UAE Tomato Market Analysis by ���ϲ�����

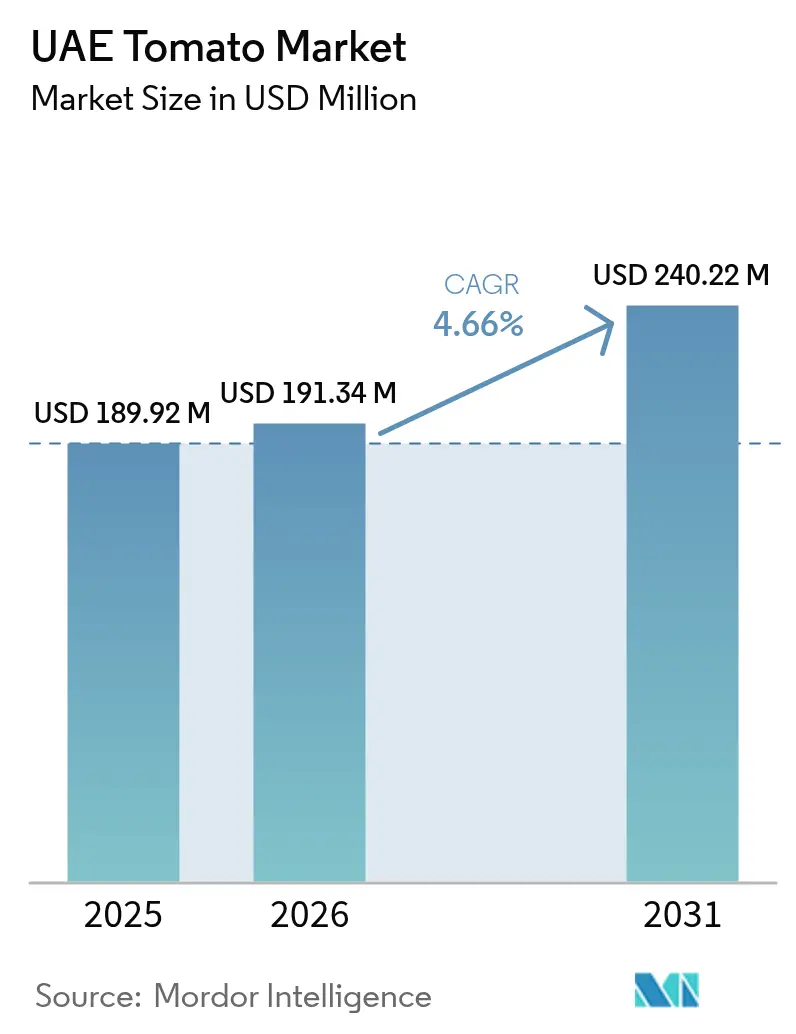

The UAE tomato market size was valued at USD 189.92 million in 2025 and estimated to grow from USD 191.34 million in 2026 to reach USD 240.22 million by 2031, at a CAGR of 4.66% during the forecast period (2026-2031). Domestic supply still covers only 10-15% of annual demand, but the gap is closing as controlled-environment acreage expands under the National Farms Sustainability Initiative. The Emirates Development Bank approved AED 721 million (USD 196 million) in 2023 for agritech and food security projects, funneling capital toward high-tech greenhouse operators rather than open-field farms. Rapid e-grocery adoption in Dubai and Abu Dhabi boosts year-round consumption, while quick-service restaurant chains insist on consistent color and shelf life conditions that imported commodity tomatoes often fail to meet. Retailers report consumer willingness to pay 20-40% premiums for locally grown, high-brix varieties, reinforcing the commercial logic behind climate-controlled cultivation.

Key Report Takeaways

- Tomato cultivation in the United Arab Emirates is transitioning from traditional farming methods to advanced indoor and hydroponic systems to address the challenges posed by harsh desert conditions. Key production areas include Abu Dhabi, Dubai, and Ras Al Khaimah, with a focus on year-round, climate-controlled, water-efficient greenhouse farming.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Tomato Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of climate-controlled greenhouse acreage | +0.8% | National, strongest in Abu Dhabi, Dubai, and Ras Al Khaimah | Medium term (2-4 years) |

| Government subsidy programs for smart farming | +0.7% | National, led by Ministry of Climate Change and Environment and Emirates Development Bank | Short term (≤ 2 years) |

| Rising demand from quick-service restaurant chains | +0.5% | National, hospitality corridors of Dubai and Abu Dhabi | Medium term (2-4 years) |

| Surge in e-grocery adoption driving tomato consumption | +0.4% | National, urban centers of Dubai and Abu Dhabi | Short term (≤ 2 years) |

| High-brix specialty varieties unlocking premium export prices | +0.3% | National output with exports across Gulf Cooperation Council | Long term (≥ 4 years) |

| Emirate-level food security funds accelerating cultivar research and development | +0.2% | Abu Dhabi and Dubai with spillover to other emirates | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Expansion of Climate-Controlled Greenhouse Acreage

Controlled-environment agriculture is rapidly eclipsing open-field farming as growers confront extreme heat and water scarcity. The Abu Dhabi Investment Office earmarked AED 152 million (USD 41 million) for agritech partnerships that emphasize robotics and indoor cultivation. Capital outlays of AED 1.5-3 million (USD 408,000-817,000) per acre are mitigated by yields of 80-100 metric tons per acre and year-round harvest windows[1]Source: Ministry of Climate Change and Environment, “National Food Security Strategy 2051,” moccae.gov.ae. Federal procurement rules that climb from 70% local sourcing in 2025 to 100% in 2030 effectively lock in demand, enabling lenders to stretch tenors and lower collateral thresholds. The UAE tomato market, therefore, gains production resiliency as climate-controlled acreage scales up. Over the medium term, operators anticipate lower unit costs as economies of scale and technology learning curves converge.

Government Subsidy Programs for Smart Farming

The Emirates Development Bank AgriTech Loans Program has earmarked AED 100 million (USD 27 million) in 2023 with loan-to-value ratios up to 90% and grace periods up to 2.5 years[2]Source: Emirates Development Bank, “AgriTech Loans Program,” edb.gov.ae. Parallel input subsidies cover half the cost of seed, fertilizer, and crop-protection purchases for registered citizen farmers, closing the affordability gap for sophisticated hydroponic rigs. The AGRIX Accelerator further delivers 20-week cohorts that blend technical mentoring with market-access coaching, while Abu Dhabi Agriculture and Food Security Authority offers phytosanitary and extension services. Together, these schemes underwrite capital costs, derisk adoption, and equip growers with operational know-how, reinforcing the positive outlook for the UAE tomato market.

Surge in E-Grocery Adoption Driving Tomato Consumption

Online grocery platforms, including Carrefour, Noon, and Instashop, experienced double-digit order growth in 2025 as one-hour delivery became a standard service in Dubai and Abu Dhabi. Digital product listings emphasized details such as origin, harvest date, and pesticide-free claims, enabling greenhouse operators to market premium products like Pure Harvest Candy Tomatoes, priced at AED 15.99 for 350 grams (USD 12.44 per kilogram). These platforms also provided consumers with greater transparency and convenience, fostering trust and encouraging repeat purchases. Shorter fulfillment chains reduced spoilage and preserved flavor quality, attributes that resonated with health-conscious millennials. The convenience of these services increased the purchase frequency of cherry and vine tomato varieties, boosting retail velocity for locally grown produce and contributing to higher overall tomato consumption.

High-Brix Specialty Varieties Unlocking Premium Export Prices

Gulf retailers prize high-brix tomatoes for their sweetness and shelf life, paying premiums that reached EUR 3.50 per kilogram (USD 3.80) in the Netherlands during 2025. United Arab Emirates growers use closed-loop irrigation and climate sensors to drive soluble-solids accumulation, enabling price uplifts of 20-40% over commodity imports. Dubai’s free-zone logistics support re-exports to Oman, Qatar, and Bahrain without tariff drag, while traceability protocols help meet hotel procurement standards. These factors lift farm margins and validate the capital intensity of greenhouse builds, adding a structural growth lever for the UAE tomato market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated desalinated-water tariffs | -0.8% | National, most acute where groundwater is absent | Medium term (2-4 years) |

| Shortage of skilled agronomists | -0.6% | National, scarcity in controlled-environment know-how | Long term (≥ 4 years) |

| Volatile electricity prices impacting cooling costs | -0.5% | National, heavier burden on large greenhouses | Short term (≤ 2 years) |

| Limited arable land outside controlled environments | -0.3% | National, restricts open-field expansion | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Elevated Desalinated-Water Tariffs

Ninety percent of potable water in the United Arab Emirates is produced by desalination, and greenhouse operators often pay more than USD 0.50 per cubic meter once pumping and storage mark-ups are added to production costs of USD 0.306 recorded at Hassyan. Tomatoes consume 3-5 cubic meters per kilogram, so water outlays can reach 15-25% of operating expense. The Water Security Strategy 2036 urges 95% wastewater reuse, yet uptake lags because distribution pipes and salinity treatment remain under-built. Until recycled supply scales, tariffs will temper profitability and widen the affordability gap for smallholder entrants.

Volatile Electricity Prices Impacting Cooling Costs

Cooling systems account for 40-60% of greenhouse gas emissions from power consumption, while commercial tariffs fluctuate with global fuel indices. The Dubai Electricity and Water Authority reported a deferral balance of AED 367 million (USD 100 million) in 2024, as pass-through adjustments subjected users to commodity price volatility[3]Source: Dubai Electricity and Water Authority, “Integrated Report 2024,” dewa.gov.ae. Net-metering schemes under Shams Dubai and the five-megawatt caps in Abu Dhabi help mitigate peak demand, but the initial costs of solar installations remain significant. These schemes allow users to generate their own electricity and offset their consumption, thereby reducing their reliance on the grid. Despite these measures, until renewable energy sources fully offset cooling loads, margin compression is projected to persist.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Abu Dhabi holds the largest slice of controlled-environment acreage, buoyed by the Abu Dhabi Agriculture and Food Security Authority’s technical outreach and concessionary tariffs. Silal Food and Technology Company operates multi-hectare blocks that funnel fruit into defense, education, and health service kitchens under the 70% local rule effective in 2025. Net-metering allowances up to five megawatts further sweeten project economics, encouraging capital inflows and anchoring the emirate’s leadership in the UAE tomato market.

Dubai ranks as the fastest-growing geography. Vertical farms such as Badia Farms ride densified urban demand and 60-minute e-grocery windows to capture premium baskets. Subsidized electricity for Emirati-owned holdings, settled by a Department of Finance outlay of AED 2,234 million (USD 608 million) in 2024, indirectly cushions operating costs. Logistics connectivity at Jebel Ali Port and Dubai World Central Airport streamlines both inbound input flows and re-exports, accelerating scale-up plans announced by Pure Harvest Smart Farms.

The Northern Emirates, including Ras Al Khaimah, Fujairah, and Umm Al Quwain, host a mosaic of citizen-owned greenhouses that benefit from input subsidies but face higher transport costs. Lower land prices partially offset freight, though operators still rely on distributor networks such as Kibsons and Barakat to reach metropolitan shelves. Ministry-run extension centers in Sharjah and Ajman help disseminate pest-resistant cultivars and water-saving practices, aligning all emirates with the country’s 2051 food security targets. Collectively, geographic diversification insulates the UAE tomato market against localized climate shocks.

Competitive Landscape

The UAE tomato market features more than 38,000 licensed farms, yet is top-heavy fewer than 20 operators controlling most greenhouse capacity. Pure Harvest Smart Farms Limited, Elite Agro Projects LLC, and Silal Food and Technology Company PJSC leverage multiyear procurement contracts and deep balance sheets to commission Dutch glasshouses with automated climate and fertigation loops. Pure Harvest Smart Farms Limited’s USD 180.5 million raise in 2025 funds additional acreage and artificial-intelligence crop steering, reinforcing first-mover advantage.

Mid-tier players such as Emirates Hydroponics Farms LLC, Badia Farms LLC, and VeggiTech Farms LLC carve niches in cherry and vine varieties, banking on vertical stacks that promote pesticide-free branding and year-round micro-batches. In 2023, Carrefour’s partnership with the Ministry of Climate Change and Environment opened grading, packing, and last-mile distribution to 6,000 smallholders, slightly diluting the scale advantage of incumbents. Concessional financing under the AgriTech Loans Program makes it easier for cooperatives to retrofit evaporative pad and fan systems, nudging fragmentation lower.

Technology remains the decisive battleground. High-resolution multispectral imaging, Internet of Things telemetry, and algorithmic climate models push yields toward 100 metric tons per acre, halving unit costs relative to conventional tunnels. Operators are slow to digitize risk margin attrition when electricity or water surcharges are introduced. With white space in processing still unclaimed, several greenhouse firms are scouting for joint ventures to build tomato paste and sauce lines to lock in downstream value. Competitive intensity is forecast to heighten as subsidy sunsets near, prompting efficiency races across the UAE tomato market.

Recent Industry Developments

- January 2026: Dubai Municipality has launched the third Hatta Farming Festival, emphasizing local agriculture, with over 25 Emirati farmers presenting high-quality produce, including tomatoes. Among the notable participants is Hatta Farms, a sustainable local farm utilizing hydroponic techniques for a portion of its production. The farm is especially recognized for its fresh tomatoes.

- May 2025: United Arab Emirates agri-tech firm Silal has entered into a strategic partnership with China's Shouguang Vegetable Industry Group (SVG) to develop a USD 33 million smart agricultural technology hub in Al Ain, near Abu Dhabi. The facility, covering approximately 100,000 square meters, will incorporate artificial intelligence, robotics, and advanced greenhouse systems tailored to the United Arab Emirates's arid climate. It aims to cultivate over a dozen crop varieties, including tomatoes, while reducing water and fertilizer usage by up to 30%.

- February 2025: Pure Harvest Smart Farms Limited and PlanTFarm, have launched the redeveloped Al Ain farm. This facility is designed as a pioneering, multi-purpose, high-tech controlled environment agriculture (CEA) farming operation. The farm utilizes advanced AI-powered technology to deliver a new range of fresh, high-quality products, including tomatoes. These products will be divided between innovative branded consumer products and a resource-efficient animal fodder initiative.

UAE Tomato Market Report Scope

A tomato is a fruit that is commonly treated as a vegetable in culinary contexts. It is the edible, fleshy fruit of the plant Solanum lycopersicum, which belongs to the nightshade family (Solanaceae). Tomatoes are typically red when ripe, though they can also be yellow, orange, green, or purple, depending on the variety. The UAE Tomato Market Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, Regulatory Framework, Logistics and Infrastructure, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Tomato

| Production Analysis | Production Volume | |

| Area Harvested and Yield | ||

| Consumption Analysis (Value and Volume) | ||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume |

| Key Supplying Markets | ||

| Export Market Analysis | Export Value and Volume | |

| Key Destinations Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Tomato | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

How large will the UAE tomato market be by 2031?

Forecasts point to USD 240.22 million in sales by 2031, reflecting a 4.66% compound annual growth rate from 2026.

Which production method supplies most tomatoes within the country?

Controlled-environment systems such as hydroponic greenhouses and vertical farms supplied 85% of volume in 2025 and continue to gain share.

What are the main cost pressures on growers?

High desalinated-water tariffs, electricity for cooling, and limited skilled agronomy labor form the largest operating cost challenges.

How do government programs support new greenhouse projects?

Subsidies refund 50% of select inputs and concessional loans cover up to 90% of project value with long tenors, lowering the capital barrier for technology adoption.

Page last updated on: