Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

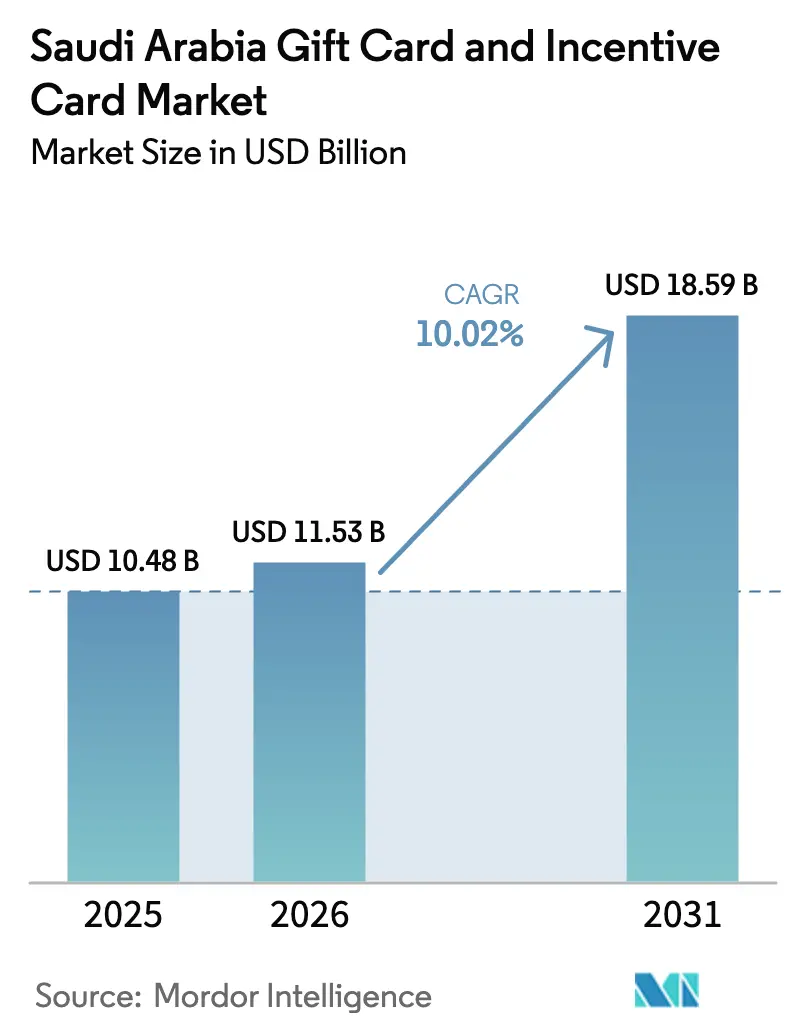

| Base Year Market Size (2025) | USD 10.48 Billion |

| Market Size (2026) | USD 11.53 Billion |

| Market Size (2031) | USD 18.59 Billion |

| Growth Rate (2026 - 2031) | 10.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Gift Card And Incentive Card Market Analysis by ���ϲ�����

The Saudi Arabia Gift Card And Incentive Card Market size is expected to increase from USD 10.48 billion in 2025 to USD 11.53 billion in 2026 and reach USD 18.59 billion by 2031, growing at a CAGR of 10.02% over 2026-2031.

Policy execution under Vision 2030’s Financial Sector Development Program continues to prioritize cashless transactions and modern rails, supporting open API connectivity and real-time use cases for prepaid products at a national scale. Corporate procurement frameworks linked to the Regional Headquarters Program and labor localization policies steer budgets to digital incentives that are faster to issue, simpler to account for, and easier to redeem across physical and online channels. Online distribution grows on the back of established consumer protections under the E-Commerce Law and the Ministry of Commerce’s Maroof program, which reduces friction for acquiring and redeeming gift codes across regulated storefronts. Bank-grade API ecosystems and improved KYC procedures compress approval timelines, promote reliable settlement, and expand interoperability, which collectively support new prepaid experiences inside loyalty programs and checkout flows.

Key Report Takeaways

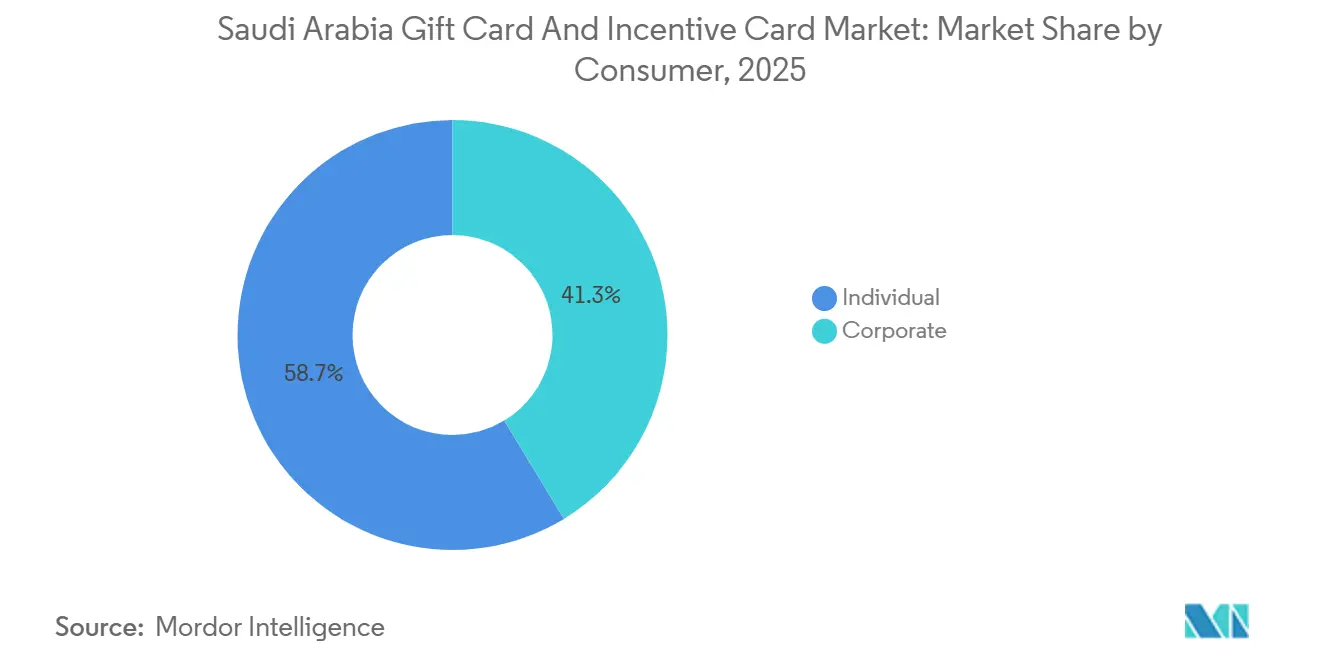

- By consumer, corporate buyers held 41.33% of the Saudi Arabia gift card and incentive card market share in 2025, and the SME sub-segment is projected to expand at a 15.33% CAGR through 2031.

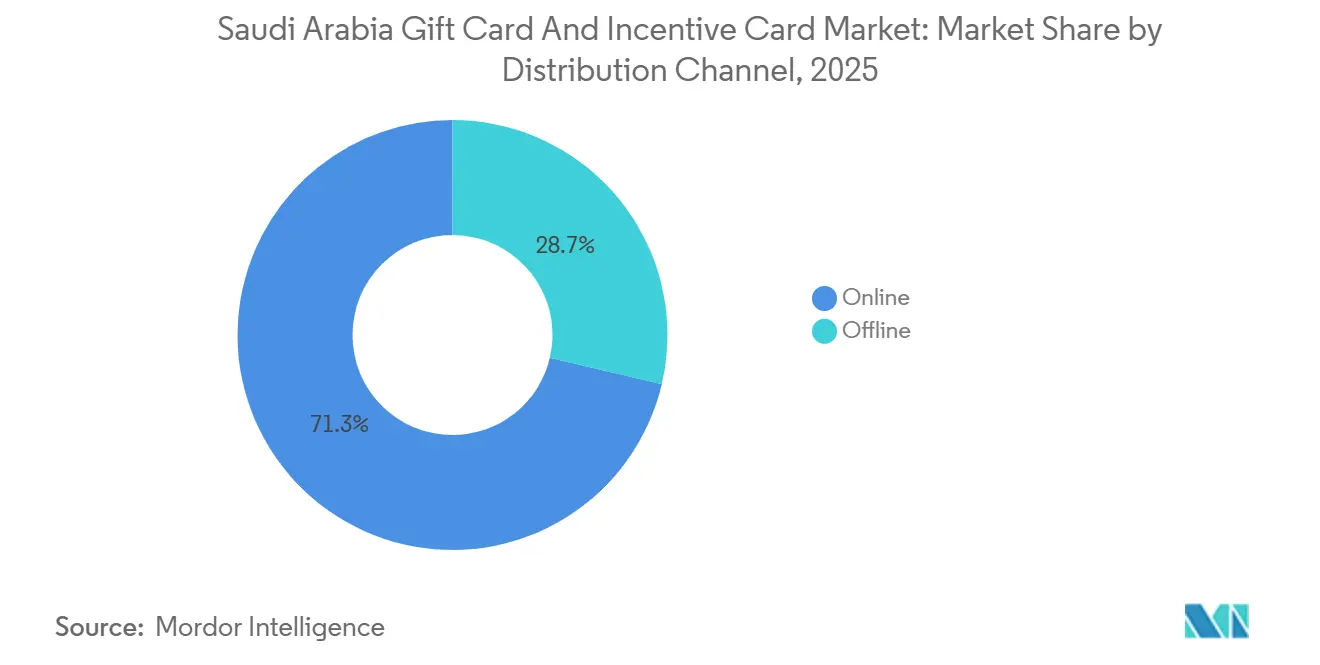

- By distribution channel, online captured 71.33% of the Saudi Arabia gift card and incentive card market share in 2025 and is forecast to grow at a 19.37% CAGR through 2031.

- By product, e-gift cards accounted for 63.76% of the Saudi Arabia gift card and incentive card market share in 2025 and are projected to advance at an 18.24% CAGR through 2031.

- By geography, Central Province led with a 35.64% of the Saudi Arabia gift card and incentive card market in 2025, while Northern Province is set to record the fastest growth at a 13.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Gift Card And Incentive Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of contactless payment solutions | 2.3% | Global (concentrated in Riyadh, Jeddah, Dammam) | Short term (≤ 2 years) |

| Government efforts to promote a cashless economy | 3.1% | National, with enforcement led by SAMA and CMA | Medium term (2-4 years) |

| Expansion of e-commerce marketplaces | 2.8% | Urban hubs (Riyadh, Jeddah) with spill-over to tier-2 cities | Short term (≤ 2 years) |

| Growing corporate focus on tax-efficient employee incentives | 1.9% | National, concentrated in Riyadh RHQ clusters | Medium term (2-4 years) |

| Increased use of gift cards for expatriate remittances | 0.7% | Eastern Province (Dammam), Central Province (Riyadh) | Long term (≥ 4 years) |

| Launch of open-loop prepaid rails by Saudi Payments | 1.4% | National integration via the Mada network | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Government Efforts to Promote a Cashless Economy

Saudi Arabia’s Financial Sector Development Program sets clear non-cash transaction objectives, and it anchors the scale-up of interoperable payment infrastructures and standardized digital rails that benefit prepaid products across retail and online commerce. The open banking agenda under Vision 2030 advances connectivity for account information and payment initiation, which allows issuers and platforms to move funds into gift card balances and confirm availability with fewer manual steps. This policy setting improves the economics of issuance at scale for workforce rewards and loyalty programs, since onboarding, verification, and settlement can be automated in line with bank-grade controls. It also aligns with consumer protection measures embedded in the E-Commerce Law and the Maroof verification regime, which provide clarity for digital storefronts where gift codes are displayed, transacted, and redeemed. As corporate HR policies evolve to integrate non-cash benefits, the policy environment enables issuance practices that are consistent with KYC and AML standards, thus reinforcing trust in the Saudi Arabia gift card and incentive card market.

Expansion of E-Commerce Marketplaces

E-commerce penetration continues to rise, and the share of digital spend observed in card networks has increased, confirming that consumers are habituated to buying and redeeming value online across broader retail categories than before. The legal framework for e-commerce, including disclosures and dispute resolution under the E-Commerce Law, reduces friction and dispute risk for code-based digital goods, which supports growth in the Saudi Arabia gift card and incentive card market. Online distribution already accounts for a significant share of category value and is projected to grow the fastest, helped by mobile-first checkout experiences and wallet-linked redemption features. Large omnichannel retailers have launched first-party digital programs, which demonstrates that value-chain participants are internalizing digital issuance and paperless redemption as part of their standard consumer journeys. With bank APIs enabling instant balance checks and confirmations, e-gift flows become smoother and less error-prone, which supports both conversion and repeat usage in the Saudi Arabia gift card and incentive card market.

Growing Corporate Focus on Tax-Efficient Employee Incentives

Corporate buyers represent a large and expanding share of volume, and SMEs are projected to grow faster than the broader category as incentives are used to recruit, retain, and recognize talent across sectors and geographies. The Regional Headquarters Program and related policies create pathways for multinationals to align compensation and benefits with digital-first corporate governance, which encourages the use of regulated prepaid instruments for non-cash rewards [1]U.S. Department of State, “2025 Investment Climate Statements: Saudi Arabia,” U.S. Department of State, state.gov. Wage support and training programs delivered through government-backed channels reduce near-term labor costs for employers, which allows HR teams to allocate funds to scalable, trackable recognition schemes across the employee lifecycle[2]HRSD, “Progress in the Saudi Labor Market,” Ministry of Human Resources and Social Development, hrsd.gov.sa. Banking APIs allow corporate platforms to issue, top up, and reconcile gift cards in near real time, improving spend visibility and automating compliance checks for programs that require audit trails. With clear rules on account opening and ongoing monitoring, issuers can support enterprise-grade workflows while meeting supervisory expectations, which sustains adoption in the Saudi Arabia gift card and incentive card market.

Launch of Open-Loop Prepaid Rails by Saudi Payments

National programs under Vision 2030 have prioritized interoperability and real-time clearing across payment rails, which allows prepaid balances to function across retail categories and merchant types with fewer acceptance gaps. Unified switching and standardized messaging reduce historical fragmentation between closed-loop programs, supporting wider acceptance for reloadable and single-use value across POS and online channels. Banks have published extensive APIs that third-party platforms can use to verify balances, initiate payment orders, and post redemptions, which accelerates integrations for corporate issuers and consumer marketplaces. Compliance frameworks, including AML and counter-fraud rules, provide the governance guardrails necessary to expand issuance while protecting consumers and merchants, which builds long-term trust in the Saudi Arabia gift card and incentive card market. With these elements in place, issuers and merchants can converge on standards that reduce breakage and improve utility for both physical and e-gift formats while maintaining regulatory clarity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence of universal redemption interoperability | -1.4% | National, cross-retailer friction | Medium term (2-4 years) |

| Increased fraud and chargeback risks in secondary card markets | -0.8% | Urban high-density areas (Riyadh, Jeddah) | Short term (≤ 2 years) |

| Insufficient Arabic-first user experience on global e-gift platforms | -0.6% | National, with a concentration in older demographics | Short term (≤ 2 years) |

| Prepaid card loading restrictions under SAMA AML regulations | -1.1% | National, broader GCC implications | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Absence of Universal Redemption Interoperability

Fragmented redemption standards persist across retailers and platforms, and issuers often manage their own rules for pooling or transferring balances, which constrain fluid usage of stored value beyond a single merchant ecosystem. This dynamic reduces utility for recipients who hold multiple small-denomination balances and cannot combine them for larger purchases, especially in categories where closed-loop policies are strict. Open banking standards published under Vision 2030 present a route to better interoperability through balance verification and payment initiation APIs, but commercial and policy harmonization among issuers and merchants is still required for broad-based balance transfer features to take root. Clearer market practices on redemption portability would improve user experience and lift utilization in the Saudi Arabia gift card and incentive card market without compromising loyalty constructs that merchants value. As interoperability improves within national rails, cardholders and corporate buyers would face fewer constraints linking incentives to high-value purchases while preserving transparency and auditability.

Prepaid Card Loading Restrictions Under SAMA AML Regulations

Anti-money laundering requirements establish thresholds and monitoring obligations for prepaid instruments, which can limit high-frequency or high-value loads unless customer due diligence is elevated, documented, and continuously monitored. These controls help protect the ecosystem but also add operational steps for issuers and corporate buyers, especially where beneficiaries include senior executives or high-risk categories that trigger enhanced due diligence. Account-opening and ongoing monitoring rules require verification and screening infrastructure, which can increase costs for smaller providers and lengthen onboarding timelines for new programs. Identity and fraud risk frameworks offered by specialized vendors can help automate screening and case management, but deployment requires strong data governance and continuous calibration against evolving regulatory guidance [3]TrustDecision, “The Fraud and Compliance Guide for Saudi Fintechs,” TrustDecision, trustdecision.com. Clear internal policies and bank-grade API integrations can streamline compliance while maintaining usability, which supports sustained adoption in the Saudi Arabia gift card and incentive card market under supervisory expectations.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consumer: Corporate SME Acceleration Drives Tax-Neutral Incentive Shift

Corporate buyers held 41.33% of the Saudi Arabia gift card and incentive card market share in 2025, and SMEs are projected to grow at a 15.33% CAGR through 2031 as employers align recognition and benefits with digital-first operations and audit-friendly prepaid instruments. The Regional Headquarters framework and related policy levers have encouraged large enterprises to modernize HR playbooks, which include non-cash incentives that are efficient to distribute and reconcile across locations. Wage support and training incentives introduced by public programs provide budget room for performance-linked rewards, accelerating employer adoption among SMEs that prioritize scalable, trackable disbursement methods. The Saudi Arabia gift card and incentive card market also benefits from onboarding and KYC clarity that reduces delays for corporate issuance, while bank APIs improve real-time visibility into spend and balances to support stronger governance. As corporate procurement standardizes around open APIs and unified workflows, card program managers streamline issuance cycles and improve user experience at scale across employee segments in the Saudi Arabia gift card and incentive card industry.

Individual consumers accounted for a significant share of the category's value in 2025, driven by online shopping trends and holiday digital gifting, which increased demand for instant and mobile-friendly e-gift formats. Seasonal spikes in search and spending recorded by network providers and platforms indicate that time-bound promotional windows and holiday campaigns drive conversion for digital codes and wallet-linked redemption flows. Better disclosures and consumer protections under the E-Commerce Law, combined with merchant verification via Maroof, continue to expand the base of trusted sellers, which supports repeat purchases of digital gift vouchers. Corporate issuers are likely to deepen personalization features as APIs enable rule-based top-ups and event-triggered rewards, creating crossover adoption where recipients use incentives to fund retail and subscription categories favored in e-commerce. This two-sided expansion positions the Saudi Arabia gift card and incentive card market to serve both enterprise-grade workflows and consumer-friendly digital experiences with consistent reliability and security.

By Distribution Channel: Online Dominance Fueled by Mobile-First Checkout Integration

Online channels accounted for 71.33% of category value in 2025 and are projected to grow at a 19.37% CAGR through 2031, enabled by wallet readiness, mobile-first checkout design, and verified storefronts that simplify code delivery and redemption. Legal scaffolding under the E-Commerce Law and the Maroof program drives merchant accountability and reduces buyer hesitation for digital goods, which supports greater throughput for instant e-gift issuance. Bank API ecosystems further improve conversion by enabling instant balance checks and faster payment confirmations during peak traffic windows, which reduces abandonment and failed redemptions. As retailers grow their proprietary apps and integrate redemption in the account layer, consumers experience fewer steps from purchase to use, supporting healthier repeat rates in the Saudi Arabia gift card and incentive card market. This environment favors e-gift formats and embedded loyalty value, where code-based incentives flow seamlessly into wallets, checkout pages, and order histories for audit and customer support.

Offline channels maintained a significant market share, driven by corporate bulk procurement and scenarios emphasizing physical presentation, despite the increasing adoption of paperless processes in various industries. Large-format and grocery retailers continue to refresh their store fleets and loyalty programs, and they increasingly pair in-store racks with digital receipts and app-based redemption to reduce waste and simplify balance tracking. Corporate buyers also favor in-person pickup in certain cases for documentation, distribution, or ceremony, which sustains a durable share for physical cards and store-based procurement within the Saudi Arabia gift card and incentive card market. Banks and fintech providers have supported both channels by exposing APIs that power instant verification and settlement, which reduces reconciliation cycles and improves support operations when issues arise at POS. As omnichannel journeys become more cohesive, offline and online distribution reinforce each other to improve utility and reduce friction for reloadable and single-use formats in the Saudi Arabia gift card and incentive card industry.

By Product: E-Gift Card Supremacy Driven by Instant Delivery and Mobile Wallet Integration

E-gift cards held 63.76% of sales in 2025 and are projected to grow at an 18.24% CAGR through 2031, reflecting user preference for instant delivery, mobile wallet compatibility, and simple reuse within app ecosystems. Real-time bank connectivity for balance verification and payment initiation enhances user experience and reduces failed redemptions, which improves persistence and repeat purchases for digital codes across leading categories such as grocery, electronics, travel, and entertainment. As more retailers integrate redemption workflows into account profiles, digital notifications and activity logs help recipients manage balances in a transparent, low-friction manner that supports higher utilization. Issuers also rely on compliance-ready onboarding and monitoring to maintain trust as volumes scale, which is consistent with supervisory expectations for identity verification and suspicious activity reporting. These elements strengthen the Saudi Arabia gift card and incentive card market by aligning consumer convenience with governance discipline in the e-gift format.

Physical cards maintained a significant share of product sales, driven by corporate bulk issuance and their appeal in formal gifting, while retailers advanced paperless receipts and QR-linked account integrations. Store networks continue to integrate loyalty points and gift balances into a unified profile, which helps reduce waste from packaging and improves customer service with reliable transaction histories. As instant funding and verification become standard through bank APIs, physical card issuance can pair with digital account management, which preserves ceremonial value while improving utility in everyday use. Vendors enhance fraud and compliance controls to protect program integrity, allowing issuers and merchants to support both physical and digital experiences in line with risk frameworks. This hybrid strategy keeps physical cards relevant while the Saudi Arabia gift card and incentive card market tilts toward e-gift formats for speed, personalization, and convenience at scale.

Geography Analysis

Central Province led with 35.64% in 2025, reflecting the concentration of corporate headquarters, financial institutions, and national programs that drive procurement and redemption activity through a dense network of regulated merchants and digital storefronts in the Saudi Arabia gift card and incentive card market. Policy incentives linked to the Regional Headquarters framework channel enterprise activities into Riyadh, and this catalyzes demand for non-cash rewards and employee benefits delivered through compliant prepaid instruments. Government-backed digitization under Vision 2030 supports interoperable payment rails and open banking integrations that are widely adopted in the capital, which improves usability and acceptance for e-gift and physical cards. Retailers have expanded paperless features and loyalty integration inside their apps, which helps residents redeem balances more efficiently and reduces operational overhead for store networks. These conditions underpin steady growth in redemption velocity and repeat usage in the Central Province within the Saudi Arabia gift card and incentive card market.

Western Province contributes a substantial share, supported by strong retail and hospitality ecosystems that anchor omnichannel gift experiences in major urban centers. Airline loyalty programs have expanded partner networks and digital redemption features that integrate travel and retail value, which encourages cross-category usage of stored value by residents and visitors alike. Verified e-commerce merchants continue to increase under the Ministry of Commerce’s frameworks, bringing more regulated storefronts into the ecosystem that accept and distribute digital codes in a compliant manner. With increasing reliance on bank APIs for real-time payment confirmations and refunds, retailers in key Western Province cities benefit from lower friction and faster service recovery when issues arise during redemption. This infrastructure alignment and partner-led expansion sustain the region’s role as a growth anchor for the Saudi Arabia gift card and incentive card market.

Northern Province is projected to record the fastest growth at a 13.25% CAGR through 2031, reflecting expanding economic activity and workforce inflows linked to national development priorities, which favor flexible, non-cash benefits and digital retail experiences. Eastern Province maintains a strong foundation supported by large employers, telecom connectivity, and payments digitization that improve acceptance outcomes across store networks and logistics corridors. National tourism and infrastructure programs supported in budget planning indicate continued investment in mobility and services, which lifts retail demand and expands the base of merchants that can distribute and redeem gift value at scale. As banks expose more APIs and retailers migrate to paperless features in loyalty and receipts, the geography of acceptance becomes more even across provinces, which benefits the Saudi Arabia gift card and incentive card market. This combination of policy, infrastructure, and retail execution supports sustained expansion across Central, Western, Eastern, Northern, and Southern provinces over the forecast period.

Competitive Landscape

Market concentration is moderate, with the top five players accounting for just over half of activity in 2025, which leaves room for specialist issuers, white-label platforms, and fintech collaborators to win share by solving integration, personalization, or compliance pain points in the Saudi Arabia gift card and incentive card market. Program scale increasingly depends on API maturity and orchestration capabilities, and banks are enabling partners to verify balances, initiate payments, and automate reconciliation through extensive developer suites. As retailers roll out paperless receipts and app-linked redemption, ecosystem players position themselves to support cross-channel journeys that emphasize speed, clarity, and security for both e-gift and physical cards.

Leading issuers and retailers continue to differentiate on loyalty integration and user experience, while airlines expand partner networks that translate travel activity into redeemable value across everyday retail categories. Fintech platforms deepen ties with regulated financial institutions so that onboarding, monitoring, and reporting remain consistent with AML requirements as programs scale across consumer and corporate segments. New co-branded instruments targeting digital-native communities show how brand partnerships can unify spend categories and elevate engagement with incentives that tie unique benefits to card usage and affiliate ecosystems in the Saudi Arabia gift card and incentive card market.

Ecosystem cooperation is also visible in treasury and API partnerships that help corporates consolidate workflows for disbursements, liquidity, and risk management, including foreign exchange and interest-rate tools that surround incentive and payment operations. Category expansion in telecom-adjacent fintech propositions suggests new distribution channels for prepaid value and embedded services, which can feed incremental demand for digital codes and reloadable cards. With public-sector programs emphasizing digital rails and interoperability, the Saudi Arabia gift card and incentive card market encourages both incumbents and challengers to compete on service reliability, compliance readiness, and seamless user journeys at checkout and in-app.

Saudi Arabia Gift Card And Incentive Card Industry Leaders

STC Pay

Jarir Bookstore

Virgin Megastore

Carrefour Saudi

Amazon.sa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Alrajhi Bank, in collaboration with Saudi esports leader POWR, introduced a co-branded payment card. The “Power” Card offers 10% cashback at the POWR Store, exclusive event access, monthly POWR Palace visits, and opportunities to feature in POWR content, with more benefits forthcoming.

- September 2025: Al Rajhi Bank signed a memorandum of understanding with SingleView to develop innovative digital treasury solutions for corporates and SMEs, leveraging open APIs for integrated financial services, automated processes, and enhanced liquidity and risk management, including advanced foreign exchange and interest rate products.

- June 2025: flyadeal partnered with Saudia's AlFursan loyalty program, enabling members to earn miles on FlyMax and FlyPlus fare classes and redeem miles on any scheduled flyadeal flight with unlimited seat availability, no blackout dates, and competitive booking rates, with digital redemption available via flyadeal's website and application.

- May 2025: Saudia’s AlFursan Loyalty Program partnered with Al-Dawaa Medical Services Co. (DMSCO), enabling ARBAHI loyalty members to convert points into AlFursan miles. This collaboration enhances member benefits, offering seamless rewards redemption for flights, upgrades, and exclusive perks through Al-Dawaa’s secure digital platform.

Saudi Arabia Gift Card And Incentive Card Market Report Scope

Gift cards and incentive cards are prepaid payment tools issued by retailers, banks, or firms, serving as promotional strategies to enhance customer acquisition, brand visibility, and sales while offering monetary alternatives for purchasing goods or services.

The Saudi Arabia gift card and incentive card market report is segmented by consumer (individual, corporate), distribution channel (online, offline), product (e-gift card, physical card), and geography (Central Province, Western Province, Eastern Province, Northern Province, Southern Province). The market forecasts are provided in terms of value (USD).

By Consumer

| Individual | |

| Corporate | Small-scale Enterprise |

| Mid-tier Enterprise | |

| Large Enterprise |

By Distribution Channel

| Online |

| Offline |

By Product

| E-Gift Card |

| Physical Card |

By Geography

| Central Province |

| Western Province |

| Eastern Province |

| Northern Province |

| Southern Province |

| By Consumer | Individual | |

| Corporate | Small-scale Enterprise | |

| Mid-tier Enterprise | ||

| Large Enterprise | ||

| By Distribution Channel | Online | |

| Offline | ||

| By Product | E-Gift Card | |

| Physical Card | ||

| By Geography | Central Province | |

| Western Province | ||

| Eastern Province | ||

| Northern Province | ||

| Southern Province | ||

Key Questions Answered in the Report

What is the size and growth outlook for the Saudi Arabia gift card and incentive card market in 2026?

The market size is expected to grow from USD 10.48 billion in 2025 to USD 11.53 billion in 2026 and is forecast to reach USD 18.59 billion by 2031 at a 10.02% CAGR over 2026-2031.

Which segments lead in adoption across Saudi Arabia?

Online distribution leads with 71.33% in 2025, e-gift cards hold 63.76% by product, and corporate buyers account for 41.33% by consumer, each supported by strong policy and digital infrastructure tailwinds.

How are government programs influencing prepaid and gift solutions?

Vision 2030's Financial Sector Development Program and open banking agenda standardize rails, protect consumers, and speed integrations, which together support prepaid issuance and redemption at scale.

Why are corporate buyers accelerating their spending on incentives?

RHQ policies and labor programs encourage digital, auditable rewards, while banking APIs streamline issuance, top-ups, and reconciliation for employee incentives.

Which regions are most important within the Kingdom?

Central Province leads with 35.64% in 2025 due to the concentration of headquarters and infrastructure, and Northern Province is projected to expand the fastest at a 13.25% CAGR through 2031.

What features do leading platforms prioritize to compete effectively?

Leaders emphasize API-enabled real-time balances, paperless receipts, loyalty integration, and strong AML controls to deliver fast, compliant user journeys across channels.

Page last updated on: