United Arab Emirates Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

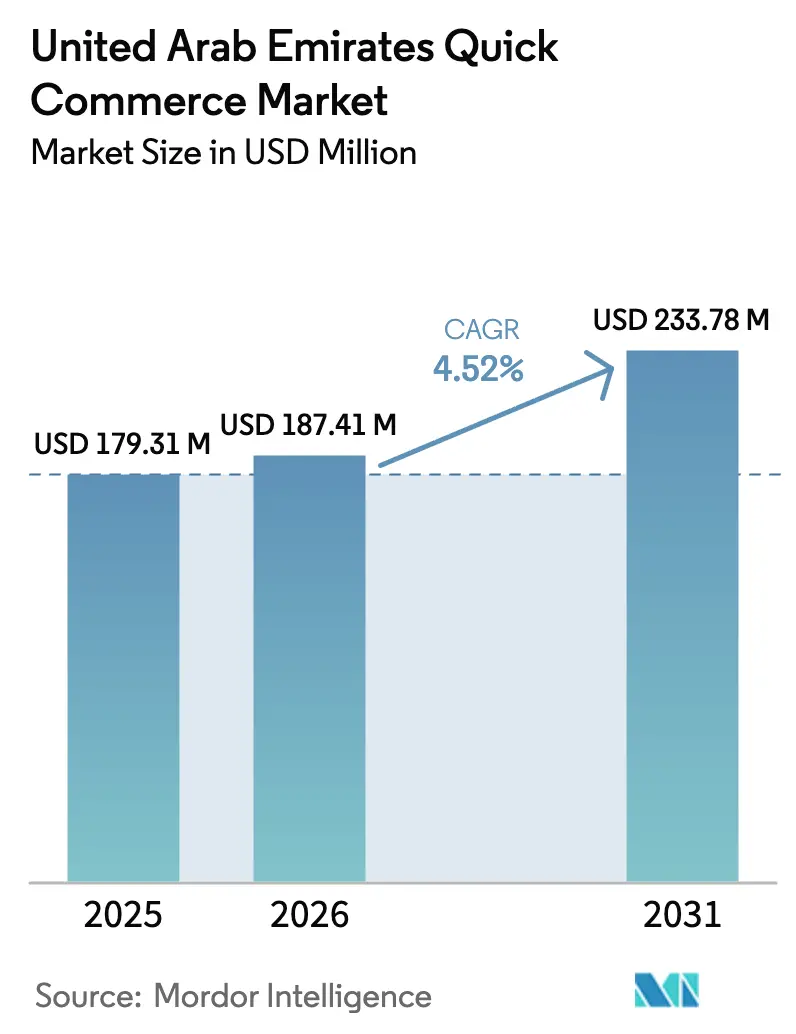

| Base Year Market Size (2025) | USD 179.31 Million |

| Market Size (2026) | USD 187.41 Million |

| Market Size (2031) | USD 233.78 Million |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

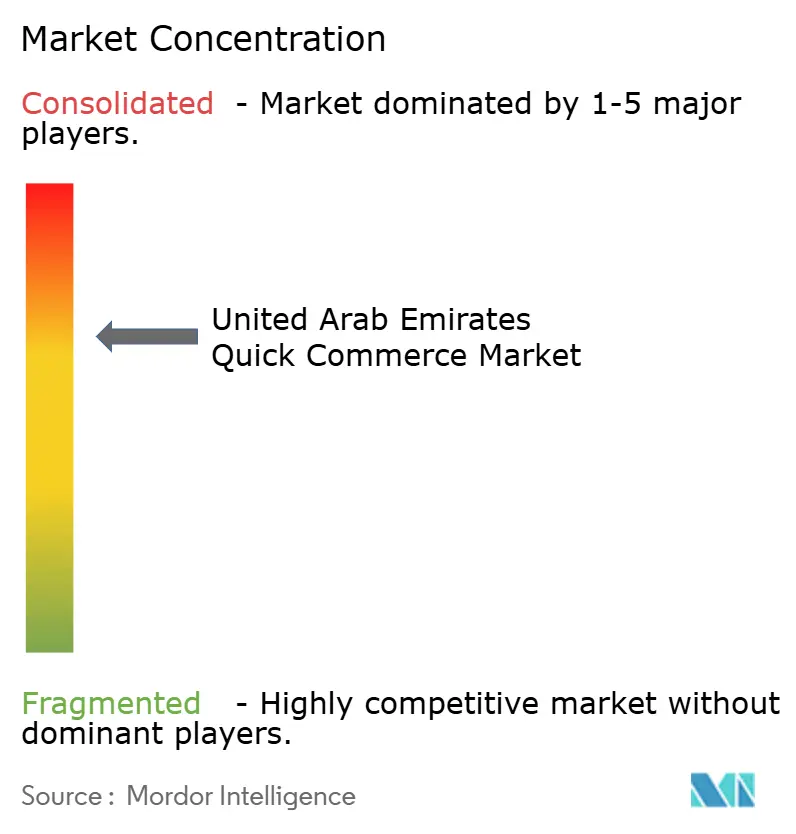

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Quick Commerce Market Analysis by ���ϲ�����

The United Arab Emirates quick commerce market size was valued at USD 179.31 million in 2025 and is estimated to grow from USD 187.41 million in 2026 to reach USD 233.78 million by 2031, at a CAGR of 4.52% during the forecast period (2026-2031). The measured expansion reflects a maturing ecosystem in which sovereign capital, micro-fulfillment infrastructure, and artificial-intelligence logistics converge to reset last-mile delivery economics. Platform operators are prioritizing density thresholds of 150-200 daily orders per dark store, while subscription models such as Deliveroo Plus and Talabat Pro improve customer lifetime value and dampen discount fatigue. Intensifying competition centers on ultra-fast 15-minute and sub-10-minute windows that push real-estate and labor costs higher, yet high smartphone penetration and digital-wallet adoption sustain repeat-purchase frequency. Regulatory guardrails, specifically Federal Decree-Law No. 33 of 2021, elevate labor expenses but also create a compliance moat that favors well-capitalized players.

Key Report Takeaways

- By product category, grocery and staples led with 50.87% revenue share of United Arab Emirates quick commerce market in 2025, while fresh produce and dairy is projected to expand at a 5.49% CAGR through 2031.

- By delivery time promise, the 11-30 minute band accounted for 54.61% of 2025 revenue of UAE quick commerce market, whereas the less-than-10 minute segment is forecast to grow at 6.02% CAGR to 2031.

- By city tier, Tier I metros captured 61.92% of 2025 demand, and Tier II cities are poised to advance at a 5.27% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in On-Demand Lifestyle Among Emirati Millennials | +1.2% | Tier I metros, spillover to Tier II cities | Short term (≤ 2 years) |

| High Smartphone Penetration and Digital Wallet Adoption | +0.9% | National, concentrated in urban Emirates | Medium term (2-4 years) |

| Strategic Investments by Sovereign Wealth Funds | +0.7% | National, anchored in Dubai and Abu Dhabi | Long term (≥ 4 years) |

| Expansion of Micro-Fulfillment Dark Stores | +0.6% | Tier I metros expanding to Tier II cities | Medium term (2-4 years) |

| AI-Driven Route Optimization for Hyper-Local Delivery | +0.5% | National, early adoption in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Growing Appetite for Health-Focused Fresh Produce | +0.4% | Tier I metros, emerging in Tier II cities | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Surge In On-Demand Lifestyle Among Emirati Millennials

Millennials account for close to 60% of the UAE’s 10.08 million residents and prioritize convenience over price, which propels the United Arab Emirates' quick commerce market toward sub-30-minute fulfillment. Dual-income households in Dubai and Abu Dhabi earned median incomes above USD 80,000 in 2025, and they willingly pay premium fees for speed. Platforms respond by deploying predictive inventory algorithms that pre-position high-velocity SKUs within 2-3 kilometers of dense residential clusters, trimming delivery windows to 10 minutes. Noon scaled its Noon Minutes service to 12 dark stores across Dubai and Sharjah to capitalize on areas exceeding 200 transactions per square kilometer per day. Faster delivery feeds higher order frequency, reinforcing the density economics that underpin profitability.

High Smartphone Penetration And Digital Wallet Adoption

Smartphone penetration reached 96.4% in 2025, and digital-wallet usage climbed to 68% of adults, sharply lowering checkout friction. Cart abandonment rates shrank from 22% in 2023 to 14% in 2025 as one-click payment solutions took hold. Talabat and Noon processed 78% of 2025 orders through Apple Pay, Samsung Pay, or local wallets. Expatriates like Indians, Pakistanis, and Filipinos, representing 88% of the national population, show high digital literacy and accelerate repeat purchases. The UAE Central Bank’s Digital Payment Strategy targets 90% cashless transactions by 2026, ensuring continued momentum. Subscription programs flourish under this frictionless environment, boosting customer lifetime value by 30-35%.

Strategic Investments By Sovereign Wealth Funds

Abu Dhabi Investment Authority and Mubadala injected an estimated USD 1.2 billion into e-commerce and logistics assets during 2024-2025, underwriting automation, cold-chain upgrades, and fleet electrification that cut per-order emissions by up to 25%. The April 2025 ADNOC-Noon partnership converted 50 fuel stations into micro-fulfillment hubs, achieving 15-minute coverage across vast catchment areas. Mubadala’s backing of Noon’s autonomous ground-vehicle pilots in Dubai Marina and Yas Island furthers the UAE’s National Strategy for Artificial Intelligence 2031. Public-private synergy lowers financing risk for long-gestation infrastructure and accelerates the adoption of robotics and AI in last-mile operations.

Expansion Of Micro-Fulfillment Dark Stores

Operators opened roughly 80-100 micro-fulfillment centers across major Emirates through 2025, each covering 1-3 square kilometers and stocking 1,500-2,500 SKUs. Carrefour’s automated 10,000 square-meter Dubai facility processes 3,000 orders per hour, slicing labor costs by 30% and enabling same-day delivery across 90% of the city. Deliveroo established six HOP dark stores in Abu Dhabi, targeting 10-minute grocery drops.[1]Gulf News, “Dark Store Expansion in UAE,” gulfnews.com Density remains the profit linchpin, compelling creative hybrid models in Tier II cities where rents are lower but order volumes trail Tier I by up to 35%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Unit-Economics Pressure from Discounts | -0.8% | National, acute in Tier I metros | Short term (≤ 2 years) |

| Limited Late-Night Delivery Windows (Labor Rules) | -0.5% | National, governed by Federal Decree-Law No. 33 of 2021 | Medium term (2-4 years) |

| Rising Real-Estate Costs for Prime Dark Stores | -0.4% | Tier I metros (Dubai, Abu Dhabi) | Medium term (2-4 years) |

| Customer Fatigue from Push Notifications | -0.3% | National, concentrated in high-frequency cohorts | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Intensifying Unit-Economics Pressure From Discounts

Average promotional spend reached 18-22% of gross merchandise value in 2025, eroding margins and delaying breakeven.[2]Financial Times, “UAE Quick Commerce Profitability Challenges,” ft.com Talabat’s customer-acquisition costs rose 25% year on year as first-order subsidies climbed to AED 40 (USD 10.89). Noon aims to curb subsidies by 5-7 percentage points annually, risking volume attrition if rivals keep spending. With 62% of users holding three or more app accounts, churn remains high. Subscription penetration below 15% of actives is insufficient to offset promotional drag.

Limited Late-Night Delivery Windows

Federal Decree-Law No. 33 caps daily work at eight hours and restricts night shifts, raising labor costs by up to 15% for platforms seeking 24-hour coverage.[3]UAE Ministry of Human Resources and Emiratisation, “Laws and Legislation,” mohre.gov.ae Peak demand between 8 PM and 11 PM collides with mandated rest periods, curtailing service hours and ceding late-night sales to convenience stores. Annual leave and gratuity obligations add AED 8,000 (USD 2,178) - 12,000 (USD 3,268) per rider, widening the cost gap with gig-economy models used in other regions. Hybrid fleets mixing employees and freelancers remain constrained by unclear gig-worker status in Tier II corridors.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Fresh Produce Accelerates Premiumization

The fresh produce and dairy segment is forecast to outpace the United Arab Emirates quick commerce market by nearly 100 basis points, expanding at 5.49% per year through 2031. Kibsons logged 35% growth in same-day orders for organic vegetables, grass-fed dairy, and free-range eggs in 2025. Grocery and staples retained 50.87% of 2025 revenue, anchored by pantry essentials that drive subscription bundles and stabilize unit economics. Snacks and beverages, personal care and OTC pharma, and home-care supplies together form about one-third of sales, with personal care climbing 4.8% as pharmacy tie-ups enable 30-minute delivery of vitamins and cosmetics.

Premium fresh demand spurs vertical-farming partnerships that cut food miles and extend shelf life by up to 50%. Regulatory adherence to Dubai Municipality cold-chain rules adds AED 3-5 per order but strengthens consumer trust. Electronics and accessories remain smaller but strategically important, driven by Careem’s 60-minute Quik Electronics service. Pet care and flowers, each under 3% of revenue, carry high average basket values that improve margins. Spinneys’ chef-prepared meal initiative broadens category scope and taps time-scarce professionals.

By Delivery Time Promise: Sub-10-Minute Windows Gain Traction

The less-than-10-minute segment is projected to grow 6.02% annually through 2031, the fastest among all delivery bands. Deliveroo, Amazon, and Talabat spearhead ultra-fast fulfillment, forcing incumbents to compress delivery radiuses to 1 kilometer in dense corridors such as Dubai Marina. The 11-30-minute band, holding 54.61% share in 2025, balances SKU breadth with economic density by serving 2-3 square kilometers per dark store. United Arab Emirates quick commerce market size gains from this tier as operators achieve break-even at 150-180 orders daily.

Capex intensity for sub-10-minute service is high due to prime rents topping AED 120 (USD 32.68) per square meter in Tier I districts. Predictive inventory based on weather and local events mitigates stock-outs, while AI rider allocation trims average delivery times by up to five minutes. The 31-60-minute window remains relevant for bulky items, using vans rather than motorbikes. Labor-law restrictions limit overnight coverage, so many platforms cap service at 11 PM, ceding nighttime demand to convenience retailers.

By City Tier: Secondary Corridors Present Growth Upside

Tier I metros delivered 61.92% of 2025 revenue, but Tier II cities are forecast to compound at 5.27% a year, surpassing the overall United Arab Emirates quick commerce market. Rental costs in Sharjah and Ajman trail Dubai by 30-40%, yet order volumes lag by up to 35%. Noon’s deployment of three Sharjah dark stores stocking 1,800 SKUs tailored to South Asian and Filipino tastes illustrates a hybrid spoke-and-hub model.

The UAE quick commerce market share in Tier II hinges on reaching 120-150 orders per dark store per day. Expatriate communities, which constitute up to 80% of Sharjah’s population, exhibit high digital literacy, supporting rapid adoption. Enforcement of labor rules is more flexible outside Dubai and Abu Dhabi, trimming per-rider labor costs by up to 12%. Tier III emirates remain subscale, accounting for less than 5% of revenue, with next-day delivery prevailing over quick commerce due to sparse demand and long distances.

Geography Analysis

Tier I metros, Dubai and Abu Dhabi, dominate the United Arab Emirates quick commerce market, together securing 61.92% of 2025 sales. Dubai houses around 60 dark stores clustered in Marina, Business Bay, Downtown, and JLT, each posting densities of 200-250 transactions per square kilometer daily. Abu Dhabi’s ecosystem is smaller yet expanding, powered by Deliveroo HOP and ADNOC-Noon fuel-station conversions, which cut real-estate costs and unlock 15-minute coverage.

Tier II cities such as Sharjah, Ajman, and Ras Al Khaimah contribute a rising share thanks to lower rents and underserved expatriate populations in the UAE quick commerce market. Sharjah’s 1.8 million residents show 65% digital-wallet adoption, and operators employ spoke-and-hub logistics from Dubai or local dark stores to serve 5-7 square-kilometer catchments. Order densities remain 25-35% lower than Tier I, necessitating promotional spend and hybrid fleets to reach breakeven.

Tier III emirates, Fujairah and Umm Al Quwain, remain peripheral. Sparse populations of 300-500 residents per square kilometer and long delivery radiuses of up to 90 kilometers hinder ultra-fast models. Platforms rely on regional warehouses for next-day delivery. Uniform federal regulations create consistent compliance costs, which weigh heaviest on operators lacking volume scale in these regions.

Competitive Landscape

Twenty profiled operators vie for share in a moderately concentrated arena where the top five, Talabat, Noon, Careem, Amazon, and Deliveroo, control roughly 65-70% of revenue. Talabat’s USD 2 billion IPO funded aggressive M&A, including the USD 32 million InstaShop acquisition that removed overlapping dark stores and improved asset utilization. Pure-play platforms emphasize AI-driven logistics and ultra-fast delivery, while omnichannel grocers such as Carrefour, Lulu, Spinneys, and Choithrams exploit in-store footfall to cross-subsidize online orders and offer click-and-collect.

Technology capability is a decisive competitive lever. Carrefour’s robotic distribution center in Dubai processes 3,000 orders hourly, slashing per-item labor time, whereas Noon’s 30,000-square-meter KEZAD facility halves order-processing durations to six minutes. Vertical-farming alliances with Badia Farms and Pure Harvest create freshness differentiation and sustainability narratives. Low switching costs, 62% of users maintain accounts on three or more apps, pressure platforms to innovate loyalty propositions. Subscription penetration remains below 15%, so discount wars persist, straining margins for smaller entrants such as YallaMarket and El Grocer.

Market entry barriers rise as compliance costs climb. Labor regulations restrict late-night operations and impose mandatory benefits, while Dubai Municipality food-safety standards demand temperature-controlled packaging. Well-capitalized players absorb these expenses and leverage data to fine-tune inventory and routing, widening the competitive moat. Smaller operators risk acquisition or niche positioning in organic, halal, or cooperative formats.

United Arab Emirates Quick Commerce Industry Leaders

Talabat UAE Company LLC

Noon UAE Grocery Delivery LLC

Careem Networks FZ LLC

InstaShop Ltd

Deliveroo Dubai LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Amazon introduced Amazon Now in Dubai and Abu Dhabi, pledging 15-minute delivery across 1,500-2,000 SKUs.

- September 2025: Carrefour opened a 10,000 square-meter automated distribution center in Dubai Industrial City, enabling same-day coverage for 90% of the city.

- April 2025: ADNOC Distribution partnered with Noon to retrofit 50 fuel stations into micro-fulfillment hubs that support 15-minute delivery.

- February 2025: Talabat acquired InstaShop for USD 32 million, consolidating dark-store capacity.

United Arab Emirates Quick Commerce Market Report Scope

The United Arab Emirates Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and Other Product Categories), Delivery Time Promise (Less than 10 Minutes, 11-30 Minutes, and 31-60 Minutes and More), City Tier (Tier I Metros, Tier II Cities, and Tier III and Below). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| Tier I Metros |

| Tier II Cities |

| Tier III and Below |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More | |

| By City Tier | Tier I Metros |

| Tier II Cities | |

| Tier III and Below |

Key Questions Answered in the Report

How large is the United Arab Emirates quick commerce market today?

The market stood at USD 187.41 million in 2026 and is projected to reach USD 233.78 million by 2031, growing at a 4.52% CAGR.

Which product category is expanding fastest within UAE quick deliveries?

Fresh produce and dairy is forecast to grow at 5.49% annually, outpacing overall sector growth due to demand for organic and locally farmed items.

What delivery-time segment is gaining the most traction?

Orders fulfilled in less than 10 minutes are set to rise at 6.02% CAGR, driven by ultra-fast services from Deliveroo, Amazon, and Talabat.

How are Tier II emirates contributing to growth?

Sharjah, Ajman, and Ras Al Khaimah are expected to compound at 5.27% annually as operators exploit lower rents and underserved expatriate customer bases.

Which factors most constrain profitability?

Aggressive discounting that lifts promotional spend to more than 18% of GMV and labor rules that restrict late-night shifts are the key margin pressures.

Who are the leading players in the UAE quick commerce space?

Talabat, Noon, Careem, Amazon, and Deliveroo constitute the top tier, collectively capturing roughly 65-70% of sector revenue.

Page last updated on: