Functional Flour Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

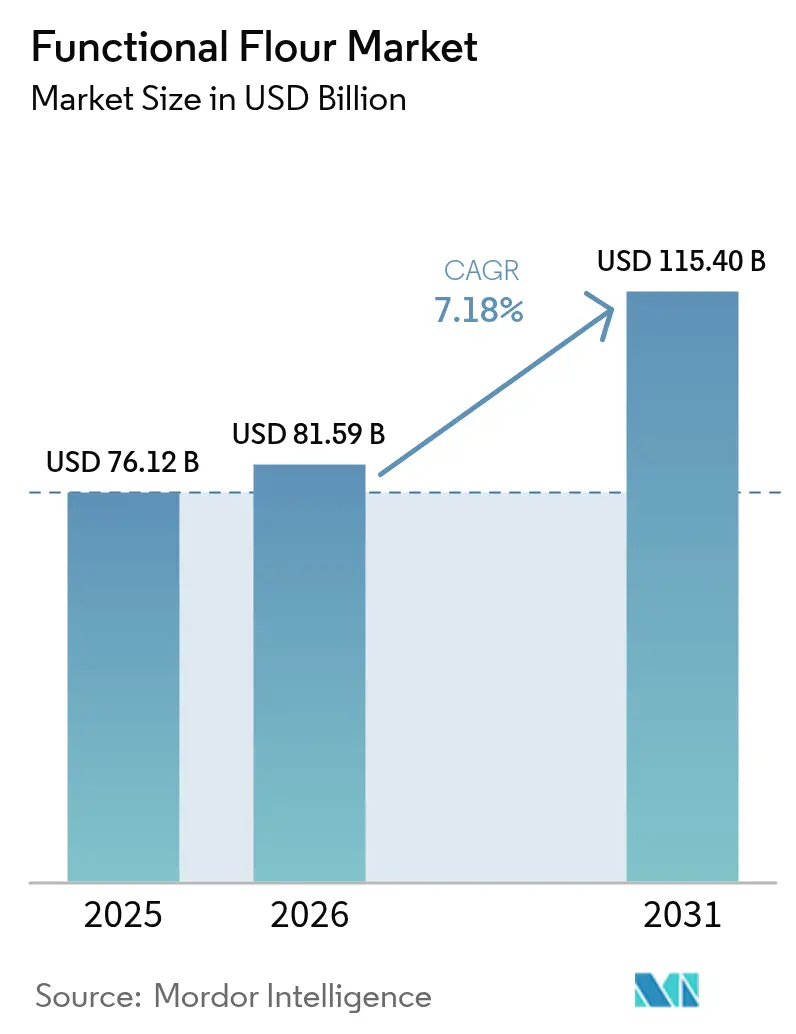

| Market Size (2026) | USD 81.59 Billion |

| Market Size (2031) | USD 115.40 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

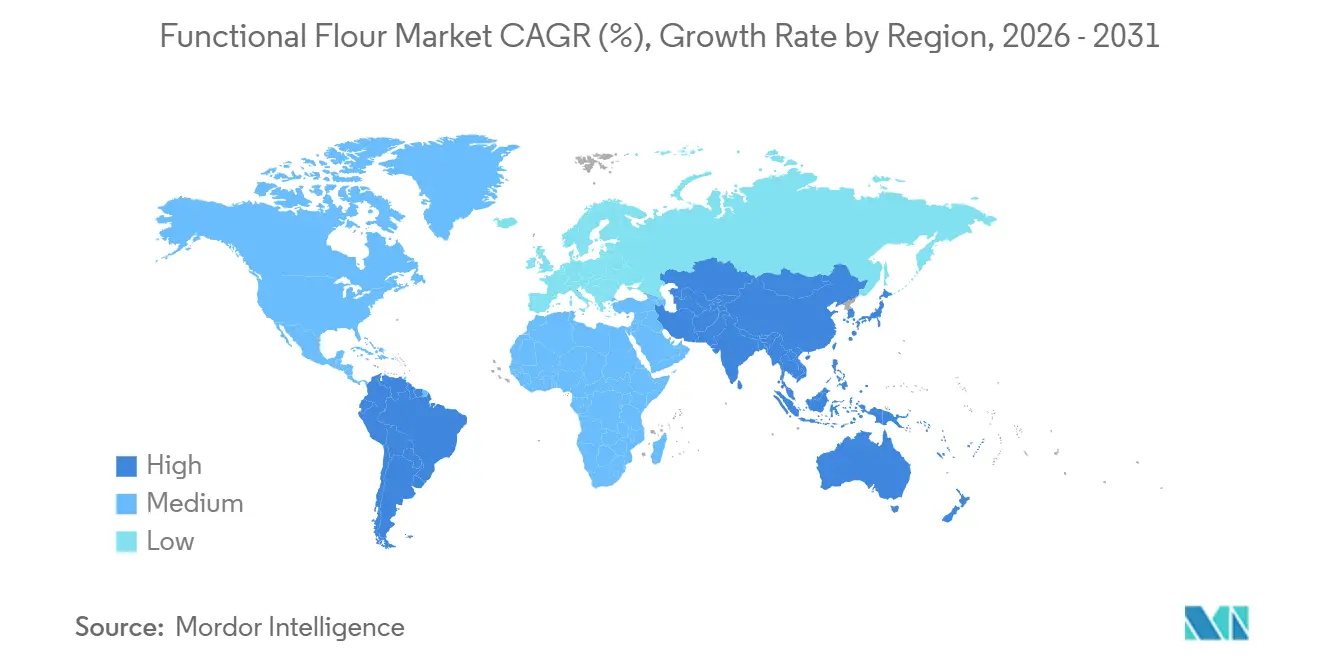

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Functional Flour Market Analysis by ���ϲ�����

The functional flour market size is expected to increase from USD 76.12 billion in 2025 to USD 81.59 billion in 2026 and reach USD 115.40 billion by 2031, growing at a CAGR of 7.18% over 2026-2031. Accelerated demand for clean-label texturizers, fortification mandates in staple foods, and sustained growth of plant-based protein formats keep the functional flour market on an upward trajectory. Legume-based ingredients are gaining share because they supply protein concentrations above 20% while remaining free from the top eight allergens, enabling formulators to diversify beyond wheat. Precision extrusion and heat-moisture treatment let processors tailor gelatinization profiles, cutting reliance on hydrocolloids and opening cost-effective reformulation pathways. At the same time, side-stream upcycling creates new profit pools by turning oat-milk pulp, okara, and brewers’ spent grain into high-fiber functional flours, meeting corporate sustainability targets and retailer scorecards. Supply-chain resilience is now a strategic differentiator as drought-linked yield swings in Canada and Europe raise input-price volatility and heighten the need for diversified sourcing contracts.

Key Report Takeaways

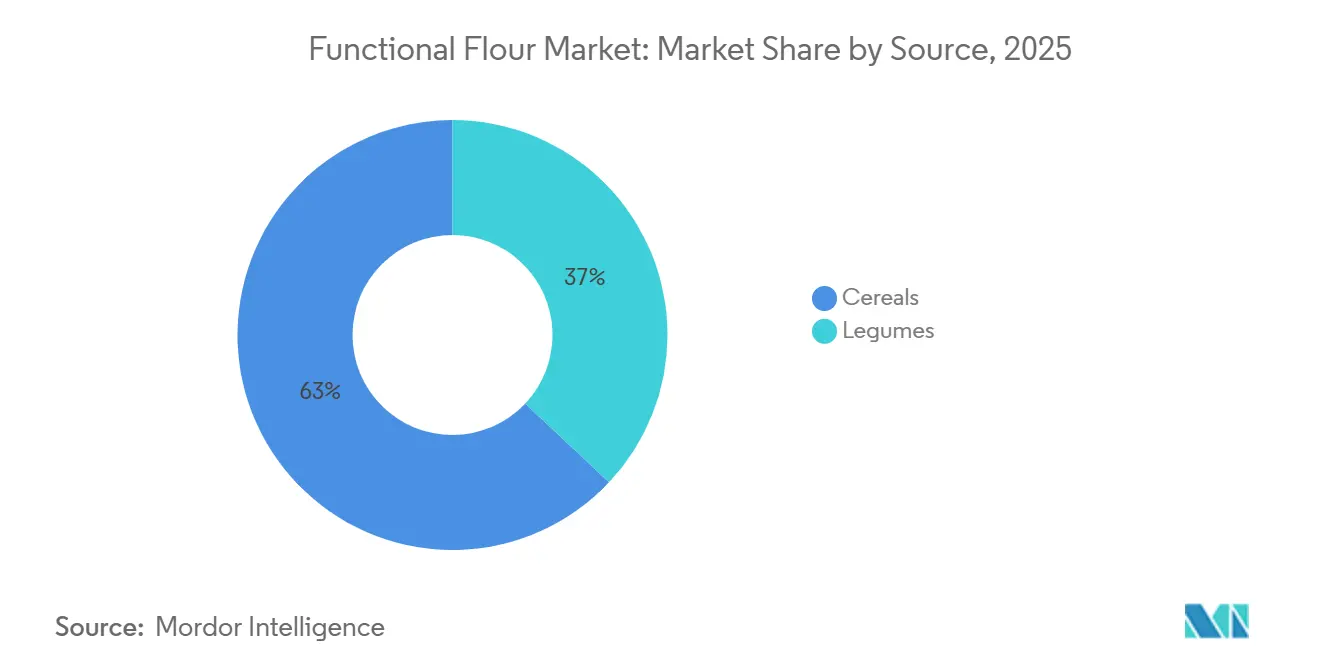

- By source, cereals commanded 62.98% of functional flour market share in 2025, while legumes are poised to grow at an 8.74% CAGR through 2031.

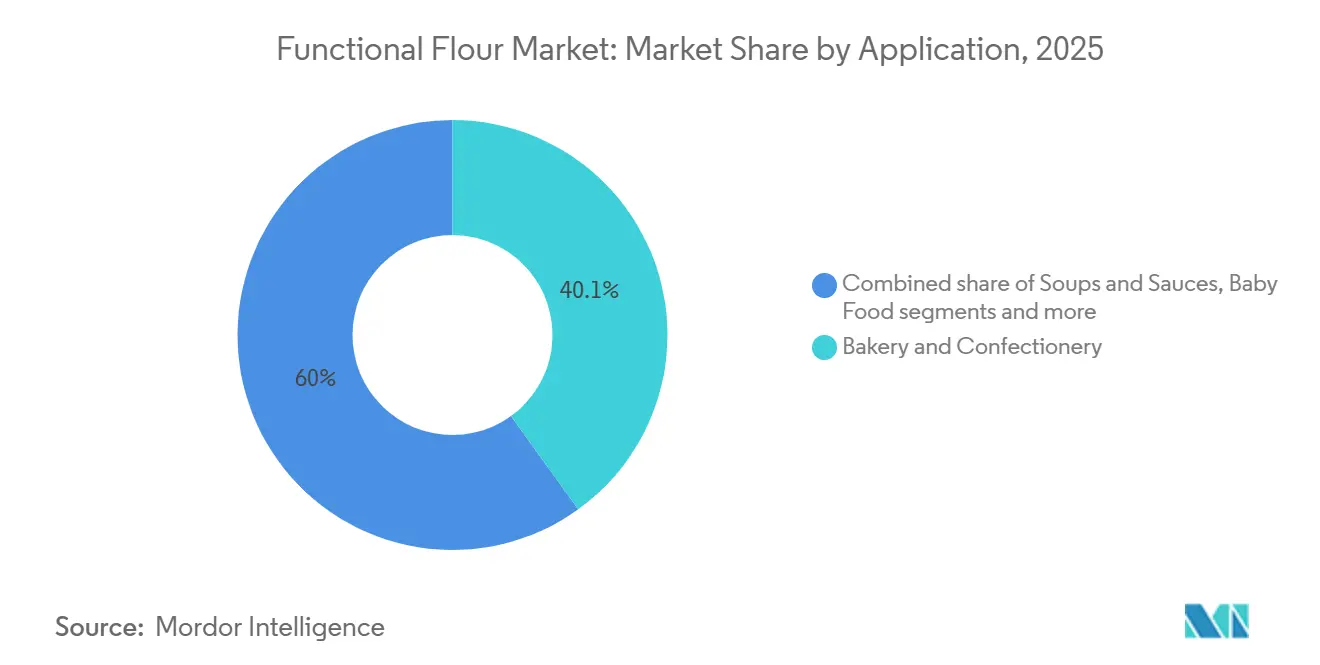

- By application, bakery and confectionery accounted for 40.05% share of the functional flour market size in 2025, whereas meat alternatives are set to register a 7.63% CAGR to 2031.

- By geography, North America led with a 33.22% revenue share in 2025, while Asia-Pacific is projected to advance at an 8.79% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Functional Flour Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bakery and snack industry demand for texture control and shelf-stability | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing use in specialty and high-margin segments (sports nutrition, baby foods, fortified staples) | +1.5% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Growth in plant-based food and alternative proteins | +2.1% | North America, Europe, Asia-Pacific core markets | Long term (≥4 years) |

| Adoption of precision extrusion and heat-moisture treatment unlocking customized functional traits | +1.2% | Global, led by North America and Western Europe | Short term (≤2 years) |

| Up-cycling of food-processing side-streams into high-fiber flours | +0.9% | Europe, North America, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Regulatory support and food-safety standards harmonization | +0.7% | Global, particularly Europe, Asia-Pacific, Middle East | Long term (≥4 years) |

| Source: ���ϲ����� | |||

Bakery and snack industry demand for texture control and shelf-stability

The bakery and snack industry is witnessing a growing emphasis on texture control and shelf stability, driven by shifting consumer preferences and market demands. Manufacturers are striving to deliver consistent sensory quality, such as soft bread crumbs or crisp crackers, while addressing the increasing demand for nutritional and functional benefits in staple products. This trend is reflected in the rising expenditure of United Kingdom households on bread and cereals, which reached GBP 23.38 billion in 2025, up from GBP 22.32 billion in 2022, as per the Office for National Statistics (UK), underscoring robust demand for high-quality products [1]Source: Office for National Statistics (UK), "Consumer Trends: Chained Volume Measure, Seasonally Adjusted," ons.gov.uk . To meet these expectations, industrial bakers and snack producers are collaborating with ingredient suppliers like Archer Daniels Midland Company and Cargill, Incorporated. These suppliers are innovating functional flours that enhance water absorption, dough rheology, and product texture, while also incorporating health-focused attributes such as higher fiber, protein content, or gluten-free functionality. This collaboration enables manufacturers to balance clean-label claims with technical performance, ensuring products remain fresher for longer without compromising on mouthfeel or structural integrity. Such advancements are critical in a competitive market environment characterized by heightened consumer expectations and supply chain challenges.

Growing use in specialty and high-margin segments (sports nutrition, baby foods, fortified staples)

Shifting lifestyle and health priorities are driving growth in the functional flour market, particularly in specialty and high-margin segments such as sports nutrition, baby foods, and fortified staples. With 21.5% of United States adults expected to participate in sports, exercise, and recreational activities daily in 2024, up from 20.1% in 2022, there is increasing demand for nutrient-enhanced sports nutrition that support performance and recovery [2]Source: Bureau of Labor Statistics, "American Time Use Survey - 2023 Results," bls.gov . Concurrently, heightened parental focus on nutrient-dense baby foods and fortified staples is encouraging food manufacturers to source specialized functional flours that provide tailored nutritional profiles, improved digestibility, and enhanced processing performance. Key suppliers, including Ardent Mills and Swedish Oat Fiber, are innovating with fiber-enriched flours that help formulators meet protein and clean-label requirements while maintaining texture and processability in finished products. These developments reflect how consumer health trends are reshaping ingredient strategies across the value chain. Furthermore, the market is expanding as customers increasingly seek differentiated, higher-margin products that align with active and preventive health objectives, reinforcing the role of functional flours in addressing evolving consumer demands.

Growth in plant-based food and alternative proteins

Rising consumer interest in sustainable, animal-free diets is driving significant changes in the functional flour market, as demand grows for flours that enhance texture, protein content, and functional performance in plant-based applications. Data reveals that 6 in 10 or 59% of U.S. households purchased plant-based foods in 2024, reflecting widespread adoption [3]Source: The Good Food Institute, "U.S. Retail Market Insights for the Plant-Based Industry," gfi.org. This trend, as highlighted by The Good Food Institute and the Plant Based Food Association, is encouraging food manufacturers to reformulate bakery, snack, and meat-alternative products with ingredients that replicate the mouthfeel and structure of traditional options. To meet these evolving needs, companies such as Scoular and Ingredion Incorporated are developing tailored solutions, including pea protein-fortified flours, chickpea and lentil flours with enhanced emulsification properties, and tapioca or rice flour blends engineered for specific viscoelastic characteristics. These innovations enable brands to address consumer expectations for sustainability, nutrition, and sensory quality without compromising product performance. The interplay between the growth of plant-based foods and advancements in functional flour underscores the market's focus on delivering ingredient solutions that align with current consumer preferences and industry demands.

Adoption of precision extrusion and heat-moisture treatment unlocking customised functional traits

Manufacturers in the functional flour market are increasingly adopting precision extrusion and heat-moisture treatment technologies to develop ingredients with specific performance characteristics. These methods enable the customization of functional traits such as water absorption, controlled gelatinization, and targeted digestibility, addressing evolving product standards and complex processing requirements. By refining starch, protein, and fiber structures, these technologies help bakers and food formulators achieve consistent texture, extended shelf life, and reliable processing in finished products. Additionally, these advanced techniques allow for the creation of flours with tailored functional profiles, such as enhanced emulsification for vegan pâtés, modified pasting properties for gluten-reduced breads, and improved gel strength for high-protein bars. This capability is critical as brands compete on both performance and clean-label attributes. Leading ingredient suppliers, including Ardent Mills (a joint venture of Conagra Brands, Cargill, and CHS) and MGP Ingredients, Inc., are leveraging these technologies to produce engineered functional flours that reduce reliance on chemical additives while delivering targeted nutritional and sensory outcomes. As formulators demand predictable and customizable ingredient functionality across bakery, snack, and specialty applications, the integration of precision extrusion and heat-moisture treatment is becoming a cornerstone of innovation, linking end-product quality with upstream ingredient design.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of raw materials and production | -1.4% | Global, acute in North America and Europe | Short term (≤2 years) |

| Supply-chain volatility and limited scalability | -1.1% | Global, concentrated in pulse-producing regions (Canada, India, Australia) | Medium term (2-4 years) |

| Potential allergen and cross-contamination risks | -0.6% | North America, Europe, Asia-Pacific urban markets | Medium term (2-4 years) |

| Functional-performance drift across crop varieties hindering standardization | -0.8% | Global, particularly affecting legume-based flours | Long term (≥4 years) |

| Source: ���ϲ����� | |||

High cost of raw materials and production

The high cost of raw materials and production poses a significant challenge in the functional flour market. Specialty grains, ancient seeds, and legume sources are inherently more expensive than conventional wheat due to limited cultivation areas, premium sourcing requirements, and volatile supply dynamics. These higher raw material costs are further amplified by processing expenses, including specialized milling, quality control, and targeted fortification methods, which enhance the ingredient's functionality compared to standard flour. This cost burden directly impacts B2B suppliers and food manufacturers. For example, The Scoular Company invests in advanced processing for high-protein and pulse-based flours but faces premium input costs for peas and chickpeas, along with the capital-intensive nature of air classification equipment required to ensure consistent functional traits. Food formulators often weigh the technical benefits of functional flours against conventional alternatives, particularly in price-sensitive segments where higher ingredient costs can compress margins and slow adoption. Additionally, supply chain challenges, such as seasonal availability and transportation cost fluctuations, further increase production expenses. These factors make it difficult for manufacturers to scale niche functional flours without passing costs to customers or accepting reduced margins. This underscores the importance of cost management, grower partnerships, and process efficiencies for B2B functional flour manufacturers aiming to remain competitive.

Potential allergen and cross-contamination risks

Allergen and cross-contamination risks are critical challenges in the functional flour market. Functional flours, often derived from pulses, nuts, seeds, and alternative grains, carry inherent allergen profiles such as pea, soy, and nut flours. When processed in facilities handling wheat or gluten, the need for stringent segregation, cleaning, and testing protocols becomes essential to prevent cross-contact, which could lead to health risks and regulatory complications. To address these concerns, ingredient suppliers and food manufacturers invest in specialized allergen management systems and traceability measures, adding complexity and cost. For example, Avena Foods employs dedicated production lines and certification processes to mitigate cross-contamination risks, particularly for gluten-free and allergen-free claims, ensuring safety alongside functionality. In a market driven by clean-label and health-focused demands, managing allergen risks is integral to quality control, as even minor contamination can result in recalls, brand damage, or regulatory scrutiny. These challenges necessitate close collaboration between manufacturers and producers to implement robust segregation, testing, and certification practices. Balancing ingredient innovation with rigorous risk mitigation strategies is essential to maintaining consumer trust and ensuring compliance across bakery, snack, and specialty food applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Legumes Outpace Cereals on Protein Demand

Cereal-based functional flours hold the largest share in the market, contributing 62.98% to overall expansion. Staples such as rice, corn, and wheat remain essential in Asia-Pacific diets and global bakery systems. Oat flour is increasingly favored for its beta-glucan content, which supports cholesterol-reduction claims approved by the U.S. Food and Drug Administration. Barley flour, traditionally linked to brewing and malt-extract industries, is now being adapted for soups and ready meals through low-beta-glucan variants to meet convenience-driven consumption trends. Quinoa and buckwheat flours bolster gluten-free premiumization strategies, while rye flour retains regional importance in Scandinavian and Eastern European bakery traditions, where sourdough fermentation addresses its dense crumb structure. These factors collectively underscore the foundational role of cereal-based flours in both heritage and volume-driven applications.

Legume-based functional flours are projected to grow at a faster CAGR of 8.74% through 2031, driven by the rising demand for plant-based protein formulations that emphasize amino acid completeness and allergen avoidance. Pea flour leads this segment with its neutral flavor and 20–25% protein concentration, making it ideal for dairy alternatives and meat analogues. Lentil flour is gaining traction in gluten-free bakery applications due to its binding properties and high iron content, exceeding 7 mg per 100 g, supporting anemia-reduction initiatives in South Asia. Soybean flour remains relevant in cost-sensitive applications, while chickpea and fava-bean flours cater to premium niches tied to clean-label and ethnic formulations. Advanced milling and air-classification technologies from suppliers like Bühler Group enable tailored protein functionality, supporting growth and diversification within this segment.

By Application: Meat Alternatives Drive Fastest Expansion

The bakery and confectionery segment accounts for the largest share of the functional flour market, contributing 40.05% to projected 2025 revenue. This growth is attributed to the increasing demand for clean-label reformulation and gluten-free products, which are transforming bread, cakes, and sweet goods to meet consumer expectations for transparent ingredient lists. Manufacturers are replacing chemical improvers with enzyme-treated and specialty flours to enhance crumb softness, moisture retention, and shelf stability while maintaining clean-label standards. Savory snacks are also utilizing functional flours to reduce fat absorption and increase protein content, as demonstrated by lentil-flour tortilla chips delivering 18% protein compared to 6% in corn-based alternatives. Additionally, soups, sauces, and ready-to-eat products are adopting pre-gelatinized and resistant-starch flours to improve efficiency and nutritional value, addressing the needs of convenience-driven categories.

The meat alternatives segment represents the fastest-growing application, with a projected CAGR of 7.63% through 2031. This expansion is driven by the rising popularity of plant-based meat and the need to replicate the texture and juiciness of animal protein using functional-flour blends. Pea and soy flours form the protein base, while wheat gluten and modified starches provide elasticity and moisture retention. Suppliers such as Roquette Frères are supporting this trend by offering pulse-derived functional flours and texturizing solutions tailored for advanced processing techniques, enabling manufacturers to enhance product quality and scalability.

Geography Analysis

North America is expected to account for 33.22% of the global functional flour market revenue by 2025, driven by its integrated ecosystem spanning raw material supply to value-added ingredient innovation. The United States' mature plant-based food sector and Canada’s position as the largest global exporter of pulses underpin this dominance. The demand for pea and soy flours in meat analogues and dairy alternatives is reinforced by the strong presence of alternative-protein brands in the United States, while Canada’s pulse infrastructure ensures reliable export flows of lentils and peas for functional milling. Companies like SunOpta Inc. capitalize on this regional strength by processing and supplying pulse-based functional flours tailored for protein fortification and gluten-free systems, aligning agricultural scale with formulation-driven demand.

The Asia-Pacific region is projected to grow at a CAGR of 8.79% through 2031, supported by rapid urbanization, rising disposable incomes, and government-led fortification mandates. In China, younger consumers adopting flexitarian diets are driving demand for pea- and soy-based flours in meat analogues and dairy alternatives. Japan’s aging population is increasing interest in high-protein, easy-to-digest flour systems for senior nutrition, while Australia’s gluten-free bakery segment is incorporating chickpea and lentil flours. The 2024 approval of lupin flour as a novel ingredient with mandatory allergen labeling by Food Standards Australia New Zealand further supports ingredient diversification. These factors position Asia-Pacific as a high-growth consumption hub and an innovation corridor for fortified and specialty flour solutions.

Europe maintains steady revenue contributions, driven by clean-label expectations and advanced regulatory frameworks that encourage minimally processed, transparently sourced functional flours. The region’s bakery culture and demand for gluten-free premium products sustain interest in oat, rye, and pulse-derived flours. Meanwhile, South America and the Middle East and Africa are witnessing growth due to national fortification programs and expanding middle-class populations seeking affordable protein-enriched staples. Soy, corn, and pulse flours dominate mass-market applications, with B2B innovators like Cosucra Groupe Warcoing supporting protein standardization and fiber enrichment strategies across these regions.

Competitive Landscape

The functional flour market is moderately fragmented, with vertically integrated grain merchants such as Cargill, ADM, and Bunge playing a dominant role. These companies manage significant commodity volumes through their global sourcing networks and multi-modal logistics, helping to stabilize input costs despite volatile grain prices and climate-related disruptions anticipated in 2026. By supplying flours with consistent specifications, they support multinational food manufacturers in producing bakery staples and snacks. Their operational scale ensures cost-efficient handling of high-volume orders for pre-cooked and fortified flours, meeting the growing demand driven by increasing household expenditures on staple foods across regions like North America and Asia-Pacific.

Cargill utilizes proprietary milling and modification technologies to deliver uniform gluten-free and high-fiber flours, which are essential for multinational snack producers seeking texture consistency in extruded products. ADM complements this by offering pulse- and cereal-based blends optimized for fortified staples, supported by multi-site logistics to address regional shortages. Bunge further strengthens the market by providing additive-free, stable flours for pasta and ready-to-eat foods, ensuring cost predictability and enabling manufacturers to maintain margins despite economic pressures and raw material price fluctuations expected in 2026.

Specialized processors like Ingredion and Associated British Foods focus on high-margin segments by delivering application-specific solutions. Ingredion’s texturizing flour systems enable precise viscosity control in plant-based patties, helping brands differentiate in the expanding alternative protein market while adhering to organic certifications demanded by premium consumers. Associated British Foods enhances this segment by offering certified organic pulse flours for hypoallergenic baby foods and gluten-free mixes. These efforts foster innovation and long-term partnerships, positioning these companies as key contributors to specialty growth within the evolving functional flour market.

Functional Flour Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Associated British Foods plc

-

Ingredion Incorporated

-

Bunge Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Protein Industries Canada, Maia Farms, and Phytokana Ingredients collaborated on a CAD 32.5 million (approximately USD 23.5 million) project to transform Canadian-grown fava beans into nutritious and sustainable ingredients for plant-based foods. Phytokana, an Alberta-based start-up, utilized its proprietary technology, designed to avoid the use of heat and chemicals, to process novel fava bean varieties into protein concentrate, starch flour, and fava flour with enhanced taste, texture, and nutritional value. These ingredients retained their natural functionality, making them suitable for applications in dairy alternatives, plant-based meats, and other food products.

- July 2024: Cargill launched SimPure 92260, a soluble rice flour developed to address consumer demand for recognizable ingredients. It matched the taste, texture, and functionality of maltodextrin, a common bulking agent and flavor carrier. SimPure 92260 offered similar viscosity, bulking properties, and sensory characteristics as 10 DE maltodextrin, enabling direct substitution in applications such as reduced-sugar bakery products, dairy, powdered beverages, convenience foods, sauces, dressings, snacks, cereals, bars, seasoning mixes, and flavor carriers.

- May 2024: GoodMills Innovation, a key participant in the food industry, introduced Smart Wheat high-protein flour for bakery applications. This flour contained a native protein that supported the development of gluten networks in the dough, improving its extensibility.

Global Functional Flour Market Report Scope

Functional flours are modified heat or non-traditional flours that claim to improve health benefits beyond that of the nutrition found in flour. Functional flour may also include flours that are fortified with vitamins, herbs, and even nutraceuticals.

The Functional Flour market is segmented by Source (Cereals and Legumes), Type (Specialty Flour and Conventional Flour), Application (Bakery, Savory Snacks, Soups and Sauces, Ready-to-Eat (RTE) Products, and Other Applications); and Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. The report offers the market size and values in (USD Million) during the forecast years for the above segments.

| Cereals | Rye |

| BuckWheat | |

| Oats | |

| Barley | |

| Quinoa | |

| Others (Rice, Corn, Sorghum) | |

| Legumes | Pea |

| Lentil | |

| Soybean | |

| Others (Chickpea, Fava Bean) |

| Bakery and Confectionery |

| Savory Snacks |

| Soups and Sauces |

| Ready To Eat Products |

| Baby Food |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Source | Cereals | Rye |

| BuckWheat | ||

| Oats | ||

| Barley | ||

| Quinoa | ||

| Others (Rice, Corn, Sorghum) | ||

| Legumes | Pea | |

| Lentil | ||

| Soybean | ||

| Others (Chickpea, Fava Bean) | ||

| By Application | Bakery and Confectionery | |

| Savory Snacks | ||

| Soups and Sauces | ||

| Ready To Eat Products | ||

| Baby Food | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of global functional flour sales by 2031?

They are projected to reach USD 115.40 billion, reflecting a 7.18% CAGR from 2026 to 2031.

Which ingredient type is growing fastest within functional flours?

Legume-based flours, spearheaded by pea and lentil variants, are advancing at an 8.74% CAGR to 2031.

Why are functional flours important in plant-based meat?

They create cohesive protein matrices during high-moisture extrusion, replacing hydrocolloids while improving juiciness and bite in meat analogues.

Which region is expected to post the fastest growth?

Asia-Pacific, supported by fortification mandates and a shift toward flexitarian diets, is forecast to expand at an 8.79% CAGR through 2031.

Page last updated on: