Prosthetics And Orthotics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

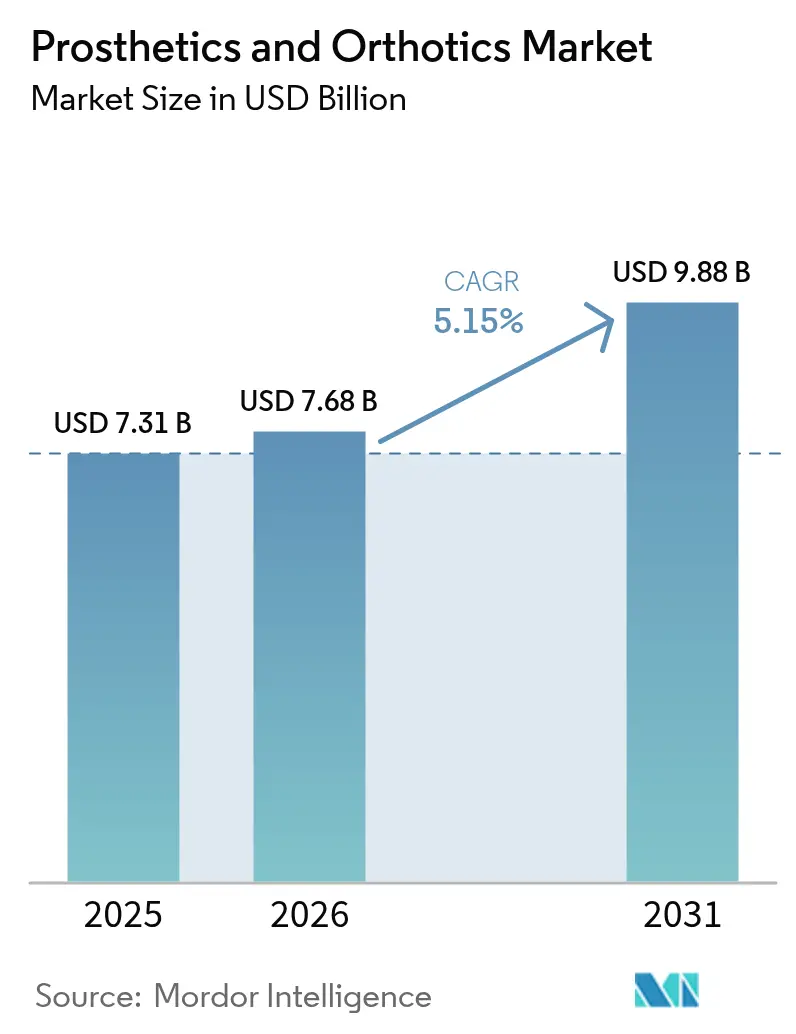

| Market Size (2026) | USD 7.68 Billion |

| Market Size (2031) | USD 9.88 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

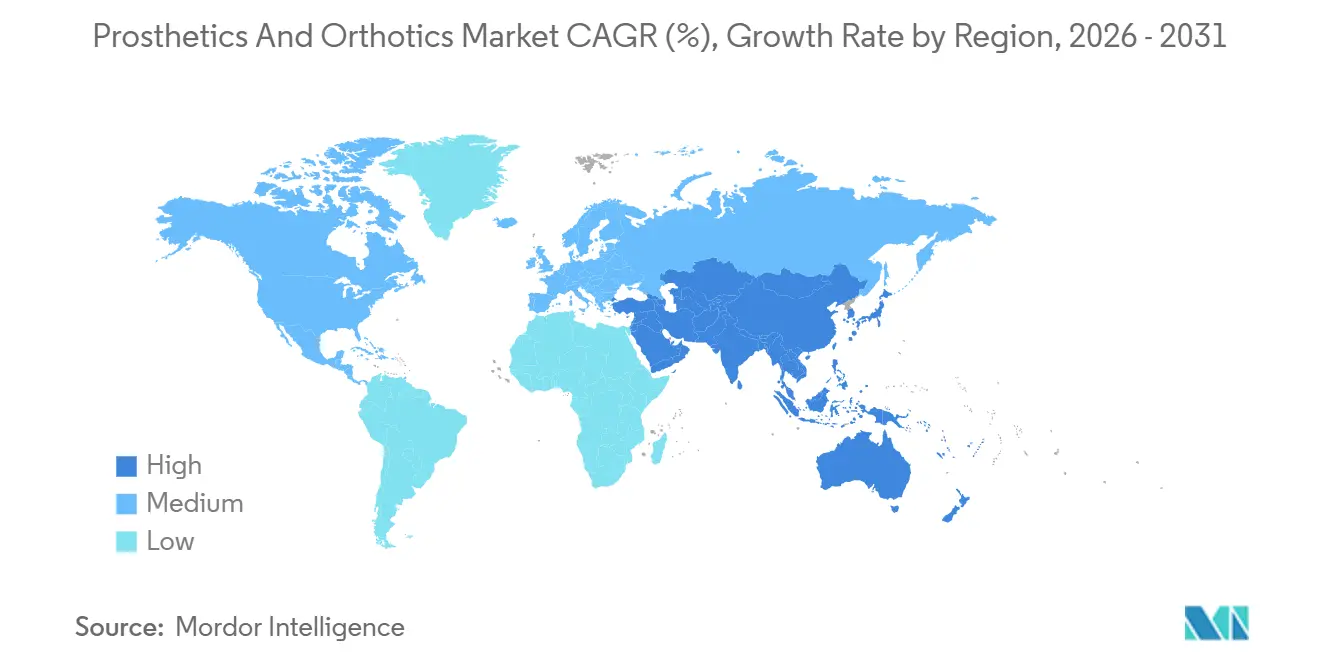

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Prosthetics And Orthotics Market Analysis by ���ϲ�����

The Prosthetics And Orthotics Market size is expected to grow from USD 7.31 billion in 2025 to USD 7.68 billion in 2026 and is forecast to reach USD 9.88 billion by 2031 at 5.15% CAGR over 2026-2031.

Rising diabetes-related amputations, an aging global population, and rapid advances in microprocessor-controlled devices jointly sustain demand. Providers increasingly integrate digital gait-analytics platforms that enable remote follow-up, while payers broaden coverage for premium components that cut fall-related readmissions. Private-equity interest in specialized clinic chains intensifies competitive dynamics, and 3D-printing compresses socket-fabrication lead times, improving patient experience. At the same time, military R&D pipelines accelerate commercial innovation, yielding powered joints and neural interfaces that redefine functional benchmarks.

Key Report Takeaways

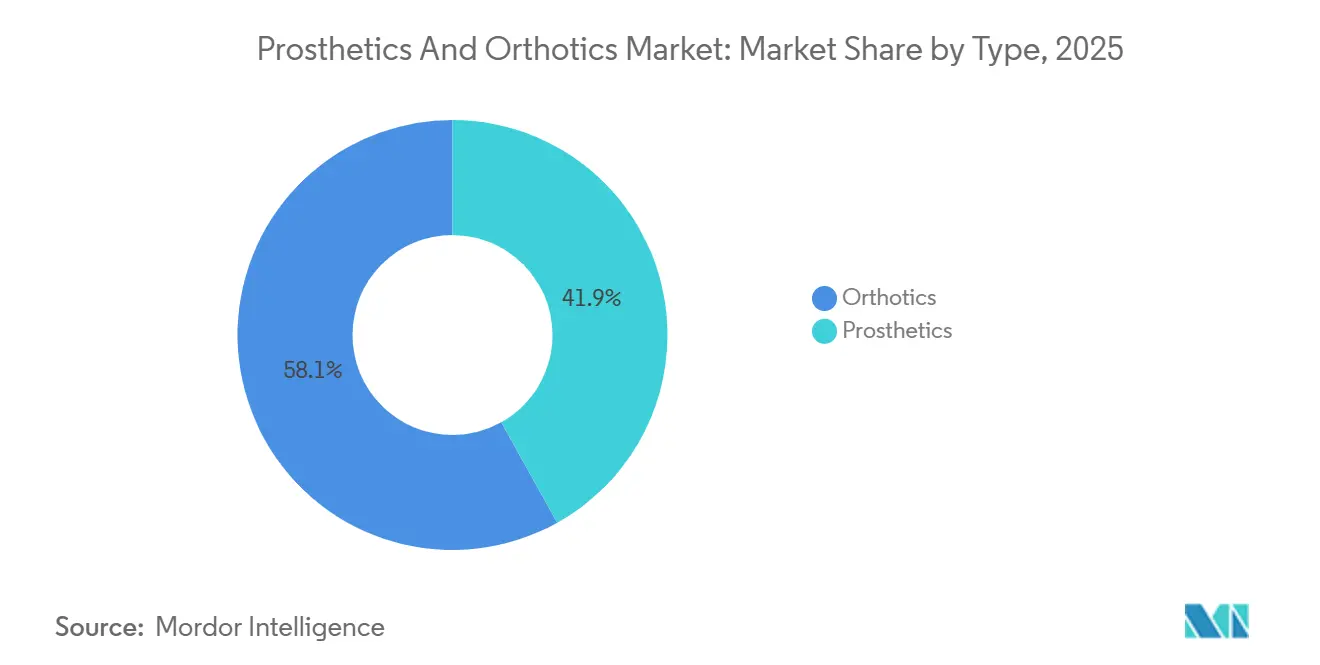

- By type, orthotics led with 58.1% of the Prosthetics and Orthotics market share in 2025, whereas prosthetics are on track to post a 6.22% CAGR to 2031.

- By technology, conventional body-powered systems held 45.11% of the prosthetics and Orthotics market size in 2025, while microprocessor-controlled systems are advancing at a 6.11% CAGR through 2031.

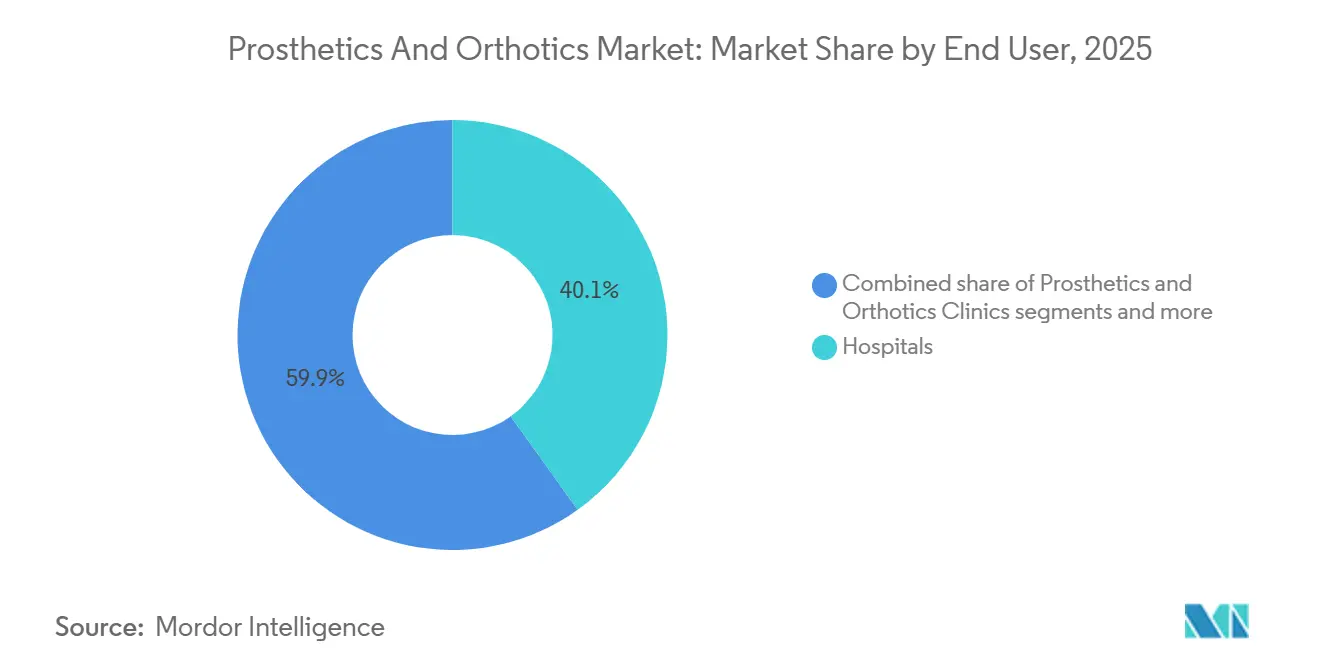

- By end user, hospitals accounted for 40.1% of revenue in 2025, yet dedicated prosthetics-and-orthotics clinics are forecast to expand at a 7.43% CAGR through 2031.

- North America accounted for 43.3% of the prosthetics and orthotics market share in 2025, whereas Asia-Pacific is set to grow at a 7.91% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Prosthetics And Orthotics Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Rise in Diabetes-Related Amputations | +1.2% | Global, acute in North America, Middle East, South Asia | Medium term (2-4 years) |

| Ageing Population & Osteoarthritis Burden | +1.0% | North America, Europe, Japan | Long term (≥ 4 years) |

| Advances in Micro-Processor & Myoelectric Technologies | +0.9% | North America, Europe, APAC | Medium term (2-4 years) |

| Expanding Reimbursement in Developed Markets | +0.8% | North America, Western Europe | Short term (≤ 2 years) |

| AI-Driven Predictive Gait-Analytics Adoption | +0.6% | North America, Europe pilots; APAC emerging | Medium term (2-4 years) |

| Military R&D Spill-Over Into Civilian Devices | +0.5% | United States, NATO allies, Israel | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rapid Rise in Diabetes-Related Amputations

Diabetes-linked lower-extremity amputations anchor baseline unit demand for prosthetic limbs, but they also catalyze reimbursement advocacy that ties advanced devices to limb-salvage outcomes. The International Diabetes Federation counted 588.7 million people with diabetes in 2024 and projects 852.5 million by 2050 [1]International Diabetes Federation, “IDF Diabetes Atlas, 10th Edition,” diabetesatlas.org. In the United States, roughly 165,000 amputation hospitalizations occur each year, with Black Americans experiencing a significantly higher incidence. Canada logged 7,720 diabetes-related amputations in its latest reporting cycle, underscoring pressures within single-payer systems. Manufacturers that embed residual-limb health sensors position themselves as partners in value-based care, moving revenue from episodic sales to recurring analytics subscriptions.

Ageing Population & Osteoarthritis Burden

The World Health Organization forecasts 2.1 billion people aged 60+ by 2050, up from 1.4 billion in 2024 [2]World Health Organization, “Ageing and Health,” who.int. Knee osteoarthritis alone affects 365 million patients, fueling orthotic brace prescriptions that delay total-joint replacement. Japan, where 29% of residents are 65 years or older, incubates ultralight carbon-fiber ankle-foot orthoses now diffusing into Western markets. Vendors that pair braces with telerehabilitation platforms capture adherence data prized by payers seeking outcome-based payments.

Advances in Microprocessor & Myoelectric Technologies

Medicare’s 2024 policy extends microprocessor-knee coverage to K2 ambulators, unlocking tens of thousands of additional candidates annually. Ottobock’s C-Leg 4 and Ö�����ܰ�’s POWER KNEE feature machine-learning algorithms that cut stair-fall risk. A Nature Medicine study validated the Agonist-Antagonist Myoneural Interface, which let amputees walk 41% faster and generate 187% greater peak power than traditional methods. Companies that invest in surgeon education on AMI techniques stand to dominate the premium limb-loss segment.

Expanding Reimbursement in Developed Markets

North American and European payers widen coverage for advanced components after evidence of lower fall-related admissions. U.S. private insurers, such as Health Care Service Corporation, updated their policies following Medicare’s lead. Germany’s sickness funds reimburse medically necessary devices yet demand direct price negotiation, trimming margins. In the U.K., National Health Service waitlist bottlenecks have given rise to an out-of-pocket fast-track market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Cost & Uneven Reimbursement | -0.7% | Global, acute in low- and middle-income countries; U.S. underinsurance pockets | Short term (≤ 2 years) |

| Shortage of Certified O&P Clinicians | -0.5% | United States, Canada, Western Europe; emerging APAC | Medium term (2-4 years) |

| Carbon-Fiber Supply-Chain Volatility | -0.3% | Global, concentrated among aerospace-grade composite users | Short term (≤ 2 years) |

| Pay-For-Outcome Reimbursement Risk | -0.2% | United States pilots; limited European uptake | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Device Cost & Uneven Reimbursement

Microprocessor knees list between USD 18,000-100,000, placing Ottobock’s C-Leg near USD 50,000-70,000 [3]Johns Hopkins Medicine, “Prosthetic Limb Costs and Insurance Coverage,” hopkinsmedicine.org. Medicaid caps and state variability still block many U.S. patients, while out-of-pocket costs in low-income nations surpass annual incomes. Tiered portfolios with upgrade paths remain scarce, leaving a gap for new entrants.

Shortage of Certified O&P Clinicians

Roughly 10,000 certified orthotists and prosthetists practice in the United States, an aging talent pool that cannot match accelerating demand. Rural users travel long distances for fittings, undermining compliance. Automation tools that pre-design sockets can lighten the clinician workload, but regulations still require licensed sign-off.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Orthotics Dominate, Prosthetics Accelerate

Orthotics captured 58.1% of the Prosthetics and Orthotics market share in 2025, led by lower-limb bracing for 365 million knee-osteoarthritis patients. Spinal and upper-limb supports add stable revenue, benefiting from prefabricated SKUs ordered via e-commerce. Conversely, prosthetics contributed a smaller base yet will post a 6.22% CAGR, propelled by microprocessor-controlled knees that enable variable cadence. Consumables such as liners and suspension sleeves provide sticky recurring sales that anchor the Prosthetics and Orthotics market size growth across replacement cycles.

ISO 22523 and ISO 8549 compliance streamlines CE-marking and FDA 510(k) pathways. Orthotic commoditization risk rises as 3D-printing lowers entry barriers, whereas proprietary control algorithms protect prosthetic margins. Vendors bundling digital physiotherapy content with braces further differentiate in a crowded field.

By Technology: Microprocessor Systems Gain Ground

Conventional body-powered devices retained 45.11% of the prosthetics and Orthotics market size in 2025, thanks to affordability and low maintenance. Yet microprocessor knees and ankles are gaining at 6.11% CAGR, buoyed by 2024 reimbursement expansion. Electric myoelectric hands target users who demand precision grip for office tasks, while hybrid systems offer battery-free backup valued by military users.

Additive-manufactured sockets slash fabrication time to 48 hours, though fatigue limitations curb adoption for definitive limbs. Robotic rehab exoskeletons generate per-session revenue at therapy centers, and sensory-feedback prototypes such as Integrum’s OPRA pave the path to intuitive limb control. The technology mix thus tilts toward smart, service-enabled hardware that maintains high average selling prices.

By End User: Clinics Capture Specialized Fitting

Hospitals and clinics accounted for 40.1% of 2025 revenue, bundling acute care, rehab, and first-fit devices. Specialized prosthetics-and-orthotics clinics, however, are set to post a 7.43% CAGR as private-equity funding fuels roll-ups offering same-day digital scanning. Home-care channels expand via off-the-shelf braces delivered with tele-coaching, while Veterans Affairs centers sustain predictable device cycles at negotiated prices.

Nascent direct-to-consumer portals sell cosmetic covers and activity feet, capturing accessory share without violating fitting regulations. An omnichannel model—acute fitting in hospitals, complex cases at specialty clinics, consumables online—best aligns with evolving user preferences.

Geography Analysis

North America held 43.3% of Prosthetics and Orthotics market share in 2025 on the strength of VA funding and Medicare reforms. Canada’s single-payer model reimburses clinically necessary devices, yet long queues spur a parallel cash-pay segment. Mexico relies on charitable and medical-tourism flows, limiting premium uptake.

Europe ranks second by value; Germany’s statutory system funds devices yet caps tariffs below full cost, driving volume but squeezing profitability. The European Union Medical Device Regulation stretches notified-body capacity, delaying product launches and dampening short-term Prosthetics and Orthotics market size addition.

Asia-Pacific is forecast for a 7.91% CAGR through 2031, fueled by India’s Assistance to Disabled Persons subsidy, China’s wider urban insurance coverage, and Japan’s super-aged demographic looking for lightweight orthoses. South Korea and Australia exhibit high per-capita adoption within universal schemes. Southeast Asia remains cost-sensitive and favors low-cost mechanical limbs. The Middle East bifurcates between GCC states that reimburse premium devices and sub-Saharan Africa, where NGO donations dominate. South America’s growth is tempered by fiscal constraints in Brazil and Argentina.

Competitive Landscape

Ottobock, Ö�����ܰ�, and Hanger Inc. collectively account for a significant portion of global revenue, leaving a fragmented tail of regional specialists and contract manufacturers. Hanger’s USD 1.2 billion buyout by Patient Square Capital illustrates rising private-equity appetite for cash-flow-stable clinic chains. Incumbents differentiate via proprietary microprocessor algorithms, vertically integrated clinics, and component ecosystems that discourage cross-brand mixing.

Emerging challengers apply 3D-printing to deliver custom sockets at discounts, though regulatory oversight checks rapid scaling. Integrum’s osseointegrated implants and sensory-feedback pathway create a premium niche shielded by surgical complexity. Patent filings now center on software, Ö�����ܰ�’s 2024 machine-learning socket-fit algorithm being one example, signaling that competitive advantage pivots toward data as much as hardware.

Robotic exoskeleton suppliers such as Ekso Bionics and Cyberdyne monetize per-therapy-session models, sidestepping direct competition with personal prosthetics. Overall, mid-level concentration and technology segmentation together define a market where scale, digital infrastructure, and clinician partnerships outweigh pure manufacturing capacity.

Prosthetics And Orthotics Industry Leaders

Ö�����ܰ�

Ottobock

Bauerfeind AG

Blatchford Limited

Hanger Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Ö�����ܰ� reported that updated Local Coverage Determinations (LCDs) took effect on 25 January 2026, expanding access to osteoarthritis knee braces by allowing clinicians to cite a patient’s “willingness to use” the device as a qualifying reimbursement criterion.

- October 2025: Motorica launched a digital-first workflow for pediatric and adult upper-limb prosthetics that relies on smartphone-based 3D scanning and cloud-hosted digital modeling to deliver highly customized bionic arms without the need for traditional physical molds.

- April 2025: Ö�����ܰ� introduced the Pro-Flex Terra foot prosthesis, co-developed with BASF, which employs Cellasto micro-cellular material that adapts to walking conditions without mechanical adjustments and replicates muscle-tendon energy return.

Global Prosthetics And Orthotics Market Report Scope

As per the scope of the report, prosthetics and orthotics (P&O) is a specialized healthcare field that combines clinical assessment with engineering to restore mobility and enhance physical function. While often practiced together, they serve distinct purposes: prosthetics involve the design and fitting of artificial limbs to replace missing body parts due to amputation or congenital conditions, while orthotics focuses on external braces or supports (orthoses) that stabilize, align, or improve the function of existing limbs or the spine.

The prosthetics and orthotics market is segmented by type, technology, end-user, and geography. By type, it is segmented into orthotics and prosthetics. By technology, the market is segmented into conventional / body-powered, electric-powered / myoelectric, micro-processor controlled, hybrid, 3D-Printed / additive-manufactured, robotic / powered exoskeletal, and sensory-feedback enabled. By End users, the market is segmented into hospitals, prosthetics & orthotics clinics, rehabilitation centers, home-care settings, military & veterans affairs facilities, and e-commerce / direct-to-consumer.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Orthotics | Lower-Limb Orthotics | Ankle-Foot Orthoses (AFO) |

| Knee Orthoses | ||

| Hip Orthoses | ||

| Upper-Limb Orthotics | ||

| Spinal Orthotics | ||

| Prosthetics | Lower-Extremity Prosthetics | Micro-processor Knees |

| Powered Ankles/Feet | ||

| Upper-Extremity Prosthetics | ||

| Liners, Sockets & Modular Components | ||

| Conventional / Body-Powered |

| Electric-Powered / Myoelectric |

| Micro-processor Controlled |

| Hybrid |

| 3D-Printed / Additive Manufactured |

| Robotic / Powered Exoskeletal |

| Sensory-Feedback Enabled |

| Hospitals |

| Prosthetics & Orthotics Clinics |

| Rehabilitation Centers |

| Home-Care Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Orthotics | Lower-Limb Orthotics | Ankle-Foot Orthoses (AFO) |

| Knee Orthoses | |||

| Hip Orthoses | |||

| Upper-Limb Orthotics | |||

| Spinal Orthotics | |||

| Prosthetics | Lower-Extremity Prosthetics | Micro-processor Knees | |

| Powered Ankles/Feet | |||

| Upper-Extremity Prosthetics | |||

| Liners, Sockets & Modular Components | |||

| By Technology | Conventional / Body-Powered | ||

| Electric-Powered / Myoelectric | |||

| Micro-processor Controlled | |||

| Hybrid | |||

| 3D-Printed / Additive Manufactured | |||

| Robotic / Powered Exoskeletal | |||

| Sensory-Feedback Enabled | |||

| By End User | Hospitals | ||

| Prosthetics & Orthotics Clinics | |||

| Rehabilitation Centers | |||

| Home-Care Settings | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the forecast value of the Prosthetics and Orthotics market by 2031?

It is projected to reach USD 9.88 billion by 2031.

Which technology segment is growing fastest within the Prosthetics and Orthotics market?

Microprocessor-controlled technology leads with a 6.11% CAGR forecast for 2026-2031.

Why is Asia-Pacific considered the most attractive growth region?

Policy subsidies in India, Japan’s super-aged population, and broader insurance in China drive a 7.91% CAGR outlook.

How did Medicare influence U.S. demand in 2024?

By extending microprocessor-knee coverage to K2 ambulators, adding tens of thousands of eligible beneficiaries.

Page last updated on: