Israel Fruits And Vegetables Market Analysis by ���ϲ�����

The Israel fruits and vegetables market size was valued at USD 6.60 billion in 2025 and is estimated to grow from USD 6.85 billion in 2026 to reach USD 7.95 billion by 2031, at a CAGR of 3.80% during the forecast period (2026-2031). Recent growth is based on the wider adoption of precision irrigation, which now serves roughly three-quarters of cultivated land, a new agrivoltaic framework that will generate 100 megawatts of dual-use solar energy for greenhouses, and convergence with the European Union's pesticide rules, which reduce compliance costs for exporters. Labor remains the chief bottleneck as the 32,490-person Thai quota covers just two-thirds of harvest needs, pushing cooperatives toward automation and vertical farming. Intensifying water salinity in the Sea of Galilee deters northern citrus and avocado growers, while fertilizer prices jumped in early 2026 after Gulf shipping disruptions tightened potassium nitrate and phosphorus supply. Even so, Europe continues to absorb premium greenhouse tomatoes and citrus, and Gulf Cooperation Council states now offer the steepest demand trajectory, reflecting normalization agreements that speed customs clearance.

Key Report Takeaways

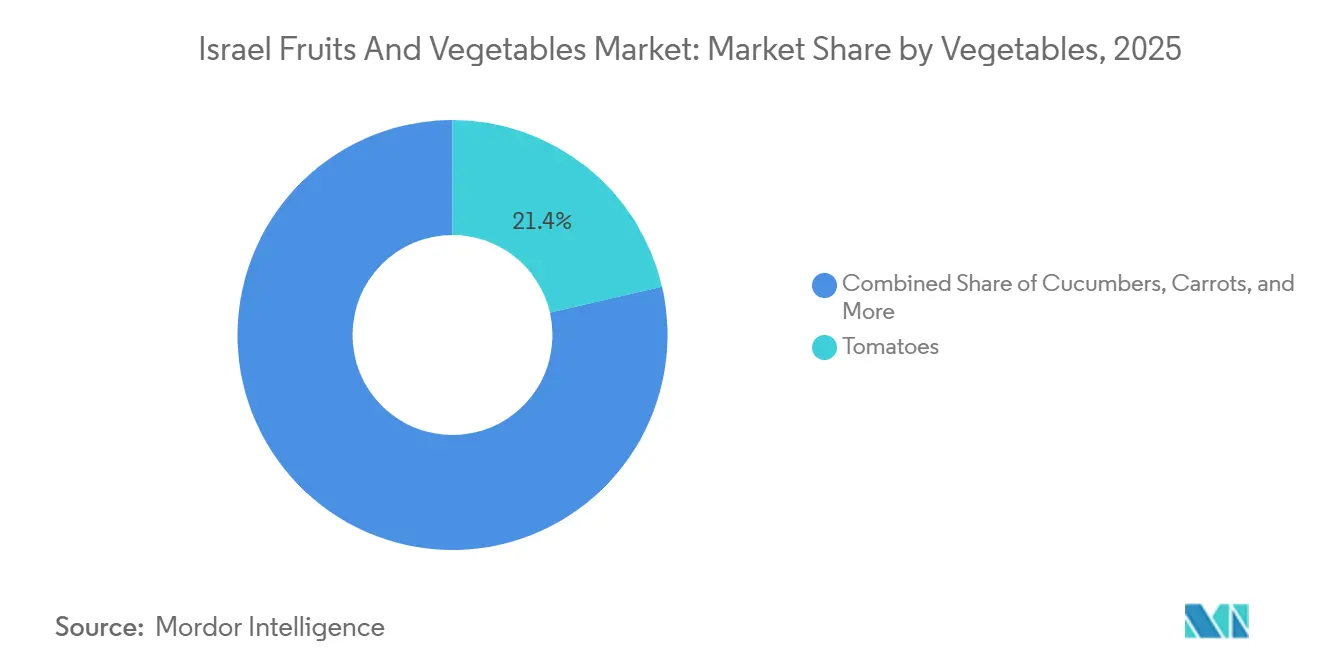

- By vegetable type, tomatoes led with the largest share, accounting for 21.4% of the Israel fruits and vegetables market share in 2025, whereas leafy greens have registered the fastest growth at 4.1% CAGR through 2026-2031.

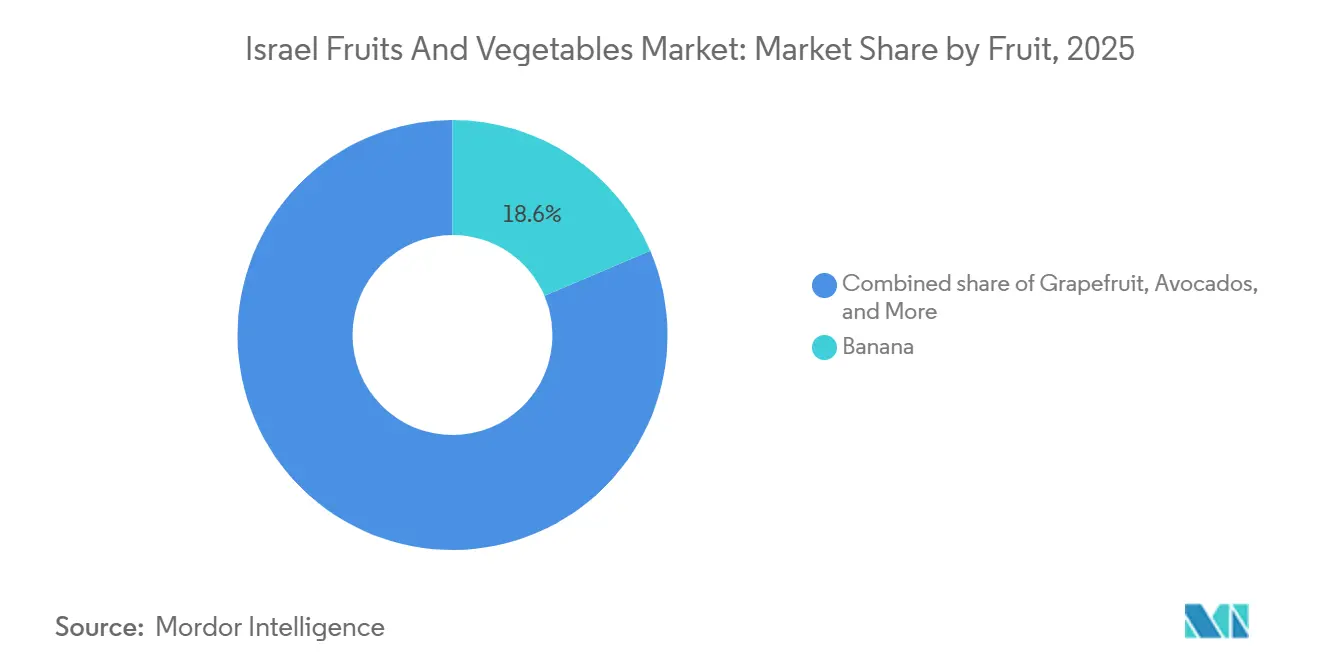

- By fruit type, bananas held the largest share, accounting for 18.6% of the Israel fruits and vegetables market size in 2025, whereas avocados are projected to register the fastest 4.4% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Israel Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in precision-irrigation adoption across Negev and Arava | +0.6% | National focus on Negev, Arava, and Jordan Valley | Medium term (2-4 years) |

| Government 50 MW Agri-PV pilot subsidies | +0.4% | Negev, Arava, and Gaza envelope | Long term (≥ 4 years) |

| European Union (EU) and Israel protocol easing pesticide-residue compliance | +0.5% | Nationwide, export-oriented growers | Short term (≤ 2 years) |

| Rapid expansion of the post-harvest cold-chain hubs in Judea and Galilee | +0.3% | Judea, Galilee, and northern corridors | Medium term (2-4 years) |

| Export premium for climate-neutral produce to Scandinavia | +0.2% | Nationwide, with spillover to Western Europe | Long term (≥ 4 years) |

| Controlled-environment farming breakthroughs in the Gaza envelope | +0.4% | Gaza envelope and southern border | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Surge in Precision-Irrigation Adoption Across Negev and Arava

The majority of Israel's cultivated land utilizes drip irrigation, positioning the country as a global leader in water-efficient agriculture. These systems achieve high water-use efficiency, significantly reducing water consumption while increasing crop yields, depending on the crop type and environmental conditions. In 2025, the Ministry of Agriculture earmarked NIS 44 million (USD 11.9 million) to digitize field data, enabling artificial intelligence platforms to further trim water use by 15%-30%[1]Source: Israel Innovation Authority, “Israeli Government Invests USD 13 Million to Establish Data Repositories for AI R and D,” iaeai.org. Growers in the Negev and Arava recycle drainage water and mix it with brackish groundwater to maintain export-grade tomatoes and peppers despite saline surface water. The Israel Water Authority has started pumping desalinated water into the Sea of Galilee, ensuring that irrigation gains are not negated by shrinking freshwater reserves. Together, efficient hardware and data tools sustain the Israel fruits and vegetables market even as droughts restrict Spain and Italy.

Government 50 MW Agri-PV Pilot Subsidies

A national outline plan approved in January 2026 sets a 30% field-coverage cap and minimum clearances so solar roofs do not block machinery[2]Source: Israel Ministry of Energy, “Solar Roofing Program Guidelines,” gov.il. In 2025, Bar-Ilan University field tests showed that 26% panel shade can boost the combined land value by 24% despite a 19.4% crop dip, paying back in roughly 13.5 years. Energy savings matter most to greenhouse operators in the Negev, where cooling drives summer bills to 20% or more of total costs. Early adopters report lower leaf temperatures and an extra crop cycle for strawberries and lettuce. Because crop revenue must stay higher than power revenue, Israel’s scheme keeps farmland productive while lowering operating costs, underpinning long-run growth for the Israel fruits and vegetables market.

European Union (EU) and Israel Protocol Easing Pesticide-Residue Compliance

Israel adopted European Union limits in August 2025, ending the need for dual spray calendars and heavy documentation. Harmonization arrives as supermarkets push pesticide-free shelves, giving Israeli growers a head start over Turkish or Moroccan peers. The rule still allows local sales to follow Codex limits, giving domestic channels flexibility. Exporters now market produce as meeting intra-EU safety norms, which eases entry into Germanic and Nordic chains that view Israel as a trusted supplier. Less paperwork cuts overhead, directly lifting margins inside the Israel fruits and vegetables industry.

Rapid Expansion of the Post-Harvest Cold-Chain Hubs in Judea and Galilee

Drought and conflict exposed weak storage, volunteers saved thousands of metric tons in 2024, but quick spoilage sliced returns by two-thirds. From 2025, co-ops pooled capital to fund modular refrigeration near Akko and Kiryat Shmona, reducing field heat within 90 minutes of harvest. Controlled-atmosphere rooms now let apple and pear growers drip-feed exports over five months, smoothing revenue and meeting weekly retail orders. Sensors feed blockchain logs that prove temperature integrity for European buyers. Better logistics reduce food loss, reinforcing both food security and profitability in the Israel fruits and vegetables market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cap on seasonal migrant labor permits | -0.5% | Gaza envelope and northern border hot spots | Short term (≤ 2 years) |

| Irrigation-water salinity spikes from Sea-of-Galilee transfers | -0.4% | Upper Galilee and Jordan Valley | Medium term (2-4 years) |

| Volatile shekel increasing input-cost uncertainty | -0.3% | Nationwide | Short term (≤ 2 years) |

| Biosecurity risk from Tomato Brown Rugose Virus (ToBRFV) | -0.3% | Nationwide, the European Union and North America trade | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Cap on Seasonal Migrant Labor Permits

As of October 2025, Israel allowed 32,490 Thai farm workers, leaving a 15,000-worker gap at harvest peaks. January 2026 rules allow service firms to hire foreigners on growers’ behalf, easing paperwork while still capping overall numbers[3]Source: Israel Population and Immigration Authority, “Foreign Agricultural Worker Authorizations 2025,” piba.gov.il. Pay climbs toward USD 1,700 per month, tempting many workers into better-paid construction jobs, thinning fields just when tomatoes ripen. Volunteer crews cover only one-tenth the productivity of trained pickers, so co-ops accelerate the adoption of optical sorters and robotic harvesters. Unless quotas rise, labor scarcity will check acreage expansion in high-touch crops, trimming upside for the Israel fruits and vegetables market.

Irrigation-Water Salinity Spikes from Sea-of-Galilee Transfers

As per the Israel Water Authority, Chloride levels in the lake neared 300 mg per liter in 2025 as inflows shrank, breaching the 250 mg yield threshold for citrus and avocado. Desalinated back-pumping began at 1,000 m³ per hour but raises the depth by only half a centimeter per month, far short of offsetting drought. Farms mix brackish well water with treated effluent, adding cost and limiting micronutrient uptake, and salt-tolerant rootstocks sacrifice 10%-15% yield. Northern growers debate switching to olives or almonds, which carry lower export premiums. Persistent salinity will test the resilience of the Israel fruits and vegetables industry unless larger desalination volumes materialize.

Segment Analysis

By Vegetable: Tomatoes Lead, Leafy Greens Surge

Tomatoes held the largest 21.4% of the Israel fruits and vegetables market share in 2025, reflecting entrenched domestic demand and mature greenhouse logistics that supply European retailers year-round. Leafy greens cultivated in vertical farms are projected to post the fastest 4.1% CAGR during 2026-2031, propelled by pesticide-free production, 90% lower water use, and proximity to urban consumers. Together, these two categories anchor investment strategies, growers expand high-Brix cherry tomato houses in the Arava, while tech start-ups install climate-controlled stacks near Tel Aviv to capitalize on subscription sales. Their complementary growth paths indicate that precision agriculture and controlled environments will continue to dominate capital flows within the vegetable market.

Cucumbers, carrots, and onions rank next in consumption, each benefiting from drip irrigation that lifts yield per cubic meter of water, yet facing tighter labor budgets that favor mechanization. Eggplants grown in the Jordan Valley serve both local and Jordanian markets but remain vulnerable to currency swings that raise seed costs. Cabbage, the smallest segment, supplies processors for coleslaw and sauerkraut rather than export chains, limiting upside in prices. Collectively, these secondary crops provide crop rotation benefits and hedge risk, but their slower growth underscores how future margins hinge on high-value greenhouse produce.

By Fruit: Avocados Accelerate, Bananas Stabilize

Bananas captured the largest 18.6% of the Israel fruits and vegetables market share in 2025, supported by year-round harvests in the Jordan Valley and coastal plains that secure domestic self-sufficiency. Avocados are forecast to post the fastest 4.4% CAGR over 2026-2031, driven by expanding Hass orchards, rising European off-season demand, and grower alliances that integrate Peru and Morocco acreage for uninterrupted supply. The divergent trends illustrate a shift from volume-oriented tropical staples toward premium healthy-fat snacks that command higher unit prices. As a result, exporters prioritize cold-chain and carbon-neutral certification to sustain avocado premiums while banana growers focus on disease-resistant cultivars to maintain steady output.

Grapefruit production, centered on Sweetie and Jaffa varieties, maintains niche appeal in Europe but faces reallocation of land toward higher-margin mandarins and avocados. Apples from the Golan Heights now rely on controlled-atmosphere storage to reduce seasonal price swings, while watermelons in sandy Negev soils gain share through seedless hybrids that satisfy urban convenience shoppers. Medjool dates continue to outperform most minor fruits thanks to consistent export demand and Israel’s drip-irrigated desert plantations, and kiwifruit remains a small yet promising category leveraging the Golan’s cool nights for off-season European delivery. These remaining segments round out the fruit basket, balancing revenue streams and insulating the industry from single-crop shocks.

Geography Analysis

Israel's fruit and vegetable sector prioritizes domestic consumption while optimizing for export markets, balancing food security with profitability. Geographical diversification across regions such as the Galilee, coastal plains, Jordan Valley, and Negev/Arava ensures year-round supply through climate variation and greenhouse technologies. The sector spans approximately 1.2 million hectares for fruit and 55,000 hectares for vegetables, ensuring consistent output to meet domestic demand. While staple vegetables like tomatoes and cucumbers are largely consumed locally, exports focus on premium-grade, longer shelf-life, or seasonal surplus produce. This approach aligns exports with high-value markets that emphasize quality, traceability, and off-season supply, complementing domestic stability.

Europe and the Middle East are the primary external demand centers, driven by distinct dynamics. Europe accounts for 34% of exports, supported by harmonized pesticide standards and demand for greenhouse-grown tomatoes, avocados, and citrus. These crops are cultivated in coastal and southern regions, where proximity to ports ensures efficient trade. The Middle East, the fastest-growing export region, benefits from normalization agreements that reduce border friction and Gulf retailers' demand for year-round fresh produce. Truck routes through Jordan now deliver leafy greens to Riyadh and Dubai within 48 hours, effectively extending Israel's domestic fresh-produce supply chain into premium neighboring markets.

Asia-Pacific markets, including Japan, South Korea, and Singapore, favor durable exports like citrus and root vegetables due to long transit times. Africa, while currently importing Israeli seeds and irrigation technology, represents a potential future partner for bilateral produce trade. Other regions, such as North America, South America, Russia, and Oceania, play niche roles, constrained by logistics and competition, but contribute to diversification, reducing reliance on core markets. Infrastructure upgrades and technological advancements are set to enhance integration across production, consumption, and export flows. Israel's fruit and vegetable market thrives on a synchronized model where geographically distributed production meets strong domestic consumption needs first, while exports act as a targeted value-enhancement channel.

Competitive Landscape

The combined revenue of the five largest firms, including Mehadrin, Arava Export Growers, Galilee Export, Carmel Agrexco Fresh Produce, and Tnuva Fresh Produce Division, accounted for a moderate share of the Israeli fruits and vegetables market in 2025, underscoring a fragmented competitive field. Arava Export Growers partnered with vertical-farm operators in early 2026 to supply hydroponic leafy greens to Gulf Cooperation Council buyers, signaling a pivot toward premium, climate-controlled produce. These moves show the two largest players are diversifying geography and technology to defend margins as labor and water constraints tighten at home.

Galilee Export scaled its Peru orchards in 2024, adding counter-seasonal avocados that keep European shelves stocked when Israeli harvests wane. Carmel Agrexco Fresh Produce expanded cold-chain capacity at Ashdod Port in late 2025, cutting transit time to Central European supermarkets by two days. Tnuva Fresh Produce Division upgraded its refrigerated hubs near Haifa in 2025, aiming to achieve farm-to-retail integration and secure display space in domestic supermarkets. Collectively, these companies use logistics and overseas acreage to smooth supply volatility and differentiate on freshness.

Looking ahead, leading firms plan wider agrivoltaic deployments to lower greenhouse gas emissions and support carbon-neutral labels sought by European chains. Continued investment in blockchain traceability will help exporters meet tightening food-safety audits and satisfy Gulf and Scandinavian buyers who demand shipment-level data. Companies are also courting venture-capital funds focused on artificial-intelligence irrigation and automated harvesting to curb labor shortages. Such strategic moves position market leaders to capture share from smaller cooperatives and to reinforce overall growth in the Israel fruits and vegetables industry.

Recent Industry Developments

- April 2026: Israel introduced a pilot program that lets farm service contractors recruit and manage foreign labor, lightening the quota burden on individual growers. This added staffing flexibility is anticipated to ease harvest bottlenecks, raise marketable volumes, and support steady revenue growth for the Israel fruits and vegetables sector.

- September 2025: Mehadrin unveiled a Moroccan project spanning 1,000 hectares of avocados and 400 hectares of citrus. The overseas venture secures counter-seasonal output, stabilizing export volumes and underpinning revenue growth when domestic harvests face water risks.

- August 2025: The Ministry of Health fully aligned Israel’s pesticide-residue standards with updated European Union limits, removing the need for separate domestic and export spray protocols. Streamlined compliance lowers testing costs and speeds border clearance, bolstering Israel’s competitiveness in Europe and paving the way for larger export volumes.

Israel Fruits And Vegetables Market Report Scope

Fruits and vegetables are important supplements to the human diet as they provide the essential nutrients for maintaining health. The Israel Fruits and Vegetables Market Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, Regulatory Analysis, List of Key Players, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Vegetable

| Tomatoes | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Cucumbers | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Carrots | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Onions | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Eggplants | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Leafy Greens | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Cabbage | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

By Fruit

| Grapefruit | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Bananas | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Avocados | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Watermelons | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Apples | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis |

| By Vegetable | Tomatoes | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Cucumbers | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Carrots | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Onions | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Eggplants | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Leafy Greens | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Cabbage | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| By Fruit | Grapefruit | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Bananas | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Avocados | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Watermelons | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Apples | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

Key Questions Answered in the Report

What is the current size of the Israel fruits and vegetables market?

The Israel fruits and vegetables market size was USD 6.85 billion in 2026.

Which vegetable segment is the largest in Israel?

Tomatoes held the largest 21.4% share of vegetable output in 2025, maintaining leadership through their integration with precision greenhouses.

Which fruit segment is expanding the fastest in Israel from 2026 to 2031?

Avocados are forecast to grow at the fastest 4.4% CAGR during 2026-2031, bolstered by expanding Hass orchards and rising European demand.

Which export region offers the highest growth opportunity?

Western Asia, particularly the Gulf Cooperation Council countries, offers significant growth opportunities for Israeli produce exports during 2026-2031.

How concentrated is the supplier landscape?

The top five players command only a moderate share of Israel's fruit and vegetable market, indicating a low concentration score of 3 and a fragmented supplier base.

What technology is most critical for future yield gains?

Precision irrigation combining drip lines with real-time data analytics is anticipated to deliver the biggest incremental water savings and yield improvements across Israeli horticulture.

Page last updated on: