Microphone Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.96 Billion |

| Market Size (2031) | USD 3.85 Billion |

| Growth Rate (2026 - 2031) | 5.40% CAGR |

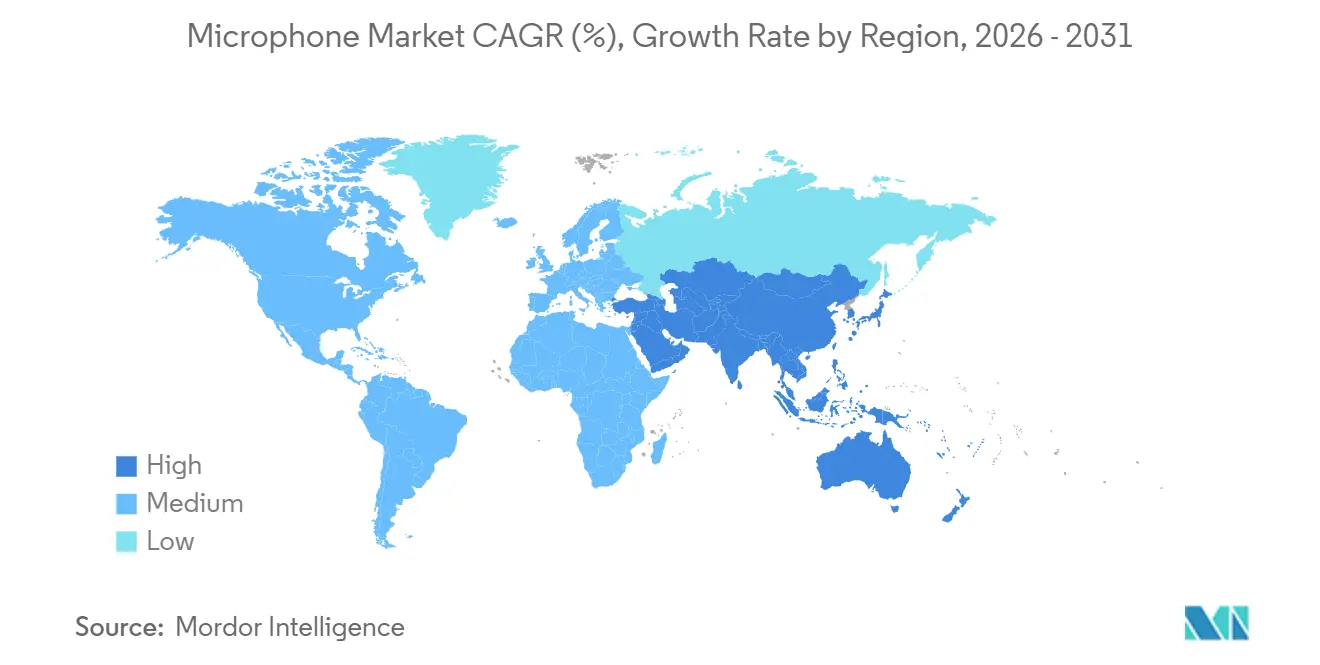

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Microphone Market Analysis by ���ϲ�����

The Microphone market size is projected to expand from USD 2.52 billion in 2025 and USD 2.96 billion in 2026 to USD 3.85 billion by 2031, registering a 5.4% CAGR between 2026 and 2031. Shipments are shifting rapidly from legacy electret condenser capsules toward compact digital MEMS arrays as edge-AI voice processing, automotive electrification and enterprise hybrid-work infrastructure converge. Wireless configurations already dominate because regulators continue to re-farm sub-1 GHz spectrum, while the proliferation of true wireless earbuds hastens the migration to Bluetooth Low Energy and other 2.4 GHz protocols. Asia-Pacific suppliers leverage vertical integration and government incentives to hold cost advantages in MEMS fabrication, whereas Europe and North America emphasize compliance and premium audio performance. Consolidation continues as component makers bundle microphones with DSP, neural processors and amplifiers to capture more value per socket.

Key Report Takeaways

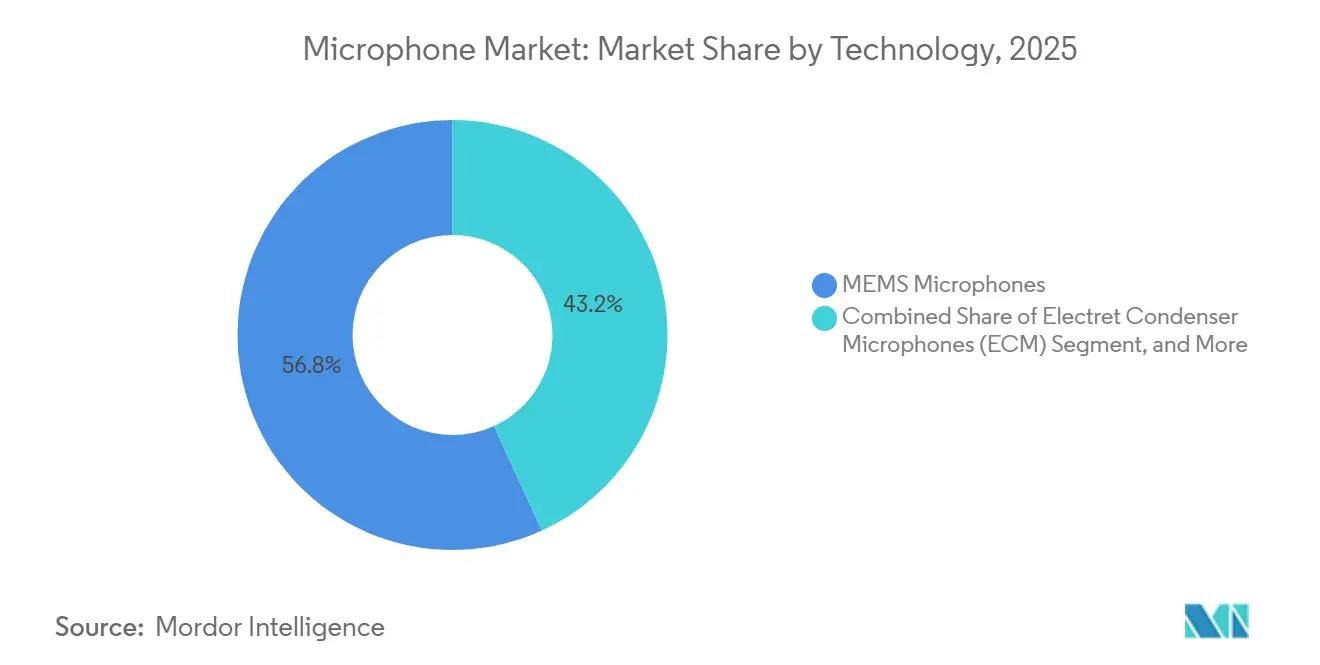

- By technology, MEMS microphones captured 56.81% of the Microphone market share in 2025 and are forecast to grow at a 5.88% CAGR through 2031.

- By product type, array and beam-forming modules are advancing at a 6.02% CAGR, the fastest in the segment hierarchy.

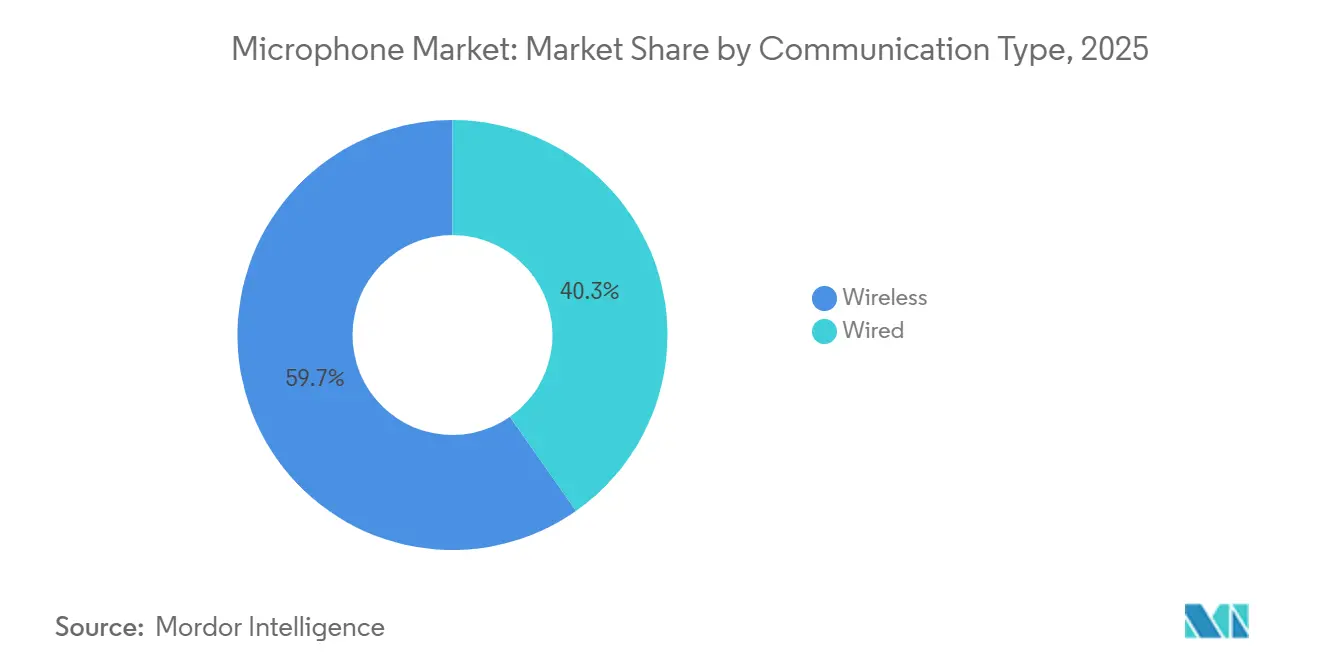

- By communication type, wireless systems accounted for 59.74% of the Microphone market size in 2025 and are projected to expand at 5.61% CAGR over 2026-2031.

- By end-user vertical, healthcare and medical devices are poised to rise at a 6.73% CAGR, outpacing all other industries.

- By geography, the Middle East region in the microphone market is forecast to post a 6.11% CAGR through 2031, the highest regional growth rate.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Microphone Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of MEMS microphones in true-wireless earbuds across Asia | +1.2% | Asia-Pacific core, spillover to North America and Europe | Medium term (2-4 years) |

| Automotive OEM shift to in-cabin voice UX for EV platforms (Europe and North America) | +0.9% | Europe and North America, early adoption in China | Long term (≥4 years) |

| Rapid adoption of AI-enabled beam-forming arrays in enterprise UC equipment | +0.8% | Global, concentrated in North America and Europe | Short term (≤2 years) |

| Content-creator economy fueling premium handheld and USB mics (North America) | +0.5% | North America, Western Europe | Short term (≤2 years) |

| Government mandates for wireless spectrum re-farming driving digital migration | +0.6% | Global, regulatory pressure highest in North America and Europe | Medium term (2-4 years) |

| Surge in health-wearables deploying acoustic biosensing microphones | +1.0% | Global, led by North America and Asia-Pacific | Long term (≥4 years) |

| Source: ���ϲ����� | |||

Proliferation of MEMS Microphones in True-Wireless Earbuds Across Asia

True wireless earbuds remained the primary driver of shipments in the Microphone market in 2025, as Asia-Pacific brands outproduced competitors elsewhere. Digital MEMS capsules, small enough to fit 3 mm × 4 mm slots, now support multi-mic active noise cancellation and far-field voice pickup while drawing minimal power. Syntiant’s 2024 acquisition of Knowles’ consumer MEMS unit aligns neural processors with sensors, reducing latency for always-on voice wake functions.[1]Knowles Corporation, “Knowles Completes Sale of Consumer MEMS Microphone Business,” KNOWLES.COM Chinese suppliers AAC Technologies and Goertek expanded 200 mm wafer capacity to serve domestic smartphone OEMs, further amplifying supply advantages. The shift to digital interfaces such as I²S simplifies PCB routing and reduces EMI, which matters more as Bluetooth 5.3 and LE Audio introduce tighter RF coexistence requirements.

Surge in Health-Wearables Deploying Acoustic Biosensing Microphones

Healthcare wearables are emerging as a major demand node because MEMS microphones enable continuous, non-invasive capture of cardio-respiratory signals with clinical-grade fidelity. A 2025 Scientific Reports study reported 93.21% accuracy in classifying lung sounds using MEMS sensors, validating the viability of remote auscultation. Device makers now pair sensors with on-device neural models that spot cough events and respiratory distress in real time, supporting telemedicine workflows. Growth is strongest in North America, where reimbursement codes for remote patient monitoring already exist, and in Asia-Pacific, where aging populations drive preventive-care spending. Suppliers that integrate acoustic sensors with low-power edge-AI increasingly win design slots because hospitals demand HIPAA-compliant, always-on endpoints that never upload raw voice data to the cloud.

Automotive OEM Shift to In-Cabin Voice UX for EV Platforms

Electric-vehicle cabins are quieter than those of internal-combustion models, enabling far-field voice assistants to operate reliably. BMW’s Alexa+ system, launched in 2026, employs distributed MEMS arrays along the headliner and pillars, delivering sub-300 ms wake-word response for navigation and climate commands. Mercedes-Benz has already deployed multi-zone voice control in more than 3 million vehicles. European and North American safety regulators endorse voice-over-touchscreens to reduce driver distraction, compelling OEMs to specify digital MEMS capsules with integrated DSPs for beamforming and echo cancellation. Tier-one suppliers bundle microphones with cameras and radar to create multimodal driver-monitoring suites, positioning themselves for Euro NCAP’s forthcoming interior-sensing requirements.

Rapid Adoption of AI-Enabled Beam-Forming Arrays in Enterprise UC Equipment

Hybrid-work policies sustain demand for ceiling arrays that remove table clutter and intelligently track speakers. Cisco’s Ceiling Microphone Pro features a 64-element array that forms eight adaptive beams, covering classrooms and boardrooms without fixed pickup zones.[2]Cisco Systems, “Cisco Ceiling Microphone Pro,” CISCO.COM Yamaha’s ADECIA firmware update in 2025 added AI De-Noiser acceleration and raised capacity to 64 wireless tabletop units per processor, addressing enterprise-scale needs. Integrators prefer these solutions because IEEE 802.1X authentication and SNMP monitoring slot easily into corporate IT routines. The result is shorter installation cycles and reduced reliance on standalone DSP hardware, an advantage in markets facing skilled-labor shortages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RF congestion and interference risk in sub-1 GHz bands for wireless mics | -0.7% | North America and Europe, regulatory pressure on analog systems | Medium term (2-4 years) |

| BOM-cost inflation from silicon substrate shortages (MEMS fabs) | -0.6% | Global, acute in Asia-Pacific MEMS supply chain | Short term (≤2 years) |

| Counterfeit after-market capsules diluting brand value in Asia-Pacific | -0.4% | Asia-Pacific, concentrated in China and Southeast Asia | Long term (≥4 years) |

| Stringent EU WEEE/RoHS recycling targets raising compliance costs | -0.5% | Europe, spillover to exporters targeting EU markets | Long term (≥4 years) |

| Source: ���ϲ����� | |||

RF Congestion and Interference Risk in Sub-1 GHz Bands for Wireless Mics

As the FCC auctions 600 MHz blocks to mobile carriers, analog wireless microphones lose clear spectrum, forcing users into the crowded 2.4 GHz ISM band. Digital systems offer encryption and eliminate companding artifacts but face packet-loss spikes when Wi-Fi, Bluetooth and Zigbee traffic peaks.[3]AKG Acoustics Engineering Team, “Comparing Digital and Analog Wireless Mic Systems,” AKG.COM The added complexity of channel scanning and firmware updates slows adoption among budget-constrained schools and theaters, holding back revenue growth in specific professional-audio niches within the Microphone market.

BOM-Cost Inflation from Silicon Substrate Shortages (MEMS Fabs)

Tight 150 mm and 200 mm wafer supply raised MEMS microphone input costs by double-digit percentages between 2024 and 2025. Knowles reported a 9.9% year-over-year revenue dip in Q3 2024, citing substrate shortages and customer inventory corrections. Some OEMs switched to China-based foundries backed by state subsidies, but geopolitical export-control risks add long-term uncertainty. Fabless designers without captive capacity endure the highest margin squeeze, slowing new-product cycles and tempering near-term Microphone market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Digital MEMS Dominate Consumer Electronics Integration

MEMS microphones held a 56.81% Microphone market share in 2025, and the segment is on track for a 5.88% CAGR through 2031. Digital variants displace analog MEMS because on-package A-to-D conversion eliminates EMI issues and reduces PCB complexity. Cirrus Logic began sampling an ultra-low-power voice-wake codec for AI-ready laptops in late 2025, signaling a fresh wave of demand for digital MEMS front ends. Electret condensers remain cost-effective for cost-sensitive applications, while dynamic capsules remain relevant for high-SPL applications like live sound. Ribbon microphones retain a boutique footprint in studio recording, valued for their figure-8 polar patterns. The Microphone market size attributable to MEMS is therefore expanding faster than the overall category as consumer electronics OEMs demand higher integration and lower power profiles.

Analog MEMS remain attractive for cabin-noise cancellation in automobiles and basic industrial monitoring, where simple analog chains suffice. Yet the ecosystem momentum behind I²S and SoundWire bus architectures ensures that digital MEMS will continue climbing the mix. Suppliers able to embed DSP or neural accelerators inside the microphone package differentiate on latency and power, critical for always-listening devices. Consequently, design wins now hinge on total module functionality rather than raw acoustic specifications, accelerating platform lock-in across smartphones, laptops and wearables.

By Product Type: Array Modules Lead Enterprise Conferencing Shift

Array and beam-forming modules recorded the fastest growth rate at 6.02% CAGR as enterprises swapped boundary microphones for ceiling arrays that streamline meeting spaces. Head-worn systems held 32.47% of shipments in 2025 because fitness instructors and broadcasters value mobility; however, their unit growth trails that of arrays. Freestanding USB mics such as Logitech’s Blue Sona cater to the creator economy that prizes plug-and-play gain boosts.

Dynamic handheld microphones remain staples for live vocals, supported by condenser variants on instruments and in studio situations. Gooseneck models still anchor podiums but face encroachment from wireless tabletop units that remove cable management headaches. The microphone market size for array modules is set to widen as AI software bundles automate beamforming, echo cancellation, and noise suppression, reducing commissioning time for IT departments and integrators.

By Communication Type: Wireless Gains Share Despite Spectrum Challenges

Wireless solutions represented 59.74% of the Microphone market size in 2025 and should climb at 5.61% CAGR through 2031. Bluetooth LE Audio, proprietary 2.4 GHz links, and digital UHF platforms replace analog UHF systems displaced by spectrum auctions. Fitness studios, classrooms, and corporate presenters prioritize mobility over the higher latency and battery maintenance burdens, driving uptake.

Wired XLR connections persist in studios and broadcast control rooms where deterministic latency and long-distance balanced lines remain essential. Manufacturers mitigate 2.4 GHz congestion by layering frequency hopping and adaptive modulation, though these features raise bill-of-materials costs. As a result, wireless growth is strongest in segments that can tolerate potential packet loss, while mission-critical users occasionally revert to cables, preserving a stable wired revenue core of the microphone market.

By End-User Vertical: Healthcare Emerges as Fastest-Growing Segment

Consumer electronics accounted for 41.82% of revenue in 2025, driven by smartphones and wearables that integrate multiple MEMS capsules per device. Healthcare applications-ranging from digital stethoscopes to respiratory patches-lead growth with a 6.73% CAGR as providers embrace tele-consultation workflows. Broadcasting and media outlets still invest in premium handheld and studio condensers to maintain signal quality for podcasts and live streams.

Corporate and institutional buyers adopt ceiling arrays and large-scale wireless systems to modernize hybrid-meeting suites. Live performance venues gradually refresh RF rigs as budgets recover post-pandemic. Automotive OEMs are moving to multi-mic arrays for voice assistants and interior noise control, a trend that is reinforcing MEMS penetration. Industrial and environmental monitoring remains a niche but is accelerating as rugged MEMS sensors gain IP-rated housings suitable for harsh environments. Together these shifts diversify the revenue base of the microphone market and insulate it from single-vertical volatility.

Geography Analysis

Asia-Pacific held 45.77% of global revenue in 2025, underpinned by China’s scale in MEMS wafer processing and module assembly. Local champions AAC Technologies and Goertek secure preferential supply for domestic smartphone giants, reinforcing regional dominance. Japan and South Korea focus on packaging innovation and high-SNR performance, while India and Southeast Asia attract new green-field plants that hedge geopolitical exposure.

North America ranked second, buoyed by enterprise spending on hybrid-work upgrades and a vibrant creator economy purchasing premium USB and XLR devices. Content platforms such as YouTube and Twitch incentivize high-quality audio capture, creating a steady pull for mid-range condenser microphones. Europe emphasizes WEEE and RoHS compliance, concentrating share among established brands that can shoulder recycling costs. EU rules also encourage modular designs that simplify end-of-life disassembly, subtly altering product roadmaps for global vendors.

The Middle East and Africa region, though small in absolute dollars, is forecast to post the fastest expansion at 6.11% CAGR, driven by Saudi Arabia and the United Arab Emirates deploying telemedicine and distance-learning infrastructure. South America’s growth is moderate as macroeconomic headwinds curb capital outlays in broadcast and live-event markets. Overall, regional variations in regulatory policy, supply-chain incentives and digital-transformation budgets shape localized opportunity pockets within the microphone market.

Competitive Landscape

The Microphone market is moderately fragmented. Traditional audio houses-Shure, Sennheiser, and Audio-Technica-defend premium dynamic and condenser segments, leaning on decades-old brand trust and global channel reach. MEMS-focused semiconductor vendors such as Infineon, STMicroelectronics, TDK-InvenSense, and Knowles compete on noise floor, package size, and power metrics.

Syntiant’s USD 150 million purchase of Knowles’ consumer MEMS line in 2024 encapsulates a trend toward vertically integrating sensors with neural inference silicon, enabling turnkey always-on voice designs that conserve battery life. Harman’s USD 350 million acquisition of Masimo’s audio assets in 2025 signals that automotive and professional-audio integrators want complete microphone-to-speaker stacks that include DSP software. DPA Microphones’ majority stake in Austrian Audio shows boutique studio brands consolidating to defend engineering depth and European manufacturing heritage.

Chinese incumbents AAC Technologies and Goertek leverage captive fabs and state incentives to offer cost-optimized MEMS modules, pressuring Western suppliers on high-volume consumer deals. Meanwhile, Cisco, Yamaha and Crestron differentiate enterprise arrays through software ecosystems and security integration, emphasizing manageability over raw acoustic specs. Suppliers that can deliver full-stack solutions-sensor, processor, algorithm and cloud hooks-capture higher average selling prices and tighten customer lock-in, positioning themselves favorably as the Microphone market transitions to AI-centric architectures.

Microphone Industry Leaders

Knowles Corporation

AAC Technologies Holdings

Sony Corporation

Shure Incorporated

Goertek Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Cisco released a firmware upgrade that adds spatial-audio export to its Ceiling Microphone Pro, enabling multichannel immersion for remote participants.

- July 2025: Yamaha introduced the YCM705 large-diaphragm condenser microphone for creators requiring studio-grade quality in home setups.

- May 2025: Harman, a Samsung unit, acquired Masimo’s audio division for USD 350 million, expanding its automotive and professional-audio component portfolio.

- May 2025: Yamaha rolled out ADECIA Firmware V3.0, boosting support to 64 RM-W wireless tabletop microphones per processor and adding AI De-Noiser hardware acceleration.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global microphone market as every stand-alone wired or wireless transducer, dynamic, condenser, electret, MEMS, ribbon, and beam-forming arrays sold as finished components or finished devices that convert acoustic energy into electrical signals for consumer, professional, automotive, and industrial uses.

Scope Exclusion: Integrated acoustic dies embedded inside chipsets, pure software voice-processing tools, and refurbished units lie outside our coverage.

Segmentation Overview

- By Technology

- MEMS Microphones

- Analog MEMS

- Digital MEMS

- Electret Condenser Microphones (ECM)

- Dynamic Microphones

- Ribbon Microphones

- MEMS Microphones

- By Product Type

- Handheld

- Head-worn

- Gooseneck

- Freestanding / USB

- Array and Beam-forming Modules

- By Communication Type

- Wired

- Wireless

- By End-user Vertical

- Broadcasting and Media

- Consumer Electronics

- Corporate and Institutional

- Live Performances and Events

- Automotive

- Healthcare and Medical Devices

- Industrial and Environmental

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed MEMS wafer fabs, touring sound rental managers, smartphone ODM buyers, and component distributors across Asia-Pacific, North America, and Europe. These conversations surfaced attach-rate shifts, typical selling prices, and regulatory pinch points, helping us close secondary gaps and ground final assumptions.

Desk Research

We mapped demand pools through public datasets such as UN Comtrade HS 8518 shipment codes, ITU handset statistics, JEITA audio hardware output, and OICA vehicle production registers, which let us anchor baseline volumes before overlaying price curves. Trade association papers from the Audio Engineering Society, US FCC equipment grant lists, and region-specific RF spectrum releases then shaped technology adoption rates, while company 10-Ks, investor decks, and news archived in Dow Jones Factiva provided channel and ASP color. To refine company share splits, we turned to D&B Hoovers and cross-checked reported revenues with patent family counts from Questel; this pairing clarifies how much value flows into emerging MEMS classes versus legacy capsules. The sources cited remain illustrative, and many additional documents informed our desk work.

Market-Sizing & Forecasting

A top-down model starts with host device outputs, smartphones, TWS earbuds, conferencing endpoints, and vehicles, and multiplies them by validated microphone attach rates, which are then cross-checked with sampled ASPs from supplier roll-ups for selective bottom-up sense checks. Key variables include smartphone refresh cycles, streaming creator counts, automotive voice UX penetration, RF spectrum releases, and silicon wafer pricing. Multivariate regression that links GDP, consumer electronics spend, and live event ticket revenue underpins forecasts, while scenario analysis stresses silicon supply shocks. Data gaps are bridged through region-weighted averages taken from primary interviews.

Data Validation & Update Cycle

Outputs pass a two-layer analyst review; any variance beyond threshold triggers re-checks against shipment databases and follow-up calls. Figures refresh annually, with interim updates when tariffs, spectrum rulings, or major technology pivots alter inputs.

Why Mordor's Microphone Market Baseline Deserves Confidence

Published estimates diverge because each firm draws different service boundaries, price bases, and refresh cycles.

By staying within a declared scope, applying device-level attach logic, and updating every year, ���ϲ����� delivers a balanced, transparent baseline that decision-makers can reproduce and trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.51 B | ���ϲ����� | - |

| USD 2.88 B | Global Consultancy A | Includes MEMS die revenue inside smartphones and fixes values to 2024 FX rates |

| USD 7.59 B | Research Firm B | Aggregates microphones with full audio peripherals and uses VAT-inclusive retail sales |

| USD 4.46 B | Industry Analyst C | Applies steep ASP erosion assumption and three-year refresh cadence |

Published estimates diverge because each firm draws different service boundaries, price bases, and refresh cycles.

By staying within a declared scope, applying device-level attach logic, and updating every year, ���ϲ����� delivers a balanced, transparent baseline that decision-makers can reproduce and trust.

Key Questions Answered in the Report

How large will the Microphone market be by 2031?

Forecasts indicate it will reach USD 3.85 billion by 2031 at a 5.4% CAGR from 2026 to 2031.

Which technology leads current revenue?

MEMS microphones held 56.81% of Microphone market share in 2025 and remain the growth engine through 2031.

Why are array microphones growing so quickly?

Enterprise hybrid-work investments favor ceiling arrays that track multiple speakers and integrate AI beamforming, driving a 6.02% CAGR for this product type.

What vertical shows the fastest demand rise?

Healthcare and medical devices post a 6.73% CAGR because acoustic biosensing enables remote respiratory and cardiac monitoring.

Which region is expanding the quickest?

The Middle East and Africa Microphone market is projected to grow at 6.11% CAGR thanks to telemedicine and digital-government programs.

How are suppliers responding to spectrum re-allocation?

Vendors migrate from analog UHF to encrypted 2.4 GHz digital links and add frequency-hopping algorithms to mitigate congestion issues.

Page last updated on: