Hong Kong Credit Cards Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

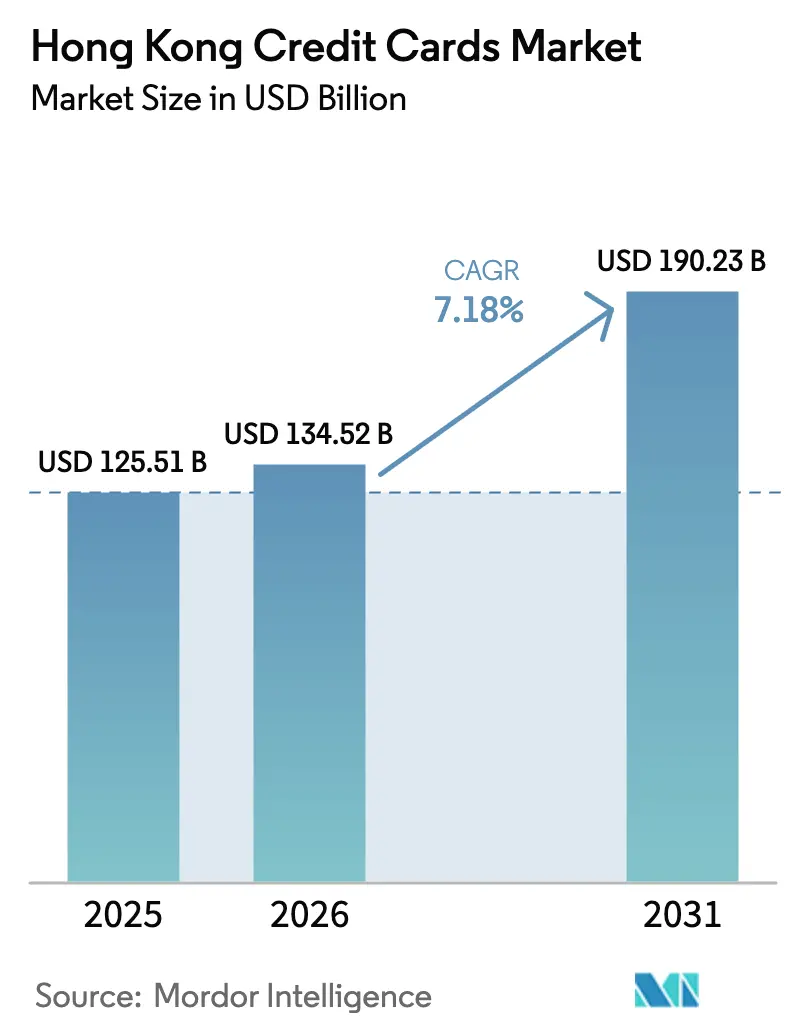

| Base Year Market Size (2025) | USD 125.51 Billion |

| Market Size (2026) | USD 134.52 Billion |

| Market Size (2031) | USD 190.23 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

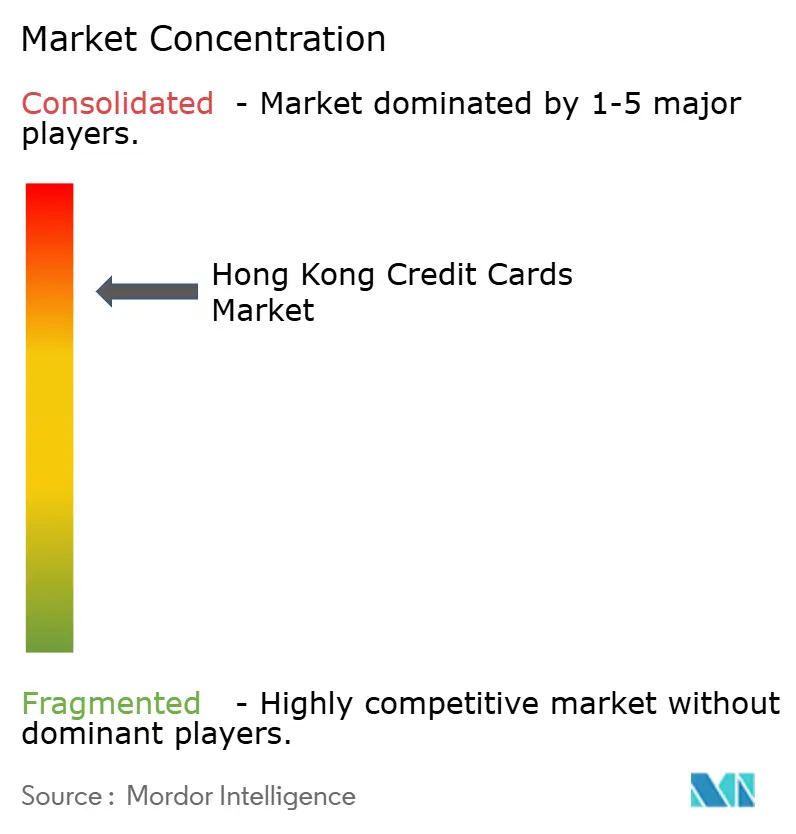

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Credit Cards Market Analysis by ���ϲ�����

The Hong Kong Credit Cards Market size is projected to be USD 125.51 billion in 2025, USD 134.52 billion in 2026, and reach USD 190.23 billion by 2031, growing at a CAGR of 7.18% from 2026 to 2031.

The growth path reflects a shift from a recovery phase to a utility-led expansion anchored in contactless transit tokenization across the city’s rail network, which has expanded open-loop acceptance for Visa, Mastercard, and UnionPay at more than 2,400 upgraded gates. Eight licensed virtual banks are scaling instant-issuance and digital-first card experiences that widen access for younger and digitally active cohorts while increasing competitive pressure on incumbent issuers. Cross-boundary retail usage is set to deepen as Hong Kong’s Faster Payment System links with the mainland’s IBPS under Payment Connect and as the HKMA expands the cross-boundary eCNY pilot with local top-up through participating banks. At the same time, issuers face higher compliance costs due to stepped-up anti-fraud safeguards and device-bound authentication standards, which shape product economics and encourage a pivot toward experiential rewards and premiumization.

Key Report Takeaways

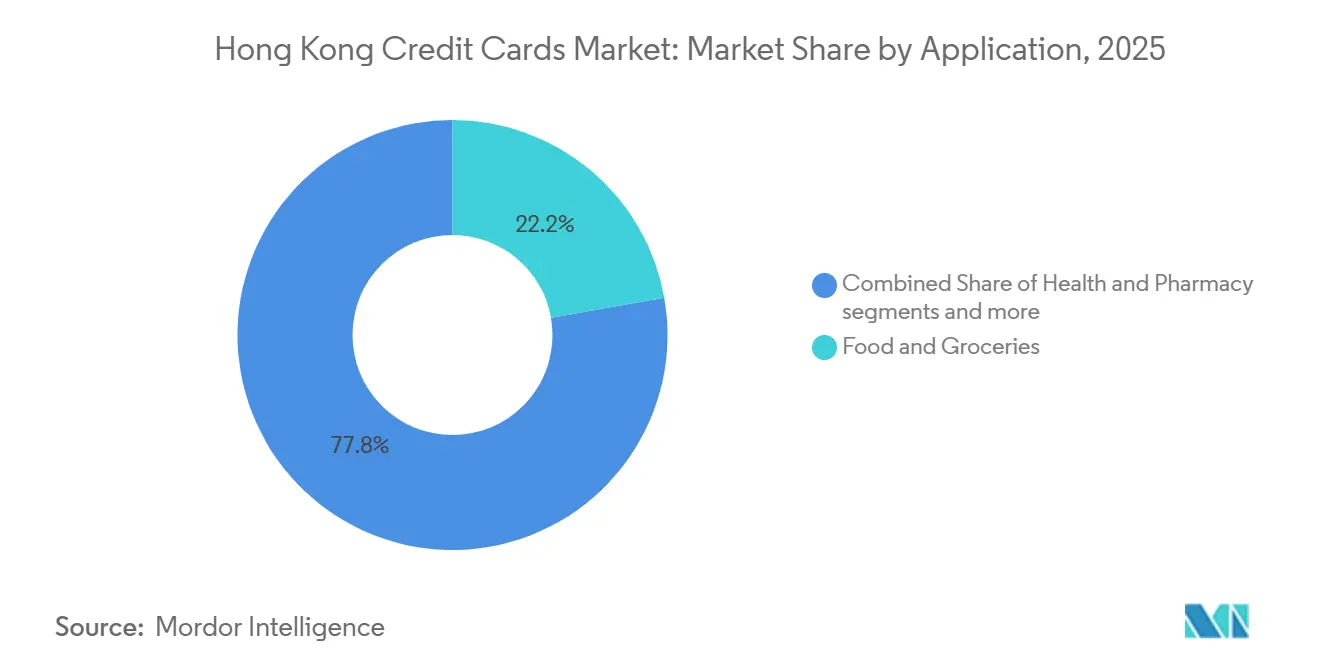

- By application, food & groceries led with 22.23% of the Hong Kong credit cards market share in 2025, while travel & tourism is projected to grow at a 9.82% CAGR through 2031.

- By card type, general-purpose credit cards held 87.82% of the Hong Kong credit cards market share in 2025, and specialty & other credit cards are forecast to expand at a 7.91% CAGR to 2031.

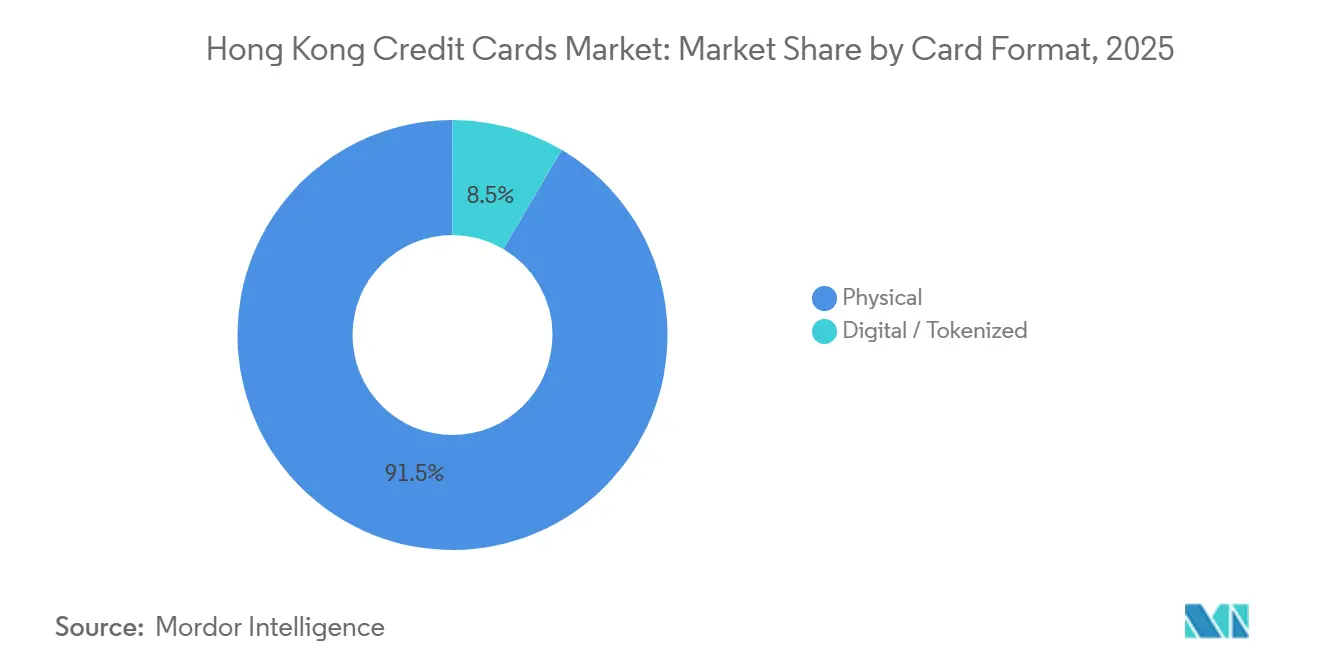

- By card format, physical cards accounted for 91.51% of the Hong Kong credit cards market share in 2025, while digital/tokenized cards are set to grow at a 10.13% CAGR through 2031.

- By provider, Visa commanded 51.32% of the Hong Kong credit cards market share in 2025, and other providers are projected to post an 8.41% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hong kong contributes to a system defined not by any single country or region but by the interaction of many. The global credit cards market data by ���ϲ����� represents that combined structure.

Hong Kong Credit Cards Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing card penetration across consumer segments | +1.2% | Hong Kong-wide, with spillover to Macau via GBA integration | Medium term (2-4 years) |

| Consumer preference for cashback and rewards | +1.5% | Hong Kong core, extending to mainland GBA cities for cross-border spend | Short term (≤ 2 years) |

| Government initiatives driving digital payment adoption | +0.8% | Hong Kong domestic, pilot zones in Shenzhen for FPS-IBPS linkage | Short term (≤ 2 years) |

| Virtual bank cards are expanding financial accessibility | +1.3% | Hong Kong retail, with early gains among the 18-35 demographic in Kowloon and NT | Medium term (2-4 years) |

| Cross-border spending growth in the Greater Bay Area | +1.6% | Hong Kong–Guangdong–Macau corridor, concentrated in Shenzhen and Guangzhou | Long term (≥ 4 years) |

| ���ϲ�����less transit tokenization is boosting credit usage | +0.8% | Hong Kong Island, Kowloon, New Territories | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Increasing Card Penetration across Consumer Segments

Hong Kong’s large installed base of credit cards strengthens the usage foundation and converts the market into a replacement and activation story rather than a pure acquisition race, as total cards in circulation reached 25.08 million in Q3 2025 with a 23.6% year-on-year jump that reflects renewed issuance and multi-card strategies. [1]Hong Kong Monetary Authority, “Statistics of Payment Cards Issued in Hong Kong for Third Quarter 2025,” Hong Kong Monetary Authority, hkma.gov.hk. Consumers often optimize daily categories across different products, such as grocery co-brands with elevated rebates and overseas travel cards with enhanced miles accrual, which supports sustained transaction growth per user. The strong base is also reinforced by contactless acceptance in transit, which converts habitual micro-payments into card-eligible events on a scale. As a result, issuers focus on activation, category-specific value, and cross-sell into premium or lifestyle propositions to differentiate in a dense portfolio landscape. This installed-base dynamic underpins steady growth in the Hong Kong credit cards market through improved engagement rather than broad-based new-to-card expansion.

Consumer Preference for Cashback and Rewards

Rewards-led models continue to anchor loyalty and encourage higher spending per card, with Asia Miles-linked and cashback propositions positioned as everyday value mechanics rather than episodic promotions. Mox Credit’s structure of 1 Asia Mile per USD 0.51 (HKD 4.00) spent and 0% foreign exchange fees on overseas and online transactions aligns with cross-border usage patterns and reduces friction for travel-focused users[2]Mox Bank, “Mox Credit Card Introduces Best-in-town Offer,” Mox Bank, mox.com. Aggregator platforms like ShopBack further layer incentives over issuer rewards, which condition cardholders to compare offers and channel more wallet share through cards when the combined value stack is superior to cash or bank-transfer alternatives. Premium cards such as HSBC Privé elevate non-price differentiation through curated access and experiences, which resonates with affluent users and deepens stickiness without relying solely on high rebate burn. These features collectively sustain momentum in the Hong Kong credit cards market by blending everyday utility with experiential appeal that is difficult for substitutes to replicate at scale.

Greater Bay Area Cross-Border Spend Tailwind

Cross-boundary flows are becoming more seamless due to institutional linkages and wallet interoperability, which expands the addressable pool for Hong Kong-issued credentials in everyday and travel contexts. The HKMA’s cross-boundary eCNY pilot expansion allows Hong Kong residents to open and top up wallets locally, enabling small-value cross-border transactions that complement card-based usage in the Greater Bay Area. Local banks are integrating RMB services that align with this cross-border usage pattern, which supports future card-linked and wallet-linked experiences for commuters and travelers between Hong Kong and Guangdong. As awareness rises and acceptance networks mature across retail and transit, more Hong Kong consumers combine cards with other interoperable options, which increases the overall frequency of digital payments. This cross-border normalization supports multi-currency and travel-linked propositions, and it strengthens the long-term growth profile of the Hong Kong credit cards market.

���ϲ�����less Transit Tokenization Boosts Micro Ticket Credit Use

Open-loop contactless across heavy rail, alongside payment-enabled devices, turns daily commutes into consistent card-eligible micro-transactions, which raises transaction counts per active card. Visa’s targeted mobility promotions, such as taxi cashback across thousands of vehicles, further extend transit-linked acceptance and build everyday familiarity with tapping cards and devices. [3]Visa, “Visa Powers Smart Mobility for Hong Kong Travelers with Taxi Promotion,” Visa, visa.com.hk. Octopus continues to process millions of daily taps at wide coverage points, which ensures commuters have multiple contactless options, while also keeping the overall environment NFC-first. The combination of open-loop gates, curated mobility incentives, and established closed-loop behavior keeps contactless at the center of the city’s payment habits, which sustains card usage in low-ticket, high-frequency contexts. This embedded transit utility is a structural support for the Hong Kong credit cards market, since it promotes habitual tapping and routine activation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin squeeze in a saturated issuer landscape | -0.9% | Hong Kong-wide, acute among mid-tier issuers lacking scale | Short term (≤ 2 years) |

| Higher rates and household debt tighten underwriting | -0.7% | Hong Kong domestic, ripple effects in GBA cross-border lending pilots | Medium term (2-4 years) |

| Rising cyber-fraud drives compliance cost | -1.1% | Global, with Hong Kong as a financial hub | Short term (≤ 2 years) |

| FPS and e-wallet substitution cannibalize low-value spend | -0.6% | Hong Kong retail, especially micro-merchants and transit | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Margin Squeeze in a Saturated Issuer Landscape

Competition is intense across 28 retail banks and multiple virtual banks, which compresses margins as issuers balance acquisition incentives with sustainable unit economics. TransUnion reported a decline in credit card originations while consumer enquiries dipped modestly, indicating that lenders exercised greater selectivity as risk costs rose, which weighs on portfolio growth from new accounts. At the same time, stepped-up anti-fraud controls and real-time suspicious account alerts require material investment in systems and operations that can pressure smaller issuers. As issuers face higher compliance costs, more portfolios pivot to experience-led and partnership-led differentiation rather than pure cashback escalation to keep economics within target ranges. Funding flows to digital players also influences competitive posture, as new capital often supports product expansion and customer acquisition at lower short-term margins.

Higher Rates and Household Debt Tighten Underwriting

Credit card receivables rose into year-end 2025, yet delinquency metrics remained low, which suggests lenders prioritized transactors and tightened underwriting standards for revolvers in a high-rate backdrop. The mix shift toward transactors reduces interest income per card and heightens dependence on merchant discount revenue, which intensifies the search for fee-based value and premium features. Bank of China’s disclosures showed a higher nonperforming loan ratio in mainland credit cards, which underscores the need to balance growth and asset quality in cross-border consumer finance. TransUnion’s data on subprime originations points to a bifurcation where riskier segments see activity even as prime segments saturate, which raises the importance of precise underwriting and early-warning controls. This environment moderates expansion within the Hong Kong credit cards market as issuers emphasize portfolio resilience over rapid account growth.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Food & Groceries Anchored by Everyday Rewards, Travel & Tourism Accelerating on Zero FX Propositions

Food & Groceries accounted for 22.23% of spending in 2025 within the Hong Kong credit cards market size, supported by supermarket co-brands and linked auto-reload that encourage routine card usage in daily purchases. Retailer partnerships like Hang Seng enJoy offer elevated rebates across major chains, which reinforce habitual card-on-file behavior for weekly baskets and pantry restocking. Health & Pharmacy purchases benefit from targeted rebates and category-inclusion rules, which sustain prescription and wellness through cards when eligible. Restaurants & Bars uptake is supported by group dining offers and weekday incentives, while tokenized wallets on mobile devices streamline in-venue payments for higher cadence. Consumer Electronics and Media & Entertainment remain episodic but are aided by one-tap checkout and card-on-file capabilities in app stores and streaming services.

Travel & Tourism is the fastest-growing application with a 9.82% CAGR over 2026-2031, powered by zero FX card propositions and miles accrual that improve the economics of cross-border transactions. Mox Credit’s 1 Asia Mile per USD 0.51 (HKD 4.00), combined with 0% foreign exchange fees, converts overseas purchases into rewards currency more efficiently, which stimulates card use in travel and e-commerce across borders. Open-loop transit acceptance on the MTR has also normalized tapping with global network credentials, which builds comfort with contactless usage and supports portability for travelers. Other Applications, such as utilities, insurance, and government services, contribute steady volumes when acceptance is enabled, though issuers continue to calibrate rebate economics in lower-margin bill-pay categories. Combined, these category dynamics sustain recurring usage and help diversify the Hong Kong credit cards market across staples, discretionary, and travel-linked spends.

By Card Type: General-Purpose Dominance with Specialty Growth Led by Travel and Digital First Propositions

General-purpose credit cards held 87.82% share in 2025 within the Hong Kong credit cards market, reflecting universal acceptance and incumbent distribution strength, while Specialty & Other Credit Cards are projected to grow at 7.91% CAGR to 2031. General-purpose portfolios remain the default for payroll-linked and household spending due to the breadth of acceptance and stable benefits. Specialty cards differentiate on targeted value propositions such as premium experiences or travel benefits, which help issuers segment customers and capture higher spending per account. Airline and travel-linked co-brands tie cardholders into loyalty ecosystems with flexible redemption and companion travel privileges, which support durable usage among frequent travelers. These patterns position specialty products as growth drivers in niches where general-purpose value is less distinctive.

Virtual banks amplify specialty-led growth with digital-first mechanics that improve the user experience for online checkout and subscription commerce, supported by tokenization and numberless card designs. Multi-currency and zero FX features appeal to cross-border freelancers and frequent travelers, which shifts spend from cash and bank transfers to card credentials that deliver rewards and protections. Issuers also use premium experiences and concierge access to retain affluent segments, which sustains high average ticket sizes and supports fee income. The net effect is that while general-purpose portfolios anchor the base, specialty growth elevates the overall mix of the Hong Kong credit cards industry toward more differentiated propositions. This balance supports steady expansion in the Hong Kong credit cards market as issuers align offers with distinct lifestyle and travel profiles.

By Card Format: Physical Persistence with Rapid Tokenized Adoption in High-Frequency Use Cases

Physical cards represented 91.51% of circulation in 2025 in the Hong Kong credit cards market, while digital/tokenized formats are expected to grow at a 10.13% CAGR through 2031. Open-loop contactless acceptance across heavy rail validates that cards and tokenized devices are interoperable at scale, which expands the practical utility of digital wallets in daily routines. Octopus’s entrenched role in transit and retail reinforces contactless habits that benefit both closed-loop and open-loop credentials, while preserving consumer choice on speed and convenience. As issuers embed tokenization and numerous card features, consumers gain stronger in-app controls that increase trust for card-not-present transactions. These patterns point to multi-format coexistence where physical cards remain the default backup while mobile tokens scale in everyday tap environments.

Digital-first issuance is accelerating, with HSBC enabling immediate online spending for approved customers through virtual credentials, which reduces time-to-first transaction and boosts early engagement. ZA Bank’s Click to Pay implementation, backed by Visa Token Service, demonstrates improved authorization and lower fraud in the region, which underscores the risk-reduction benefits of tokenization for issuers and merchants. As more daily acceptance moves to contactless and in-app interfaces, tokenized formats are poised to capture a larger share of active credentials, especially among younger cohorts. Over the forecast period, physical and tokenized formats together will continue to advance the Hong Kong credit cards market by pairing reliability with enhanced security and convenience. This dual-track evolution supports the long-term expansion of the Hong Kong credit cards market size across online and offline channels.

By Provider: Visa’s Mobility Push Meets Premium and B2B Differentiators from Other Networks

Visa held 51.32% provider share in 2025 in the Hong Kong credit cards market, supported by a first-mover advantage in MTR open-loop contactless acceptance and targeted mobility promotions such as taxi cashback across thousands of vehicles. Mastercard scaled transit acceptance alongside Visa in heavy rail and leaned into lifestyle and entertainment access with issuer partners, which provides an experiential alternative to pure cashback competition. American Express concentrated on corporate and commercial solutions, with survey data showing that nearly half of Hong Kong businesses prioritized online fraud prevention, which supports the uptake of cards with stronger expense controls. Across providers, contactless ubiquity and tokenization standards support authorization rates and risk outcomes, which help all networks expand everyday use cases in the Hong Kong credit cards market.

Other Providers, including UnionPay and American Express, are projected to grow at an 8.41% CAGR through 2031, helped by deepening GBA linkages, commercial card use cases, and expanding tokenization in e-commerce. Issuer partnerships for multi-currency and business-spend controls create targeted pathways for growth outside mass consumer cashback, especially in cross-border procurement and travel. Provider strategies in Hong Kong also emphasize merchant acceptance breadth, consistent tap performance in transit, and integration with mobile wallets, which sustain card-based rails even as alternatives scale. Together, these moves balance share defense by incumbents with growth from specialized propositions, which supports a healthy competitive rhythm across the Hong Kong credit cards market. This competitive configuration aligns with steady provider diversification alongside Visa’s established position in the Hong Kong credit cards market.

Geography Analysis

Hong Kong remains the core of the Hong Kong credit cards market, with domestic transactions totaling USD 22.27 billion (HKD 173.3 billion) in Q3 2025, while overseas transactions accounted for USD 13.25 billion (HKD 103.10 billion), which underscores the importance of local spend even as cross-border usage grows. The market’s daily acceptance backbone runs through contactless transit and broad merchant coverage, which supports routine activation and shortens the path to habitual usage across categories. Open-loop and closed-loop systems coexist in the city, and this multi-rail environment increases digital payment familiarity as users alternate between different tap and online flows. The interplay of local acceptance, cross-border travel, and online commerce thus anchors the Hong Kong credit cards market size and supports a balanced growth mix across use cases.

Greater Bay Area linkages are becoming more relevant to the Hong Kong credit cards market as Payment Connect enables instant small-value cross-boundary remittances, which increases consumer comfort with digital flows across Hong Kong and Guangdong. The expansion of the cross-boundary eCNY pilot allows Hong Kong residents to open and top up eCNY wallets locally through participating banks, which introduces another interoperable channel for everyday and travel-linked payments in the region. As more GBA residents commute and travel across borders, multi-currency and hospitality-linked card features become a practical lever for issuers to capture incremental spend from frequent crossers. The combined effect is a gradual widening of addressable cross-border usage for Hong Kong-issued cards that complements domestic activation.

Transit and mobility also shape geographic usage patterns, since contactless acceptance across heavy rail and taxi fleets makes tapping a city-wide norm, which supports spending across Hong Kong Island, Kowloon, and the New Territories. Issuer promotions tied to mobility and lifestyle facilitate everyday activation that then extends to cross-border e-commerce and travel. As digital rails deepen across the GBA, tokenized cards and wallets gain further relevance for both local and regional transacting, which underpins steady geographic diversification. These developments strengthen the resilience of the Hong Kong credit cards market by anchoring demand locally while opening credible cross-border avenues for growth.

The credit cards market is analyzed by ���ϲ����� across multiple other geographies, with in-depth regional assessments available for Europe. This is complemented by country-specific insights for Japan, Israel, and Canada, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Hong Kong credit cards market features a concentrated core of incumbent issuers complemented by virtual banks and specialized providers, with competition centered on digital onboarding, rewards design, and security standards. Incumbents maintain scale advantages through established portfolios and broad acceptance, while new entrants pursue app-centric experiences and targeted offers to win share. Strategic moves include premiumization through experiential access, where HSBC Privé targets affluent users with curated benefits that reinforce high average spends. Networks are also deepening everyday relevance, with Visa’s taxi promotion extending contactless usage beyond rail to road transport across large fleets. Together, these moves show a dual strategy of mass-market activation and segment-led differentiation that shapes competitive outcomes in the Hong Kong credit cards market.

Virtual banks are accelerating feature velocity and adoption through tokenization, numberless designs, and integrated FX and investing, which expand addressable use cases and build deeper engagement. ZA Bank’s Click to Pay implementation uses network tokenization to reduce fraud risk and increase approval rates for e-commerce transactions, which benefits both cardholders and merchants. WeLab is investing to grow multi-currency debit and FX at cost price, which provides a card-linked alternative to foreign currency fees and encourages overseas spending. Commercial cards are also advancing, as fintech issues bring instant virtual issuance and expense automation to SMEs that want operational control and FX hedging in one stack. This mix of consumer and commercial innovation supports steady diversification within the Hong Kong credit cards market.

Regulatory initiatives play an important shaping role, with the HKMA and PCPD introducing joint examinations and expanding suspicious account alerts, which lifts the baseline for fraud resilience and data protection across issuers. Issuers that move early on device-bound authentication and tokenization stand to reduce fraud and improve approval rates, which reinforces trust in online card usage. Mobility-linked acceptance also remains a shared priority since contactless experiences in transit and taxis prime users to tap cards and devices across other retail categories. These factors combine to maintain an oligopolistic core with active challengers, which supports both stability and incremental innovation in the Hong Kong credit cards market.

Hong Kong Credit Cards Industry Leaders

HSBC

Citibank (Hong Kong) Limited

Bank of China (Hong Kong) / BOC Credit Card

Standard Chartered Bank (Hong Kong) Limited

American Express International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: WeLab Bank partnered with Mastercard to launch the WeLab Global Wallet Debit Card, supporting exchange of up to 11 major currencies, cost-price FX with zero mark-up or hidden fees, and a 0.4% cash rebate on global spending. The card enables local currency withdrawals from JETCO ATMs in Hong Kong and Mastercard ATMs abroad, and overseas spending with the card tripled within a month of launch. This move targets cross-border use cases that previously faced friction from foreign currency transaction fees.

- July 2025: Visa introduced a campaign promoting its "Tap to Pay" feature for taxi fares, offering a USD 1.29 (HKD 10.00) rebate on eligible rides exceeding (USD 12.85+) HKD 100.00. This initiative supports contactless payment adoption, expands merchant coverage, and highlights a tenfold increase in taxi acceptance since 2022.

- July 2025: Mainland and Hong Kong authorities launch Payment Connect to link the mainland’s IBPS with Hong Kong’s FPS, enabling real-time cross-boundary remittances using recipient mobile or account numbers. The first transaction took place in Shenzhen, and the initiative supports instant small-value remittances that are expected to broaden cross-border digital usage. The linkage expands consumer familiarity with interoperable digital rails in the Greater Bay Area.

- May 2025: ZA Bank became the first issuer in Hong Kong and Asia Pacific to enable Click to Pay with Visa as a standard card feature. The tokenized checkout experience, powered by Visa Token Service, reduces fraud and increases authorization rates on average relative to PAN-based card-not-present transactions. Cardholders can enroll through the ZA Bank app, which simplifies e-commerce checkout and strengthens security.

Hong Kong Credit Cards Market Report Scope

A credit card is a payment instrument issued by financial institutions, such as banks or credit card companies, enabling users to make purchases and access credit within a predefined limit. In Hong Kong, its functionality mirrors global standards.

The Hong Kong credit cards market report is segmented by application (food & groceries, health & pharmacy, restaurants & bars, consumer electronics, media & entertainment, travel & tourism, other applications), card type (general-purpose credit cards, specialty & other credit cards), and card format (physical, digital/tokenized), provider (visa, mastercard, and more). The market forecasts are provided in terms of value (USD).

| Food & Groceries |

| Health & Pharmacy |

| Restaurants & Bars |

| Consumer Electronics |

| Media & Entertainment |

| Travel & Tourism |

| Other Applications |

| General-Purpose Credit Cards |

| Specialty & Other Credit Cards |

| Physical |

| Digital / Tokenized |

| Visa |

| Mastercard |

| Other Providers |

| By Application | Food & Groceries |

| Health & Pharmacy | |

| Restaurants & Bars | |

| Consumer Electronics | |

| Media & Entertainment | |

| Travel & Tourism | |

| Other Applications | |

| By Card Type | General-Purpose Credit Cards |

| Specialty & Other Credit Cards | |

| By Card Format | Physical |

| Digital / Tokenized | |

| By Provider | Visa |

| Mastercard | |

| Other Providers |

Key Questions Answered in the Report

What is the growth outlook and size for the Hong Kong credit cards market by 2031?

The Hong Kong credit cards market size was USD 125.51 billion in 2025 and is forecast to reach USD 190.23 billion by 2031 at a 7.18% CAGR over 2026-2031.

Which application leads card spending in Hong Kong, and which one is growing fastest?

Food & Groceries led with 22.23% of 2025 spending, while Travel & Tourism is the fastest-growing application at a 9.82% CAGR through 2031.

How are tokenized and virtual cards changing usage patterns in Hong Kong?

Tokenized cards and Click to Pay improve security and authorization in e-commerce, while virtual issuance enables immediate spending and faster activation, supporting daily adoption in transit and retail.

Which providers are setting the pace in mobility and premium propositions?

Visa expanded mobility acceptance with taxi promotions and open-loop transit, while premium co-branded propositions such as HSBC Privé emphasize experiential benefits to retain affluent segments.

What regulatory measures most affect card issuers in Hong Kong in 2026?

Joint HKMA and PCPD examinations on fraud and data protection, plus expanded suspicious account alerts, increase compliance requirements and encourage tokenization and device-bound authentication.

How do Greater Bay Area initiatives influence credit card usage by Hong Kong residents?

Payment Connect links FPS with IBPS for instant cross-border remittances, and the expanded eCNY pilot allows local top-ups, together broadening cross-border digital usage that complements card-based spending.

Page last updated on: