Iran ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

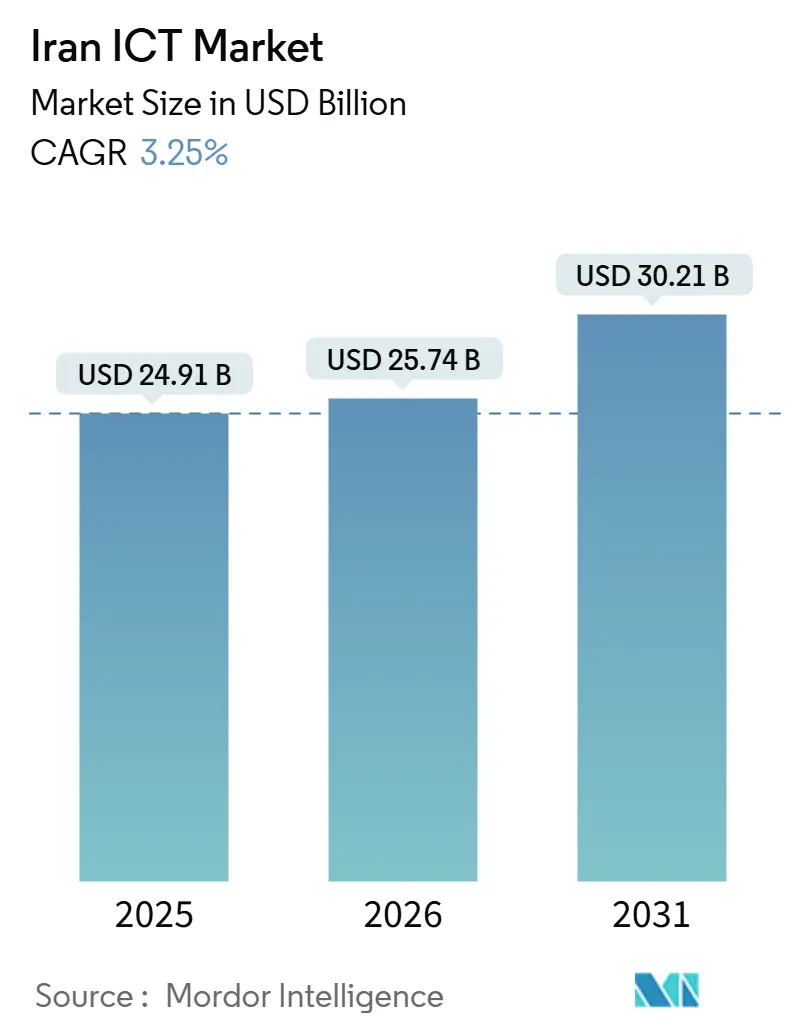

| Base Year Market Size (2025) | USD 24.91 Billion |

| Market Size (2026) | USD 25.74 Billion |

| Market Size (2031) | USD 30.21 Billion |

| Growth Rate (2026 - 2031) | 3.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Iran ICT Market Analysis by ���ϲ�����

The Iran ICT Market size is expected to grow from USD 24.91 billion in 2025 to USD 25.74 billion in 2026 and is forecast to reach USD 30.21 billion by 2031 at 3.25% CAGR over 2026-2031.

A structural realignment underlies this gradual topline growth: U.S. sanctions squeezed Western vendors out, Chinese suppliers stepped in, and domestic manufacturers accelerated import substitution. Government spectrum auctions fast-tracked 5G deployment, while the National Information Network deepened Tehran’s push for digital sovereignty. Knowledge-based companies began mass-producing 4G and 5G base stations in 2025, signaling an emerging hardware ecosystem. Cloud adoption gained momentum after a centralized government cloud launch in 2024, and integration of the Shetab and Mir payment rails demonstrated how sanctions pressure can generate new cross-border digital corridors.

Key Report Takeaways

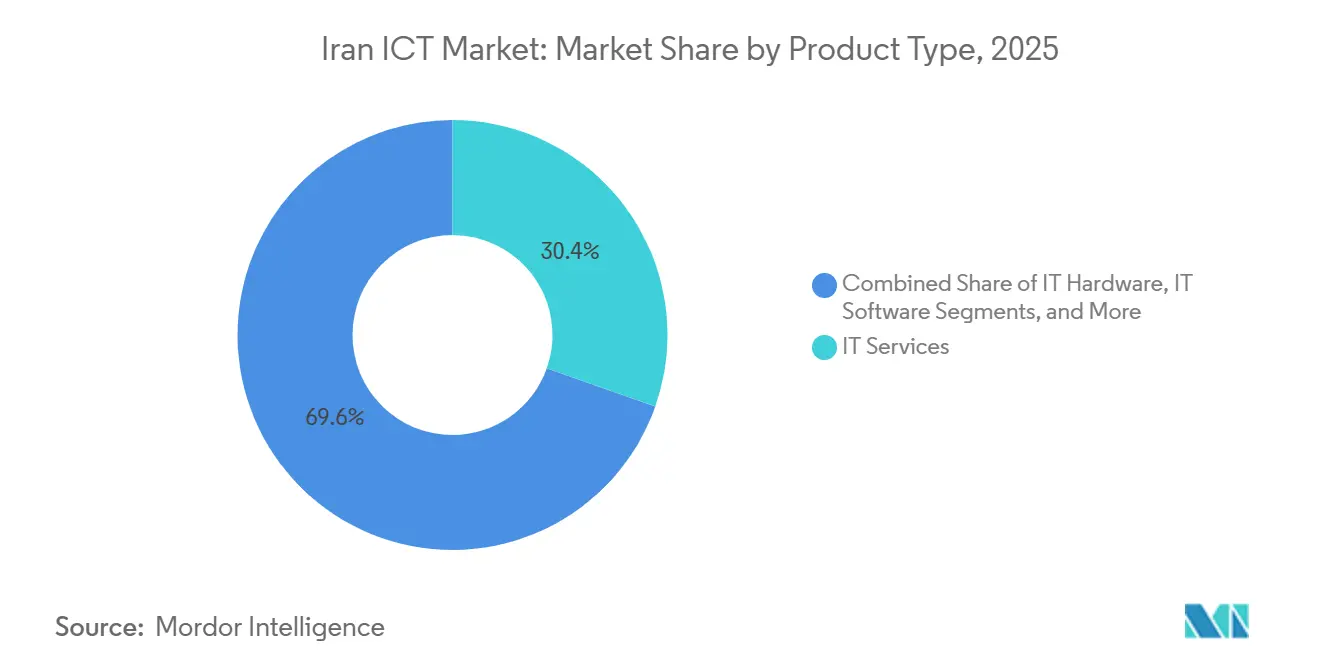

- By product type, IT Services led with 30.40% revenue share in 2025, while IT Security is projected to post the fastest 6.60% CAGR through 2031.

- By enterprise size, Large Enterprises held 64.32% of the Iran ICT market share in 2025, while Small and Medium Enterprises record the highest projected 4.10% CAGR to 2031.

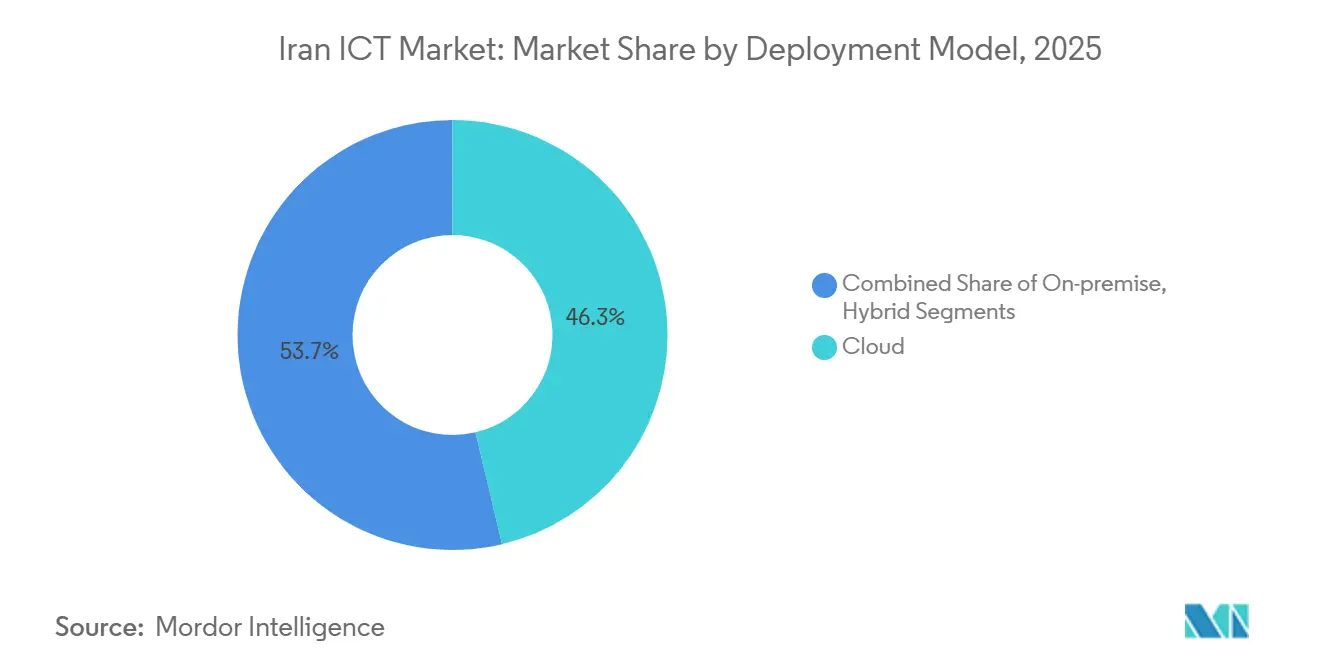

- By deployment model, cloud accounted for 46.30% of the Iran ICT market size in 2025 and is advancing at a 5.20% CAGR to 2031.

- By end-user vertical, Government and Public Administration commanded 25.34% revenue share in 2025, whereas Gaming and Esports is forecast to expand at a 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Iran ICT Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G Roll-Out Backed by Government Spectrum Auctions | +0.8% | National, with early deployment in Tehran and major metropolises | Medium term (2-4 years) |

| Surge in E-Commerce and Digital Payment Penetration | +0.7% | National, with urban centers leading adoption | Short term (≤ 2 years) |

| Increase in ICT Spend by Oil and Gas Modernization Programmes | +0.5% | National, concentrated in upstream and midstream facilities | Medium term (2-4 years) |

| Growth of Persian-Language SaaS Tools for SMEs | +0.4% | National, with higher uptake in Tehran, Isfahan, Shiraz knowledge-based clusters | Medium term (2-4 years) |

| Re-Export of Refurbished Hardware via Free-Trade Zones | +0.2% | Kish, Qeshm free-trade zones with spillover to regional markets | Long term (≥ 4 years) |

| Domestic Demand for Low-Power Edge AI Chipsets in IoT Devices | +0.3% | National, with manufacturing hubs in Tehran, Tabriz, and industrial corridors | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rapid 5G Roll-Out Backed by Government Spectrum Auctions

After assigning the 3.5-3.7 GHz bands, the ministry set an ambitious target of reaching 4,000 live 5G sites by March 2025, representing a significant increase from 1,313 sites just a year earlier. This expansion highlights the ministry's commitment to accelerating 5G deployment and enhancing connectivity infrastructure. The snap-back of sanctions in 2018 led to the withdrawal of Western vendors, creating a gap that Huawei filled as a temporary supplier to maintain progress. By July 2025, a domestic company successfully delivered 5G New Radio equipment, marking a significant milestone in reducing reliance on imports and fostering local innovation. Mobile network build-outs have proven to be more cost-effective per subscriber compared to fiber, offering a critical advantage in the face of weak capital formation and the ongoing depreciation of the rial. This dual-track strategy, which combines rapid foreign procurement for immediate needs with a focus on domestic research and development to achieve technological sovereignty, closely mirrors China's approach to advancing its technology sector.

Surge in E-Commerce and Digital Payment Penetration

Digital payment use climbed as Shetab reached near-universal accessibility and sub-2-second clearing[1]Source: Nournews, “Iran’s Shetab Network Connection to Russia’s Mir Facilitates Trade Exchanges,” nournews.ir. Bilateral linkage with Russia’s Mir network in 2024-2025 opened a sanctions-resistant tourist and trade channel. The IMF ranked Iran alongside Saudi Arabia and the UAE for adult digital-payment adoption. Domestic super-apps such as Bale and Rubika monetize a Persian-language user base, keeping transaction data within national borders, a priority under cyber-sovereignty mandates.

Increase in ICT Spend by Oil and Gas Modernization Programmes

In December 2025, the National Iranian Oil Company signed contracts focused on AI and digitalization, aiming to enhance production efficiency and streamline operations. With the integration of IoT sensors, edge analytics, and AI-driven reservoir models, the company anticipates significant productivity boosts without the need for substantial capital imports. These advanced technologies are expected to optimize resource utilization, reduce operational downtime, and improve decision-making processes. Domestic vendors, harnessing engineering expertise from Sharif University, are actively customizing solutions to address the unique challenges of the industry's hazardous upstream sites. This surge in spending also extends its influence to cybersecurity vendors, who are tasked with safeguarding SCADA assets against potential threats, and to satellite links that play a critical role in transmitting real-time data from distant rigs to centralized monitoring systems.

Growth of Persian-Language SaaS Tools for SMEs

Persian-language interfaces play a crucial role in reducing linguistic challenges, while subscription-based models significantly lower upfront costs, enabling faster adoption of cloud and SaaS solutions among SMEs. This trend is further supported by government incentives designed to promote the growth of knowledge-driven companies. Additionally, the July 2025 mandate requiring cloud providers to comply with ISO standards helps to simplify compliance processes, making it easier for SMEs to integrate these technologies into their operations. Moreover, the introduction of a national AI platform in March 2025 provides SMEs with seamless access to pre-built NLP and vision models. This initiative not only democratizes the use of advanced analytics but also empowers smaller enterprises to leverage cutting-edge technologies, fostering innovation and enhancing their competitive edge in the market.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. Sanctions Limiting Access to Global Vendors | -0.6% | National, with acute impact on sectors requiring advanced Western technology | Long term (≥ 4 years) |

| Local Currency Volatility Affecting CapEx Cycles | -0.4% | National, with heightened sensitivity in import-dependent segments | Short term (≤ 2 years) |

| Electricity Rationing Impacting Data-Centre Uptime | -0.3% | National, with severe disruptions in Tehran and industrial zones during peak demand | Medium term (2-4 years) |

| Brain-Drain of Senior ICT Talent to Gulf Countries | -0.3% | National, with talent outflows concentrated in Tehran, Isfahan, Shiraz tech clusters | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

U.S. Sanctions Limiting Access to Global Vendors

Leading semiconductor firms, enterprise software companies, and cloud platforms find themselves stymied by OFAC restrictions, which have significantly impacted their ability to operate in certain regions. Ericsson's revenue from Iran plummeted post-2018, highlighting a broader trend of vendor exodus as companies faced increasing regulatory and operational challenges. These sanctions not only restrict operations but also deny crucial security patches, thereby amplifying vulnerability risks and exposing systems to potential threats. Despite these challenges, companies like Farabin, under mounting pressure, ramped up production of LTE base stations in 2025 to address the growing demand for localized solutions. While this move led to a slower deployment of infrastructure, it also fostered a deeper localization of operations, enabling the development of more region-specific technologies and solutions.

Local Currency Volatility Affecting CapEx Cycles

Operators are experiencing significant pressure on their margins as the rial continues to depreciate. This is primarily because equipment costs are denominated in hard currencies, while revenues are generated in rials, creating a financial imbalance. MTN Irancell, for instance, has invested IRR 11 trillion (USD 63 million) in the development of a major data center. However, the company is now facing budgetary challenges as exchange-rate fluctuations inflate costs during the construction phase. Additionally, suppliers, concerned about the ongoing volatility, are increasingly demanding pre-payments in dollars or imposing risk premiums, which further escalates effective costs. This level of unpredictability is making it difficult for operators to execute multi-year network plans effectively and is causing delays in critical equipment refresh cycles, thereby impacting overall operational efficiency.

Segment Analysis

By Product Type: Security Spending Rises as Services Dominate

IT Services held the largest 30.40% slice of the Iran ICT market in 2025. Systems integration and managed services are labor-intensive, a natural fit for a knowledge-rich yet capital-scarce environment. Operators juggle Huawei, domestic, and legacy Western assets, so integrators remain indispensable. IT Security, although smaller, is expanding at a 6.60% CAGR. Iranian-sponsored cyber campaigns prompt mirrored investments in defensive tooling, from endpoint protection to security operation centers.

Localization milestones deepen hardware opportunities. Farabin’s LTE base-station production and localized 5G NR radios, both launched in 2025, illustrate import substitution. Operators can now source radios, routers, and microwave links locally, alleviating sanctions bottlenecks. AI-embedded network analytics improve spectrum efficiency and predictive maintenance. Meanwhile, IT Software growth benefits from Persian super-apps that bundle chat, video, and mini-stores, monetizing a captive user base and driving platform-as-a-service revenue.

By Enterprise Size: Cloud Levels the Playing Field for SMEs

Large Enterprises absorbed 64.32% of 2025 spending, reflecting oil, telecom, and banking priorities. These giants afford private links, redundant power, and in-house security teams. Still, legacy mainframes and bespoke applications slow modernization. SMEs, aided by SaaS and pay-as-you-go cloud, are forecast to contribute a rising share as their 4.10% CAGR outpaces the total Iran ICT market. Government R&D vouchers and knowledge-based tax holidays sweeten ROI for cloud migration.

Local providers certify under ISO 27017 and ISO 27018 to win public-sector workloads, establishing reference architectures that SMEs trust. The national AI platform lowers the entry barrier by packaging NLP and vision APIs, so startup teams can add smart features without deep data-science benches. As SMEs digitize inventory and payment flows, they extend the footprint of the Iran ICT market into provincial cities, broadening addressable demand beyond Tehran.

By Deployment Model: Cloud Gains Ground Despite Sovereignty Fears

Cloud captured 46.30% of the Iran ICT market size in 2025 and should grow at a 5.20% CAGR through 2031. The 2024 centralized government cloud pooled resources, then the 2025 tender for ISO-compliant providers set baseline security norms. Hybrid patterns prevail: sensitive oilfield telemetry stays on-premise while less-critical HR apps migrate to the cloud. Electricity rationing, however, challenges uptime. Providers invest in diesel backups and modular batteries, yet grid instability remains a cost driver.

On-premise environments persist in defense, oil, and large banks under strict data-locational rules. They also act as cloud landing zones, hosting local zones for latency-sensitive workloads. The Iran ICT industry thus evolves toward an ecosystem where public and private clouds interconnect via national internet exchange points, routing domestic traffic internally to satisfy sovereignty laws.

By End-User Industry Vertical: Sovereignty Leads, Gaming Thrives

Government and Public Administration commanded 25.34% of 2025 revenues. Digital-ID rollouts, e-government portals, and expansion of the National Information Network anchor demand. Shetab-Mir integration extends public-sector fintech ambitions beyond borders. Gaming and Esports, with a 6.12% CAGR, benefits from a median age of 32 and ubiquitous smartphones. Domestic studios publish Persian-language titles, and streaming platform Aparat monetizes via advertising and in-game micro-purchases.

BFSI pushes cybersecurity and core modernization, yet overseas clearing restrictions complicate appetite for real-time settlement platforms. Oil and Gas modernization contracts drive AI, IoT, and satellite links for offshore rigs. Healthcare taps telemedicine, propelled by pandemic-era policy tailwinds. Retail and logistics capitalize on 85% digital-payment penetration, with last-mile platforms integrating QR and Mir Pay options for Russian tourists.

Geography Analysis

Tehran dominates the Iran ICT market, generating roughly 70% of Speedtest samples and housing the largest data centers[2]Source: AINITA Project, “Iran in Speed Internet and Restrictions, Disruptions,” ainita.net . Secondary clusters in Isfahan, Shiraz, Tabriz, and Mashhad thrive around technical universities and government grants. Urban internet penetration of 83% contrasts with 66% in rural districts, guiding policy makers toward mobile 5G as a cost-efficient broadband substitute.

Kish and Qeshm free-trade zones function as technology entrepôts. Traders refurbish imported servers and networking gear for re-export, while incubators attract startups experimenting with relaxed customs, creating spillovers into the broader Iran ICT market. The tiered internet framework yields a dual reality: state agencies enjoy a controlled domestic backbone, whereas citizens rely on VPNs, estimated at 80% penetration, to reach blocked services.

External connectivity remains fragile. Two cable cuts in late 2024 removed up to 37% of bandwidth, exposing the risk of limited redundancy. Starlink’s gray-market uptake, estimated at 20,000-30,000 terminals by late 2024, introduces an uncensored pathway, although import costs run USD 700-2,000 per kit. Brain drain is acute in Tehran, Isfahan, and Shiraz, where half the startup community contemplates relocation to Gulf neighbors that offer higher pay and open capital markets.

Competitive Landscape

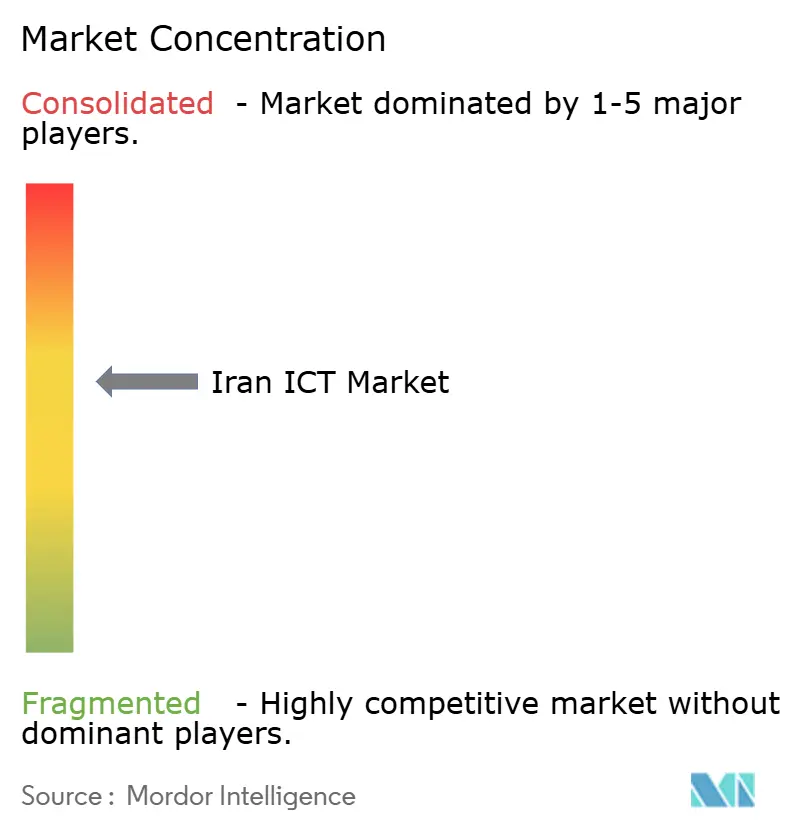

The market is moderately fragmented. Telecommunication Company of Iran, MTN Irancell, and Rightel control core connectivity through exclusive spectrum holdings, while private ISPs compete on value-added services. Hamrahe Avval leads with 57% retail ISP share. Domestic manufacturers, notably Farabin, entered radio-access hardware production in 2025, nudging the ecosystem toward self-reliance.

Still, Chinese partnerships remain pivotal. Leaked 2023 documents list USD 325 million for Telecommunication Company of Iran modernization and USD 250 million for Irancell upgrades with Chinese vendors[3]Source: Iran International Newsroom, “Leaked Document Reveals Iran’s Multiple Telecom Deals With China,” iranintl.com . Satellite projects valued between USD 100 million and USD 450 million complement terrestrial investments. The pattern reflects a hybrid model, balancing local capability building with selective foreign sourcing.

White-space growth areas include cybersecurity frameworks tailored for Persian networks, edge AI appliances for factory automation, and sanctions-resistant fintech connectors. The Shetab-Mir linkage showcases exportable expertise in alternative payment infrastructure. Potential disruptors range from Starlink’s low-earth-orbit backhaul to super-apps that can bundle communications, gaming, and e-commerce. The National AI Organization, backed by USD 115 million, seeks to cultivate domestic AI champions able to embed smart functions across verticals.

Iran ICT Industry Leaders

Irancell Telecommunication Services Company (Private Joint Stock)

Telecommunication Company of Iran

Rightel Communications Service Company

Asiatech Data Transmission Company

Iran High-Tech Networks Development Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Starlink began offering free service inside Iran, promising uncensored connectivity and challenging the incumbent ISP model.

- May 2025: The Central Bank of Iran completed phase two of the Shetab-Mir integration, allowing Mir Pay NFC transactions at Iranian point-of-sale terminals.

- March 2025: A national AI platform prototype debuted, giving SMEs access to ready-trained NLP and vision models.

- January 2025: The government allocated USD 115 million to the National AI Organization for research and talent programs.

Iran ICT Market Report Scope

Information and communication technologies or ICT is a broader term for information technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services enabling users to store, access, transmit, retrieve, and manipulate information in a digital form. The revenue tracks the product offerings provided by the companies.

The Iran ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security, and Communication Services), End-User Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Deployment Model (On-premise, Cloud, and Hybrid), and End-User Industry Vertical (Government and Public Administration, BFSI, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, and Gaming and Esports). Market Forecasts are Provided in Terms of Value (USD).

| IT Hardware |

| IT Software |

| IT Services |

| IT Infrastructure |

| IT Security |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Gaming and Esports |

| Other Verticals |

| By Products Type | IT Hardware |

| IT Software | |

| IT Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services | |

| By End-User Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By Deployment Model | On-premise |

| Cloud | |

| Hybrid | |

| By End-User Industry Vertical | Government and Public Administration |

| BFSI | |

| Energy and Utilities | |

| Retail, E-commerce and Logistics | |

| Manufacturing and Industry 4.0 | |

| Healthcare and Life Sciences | |

| Oil and Gas (Up-, Mid-, Down-stream) | |

| Gaming and Esports | |

| Other Verticals |

Key Questions Answered in the Report

What is the projected value of the Iran ICT market by 2031?

Forecasts place the market at USD 30.21 billion in 2031, reflecting a 3.25% CAGR over 2026-2031.

Which segment is expanding fastest within the Iran ICT market?

IT Security shows the highest segment CAGR at 6.60%, driven by rising cyber-threat awareness.

How large is cloud deployment in the Iran ICT market today?

Cloud models represented 46.30% of 2025 spending and are set to rise at a 5.20% CAGR.

Why are SMEs gaining relevance in Iranian ICT spending?

Persian-language SaaS tools and government incentives support a 4.10% CAGR for the SME segment to 2031.

Page last updated on: