United States Feed Enzymes Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

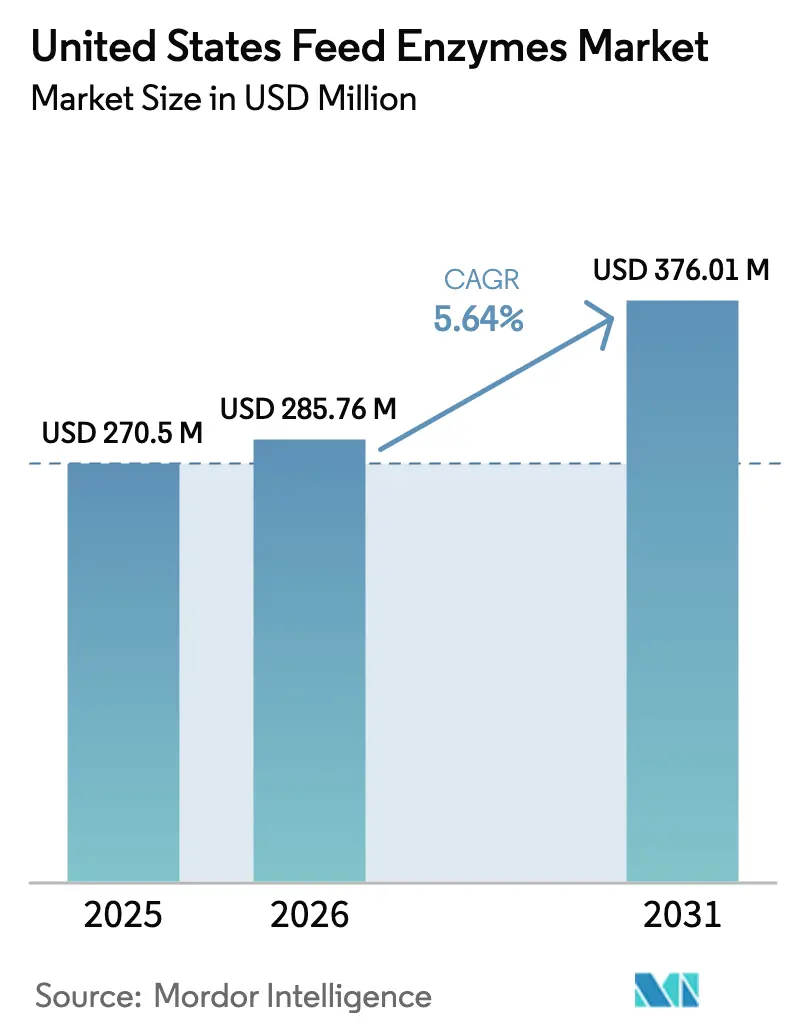

| Base Year Market Size (2025) | USD 270.5 Million |

| Market Size (2026) | USD 285.76 Million |

| Market Size (2031) | USD 376.01 Million |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

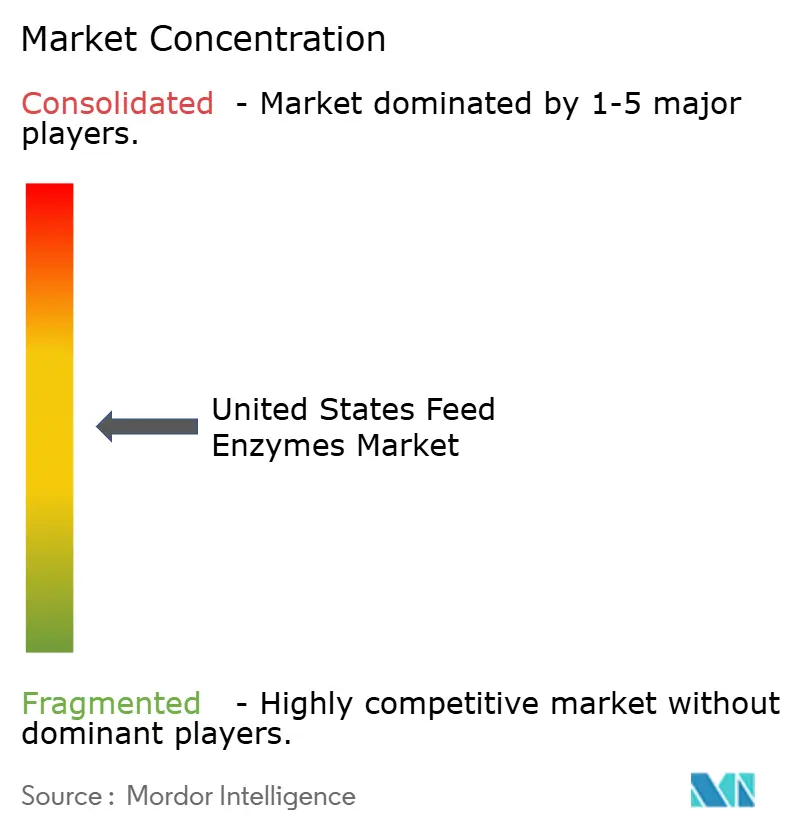

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

United States Feed Enzymes Market Analysis by ���ϲ�����

The feed enzymes market size is expected to grow from USD 270.5 million in 2025 to USD 285.76 million in 2026 and is forecast to reach USD 376.01 million by 2031 at 5.64% CAGR over 2026-2031. Growth momentum stems from cost-driven demand for higher feed conversion efficiency, a rising consumer appetite for animal protein, and the regulatory phase-out of antibiotic growth promoters, which pushes producers toward functional additives. Consolidation among suppliers is accelerating, highlighted by Novonesis acquiring DSM-Firmenich’s feed enzyme alliance[1]Source: Novonesis, “Novonesis Completes Acquisition of DSM-Firmenich Feed Enzyme Business,” novonesis.com . The uptake of thermostable multi-enzyme blends is increasing as feed mills standardize high-temperature pelleting to mitigate contamination risks, while the expansion of commercial aquaculture and stricter methane-reduction targets in ruminants further widens the addressable base for enzymatic solutions. Precision nutrition programs that match enzyme profiles to regional grain quality are emerging as a competitive differentiator, especially in the Midwest corn belt, where corn and soybean price volatility intensifies focus on digestibility improvements[2]Source: USDA Economic Research Service, “Livestock and Meat Domestic Data,” ers.usda.gov .

Key Report Takeaways

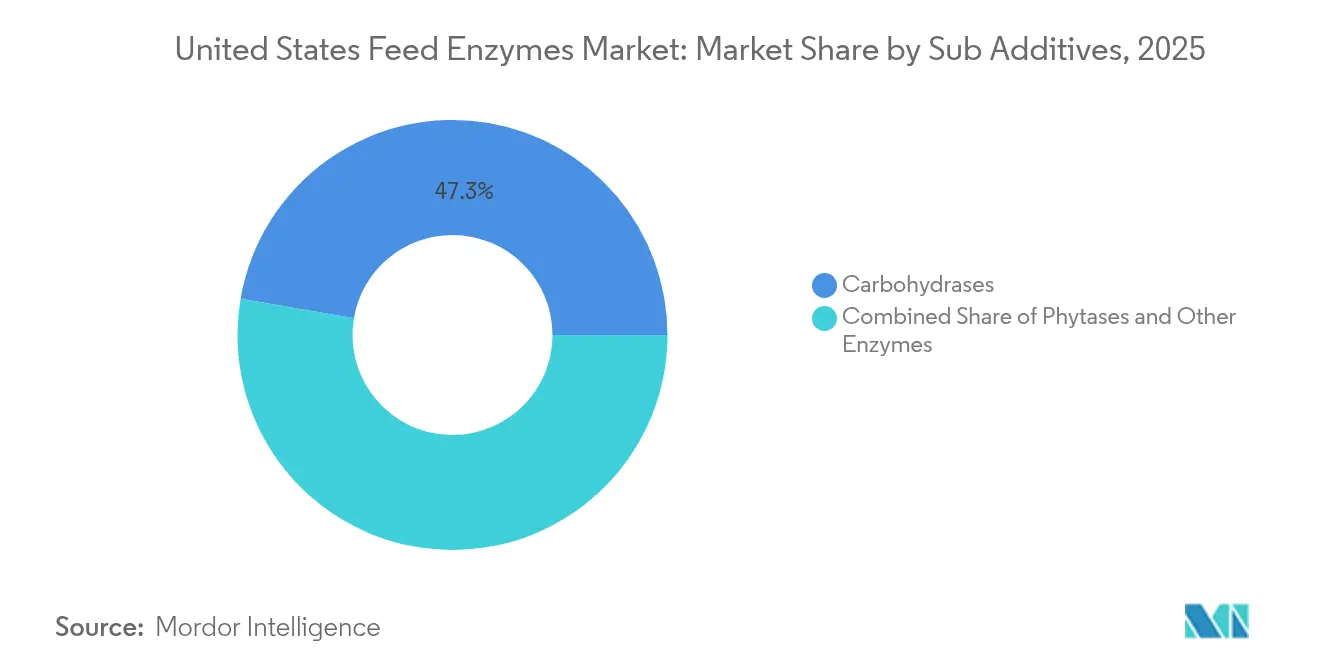

- By sub-additive, carbohydrases led with 47.31% revenue share in 2025, whereas phytases are projected to register the fastest 5.69% CAGR through 2031.

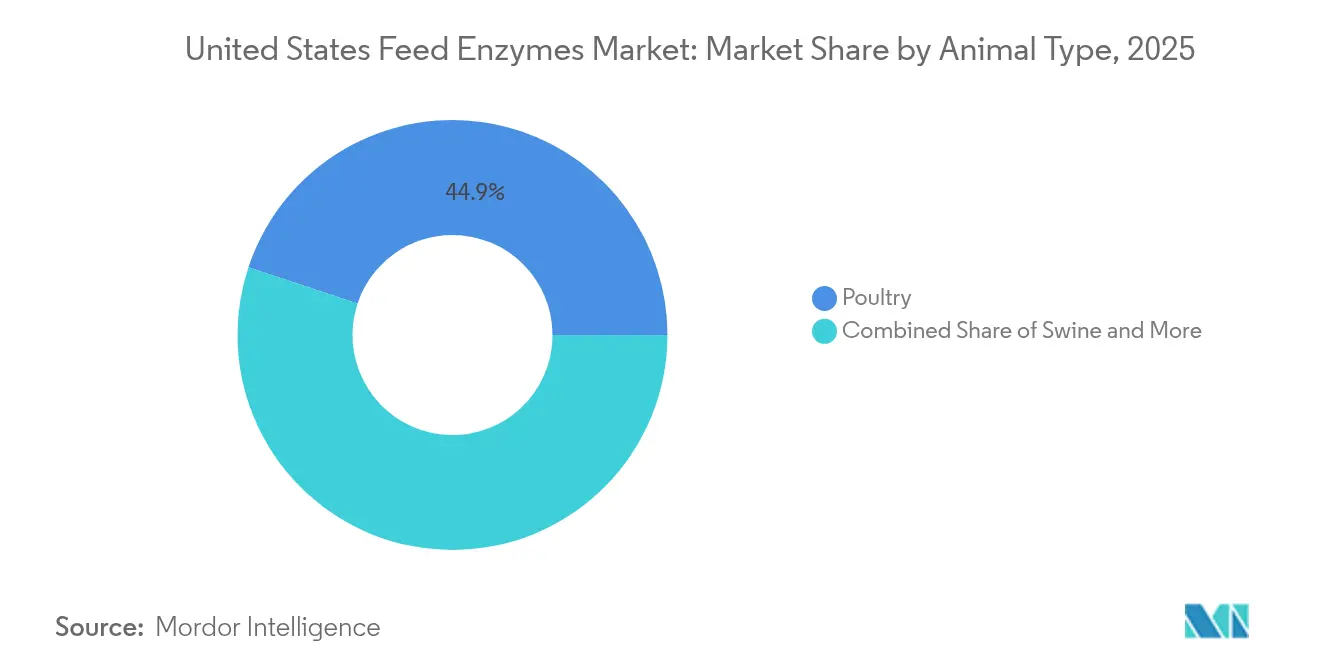

- By animal, poultry held 44.90% share of the feed enzymes market size in 2025, while ruminants are advancing at a 6.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Feed Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for animal protein | +1.80% | National, strongest in Midwest and Southeast | Medium term (2-4 years) |

| Ban on antibiotic growth promoters (AGPs) | +1.50% | National, FDA enforcement across all states | Short term (≤ 2 years) |

| Feed cost savings via better feed conversion ratios | +1.20% | National, highest relevance in corn belt | Short term (≤ 2 years) |

| Rapid expansion of commercial aquaculture | +0.90% | Coastal and inland aquaculture hubs | Long term (≥ 4 years) |

| Adoption of thermostable multi-enzyme blends in tropical markets | +0.60% | Southern states with high-temperature pelleting | Medium term (2-4 years) |

| Carbon-footprint labeling pressure on livestock producers | +0.40% | Early adoption in California and Northeast | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising Demand for Animal Protein

Per-capita meat intake in the country is substantial, with poultry alone accounting for half of the total, reinforcing a large baseline for nutritional efficiency technologies. Feed enzymes deliver 3–5% better feed conversion in commercial broilers, equivalent to USD 0.15–0.25 savings per bird under 2025 feed prices[3]Source: Poultry Science Association, “Enzyme Supplementation Improves Broiler Feed Conversion,” poultryscience.org . Population growth, projected at 8.2% by 2030, will add protein-oriented demographic groups, sustaining long-term enzyme demand. Integrators are increasingly embedding enzyme programs into least-cost formulation software, thereby strengthening the value proposition. Retailers’ focus on protein affordability supports volume uptake over premium pricing niches. Consequently, the feed enzymes market continues to closely align with the trajectory of U.S. meat production.

Ban on Antibiotic Growth Promoters (AGPs)

FDA’s Veterinary Feed Directive eliminated over-the-counter antibiotic use for growth promotion, pushing 95% of commercial poultry and 87% of swine producers to search for functional alternatives. Multi-enzyme blends that combine carbohydrase and phytase activities now underpin many replacement protocols, as they provide both nutrient release and gut health support. Early-adopter states such as California and New York increased enzyme inclusion rates faster due to stricter auditing. Supply chain stakeholders, from feed mills to integrators, demand data-rich dossiers demonstrating equivalence to former antibiotic benchmarks. Established brands with regulatory-approved portfolios thus secure first-mover advantages. The resulting sales uplift explains much of the near-term acceleration in the feed enzymes market growth.

Feed Cost Savings via Better Feed Conversion Ratios

Corn and soybean meal priced significantly per ton in 2024, triggering a stronger emphasis on nutrient release technologies that mitigate ingredient inflation. Phytase uptake increased 23% year-over-year, as it reduces the need for expensive inorganic phosphate inclusion. Economic modeling by integrators shows a 3.2:1 payback ratio under current price scenarios, compressing capital recovery periods to under six months. Feed mills are bundling enzyme packages within complete diet offerings to ease logistics and boost margin capture. The efficiency driver remains structurally supportive, given consensus forecasts for tight grain balances through 2026. As a result, feed conversion economics represent the clearest single determinant of near-term purchasing decisions.

Carbon-footprint Labeling Pressure on Livestock Producers

California and Northeast retailers are piloting beef and dairy carbon labels that quantify methane intensity, prompting producers to embrace methane-curbing feed strategies. Trials show enzyme inclusion reduces enteric methane by 8–12% in dairy cows without compromising milk yield. Sustainability-linked financing is beginning to incorporate feed efficiency metrics, making enzyme adoption a pathway to preferential borrowing costs. Large food brands have set 2030 Scope 3 reduction targets, integrating feed additives into supplier scorecards. As measurement protocols improve, anticipated monetization of carbon reductions will expand demand. This evolving compliance environment solidifies the long-term value proposition of feed enzymes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile fermentation-substrate prices | −0.8% | National, fermentation hubs in Midwest | Short term (≤ 2 years) |

| Lengthy multi-region regulatory approvals | −0.6% | National, FDA oversight plus state reviews | Medium term (2-4 years) |

| Limited efficacy in high-phytate insect-based feeds | −0.4% | Coastal and urban insect-farming zones | Long term (≥ 4 years) |

| Substitution threat from direct-fed microbials | −0.3% | National, strongest in organic and premium segments | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Volatile Fermentation-Substrate Prices

Prices for corn steep liquor surged in 2024, compressing enzyme producer margins and necessitating quarterly price adjustments. Fermentation inputs now compete with ethanol and bioplastic sectors, tightening supply. Large suppliers hedge exposure through multi-substrate plants and long-term farmer contracts, but smaller players lack similar buffers. Spot market volatility complicates feed mill planning, undermining the effectiveness of locked-in feed formulations. The shift drives consolidation as scale becomes critical to cost resilience. Unless substrate diversification advances rapidly, input inflation will continue to be a constraint on near-term market growth.

Lengthy Multi-region Regulatory Approvals

New enzyme approvals typically require 18–24 months under the FDA’s Food Additive Petition framework, with an additional three to six months in states such as California that impose further review. The escalating data burden favors incumbents with dedicated regulatory staff. Start-ups often pivot to contract-manufacturing or licensing rather than full commercialization. Slow approvals defer revenue capture on R&D pipelines, dampening investor appetite for novel enzyme modalities. Although global harmonization discussions continue, practical alignment remains limited. Prolonged timelines, therefore, temper the rollout of cutting-edge solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Carbohydrases Lead while Phytases Drive Future Growth

By sub-additive, carbohydrases led with 47.31% revenue share in 2025, underpinned by consistent 3–4% gains in metabolizable energy when xylanase and beta-glucanase are included in corn-soy diets. Their dominance stems from their broad applicability across poultry and swine rations, mature performance data, and compatibility with high-temperature pelleting, following recent advances in protein engineering. Thermostable variants have gained widespread adoption in the Southeast, where mills commonly operate at temperatures exceeding 90 °C. Despite maturing penetration, the segment is forecast to expand at a respectable CAGR through 2031 as integrators optimize dosing protocols and blend carbohydrases with proteases for synergistic effects. Carbohydrase revenue streams thus remain foundational to supplier profitability and R&D funding pools.

Phytases are projected to register the fastest 5.69% CAGR through 2031, aided by rising phosphorus prices and tightening discharge regulations. Their 2025 share remained moderate, yet installations in layer and swine diets increased 18% year over year. As phosphorus excretion limits tighten, phytase inclusion offsets inorganic phosphate usage, preserving diet cost balance while supporting sustainability scorecards. Next-generation products deliver higher activity retention after pelleting, improving unit economics. Over the forecast horizon, phytases are anticipated to capture incremental share, especially in ruminant methane-reduction programs where phosphorus availability links to feed efficiency gains. Close formulation alignment with specific high-phytate ingredients, including insect protein, positions phytase suppliers at the forefront of innovation, sustaining the feed enzymes industry growth narrative.

By Animal: Poultry Dominance Faces Ruminant Growth Challenge

Poultry applications commanded 44.90 percent market share in 2025, leveraging the sector's industrial scale and standardized production systems that facilitate consistent enzyme adoption, yet ruminants emerge as the fastest-growing segment with 6.02 percent CAGR driven by methane reduction mandates and carbon footprint pressures that favor feed efficiency improvements. Broiler operations within the poultry segment show the highest enzyme penetration rates at 78 percent of commercial facilities, reflecting the technology's proven return on investment in high-volume, cost-sensitive production environments where feed conversion improvements of 2-3 percent translate to significant economic benefits.

Ruminant applications benefit from emerging research on methane mitigation, with enzyme supplementation reducing enteric methane emissions by 8-12 percent in dairy cattle trials, creating regulatory compliance opportunities as carbon pricing mechanisms expand across agricultural sectors. Aquaculture represents the smallest but most dynamic segment, with specialized enzyme formulations for fish and shrimp feeds showing 28 percent annual growth as recirculating aquaculture systems require feeds that minimize waste production and maintain water quality parameters.

Geography Analysis

The Midwest corn belt accounted for the majority of 2025 sales, anchored by dense poultry and swine populations and integrated supply chains that favor bulk purchases of enzyme-enhanced concentrate. Regional corn and soybean production supports the development of least-cost formulations that benefit from the inclusion of carbohydrase and protease, thereby locking in baseline demand. Large on-farm feed mills typical of Iowa and Illinois negotiate multi-year supply agreements, stabilizing volume for major suppliers. State universities in the region conduct extensive extension work on enzyme efficacy, thereby reinforcing the credibility of adoption among producers.

The Southeast is the fastest-growing region. Broiler production continues to migrate toward Georgia, Alabama, and Mississippi due to their warmer climates and favorable labor economics, creating fresh demand for high-temperature-stable enzymes. Emerging aquaculture clusters in Alabama and North Carolina enhance protease and lipase uptake through diets rich in fishmeal substitutes. Distribution hubs near Savannah and Mobile optimize logistics for temperature-controlled additives, further improving service levels. Public-private partnerships, such as extension trials on shrimp feed digestibility, facilitate the rapid transfer of knowledge into commercial practice.

The West Coast and Northeast together represented moderate share of 2025 volume yet skew toward premium enzyme formulations. California’s Proposition 12 rules require cage-free systems that consume 12–15% more feed, prompting layer producers to deploy phytase and carbohydrase to offset cost penalties. Dairy operators in the Pacific Northwest use enzyme supplements to support milk yields under pasture-based systems with variable forage quality. Environmental regulations on nutrient runoff in Chesapeake Bay and Puget Sound accelerate phytase adoption to mitigate phosphorus discharge. Although absolute consumption lags that of the corn belt, higher per-ton additive spend elevates average selling prices, supporting niche-focused suppliers.

Competitive Landscape

Market leadership remains moderately concentrated, with the top five vendors holding a significant share of revenue in 2024. DSM-Firmenich AG led, leveraging a broad enzyme and vitamin portfolio that integrates technical services. Novonesis’ 2024 purchase of DSM-Firmenich’s feed enzyme alliance signals deeper consolidation and strengthens its position in thermostable technology. Archer-Daniels-Midland’s share benefits from vertical integration into feed milling, allowing direct pull-through of proprietary enzyme blends into finished rations.

Alltech follows, supported by yeast-based fermentation innovations that lower variable cost structures and enable the expansion of its specialty portfolio. Strategic focus across incumbents centers on capacity expansion and co-development partnerships. ADM is investing to increase its Decatur, Illinois, fermenter output by 40%, meeting rising demand for carbohydrase and phytase.

BASF launched Natuphos E phytase optimized for 90 °C pelleting, targeting mills seeking one-to-one replacement of older enzymes without over-formulation. Alltech partnered with Protix to design enzymes compatible with insect protein, positioning for future ingredient shifts. Distribution companies like Brenntag strengthen regional reach by acquiring specialized additive wholesalers, offering bundled logistics and technical support. Barriers to entry rise as regulatory data requirements and fermentation scale economics favor established players; yet, specialized firms can still succeed by targeting niche markets, such as aquaculture or organic livestock, with tailor-made solutions that larger firms overlook.

United States Feed Enzymes Industry Leaders

Alltech, Inc.

Archer Daniel Midland Co.

Brenntag SE

IFF(Danisco Animal Nutrition)

DSM-Firmenich AG (Novonesis A/S)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Novonesis completed the acquisition of DSM-Firmenich’s feed enzyme alliance, creating the sector’s largest dedicated enzyme supplier. This acquisition is anticipated to drive innovation and strengthen the development of the feed enzymes market in the United States.

- August 2024: BASF launched Natuphos E phytase, engineered for activity retention at 90 °C pelleting temperatures. This innovation is projected to support the growth of the United States feed enzymes market by enhancing feed efficiency and production processes.

- June 2024: International Flavors and Fragrances secured FDA approval for the first multi-enzyme blend registered specifically for recirculating aquaculture systems. This development is anticipated to drive innovation and growth in the United States feed enzymes market.

United States Feed Enzymes Market Report Scope

Carbohydrases, Phytases are covered as segments by Sub Additive. Aquaculture, Poultry, Ruminants, Swine are covered as segments by Animal.| Carbohydrases |

| Phytases |

| Other Enzymes |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| APAC | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of APAC | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Sub Additive | Carbohydrases | ||

| Phytases | |||

| Other Enzymes | |||

| By Animal | Aquaculture | Fish | |

| Shrimp | |||

| Other Aquaculture Species | |||

| Poultry | Broiler | ||

| Layer | |||

| Other Poultry Birds | |||

| Ruminants | Beef Cattle | ||

| Dairy Cattle | |||

| Other Ruminants | |||

| Swine | |||

| Other Animals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| APAC | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of APAC | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| ���Գپ������dzپ����� | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| �ʰ�������dzپ����� | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| ���Գپ��dz澱�岹�Գٲ� | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| �ʳ��ٴDz���Ծ����� | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| �վ��ٲ������Բ� | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| �ѱ�ٲ����DZ������� | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| ���Գ��⳾����� | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| ���Գپ�-���������Dz������� | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| �������ٱ�����dz����� | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| �����dz�����Dz���Բ��پ��Dz� | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| �Ѳ⳦�dzٴdz澱���Dz����� | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| �Ѳ⳦�dzٴdz澱�Բ� | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| �����������ٴDz���Ծ����� | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | ���������𱹾����پ��Dz� |

| �����ٳ��� | Lumpy Skin Disease Virus |

| ������ | African Swine Fever |

| �ұʴ� | Growth Promoter ���Գپ������dzپ����� |

| ������ | Non-Starch Polysaccharides |

| �ʱ��� | Polyunsaturated Fatty Acid |

| ���ڲ� | ���ڱ����ٴdz澱�Բ� |

| ���ұ� | Antibiotic Growth Promoters |

| �� | The Food And Agriculture Organization of the United Nations |

| �����ٴ� | The United States Department of Agriculture |

Research Methodology

���ϲ����� follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms