustainability push for spine-leaf architectures

The EU Energy Efficiency Directive compels UK operators to disclose PUE and carbon metrics, prompting investments in flatter fabrics with fewer hops and lower watt/Gbps ratios. Dropbox’s 400 G roll-out reports double-digit reductions in power per bit, and Equinix’s digital dashboards let customers track traffic energy intensities that shape procurement decisions. National Grid’s 1.8 GW Buckinghamshire substation will funnel cleaner power into West-London clusters, aligning with net-zero goals while enabling denser switch deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-power constraints in South-East England | −1.2% | London and surrounding counties | Short term (≤ 2 years) |

| Cost and lead-time spikes for 800 G optics/ASICs | −0.8% | Nationwide | Medium term (2–4 years) |

| New energy-/water-use disclosure rules | −0.5% | Large facilities countrywide | Long term (≥ 4 years) |

| Hyperscaler egress fees and lock-in | −0.3% | Enterprise customers across the UK | Medium term (2–4 years) |

| Source: ���ϲ����� | |||

Grid-power constraints in South-East England

National Grid warns data-center electricity demand could rise sixfold this decade, yet the capital’s transmission corridors already operate near capacity. A recent Secretary of State refusal for a West London green belt campus highlights how planning curbs add to grid scarcity, prompting shifts to East London’s Romford, where Green Mountain’s 30 MW project secured faster hookups. Ofgem’s queue-reform program may shave connection wait times, but meaningful substation builds require multi-year cycles, tempering near-term rollout velocities.[3]Ofgem, “Electricity Transmission Queue Reform,” ofgem.gov.uk

Cost and lead-time spikes for 800 G optics/ASICs

Shortages in MTP/MPO fibre assemblies and high-speed driver ICs inflate per-port prices by up to 25% compared with 2023 levels, while Broadcom’s 100 Tbit/s Tomahawk 6 silicon moves remain supply-constrained for at least two quarters. Integrated-photonics value chains resemble microelectronics in complexity; a single foundry hiccup can ripple through module availability and delay planned migrations from 100 G to 800 G fabrics across UK sites.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Outpaces Products Dominance

Products held 76.20% of the United Kingdom data center networking market in 2025, reflecting entrenched demand for switches, routers, application delivery controllers, security appliances, and optical interconnects that anchor physical infrastructure. Cisco’s Nexus 9364E-SG2 64-port 800 G switch exemplifies hardware tuned for AI-scale clusters, boasting 51.2 Tbps bandwidth and sizable on-die buffers to mask microbursts. Storage area networks now transition to NVMe-over-Fabrics, while security gateways embed AI-driven inspection engines capable of decrypt-at-line-rate, keeping hardware demand buoyant.

The services segment is smaller yet set for 7.55% CAGR as enterprises outsource design, integration, and managed operations of complex AI fabrics. Consulting firms deploy software-defined controllers such as Cisco ACI or VMware NSX to automate policy across hybrid clouds, whereas open-source OpenDaylight appeals to firms pursuing vendor-agnostic postures. Adoption of silicon-photonics optics like Coherent’s 2×400 G-FR4 Lite transceiver further nudges organisations to rely on specialist service providers for optical-layer tuning and lifecycle management.

By End-User: Manufacturing Drives Fastest Adoption

IT and telecom operators commanded 36.80% share of the United Kingdom data center networking market size in 2025 owing to continual refresh cycles that sustain broadband and cloud service quality. Banks and insurers also invest heavily; Starling Bank’s use of Digital Realty interconnects underpins mobile-only operations with sub-20 millisecond transaction latency.

Manufacturing posts the fastest 7.95% CAGR to 2031 as Industry 4.0 ties operational-technology sensors to cloud analytics. Reckitt Group links factory assets via Azure IoT to derive predictive-maintenance insights that cut downtime 10% and energy loads 3%. Government, defence, healthcare, and media verticals likewise pivot to AI-assisted workflows yet trail manufacturing’s velocity because of regulatory procurement cycles.

By Data-Center Type: Hyperscalers Accelerate Infrastructure Expansion

Colocation facilities secured 60.90% United Kingdom data center networking market share in 2025 by offering carrier-dense, cloud-neutral meet-me rooms that let enterprises blend public and private workloads seamlessly. Digital Realty’s Docklands-to-Slough campuses host latency-sensitive trading platforms, underscoring colocation’s ongoing relevance for high-frequency financial flows.

Hyperscalers expand at 9.15% CAGR fuelled by AWS’s Elastic Fabric Adapter and UltraCluster 2.0 networks, Google’s carbon-free Waltham Cross build, and Microsoft’s Leeds complex, each engineered for AI superpod topologies spanning tens of thousands of accelerators. Edge and micro sites ride 5G densification; EE activated 1,000+ small cells and Virgin Media O2 added backhaul upgrades that drop latency below 5 milliseconds, enabling content caching and AR/VR workloads near users.

By Bandwidth: High-Speed Transitions Accelerate

The 50–100 GbE tier remained the single largest at 33.90% share in 2025 because it balances throughput with capex for mainstream workloads. Dell’s 64 × 400 GbE fabric proves that even mid-size enterprises pursue fourfold uplifts in rack-to-leaf capacity without line-card sprawl.

Segments above 100 GbE will grow 8.12% CAGR; Ciena’s WaveLogic 6 Extreme 1.6 Tbps coherent optics allow metro reach at lower watts per bit, while Marvell’s 400 G/lane SerDes speeds roadmap to 1.6 T chassis by 2027. Lumentum’s indium-phosphide chipsets enabling 400 Gbps-per-lane herald a pivot toward co-packaged optics that could collapse power budgets by double digits once commercialised.

Geography Analysis

London and the South-East host most of the United Kingdom data center networking market, with 263 facilities and 1,753 MW capacity rooted in Docklands, Slough, and West London clusters that connect to transatlantic subsea cables. National Grid’s 1.8 GW Buckinghamshire substation will alleviate congestion, yet planning headwinds keep operators scanning alternative sites.

Edge initiatives reinforce this mosaic; AI Growth Zones such as Culham streamline permits within science parks that already house advanced-compute tenants. Operators weigh fiber-route diversity, renewable-energy mix, and local talent density when selecting new plots, ensuring interconnection ecosystems mature in tandem with power infrastructure so that traffic can stay within sub-10 millisecond round-trip bands nationwide.

The data center networking market is analyzed by ���ϲ����� across multiple other geographies, with in-depth regional assessments available for Europe, North America, and South America. This is complemented by country-specific insights for Spain, Italy, Canada, Chile, Netherlands, and Poland, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Vendor dynamics are in flux. Incumbent switch makers face new competition from AI-centric silicon suppliers and optics specialists. The proposed USD 14 billion HPE-Juniper merger would fuse compute, storage, routing, and automation portfolios, creating a full-stack alternative to Cisco and Arista. NVIDIA’s Spectrum-X strategy positions the GPU vendor as a credible Ethernet challenger, while Cisco becomes its exclusive ASIC supplier, tightening interdependence within the ecosystem.

Optics innovation alters boundaries between component and system players. Coherent and Lumentum lead silicon-photonics transceiver advances vital for 1.6 T roadmaps, which could compress port power to near 10 pJ/bit and thus lower TCO for hyperscalers. Intel’s 4 Tbps optical chiplet demonstration hints at co-packaged optics entering mainstream switch-SKU cycles within three years, potentially redrawing vendor pecking orders for leaf-spine deployments

United Kingdom Data Center Networking Industry Leaders

Arista Networks Inc.

Broadcom Inc.

Cisco Systems Inc.

Dell Technologies Inc.

Extreme Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Marvell Technology showcased end-to-end PCIe Gen 6 over optics at OFC 2025, enabling 10-meter low-latency links vital for disaggregated AI racks.

- March 2025: Arista Networks released EOS Smart AI Suite with Cluster Load Balancing, giving network teams job-centric visibility and tail-latency mitigation.

- February 2025: Cisco partnered with NVIDIA to integrate Silicon One ASICs with Spectrum-X Ethernet, making Cisco exclusive silicon provider for the platform.

- January 2025: Coherent Corp launched 2×400 G-FR4 Lite optical transceiver aimed at AI fabrics, removing thermoelectric coolers to cut power.

United Kingdom Data Center Networking Market Report Scope

Data center networking refers to the set of technologies, protocols, and hardware used to connect physical and network-based devices and manage the network infrastructure, storage, and processing of applications and data. Data center networking is very critical for 100% uptime of data centers. In the current web-connected world, business workloads are executed on single computers, hence leading to the need for data center networking. Networks provide servers, clients, applications, and middleware with a standard plan to stage the execution of workloads and also to manage access to the data produced.

The United Kingdom Data Center Networking Market is segmented by component type (product [ethernet switches, router, storage area network (SAN), application delivery controller (ADC)], services [installation and integration, training and consulting, support and maintenance]), by end user (IT & telecommunication, BFSI, government, and media and entertainment). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Products | Ethernet Switches |

| Routers | |

| Storage Area Network (SAN) | |

| Application Delivery Controllers (ADC) | |

| Network Security Appliances | |

| Software-Defined Networking (SDN) Controllers | |

| Optical Interconnects | |

| Services | Installation and Integration |

| Training and Consulting | |

| Support and Maintenance | |

| Managed Network Services |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Defense |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Other End-Users |

| Colocation |

| Hyperscalers/Cloud Service Providers |

| Edge/Micro Data Centers |

| Less than or Equal to 10 GbE |

| 25-40 GbE |

| 50-100 GbE |

| Greater than 100 GbE |

| By Component | Products | Ethernet Switches |

| Routers | ||

| Storage Area Network (SAN) | ||

| Application Delivery Controllers (ADC) | ||

| Network Security Appliances | ||

| Software-Defined Networking (SDN) Controllers | ||

| Optical Interconnects | ||

| Services | Installation and Integration | |

| Training and Consulting | ||

| Support and Maintenance | ||

| Managed Network Services | ||

| By End-User | IT and Telecommunications | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Government and Defense | ||

| Media and Entertainment | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial | ||

| Other End-Users | ||

| By Data-Center Type | Colocation | |

| Hyperscalers/Cloud Service Providers | ||

| Edge/Micro Data Centers | ||

| By Bandwidth | Less than or Equal to 10 GbE | |

| 25-40 GbE | ||

| 50-100 GbE | ||

| Greater than 100 GbE | ||

Key Questions Answered in the Report

What is the current size of the United Kingdom data center networking market?

The United Kingdom data center networking market size is USD 1.45 billion in 2026.

How fast will the market grow by 2031?

It is forecast to reach USD 2.07 billion by 2031, advancing at a 7.41% CAGR.

Which segment shows the fastest growth?

Hyperscale and cloud service provider facilities expand at 9.15% CAGR as AI workloads scale.

How is the power grid affecting new data center builds?

South-East England grid constraints delay London projects, steering operators toward regional hubs with available capacity.

Page last updated on: