Russia ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

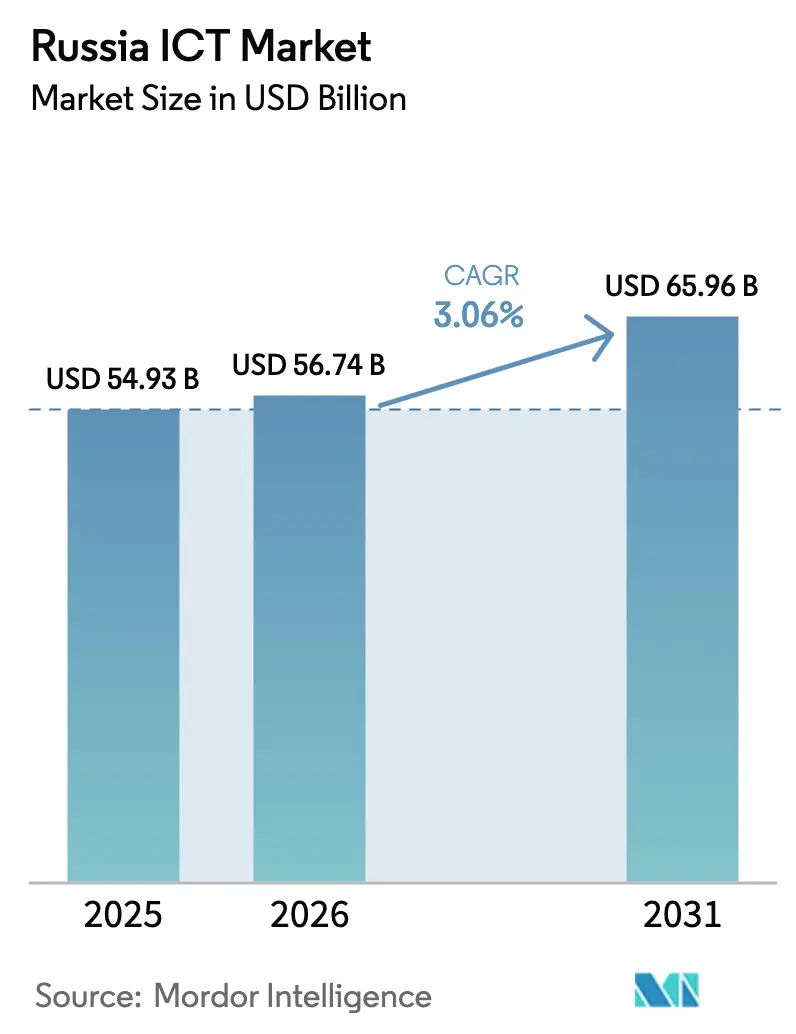

| Base Year Market Size (2025) | USD 54.93 Billion |

| Market Size (2026) | USD 56.74 Billion |

| Market Size (2031) | USD 65.96 Billion |

| Growth Rate (2026 - 2031) | 3.06% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Russia ICT Market Analysis by ���ϲ�����

The Russia ICT Market size is expected to increase from USD 54.93 billion in 2025 to USD 56.74 billion in 2026 and reach USD 65.96 billion by 2031, growing at a CAGR of 3.06% over 2026-2031. Spending is migrating from mature voice and broadband offerings toward sovereign cloud, AI-optimized workloads, and edge computing that conform to strict data-localization statutes. Import-substitution rules that require 95% domestic software and 70% domestic hardware for public contracts are redirecting billions of rubles in annual outlays to local vendors. Meanwhile, 5G rollouts in 35 cities, the Sfera low-Earth-orbit constellation, and cold-climate data center retrofits create new backbones for ultra-low-latency services. Headwinds stem from international semiconductor sanctions, a persistent exodus of 70,000-100,000 IT professionals since 2022, and rising power tariffs that squeeze data-center margins.

Key Report Takeaways

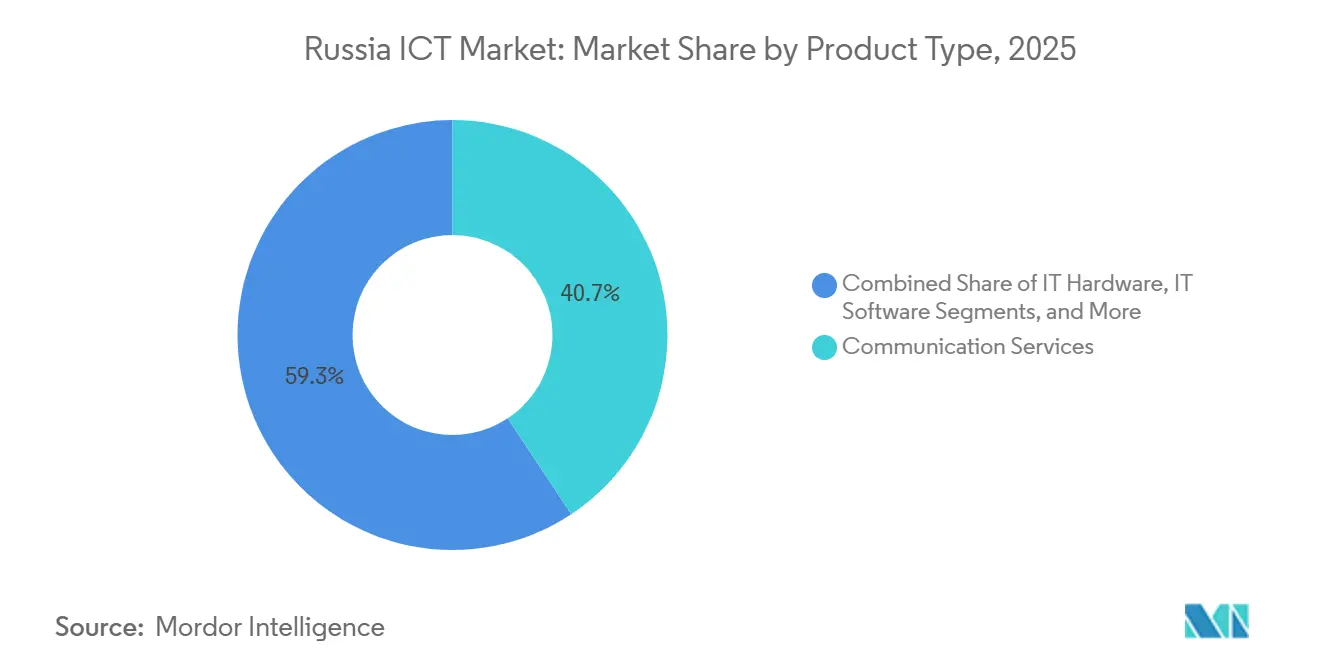

- By product type, IT Services held the largest 34.22% Russia ICT market share in 2025, while Cloud Services posted the fastest 3.32% CAGR to 2031.

- By enterprise size, large enterprises commanded 61.10% share of the Russia ICT market size in 2025, whereas SMEs are projected to expand at a 3.49% CAGR through 2031.

- By vertical, cloud captured 47.85% of the Russia ICT market share in 2025 and hybrid is forecast to advance at a 3.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Government-Led Digital Transformation and Import-Substitution Programs | +0.9% | National, early gains in Central, Northwestern, Volga FDs | Medium term (2-4 years) |

| Expansion of 5G and Fiber Infrastructure Roll-outs | +0.7% | Central and Northwestern FDs, expanding to Ural and Siberian | Medium term (2-4 years) |

| Accelerating Adoption of Domestic Cloud and Data-Center Services | +0.8% | National, concentrated in Central FD, expanding to Far Eastern FD | Short term (≤ 2 years) |

| Mandated Localization of Microelectronics and Server Supply Chains | +0.5% | Central, Northwestern, Ural FDs (manufacturing hubs) | Long term (≥ 4 years) |

| Satellite-Based LEO Connectivity for Remote Regions | +0.3% | Far Eastern, Siberian, North Caucasian FDs | Long term (≥ 4 years) |

| AI-Optimized, Cold-Climate Data-Center Retrofits | +0.2% | Siberian and Far Eastern FDs | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising Government-Led Digital Transformation and Import-Substitution Programs

Federal decree 1236 lifted domestic-content thresholds to 95% for software and 70% for hardware, steering an extra USD 2.3 billion toward homegrown vendors in 2025.[1]Government Decree 1236, “On Establishing Domestic Software Quotas,” government.ru The Digital Economy national program set aside RUB 1.8 trillion (USD 19.6 billion) through 2030 to digitize public services, extend broadband to 97% of households, and train 1 million AI specialists. Mandatory data-residency rules under Federal Law 242-FZ accelerated workload repatriation from foreign hyperscalers to SberCloud, Yandex Cloud, and VK Cloud, each reporting enterprise customer growth above 35% year over year in 2025. Import-substitution gaps also triggered a tenfold rise in venture funding for robotic-process-automation, low-code, and IIoT startups, although access to advanced GPUs remains scarce. Collectively, these policies underpin sustained topline demand while shielding the Russia ICT market from external vendor retreats.

Expansion of 5G and Fiber Infrastructure Roll-outs

By December 2025, MTS, MegaFon, and Beeline blanketed 35 cities with 5G using domestic radio units that integrate Baikal-M processors. Combined operator capex reached RUB 180 billion (USD 1.96 billion) to densify backhaul fiber and deploy millimeter-wave small cells for latency-critical verticals such as remote surgery and autonomous logistics. Rostelecom extended fiber-to-the-home to another 3.2 million premises, lifting broadband penetration across Volga and Ural districts. Domestic equipment validation delayed some roll-outs during 2024, yet by mid-2025 throughput and reliability matched legacy Ericsson and Huawei gear. The enhanced backbone is catalyzing 4.5 million active NB-IoT and LTE-M devices and opening recurring revenue in industrial telemetry, agriculture, and utilities.

Accelerating Adoption of Domestic Cloud and Data-Center Services

Yandex Cloud, SberCloud, and VK Cloud onboarded 12,000 new enterprises in 2025, a 38% jump that reflects stricter data-localization audits and ruble-denominated pricing that undercuts foreign rivals by up to 30%. SberCloud rolled out GPU-as-a-Service nodes with NVIDIA A100 accelerators procured via parallel imports, targeting AI training for banks and retailers previously dependent on AWS and Azure. Yandex Cloud launched a sovereign AI suite anchored by YandexGPT, delivering 85% accuracy on Russian-language NLP benchmarks while satisfying FSB certification for sensitive data. VK Cloud opened 15 edge micro-data centers within 50 kilometers of industrial clusters, supporting latency-sensitive robotics and video analytics. Domestic clouds also absorbed displaced engineers, hiring nearly 1,400 professionals in 2025 and partially mitigating the talent drain.

Mandated Localization of Microelectronics and Server Supply Chains

Sanctions curtailed access to sub-10-nanometer foundry capacity, compelling domestic pivot to 90-nanometer and 65-nanometer fabs run by Mikron and Angstrem. Baikal Electronics and MCST shipped Baikal-M, Baikal-S, and Elbrus processors, which power 40,000 government workstations but trail modern Intel and AMD chips on floating-point tasks. Yadro assembled 25,000 x86-compatible servers in 2025 using AMD EPYC CPUs sourced through third-country distributors to hit 70% domestic-content thresholds for public projects. The Ministry of Industry and Trade allotted RUB 45 billion (USD 490 million) to develop EUV alternatives and silicon photonics, although industry consensus places meaningful 7-nanometer output beyond 2028. Localization guarantees component security, yet lower performance per watt constrains next-generation cloud and AI deployments in the Russia ICT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| International Sanctions Constraining Access to Advanced Semiconductors | -0.6% | National, most acute in Central and Northwestern FDs | Long term (≥ 4 years) |

| Persistent Brain Drain of Skilled IT Professionals | -0.5% | National, heavy outflows from Moscow and St. Petersburg | Medium term (2-4 years) |

| Rising Power Tariffs and Grid Constraints for Data Centers | -0.3% | Ural, Siberian, Far Eastern FDs | Short term (≤ 2 years) |

| High Software Piracy Rates Dampening Vendor Revenues | -0.2% | National, prevalent in SME and consumer segments | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

International Sanctions Constraining Access to Advanced Semiconductors

Export controls from the United States, European Union, Japan, and South Korea prohibit sales of chips below 14 nanometers, making GPUs, FPGAs, and server CPUs scarce and expensive.[2]U.S. Bureau of Industry and Security, “Export Administration Regulations Russia Controls,” bis.doc.gov Parallel imports via Turkey, UAE, and China covered roughly one-third of 2025 demand but carried 50%-80% premiums that squeezed margins for system integrators and cloud providers. Domestic fabs remain locked at mature nodes ill-suited for AI accelerators and 5G cores, delaying autonomous-vehicle, predictive-maintenance, and precision-medicine initiatives by up to two years. Although RUB 120 billion is earmarked to close the lithography gap, experts caution that sub-7-nanometer mastery may take a decade. The semiconductor pinch therefore limits the upper growth potential of the Russia ICT market.

Persistent Brain Drain of Skilled IT Professionals

Between 2022 and 2025, 70,000-100,000 developers, data scientists, and architects relocated to Armenia, Georgia, Kazakhstan, Serbia, and UAE. Median Moscow salaries for senior machine-learning engineers jumped 45% to RUB 400,000 (USD 4,350) per month, inflating project costs and elongating delivery timelines. Yandex, Sber, and VK recruited 2,500 engineers from Central Asia and Eastern Europe, yet language barriers and visa delays curbed productivity. Universities turned out 120,000 IT graduates in 2025, but industry demand exceeded supply by 200,000 vacancies, forcing companies to offshore coding or adopt low-code platforms. GitHub commits by Russian developers fell 35% over three years, eroding the nation’s influence in open-source ecosystems. Talent shortages thus cap scaling speed for high-complexity deployments within the Russia ICT market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Telecommunications Anchors Revenue, Cloud Gains Share

Communications services accounted for 40.68% of 2025 spending, underscoring the historical weight of mobile voice, broadband, and enterprise connectivity in the Russia ICT market. Growth is flattening as household penetration surpasses 95% and ARPU inches upward only in low single digits. Operators now bundle 5G, IoT, and edge-computing add-ons to defend margins, while regional data-center subsidiaries propel cross-selling into colocation and managed security.

Conversely, IT services are rising at a 4.73% CAGR to 2031, encouraged by Federal Law 242-FZ and the exit of Western hyperscalers. Domestic providers entice workloads with ruble billing, lower latency, and FSB-compliant encryption. Hardware revenues lag because sanctions curtail fresh Xeon and EPYC imports, extending refresh cycles and steering budgets toward maintenance. Software gains momentum as 1C, Kaspersky, and Yandex replace SAP, Oracle, and Microsoft in public-sector stacks, although piracy is 62% among SMEs in 2024, blunts license growth. IT services, including consulting and system integration, benefit as enterprises localize foreign apps and weave disparate domestic stacks, posting 25%-30% revenue growth in 2025. Collectively, this portfolio rotation sustains the Russia ICT market even as legacy telecom revenues plateau.

By Enterprise Size: Large Enterprises Dominate Spending, SMEs Drive Volume

Large enterprises accounted for 61.23% of 2025 revenue, reflecting state-owned banks, energy majors, and telecom operators with multi-year digital-transformation roadmaps. Typical contracts bundle ERP upgrades, cyber hardening, and private-cloud deployments in deals worth USD 5-50 million that lock in support for up to 36 months. Vendor consolidation themes favor ecosystem champions such as Sber and MTS, who leverage cross-business synergies to deliver integrated propositions.

Small and medium-sized enterprises expand at a 3.96% CAGR as subsidized financing offsets capital constraints. The Russia ICT market for SMEs is still modest, yet rapid SaaS adoption is generating a pipeline of repeatable deployments for regional integrators. SMEs experience 25% annual churn, prompting cloud vendors to extend freemium tiers and offer data-migration credits. Federal Law 187-FZ obliges SMEs with public contracts to shift to certified domestic software by 2027, accelerating migrations to Astra Linux, 1C ERP, and MyOffice productivity. Limited in-house data-science talent nudges SMEs toward AutoML offerings from Yandex Cloud and VK Cloud, although concerns linger over proprietary data processed on multitenant stacks.

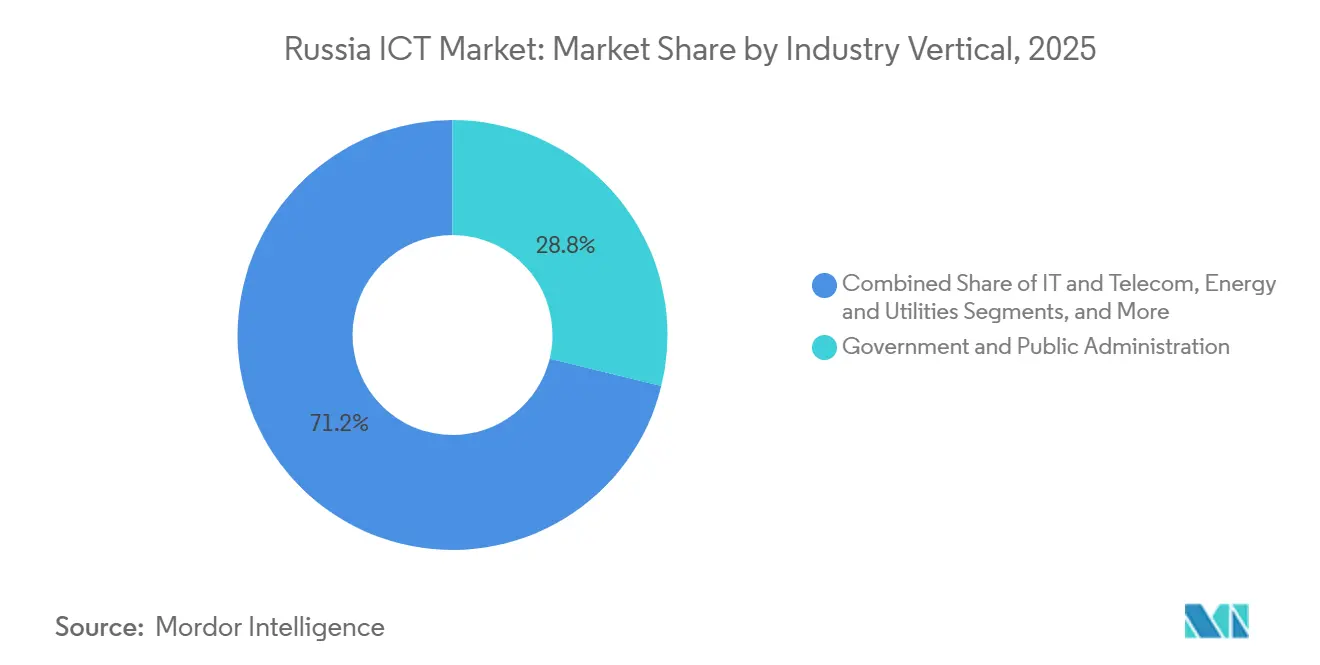

By Industry Vertical: Government Leads, Healthcare Accelerates

Government and public administration accounted for 28.81% of 2025 expenditure, powered by Gosuslugi’s 130 million registered users, who completed 95% of administrative interactions digitally. Every passport renewal, land registry update, and social-benefit payment now flows through paperless channels that cut processing times from 2 weeks to under 2 hours, freeing RUB 180 billion (USD 2.35 billion) annually for reinvestment. Agencies continue to enlarge the Russia ICT market via e-procurement mandates and secure cloud adoption.[3]Government Decree No. 1236, "Import Substitution Requirements," government.ru

Healthcare and life sciences are growing fastest at a 4.87% CAGR, propelled by the rollout of compulsory telemedicine for all regional clinics by late 2025 and the adoption of unified electronic health records across 85 federal subjects. AI-augmented oncology and cardiology pilots increased early detection rates by 15%-20%, underscoring the need for further investment in GPU clusters, PACS integration, and cybersecurity. BFSI remains the third pillar, with banks overhauling core systems, launching open-banking APIs, and processing 70% of Sberbank transactions through mobile channels in 2025. Energy, utilities, retail, and manufacturing are deepening their digital footprints through SCADA upgrades, smart meters, omnichannel e-commerce, and industrial IoT, reinforcing the diversified foundation of the Russia ICT market.

Geography Analysis

The Central Federal District accounted for 29.47% of 2025 revenue, anchored by Moscow’s dense concentration of ministries, Fortune 500 headquarters, and Tier-1 data centers that collectively house 60% of national cloud and colocation capacity. Government contracts tend to cluster in the capital, creating a virtuous cycle that attracts venture funding, technical talent, and multinational R&D labs notwithstanding emigration pressures. The district also hosts most certification bodies, giving home-based integrators a procedural edge in large public tenders.

The Northwestern Federal District, led by St. Petersburg, accounted for 18% of market turnover. The city’s legacy as a software development hub for Yandex, Kaspersky, and JetBrains sustains a vibrant engineering community, even as cross-border IT services trade with the Baltics has receded since the 2022 sanctions. The Volga Federal District captured roughly 14% revenue, buoyed by automotive and aerospace clusters in Kazan, Nizhny Novgorod, and Samara that pilot Industry 4.0 initiatives. Innopolis, Russia’s purpose-built tech city, hosts R&D centers for Kaspersky, Rostelecom, and dozens of AI startups, strengthening regional spillovers.

The Far Eastern Federal District advances at a 4.03% CAGR through 2031, standing out as the fastest geography in the Russia ICT market. Vladivostok markets itself as a digital bridge to Asia-Pacific, backed by incentives for startups on Russky Island and plans for subsea fiber routes to Japan and South Korea. Cold-climate data centers in Norilsk and Yakutsk attract GPU-intensive pilots that achieve power-usage-effectiveness ratios under 1.15 thanks to free-air cooling nine months per year. The Ural and Siberian districts, representing a combined 20% share, leverage mining, metallurgy, and energy enterprises to adopt IoT and predictive-maintenance platforms, although rising electricity tariffs and limited grid redundancy delay several planned data-center builds. Southern and North Caucasian districts collectively form a 7%-8% slice, with agriculture digitalization and rural broadband driving incremental gains.

Competitive Landscape

The top 10 vendors Rostelecom, MTS, MegaFon, Beeline, Yandex, VK, Sber ecosystem businesses, Kaspersky, 1C Company, and Positive Technologies, account for an estimated major share of the Russia ICT market revenue, leaving a long tail of regional integrators and niche software houses to service specialized demand. Vertical integration is the hallmark strategy: MTS bundles connectivity, cloud, IoT, and cybersecurity; Sber turns banking relationships into cross-sells for cloud and AI; Rostelecom fuses fixed-line access with large public-sector integration deals. Price-based competition is fiercest in IaaS, where VK Cloud undercuts rivals by 15%-20% to win smaller workloads.

Technology differentiation pivots on AI performance, data-residency guarantees, and tight integration with domestic ecosystems. YandexGPT surpassed 85% accuracy on Russian-language benchmarks in 2025, outpacing global models trained on multilingual corpora. Sber’s GigaChat specializes in financial language and benefits from vast proprietary transaction data sets. Positive Technologies leverages 24/7 SOC operations to capture managed security contracts that mid-market enterprises lack the resources to staff.

Regulatory moats further shield incumbents. GOST R and FSB certification can take two years and entail stringent audits, deterring new entrants without deep pockets and established compliance teams. Patent filings at Rospatent rose 18% in 2024, with growth in speech recognition, computer vision, and blockchain for identity, signaling continued R&D investment despite sanctions. Looking ahead, white-space opportunities lie in edge computing for manufacturing, AI-powered vertical SaaS for agriculture, and sovereign generative AI services once high-end GPU availability stabilizes.

Russia ICT Industry Leaders

-

Rostelecom PJSC

-

Mobile TeleSystems PJSC (MTS)

-

Kaspersky Lab AO

-

Yandex LLC

-

1C Company LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Rostelecom acquired 51% of DataLine for RUB 18 billion (USD 196 million), adding 25 MW of capacity and becoming Russia’s largest wholesale colocation provider.

- November 2025: MTS unveiled a national IoT platform and signed a five-year deal with Russian Railways for 50,000 predictive-maintenance sensors.

- October 2025: Yandex Cloud committed RUB 12 billion (USD 131 million) to lift GPU capacity by 50% in 2026 and launched a sovereign AI suite.

- September 2025: SberCloud partnered with Yadro to deploy 5,000 domestically assembled x86 servers, achieving 70% local-content compliance.

Russia ICT Market Report Scope

The Russia ICT market encompasses the integration and adoption of various Information and Communications Technologies (ICT), such as big data, mobility, storage, outsourcing, and cloud computing, in the Russian Federation for digitization, digital transformation, and tracking revenue from the sale of technology-related solutions.

The Russia ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security/Cybersecurity, Communication Services), Enterprise Size (Small and Medium-Sized Enterprises, Large Enterprises), Industry Vertical (Government and Public Administration, BFSI, IT and Telecom, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, Other Industry Verticals). The Market Forecasts are Provided in Terms of Value (USD).

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

| Small and Medium-sized Enterprises |

| Large Enterprises |

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Industry Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Industry Verticals | ||

Key Questions Answered in the Report

How large will Russia ICT market spending be by 2031?

Forecasts place outlays at USD 65.96 billion by 2031, reflecting a 3.06% CAGR from 2026.

Which segment is growing fastest inside Russia’s tech landscape?

Cloud and platform services lead with a projected 4.73% CAGR, driven by strict data-localization rules and sovereign AI workloads.

Why is the Far Eastern Federal District attracting ICT investment?

Vladivostok’s subsea cable plans, Russky Island incentives, and cold-climate data-center economics push the district to a 4.03% CAGR through 2031.

What is the biggest barrier to high-performance computing in Russia?

International sanctions that block sub-14-nanometer chips force reliance on older nodes, limiting GPU supply for AI training.

How are SMEs financing digital upgrades?

Government programs subsidize up to 50% of software subscriptions, enabling SMEs to adopt domestic SaaS and cloud offerings at manageable costs.

Which companies dominate managed security services?

Positive Technologies and Kaspersky hold a growing share by operating 24/7 SOCs that mid-market firms cannot staff internally.

Page last updated on: