Wheat Flour Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

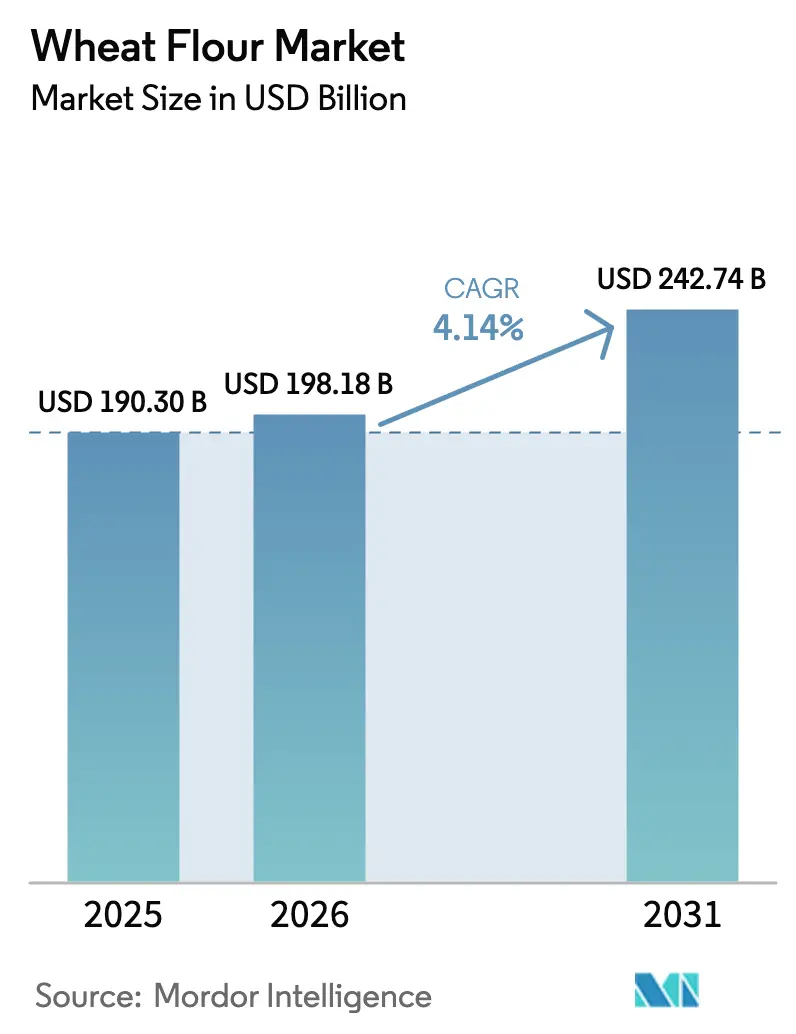

| Market Size (2026) | USD 198.18 Billion |

| Market Size (2031) | USD 242.74 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Wheat Flour Market Analysis by ���ϲ�����

The global wheat flour market size is expected to grow from USD 190.30 billion in 2025 to USD 198.18 billion in 2026 and is forecast to reach USD 242.74 billion by 2031 at 4.14% CAGR over 2026-2031. The global wheat flour market demonstrates consistent growth, driven by its critical role in staple food production, including bakery products, noodles, pasta, and ready-to-eat meals. This growth is particularly strong in densely populated and emerging economies, supported by increasing demand from foodservice and institutional catering channels. All-purpose flour dominates the market due to its broad applicability across industrial and household segments. Meanwhile, whole-wheat and organic flour variants are gaining momentum, propelled by rising health awareness and the premiumization of food products. The competitive landscape is moderately fragmented, with large vertically integrated millers leveraging procurement and distribution efficiencies. Smaller specialty players are differentiating themselves through value-added offerings, such as stone-ground and clean-label formulations. Advanced milling technologies and quality monitoring systems are becoming critical performance drivers, further shaping the competitive dynamics of the market.

Key Report Takeaways

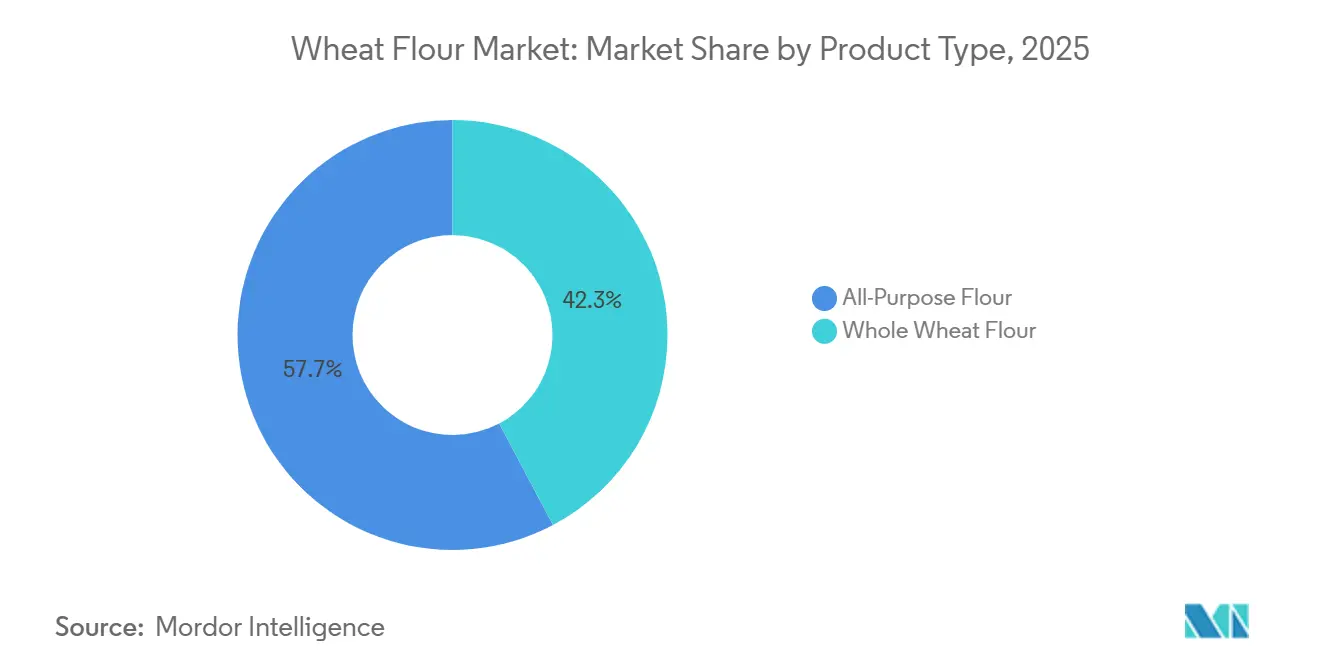

- By product type, all-purpose flour accounted for 57.74% of the wheat flour market share in 2025; whole wheat flour registers the fastest 5.03% CAGR to 2031.

- By category, conventional flour held 90.86% of the wheat flour market size in 2025; organic flour is projected to grow at a 7.21% CAGR through 2031.

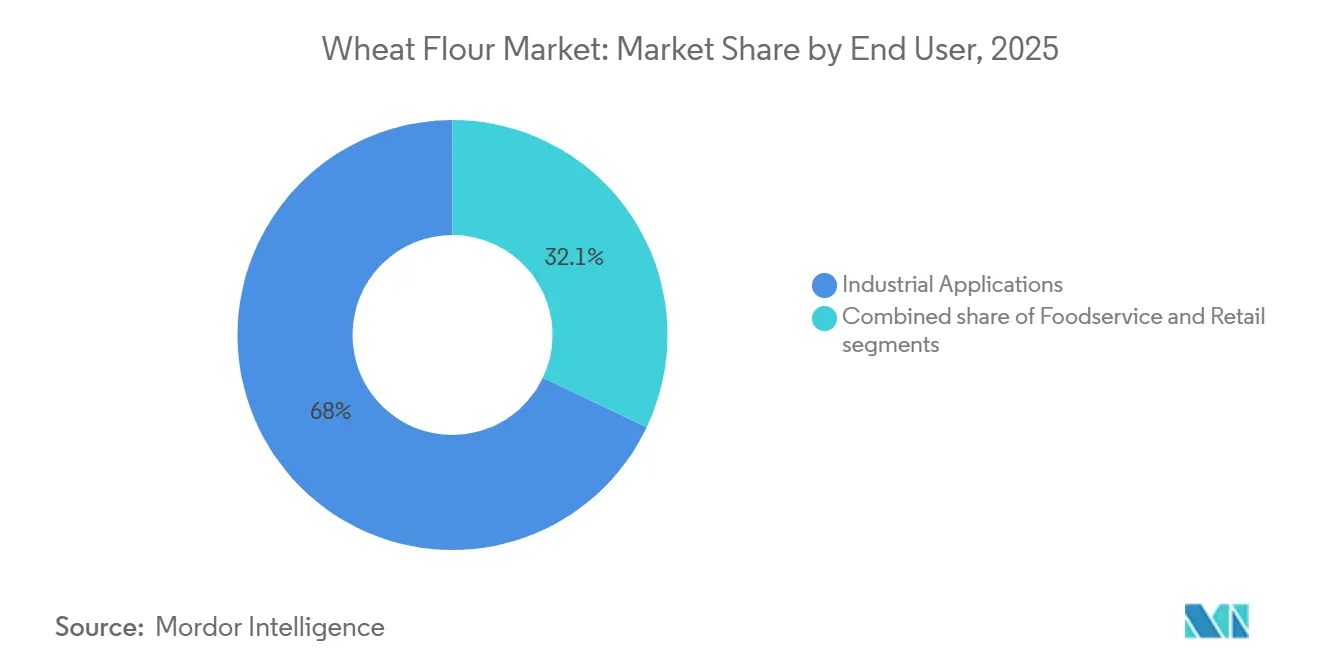

- By end user, industrial processing led with 67.95% of wheat flour market share in 2025, while the foodservice & HoReCa segment is forecast to expand at a 5.86% CAGR to 2031.

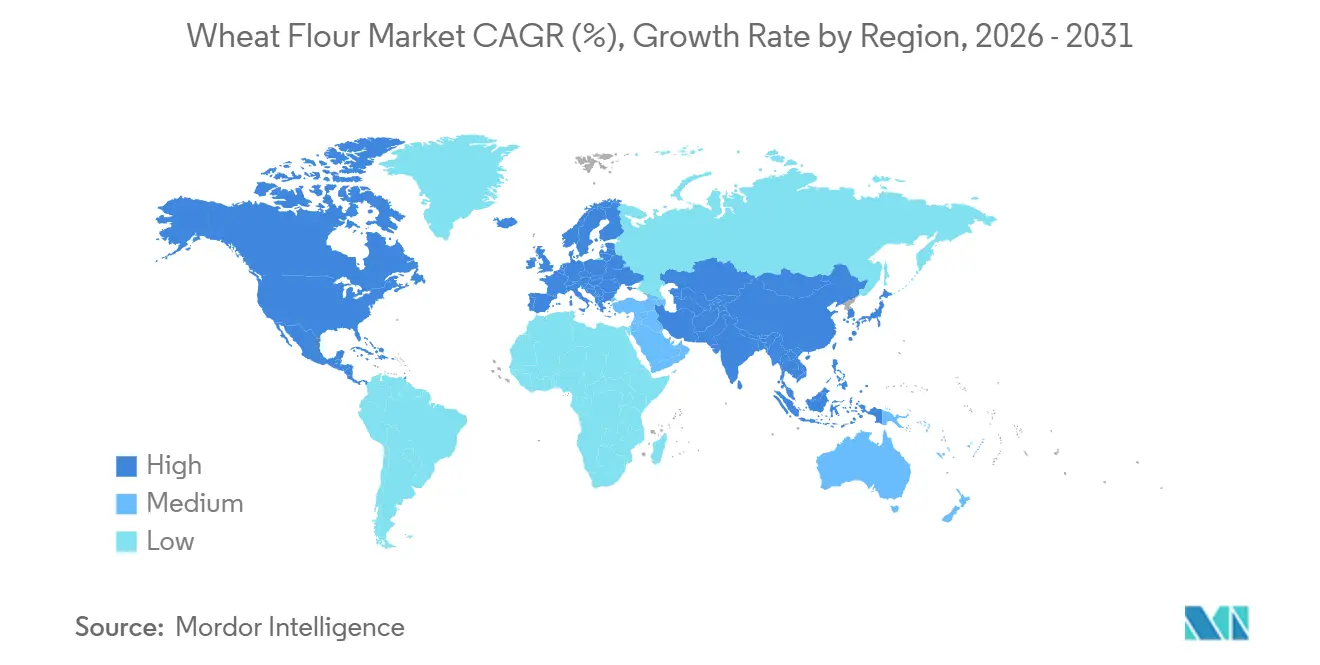

- By geography, Asia-Pacific represented 43.42% of the wheat flour market in 2025, whereas the Middle East & Africa region leads growth at a 6.88% CAGR.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wheat Flour Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for bakery and ready-to-eat foods | +0.9% | Global, with concentration in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Growing consumption of wheat-based snacks and convenience products | +0.7% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Increasing adoption of fortified wheat flour for nutritional benefits | +0.6% | Middle East & Africa, South Asia, select Latin American markets | Long term (≥ 4 years) |

| Surging interest in home baking among consumers | +0.3% | North America, Europe, Australia | Short term (≤ 2 years) |

| Technological advancements in flour milling and processing | +0.5% | Global, led by North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of foodservice, HORECA, and institutional catering sectors | +0.8% | Asia-Pacific, Middle East & Africa, urban South America | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising demand for bakery and ready-to-eat foods

The global wheat flour market is experiencing growth due to increasing demand for bakery and ready-to-eat products, driven by urbanization, rising dual-income households, and the expansion of quick-service restaurants reliant on consistent flour quality. In 2024, U.S. per capita flour consumption accounted for 128.9 pounds [1]Source: Baking Business, "Per capita flour consumption up modestly in 2024", www.bakingbusiness.com, highlighting how consumers are shifting their preferences toward convenience foods, which require efficient, large-scale industrial flour processing. Ready-to-eat formats, including frozen dough, par-baked loaves, and shelf-stable flatbreads, are driving the adoption of specialized flour blends with controlled protein levels and additives tailored for automated production processes. In key markets such as China and India, large industrial bakeries are streamlining their supplier base, prioritizing millers capable of ensuring traceability and meeting stringent food safety standards, often requiring bulk delivery capabilities. This trend is intensifying competition, as smaller regional mills face challenges in meeting certification requirements and volume commitments, thereby strengthening the position of vertically integrated grain processors within the global supply chain.

Growing consumption of wheat-based snacks and convenience products

The global wheat flour market is experiencing growth driven by increasing consumption of wheat-based snacks and convenience foods. Changing consumer lifestyles and the rise of on-the-go eating habits are fueling demand for products such as pasta, noodles, crackers, pretzels, and baked chips across both developed and emerging markets. In the Asia-Pacific region, a strong preference for instant noodles and related products is sustaining demand for specialized wheat flour blends. In North America and Europe, the shift toward baked goods and clean-label snack options is driving the replacement of heavily modified ingredients with wheat flour. According to the United States Wheat Associates Report, global wheat consumption reached approximately 800 million metric tons in 2024 [2]Source: U.S. Wheat Associates, "Global wheat consumption to total", www.uswheat.org. This transition is also reshaping product specifications, as snack manufacturers seek flour with a lighter color, improved texture, and consistent processing performance. To meet these demands, millers are adopting advanced purification, separation, and air-classification technologies. Companies equipped with modern, multi-stage milling infrastructure and strong technical expertise are well-positioned to secure long-term supply contracts. Conversely, traditional mills with limited processing capabilities face increasing competitive pressure to meet the evolving quality standards of large-scale snack producers.

Increasing adoption of fortified wheat flour for nutritional benefits

The fortified wheat flour market is undergoing significant growth as governments and health organizations prioritize enhanced nutritional standards to address deficiencies. Numerous countries now mandate the inclusion of nutrients such as iron, folic acid, zinc, and B vitamins in wheat flour. Governments worldwide are implementing policies to promote the use of fortified wheat flour. In India, the Food Safety and Standards Authority of India (FSSAI) mandates fortification standards for wheat flour under its Food Fortification Resource Centre (FFRC) initiative [3]Source: Food Safety and Standards Authority of India, "Food Safety and Standards (Fortification of Foods) Regulations, 2018", www.fssai.gov.in. This regulatory shift requires millers to implement premix procurement, precise dosing calibration, and rigorous quality testing, which, while increasing production costs, also creates opportunities to secure public procurement contracts and development-finance support. Fortified flour has thus emerged as a strategic differentiator in the market. Strategic partnerships with organizations like UNICEF and the Global Alliance for Improved Nutrition are enabling millers in regions such as Sub-Saharan Africa and South Asia to strengthen technical capabilities and stabilize supply chains. These developments position fortified wheat flour as both a critical public health solution and a competitive advantage in retail and institutional markets.

Technological advancements in flour milling and processing

Global wheat flour markets are undergoing a transformation, driven by technological advancements in flour milling and processing. Automation and smart systems are not only addressing labor shortages but also ensuring consistent quality. Large-scale mills are harnessing platforms that integrate real-time monitoring, machine learning, and predictive maintenance. This integration allows them to optimize efficiency, minimize downtime, and produce flour that meets the uniform specifications demanded by multinational food processors. Such innovations lead to reduced long-term operating costs and bolster competitiveness, especially in securing high-volume contracts. In contrast, smaller mills in regions like South America and Africa grapple with challenges. Their dependence on manual sampling and delayed quality feedback creates a technology gap, hindering their ability to meet the stringent demands of contemporary supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility and climate impact on wheat production | -0.8% | Global, acute in Black Sea region, South America, Australia | Short term (≤ 2 years) |

| Growing consumer preference for gluten-free alternatives | -0.5% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Rising competition from substitute flours | -0.4% | North America, Europe, affluent Asia-Pacific markets | Medium term (2-4 years) |

| Storage challenges and limited shelf life of wheat flour | -0.3% | Sub-Saharan Africa, Southeast Asia, humid tropical regions | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Price volatility and climate impact on wheat production

Fluctuating wheat prices and the escalating impact of climate change on wheat production are imposing significant constraints on the global wheat flour market. Extreme weather events, such as droughts and floods, are disrupting supply consistency and causing sharp fluctuations in raw material availability. These unpredictable price movements are placing considerable pressure on milling margins, particularly for small and mid-sized operators that lack structured procurement strategies, price-hedging mechanisms, or long-term sourcing agreements. In some cases, these challenges have led to temporary shutdowns during periods of elevated input costs. Additionally, the rising frequency of climate-related disruptions is undermining the reliability of traditional supply cycles, complicating production planning, inventory management, and stable pricing for downstream food manufacturers. As a result, sustained profitability increasingly relies on robust financial risk management, diversified sourcing strategies, and stronger integration across the grain value chain, creating a competitive disadvantage for less-capitalized players in the market.

Growing consumer preference for gluten-free alternatives

The increasing consumer demand for gluten-free alternatives is posing significant challenges to the global wheat flour market. This shift, largely driven by lifestyle preferences rather than medical necessity, is transforming premium retail channels. Gluten-free products such as bread, pasta, and baked goods, often commanding premium price points, are progressively replacing shelf space traditionally allocated to conventional flour. The trend is most pronounced in North America and Western Europe, where retailers are expanding their gluten-free portfolios. However, in regions like Asia-Pacific and the Middle East, the adoption remains limited due to cultural reliance on wheat-based staples and issues with taste and texture acceptance. To address this evolving demand, millers are investing in dedicated gluten-free production lines utilizing rice, tapioca, and potato starches. These operations require separate facilities to comply with stringent certification standards, increasing operational complexity and costs while intensifying competition within the market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whole Wheat Gains Despite All-Purpose Dominance

In 2025, all-purpose flour is set to command a dominant 57.74% share of the global wheat flour market. Its versatility spans industrial bakery production, home cooking, and foodservice applications. With a neutral taste, dependable gluten formation, and consistent processing performance, all-purpose flour is the go-to choice for a myriad of products, from breads and noodles to pasta and flatbreads. Meanwhile, whole-wheat flour is gaining traction, boasting a projected CAGR of 5.03% from 2026 to 2031. This surge is largely driven by health-conscious consumers and dietary fiber advocates, prompting food manufacturers and retailers to boost whole-grain content in their offerings. Many are proudly labeling these products as "clean-label" and "100% whole grain," especially in the packaged bread and tortilla segments.

Yet, whole-wheat flour's higher bran and germ content bring challenges. These include a shorter shelf life, a darker hue, and a denser texture, all of which can influence consumer acceptance and processing efficiency. To counteract these hurdles, millers are turning to cutting-edge methods like ultra-fine grinding and controlled heat treatment. These techniques aim to enhance texture, stability, and functionality, all while preserving the flour's nutritional benefits. Despite the rising popularity of whole-wheat variants, all-purpose flour remains indispensable in applications where refined characteristics are paramount, solidifying its status in large-scale industrial settings.

By Category: Organic Acceleration Challenges Conventional Scale

By 2025, conventional flour is expected to dominate the global wheat flour market with a 90.86% share. This dominance is driven by its cost efficiency, large-scale availability, and extensive application across retail, foodservice, and industrial food processing sectors, where consistent quality and price competitiveness are critical purchasing factors. In contrast, organic wheat flour is projected to grow at a CAGR of 7.21% during the forecast period (2026–2031), fueled by increasing consumer demand for certified products associated with health benefits, sustainability, and clean-label attributes. These factors enable brands to command premium pricing and strengthen their market positioning, particularly in developed markets with established organic supply chains and retail networks.

However, the growth of organic flour is constrained by supply and operational challenges, including lower agricultural productivity, higher sourcing costs, and stringent certification requirements. These demands necessitate segregated procurement, traceability, and dedicated processing systems, adding complexity and limiting scalability for millers. Despite these challenges, organic flour offers a high-value opportunity for businesses capable of managing compliant supply chains. Meanwhile, conventional flour maintains its market leadership due to its affordability and suitability for large-scale, high-volume applications.

By End User: Industrial Dominance Faces Foodservice Disruption

In 2025, industrial processing is projected to account for 67.95% of the global wheat flour market. This dominance is attributed to the requirements of large-scale manufacturers in the bakery, pasta, noodle, snack, and ready-to-eat segments, who demand consistent quality, controlled protein levels, and adherence to stringent food safety standards for automated production. Staple baked goods continue to drive high-volume consumption across major regions, while application-specific flours for pasta and noodles foster long-term supply agreements with technologically advanced millers, further strengthening the segment's market position.

During the forecast period of 2026-2031, the foodservice and HORECA sectors are anticipated to grow at a CAGR of 5.86%, driven by the recovery of out-of-home dining and the rising demand for customized flour formats with reliable, just-in-time delivery solutions. Household retail remains a strategic channel for enhancing brand visibility and achieving premium margins, particularly through e-commerce platforms and direct consumer engagement. Additionally, the animal feed segment provides an outlet for lower-grade outputs, supporting operational efficiency despite its limited contribution to overall market value.

Geography Analysis

In 2025, Asia-Pacific dominates the wheat flour market, holding a 43.42% share, driven by substantial wheat production and import reliance that supports the growth of the bakery, noodle, and convenience food industries. Rapid urbanization and increasing disposable incomes are shifting consumer preferences toward packaged and processed wheat-based products, creating opportunities for technologically advanced millers. Mature markets such as Japan and South Korea are experiencing value growth through premium and specialty flours. Despite periodic climate-related output fluctuations, Australia remains a critical wheat supplier in the region.

The Middle East and Africa are projected to grow at a CAGR of 6.88% during the forecast period (2026–2031), supported by strong population growth, urbanization, and government-backed bread consumption programs that ensure consistent demand for flour. High import dependency in several countries sustains milling and re-export activities, with Turkey serving as a major processing hub. However, operational efficiency in parts of Sub-Saharan Africa continues to be hindered by infrastructure and power constraints.

North America and Europe, as mature markets, exhibit stable consumption patterns, with growth primarily driven by demand for organic, whole-grain, and other value-added flours, alongside the recovery of the foodservice sector. In South America, increasing urbanization and evolving dietary trends are driving higher demand for bakery and pasta products. However, economic volatility introduces periodic uncertainties, while smaller markets in major cities are gradually expanding.

Competitive Landscape

The global wheat flour market exhibits moderate fragmentation. The competitive landscape is defined by the presence of numerous regional and global players, each employing diverse strategies to expand their market share. Prominent companies such as Archer Daniels Midland Company, General Mills Inc., and Bunge Global SA have established strong brand equity and extensive distribution networks. These key players are leveraging their resources to drive innovation, introducing products like fortified wheat flour and gluten-free alternatives to align with evolving consumer demands.

In recent years, investments in research and development, along with strategic partnerships, have emerged as critical approaches for companies aiming to strengthen their market position. For instance, General Mills Inc. has been actively channeling resources into research and development to develop healthier wheat flour options, including whole grain and organic variants, addressing the rising demand for nutritious food products. These strategic initiatives not only enhance market presence but also enable companies to mitigate the growing competition from private-label brands and local manufacturers.

The competitive dynamics are further influenced by advancements in milling technologies and increasing demand for wheat flour in emerging economies. For example, countries in the Asia-Pacific region, such as India and China, are witnessing significant growth in demand due to population expansion and shifting dietary habits. In response, companies are scaling up investments to expand production capacities and strengthen distribution networks in these high-growth markets. Additionally, the rising trend of health-conscious consumers opting for fortified and specialty wheat flour products is creating new growth opportunities for market participants. As the market evolves, companies that effectively adapt to these trends and implement strategic initiatives are well-positioned to gain a competitive edge and achieve long-term growth.

Wheat Flour Industry Leaders

-

Ardent Mills LLC

-

General Mills Inc.

-

Archer Daniels Midland Company

-

Bunge Global SA

-

Bob's Red Mill Natural Foods, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: King Milling Co., Michigan's largest flour miller, unveiled a state-of-the-art six-floor, 35,000-square-foot concrete mill at its flour milling complex. With a daily production capacity of 8,000 cwts of flour, this advanced facility enhances operational capabilities and strengthens the company's competitive position in the regional flour milling market.

- August 2024: Ardent Mills announced plans to modernize and expand its flour mill in Commerce City, Colorado. This strategic initiative reinforces the company's commitment to the Mountain West market by enhancing operational efficiency and increasing production capacity to meet the demands of its growing customer base. Upon completion, the Commerce City mill's daily milling capacity will increase by 9,500 hundredweights (cwts), or 475 tons, bringing the total capacity to 28,000 cwts (1,400 tons) per day.

- March 2024: Farmer Direct Foods executed a USD 2 million facility expansion in Salina, Kansas, incorporating additional warehouse space and automated packaging lines designed for 25-pound and 50-pound flour bags. This strategic investment enhances the company's operational efficiency and production capacity for stone-ground grain products derived from Kansas and Colorado wheat.

- January 2024: Bratney, in partnership with Omas, Cimbria, and PHM Brands, commissioned a state-of-the-art flour mill in Richmond, Utah. This facility represents Omas's largest mill installation in North America, strategically designed to support on-demand flour production for the snack food industry.

Global Wheat Flour Market Report Scope

Wheat flour is made by grinding or milling the wheat grain and contains all the constituents of the wheat kernels. The global wheat flour market (henceforth referred to as the market studied) is segmented by type, category, end-user, and geography. By type, the market is segmented into whole wheat flour, all-purpose flour, and others. By category, the market is segmented into organic and conventional. By end user, the market is segmented into industrial applications, foodservice/HoReCa, and household/retail. By geography, the market is segmented into North America, Europe, South America, Asia-Pacific, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| All-Purpose Flour |

| Whole Wheat Flour |

| Organic |

| Conventional |

| Industrial Applications | Food and Beverage Processors | Bakery and Confectionery |

| Pasta and Noodles | ||

| Snacks and RTE Foods | ||

| Other Food Manufacturers | ||

| Animal Feed | ||

| Other Industrial Applications | ||

| Foodservice/HoReCa | ||

| Household/Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Columbia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | All-Purpose Flour | ||

| Whole Wheat Flour | |||

| By Category | Organic | ||

| Conventional | |||

| By End User | Industrial Applications | Food and Beverage Processors | Bakery and Confectionery |

| Pasta and Noodles | |||

| Snacks and RTE Foods | |||

| Other Food Manufacturers | |||

| Animal Feed | |||

| Other Industrial Applications | |||

| Foodservice/HoReCa | |||

| Household/Retail | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Netherlands | |||

| Sweden | |||

| Poland | |||

| Belgium | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Indonesia | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Peru | |||

| Columbia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| South Africa | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the current size of the wheat flour market?

The wheat flour market size stands at USD 198.18 billion in 2026 and is forecast to reach USD 242.7 billion by 2031.

Which region leads the wheat flour market?

Asia-Pacific leads with 43.42% market share in 2025, driven by large populations and mature processing industries.

Which end use segment is growing fastest in the wheat flour market?

The foodservice & HoReCa segment posts the highest CAGR, advancing 5.86% through 2031 as dining-out rebounds.

How is climate change affecting wheat flour supply chains?

Increasing droughts and heat waves have already caused production losses, raising price volatility and forcing millers to diversify sourcing.

Page last updated on: