Loudspeaker Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

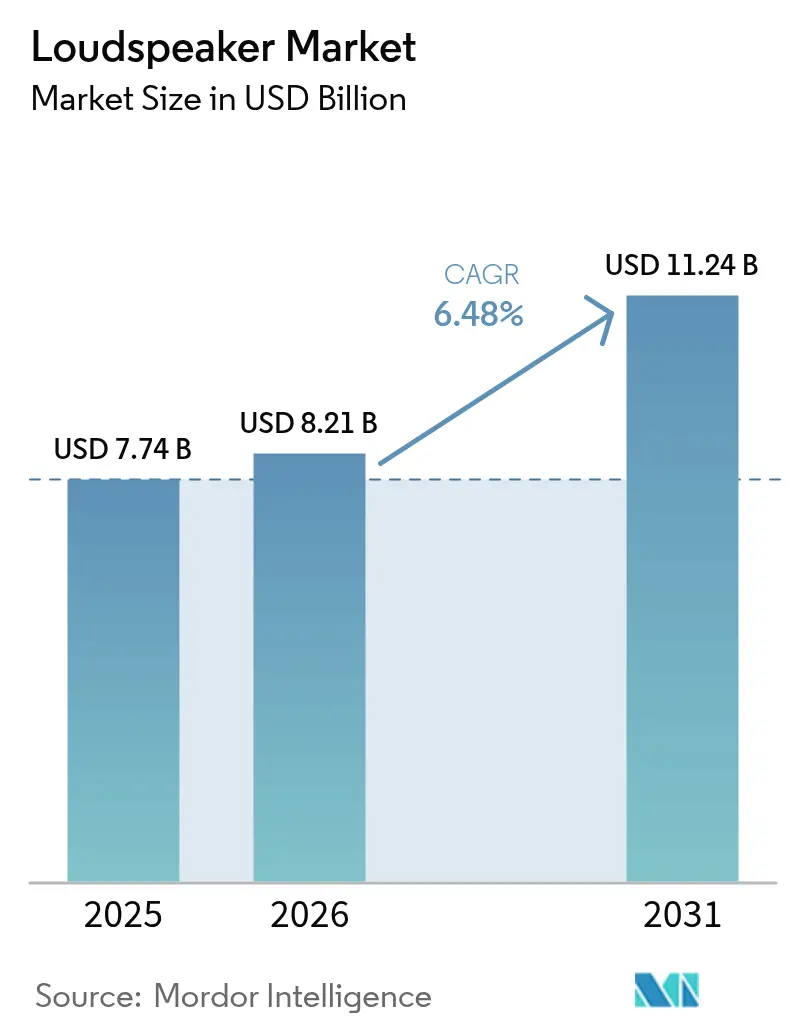

| Market Size (2026) | USD 8.21 Billion |

| Market Size (2031) | USD 11.24 Billion |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

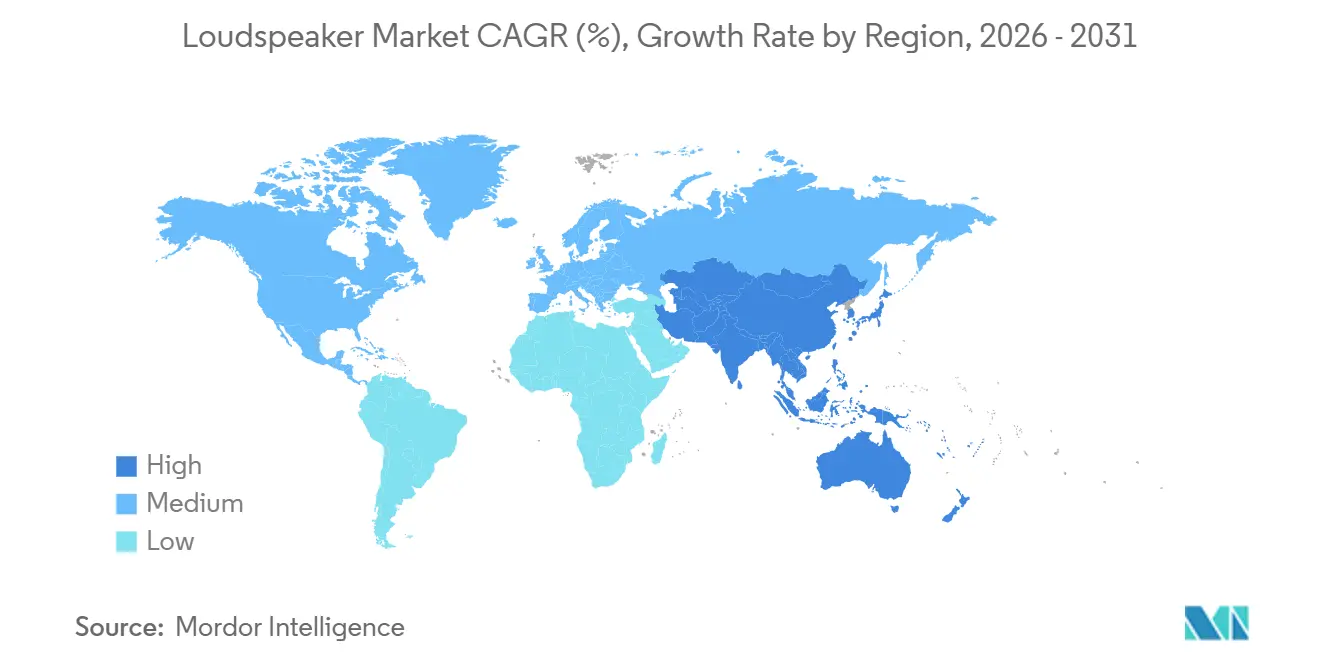

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

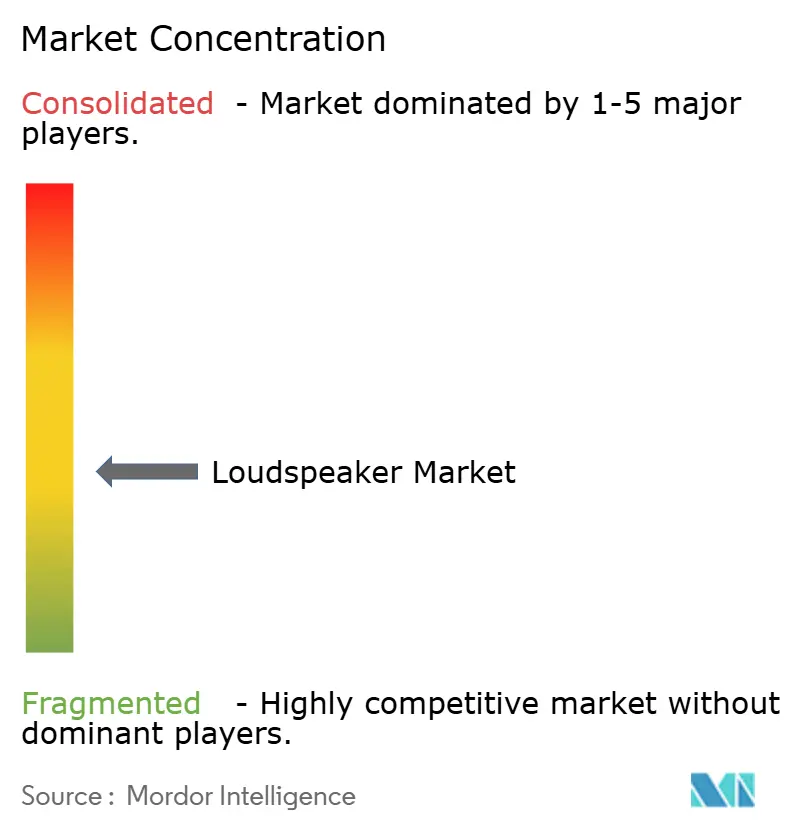

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Loudspeaker Market Analysis by ���ϲ�����

The loudspeaker market size is expected to increase from USD 7.74 billion in 2025 to USD 8.21 billion in 2026 and reach USD 11.24 billion by 2031, growing at a CAGR of 6.48% over 2026-2031. The trajectory reflects three concurrent shifts, automotive cabins are migrating to spatial-audio layouts that mask electric-vehicle power-train noise, Bluetooth LE Audio with the LC3 codec is standardizing low-latency wireless fidelity, and solid-state MEMS micro-speakers are enabling sub-1 millimeter driver arrays for ultra-slim devices. Wireless connectivity led with a 50.83% share in 2025, propelled by multi-room ecosystems that now interoperate over Thread and Matter without proprietary hubs. Active speakers accounted for 71.47% of revenue, as integrated DSP amplification reduced installer labor and enabled firmware-based room correction. Home entertainment retained the largest application share at 38.74%, yet automotive posted the fastest growth as OEMs embedded Dolby Atmos height channels in mid-tier electric sedans to counter HVAC and inverter whine.

Key Report Takeaways

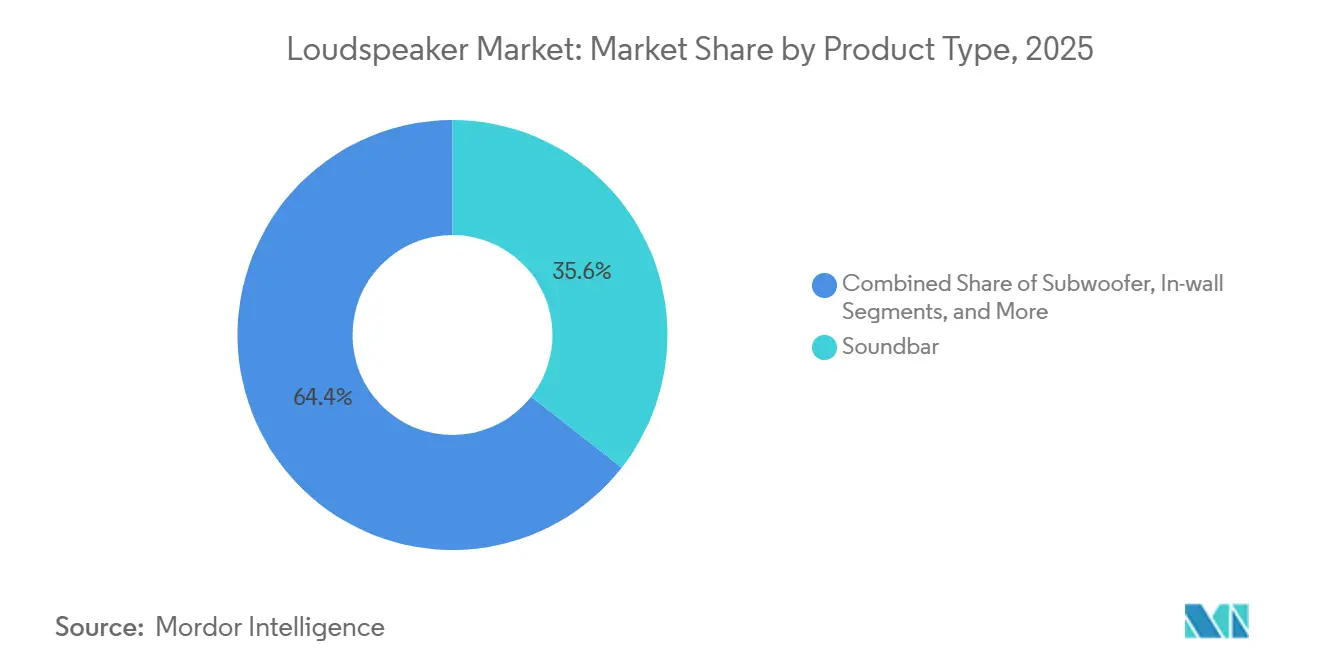

- By product type, soundbars led with 35.58% revenue share in 2025, while outdoor speakers recorded the fastest 6.54% CAGR through 2031.

- By connectivity, wireless solutions captured 50.83% of loudspeaker market share in 2025 and are projected to expand at a 6.73% CAGR to 2031.

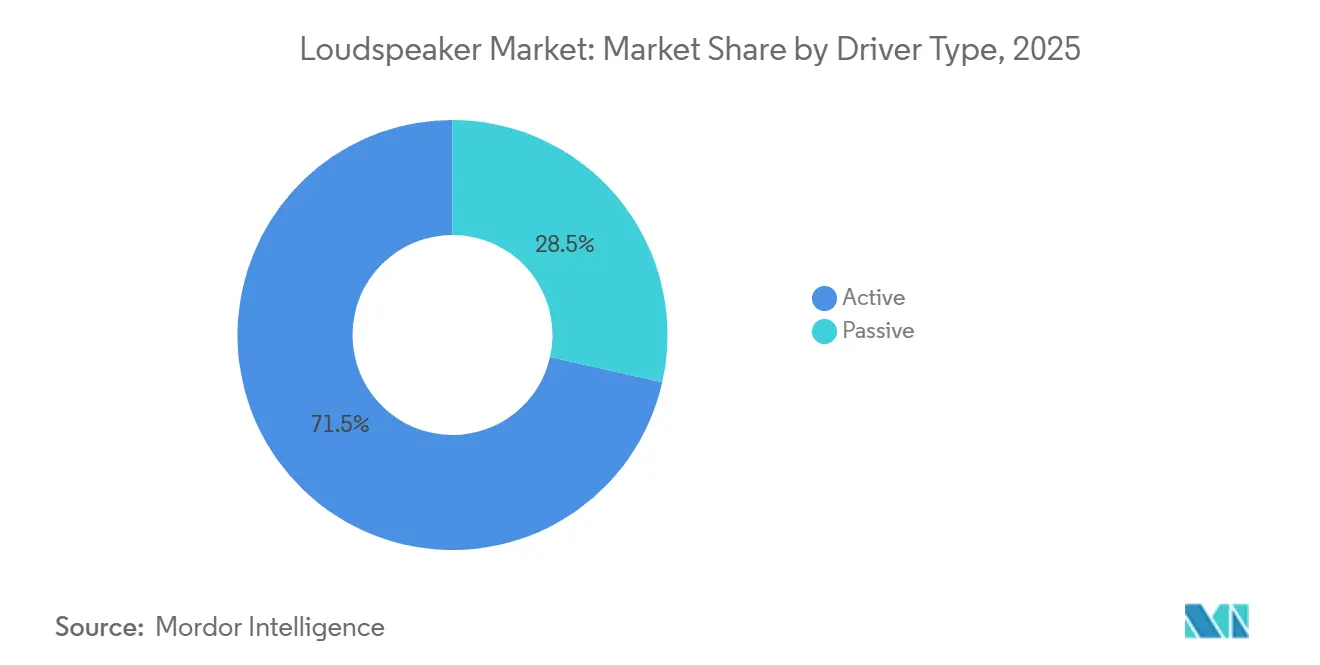

- By driver type, active models held 71.47% of the loudspeaker market in 2025; passive designs trailed but share an identical 6.50% CAGR outlook.

- By application, home entertainment accounted for 38.74% in 2025, whereas automotive is advancing at a 6.68% CAGR to 2031.

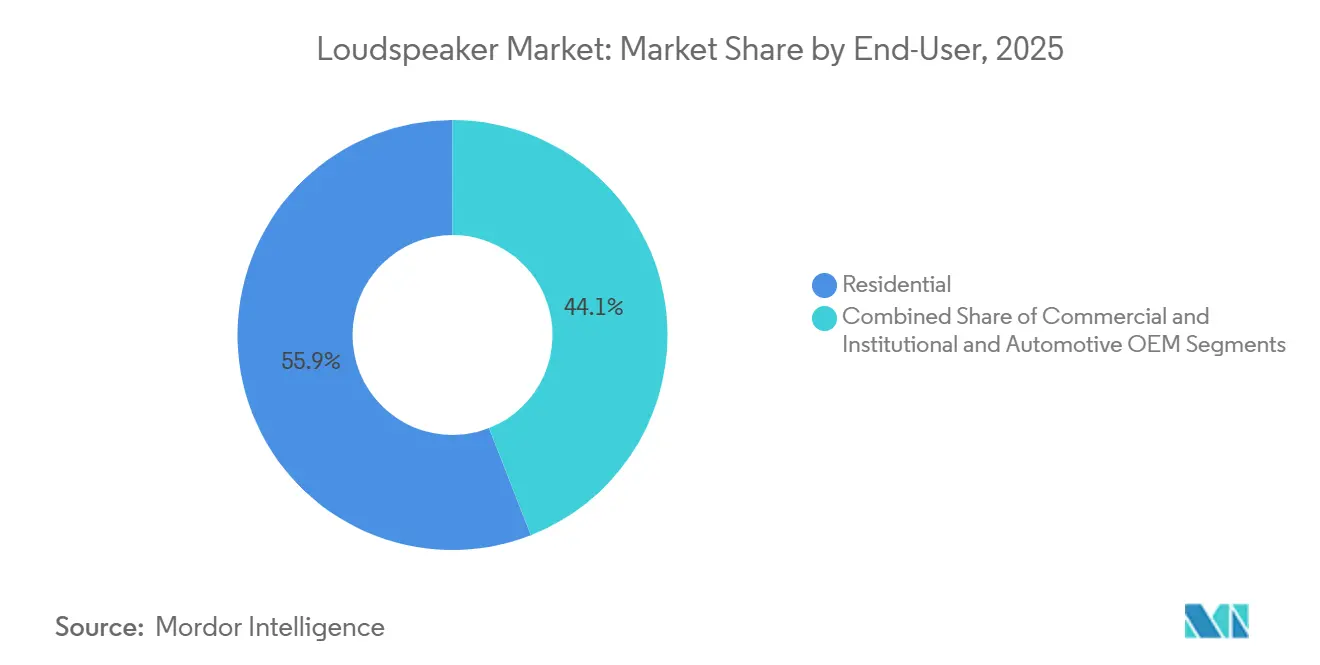

- By end-user, residential commanded 55.94% in 2025; automotive OEM channels grow fastest at a 6.77% CAGR.

- By distribution channel, online sales dominated with 64.74% share in 2025 and will rise at a 6.81% CAGR through 2031.

- By geography, North America held 33.86% in 2025, yet Asia-Pacific is projected to increase at a 6.84% CAGR, the highest regional pace.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Loudspeaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Wireless Multi-Room Speakers | +0.9% | North America and Europe, spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Rising Adoption in Automotive Infotainment Systems | +1.2% | Global, early concentration in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Growth in Home Theatre and Gaming Consumption | +0.8% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Advances in Bluetooth LE Audio (LC3) Enabling Low-Latency Hi-Fi Streaming | +1.1% | Global | Medium term (2-4 years) |

| Emergence of Auracast Public-Broadcast Loudspeaker Retrofits | +0.6% | Europe and North America, pilot deployments in Asia-Pacific | Long term (≥ 4 years) |

| Adoption of Solid-State MEMS Micro-Speakers Enabling Ultra-Thin Arrays | +0.7% | Global, manufacturing concentration in Asia-Pacific | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Advances in Bluetooth LE Audio (LC3) Enabling Low-Latency Hi-Fi Streaming

Bluetooth LE Audio moved from specification to mass-market reality in 2025 as chipset prices fell below USD 5, prompting manufacturers to abandon proprietary links in favor of a standardized broadcast layer. The LC3 codec halves the legacy SBC bitrate yet delivers comparable perceived quality, cutting power draw by about 50% and extending portable-speaker battery life from 8 hours to as much as 15 hours at similar volume levels.[1]Bluetooth Special Interest Group, “Bluetooth LE Audio,” bluetooth.com Sub-100 millisecond latency removes lip-sync issues for gaming and video. Auracast, a new broadcast profile, lets one transmitter serve unlimited receivers without pairing; pilot programs in rail stations and museums illustrate its public-address potential. Together, these advances reduce vendor lock-in and strengthen the appeal of interoperable ecosystems.

Rising Adoption in Automotive Infotainment Systems

Electric-vehicle cabins lack engine masking, so OEMs now treat audio quality as a primary differentiator. Hyundai Motor Group embeds Dolby Atmos and Ambisonics rendering in mid-tier models after extensive NVH lab validation.[2]Hyundai Motor Group, “Audio Innovation in EVs,” hyundaimotorgroup.com Texas Instruments’ AM2754-Q1 system-on-chip integrates active noise cancellation and multi-zone distribution for USD 20-26, trimming premium-audio bills of materials by up to 20% versus discrete designs. Research published in the Journal of the Audio Engineering Society found that electric-vehicle owners rate infotainment audio 18% more important than drivers of combustion cars, accelerating demand for higher-wattage amplifiers and additional speaker drivers. The loudspeaker market, therefore, benefits from design wins tied to rising electric-vehicle volumes.

Growing Demand for Wireless Multi-Room Speakers

Consumers increasingly expect seamless playback across rooms, and the leap to Thread and Matter protocols is resolving past set-up pain points. Multi-room ecosystems now deliver synchronized, lossless audio without proprietary hubs, encouraging upgrades from single portable units to whole-home arrays. North American and European households lead adoption, but urban India and China are catching up as broadband penetration rises. Brands offering app-based calibration and voice-assistant tie-ins gain share, especially when pairing requires only a smartphone QR-code scan. As a result, wireless products are forecast to displace wired units in volume terms before 2030.

Growth in Home Theatre and Gaming Consumption

Streaming platforms hosted more than 10,000 Dolby Atmos titles by 2025, pushing households to replace 2.1-channel bars with 5.1.2 or higher configurations that include height effects. Samsung’s 2025 Q-series soundbars ship with wireless rear and subwoofer speakers, cutting typical installation time from 45 minutes to under 10 minutes. The popularity of esports has driven demand for low-latency speakers that mirror on-screen cues, and LC3 now meets that requirement. While richer sound drives near-term unit sales, longer replacement cycles may temper mature-market volume growth later in the forecast.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin Pressure from Commoditisation and Asian ODM Supply | -0.5% | Global, most acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Semiconductor Supply-Chain Volatility for DSP and Amplifier ICs | -0.8% | Global | Medium term (2-4 years) |

| EU Eco-Design Standby-Power Regulations Tightening From 2026 | -0.4% | Europe, indirect impact on global product roadmaps | Short term (≤ 2 years) |

| Urban Acoustic-Zoning Laws Limiting Indoor SPL Compliance Features | -0.3% | Asia-Pacific urban centers, spillover to Europe | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Semiconductor Supply-Chain Volatility for DSP and Amplifier ICs

Lead times for key class-D amplifier and DSP chips exceeded 26 weeks in 2024 and remained elevated into 2025, forcing redesigns that cost manufacturers USD 50,000-200,000 per platform and delayed launches by up to six months. Cirrus Logic’s CS35L42 smart amplifier shortages illustrate how smartphone and automotive demand now vie for the same 28-nanometer capacity. Geopolitical risks surrounding major foundries add further uncertainty. Brands with dual-source strategies or long-term wafer agreements mitigate exposure, but smaller entrants face margin erosion and lost shelf space, weighing on the loudspeaker market growth trajectory.

EU Eco-Design Standby-Power Regulations Tightening From 2026

From January 2026, network-connected speakers sold in the European Union must draw no more than 0.3 watts in standby, down from 0.5 watts, and must display energy-use data on labels.[3]European Commission, “Eco-Design Directive Guidelines,” ec.europa.eu Compliance requires efficient switch-mode supplies and low-leakage regulators, raising bill-of-materials costs 8-12% for legacy designs. The rule especially burdens wireless multi-room models that maintain persistent network links; ODMs lacking engineering depth may exit the market, reducing choice for value-conscious buyers. While premium brands plan to market energy efficiency as a benefit, slower redesign cycles could briefly suppress unit shipments during the transition period.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Soundbars Retain Lead While Outdoor Speakers Accelerate

Soundbars captured 35.58% of the loudspeaker market in 2025, a position secured by their compact form factor and plug-and-play setup, and they remain the entry point for many households upgrading flat-panel television sound. The category benefits from widening price bands that now range from sub-USD 100 single-bar units to USD 1 800 flagship packages with wireless surrounds, giving it resilience across income brackets. Outdoor speakers are the fastest-growing segment, advancing at a 6.54% CAGR through 2031 as post-pandemic preferences shift entertainment to patios, balconies, and recreational vehicles. IP67-rated enclosures and batteries exceeding 20 hours runtime allow year-round use in harsh weather, and models with synchronized RGB lighting appeal to younger buyers who treat audio and décor as one experience.

The remainder of the product mix shows divergent trajectories. Subwoofers continue to grow alongside soundbars because low-frequency extension below 40 Hz remains critical for cinematic impact. In-wall units serve custom installations that prioritize hidden hardware over placement flexibility, though growth lags as new housing construction slows in mature economies. Floor-standing towers still dominate the audiophile niche thanks to full-range dynamics, but their share inches down as ceiling-firing soundbars replicate Atmos height effects in smaller footprints. Bookshelf and satellite speakers hold steady by anchoring expandable 5.1 and 7.1 layouts that let owners build systems over time. The outdoor surge indicates that vendors prepared to invest in ruggedized enclosures and long-life batteries can win share in an under-served corner of the loudspeaker market.

By Connectivity Technology: Wireless Gains Momentum as Matter Simplifies On-Boarding

Wireless channels accounted for 50.83% of revenue in 2025 and will outpace wired counterparts with a 6.73% CAGR to 2031, reflecting a consumer swing toward clutter-free living rooms and whole-home synchronization. Bluetooth dominates portable and automotive form factors because of low power draw, while Wi-Fi and proprietary mesh systems retain the edge in lossless streaming for home cinema. Bluetooth LE Audio with the LC3 codec halves bit-rate at equivalent subjective quality, doubling battery life in portable speakers and lowering cost barriers for entry-level models. Auracast broadcast capability lets one transmitter serve unlimited receivers, promising to displace proprietary multi-room stacks in hospitality and public-venue deployments.

Matter 1.3, certified in 2025, now offers a unified control layer across Thread, Wi-Fi, and Ethernet transports, allowing speakers from different brands to appear in a single smartphone dashboard. The simplified setup reduces return rates that once plagued first-time buyers. Wired interfaces-HDMI eARC, optical S/PDIF, and analog RCA-retain a loyal base among enthusiasts who value immune-to-dropout signal paths and millisecond-level latency, and they protect the loudspeaker market from full wireless cannibalization. Nevertheless, wireless shipments will surpass wired units before decade’s end, making antenna design, RF coexistence, and over-the-air firmware proficiency core to competitive advantage.

By Driver Type: Active Platforms Extend Reach as DSP Costs Fall

Active speakers dominated with 71.47% share in 2025 and will widen their lead, growing parallel to the total market at 6.50% CAGR yet stealing unit volume from entry-level passive kits. Integrated class-D amplification, often based on Texas Instruments TAS57-series silicon, permits 90% electrical efficiency and sub-1% total harmonic distortion at rated output, eliminating bulkier external receivers. Over-the-air updates now push room-response correction algorithms that used to require premium AVRs, giving active systems a software upgrade path that lengthens product life.

Passive speakers still serve custom installers who prefer to locate amplifiers in equipment racks for heat management and future-proofing. That channel stays relevant in high-budget theaters and two-channel purist rooms where external amplification offers tuning freedom. The passive slice of the loudspeaker market will not vanish, but its growth matches the average rather than leading it, as younger apartment dwellers favor minimalist setups that arrive fully amplified.

By Application: Automotive Becomes the Headline Growth Story

Home entertainment retained 38.74% of 2025 revenue because streaming providers added more than 10 000 Dolby Atmos titles, giving households reason to move beyond stereo sound. Yet the automotive segment is set to record a 6.68% CAGR, the highest among applications, as electric-vehicle makers package spatial audio to offset power-train quietness. Hyundai Motor Group’s integration of Dolby Atmos in mid-tier sedans illustrates how audio upgrades migrate down price ladders once exclusivity wanes at the top.

Communication endpoints for hybrid offices reached saturation after two years of conference-room retrofits, so their share plateaus. Events and outdoor entertainment rebound as live gatherings resume, but demand remains seasonal. Commercial sound reinforcement sees modest gains by swapping legacy 70-volt distributed systems for PoE-powered network nodes that simplify zoning in retail, hospitality, and school campuses.

By End-User: OEM Vehicle Channels Close the Gap on Residential Demand

Residential buyers still accounted for 55.94% of global volume in 2025, buoyed by soundbar refreshes and the popularity of voice-assistant speakers. Average replacement cycles, however, stretch five to ten years, tempering repeat sales. Automotive OEM channels, growing at 6.77% CAGR, are chipping away at that dominance by embedding branded audio packages during vehicle assembly rather than leaving upgrades to the aftermarket. Tier-one suppliers that certify AEC-Q qualified drivers and low-latency DSP stacks lock in multi-year revenue connected directly to production schedules rather than discretionary consumer spending, a structural tailwind for the loudspeaker market.

Commercial and institutional buyers are slower but steadier. Facilities managers prioritize total cost of ownership, so energy-efficient class-D amplification and cloud-based monitoring get preference. Brands that provide remote diagnostics and modular service kits create stickiness, even if upfront hardware margins are leaner.

By Distribution Channel: Online Commerce Reshapes Buying Journeys

Online storefronts captured 64.74% of revenue in 2025, with Amazon and regional e-commerce leaders handling logistics while influencers and unboxing videos reduce information gaps. Algorithmic suggestions nudge shoppers toward higher ASP bundles that include rear surrounds and subwoofers, raising basket values. Direct-to-consumer websites from legacy brands add advanced visualization tools that show room placement in augmented reality, narrowing the experiential gap with brick-and-mortar audition rooms.

Offline consumer-electronics chains still matter for premium purchases where buyers need a live audition before paying four-figure prices. Specialist audio boutiques remain indispensable for architectural installations that require pre-construction consultation, though their universe is shrinking as chain integrators consolidate. The pull of online convenience will continue to reshape the loudspeaker market, but showroom experiences will survive as aspirational touchpoints.

Geography Analysis

North America commanded 33.86% of 2025 revenue thanks to entrenched home-theater culture, early smart-home adoption, and widespread HDMI eARC support in televisions. The region’s buyers display upgrade cycles centered on new console or streaming-player launches, favoring Dolby Atmos-capable soundbars and bundled subwoofer kits. Brands focusing on limited-edition finishes, eco-friendly packaging, and buy-now-pay-later financing differentiate in a crowded shelf.

Asia-Pacific posts the highest regional CAGR at 6.84% through 2031. India’s Production Linked Incentive scheme spurs local assembly, allowing firms such as boAt and Noise to price wireless speakers 30-40% below imported rivals without eroding profitability. China continues to flood portable Bluetooth categories with high value models, while Japan’s aftermarket scene, supported by the January 2026 Autobacs and Yamaha alliance, feeds demand for drop-in car-audio upgrades. Urban density drives compact designs that balance bass output with neighbor tolerance, a nuance global brands must respect in product tuning.

Europe grows more slowly after the Eco-Design Directive lowers standby-power ceilings to 0.3 watts starting January 2026, pushing compliance costs up 8-12% and forcing many ODMs to re-engineer power supplies. Scandinavian consumers embrace these energy labels as buying guides, giving compliant premium brands a marketing edge, yet temporary stock shortfalls could cap unit growth during the transition. South America and the Middle East post mid-single-digit expansion fueled by e-commerce penetration and rising disposable incomes, though currency swings add pricing volatility. Africa remains a nascent opportunity, with urban hubs like Lagos showing appetite for rechargeable Bluetooth party speakers that double as phone chargers.

Competitive Landscape

Top Companies in Loudspeaker Market

The top 10 suppliers accounted for roughly half of global revenue in 2025, making the loudspeaker market moderately concentrated yet competitive enough to sustain brisk innovation cycles. Heritage brands lean on decades of psychoacoustic research and proprietary wave-guide geometries to justify price premiums, while Asian original-design manufacturers mass-produce reference platforms that newcomers can badge with minimal engineering. Qualcomm, MediaTek, and newer silicon houses issue turnkey Bluetooth LE Audio modules that shorten concept-to-shelf timelines to under nine months, further lowering entry barriers.

Spatial audio integration in vehicles is emerging as a decisive battleground. Suppliers able to blend low-frequency seat shakers, A-pillar height drivers, and ceiling mid-ranges into a coherent 360-degree field win multi-year platform deals. Texas Instruments’ AM2754-Q1 system-on-chip integrates noise cancellation, multichannel routing, and class-D amplification into a single package, shaving 15-20% off bills of materials and giving OEMs headroom for higher driver counts. In consumer electronics, MEMS micro-speaker start-ups such as xMEMS and SonicEdge threaten the reign of balanced-armature drivers in tablets and ultrabooks by slashing z-height to near-coin thickness while preserving 20 kHz upper response.

Price erosion remains relentless in entry-level Bluetooth categories because ODMs in Guangdong can replicate ID design and acoustic tuning within 90 days. Brands defend share with software ecosystems, regular firmware feature drops, and subscription-backed audio-calibration services that generate post-sale revenue. Regulatory pressure on standby power and right-to-repair provisions in Europe push companies to publish parts catalogs and modular schematics, which in turn reward engineering transparency and penalize sealed-unit construction.

Loudspeaker Industry Leaders

Sony Group Corporation

Apple Inc.

Sonos Inc.

Bose Corporation

Samsung Electronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Autobacs Corporation and Yamaha Corporation launched a co-developed aftermarket speaker series tailored for Japanese domestic-market vehicles, integrating DSP profiles for popular models.

- December 2025: Samsung Electronics debuted its Q-series soundbars, bundling wireless rears and subwoofers that cut installation time to under 10 minutes.

- October 2025: Bluesound released the Pulse Soundbar 2i+, its first model with Dolby Atmos height channels, priced at USD 999.

- September 2025: Hyundai Motor Group confirmed Dolby Atmos and Ambisonics deployment in mid-tier electric vehicles during an investor briefing.

Global Loudspeaker Market Report Scope

The loudspeaker is an electronic transducer that converts an electrical audio signal into a corresponding sound. The growing popularity and increasing applications of loudspeakers in different places are among the key drivers of the loudspeaker market. The market is growing as loudspeakers have become a top priority for outdoor and indoor entertainers.

The Loudspeaker Market Report is Segmented by Product Type (Soundbar, Subwoofer, In-wall, Floor-standing/Tower, Bookshelf/Satellite, Outdoor, and Other Product Types), Connectivity Technology (Wired and Wireless), Driver Type (Active and Passive), Application (Communication, Home Entertainment, Automotive, Events and Outdoor Entertainment, and Commercial Sound Reinforcement), End-user (Residential, Commercial and Institutional and Automotive OEM), Distribution Channel (Online and Offline), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Soundbar |

| Subwoofer |

| In-wall |

| Floor-standing / Tower |

| Bookshelf / Satellite |

| Outdoor |

| Other Product Types |

| Wired | |

| Wireless | Bluetooth |

| Wi-Fi / Multi-room | |

| Zigbee / Z-Wave / Thread |

| Active (Powered) |

| Passive |

| Communication |

| Home Entertainment |

| Automotive |

| Events and Outdoor Entertainment |

| Commercial Sound Reinforcement |

| Residential |

| Commercial and Institutional |

| Automotive OEM |

| Online |

| Offline - Consumer Electronics Stores |

| Offline - Specialist Audio Retailers |

| Direct-to-Consumer / Brand Outlets |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Product Type | Soundbar | |

| Subwoofer | ||

| In-wall | ||

| Floor-standing / Tower | ||

| Bookshelf / Satellite | ||

| Outdoor | ||

| Other Product Types | ||

| By Connectivity Technology | Wired | |

| Wireless | Bluetooth | |

| Wi-Fi / Multi-room | ||

| Zigbee / Z-Wave / Thread | ||

| By Driver Type | Active (Powered) | |

| Passive | ||

| By Application | Communication | |

| Home Entertainment | ||

| Automotive | ||

| Events and Outdoor Entertainment | ||

| Commercial Sound Reinforcement | ||

| By End-user | Residential | |

| Commercial and Institutional | ||

| Automotive OEM | ||

| By Distribution Channel | Online | |

| Offline - Consumer Electronics Stores | ||

| Offline - Specialist Audio Retailers | ||

| Direct-to-Consumer / Brand Outlets | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the loudspeaker market be by 2031?

It is forecast to reach USD 11.24 billion by 2031, expanding from USD 8.21 billion in 2026 at a 6.48% CAGR.

Which product category holds the highest revenue share today?

Soundbars captured 35.58% of global revenue in 2025, maintaining the lead among all form factors.

What is the fastest-growing application area?

Automotive infotainment shows the highest growth, advancing at a 6.68% CAGR as electric-vehicle makers embed spatial-audio systems.

Why is wireless adoption accelerating?

Bluetooth LE Audio and the Matter protocol simplify pairing, cut latency, and extend battery life, prompting users to shift away from wired setups.

How will EU energy rules affect manufacturers?

From January 2026 speakers must draw no more than 0.3 watts in standby, pushing brands to adopt efficient switch-mode supplies and raising bills of materials 8-12%.

Which regions present the strongest future growth?

Asia-Pacific leads with a projected 6.84% CAGR, buoyed by urbanization in India, affordable Bluetooth models in China, and aftermarket upgrades in Japan.

Page last updated on: