Automotive Parts Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 116.67 Billion |

| Market Size (2031) | USD 146.23 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

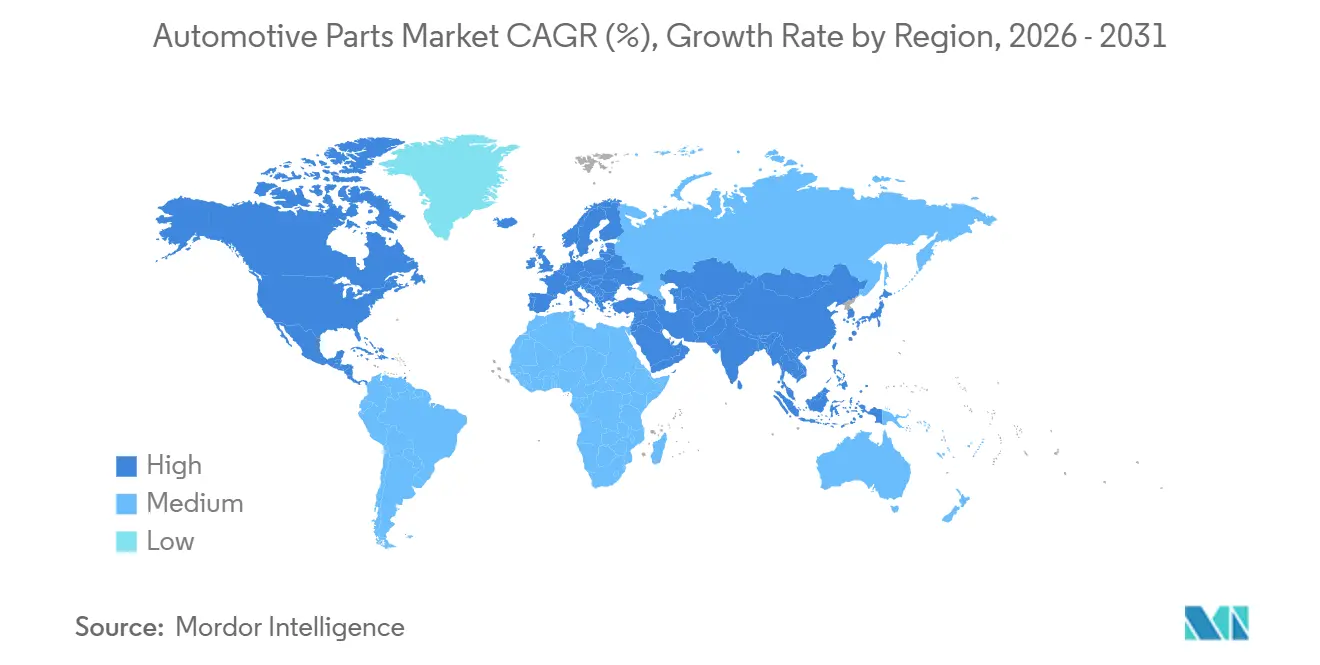

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Automotive Parts Market Analysis by ���ϲ�����

The automotive parts market size was valued at USD 111.53 billion in 2025 and estimated to grow from USD 116.67 billion in 2026 to reach USD 146.23 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031). Higher vehicle production volumes, steady aftermarket demand from an aging global fleet, and accelerating electrification together sustain this moderate growth path. Electrified powertrains shift revenue pools toward high-value electrical and electronic content, even as they reduce demand for some internal-combustion components. Digital commerce is redrawing global distribution routes for spare parts, bringing thousands of smaller suppliers into the formal supply chain. Asia-Pacific holds structural cost advantages, extensive manufacturing scale, and deep local demand, allowing the region to capture disproportionate gains in new-model sourcing. Meanwhile, semiconductor constraints, volatile raw-material input costs, and stricter data-access rules remain primary headwinds that can distort quarterly output and profitability.

Key Report Takeaways

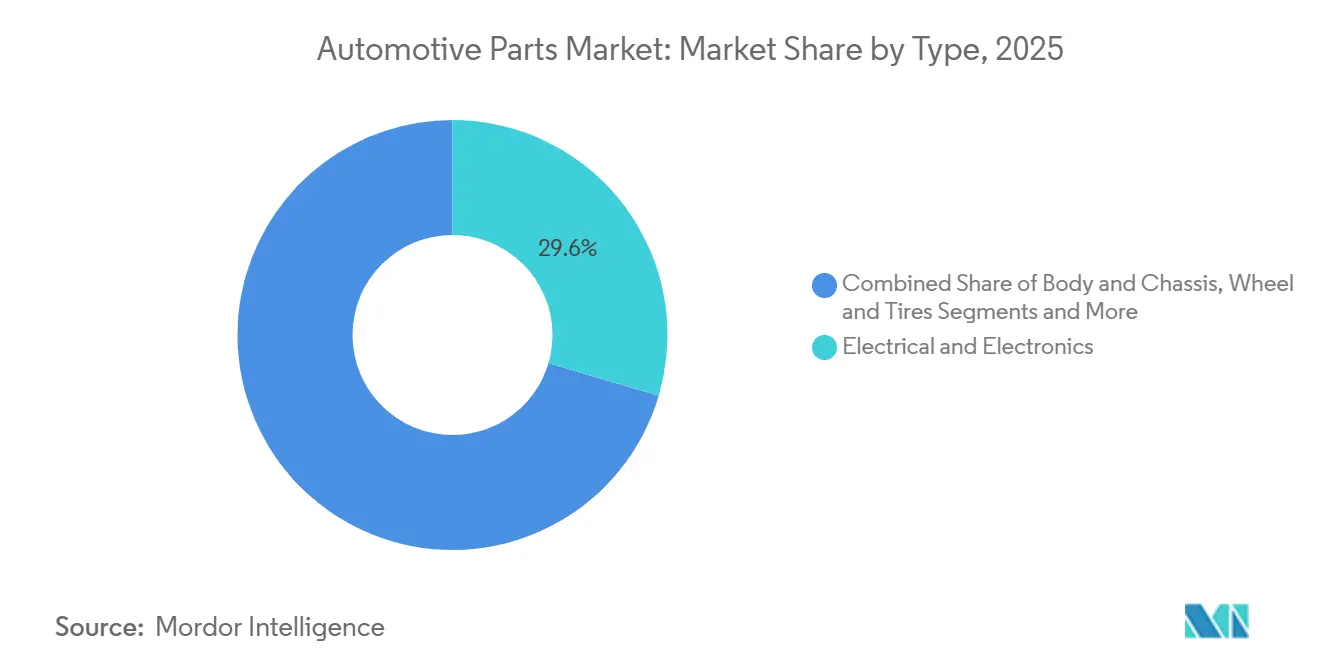

- By component type, electrical and electronics captured 29.56% of the automotive parts market share in 2025, and the segment is projected to post a 9.12% CAGR through 2031.

- By propulsion, internal-combustion vehicles held 75.88% of the automotive parts market size in 2025, while battery-electric vehicles are expected to compound at a 34.1% CAGR to 2031.

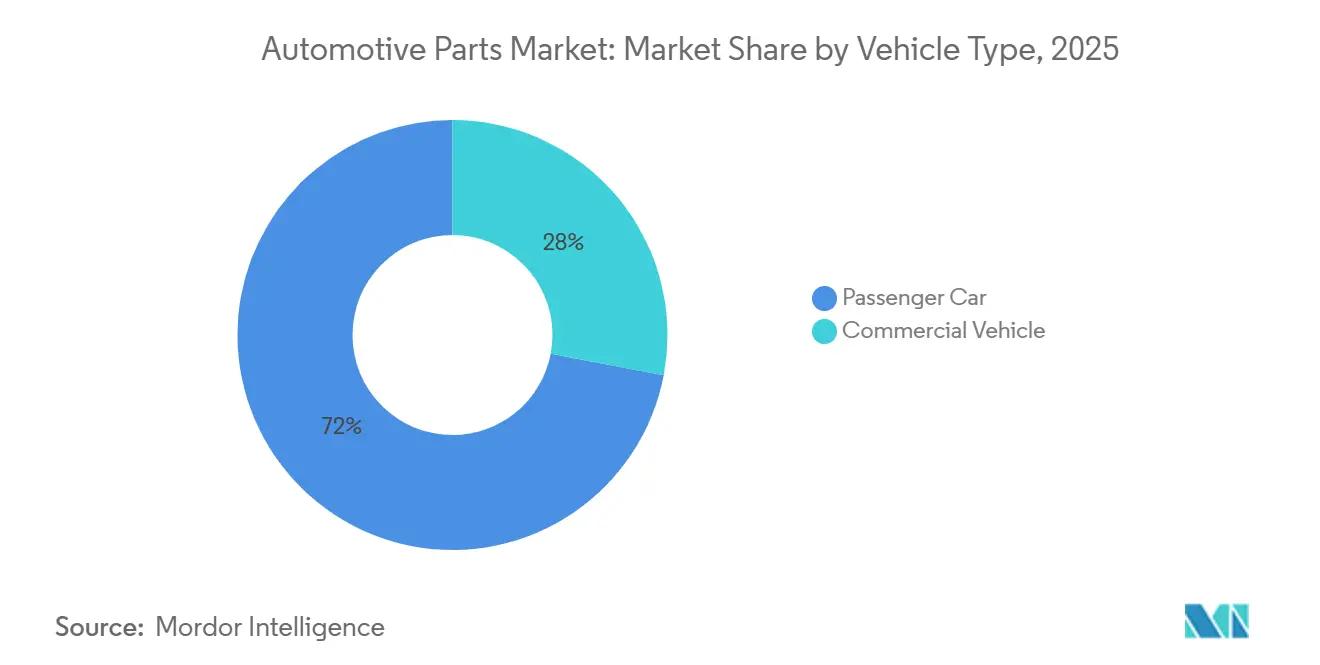

- By vehicle type, passenger cars accounted for 72.01% of the automotive parts market in 2025; the segment is expanding at a 4.82% CAGR through 2031.

- By sales channel, OEM supply chains accounted for 60.74% of the automotive parts market in 2025, whereas aftermarket e-commerce posted the fastest CAGR of 13.20% through 2031.

- By geography, Asia-Pacific led the automotive parts market with 45.31% of the market size in 2025 and is forecast to grow at a 6.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Parts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Global Vehicle Production | +1.2% | Global, with Asia-Pacific Leading Growth | Medium term (2-4 years) |

| Aging Vehicle Fleet Boosting Aftermarket Spend | +0.8% | North America and Europe Primarily | Long term (≥ 4 years) |

| Rapid Growth of E-Commerce Parts Platforms | +0.6% | Global, Accelerated in Developed Markets | Short term (≤ 2 years) |

| Light-Weighting Push for Advanced Material Components | +0.4% | Europe and North America Regulatory Drive | Long term (≥ 4 years) |

| Software-Defined Vehicles Requiring Upgradeable Hardware | +0.9% | Global, Led by Premium Segments | Medium term (2-4 years) |

| "Right-to-Repair" Legislation Widening Independent Service Share | +0.5% | US Federal, EU Regional Implementation | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rise in Global Vehicle Production

Global automotive production reached 90.5 million units in 2023, returning to pre-COVID levels, though production is expected to moderate to 88.5 million units in 2024 before recovering[1]"Automotive market faces slower growth and capacity challenges amid electrification shift", Daniel Harrison, Automotive Logistics, automotivelogistics. media. This production expansion directly correlates with increased demand for both original equipment and aftermarket parts, particularly in emerging markets where vehicle ownership rates continue to climb. China's transformation into a net vehicle exporter, primarily of low-cost internal combustion engine and electric vehicles, reshapes global supply chains and creates new demand patterns for component suppliers. The shift toward "multi-energy" production lines allows manufacturers to adapt quickly to market uncertainties while maintaining consistent parts demand across different powertrain technologies.

Software-Defined Vehicles Requiring Upgradeable Hardware

The automotive software market is expected to expand steadily over the coming years, as industry leaders anticipate a transition toward software-defined and AI-enabled vehicles by 2035. This evolution requires a shift in vehicle architecture, with hardware systems designed to support over-the-air updates, cybersecurity integration, and continuous feature enhancements across the vehicle lifecycle. Unlike conventional automotive components with fixed, static functionality, next-generation vehicles require modular, upgradeable hardware platforms that can accommodate evolving software capabilities. This architectural shift increases demand for high-performance computing units, domain controllers, advanced sensor suites, and reprogrammable electronic control units.

Rapid Growth of E-commerce Parts Platforms

The U.S. auto parts market is projected to grow to USD 41 billion from 2025 to 2029, driven by digitization, AI adoption, and e-commerce expansion. Online sales platforms are surpassing physical stores, with brakes, filters, batteries, tires, and lubricants emerging as top-selling categories[2]"U.S. auto parts market to grow driven by AI, ecommerce" Aftermarket International, aftermarketinternational.com. AI integration enhances supply chain efficiency and inventory management, while automated systems improve the customer experience through better product recommendations and faster order processing. The e-commerce transformation is particularly pronounced in the aftermarket channel, where digital platforms enable smaller suppliers to reach broader customer bases without extensive physical distribution networks, fundamentally altering traditional parts distribution models.

"Right-to-Repair" Legislation Widening Independent Service Share

The bipartisan Right to Equitable and Professional Auto Industry Repair Act, known as the REPAIR Act, was reintroduced in the United States Congress in 2025 to strengthen consumer and independent repair facility access to vehicle diagnostic data, telematics information, and software tools. The legislation builds on broader right-to-repair initiatives at both the federal and state levels, seeking to prevent original equipment manufacturers from restricting access to repair critical information increasingly embedded in software-driven vehicle systems. The legislation could significantly expand the addressable market for aftermarket parts suppliers by breaking down data access barriers that have historically favored dealership networks. With independent shops performing 80% of out-of-warranty repairs at lower costs than dealerships, successful right-to-repair implementation could accelerate aftermarket growth and increase competition in the parts distribution ecosystem.

Restraints Impact Analysis*

| Restraint | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Semiconductor Shortages | -1.1% | Global, Acute in Automotive Applications | Short term (≤ 2 years) |

| EV Shift Eroding Demand for ICE-Specific Parts | -0.7% | Europe and China Leading, US Following | Long term (≥ 4 years) |

| Volatile Raw Material Prices Disrupting Cost Structures | -0.6% | Global, with Pronounced Impact in Emerging Markets | Medium term (2-4 years) |

| Labor Shortages in Key Manufacturing Hubs | -0.5% | North America, Europe, and Parts of Asia-Pacific | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Persistent Semiconductor Shortages

The automotive semiconductor market faces continued supply constraints despite recovery efforts, with the industry experiencing production reductions of up to 40% during peak shortage periods. The automotive sector's transition to software-defined vehicles is increasing semiconductor content per vehicle from USD 800 in 2023 to an expected USD 1,350 by 2030. Supply chain vulnerabilities persist due to concentrated production in specific geographic regions and the long lead times required for automotive-grade components. The shortage particularly impacts advanced driver assistance systems and infotainment components, forcing OEMs to prioritize chip allocation and sometimes remove features from vehicles to maintain production schedules.

EV Shift Eroding Demand for ICE-Specific Parts

Electric vehicles require significantly fewer moving parts than internal combustion engines, with some estimates suggesting maintenance requirements are 40% lower than those of traditional vehicles. This transition poses particular challenges for suppliers of ICE-specific components such as exhaust systems, fuel injection parts, and traditional transmission components. However, the shift creates opportunities in new component categories, including battery management systems, electric powertrains, and thermal management solutions. The transition timeline varies significantly by region, with Europe and China leading adoption. At the same time, North America follows at a more measured pace, creating a complex global landscape where suppliers must balance declining ICE demand with emerging EV opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electronics Integration Drives Market Evolution

Electrical and electronics components hold 29.56% of the automotive parts market share in 2025 and achieved the fastest growth rate of 9.12% CAGR through 2031. This dual leadership reflects the automotive industry's fundamental shift toward connected, autonomous, and electrified vehicles that require sophisticated electronic systems. The segment encompasses critical systems including advanced driver assistance systems (ADAS), infotainment platforms, battery management systems, and vehicle-to-everything communication modules.

Driveline and powertrain components face a complex transition as traditional internal combustion engine parts experience declining demand while electric powertrain components surge. Interior and exterior segments benefit from premiumization trends and increased focus on user experience, particularly in software-defined vehicles where cabin technology becomes a key differentiator. Body and chassis components are evolving to accommodate new materials and lightweighting requirements. At the same time, wheel and tire segments remain relatively stable, with growth driven by replacement demand from aging vehicle fleets and expanding global vehicle populations.

By Propulsion: Electrification Reshapes Component Demand

Internal combustion engine vehicles accounted for 75.88% of the automotive parts market share in 2025, reflecting the installed base of existing vehicles and continued production in many global markets. However, battery-electric vehicles represent the fastest-growing segment, with an extraordinary 34.10% CAGR through 2031, driven by regulatory mandates, advances in battery technology, and expanding charging infrastructure.

Hybrid and plug-in hybrid electric vehicles serve as transitional technologies, requiring components for electric and combustion powertrains, creating complexity for suppliers and diversifying demand patterns. Fuel-cell electric vehicles remain a niche segment but show promise in commercial vehicle applications where hydrogen's energy density advantages become more pronounced. The propulsion mix varies significantly by region, with China and Europe leading the way in electrification. At the same time, North America and emerging markets maintain higher ICE shares, requiring suppliers to maintain flexible production capabilities across multiple powertrain technologies.

By Vehicle Type: Commercial Vehicles Drive Innovation Adoption

Passenger cars dominate the automotive parts market with 72.01% market share in 2025 and maintain the fastest growth rate at a 4.82% CAGR through 2031, benefiting from higher production volumes and more frequent replacement cycles. The segment drives innovation in consumer-facing technologies, including infotainment systems, connectivity features, and autonomous driving capabilities. Premium passenger vehicles often serve as testbeds for new technologies before broader market adoption, creating early demand for advanced components.

While commercial vehicles account for a smaller market share, they are experiencing strong growth driven by e-commerce expansion, urbanization, and fleet electrification initiatives. Commercial applications often justify higher component costs due to total cost of ownership considerations, making them attractive early adopters of advanced technologies such as telematics systems, predictive maintenance solutions, and alternative powertrains. The segment also benefits from longer vehicle lifecycles, which sustain aftermarket demand for replacement parts and upgrades.

By Sales Channel: Aftermarket E-commerce Transforms Distribution

Original Equipment Manufacturer channels maintain 60.74% of the automotive parts market share in 2025, reflecting the substantial value of components supplied directly to vehicle manufacturers during production. However, the aftermarket e-commerce segment is the fastest-growing, with a 13.20% CAGR, fundamentally disrupting traditional parts distribution models. Digital platforms enable direct-to-consumer sales, bypassing traditional distributor networks, reducing costs, and improving convenience.

The traditional aftermarket channel faces pressure from e-commerce growth and potential right-to-repair legislation that could increase competition by improving independent shop access to OEM data and parts. However, physical aftermarket channels retain advantages in complex installations, technical support, and immediate availability for urgent repairs. The channel mix is evolving toward an omnichannel approach, with digital platforms complementing physical distribution networks, particularly for routine maintenance items and standardized components.

Geography Analysis

Asia-Pacific maintains its dominant position, accounting for 45.31% of the automotive parts market share in 2025. It leads regional growth at a 6.19% CAGR through 2031, driven by China's automotive manufacturing supremacy and expanding domestic markets. China, as both a producer and exporter, fuels significant demand for automotive parts, serving both its domestic market and export-bound vehicles. As vehicle ownership rises and demand for aftermarket services grows, India's automotive aftermarket is experiencing notable expansion. Japan continues to leverage its technological expertise in advanced components, particularly in hybrid powertrains and precision manufacturing. At the same time, South Korea focuses on electric vehicle technologies and semiconductor solutions for automotive applications.

North America and Europe represent mature markets with established automotive ecosystems but face distinct challenges in adapting to industry transformation. The region's independent aftermarket is driven by aging vehicles and budget-conscious consumers, but growth is expected to slow post-2026 due to EV adoption. North America benefits from nearshoring trends and the Inflation Reduction Act's support for domestic EV production, though the market faces potential disruption from trade policies and Chinese automotive competition.

Emerging markets in South America, the Middle East, and Africa exhibit notable growth potential despite their currently smaller market shares. In Mexico, the auto parts sector is propelled by the expanding electric vehicle production in the United States and increasing demand for electric components. Similarly, the Middle East and North Africa are leveraging government initiatives to enhance local automotive capabilities and reduce reliance on imports, creating opportunities for both domestic and international parts suppliers.

Competitive Landscape

Several key players dominate the automotive parts market, where technological disruptions and shifting customer demands fuel intense competition. Traditional tier-one suppliers, including Robert Bosch, Continental, and Denso, uphold their leadership through significant R&D investments and strategic shifts towards electrification and enhanced software capabilities. As the industry pivots towards software-defined vehicles, competitive dynamics are evolving, compelling suppliers to bolster both hardware and software capabilities to remain relevant.

Strategic patterns reveal a fundamental shift from project-oriented to product-oriented business models, as suppliers seek scalable solutions that can generate recurring revenue streams across multiple OEM customers. White-space opportunities exist where traditional automotive suppliers intersect with technology companies, particularly in autonomous driving systems, vehicle-to-everything communication, and predictive maintenance solutions.

Emerging disruptors include technology companies entering automotive markets and Chinese suppliers expanding globally with cost-competitive offerings. The competitive landscape is further complicated by the need to simultaneously serve both traditional ICE vehicles and emerging electric platforms, requiring suppliers to maintain dual capabilities while managing the transition timeline. Companies increasingly leverage artificial intelligence and automation to enhance manufacturing efficiency and product quality, with successful implementation becoming a key competitive differentiator in cost-sensitive markets.

Automotive Parts Industry Leaders

-

Robert Bosch GmbH

-

Continental AG

-

ZF Friedrichshafen AG

-

Denso Corporation

-

Hyundai Mobis Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: American Axle & Manufacturing completed its acquisition of GKN Powder Metallurgy and GKN Automotive for USD 1.44 billion, significantly expanding its capabilities in advanced manufacturing technologies and global market presence.

- November 2024: Standard Motor Products completed the acquisition of European aftermarket supplier Nissens Automotive for approximately USD 390 million, enhancing its position in North American and European markets while leveraging Nissens' expertise in vehicle control technologies.

Global Automotive Parts Market Report Scope

Automotive parts are installed in a vehicle to provide the best driving experience. The parts include bodies, chassis, interiors, exteriors, seating, powertrains, electronics, mirrors, closures, roof systems, and modules.

The Automotive Parts Market is segmented into type (powertrain, interior and exterior, electrical and electronics, body and chassis, wheel and tires, and other types), propulsion (internal combustion engine, battery electric vehicles, hybrid electric vehicles, plug-in hybrid electric vehicles, and fuel cell electric vehicles), vehicle type (passenger cars and commercial vehicles), sales channel (original equipment manufacturers and aftermarket), and geography (North America (United States, Canada, and Rest of North America), Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, India, Japan, South Korea, and Rest of Asia-Pacific), and Rest of the World (South America and Middle East and Africa)). The report offers value terms in USD for the above-mentioned segments.

| Driveline and Powertrain |

| Interior and Exterior |

| Electrical and Electronics |

| Body and Chassis |

| Wheel and Tires |

| Other Types |

| Internal Combustion Engine |

| Battery-Electric Vehicle |

| Hybrid Electric Vehicle |

| Plug-in Hybrid Electric Vehicle |

| Fuel-Cell Electric Vehicle |

| Passenger Car |

| Commercial Vehicle |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Driveline and Powertrain | |

| Interior and Exterior | ||

| Electrical and Electronics | ||

| Body and Chassis | ||

| Wheel and Tires | ||

| Other Types | ||

| By Propulsion | Internal Combustion Engine | |

| Battery-Electric Vehicle | ||

| Hybrid Electric Vehicle | ||

| Plug-in Hybrid Electric Vehicle | ||

| Fuel-Cell Electric Vehicle | ||

| By Vehicle Type | Passenger Car | |

| Commercial Vehicle | ||

| By Sales Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Automotive Parts Market?

The Automotive Parts Market size is valued at USD 116.67 billion in 2026 and grow at a CAGR of 4.61% to reach USD 146.23 billion by 2031.

Who are the key players in Automotive Parts Market?

Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Denso Corporation and Hyundai Mobis Co., Ltd. are the major companies operating in the Automotive Parts Market.

Which is the fastest growing region in Automotive Parts Market?

Asia Pacific is projected to lead with the highest CAGR of 6.19% from 2026 to 2031.

Which region has the biggest share in Automotive Parts Market?

In 2025, the Asia Pacific accounts for the largest market share in Automotive Parts Market.

Page last updated on: