Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

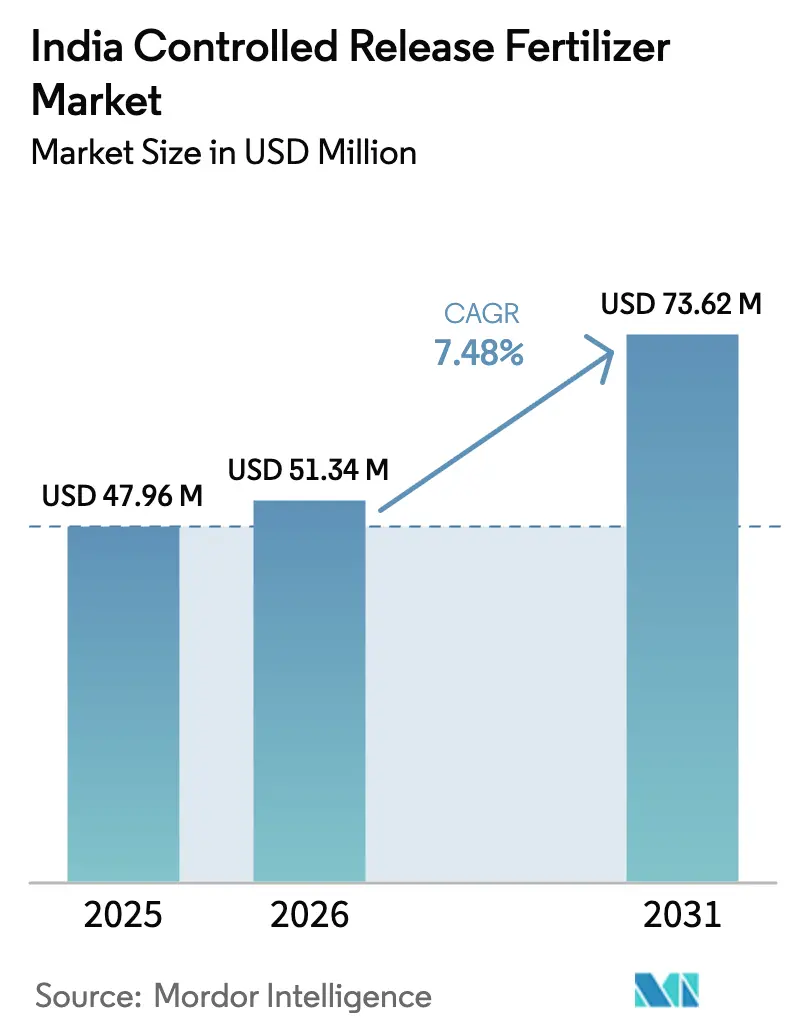

| Base Year Market Size (2025) | USD 47.96 Million |

| Market Size (2026) | USD 51.34 Million |

| Market Size (2031) | USD 73.62 Million |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

India Controlled Release Fertilizer Market Analysis by ���ϲ�����

The India controlled release fertilizer market size is projected to increase from USD 47.96 million in 2025 to USD 51.34 million in 2026 and reach USD 73.62 million by 2031, growing at a CAGR of 7.48% over 2026-2031. Recent expansion reflects a structural pivot in Indian farming as policymakers and large growers seek to raise nitrogen use efficiency, cut groundwater contamination, and lower subsidy outlays. Polymer-coated urea, polymer-sulfur hybrids, and newer bio-based coatings are gaining ground because they synchronize nutrient release with crop uptake and reduce volatilization losses, especially when paired with drip fertigation systems. At the same time, the aggressive rollout of nano urea and the enduring price gap between conventional and specialty products curb demand among the majority of farmers who till less than one hectare. Corporate sustainability scorecards, export-driven residue limits, and proposed rules on polymer residues are reshaping product design, distribution models, and competitive strategy across the India controlled release fertilizer market.

Key Report Takeaways

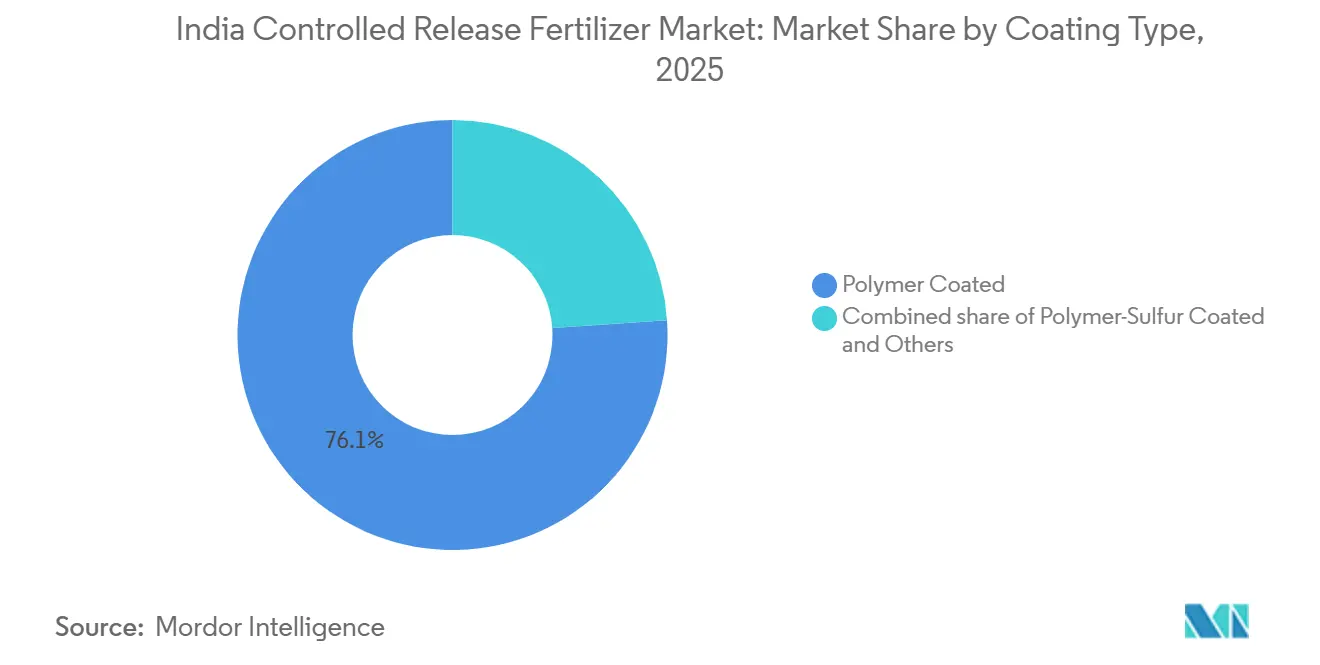

- By coating type, the polymer-coated segment accounted for 76.1% of the India controlled release fertilizer market share in 2025 and is projected to show the fastest CAGR of 7.6% from 2026 to 2031.

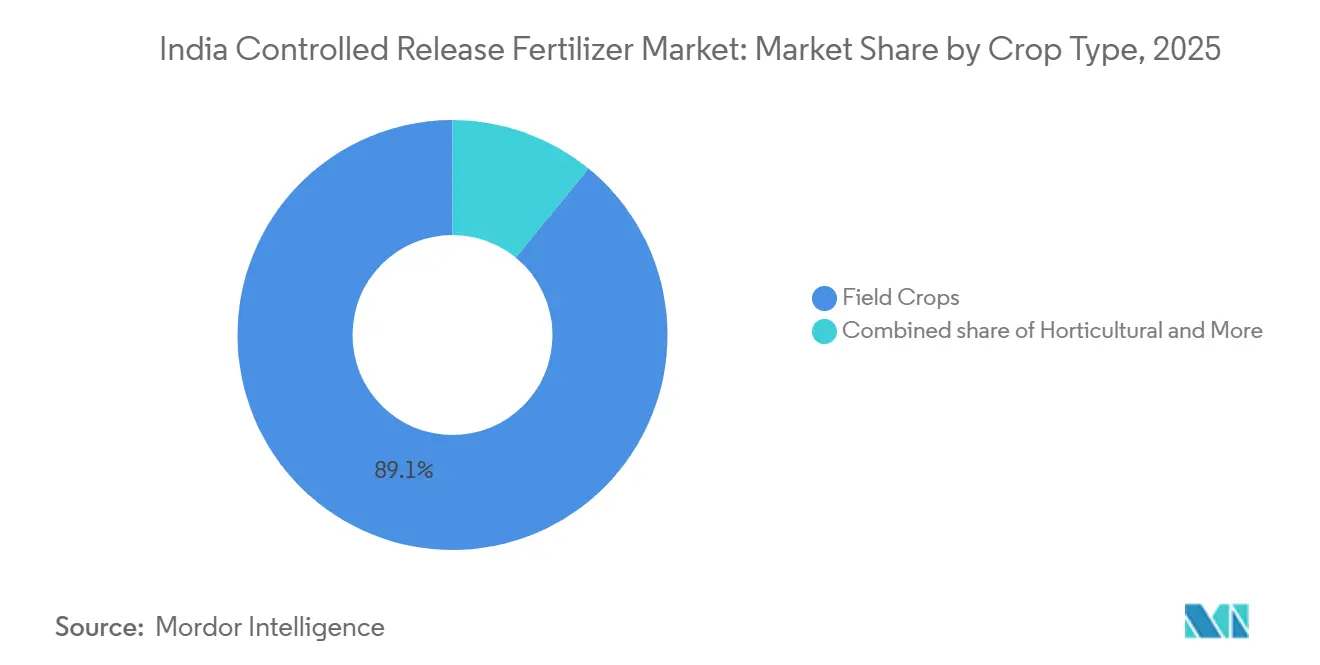

- By crop type, field crops accounted for 89.1% of the India controlled release fertilizer market size in 2025, while horticulture crops are projected to post the fastest 7.7% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Controlled Release Fertilizer Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for neem-coated and specialty fertilizers | +1.2% | Nationwide, strongest in Uttar Pradesh, Madhya Pradesh, Rajasthan | Medium term (2-4 years) |

| High yield and nitrogen use efficiency (NUE) targets | +1.8% | Punjab, Haryana, Uttar Pradesh | Long term (≥4 years) |

| Precision agriculture and fertigation expansion | +2.1% | Maharashtra, Gujarat, Karnataka, Tamil Nadu, Andhra Pradesh | Medium term (2-4 years) |

| Corporate sustainability sourcing mandates | +0.9% | Export clusters in Maharashtra, Karnataka, Gujarat | Short term (≤2 years) |

| Biodegradable-coating push under emerging micro-plastic norms | +0.7% | Nationwide, early adoption in Maharashtra, Karnataka | Long term (≥4 years) |

| Horticulture export clusters adopting controlled release fertilizers | +0.8% | Maharashtra, Karnataka, Gujarat | Short term (≤2 years) |

| Source: ���ϲ����� | |||

Government Subsidies for Neem-Coated and Specialty Fertilizers

Direct Benefit Transfer keeps neem-coated urea affordable by the Maximum Retail Price (MRP) is legally set at a low level. For instance, USD 2.67 per 45 kg bag, excluding taxes and neem-coating charges. Since 2015, every domestic urea bag is neem-coated, familiarizing farmers with extended release concepts and creating a logistics backbone for specialty SKUs[1]Source: Department of Fertilizers, “Nutrient Based Subsidy Scheme,” fert.nic.in. The federal move is amplified by state add-on incentives in Punjab and Haryana that reward the use of biodegradable coatings to curb nitrate seepage into the region’s heavily tapped aquifers. Economic Survey 2025-26 recommends converting blanket support to cash transfers, which could equalize the playing field by 2028. Firms in Uttar Pradesh and Madhya Pradesh bundle soil testing with neem-coated controlled release packs, converting a statutory coating cost into a customer acquisition lever. These visible labor and cost benefits are speeding word-of-mouth diffusion in wheat and rice belts where adoption resistance was historically high.

High Yield and Nutrient Use Efficiency (NUE) Targets

The National Mission for Sustainable Agriculture pegs a nutrient use efficiency target for 2030, a goal embedded in state action plans and backed by rising groundwater nitrate alarms. This linkage pressures local departments to promote controlled release fertilizers that boost nutrient recovery compared with standard prilled urea. Field trials by the Indian Council of Agricultural Research in 2025 showed 12-15% yield gains in basmati rice when polymer-coated urea replaced three split applications. Because the target is written into subsidy scorecards, district officials actively seek technology partners to conduct village-level trials, providing coated products with valuable on-farm validation. Over the next five years, this administrative nudge is anticipated to draw coated fertilizers more deeply into broad-acre crops, which still dominate input volumes. Adoption will accelerate once farmers are compensated for measured efficiency gains rather than per-bag purchases.

Precision Agriculture and Fertigation Expansion

The Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) - Per Drop More Crop (PDMC) component offers subsidies ranging from 45% to 55% for the installation of drip and sprinkler irrigation systems, aiming to enhance water use efficiency. Fertigation kits are effectively paired with controlled-release inputs that prevent emitter clogging and provide nutrients in alignment with daily crop uptake. In Maharashtra's grape-growing region, farmers have reported a 25-30% reduction in fertilizer costs and approximately 20% water savings after adopting coated urea through drip irrigation systems, as per National Commission for Allied and Healthcare Professions (NCPAH) data. Under the "Sahi Fasal" initiative, the Bureau of Water Use Efficiency (BWUE), in collaboration with the Atal Bhujal Yojana and the Small Farmers’ Agribusiness Consortium (SFAC), planned 14 campaigns across seven states for the financial year 2024-25. These campaigns encouraged farmers in water-stressed regions to cultivate less water-intensive and more water-efficient crops while promoting awareness of micro-irrigation techniques for better water management. Equipment manufacturers such as Jain Irrigation and Netafim co-market coated formulations, integrating hardware, agronomy, and financing solutions to alleviate capital constraints for farmers.

Biodegradable-Coating Push Under Emerging Micro-Plastic Norms

Draft Central Pollution Control Board rules propose capping polymer residues in topsoil, pressuring manufacturers to migrate from polyolefins to starch, lignin, or polyhydroxyalkanoate (PHA) coatings. Early adopters among Maharashtra grape growers are already using biodegradable layers to meet the strict EU residue audits, creating premium pricing signals that ripple across the horticulture value chain. The Bureau of Indian Standards adopted ISO 17088 for compostable plastics, providing a certification path even though no India-specific fertilizer standard exists yet. Coromandel International and Deepak Fertilisers pilot PHA-based shells that degrade within 180 days while maintaining release curves. Market leader ICL has beta-tested a tropical-grade bio-polymer that retains a 120-day nutrient release curve, leaving no visible fragments in soil samples, a combination sought by organic-certified fruit exporters. Commercial scale hinges on lowering biopolymer cost premiums.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost versus subsidized urea | -1.5% | Nationwide, acute in Bihar, Uttar Pradesh, Madhya Pradesh, Odisha | Short term (≤2 years) |

| Low farmer awareness and channel reach | -0.9% | Tier-3 mandis in Bihar, Jharkhand, Chhattisgarh | Medium term (2-4 years) |

| Heat-driven release-rate variability | -0.6% | Vidarbha, Marathwada, Rayalaseema, interior Karnataka, Telangana | Medium term (2-4 years) |

| Potential ban on non-degradable polymer residues | -0.7% | Nationwide, early enforcement in Maharashtra, Karnataka | Long term (≥4 years) |

| Source: ���ϲ����� | |||

High Upfront Cost Versus Subsidized Urea

Controlled-release fertilizers are priced at INR 45-75 per kg (USD 0.54-0.90), compared to conventional urea, which costs INR 6 per kg (USD 0.07). This results in a nutrient cost per acre that is seven to twelve times higher for coated fertilizers. Smallholders cultivating less than one hectare find it difficult to justify this premium for low-value cereals. These farmers often depend on seasonal credit and avoid higher upfront costs, even if the long-term economics of coated products are favorable. Cooperative banks remain cautious, as the resale value of specialty inputs is lower, reducing their viability as collateral for microloans. Additionally, nano urea, priced at INR 240 (USD 2.88) for a 500ml bottle, offers comparable nitrogen use efficiency (NUE) improvements, further limiting the demand for coated fertilizers. While sachet packs and pay-per-use models reduce initial costs, they require intensive distribution efforts. Consequently, the adoption of coated fertilizers follows a pyramid structure, with top-tier commercial growers adopting them first and serving as proof points, while broader adoption at the base depends on either increased subsidies or innovative pay-as-you-use delivery mechanisms.

Low Farmer Awareness and Channel Reach

Only a small share of fertilizer retailers in tier-3 markets stock coated SKUs, exposing a weak last-mile push that leaves most growers unaware of the benefits. A 2025 survey by the National Bank for Agriculture and Rural Development found minimum recognition of controlled release advantages in eastern India. Traditional dealers at village haats seldom stock coated fertilizers because turnover is slow. Extension officers receive limited training on release-rate science, leading many to default to established blanket nutrient recommendations. This knowledge gap reduces demand visibility for manufacturers, who in turn hesitate to fund last-mile demos in remote or tribal areas. Absence from Public Distribution System outlets and Krishi Vigyan Kendras deprives farmers of trusted advice. Manufacturers invest in field schools, but long payback periods cloud ROI calculations.

Segment Analysis

By Coating Type: Polymer Dominance Faces Bio-Based Disruption

Polymer-coated products accounted for 76.1% of the India controlled release fertilizer market share in 2025 and are projected to grow at the fastest CAGR of 7.6% from 2026 to 2031. Sales are strongest in drip-irrigated belts of Maharashtra, Gujarat, and Karnataka, where predictable release curves align with fertigation timetables. Draft rules on microplastic residues, however, are accelerating research into starch and Polyhydroxyalkanoate (PHA) coatings that decompose within 180 days. Early pilots signal equivalent agronomic performance but still run above polyolefin cost.

Polysulfur shells serve sulfur-deficient soils in Punjab and Haryana while providing controlled nitrogen, but adoption is narrower due to higher complexity and price. Resin and wax coatings remain niche, supplying turf and ornamental segments that value 9-12-month release and reduced labor inputs. The India controlled release fertilizer market will pivot toward biodegradable materials once cost gaps narrow, and standards clarify acceptable residue levels. Companies with patented bio-coating know-how and supply chain partners for renewable feedstocks stand to capture early mover advantage.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop Type: Horticulture Gains Momentum over Field Staples

Field crops held 89.1% of the India controlled release fertilizer market size in 2025, whereas horticultural crops are on track for the fastest 7.7% CAGR from 2026 to 2031. Large crops such as rice, wheat, and sugarcane blanket more than 125 million hectares nationwide[2]Source: Indian Council of Agricultural Research, “Field Trial Results 2025,” icar.org.in. They rely on coated NPK blends to cut labor and raise nutrient recovery, and government extension trials validate input savings of one application per season in rice. Yet price-sensitized cereal farmers shy away from costly coatings, confining use to basmati rice and high-sucrose cane blocks where premiums support experimentation.

Horticulture crops such as grape, pomegranate, and mango clusters adopt residue-safe nutrition for export acceptance. Higher revenue per hectare allows orchardists to absorb coated price premiums and reap water and labor savings. Turf and ornamental landscaping, though a sliver of tonnage, is expanding around Bengaluru, Hyderabad, and Pune as golf courses and urban municipalities demand long-release blends that cut maintenance cycles. Adoption breadth hinges on aligning product forms with end-use machinery and on demonstrating measurable yield or quality lifts that offset sticker shock. Over time, performance-linked subsidies and sustainability premiums may lift uptake among cereal growers, unlocking the largest volume pool in the India controlled release fertilizer market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

South India is anticipated to dominate the controlled release fertilizers market, driven by export-oriented horticulture and widespread drip irrigation systems[3]Source: Agricultural and Processed Food Products Export Development Authority, “Export Statistics 2024-25,” apeda.gov.in. The adoption of coated fertilizers is supported by state subsidies and compliance with agricultural practices. The region is projected to experience steady growth due to the expansion of micro-irrigation and corporate procurement incentives. Increasing water stress further emphasizes the need for nutrient-efficient and water-saving solutions. Extension agents bundle coated fertilizers with turnkey fertigation kits for greenhouse tomatoes and floriculture, cutting labor while boosting uniformity in this region.

West India holds a significant position in the market, supported by key agricultural regions specializing in crops like grapes, pomegranates, bananas, and cotton. The use of coated fertilizers aligns well with fertigation practices. However, challenges such as accelerated release rates due to extreme heat and limited adoption outside progressive farming areas hinder broader usage. Maharashtra anchors the market, propelled by its 2.5 million hectares of micro-irrigation grid and a thriving export horticulture complex centered in Nashik and Solapur. Grape growers apply coated NPK blends through fertigation tanks to meet strict European residue thresholds, and this practice now accounts for more than a quarter of their total nutrient programs.

The North Indian grain bowl of Punjab, Haryana, and Uttar Pradesh accounts for about thirty percent of national use but remains urea-centric. However, rising groundwater nitrate alerts and an expanding network of satellite crop monitors are prompting policymakers to consider subsidizing coated blends in rice-wheat rotations. North and East India face challenges in adopting controlled release fertilizers due to entrenched urea subsidies and limited awareness. High nitrogen application rates in some areas and fragmented retail networks in others further restrict adoption. Addressing these issues will require policy reforms, improved extension services, and innovations tailored to small landholdings.

Competitive Landscape

The India controlled release fertilizer market displays moderate concentration, with the top five firms such as ICL Group Ltd, Compo Expert GmbH (Grupa Azoty S.A.), Hebei Sanyuanjiuqi Fertilizer Co., Ltd (Hebei Sanyuan Agricultural Group), Zhongchuang Xingyuan Chemical Technology Co., Ltd, and Florikan ESA LLC (New Mountain Capital LLC) captured the majority of the revenue in 2025. ICL Group Ltd and Compo Expert GmbH (Grupa Azoty S.A.), New Mountain Capital (Florikan), rely on embedded agronomists in horticulture hubs to prove water-saving and yield premiums, transforming fertilizers from commodities into advisory-backed solutions. Coromandel International, Deepak Fertilisers, and Gujarat State Fertilizers and Chemicals leverage neem-coating expertise to hybridize mandatory and specialty attributes, cutting price gaps while tapping the same subsidy bucket.

Innovation centers on biodegradable coatings and temperature-responsive shells. Deepak Fertilisers commissioned a new line in Taloja with IIT Bombay technology designed to withstand 45 °C soil heat without premature discharge. Gujarat State Fertilizers and Chemicals licensed Florikan’s staged release system, aiming at customized crop-climate fits that promise differentiated agronomic value. Indian Institute of Science and IIT Kharagpur patent lignin and Polyhydroxyalkanoate (PHA) coatings, positioning domestic players to ride forthcoming residue rules. Meanwhile, Indian Farmers Fertiliser Cooperative’s nano urea offers a low-cost Nitrogen Use Efficiency (NUE) path, forcing coated producers to sharpen value propositions or bundle with finance and hardware.

Strategic partnerships are proliferating. PepsiCo India entered into a partnership with N-Drip in 2022, a producer of gravity-powered micro-irrigation systems, to support Indian farmers in improving water efficiency. This initiative is part of a global collaboration between PepsiCo and N-Drip, targeting enhanced water efficiency across 10,000 hectares. Nutrien gives specialized support for grape and pomegranate growers with soil analytics, nutrient-focused farm management solutions, and fertigation design. Such integrative moves illustrate how market leaders transcend product sales, embedding themselves in the broader precision agriculture ecosystem of the India controlled release fertilizer market.

India Controlled Release Fertilizer Industry Leaders

ICL Group Ltd

Zhongchuang Xingyuan Chemical Technology Co., Ltd

Compo Expert GmbH (Grupa Azoty S.A.)

Florikan ESA LLC (New Mountain Capital LLC)

Hebei Sanyuanjiuqi Fertilizer Co., Ltd (Hebei Sanyuan Agricultural Group)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Coromandel International introduced a new family of biodegradable polymer-coated controlled-release fertilizers for horticultural crops in Maharashtra and Karnataka. Developed in collaboration with a domestic agri-tech startup, the range addresses microplastic concerns and enhances nutrient use efficiency for high-value fruit and vegetable growers. The launch aligns with emerging rules on sustainable inputs and will help the company expand its reach in export-oriented clusters.

- July 2025: IFFCO rolled out pilot trials of its AI-enabled controlled-release fertilizer advisory platform in Uttar Pradesh and Madhya Pradesh. The digital tool blends soil health diagnostics with crop-specific nutrient modeling to generate field-level application schedules, advancing the cooperative’s plan to drive specialty fertilizer adoption through precision farming and real-time decision support.

- August 2024: The government is promoting bio-manufacturing through the BioE3 Policy, aimed at encouraging the local production of specialty fertilizers. Additionally, the Fertiliser Control Order (FCO) has been revised to incorporate liquid and nano-fertilizers.

India Controlled Release Fertilizer Market Report Scope

Controlled Release Fertilizers (CRFs) are granular fertilizers coated with polymers, resins, or sulfur, designed to release nutrients gradually over an extended period, up to 18 months. These fertilizers are formulated to align nutrient release with plant uptake requirements, primarily influenced by soil temperature and moisture, thereby minimizing leaching and volatilization.

The India controlled release fertilizer market report analyzes the industry based on coating type and crop type. By coating type, the market covers polymer coated, polymer-sulfur coated, and other variants. By crop type, it includes field crops, horticultural crops, and turf and ornamental. Market estimates and forecasts are presented in terms of value (USD) and volume (metric tons).

By Coating Type

| Polymer Coated |

| Polymer-Sulfur Coated |

| Others |

By Crop Type

| Field Crops |

| Horticultural Crops |

| Turf and Ornamental |

| By Coating Type | Polymer Coated |

| Polymer-Sulfur Coated | |

| Others | |

| By Crop Type | Field Crops |

| Horticultural Crops | |

| Turf and Ornamental |

Need A Different Region or Segment?

Customize Now

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Urea & Complex

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

���ϲ����� follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF