Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

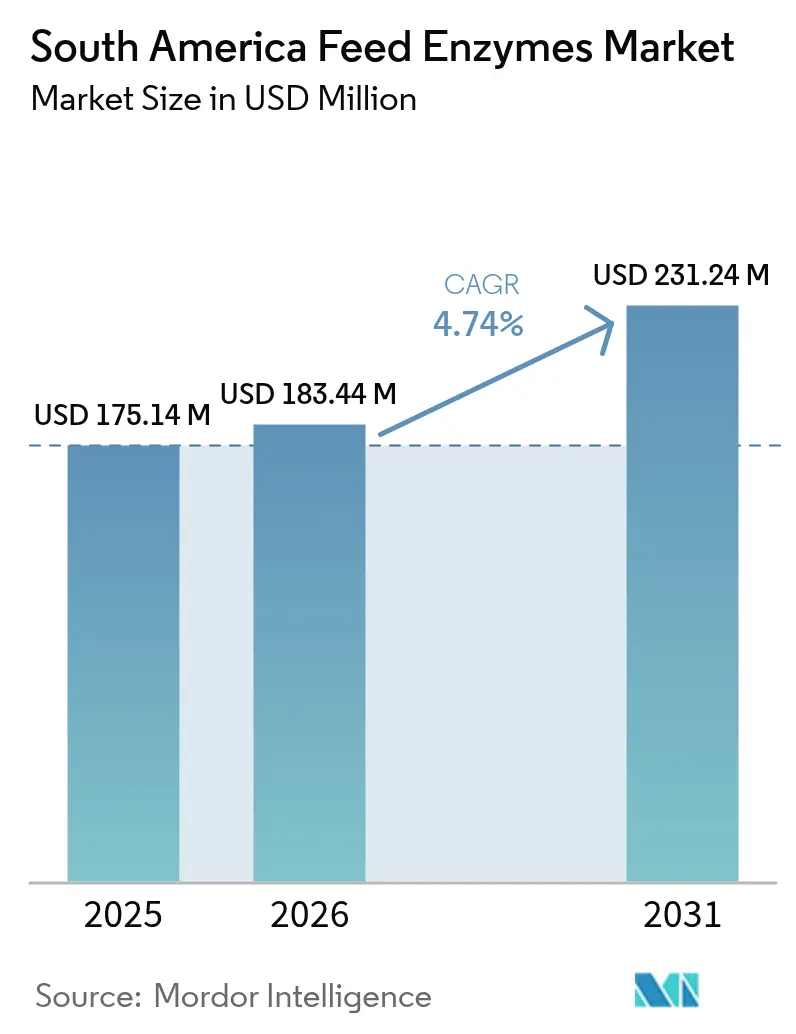

| Base Year Market Size (2025) | USD 175.14 Million |

| Market Size (2026) | USD 183.44 Million |

| Market Size (2031) | USD 231.24 Million |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

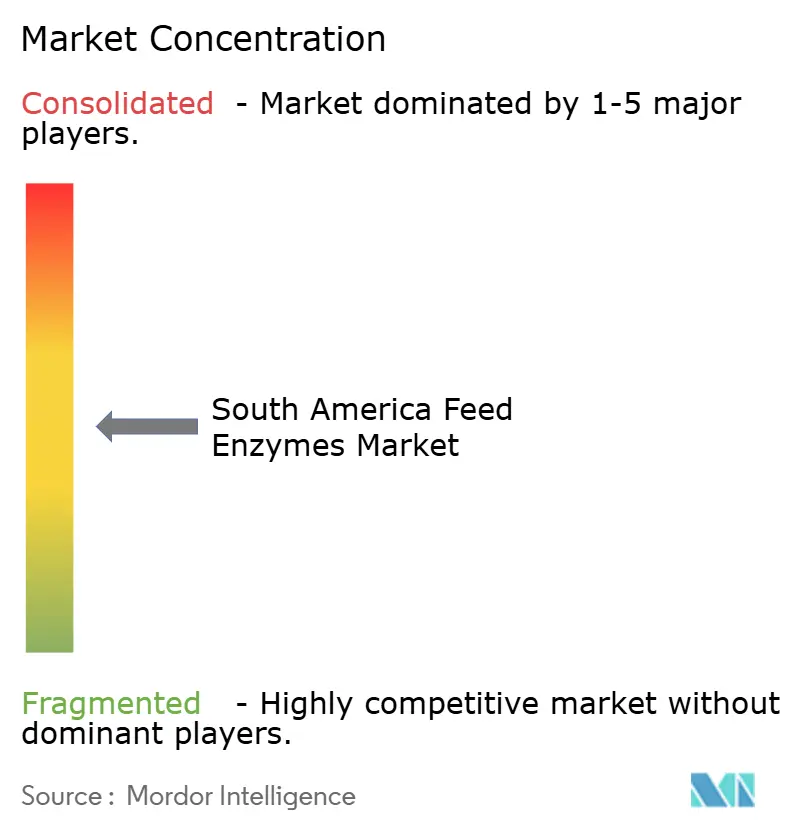

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

South America Feed Enzymes Market Analysis by ���ϲ�����

South America feed enzymes market size in 2026 is estimated at USD 183.44 million, growing from 2025 value of USD 175.14 million with 2031 projections showing USD 231.24 million, growing at 4.74% CAGR over 2026-2031. The growth is driven by the region's expanding livestock population, particularly in poultry and beef sectors, which increases the demand for enzyme-based feed additives that improve nutrient absorption and reduce feed costs. The regulatory shift away from antibiotic growth promoters and the rising costs of imported materials have accelerated the adoption of enzyme technologies that improve feed efficiency. The market is further strengthened by developments in heat-resistant, multi-carbohydrase enzymes specifically designed for corn-soy feed formulations. Market competition has intensified between established companies and regional specialists, resulting in new product development, collaborative ventures, and local manufacturing facilities to manage currency risks and improve market access.

Key Report Takeaways

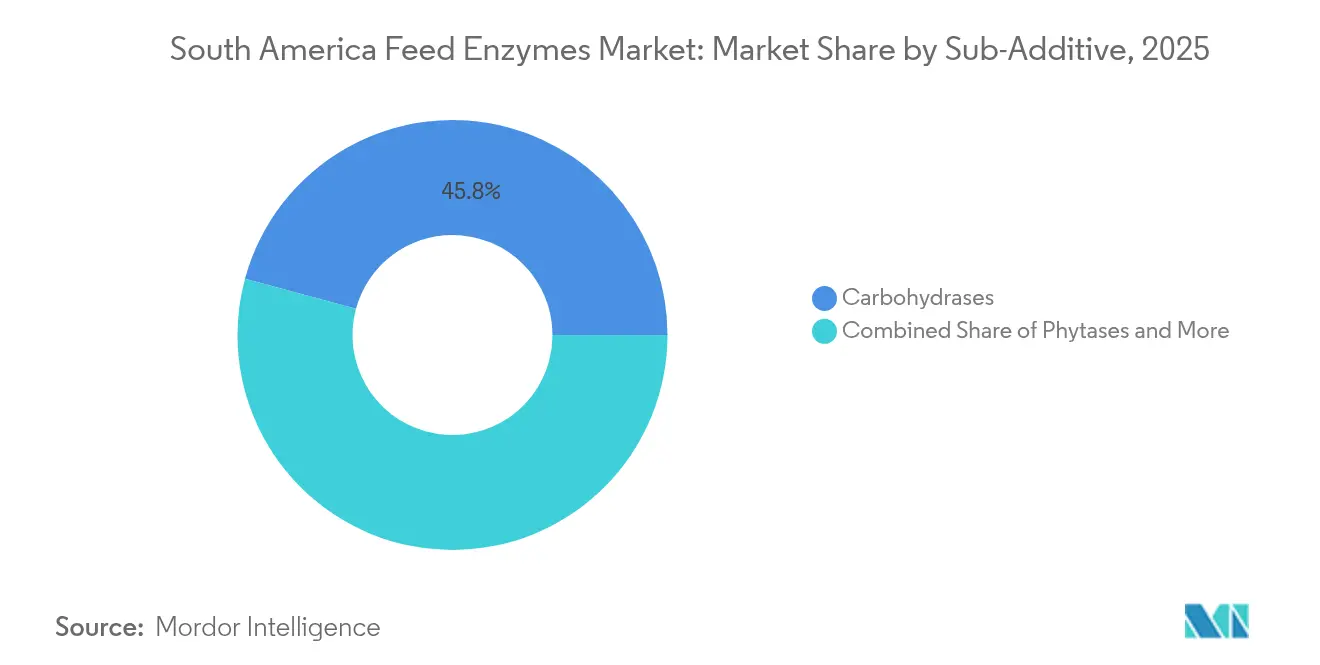

- By sub-additive, carbohydrases led with 45.78% of the South America feed enzymes market share in 2025; phytases are advancing at a 4.86% CAGR through 2031.

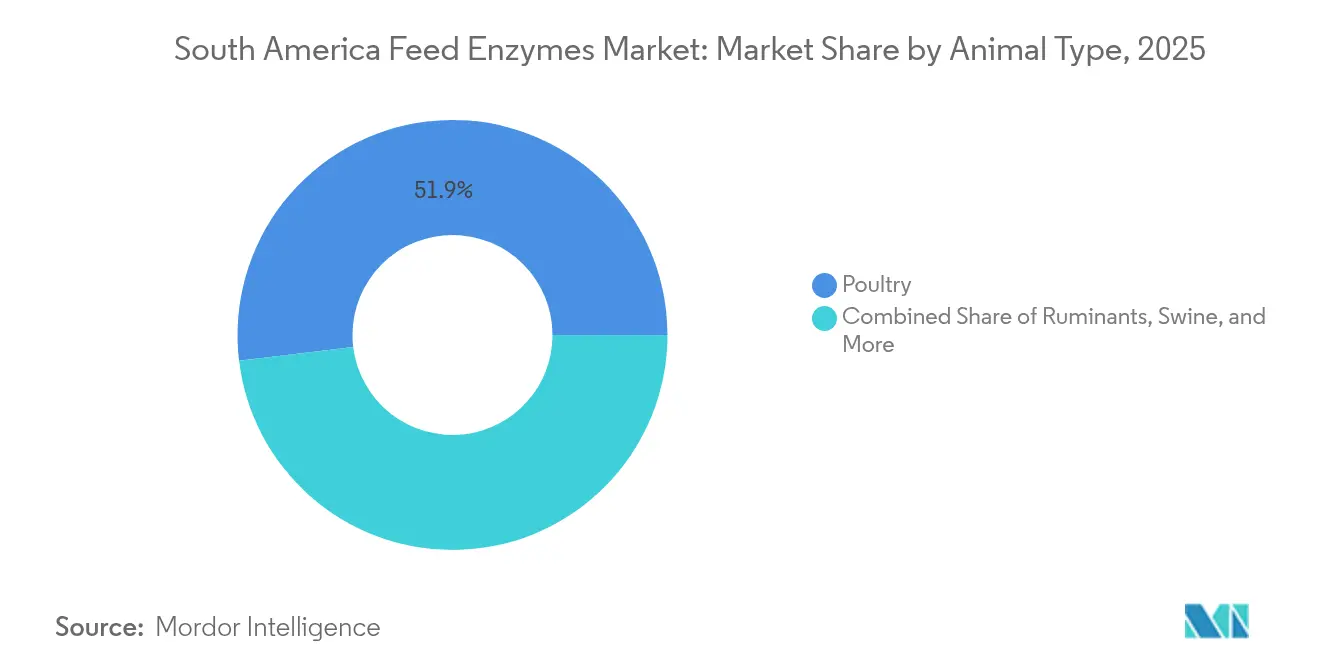

- By animal, poultry applications captured 51.92% of the South America feed enzymes market size in 2025, while ruminants are poised to expand at a 5.03% CAGR to 2031.

- By geography, Brazil commanded 56.93% of the South America feed enzymes market in 2025; Chile is forecast to grow at a 5.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Feed Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust growth of South American poultry production | +1.2% | Brazil, Argentina, Chile, spillover to Peru | Medium term (2–4 years) |

| Rising cost-benefit focus on feed efficiency | +0.9% | Region-wide with early gains in Brazil and Argentina | Short term (≤ 2 years) |

| Regulatory shift limiting antibiotic growth promoters | +0.8% | Argentina, Brazil, and Chile | Long term (≥ 4 years) |

| Expansion of integrated aquaculture value chains | +0.6% | Chile and Ecuador with extension to Brazil | Medium term (2–4 years) |

| Enzyme innovations targeting high-fiber feed meal | +0.5% | Brazil and Argentina grain belts | Long term (≥ 4 years) |

| Commodity price volatility spurring enzyme adoption | +0.4% | Global driver concentrated in Brazil | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Robust Growth of South American Poultry Production

Brazil's poultry slaughter volumes reached 6.4 billion birds in 2024, establishing a substantial production base that depends on marginal improvements in feed conversion ratios to maintain global competitiveness[1]Source: Brazilian Institute of Geography and Statistics, “Quarterly Survey of Animal Slaughter – 4Q 2024,” ibge.gov.br. Integrated producers utilize nutrition software to analyze corn-soy digestibility patterns and supplement feed with carbohydrases and proteases to optimize nutrient absorption. In Chile, vertically integrated processors prefer liquid enzyme formulations for easier dosing in automated feed systems, despite cold storage requirements. Argentina experienced increased enzyme registrations following currency stabilization, indicating higher investment in performance additives. The poultry industry's scale, data-driven operations, and focus on efficiency improvements generate consistent enzyme demand through repeat purchases.

Rising Cost-Benefit Focus on Feed Efficiency

Feed traditionally constitutes a substantial portion of total production expenses for poultry and swine operations across South America. The significant fluctuations in soybean prices within quarterly periods have compelled nutritionists to investigate and implement alternative solutions to recover diminished profit margins. Comprehensive broiler trials conducted in southern Brazil demonstrated measurable improvements in feed conversion rates when implementing multi-enzyme complexes targeting non-starch polysaccharide enzymes and phytate, compared to conventional single-mode carbohydrases. Agricultural enterprises in Argentina that implemented strategic forward contracts for comprehensive enzyme packages documented improved operational breakeven points, despite experiencing local currency depreciation. Given that enzyme supplementation represents a minimal investment per metric ton of finished feed, even modest improvements in digestibility efficiency translate into substantial cost savings for large-scale integrated operations. The combination of demonstrable financial returns and increasing sustainability compliance requirements has transformed enzyme supplementation from an optional feed component into an essential operational necessity.

Regulatory Shift Limiting Antibiotic Growth Promoters

Brazil, Argentina, and Chile aligned their feed antibiotic regulations with European standards in 2024, prohibiting prophylactic antibiotic growth promoter (AGP) inclusion in commercial feed formulations[2]Source: Brazilian Ministry of Agriculture, “Antibiotic Restrictions in Animal Feed,” gov.br. The removal of antibiotic-based performance enhancers required feed manufacturers to identify alternative solutions, with enzymes emerging as the primary substitute due to their minimal residue profile. Feed trials conducted by DSM-Firmenich AG and BASF SE demonstrated that xylanase and phytase enzyme combinations achieved equivalent or better weight gain in broilers compared to AGP-based formulations. Regulatory bodies expedited enzyme approval processes as part of their public health initiatives, reducing authorization timelines for established enzyme strains. This regulatory shift represents a permanent change, creating sustained demand for enzyme incorporation across all livestock segments.

Expansion of Integrated Aquaculture Value Chains

Chile's salmon industry reached a record harvest of 1.2 million metric tons in 2024, while Ecuador's shrimp production exceeded 1 million metric tons. Both industries operate under strict feed-conversion limits to comply with environmental discharge regulations[3]Source: National Fisheries and Aquaculture Service of Chile, “Aquaculture Production Statistics 2024,” sernapesca.cl. The use of enzymes engineered for diets with reduced fish meal helps decrease nitrogen and phosphorus discharge, enabling producers to meet regulatory biomass limits while maintaining growth rates. Tilapia producers in Brazil's Mato Grosso region have implemented similar standards, requiring local feed manufacturers to incorporate protease and beta-mannanase in their extruded feed products. Companies like Kerry Group and Vitapro collaborated in 2022 to develop premium, heat-stable formulations that maintain effectiveness at temperatures up to 130°C. The high value per metric ton of aquafeed allows enzyme suppliers to command premium prices while providing farmers with favorable returns on investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited cold-chain logistics for liquid enzymes | -0.7% | Rural Argentina and Chile | Short term (≤ 2 years) |

| Fragmented enzyme distribution channel | -0.5% | Brazil and Argentina interior regions | Medium term (2–4 years) |

| Currency depreciation pressuring import costs | -0.4% | Argentina and Brazil | Short term (≤ 2 years) |

| Slow regulatory approvals for novel enzyme strains | -0.3% | Region-wide | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Limited Cold-Chain Logistics for Liquid Enzymes

Liquid enzymes provide higher substrate specificity and faster dissolution compared to dry alternatives. They require refrigerated transport and storage, which is not readily available in many remote ranching locations. In northern Argentina, power outages that last several hours can compromise product quality during transit[4]Source: Brazilian Cold Chain Association, “Cold Chain Infrastructure Assessment 2024,” abracadeia.com.br. In Chile, fjord-based aquaculture facilities accessed via narrow mountain roads face limited refrigerated transportation capacity outside peak salmon harvest periods. Consequently, nutritionists often choose coated dry enzymes that can withstand storage at 25°C, despite their slightly lower performance. While suppliers are developing solutions such as phase-change packaging and enzyme-on-carrier beads to address temperature control challenges, high costs have limited their widespread adoption.

Fragmented Enzyme Distribution Channel

The feed ingredient market in South America operates through numerous local dealers, cooperatives, and independent brokers. The lack of dedicated nutritionists at many distribution points affects proper product usage protocols, leading to suboptimal results and negative product perception[5]Source: Brazilian Feed Industry Association, “Distribution Channel Analysis,” sindirações.org.br . Small-scale cattle producers in regions like Goiás and Córdoba face long travel distances to access feed supplies, creating inventory management challenges for retailers. While companies such as Brenntag SE and Novus International, Inc. have established extensive technical service networks, remote border regions remain underserved. The fragmented distribution landscape requires enzyme manufacturers to maintain larger field service teams compared to North America and Europe, resulting in higher selling, general, and administrative costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Additive: Carbohydrases Lead Through Corn–Soy Optimization

Carbohydrases accounted for 45.78% of the South America feed enzymes market share in 2025. These enzymes break down non-starch polysaccharides in corn and soybean meals, which are primary components of regional feed formulations. The widespread adoption of pelleted feed has increased, as current xylanase and beta-glucanase formulations maintain 90% effectiveness even after exposure to 90 °C conditioning temperatures. Poultry producers report 3-point improvements in feed conversion ratios with carbohydrase supplementation, making the enzyme cost-effective. Manufacturers increase market penetration by combining carbohydrases with phytase and protease in unified premix packages, optimizing feed-mill operations.

Phytases are experiencing the highest growth rate at 4.86% CAGR through 2031, driven by stricter environmental regulations on phosphorus discharge in poultry and aquaculture waste. Advanced phytases function optimally at lower gastric pH levels, improving phosphorus digestibility in broilers and reducing the need for mono-dicalcium phosphate supplements. The development of multi-phytase combinations specifically for high-phytic-acid soybean varieties in Mato Grosso enhances phosphorus extraction efficiency and meets the sustainability requirements of export markets.

By Animal: Poultry Dominance Meets Ruminant Growth Potential

Poultry accounts for 51.92% of the South America feed enzymes market size in 2025. This dominance stems from standardized feeding protocols and precise performance monitoring that enable efficient enzyme utilization. Feed mills incorporate enzyme dosing specifications into their Supervisory Control and Data Acquisition (SCADA) systems, ensuring accurate inclusion rates in each batch. The short six-week growth cycle of broilers allows nutritionists to quickly evaluate performance metrics and adjust formulations, making enzyme supplementation a standard practice.

The ruminant segment is projected to grow at a 5.03% CAGR through 2031 in the South America feed enzymes market. Brazil's cattle slaughter reached 32.4 million heads in 2024, indicating a shift from traditional grazing to feedlot operations using total mixed rations suitable for enzyme supplementation. The use of cellulase and hemicellulase enzymes improves neutral detergent fiber digestibility, reducing both feeding duration and methane emissions per kilogram of beef. In Argentina, dairy farms are incorporating protease in corn-silage-based diets to enhance bypass protein levels, increasing milk production without additional protein costs. These successful implementations are driving wider adoption in the ruminant sector, despite its historically limited use of feed additives.

Geography Analysis

Brazil holds 56.93% of the South America feed enzymes market share in 2025, supported by its extensive livestock operations and integrated agribusiness networks. The 2024 ban on prophylactic antibiotics in feed by Brazil's Ministry of Agriculture has created sustained demand for enzyme alternatives. While currency depreciation increases feed additive costs, exporters continue to implement efficiency-enhancing enzymes like xylanase to maintain competitive pricing globally. The emergence of local blending facilities near Mato Grosso grain hubs provides customized enzyme premixes, reducing delivery times and protecting buyers from currency fluctuations.

Chile projects the highest growth rate at 5.24% CAGR, expanding its market share through 2031. The country's integrated salmon industry depends on specialized diets incorporating protease and phytase additives to maximize protein and phosphorus utilization from plant-based meals, meeting the National Fisheries and Aquaculture Service's (SERNAPESCA) environmental regulations. The country's robust cold-chain infrastructure supports the distribution of liquid enzyme formulations, enabling improved feed conversion ratios.

Argentina's enzyme demand correlates with economic stability and regulatory progress. While the National Service of Agrifood Health and Quality (SENASA) approved 25 new enzyme products in 2024, currency instability and distribution challenges limit adoption in remote cattle-producing regions. Dairy sector modernization and increased feedlot operations indicate future growth in ruminant feed enzyme usage. Other regional markets, including Colombia, Peru, and Ecuador, comprise a smaller market share but demonstrate significant unit growth through expanding aquaculture and layer operations. Ecuador's shrimp industry utilizes protease in fish-meal-free diets, while Colombian poultry integrators adopt Brazil's model for carbohydrase implementation.

Competitive Landscape

The South America feed enzymes market shows moderate fragmentation, with the top five vendors, Novonesis A/S, Brenntag SE, Kerry Group plc, Elanco Animal Health Inc., and Archer Daniels Midland Company, collectively controlling a significant market share in 2024. Novonesis A/S holds a significant share, while Brenntag SE maintains through its continent-wide distribution network and value-added formulation services that combine enzymes with organic acids and vitamins in single-trip delivery.

Kerry Group plc maintains a significant share through its region-specific enzyme formulations designed for corn-soy and wheat-bran rations. BASF SE and Evonik Industries AG each hold mid-single-digit shares, with significant investments in thermostable platforms and digital formulation tools for enzyme efficacy prediction. Regional biotech companies are entering the market by utilizing fermentation facilities in São Paulo state to produce xylanase and phytase, benefiting from competitive sugarcane molasses prices.

In 2022, Cargill invested USD 50 million to expand its São Paulo enzyme capacity, reducing lead times and mitigating foreign exchange risks. The market may experience consolidation as smaller companies face challenges with regulatory compliance and cold-chain requirements, making them potential acquisition targets. Established companies with existing local registrations maintain an advantage due to strict national approval processes. Competition increasingly focuses on integrated service offerings that combine enzymes with analytics, pellet-mill calibration, and precision nutrition software, moving beyond price-based competition.

South America Feed Enzymes Industry Leaders

Novonesis A/S

Brenntag SE

Kerry Group Plc

Elanco Animal Health Inc.

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Novonesis acquired DSM-Firmenich's share in the Feed Enzyme Alliance for USD 1.7 billion (EUR 1.5 billion). The acquisition enabled Novonesis to integrate the alliance's complete value chain by incorporating DSM-Firmenich's sales and distribution operations with its existing research, development, and production capabilities, strengthening its position in animal biosolutions.

- February 2025: Cargill and BinSentry formed a partnership to implement artificial intelligence (AI)-powered tools for optimizing animal feed ingredient and enzyme supply chains in Brazil. Through this collaboration, Cargill became the exclusive distributor of BinSentry's inventory management platform in Brazil, aiming to enhance efficiency and profitability for pork and poultry producers.

- May 2024: Innovad Group, a company in the animal nutrition market, acquired Oligo Basics, a Brazilian supplier of nutritional feed additives, including enzymes. This acquisition expands Innovad Group's presence in Brazil and combines the product portfolios of both companies to provide natural solutions.

South America Feed Enzymes Market Report Scope

Carbohydrases, Phytases are covered as segments by Sub Additive. Aquaculture, Poultry, Ruminants, Swine are covered as segments by Animal. Argentina, Brazil, Chile are covered as segments by Country.By Sub-Additive

| Carbohydrases |

| Phytases |

| Other Enzymes |

By Animal Type

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

By Geography

| Argentina |

| Brazil |

| Chile |

| Rest of South America |

| By Sub-Additive | Carbohydrases | |

| Phytases | ||

| Other Enzymes | ||

| By Animal Type | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Geography | Argentina | |

| Brazil | ||

| Chile | ||

| Rest of South America | ||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| ���Գپ������dzپ����� | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| �ʰ�������dzپ����� | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| ���Գپ��dz澱�岹�Գٲ� | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| �ʳ��ٴDz���Ծ����� | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| �վ��ٲ������Բ� | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| �ѱ�ٲ����DZ������� | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| ���Գ��⳾����� | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| ���Գپ�-���������Dz������� | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| �������ٱ�����dz����� | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| �����dz�����Dz���Բ��پ��Dz� | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| �Ѳ⳦�dzٴdz澱���Dz����� | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| �Ѳ⳦�dzٴdz澱�Բ� | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| �����������ٴDz���Ծ����� | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | ���������𱹾����پ��Dz� |

| �����ٳ��� | Lumpy Skin Disease Virus |

| ������ | African Swine Fever |

| �ұʴ� | Growth Promoter ���Գپ������dzپ����� |

| ������ | Non-Starch Polysaccharides |

| �ʱ��� | Polyunsaturated Fatty Acid |

| ���ڲ� | ���ڱ����ٴdz澱�Բ� |

| ���ұ� | Antibiotic Growth Promoters |

| �� | The Food And Agriculture Organization of the United Nations |

| �����ٴ� | The United States Department of Agriculture |

Research Methodology

���ϲ����� follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms