Rail Road Wheels Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

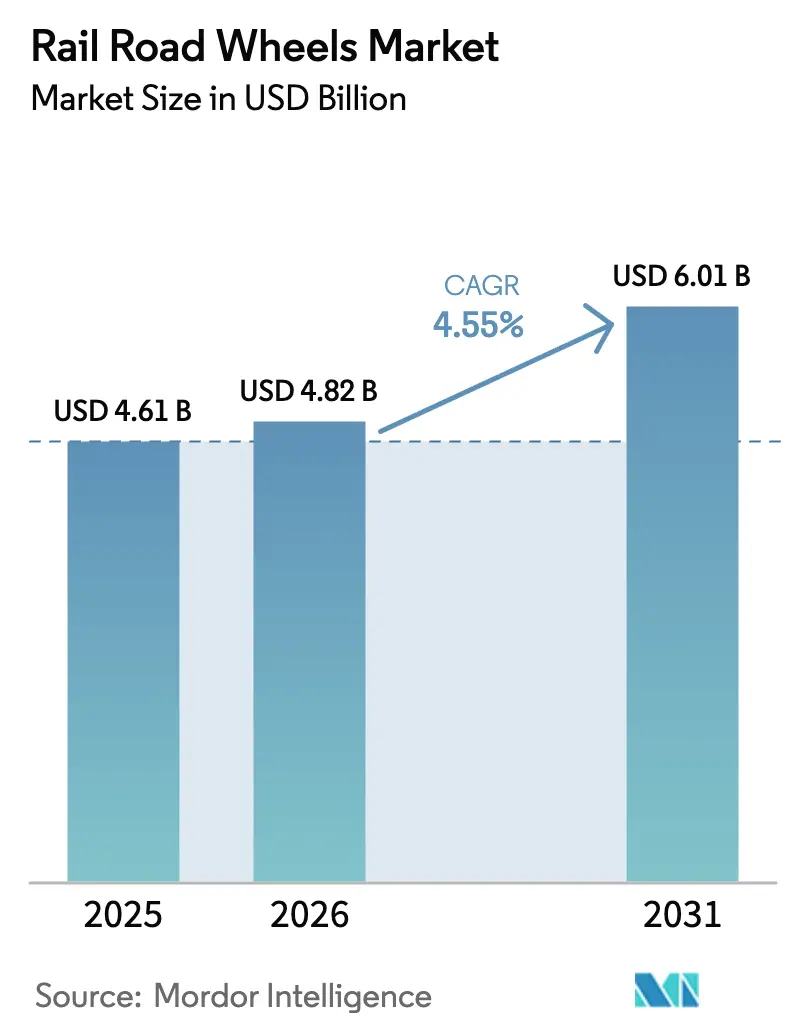

| Market Size (2026) | USD 4.85 Billion |

| Market Size (2031) | USD 6.08 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Rail Road Wheels Market Analysis by ���ϲ�����

The Rail Road Wheels Market size was valued at USD 4.64 billion in 2025 and is estimated to grow from USD 4.85 billion in 2026 to reach USD 6.08 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031). Despite fluctuations in raw material prices, the demand for forged, sensor-ready wheels is surging, driven by robust freight volumes, metro automation, and decarbonization mandates. Freight operations account for the bulk of revenue, but metro and monorail initiatives in Asia and the Middle East are experiencing steady growth. These cities are commissioning driverless lines that prefer lighter, low-noise wheels equipped with health-monitoring chips. Forged products hold a significant market share and are set to remain the gold standard, as operators prioritize fatigue resistance over the upfront savings from rolled or cast alternatives. While OEM channels account for a significant share of sales, the aftermarket is expanding due to pay-per-kilometre leasing. Maintainers are leveraging predictive analytics to prolong service life and synchronize replacement timing with fleet availability. The Asia-Pacific region, bolstered by China's suburban expansions and India's dedicated freight corridors, accounts for a substantial share of turnover. Meanwhile, the Middle East and Africa are experiencing the fastest growth, driven by Riyadh, Dubai, and Cairo's pursuit of greenfield metro systems centered on advanced wheel technologies.

Key Report Takeaways

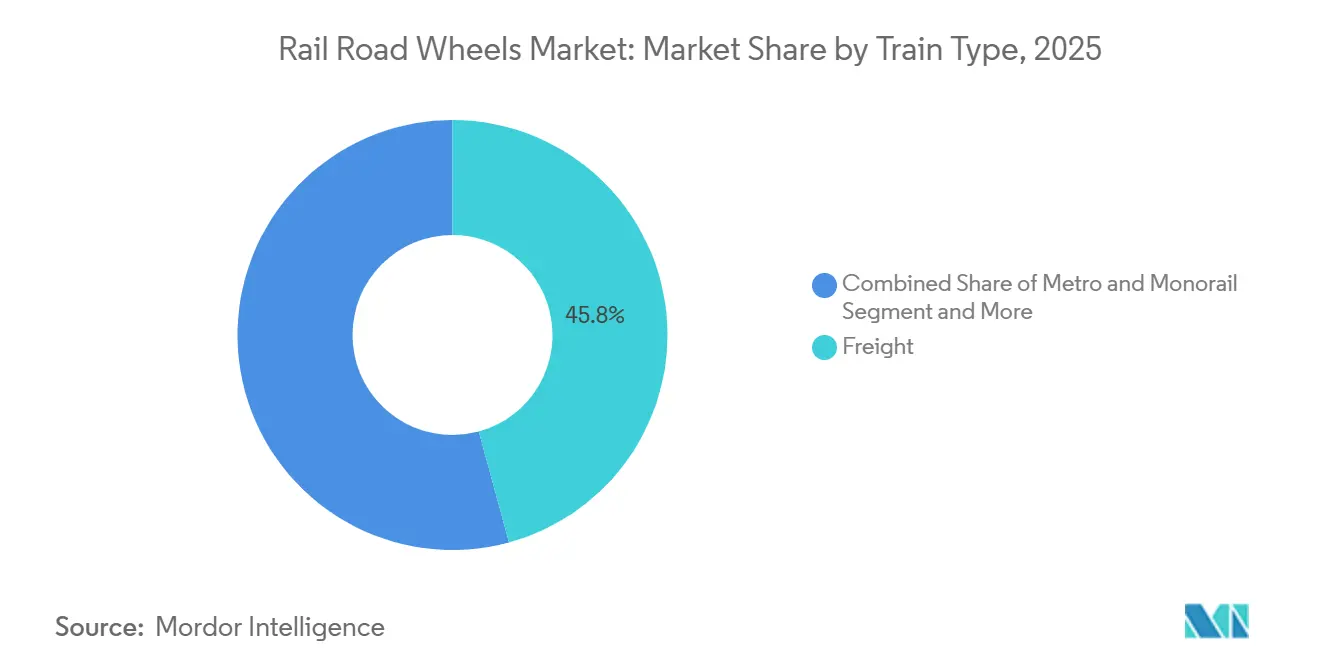

- By train type, freight operations led with 45.77% of the railway wheel market share in 2025; metro and monorail applications are projected to advance at a 5.12% CAGR through 2031.

- By wheel material, rolled carbon-steel wheels held 58.35% of the railway wheel market share in 2025; composite and hybrid designs are anticipated to grow at a 4.92% CAGR through 2031.

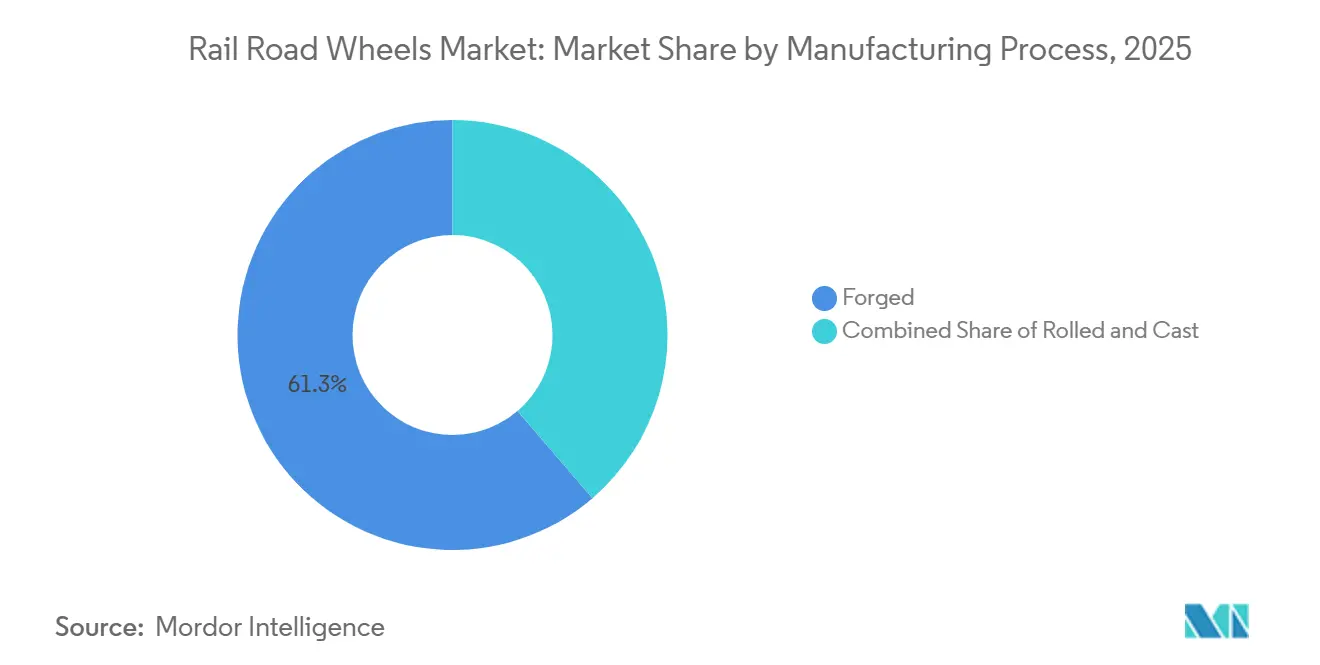

- By manufacturing process, forged wheels commanded 61.28% of the railway wheel market share in 2025; they also represent the fastest-growing segment, with a 4.86% CAGR over 2026-2031.

- By sales channel, OEM deliveries captured 59.19% of the railway wheel market share in 2025; aftermarket services are forecast to register a 4.88% CAGR through 2031.

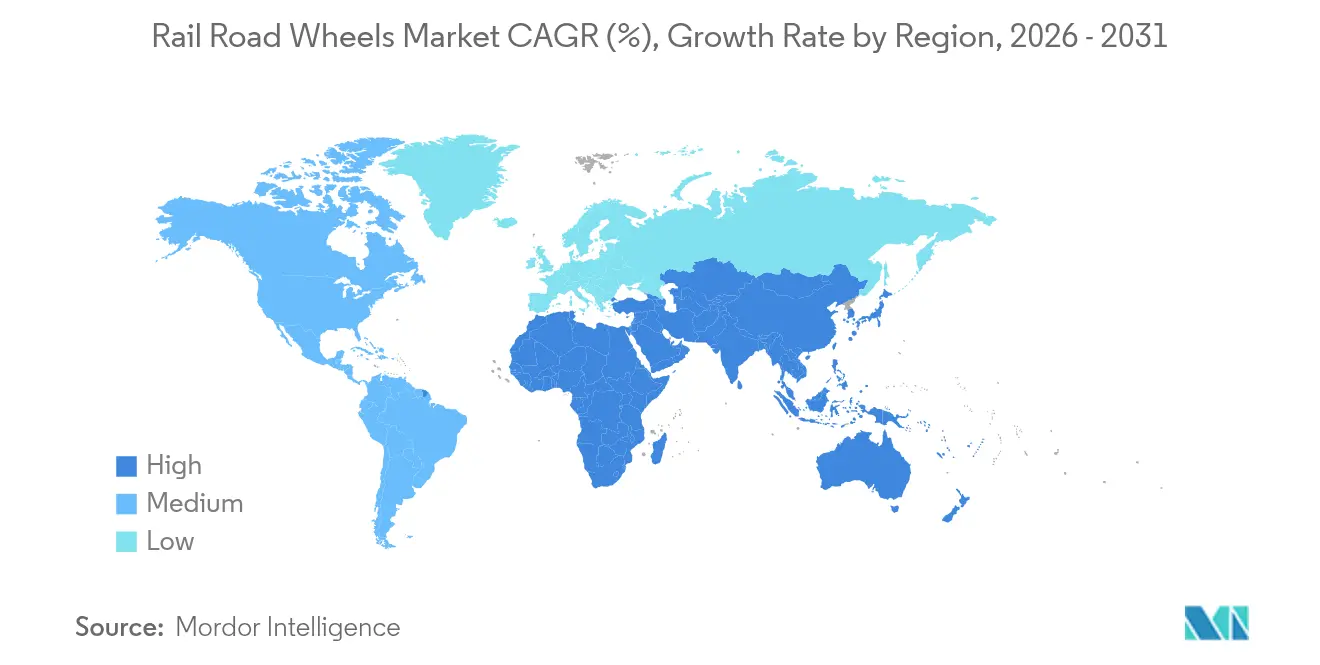

- By region, Asia-Pacific accounted for 36.84% of the railway wheel market share in 2025; the Middle East and Africa region is set to post the quickest 4.91% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rail Road Wheels Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand For High-Speed Rail Wheels | +1.2% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Dedicated Freight-Corridor Build-Outs | +0.9% | Asia-Pacific core, spill-over to Europe and Middle East | Long term (≥ 4 years) |

| Wheel-As-A-Service Leasing and Pay-Per-Kilometre Models | +0.7% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Government Incentives | +0.6% | Asia-Pacific and North America, selective EU markets | Long term (≥ 4 years) |

| OEM Integration Of Real-Time Wheel-Health Sensors | +0.5% | Global, led by developed markets | Short term (≤ 2 years) |

| Shift To Verified Low-Carbon | +0.4% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Surging Demand For High-Speed & Very-High-Speed Rail Wheels

Very-high-speed corridors, which operate at speeds exceeding 250 km/h, require forged alloy wheels with high tensile strengths. A select group of suppliers predominantly meets this demand. China recently expanded its network by adding new route-kilometres of track capable of supporting higher speeds. This expansion is projected to generate significant demand for new wheels for the CR400 train sets. Japan's N700S trains, outfitted with strain gauges, reported a notable decrease in unplanned wheel-related downtime, according to JR Central's findings[1]“N700S Series Operational Report 2025,”, Central Japan Railway, jr-central.co.jp . Europe's Lyon-Turin and Fehmarn Belt links require EN 13262-compliant wheels to ensure cross-border interoperability. Concurrently, Saudi Arabia is exploring a service exceeding 350 km/h between Riyadh and Jeddah, a development likely to elevate alloy-steel consumption. These strategic moves not only secure a consistent demand for premium forged wheels but also hasten the adoption of in-wheel sensors, bolstering fleetwide predictive maintenance.

Dedicated Freight-Corridor Build-Outs In Asia & Europe

Dedicated corridors in India separate heavy-haul wagons from passenger traffic, allowing for heavy axle loads and high operating speeds. While these speeds accelerate wear, they also enhance logistics economics. India's Western Dedicated Freight Corridor (DFC), spanning a significant distance, utilizes Class D wheels designed for an extended lifespan. This design choice suggests a substantial need for wheel replacements within the corridor's initial years of operation. The China-Europe express routes handle numerous trips annually. Each trip necessitates regular inspections and wheel replacements after extensive usage, all while contending with harsh continental climates. Europe's TEN-T initiative is upgrading to longer trains. These upgrades not only raise specifications for rolling-contact fatigue resistance but also encourage operators to adopt forged micro-alloyed wheels. These advanced wheels come equipped with acoustic crack-detection sensors, extending the intervals between manual checks.

Wheel-As-A-Service Leasing & Pay-Per-Kilometre Models

Operators transfer wheel ownership to service firms through leasing contracts. These firms focus on extending the wheel's lifespan rather than maximizing sales volume. Wabtec's program prices wheels based on distance traveled, integrates sensor analytics, and mitigates significant derailment liabilities for each failure. Deutsche Bahn's pilot program reduced wheel operational expenses by optimizing turning schedules. Metro networks, such as Riyadh, have adopted long-term availability-based contracts. New capacities are being nudged onshore due to protectionist and sustainability measures. Ramkrishna Forgings commissioned a new plant, benefiting from India's Production-Linked Incentive, which offers rebates on incremental domestic sales. Amsted Rail expanded its operations in Georgia, spurred by the U.S. Infrastructure Investment and Jobs Act, which mandates a significant percentage of domestic content for federal funding. GHH-Valdunes, capitalizing on the EU's Critical Raw Materials Act that provides low-interest loans, inaugurated a press in France, boosting the region's forged-wheel capacity. The company enforces penalties for unexpected downtimes and promotes the adoption of composite wheels. Although composite wheels have a higher initial cost, they offer a significantly longer lifespan.

Government Incentives for Domestic Forging and Heat-Treat Capacity

New capacities are being nudged onshore due to protectionist and sustainability measures. Ramkrishna Forgings commissioned a new plant, benefiting from India's Production-Linked Incentive, which offers rebates on incremental domestic sales. Amsted Rail expanded its operations in Georgia, spurred by the U.S. Infrastructure Investment and Jobs Act, which mandates a significant percentage of domestic content for federal funding. GHH-Valdunes, capitalizing on the EU's Critical Raw Materials Act that provides low-interest loans, inaugurated a press in France, boosting the region's forged-wheel capacity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Metallurgical Coke and Alloy Scrap Price Volatility | -0.8% | Global, with acute impact in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Anti-Dumping Duties | -0.6% | North America and EU, affecting Asian suppliers | Medium term (2-4 years) |

| Fragile Global Supply Chain | -0.5% | Global, with critical bottlenecks in Asia-Pacific | Medium term (2-4 years) |

| Certification Lags | -0.3% | Global, with regulatory complexity in North America and EU | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Metallurgical Coke and Alloy Scrap Price Volatility

Coke prices increased significantly as China and Australia restricted exports, putting pressure on wheel-forger margins tied to long-term supply contracts [2]"Canada Imposes Duties on Chinese Products", Government of Canada, canada.ca. Bharat Forge experienced a notable impact on EBITDA as a result. Additionally, nickel-chromium scrap prices rose sharply due to growing demand for EV batteries, diverting high-grade scrap. Smaller forgers were forced to pay substantial premiums compared to carbon-steel scrap. With scrap supply remaining unstable, capital expenditure decisions have been delayed, further tightening the short-term availability of alloy wheels.

Anti-Dumping Duties On Imported Wheels

Canada imposed definitive duties on wheels imported from China, disrupting a significant share of North American imports and increasing rail operators' procurement costs. The EU initiated an anti-subsidy investigation into products from China, with potential penalties expected in the future. Meanwhile, India extended its duties for a prolonged period. While these duties protect domestic forging industries, they also lead to inventory shortages during demand surges and complicate the standardization of fleets across borders.

Segment Analysis

By Train Type: Freight Dominance Meets Urban Growth

Freight keeps volume leadership with 45.77% of 2025 revenue and benefits from Class D/E upgrades that maintain a robust replacement cadence. Metro and monorail wheels are advancing 5.12% annually to 2031, buoyed by driverless lines in Riyadh, Dubai, Doha, and Mumbai that demand low-noise, sensor-embedded wheels. The railway wheel market for metro applications is expected to grow significantly, outpacing the overall market. Long-distance passenger fleets are increasingly demanding alloy wheels capable of handling centrifugal loads at high speeds. Concurrently, suburban networks in regions such as Japan and Europe are transitioning to lighter wheels, thereby reducing traction power. Due to their differing duty cycles, freight wheels typically need to be replaced after extensive use. In contrast, metro wheels equipped with regenerative-brake systems can extend their service life considerably, shifting consumption patterns even as overall demand increases.

Metro systems are gaining prominence, driven by urban mobility funding and public recognition of the advantages of quieter, greener mass transit. Integrated sensor packages that monitor temperature, vibration, and strain relay data to CBTC platforms. These platforms adjust speed to safeguard both wheels and tracks. While freight operators dominate the consumption of commodity-rolled wheels in budget-sensitive corridors, leading heavy-haul railroads are experimenting with health-monitored forged sets. This move aims to mitigate derailment risks and lower insurance premiums. The railway wheel market finds itself at a crossroads: balancing the consistent, high-volume demand from freight against the swift technological advancements in metro systems. This dynamic compels suppliers to curate diverse portfolios that cater to each duty profile while safeguarding their profit margins.

Note: Segment shares of all individual segments available upon report purchase

By Wheel Material: Carbon-Steel Resilience Versus Composite Innovation

Rolled carbon-steel led 2025 revenue with 58.35% share because it satisfies suburban speeds at the lowest cost. Alloy-steel wheels serve the high-speed and heavy-haul segments at price premiums of 40-50% while delivering 15% longer life, justifying their cost when safety margins are thin. Composite and hybrid products are advancing 4.92%, with the railway wheel market share for composites poised to cross 10% by 2031 after the EU approved the first EN 13979-1-compliant carbon-fiber hub in 2025.

Leasing contracts are now spreading out higher upfront costs over longer mileage allowances, making lifecycle economics more favorable. While certification costs remain steep, major suppliers are absorbing these expenses, positioning themselves as early movers. In the freight sector, carbon-steel wheels are favored for their repairability. BNSF opted for rolled sets in its intermodal fleet, resulting in lower total costs over time. Governments in the Asia-Pacific are co-funding composite trials, signaling a shift towards hybrids. These hybrids combine steel treads with polymer webs, aiming to strike a balance between affordability and weight savings.

By Manufacturing Process: Forged Excellence Drives Market Leadership

Forged wheels commanded 61.28% of the railway wheel market share in 2025 and represent the fastest-growing segment, with a 4.86% CAGR over 2026-2031, as high-speed and heavy-haul services demand superior mechanical properties. The Rail Road Wheels market size associated with forged production benefits from stringent defect tolerances and extended fatigue life that reduce derailment risk. India’s investment in a 220,000-unit-per-year forge underscores the worldwide recognition of forging’s strategic importance. Rolled wheels still serve cost-sensitive freight and locomotive markets, leveraging lower energy consumption during forming. Cast wheels, while a smaller slice, support complex geometries in low-speed mining operations.

Process advances include vacuum degassing and robotic ultrasonic inspection that ensure internal cleanliness. European forges are trialing induction-heating blanks to cut natural gas use by one-fifth, aligning with carbon goals. Hollow-forging techniques shave up to 12 kg per wheel, useful in metro applications to reduce unsprung mass. Adopters cite longer maintenance intervals with rolled wheels, resulting in lower lifecycle costs despite a higher acquisition price. Consequently, forging remains the go-to option for safety-critical fleets worldwide.

Note: Segment shares of all individual segments available upon report purchase

By End Use: OEM Leadership Meets Aftermarket Acceleration

OEM deliveries captured 59.19% of the railway wheel market share in 2025; aftermarket services are forecast to register a 4.88% CAGR through 2031. Leasing companies specify wheels with extended tread hardness to minimize mid-lease charges, influencing material mixes. Sensor-enabled wheels that feed fleet-management dashboards are popular retrofit items sold on subscription, with analytics access adding recurring income.

Repair depots use flash-butt welding to rebuild worn rims, reducing material waste compared to complete replacement. North American Class 1 railroads recently renegotiated multi-year supply deals, now guaranteeing faster turnaround times, highlighting rising service expectations. This shift in the aftermarket landscape has prompted regional stocking hubs to address shipping delays from Asia, contributing to increased local employment. While both OEM and service pathways will continue to operate simultaneously, maintenance-centric offerings are experiencing stronger revenue momentum.

Geography Analysis

Asia-Pacific dominated with 36.84% of the railroad wheels market share in 2025, anchored by China’s 155,000-kilometer network and India’s locomotive upgrade program. CRRC’s global leadership in wheel supply is reinforced by its 2023 ESG pledge to hit carbon neutrality by 2035, aligning environmental goals with export competitiveness. India’s forged-wheel plant aims for self-reliance, reduced import exposure, and export potential for ASEAN neighbors. Japan continues to innovate premium steel grades, while South Korea’s Korail integrates indigenous monitoring systems that provide real-time wear data to control centers. Together, these initiatives underpin sustained regional demand.

The Middle East & Africa is the fastest-growing region, with a 4.91% CAGR. Saudi Arabia’s USD 45 billion rail blueprint, featuring the 1,300-kilometer landbridge, requires wheels rated for 230 km/h desert operation and abrasion-resistant alloys that handle sand ingress. Egypt’s modernization to handle 2 million daily passengers by 2030 relies on imported GE locomotives and locally assembled passenger cars, resulting in high aftermarket demand for forged wheels. With 85% of Africa’s track, South Africa is opening freight slots to private operators, prompting fresh procurement of wheels optimized for manganese ore weight profiles. The region’s growth creates an attractive export outlet for Asian and European forging groups.

Europe maintains a mature but steadily expanding footprint. Alstom’s outlay to enlarge French capacity and digitize wheel assembly lines demonstrates ongoing investment. The proposed Trans-Europe high-speed grid will specify low-noise mats and composite dampers. Valdunes’ rescue by Europlasma, backed by French state support, secures domestic wheel sovereignty, while Italy forges ramp supplies for the Turin-Lyon base tunnel. Block-train volume between China and Europe is driving demand for freight wheels certified to EN 13262, helping sustain volume stability amid passenger-fleet renewal cycles.

Competitive Landscape

The railroad wheels market is moderately consolidated. Amsted Rail leverages vertical integration from steel melt shops to service centers, capturing global OEM and aftermarket orders. ArcelorMittal combines captive raw-material mining with advanced metallurgical R&D, enabling differentiated bainitic grade offerings. CRRC’s scale advantage allows aggressive pricing on complete wheel sets bundled with axles and bearings, crowding smaller players in emerging markets. Meanwhile, private equity-backed Stellex Capital acquired McConway & Torley and Standard Forged Products, signifying financial interest in niche forging assets.

Technology is the new battleground. L.B. Foster’s Mk-IV Wheel Impact Load Detector pairs ultrasonic hubs with cloud analytics, winning contracts on Union Pacific lines. Siemens Mobility integrates 5G edge nodes that stream wheel data into Railigent dashboards, enabling fleet-wide analytics. Composite wheel start-ups face certification hurdles yet entice operators with potential double-digit weight savings.

Trade-policy uncertainty prompts localized investment: Mexican forges expand to serve a duty-shielded U.S. market, while Indian public-private ventures chase metro wheel tenders. Overall, competitive advantage rests on a mix of manufacturing excellence, digital capability and geopolitical agility.

Rail Road Wheels Industry Leaders

-

Alstom SA

-

Amsted Rail

-

Bharat Forge Limited

-

ArcelorMittal SA

-

Comsteel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Indian Railways partnered with Ramakrishna Forgings and Titagarh Rail Systems to build a Tamil Nadu forged-wheel plant, targeting 80,000 units per year from 2026.

- February 2025: Alstom signed a framework with Deutsche Bahn for 1,890 digital interlocking units to be delivered through 2032.

Global Rail Road Wheels Market Report Scope

The Rail Road Wheels Market is segmented by Train Type (Metro and Monorails, Suburban Trains, Long-Distance Trains, and Freight Trains) and Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers market size and forecasts of the railroad wheels market in USD billion for all the above segments.

| Metro & Monorail |

| Suburban |

| Long-Distance Passenger |

| Freight |

| Rolled Carbon-Steel |

| Alloy-Steel |

| Composite / Hybrid |

| Rolled |

| Forged |

| Cast |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Train Type | Metro & Monorail | |

| Suburban | ||

| Long-Distance Passenger | ||

| Freight | ||

| By Wheel Material | Rolled Carbon-Steel | |

| Alloy-Steel | ||

| Composite / Hybrid | ||

| By Manufacturing Process | Rolled | |

| Forged | ||

| Cast | ||

| By End-Use | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the railway wheel market by 2031?

It is forecast to reach USD 6.08 billion, rising from USD 4.85 billion in 2026 at a 4.62% CAGR.

Which segment is growing fastest within the railway wheel market?

Metro and monorail wheels lead with an annual growth rate of 5.12% through 2031 due to driverless urban rail expansion.

How are pay-per-kilometre models impacting wheel procurement?

They shift ownership to service providers who optimize wheel life with predictive analytics, enlarging the aftermarket’s revenue share.

What region holds the largest revenue share today?

Asia-Pacific commands 36.84% of current sales, supported by Chinese suburban growth and Indian freight corridors.

Which region shows the fastest wheel demand growth through 2031?

The Middle East & Africa is set to expand at a 4.91% CAGR through 2031, fueled by large-scale corridor investments.

Page last updated on: