Pet Oral Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.24 Billion |

| Market Size (2031) | USD 4.43 Billion |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Pet Oral Care Products Market Analysis by ���ϲ�����

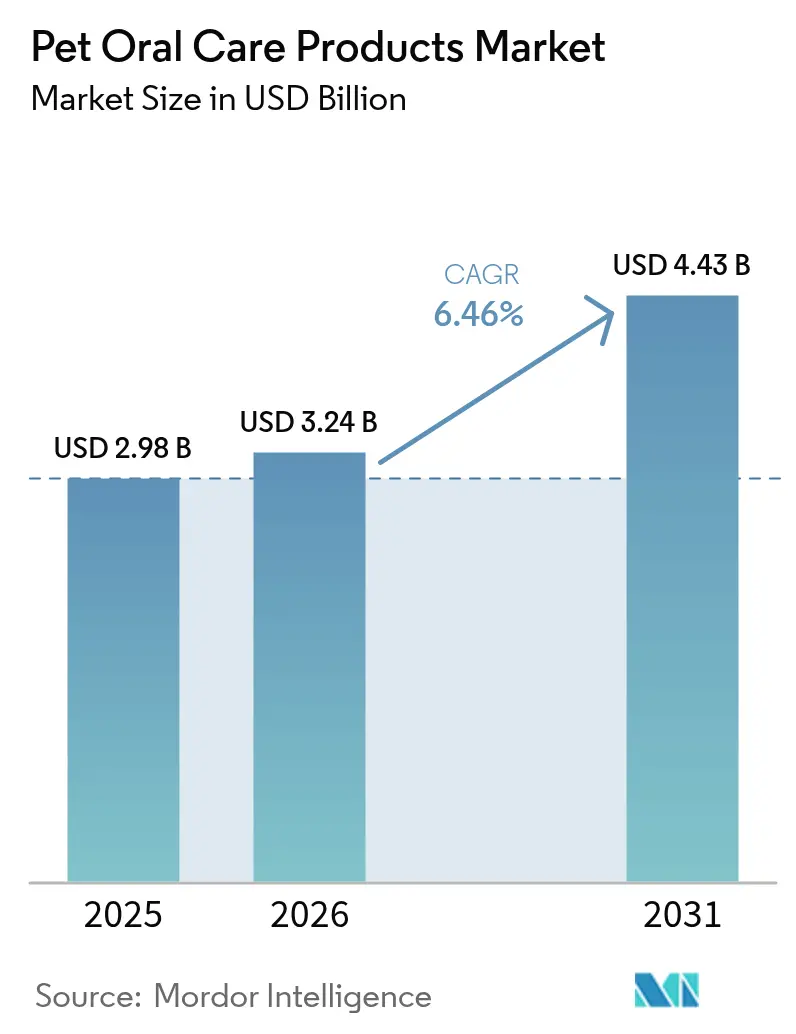

The pet oral care products market size is projected to expand from USD 2.98 billion in 2025 and USD 3.24 billion in 2026 to USD 4.43 billion by 2031, registering a 6.46% CAGR between 2026 to 2031. Improving preventive care awareness, rapid uptake of functional chews, and digitally enabled monitoring are driving momentum across every region. Disease prevalence remains high, affecting more than 8 in 10 adult companion animals, keeping the clinical need visible to owners and veterinarians. E-commerce subscriptions now translate compliance gaps into recurring revenue, aided by same-day delivery and simple auto-reorder options that lift basket size. Ingredient innovation, especially seaweed extracts, enzymes, and postbiotics, gives premium brands space to command price premiums while satisfying the growing demand for label transparency. At the same time, counterfeit risk, inflation-driven price sensitivity, and variable claim regulations generate headwinds that manufacturers must address through authentication tools, pack downsizing, and rigorous clinical validation.

Key Report Takeaways

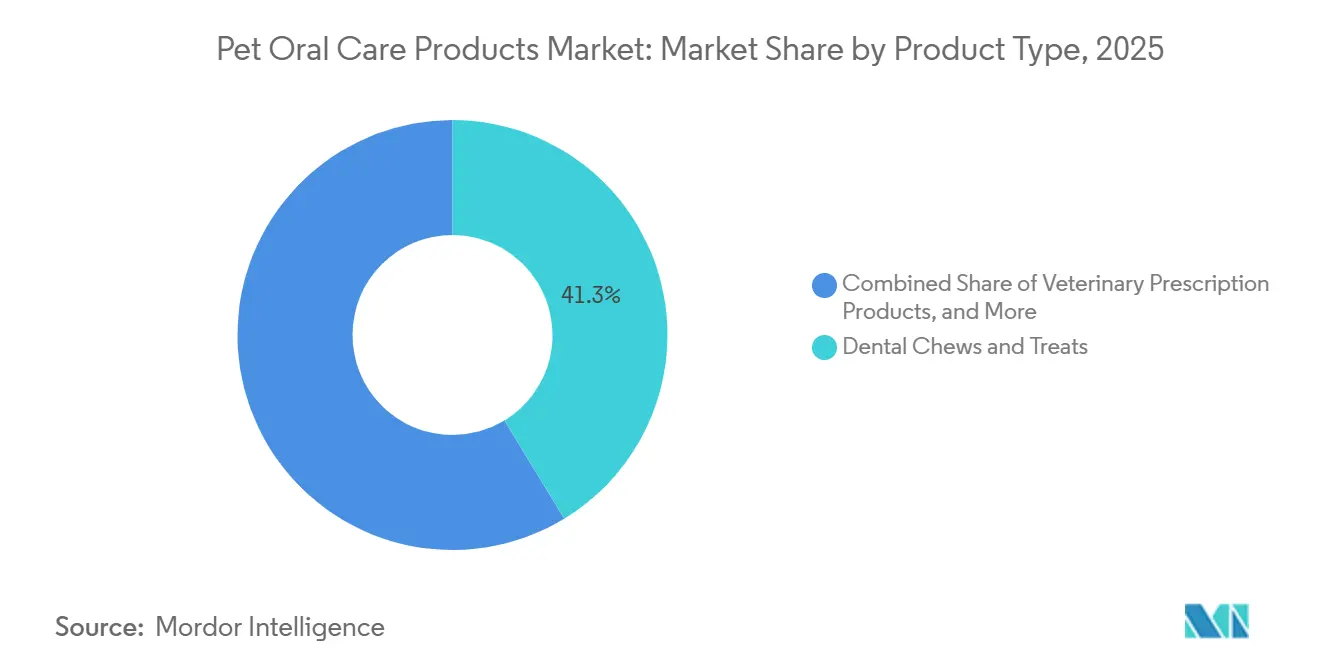

- By product type, dental chews and treats led with 41.3% of the pet oral care products market share in 2025, while oral probiotic tablets are forecast to expand at a 7.4% CAGR through 2031.

- By animal type, dogs accounted for a 64.5% share of the pet oral care products market size in 2025, and cats are advancing at a 6.1% CAGR to 2031.

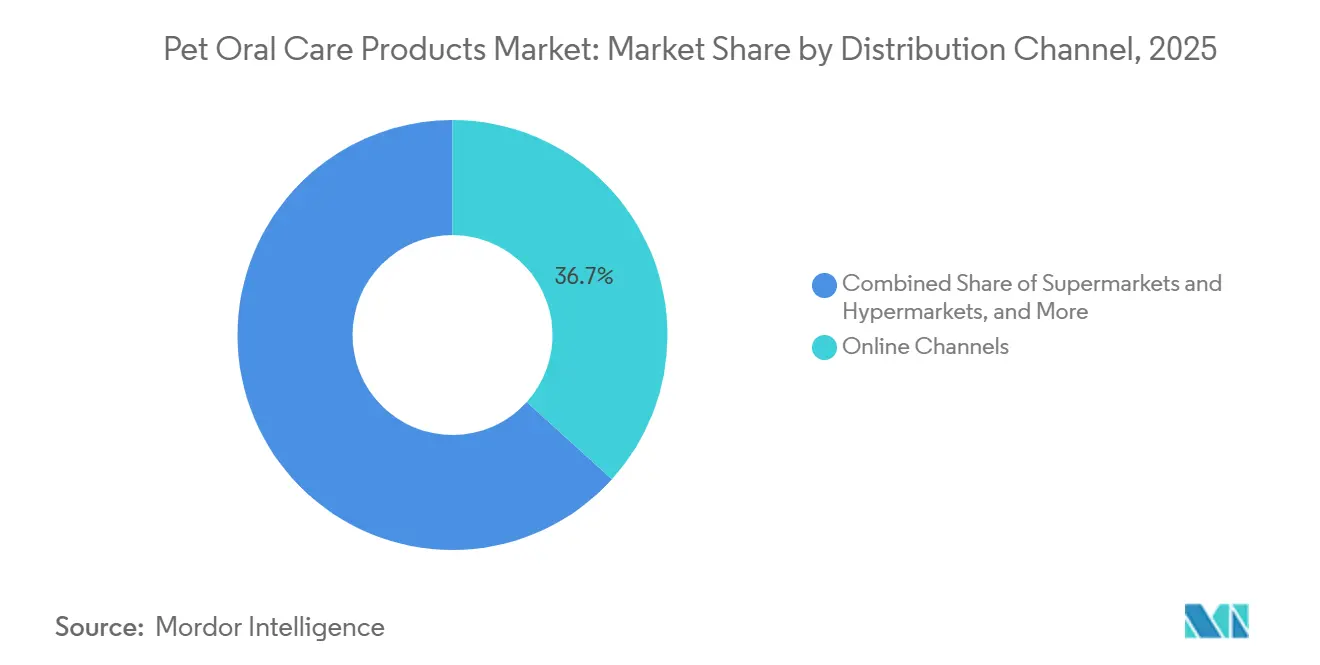

- By distribution channel, online platforms captured 36.7% of revenue share in 2025, and subscription boxes are projected to show the fastest growth at a 7.9% CAGR through 2031.

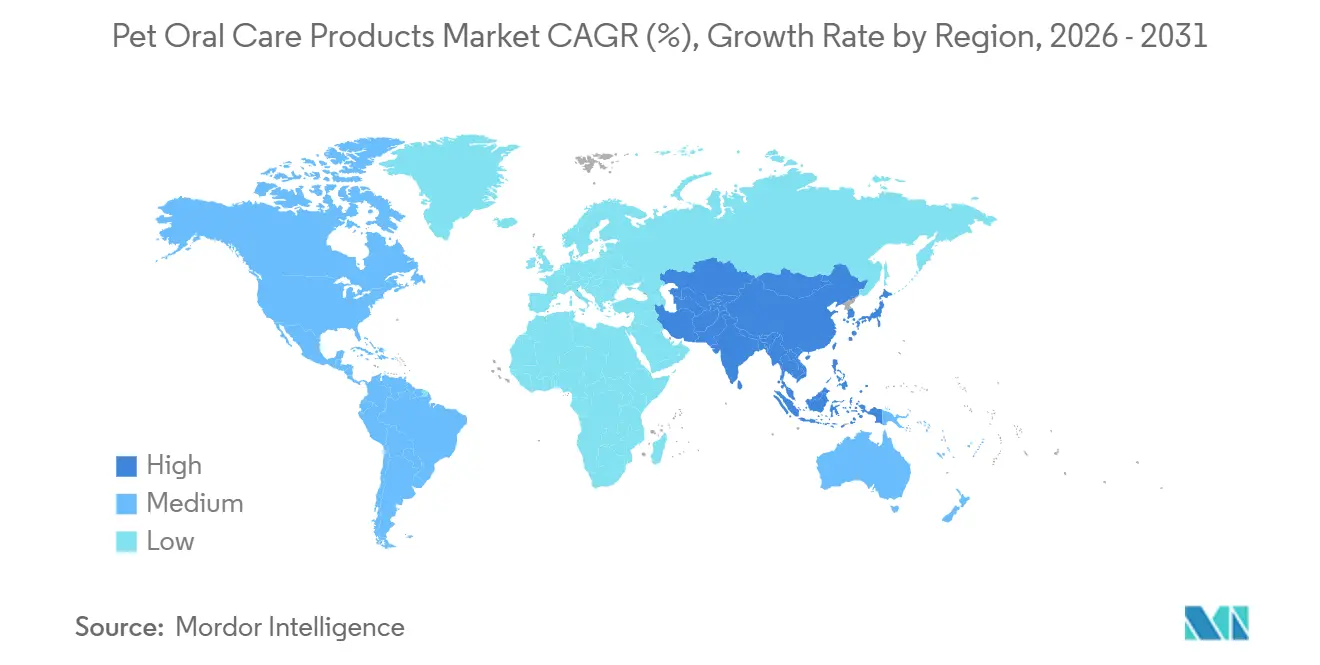

- By geography, North America held a 46.5% share in 2025, while Asia-Pacific is the fastest-growing region, with a 6.6% CAGR to 2031.

- Mars, Incorporated, Colgate-Palmolive Company, Nestlé Purina PetCare, Virbac S.A., and Elanco Animal Health Incorporated accounted for significant market revenue in 2025.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pet Oral Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of periodontal disease in pets | +0.9 | North America and Europe, with spillover worldwide | Long term (≥ 4 years) |

| Rising pet humanization and premium spend | +1.0 | North America, Europe, and urban Asia-Pacific | Medium term (2 - 4 years) |

| E-commerce expansion boosting direct-to-consumer oral-care subscriptions | +0.8 | Global, led by North America and Europe | Short term (≤ 2 years) |

| Novel functional ingredients driving product differentiation | +0.9 | North America and Europe first, then Asia-Pacific | Medium term (2 - 4 years) |

| Artificial intelligence enabled chew design improving dental efficacy and owner engagement | +0.5 | North America and Europe initially | Medium term (2 - 4 years) |

| Personalized microbiome-targeted formulations gaining traction | +0.4 | North America and Europe, and niche Asia-Pacific markets | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

High Prevalence of Periodontal Disease in Pets

Periodontal disease already affects most adult dogs and cats, making it the single largest clinical trigger for product adoption. Average professional cleaning costs remain above USD 350 per procedure in the United States, which pushes many owners toward preventive chews and water additives that appear cost-effective over time[1]Source: American Society for the Prevention of Cruelty to Animals Data Team, “Pet Ownership Costs,” aspca.org. As pet populations age in Europe and North America, incidence is set to rise further, deepening baseline demand. Emerging economies such as China are seeing younger pet cohorts today, yet a similar burden is projected as these cohorts mature, keeping the pet oral care products market firmly in a growth cycle.

Rising Pet Humanization and Premium Spend

In the United States, the majority of pet owners consider their pets as family and frequently purchase enhanced formulations that mirror human dental care practices. This trend highlights the growing emphasis on pet health and wellness, with owners increasingly seeking products that align with their own standards of care. A similar trend is observed in South America, where the majority of the pet owners share this perspective. However, taxation in Brazil is reducing disposable income and potentially affecting purchasing behavior. Despite this, brands with third-party clinical validation, such as the Veterinary Oral Health Council seal, effectively leverage this premium sentiment to justify higher shelf prices, contributing to value growth in the pet oral care products market.

Novel Functional Ingredients Driving Product Differentiation

Seaweed extract Ascophyllum nodosum and postbiotic Lactobacillus plantarum strains have demonstrated effectiveness in reducing plaque and halitosis, as evidenced by peer-reviewed trials. These ingredients target oral bacteria and improve overall oral hygiene in pets. Enzyme complexes containing glucose oxidase disrupt biofilm without the need for brushing, addressing compliance challenges and making oral care more accessible for pet owners. Manufacturers use ingredient science to enhance the premium positioning of pet oral care products and secure veterinarian endorsements, thereby further building consumer trust. Increasing clinical evidence is encouraging retailers to allocate additional shelf space, thereby expanding consumer access and driving market growth.

Personalized Microbiome-Targeted Formulations Gaining Traction

Companies are now developing strains specifically suited to the unique oral microbiota of dogs and cats. This differentiation addresses the distinct needs of each species, enhancing product effectiveness and improving overall oral health. Postbiotics offer shelf stability, eliminating the need for cold chain logistics and attracting online shoppers with their convenience and longer shelf life. Early adopters in North America and Europe are willing to pay premium prices, as noticeable improvements in breath freshness within one week encourage repeat purchases and build customer loyalty. While regulatory clarity will influence scalability, pilot launches indicate potential for broader market adoption in the future, signaling a shift toward mainstream acceptance of these products and their benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low owner compliance with tooth-brushing regimens | −0.8 | Worldwide, acute in emerging regions | Medium term (2 - 4 years) |

| Regulatory ambiguity on product efficacy claims | −0.5 | North America and Europe chiefly | Long term (≥ 4 years) |

| Counterfeit chew products undermining brand trust | −0.4 | Online channels in Asia-Pacific and South America | Short term (≤ 2 years) |

| Inflation-driven price sensitivity in emerging markets | −0.6 | South America, Middle East, and Africa | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Low Owner Compliance with Tooth-Brushing Regimens

Daily brushing remains a challenging goal. Surveys in Sweden and the United Kingdom indicate adherence rates remain less, even with veterinary recommendations. Factors such as pet resistance, time limitations, and the lack of immediate visible results discourage owners. While passive delivery formats are increasingly adopted, they do not fully replicate the effectiveness of mechanical plaque removal, limiting their impact on population-level disease reduction. Brands are focusing on education and offering bundled products, such as chews and easy-grip finger wipes, to gradually improve compliance. Additionally, efforts are underway to develop innovative tools and techniques that simplify the brushing process, aiming to address barriers faced by pet owners and improve overall adherence rates.

Regulatory Ambiguity on Product Efficacy Claims

The Food and Drug Administration Center for Veterinary Medicine distinguishes clearly between food and drug classifications. Recent policy changes have transferred responsibility for ingredient definitions to individual states, leading to duplication of costs for nationwide product launches[2]Source: Food and Drug Administration Center for Veterinary Medicine, “Regulatory Updates,” fda.gov. This shift creates challenges for companies seeking to maintain consistency across state lines, thereby increasing compliance complexity. Additionally, European Union regulations 2025/2091 and 2025/2154 mandate good manufacturing practices for veterinary medicinal products, compelling smaller companies to outsource production[3]Source: European Food Safety Authority, “Good Manufacturing Practice Regulations,” efsa.europa.eu. These regulations aim to ensure product quality but place significant financial and operational burdens on smaller firms. This fragmented regulatory environment requires global brands to stagger product rollouts and modify labels, increasing overhead costs and hindering growth in the pet oral care products market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dental Chews and Treats Dominate but Oral Probiotic Tablets Gain Ground

Dental chews and treats were the largest product type, accounting for 41.3% of the pet oral care products market share in 2025. Many formulations carry the Veterinary Oral Health Council seal, lending credibility that supports premium shelf placement. Wider format options now address breed size, calorie concerns, and targeted mechanical abrasion for back molars. As omnichannel retailers expand shelf slots, chews remain the top-of-mind entry point, especially when owners first recognize bad breath.

The fastest growing segment, oral probiotic tablets, is posting a 7.4% CAGR through 2031. Microbiome-modulating postbiotic strains provide noticeable improvements in breath freshness within seven days, offering a clear benefit that fosters word-of-mouth adoption. Combination packs with tablets and chews deliver dual-action benefits, improving plaque control without the need for brushing. This approach also creates upselling opportunities, driving growth in the pet oral care products market.

By Animal Type: Dogs Lead while Cats Accelerate

Dogs are the largest pet type and account for 64.5% of the pet oral care products market size in 2025, as canine owners show greater engagement with at-home routines and veterinarians emphasize gum health during annual visits. Larger oral cavities and reward-based training make it easier to administer chews and flavored pastes. Mass-market advertising further focuses brand messaging on canines, reinforcing their dominance among first-time buyers.

Cats, advancing at a 6.1% CAGR, are starting to close the gap. Feline offerings now feature smaller chew dimensions, softer textures, and salmon or poultry flavor profiles that align with natural preferences. Antech Diagnostics’ feline-specific RapidRead Dental tool guides veterinarians toward earlier lesion detection, which, in turn, prompts owners to maintain daily home care. As indoor cat populations rise across Asia-Pacific, this momentum should translate into additional share gains in the pet oral care products market.

By Distribution Channel: Online Rises while Subscription Boxes Disrupt

Online platforms were the largest distribution channel, accounting for 36.7% of pet oral care product sales in 2025. Search filters, bundled discounts, and a fast checkout experience encourage multi-unit purchases, while consumer reviews reduce perceived risk for first-time buyers. In China, live-stream commerce on Douyin and Xiaohongshu helps niche brands surface quickly, adding depth to categories without the constraints of shelf space.

Subscription boxes are recording the fastest growth, rising 7.9% through 2031, as curated kits arrive at predictable intervals that align with product depletion cycles. Brands use subscriber data to refine formulations and cross-sell supplements, creating sticky customer relationships. Offline retailers respond by adding click-and-collect services and loyalty apps, yet the convenience edge of direct-to-home delivery keeps pushing more volume toward e-commerce, reinforcing digital leadership within the pet oral care products market.

Geography Analysis

North America is the largest region, capturing 46.5% of the pet oral care products market in 2025, led by the United States, where 56.3 million households keep dogs and 43.1 million keep cats[4]Source: American Veterinary Medical Association, "U.S. pet ownership statistics," avma.org. Veterinary advice continues to influence purchase decisions, and recent artificial intelligence launches from Mars, Incorporated and Antech heighten consumer awareness, reinforcing uptake. Price increases in professional services also nudge owners toward preventive products. Canada mirrors these trends but exhibits slightly lower premium spend, while Mexico shows volume growth through value channels, moderated by disposable income levels.

Asia-Pacific posts the fastest 6.6% CAGR through 2031, driven by rising disposable incomes, urban densification, and smaller household sizes, which are boosting pet adoption. Chinese consumers spend more per month on pets, a clear sign of willingness to pay for premium oral care. Japan’s aging pet cohort demands senior-focused formulations, while India and South Korea deliver double-digit volume gains from a low base. High e-commerce penetration shortens market-entry lead times, allowing innovators to capture share quickly.

Europe benefits from strict welfare legislation taking effect in 2028 that mandates microchipping and elevates care standards. Germany, the United Kingdom, and France make up the core demand triangle, with Northern Europe showing the highest veterinary compliance rates. Good manufacturing practice regulations, scheduled for implementation in 2026, are projected to limit the involvement of smaller importers, leading to a consolidation of market share among established brands. Currency stability and moderate inflation continue to support purchasing power, ensuring steady growth in the pet oral care products market.

Competitive Landscape

The pet oral care products market is characterized by moderate concentration, where a small group of multinational leaders balances the influence of specialty disruptors. Mars, Incorporated, Colgate-Palmolive Company, Nestlé Purina PetCare, Virbac S.A., and Elanco Animal Health Incorporated accounted for significant market revenue in 2025. The company relies on global logistics and veterinary trust to secure broad availability. Mars, Incorporated expanded its portfolio in 2025 with the Greenies Canine Dental Check, a smartphone image analysis tool that links products to personalized advice, giving the company a data advantage and deepening retention inside the pet oral care products market.

Swedencare AB is driving ingredient innovation and a surge in the dental segment following the acquisition of Vetio. Direct-to-consumer specialists like Petlab Co. and Zesty Paws thrive online through influencer partnerships and subscription bundles. Central Garden and Pet Company boosts Nylabone chew sales by refreshing flavor assortments, while Virbac S.A. and Elanco Animal Health Incorporated defend prescription niches by integrating periodontal gels into in-clinic treatment protocols.

Intellectual property filings point to future convergence between toys, diagnostics, and consumables. Hill’s Pet Nutrition holds patents for sensor-embedded play devices that gather breath and pH data, laying the groundwork for personalized regimens. Better Business Bureau alerts about counterfeit chews spur legitimate firms to adopt blockchain traceability, heightening barriers for gray-market sellers and reinforcing trust in branded offerings. Private equity continues to view the segment as fertile, with roll-up strategies accelerating consolidation across mid-tier brands.

Pet Oral Care Products Industry Leaders

-

Mars, Incorporated

-

Colgate-Palmolive Company

-

Nestlé Purina Petcare

-

Virbac S.A.

-

Elanco Animal Health Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: OMNI Pet Limited has introduced Dual-Texture Dental Sticks for dogs, featuring a unique design and "PlaqBlast" technology to reduce plaque and improve breath. The product features a hard, eight-sided snowflake-shaped outer shell that mechanically removes plaque and debris, complemented by a softer, mint-flavored core that releases natural anti-plaque ingredients.

- October 2025: HICC Pet has introduced Oral Care Gel, featuring a gentle, rinse-free formula containing Hypochlorous Acid (HOCl), a naturally occurring antimicrobial agent trusted by veterinarians. The primary active ingredient, Hypochlorous Acid (HOCl), is a substance naturally produced by mammalian white blood cells, which effectively eliminates odor-causing compounds and helps break down plaque and tartar.

- July 2025: Pet Honesty, a science-driven pet supplement brand recognized for its vet-recommended formulations, has introduced Fresh Breath Dental Bites, a clean-label dental supplement designed exclusively for cats. These chews, featuring a crunchy exterior and creamy interior, promote healthy gums, cleaner teeth, and fresher breath without the need for brushing.

- May 2025: Mars, Incorporated has launched a range of artificial intelligence-powered digital tools to help pet owners monitor their pets' health. The initiative begins with a smartphone-based dental check for dogs, utilizing AI trained on over 53,000 images to analyze photos of dogs' teeth and gums. This tool helps identify signs of tartar buildup and gum irritation.

Global Pet Oral Care Products Market Report Scope

Pet oral care products include various appliances, medicines, and other chemicals used to maintain proper oral hygiene and prevent dental diseases in pets. The Pet Oral Care Products Market Report is Segmented by Product Type (Toothpaste, Toothbrush, Mouthwash and Rinses, Dental Chews and Treats, Water Additives and Sprays, Veterinary Prescription Products, Dental Wipes, Oral Probiotic Tablets, and Other Product Types), by Animal Type (Dogs, Cats, Rabbits, Ferrets, and Others), by Distribution Channel (Supermarkets and Hypermarkets, Online Channels, Specialized Pet Shops, Veterinary Channels, Subscription Boxes, Grooming Salons, and Other Channels), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Toothpaste |

| Toothbrush |

| Mouthwash and Rinses |

| Dental Chews and Treats |

| Water Additives and Sprays |

| Veterinary Prescription Products |

| Dental Wipes |

| Oral Probiotic Tablets |

| Other Product Types |

| Dogs |

| Cats |

| Rabbits |

| Ferrets |

| Others |

| Supermarkets and Hypermarkets |

| Online Channels |

| Specialized Pet Shops |

| Veterinary Channels |

| Subscription Boxes |

| Grooming Salons |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Product Type | Toothpaste | |

| Toothbrush | ||

| Mouthwash and Rinses | ||

| Dental Chews and Treats | ||

| Water Additives and Sprays | ||

| Veterinary Prescription Products | ||

| Dental Wipes | ||

| Oral Probiotic Tablets | ||

| Other Product Types | ||

| By Animal Type | Dogs | |

| Cats | ||

| Rabbits | ||

| Ferrets | ||

| Others | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Online Channels | ||

| Specialized Pet Shops | ||

| Veterinary Channels | ||

| Subscription Boxes | ||

| Grooming Salons | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What growth rate is projected for the pet oral care products market through 2031?

The category is forecast to post a 6.46% compound annual growth rate between 2026 and 2031, rising from USD 3.24 billion in 2026 to USD 4.43 billion by the end of the period.

Which product format currently holds the largest share?

Dental chews and treats account for 41.3% of global revenue thanks to their simplicity, palatable flavors, and broad veterinary support.

Why are probiotic tablets considered the fastest growing segment?

Postbiotic formulations demonstrate quick breath-freshening benefits and require no brushing, driving a 7.4% annual growth pace to 2031.

How important is online retail for the category?

Online platforms already make up 36.7% of worldwide sales, and subscription models that deliver curated dental kits are expanding nearly 8% annually.

Which region leads and which region grows fastest?

North America commands 46.5% of sales today, while Asia-Pacific shows the highest regional growth at a 6.6% compound annual rate through 2031.

Page last updated on: