Pet Daycare Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

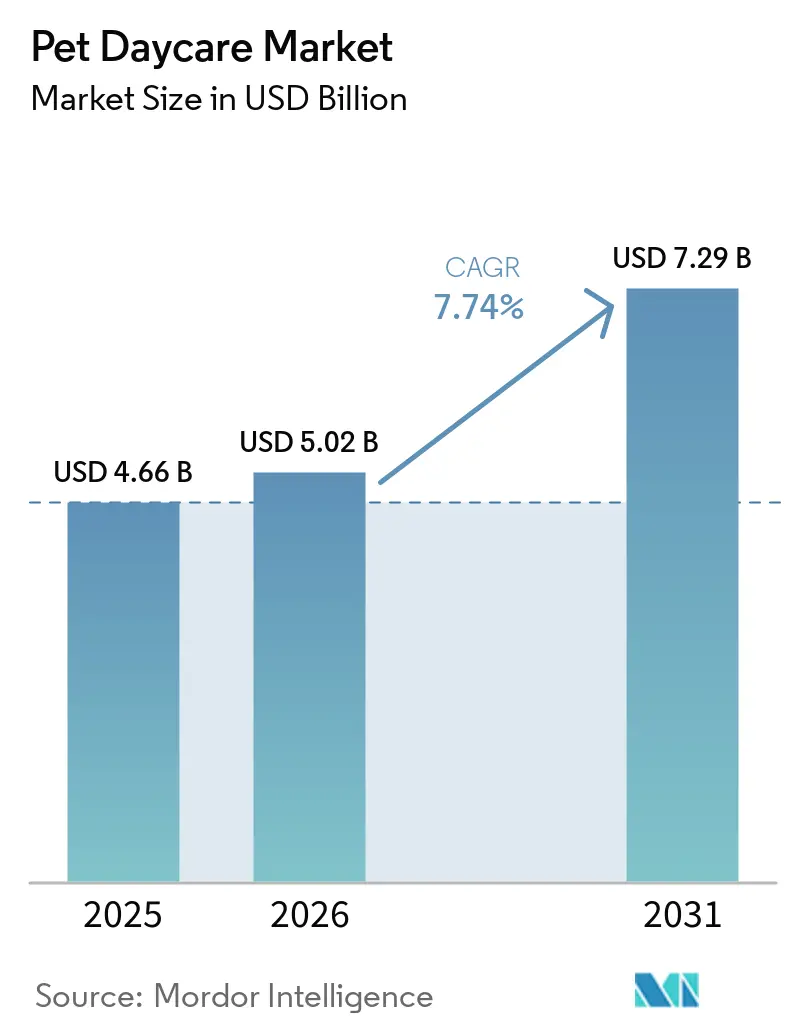

| Market Size (2026) | USD 5.02 Billion |

| Market Size (2031) | USD 7.29 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Pet Daycare Market Analysis by ���ϲ�����

The pet daycare market size was valued at USD 4.66 billion in 2025 and is anticipated to grow from USD 5.02 billion in 2026 to USD 7.29 billion by 2031, registering a 7.74% CAGR through the forecast period (2026-2031). The pet daycare market is built on a durable demand base, as many households now treat companion animal care as a routine spending priority rather than a discretionary purchase. North America remains the largest regional revenue center because franchise penetration is highest there, organized supply is more mature, and full-day work schedules keep supervised daytime care relevant for urban households. Asia-Pacific is the fastest-growing regional market for pet daycare, driven by urbanization, rising pet ownership, and first-time premium pet care spending, which are widening the formal customer base. Digital booking, recurring memberships, and enrichment-based services are improving revenue quality for operators that can pair convenience with visible care standards. Higher labor, real estate, insurance, and compliance costs are also raising the operating threshold, creating more room for disciplined, tech-enabled providers in the pet daycare market.

Key Report Takeaways

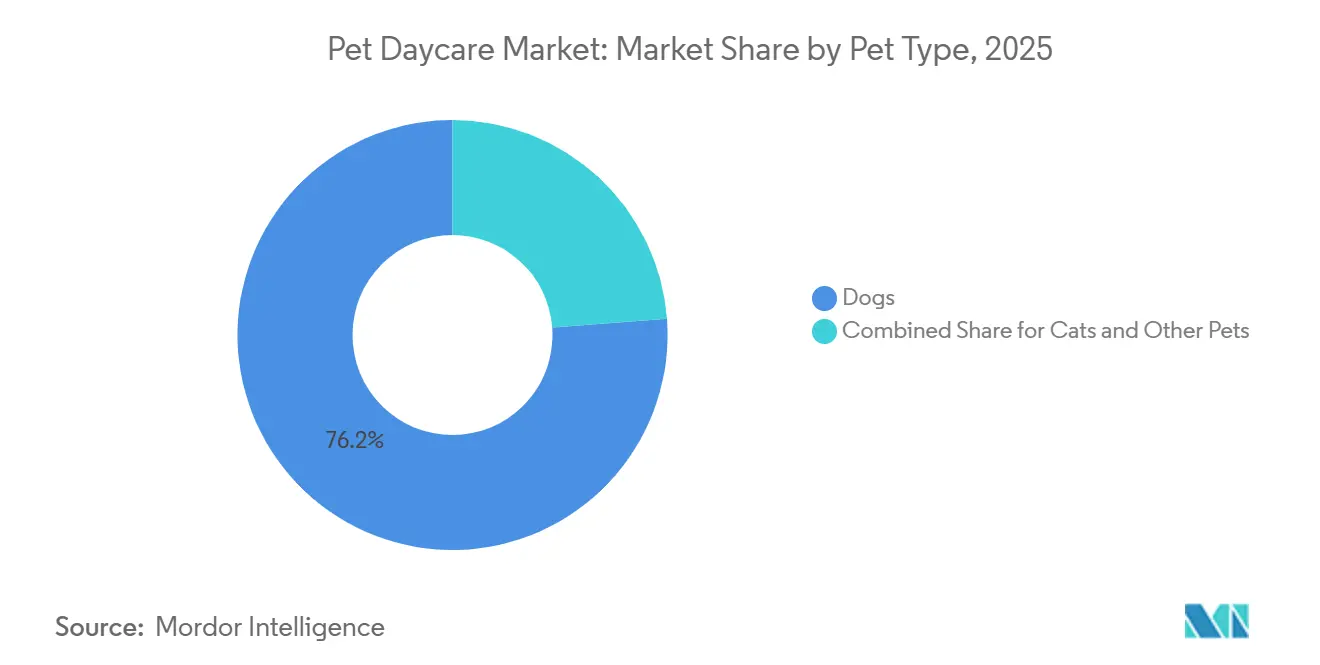

- By pet type, dogs held the largest 76.2% of pet daycare market share in 2025, while cat daycare is projected to expand at the fastest 9.1% CAGR through 2026-2031.

- By service type, day boarding (Full-Day) accounted for the largest 53.9% share of the pet daycare market size in 2025, while enrichment and training add-ons are projected to grow at the fastest 7.9% CAGR through 2026-2031.

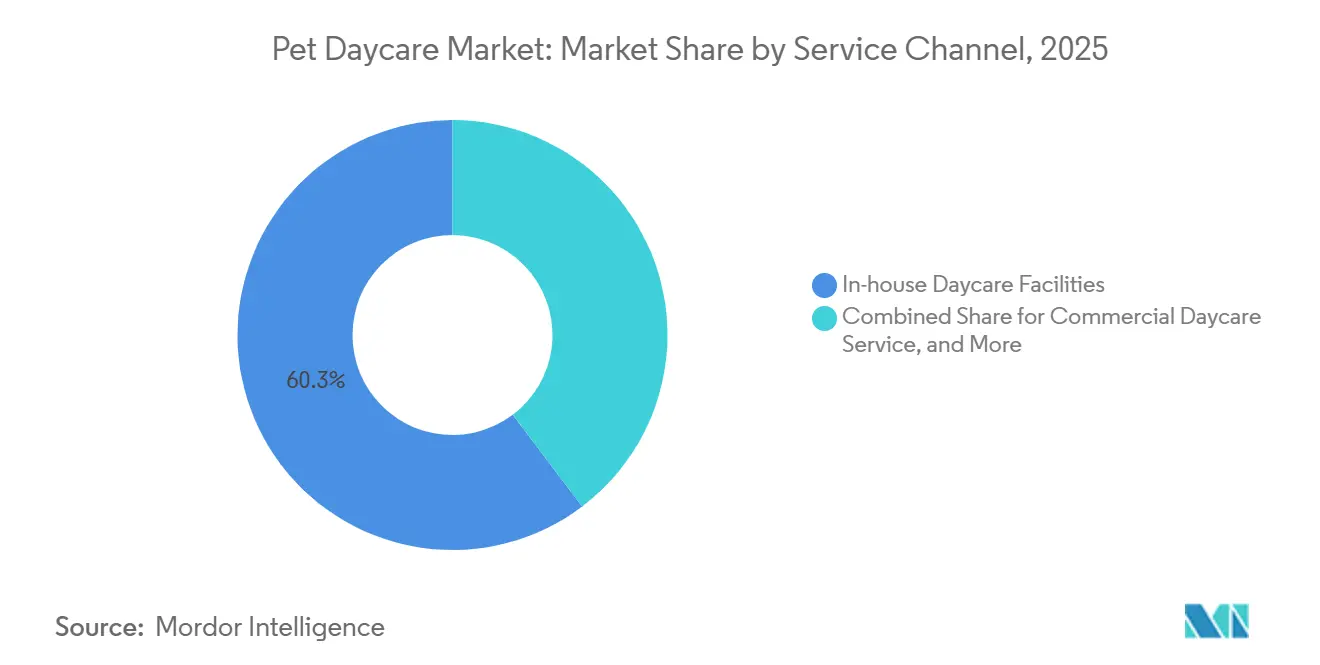

- By service channel, in-house daycare facilities held the largest 60.3% of pet daycare market share in 2025, while digital marketplaces are projected to grow at a 12.8% CAGR through 2026-2031.

- By pricing model, pay-as-you-go held the largest 71.1% of pet daycare market share in 2025, while subscription and membership pricing are projected to grow at the fastest 14.3% CAGR through 2026-2031.

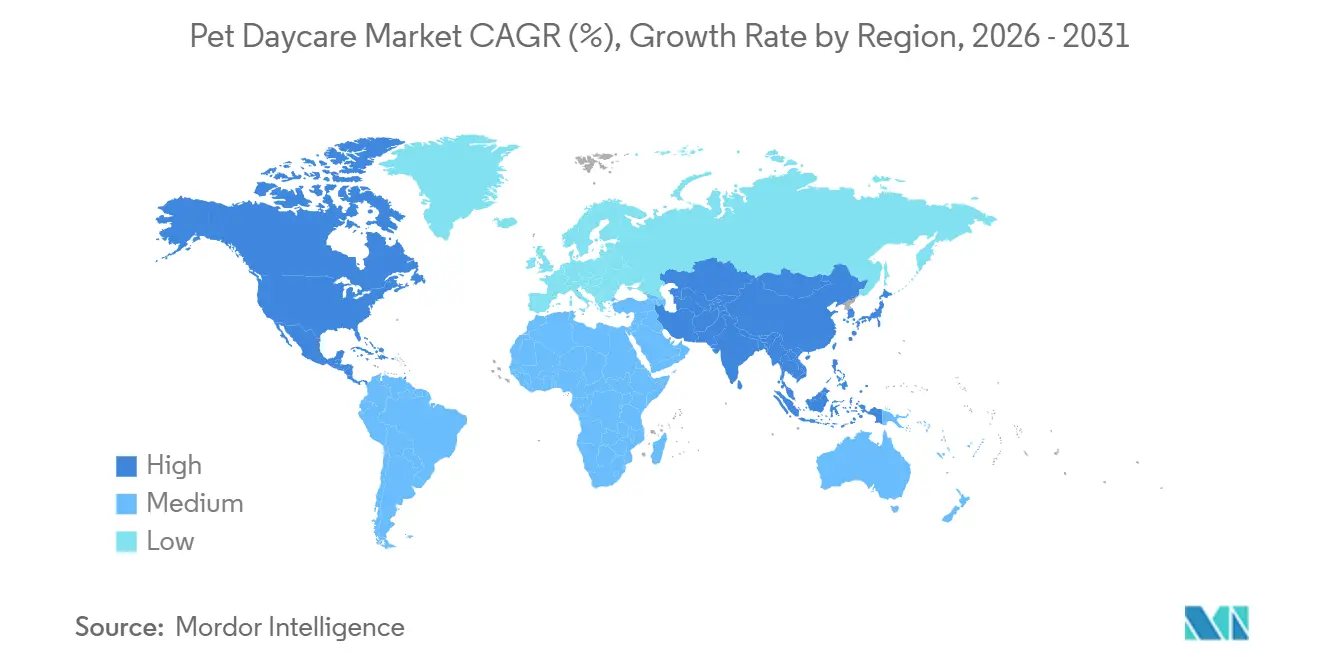

- By geography, North America accounted for 37.6% share of the pet daycare market size in 2025, while Asia-Pacific is projected to expand at the fastest 10.3% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pet Daycare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet humanization and premium care spend | +2.0% | Global, with the strongest relevance in North America, the United Kingdom, Germany, Japan, and China | Long term (≥ 4 years) |

| Dual-income households and return-to-office time pressure | +1.3% | North America and Western Europe, with secondary relevance in Australia, Japan, and South Korea | Medium term (2-4 years) |

| Digital booking and membership adoption | +0.9% | North America, Asia-Pacific, and Western Europe | Medium term (2-4 years) |

| Franchise-led formalization of fragmented supply | +0.8% | North America, with early-stage expansion relevance in Australia, the United Arab Emirates, and the United Kingdom | Long term (≥ 4 years) |

| Employer-sponsored pet care benefits | +0.5% | Global, with the strongest near-term traction in North America, the United Kingdom, Germany, China, and Japan | Medium term (2-4 years) |

| Safety-tech and compliance software scaling trust | +0.3% | Primarily the United States, with early adoption in Canada and the United Kingdom | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rising Pet Humanization and Premium Care Spend

The pet daycare market is experiencing growth due to the increasing tendency of pet owners to treat their pets as family members. This has led to rising demand for supervised care, enrichment activities, and premium service offerings. As owners prioritize animal wellbeing, socialization, and personalized attention, daycare services are expanding beyond basic supervision to provide comprehensive care solutions. This trend is particularly notable in Germany, one of the largest pet care markets in Europe. According to the Zentralverband Zoologischer Fachbetriebe Deutschlands (ZZF) and Industrieverband Heimtierbedarf (IVH), 33.9 million pets resided in German households in 2024. The substantial pet population is driving higher spending on quality care services and increasing demand for pet daycare facilities.

Dual-Income Households and Return-to-Office Time Pressure

The pet daycare market is also benefiting from work schedules that leave pets home alone for longer periods of the day. Spot Pet Insurance found in 2026 that 15% of surveyed United States pet parents had declined promotions or job offers that required 5 in-office days due to pet care needs, showing how care logistics are now tied to employment decisions. Airvet reported in 2025 that 70% of its workforce identifies as a pet parent, indicating a large addressable pool for recurring daycare use[1]Source: Airvet, “2025 Survey: The Impact of Pet Benefits on Your Workforce,” September 2025, airvet.com.. In San Francisco, premium facilities reported full occupancy and waitlists in 2026, which illustrates how schedule-driven urban demand is translating into capacity pressure and pricing power. This pattern supports repeated weekday use and makes the pet daycare market less dependent on one-off travel-related bookings.

Digital Booking and Membership Adoption

Digital tools are enhancing operational efficiency and customer engagement in the pet daycare market by streamlining processes such as booking, monitoring, and membership management. As service providers expand their digital capabilities, pet owners benefit from increased visibility into their pets’ activities and health, while daycare operators improve customer retention through recurring service plans. For instance, in January 2026, Dogtopia reported that its DASH by Dogtopia monitor and app integration offered pet owners real-time updates on steps, distance, and rest, fostering engagement beyond daycare visits. This trend toward connected services is also driving membership adoption, with Skiptown reporting a 68% year-over-year increase in bundle sales during the first quarter of 2026. Additionally, platforms like Rover are expanding their digital ecosystems by incorporating complementary services, strengthening long-term customer relationships, and contributing to growth in the pet daycare market.

Safety-Tech and Compliance Software Scaling Trust

Trust is central to the pet daycare market, and operators are investing in systems that make care quality more visible and easier to verify. Massachusetts enacted Ollie’s Law in 2024, which introduced mandatory injury reporting, caregiver-to-animal ratios, and capacity limits for dog daycare settings, and that move signals tighter oversight across the United States[2]Source: Stateline, “Lack of Doggie Day Care Rules Leaves Many Pet Owners in the Dark,” stateline.org . When reporting rules tighten, operators with auditable workflows, digital records, and standardized staff procedures are better positioned to win owner confidence. Dogtopia’s real-time wellness data and app visibility show how technology is moving from a brand differentiator to a practical trust tool in daily operations. This is helping the pet daycare market attract customers who want proof of care quality before they accept premium pricing.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High urban real estate and labor costs | -1.5% | North America and Western Europe, with the sharpest pressure in dense United States metros, Canada, the United Kingdom, Germany, and Australia | Long term (≥ 4 years) |

| Fragmented licensing and welfare compliance | -0.9% | United States, the United Kingdom, Germany, and Australia, with emerging complexity in China | Medium term (2-4 years) |

| Insurance inflation and biosecurity risk | -0.7% | Global, with highest severity in North America, the United Kingdom, Germany, and Australia | Long term (≥ 4 years) |

| Caregiver burnout and schedule instability | -0.6% | North America, with meaningful exposure in Canada, the United Kingdom, and Germany | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High Urban Real Estate and Labor Costs

The pet daycare market experiences significant operational challenges in densely populated urban areas, where both staffing and facility costs are elevated. In major cities, operators are required to provide sufficient space, employ trained staff, and offer enrichment programs, all while adhering to increasingly strict welfare and safety regulations. This issue is particularly pronounced in the United Kingdom, one of the largest pet care markets in Europe. In April 2025, the National Living Wage in the UK rose by 6.7% to GBP 12.21 (USD 16.20) per hour, according to the United Kingdom government, leading to higher labor costs for service-based businesses that depend on constant staff supervision[3]Source: United Kingdom Government, “National Living Wage and National Minimum Wage Rates from April 2025,” gov.uk.. This dynamic may hinder expansion in high-cost urban areas and drive growth in more affordable secondary locations.

Insurance Inflation and Biosecurity Risk

Biosecurity events are recurring constraints because the pet daycare market relies on group settings where illness concerns can quickly affect attendance and operating standards. Concerns about canine infectious respiratory disease in 2024 and 2025 increased attention to screening, vaccination checks, sanitation, and isolation protocol. These steps are necessary, but they also add cost and raise the risk of temporary disruption when owners become cautious about group-care environments. Insurance providers are responding to those risks with tighter underwriting and greater scrutiny of safety practices, favoring more disciplined operators. This restraint is unlikely to reverse demand for the pet daycare market, but it does make operating resilience and documented care protocols more important than before.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Dogs Hold the Largest Base While Cats Show the Fastest Expansion

Dogs accounted for 76.2% of revenue in the pet daycare market in 2025, which makes them the largest pet category by a wide margin. That position reflects the fact that dogs are the most established users of supervised daytime care, especially when owners need a full workday solution. The dog segment also aligns well with structured exercise, social play, and behavior management programs that organized facilities can deliver at scale. In the pet daycare industry, this makes dogs the clearest fit for full-day attendance and recurring use. The segment remains central to franchise economics because capacity planning, staffing models, and enrichment packages are usually built around canine care patterns.

Cat daycare is the fastest pet segment, with a projected 9.1% CAGR in 2026-2031. The American Pet Products Association noted in 2025 that cat owners are engaging more deeply with training, celebrations, outdoor gear, and enrichment routines, which suggests a more active care mindset than in the past. That behavioral shift is expanding the addressable market for feline-specific daycare formats in urban settings where owners want monitored care rather than leaving their cats unattended for long periods. Other pet types remain niche in the pet daycare market, but they are part of the broader premium care trend in markets where companion animal ownership is diversifying. Over time, operators who design separate spaces, calmer handling protocols, and species-specific enrichment should be better placed to capture this faster-growth mix.

By Service Type: Full-Day Boarding is the Largest Format While Enrichment Add-Ons Grow Fastest

Day boarding (Full-Day) accounted for 53.9% of the pet daycare market share in 2025, confirming that full-day coverage remains the core use case. The format suits urban households that need reliable drop-off and pickup on office days. It also supports higher average daily revenue by giving operators more time to layer feeding, rest, play, and premium monitoring into a single visit. The strongest operators use this format to anchor occupancy and build customer habits around weekday attendance. Half-Day Daycare remains relevant in hybrid work settings, but it does not carry the same revenue depth as full-day placement.

Enrichment and training add-ons are the fastest service segment, with a projected 7.9% CAGR in 2026-2031. Dogtopia’s 2026 rollout of the DASH activity monitor shows how providers are turning exercise and behavioral tracking into a visible value layer rather than a hidden back-end task. This is important because owners increasingly want proof that daycare is improving wellness, not only solving a time-management problem. Overnight boarding and sitting still matter during travel peaks, but enrichment is where a larger share of future pricing power is forming in the pet daycare market. Providers that combine full-day care with measurable enrichment are likely to keep customers longer and lift spend per visit.

By Service Channel: In-House Facilities Stay Largest While Digital Marketplaces Expand Fastest

In-house daycare facilities accounted for 60.3% of the pet daycare market share in 2025, maintaining their position as the largest channel. This channel benefits from the trust value of inspected spaces, visible staff supervision, and standardized vaccination screening. It also suits customers who want a single provider to manage recurring daytime care, grooming, training, or boarding at a fixed location. In the pet daycare industry, physical facilities remain the benchmark for quality and safety. Commercial daycare services and mobile formats are growing around convenience needs, but they remain smaller than organized facility-based care.

Digital marketplaces are the fastest service channel, with a projected 12.8% CAGR in 2026-2031. Digital platforms are widening from matchmaking into adjacent care services that can deepen customer frequency. That expansion matters because it makes digital channels more useful even when owners are not booking overnight stays or standard sitting visits. The main challenge for marketplaces remains trust, but stronger credentialing, service breadth, and easier digital workflows are narrowing that gap. As these features improve, the pet daycare market is likely to see a more balanced split between physical scale and platform convenience.

By Pricing Model: Pay-as-You-Go Remains Largest While Subscriptions Change Revenue Quality Fastest

Pay-As-You-Go held 71.1% of the pet daycare market share in 2025, making it the largest pricing model. This reflects the fact that many owners still trial a provider transaction by transaction before moving into a recurring plan. The model also fits households with changing office schedules, seasonal travel, or irregular care needs. For operators, however, this format keeps demand visibility lower and makes weekly revenue more sensitive to schedule changes. That is why many providers now run flexible pay-per-visit options alongside stronger recurring bundles.

Subscription and membership pricing is the fastest pricing format, with a projected 14.3% CAGR in 2026-2031. Membership-based daycare programs are enabling operators to establish stronger and more predictable customer relationships in the pet daycare market. These recurring plans streamline access to services, promote consistent attendance, and minimize the challenges of repeated booking processes. Consequently, providers can enhance customer retention while achieving more stable revenue streams. Additionally, membership models allow operators to combine daycare, grooming, training, and other value-added services, thereby increasing overall customer engagement. As pet owners prioritize convenience and continuity of care, recurring service plans are emerging as a key strategy for fostering long-term loyalty and supporting sustainable business growth in the pet daycare market.

Geography Analysis

North America accounted for 37.6% of revenue in 2025, making it the largest regional market. The United States remains the core engine because organized franchises are more established and consumer familiarity with paid daycare is stronger than in most other regions. San Francisco facilities reported waitlists and premium daily pricing in 2026, indicating that urban demand can support higher-priced service models. Camp Bow Wow and Dogtopia continue to expand their network footprints, which helps normalize organized pet care for a wider owner base across the region. Tighter state-level attention to safety and reporting is also creating a clearer divide between compliant multi-site operators and smaller informal providers in the pet daycare market.

Asia-Pacific is the fastest regional block in the pet daycare market, with a projected 10.3% CAGR in 2026-2031. Growth in this region is tied to urbanization, rising pet ownership, and first-generation premium spending in large consumer markets such as China and India. The region is still earlier in organized supply development than North America, which gives chains, digital platforms, and premium independents more room to shape category habits. Japan and South Korea are important for premium and technology-led care formats, while Australia remains relevant for formal welfare standards and professional service uptake. This combination of newer demand and evolving formal supply makes Asia-Pacific the fastest-growing market for pet daycare over 2026-2031.

Europe is projected to grow, benefiting from high welfare awareness, strong urban pet ownership, and greater acceptance of app-based service models. South America is projected to expand, with Brazil standing out as the largest regional demand center for organized pet services. The Middle East is p to record rapid growth concentrated in the United Arab Emirates and Saudi Arabia, where premium urban pet care is formalizing. Africa is anticipated to transform from a low-penetration base to rapid growth, with South Africa remaining the most visible organized development hub. Outside North America, the pet daycare market is therefore growing through a mix of premium urban niches, digital adoption, and the gradual formalization of supply, rather than a single global pattern.

Competitive Landscape

The pet daycare market remains highly fragmented, with the top 5 operators accounting for descent share in 2025. PetSmart LLC was the largest single provider, followed by Rover, Camp Bow Wow, Dogtopia Enterprises LLC, and Destination Pet LLC. This structure keeps pricing and service quality dispersed across the pet daycare market rather than concentrated in a few brands. In practice, owners often choose providers on visible trust signals such as webcams, vaccination checks, trained staff, and structured activity rather than brand scale alone. That makes local execution and reputation especially important, even when national chains are present.

Companies are employing various strategies to expand their scale and enhance market presence. In January 2024, Pet Resort Hospitality Group completed five brand acquisitions, reflecting sustained investor interest in consolidating pet care businesses. Similarly, Digs Dog Care established a national platform by acquiring 17 pet resorts, underscoring the growing role of multi-location operators in the industry. Franchise expansion continues to be a significant growth strategy, with Dogtopia entering multi-unit development agreements to accelerate its market reach. Additionally, investments in digital infrastructure and operational technology are gaining importance, supporting customer engagement, ensuring service consistency, and enabling scalable growth within the pet daycare market.

Growth opportunities in the pet daycare market are most evident in secondary cities, office-linked pet care formats, and premium services designed to meet specific pet needs. Competitive dynamics are increasingly influenced by the expansion of complementary pet services, the rising use of digital platforms, and the adoption of membership-based models that enhance convenience and customer retention. Market participants are optimizing their business formats to improve scalability, operational efficiency, and market reach. As the industry progresses, competition is increasingly centered on service differentiation, technology integration, customer experience, and the development of long-term relationships through specialized and value-added care services.

Pet Daycare Industry Leaders

PetSmart LLC

Rover, Inc.

Camp Bow Wow

Dogtopia Enterprises LLC

Destination Pet LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Digs Dog Care expanded into a national pet care platform by acquiring 17 pet resorts across the United States. This acquisition created a multi-location network offering daycare, boarding, grooming, and veterinary services. The initiative enhanced the company's presence in the pet care market.

- March 2026: Rover, Inc. formally launched dog training across the United States following an October 2024 pilot that onboarded 1,600 credentialed trainers and facilitated over 6,000 sessions. The launch extends Rover's addressable service scope beyond overnight care and sitting into behavioral services.

- March 2026: Camp Bow Wow spotlighted its reduced-investment franchise model at the Multi-Unit Franchising Conference 2026 in Las Vegas, targeting experienced multi-unit operators for strategic portfolio expansion in high-demand markets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pet daycare market as the yearly revenue earned by licensed facilities that supervise companion animals during daytime or overnight stays, provide structured play, feeding, and safety monitoring, and charge a service-only fee. According to ���ϲ�����, bookings generated through digital marketplaces are included when the actual care occurs at an accredited center.

Scope Exclusion: In-home pet sitting performed by individuals and pure-play grooming visits fall outside the present scope.

Segmentation Overview

- By Pet Type

- Dogs

- Cats

- Other Pet Types

- By Service Type

- Day Boarding (Full-Day)

- Half-Day Daycare

- Overnight Boarding

- Pet Sitting

- Enrichment and Training Add-ons

- By Service Channel

- In-house Daycare Facilities

- Commercial Daycare Services

- Mobile and Pop-up Daycare

- Digital Marketplace

- By Pricing Model

- Subscription and Membership

- Pay-As-You-Go

- Corporate-Sponsored

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts spoke with daycare owners, franchisors, insurance underwriters, and animal-behavior consultants across North America, Europe, and Asia. They then fielded an online survey of pet parents to verify average spend, occupancy, and seasonal swings. These insights refined variable choices and stress-tested forecast inflection points.

Desk Research

We reviewed public sources such as United States Bureau of Labor Statistics pet-service payroll tables, Eurostat business statistics, and HS-2309 customs flows, along with releases from the American Pet Products Association, Pet Industry Federation, and Japan Pet Food Association. Company 10-Ks, franchise disclosure documents, and lease filings clarified capacity and rate cards, while news wires mapped new center openings. Subscription resources, D&B Hoovers for chain financials and Dow Jones Factiva for deal flow, supplemented the open data. The references cited are illustrative; many additional open and paid materials informed data collection and validation.

Market-Sizing & Forecasting

Our model starts with a top-down rebuild of spend: pet population multiplied by service penetration multiplied by average price, followed by payroll-to-revenue cross-checks. Bottom-up outlet roll-ups, franchise counts multiplied by sampled ticket size, serve as an independent yardstick before reconciliation. Key inputs include live pet population growth, dual-income household share, median service price shifts, urban kennel density, and local licensing requirements. A multivariate regression on these drivers projects 2026-2030 figures, with scenario analysis layering macro shocks.

Data Validation & Update Cycle

Outputs clear automated variance screens, senior analyst review, and peer audit before release. We refresh findings annually and issue interim updates when policy or disease events materially alter pet mobility patterns.

Why Mordor's Pet Daycare Baseline Commands Reliability

Published estimates often diverge because firms vary service scope, currency treatment, and refresh cadence.

Mordor's disciplined inclusions, annual update, and two-pass validation deliver a balanced, traceable baseline that decision-makers can rely on.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.66 B (2025) | ���ϲ����� | - |

| USD 4.74 B (2025) | Global Consultancy A | Omits mobile bookings; relies on one expert panel for base year |

| USD 2.43 B (2024) | Industry Association B | Scales regional sample globally; static currency conversion |

| USD 3.50 B (2023) | Research Journal C | Historic extrapolation; no operator roll-ups |

Differences narrow once scope and assumptions are aligned, and Mordor's figure sits mid-range, reflecting transparent variables and repeatable steps that clients can audit with limited effort.

Key Questions Answered in the Report

What is the current outlook for pet daycare spending?

The pet daycare market size is valued at USD 5.02 billion in 2026.

Which region generates the most revenue today?

North America is the largest regional contributor, accounting for 37.6% of 2025 revenue, supported by mature franchise supply and strong consumer familiarity with organized care.

Which geography is expanding the fastest through 2031?

Asia-Pacific is the fastest-growing regional market, with a projected 10.3% CAGR in 2026-2031, as urban pet ownership and premium care spending rise.

Which service format is most important for providers?

Day Boarding (Full-Day) is the largest service type, with a 53.9% share in 2025, while Enrichment and Training Add-ons are the fastest-growing, with a 7.9% CAGR in 2026-2031.

How are digital platforms changing revenue models?

Digital Marketplaces are projected to grow at a 12.8% CAGR in 2026-2031, and subscription pricing is rising even faster at 14.3%, suggesting stronger recurring revenue models.

Page last updated on: