Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

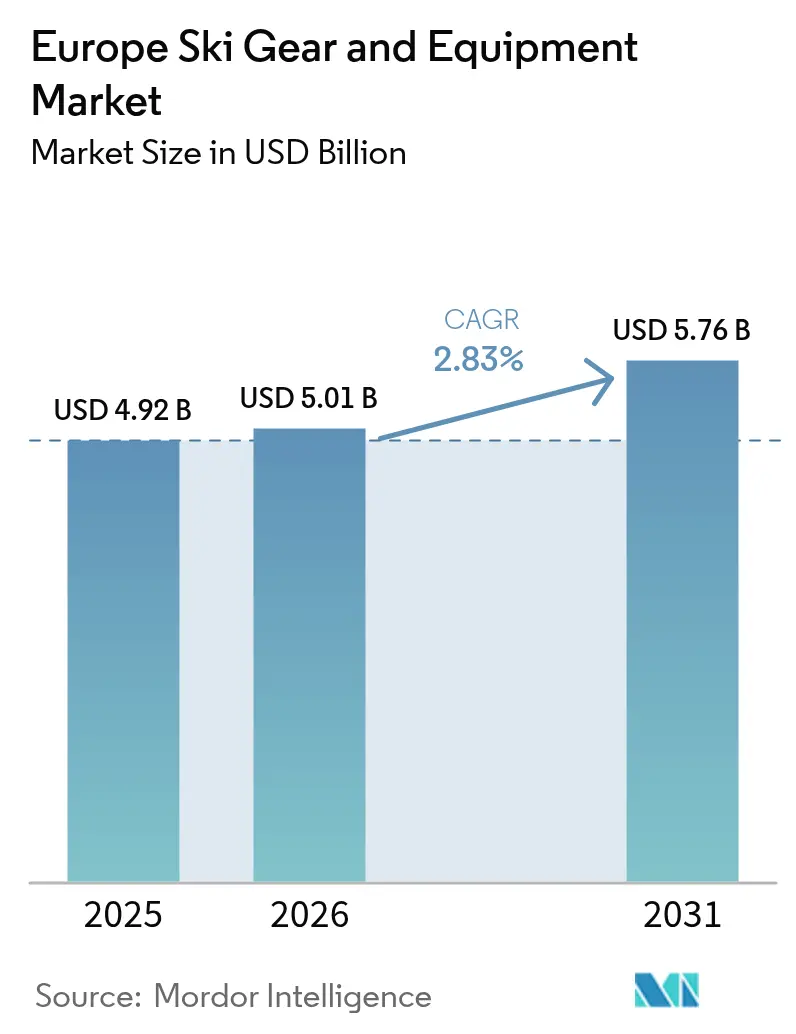

| Base Year Market Size (2025) | USD 4.92 Billion |

| Market Size (2026) | USD 5.01 Billion |

| Market Size (2031) | USD 5.76 Billion |

| Growth Rate (2026 - 2031) | 2.83% CAGR |

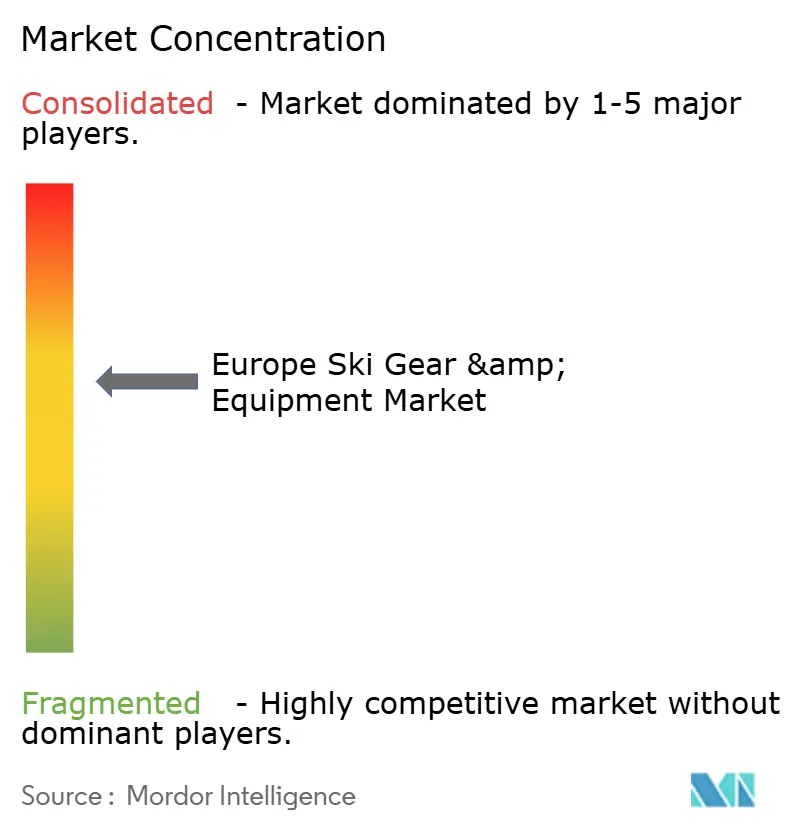

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Europe Ski Gear And Equipment Market Analysis by ���ϲ�����

The Europe ski gear and equipment market size reached USD 4.92 billion in 2025, and is projected to reach USD 5.01 billion in 2026, and USD 5.76 billion by 2031, with a CAGR of 2.83% from 2026 to 2031. Consumer behavior is shifting as rental subscriptions gain popularity, reducing the emphasis on ownership. At the same time, premiumization strategies are enabling brands to maintain margins despite a plateau in total skier-days. Factors such as mandatory helmet laws, school-based youth programs, and EU sustainability regulations are driving shorter replacement cycles for protective gear and apparel. Digital commerce is addressing the advice gap through tools like virtual boot-fit applications, expanding geographic accessibility, and mitigating peak-season stock shortages. Additionally, infrastructure investments in Spain and Eastern Europe are redirecting demand from saturated Alpine regions to emerging markets with fewer altitude-related snow challenges.

Key Report Takeaways

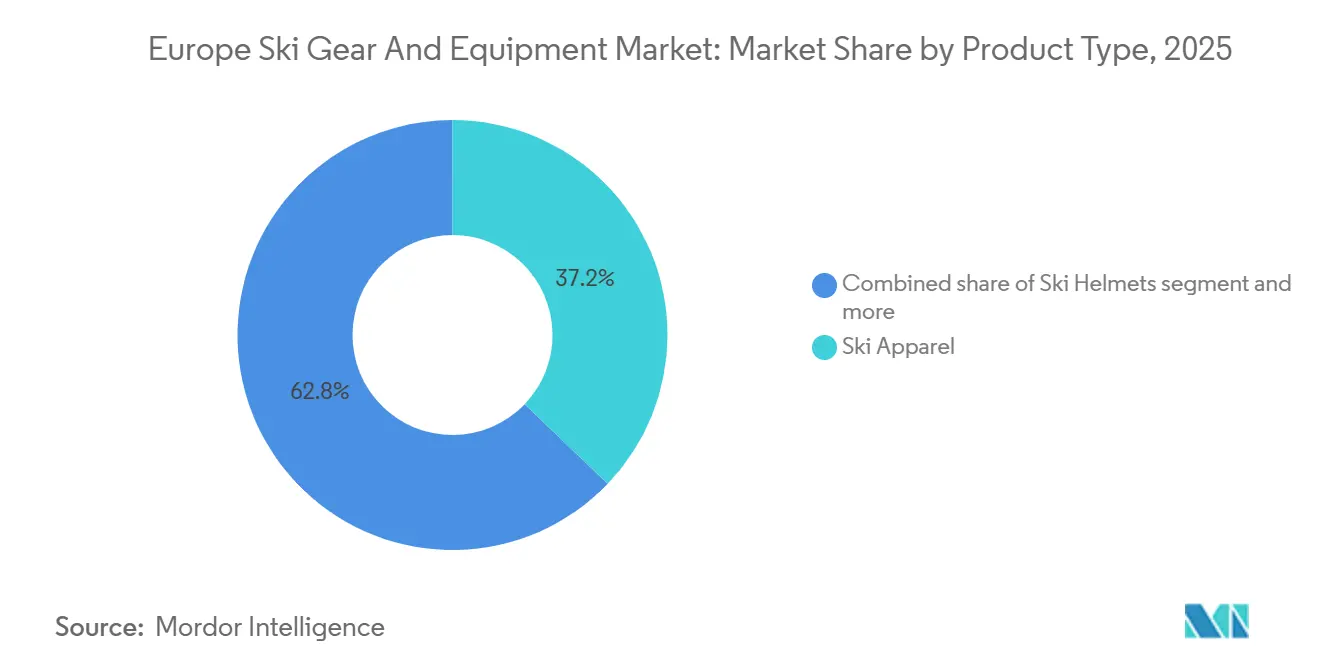

- By product type, ski apparel led with 37.17% share in 2025, while ski helmets posted the fastest 3.38% CAGR forecast for 2026-2031 across the Europe ski gear and equipment market.

- By end-user, male skiers accounted for 59.09% share in 2025, whereas the female segment is on track for a 4.56% CAGR through 2031.

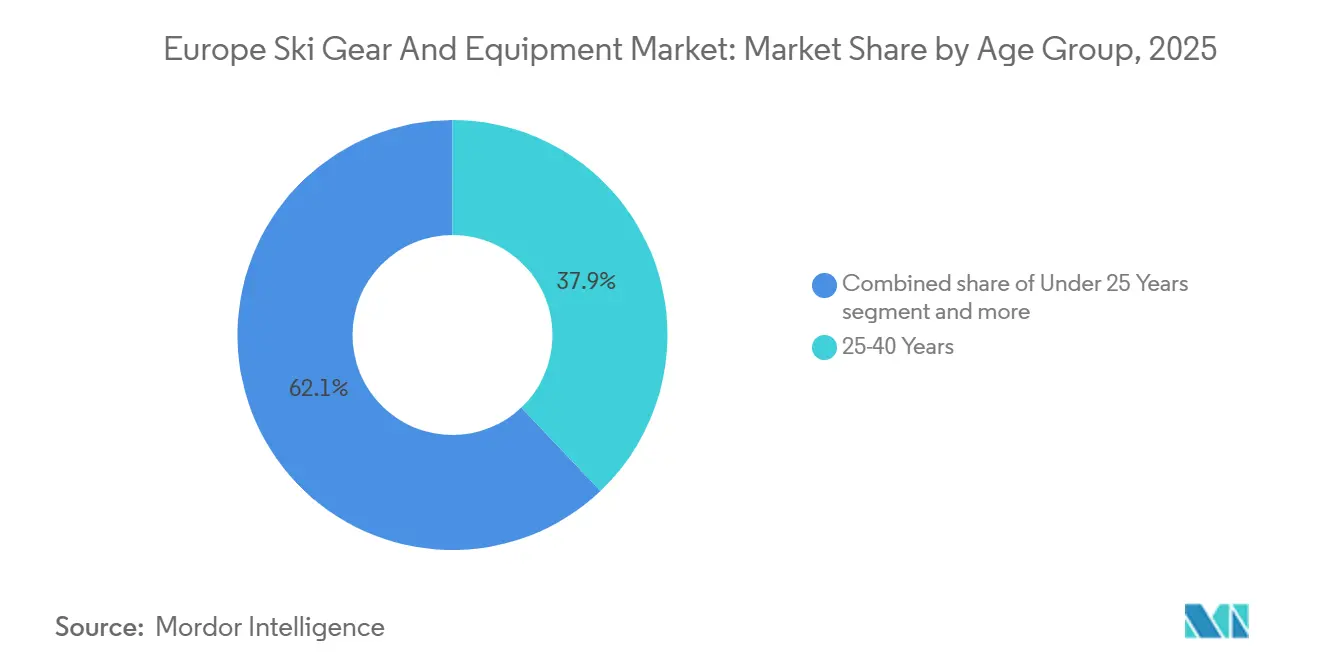

- By age group, the 25-40 years cohort captured 37.91% in 2025, yet the under-25 segment is accelerating at a 5.58% CAGR to 2031.

- By distribution, offline retail stores retained 65.15% share in 2025, but online channels are expanding at a 5.94% CAGR during 2026-2031.

- By geography, Germany held 16.87% share in 2025, while Spain shows the quickest 4.76% CAGR outlook to 2031 for the Europe ski gear and equipment market.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Ski Gear And Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing popularity of winter sports tourism | +0.8% | Germany, Austria, Switzerland, France, spillover to Spain and Italy | Medium term (2-4 years) |

| Expansion of ski resorts and facilities | +0.6% | Spain, Poland, Slovakia, secondary markets in Italy | Long term (≥ 4 years) |

| Rising participation in recreational skiing | +0.5% | Pan-European, concentrated in Sweden, Norway, emerging markets | Medium term (2-4 years) |

| Expansion of ski gear rental models | +0.4% | Urban centers in Germany, France, Netherlands; airport hubs | Short term (≤ 2 years) |

| Focus on sustainability and eco-friendly products | +0.3% | EU-27, led by Germany, France, Scandinavia | Long term (≥ 4 years) |

| Technological innovations in design and materials | +0.3% | Research and Development clusters in Switzerland, Austria, Italy | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Growing popularity of winter sports tourism

The growing popularity of winter sports tourism across Europe is a significant driver for the ski gear and equipment market. Factors such as rising disposable incomes, improved access to ski resorts, and appealing winter travel packages have contributed to increased participation in activities like skiing and snowboarding. According to the Sport England report, approximately 298,500 people in England participated in winter sports between November 2023 and November 2024, up from 290,500 in the previous period, indicating a steady increase in engagement [1]Source: Sport England, "Active Lives Adult Survey November 2023-24", sportengland.org. Similarly, major winter tourism destinations are experiencing robust growth in visitor activity. Statistics Austria reported that overnight stays in Austrian winter tourism accommodations reached 51.35 million from November 2024 to February 2025, a 1.5% rise compared to the previous year, highlighting sustained demand for winter travel experiences[2]Source: Statistics Austria, "Already 51 million overnight stays in the 2024/25 winter season", statistik.at. These developments are encouraging consumers to invest in high-quality ski gear, apparel, and accessories, not only for improved performance and safety but also to enhance their overall winter sports experience. As a result, the growth in participation and tourism is driving the continued expansion of the European ski gear and equipment market.

Expansion of ski resorts and facilities

The expansion and modernization of ski resorts across Europe are key factors driving the growth of the ski gear and equipment market. Upgraded resorts and enhanced facilities improve the skiing experience, attracting more domestic and international tourists and encouraging greater participation in winter sports. As resorts invest in advanced infrastructure, visitors are more likely to purchase high-quality ski equipment, apparel, and accessories, thereby increasing market demand. For instance, in December 2025, Spain’s Sierra Nevada ski resort allocated approximately EUR 19 million for upgrades during the winter season. These upgrades included new conveyor lifts in the Borreguiles beginner area, improved snowmaking systems, renovated on-mountain facilities, and additional snow groomers to enhance slope conditions. This investment reflects a broader trend among European ski destinations to modernize facilities, expand slope capacity, and improve visitor experiences, directly contributing to the growth of the ski gear and equipment market. Additionally, expanded resort facilities often include ski schools, rental shops, and specialized zones catering to both beginners and advanced skiers, driving demand for both entry-level and premium ski products. As resorts continue to improve accessibility and on-mountain services, the demand for high-performance, safety-oriented, and comfort-focused ski gear is expected to grow steadily across Europe.

Rising participation in recreational skiing

The increasing popularity of recreational skiing across Europe is a key driver for the ski gear and equipment market. Factors such as rising disposable incomes, greater leisure time, and improved access to ski resorts have encouraged more individuals and families to adopt skiing as a recreational activity. Demographic changes are also reshaping the participant base, with first-time skiers over the age of 30 constituting a significant share of new participants. This group demonstrates unique purchasing behavior, prioritizing safety, evidenced by helmet adoption rates nearing 100%, and favoring rentals over ownership during their initial seasons. Typically, they transition to equipment ownership after 3-4 seasons of consistent skiing. To address this segment, brands are offering bundled helmets with apparel packages, trade-in credits, and beginner-friendly kits to ease the shift from rentals to ownership. The expansion of recreational skiing is also driving demand for a broader range of products beyond traditional ski gear. Consumers are increasingly investing in high-performance apparel, technical gloves, goggles, and other accessories to enhance both comfort and safety. Furthermore, the growing number of adult beginners has led brands to emphasize ergonomic designs, adjustable equipment, and customizable options, catering to varying body types and skill levels.

Expansion of ski gear rental models

The increasing adoption of ski gear rental models across Europe is driving growth in the ski gear and equipment market. Ski resorts, specialty stores, and online platforms are offering flexible rental options, enabling consumers to access high-quality skis, snowboards, boots, and protective gear without the need for full ownership. This approach is particularly appealing to beginners, occasional skiers, and adult-onset participants who value convenience, cost-effectiveness, and safety. The expansion of rental programs is also encouraging consumers to experiment with premium or technologically advanced equipment that they might not initially purchase. This exposure to high-end products increases brand visibility and can drive future ownership. Additionally, brands and resorts are enhancing customer experiences by bundling rental packages with apparel, helmets, and accessories, creating opportunities for upselling. Rental models also promote sustainable practices by allowing multiple users to share high-quality gear, aligning with the growing consumer focus on environmental responsibility. By reducing entry barriers and providing access to a diverse range of equipment, these rental models are increasing participation in winter sports. This, in turn, is boosting demand for both rental services and eventual personal ownership, contributing to the growth of the European ski gear and equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal dependence of skiing activities | -0.5% | Pan-European, acute in low-altitude resorts (<1,500 meters) in Germany, France, Italy | Short term (≤ 2 years) |

| Intense competition from alternative winter sports | -0.3% | Urban markets in Netherlands, United Kingdom, Germany; youth demographics | Medium term (2-4 years) |

| High cost of ski gear and equipment | -0.2% | Price-sensitive markets in Southern and Eastern Europe | Short term (≤ 2 years) |

| Dependency on tourism trends | -0.2% | Tourism-dependent economies: Austria (Tyrol), Switzerland (Valais), France (Savoie) | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Seasonal dependence of skiing activities

The ski gear and equipment market in Europe is significantly impacted by the seasonal nature of skiing activities, which restricts revenue generation primarily to the winter months. This seasonal concentration limits revenue to a 16–20 week period each year, creating inventory and cash-flow challenges, particularly for independent retailers. During the off-season, demand for skis, snowboards, boots, and accessories declines sharply, resulting in underutilized inventory, higher storage costs, and the need for markdowns to clear unsold stock. This seasonality also reduces revenue predictability and complicates cash-flow management, posing difficulties for smaller retailers and new market entrants in sustaining operations throughout the year. Manufacturers and distributors face similar challenges, as production and supply planning must align with short demand periods, often requiring rapid scaling or temporary workforce adjustments. Additionally, the seasonal dependency limits opportunities for continuous customer engagement and brand loyalty, as purchasing decisions are typically confined to a few peak months. While strategies such as off-season promotions, rental models, and diversification into complementary winter sports equipment can help mitigate some of these challenges, the inherent seasonality of skiing remains a structural constraint on consistent market growth in Europe.

Intense competition from alternative winter sports

The European ski gear and equipment market is experiencing increasing competition from alternative winter sports, which are drawing consumer interest and discretionary spending. As winter sports enthusiasts explore diverse activities, traditional alpine skiing now competes with snowboarding, winter hiking, and cross-country skiing, each requiring specialized gear. Between 2020 and 2025, snowboarding participation in Europe grew at an annual rate of 4.2%, surpassing alpine skiing's 2.1% growth [3]Source: International Ski Federation, fis-ski. This trend is driven by the expansion of terrain parks and the strong appeal of snowboarding among younger consumers. The diversification of winter sports spending limits expenditure on traditional ski equipment, creating challenges for alpine skiing brands in retaining market share. The rise of alternative sports also impacts innovation and pricing strategies, as consumers evaluate the perceived value and excitement of various activities before making purchasing decisions. Retailers and manufacturers must address the evolving preferences of a younger, trend-driven demographic that may favor one activity over another. As a result, the growth of alternative winter sports serves as a structural constraint on the ski gear and equipment market, compelling brands to adapt their product offerings to remain competitive.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Dominates, Helmets Accelerate

Ski apparel accounted for 37.17% of market revenue in 2025, driven by its high replacement frequency and fashion-driven obsolescence cycles, which encourage repeat purchases every 2-3 seasons. The skis and poles segment, while essential, is facing commoditization pressures due to increasing rental penetration. Growth in this segment is further limited by extended replacement cycles, as recreational skiers now replace skis every 7-8 years compared to 5-6 years a decade ago. This shift is attributed to advancements in materials, such as carbon-reinforced cores and sintered bases, which enhance durability. Ski boots are benefiting from customization trends, with innovations like heat-moldable liners and 3D-printed shells improving fit.

Ski helmets are projected to grow at a CAGR of 3.38% through 2031, supported by mandatory helmet laws in Austria (introduced in 2016 for minors and extended to adults in 2024) and Italy (mandating helmet use for all ages by 2025). These regulations are driving the normalization of helmet use across various demographics. The "Others" category, which includes goggles, gloves, and accessories, is experiencing growth through the integration of smart technologies. For instance, goggles equipped with heads-up displays for speed and navigation sold 85,000 units across Europe in 2024-2025, with price points ranging from EUR 400-600 (USD 432-648).

By End-User: Female Segment Outpaces Male Growth

In 2025, the male segment accounted for a dominant 59.09% share of the European ski gear and equipment market, reflecting historically higher participation rates among men. However, the female segment is projected to grow at a notable CAGR of 4.56% through 2031, driven by targeted product development, gender-specific designs, and focused marketing efforts. Ski brands are increasingly acknowledging the purchasing power and influence of female skiers, leading to innovations such as lightweight skis, ergonomically designed boots, stylish apparel, and performance-oriented accessories tailored specifically for women. Furthermore, social media, influencer campaigns, and women-focused ski events are enhancing engagement and fostering brand loyalty among female consumers.

The maturity of the male segment has prompted brands to focus on expanding wallet share rather than participant growth. Affluent male skiers are increasingly investing in premium touring equipment, including skis with integrated climbing skins and lightweight bindings, for backcountry skiing. In contrast, the female segment presents opportunities for both participant growth and wallet share expansion, as more women are entering skiing and snowboarding through beginner programs, ski schools, and recreational packages.

By Age Group: Youth Engagement Drives Future Pipeline

The 25-to-40-year demographic segment is projected to maintain its market dominance, holding a 37.91% market share in 2025. This group exhibits significant purchasing power and established preferences for outdoor recreational activities. They display strong brand consciousness and a consistent willingness to invest in premium-quality, technologically advanced ski equipment and apparel. Their influence as market trendsetters plays a critical role in shaping product demand and driving innovation. Additionally, their participation in organized skiing expeditions and family-oriented recreational activities supports sustained demand for ski equipment.

The under-25 age demographic is expected to achieve the highest growth in the European ski gear and equipment market, with a compound annual growth rate of 5.58% through 2031. This growth is driven by increased youth participation in winter sports, supported by structured youth development programs, educational initiatives, and family-focused winter tourism offerings. This segment shows a strong preference for beginner-level equipment and modern ski gear tailored to young consumers. Market players are fostering this growth through the introduction of equipment rental services and specialized product lines. Additionally, the widespread use of digital media platforms portraying winter sports as aspirational activities further enhances youth engagement, positioning this demographic as a key driver of market growth in Europe.

By Distribution Channel: Digital Gains, Physical Endures

Offline retail stores accounted for 65.15% of the market share in 2025, driven by the tactile nature of ski equipment purchasing. Boot fitting often requires in-person try-ons, and ski selection benefits from expert consultation, which online channels find challenging to replicate. These stores excel in providing personalized shopping experiences and technical expertise, which are critical for specialized equipment purchases. Customers frequently visit specialty stores or brand-owned outlets to test products, receive professional fittings, and obtain expert guidance tailored to their skill level and skiing style. Strategically located in ski resort areas and urban sports retail centers, these stores also cater to tourists' immediate equipment needs. Additionally, they strengthen their market position by offering services such as equipment maintenance, rentals, and customization.

Online retail stores are experiencing the highest growth rate in the European ski gear and equipment market, with a CAGR of 5.94% projected through 2031. This growth is fueled by consumers' increasing preference for convenient shopping options, extensive product selections, and accessibility. E-commerce platforms offer 24/7 shopping access, competitive pricing, detailed product information, and easy comparison tools, appealing particularly to younger and urban consumers. The adoption of digital technologies, such as augmented reality (AR) for virtual fittings, user reviews, and personalized recommendations, enhances the online shopping experience. Furthermore, online retail enables brands to reach customers beyond traditional resort locations, facilitating expansion into new geographical markets.

Geography Analysis

Germany is projected to lead the European ski equipment market with a 16.87% share in 2025. This dominance is attributed to high consumer purchasing power, which supports consistent investment in quality ski gear and apparel. The country's extensive retail networks ensure widespread accessibility to equipment in both urban areas and ski resorts. Additionally, Germany's proximity to the Bavarian Alps, Austria, and Switzerland encourages regular skiing participation. The market's strength is further bolstered by active ski clubs, government support, and well-developed winter sports infrastructure.

Spain's ski equipment market is expected to grow at a compound annual growth rate (CAGR) of 4.76% through 2031. This growth is driven by rising interest in winter sports, increasing disposable incomes, and the expansion of ski tourism infrastructure. Government and tourism agencies actively promote winter sports, particularly in the Pyrenees and Sierra Nevada regions. Improved transportation networks and enhancements to ski resorts have made these areas more accessible to both domestic and international visitors. Additionally, evolving lifestyle preferences toward outdoor activities and greater health awareness among younger populations contribute to market growth.

The United Kingdom, Italy, France, the Netherlands, Switzerland, Austria, and Sweden maintain strong positions in the European ski equipment market, supported by high participation rates and established equipment preferences. France and Austria remain key Alpine destinations, offering extensive lift systems and international appeal, which drive significant rental and premium equipment sales. Switzerland continues to hold a premium market position due to its luxury resorts and advanced infrastructure. Collectively, the Europe ski-gear and equipment market is characterized by a mix of established Alpine regions and emerging high-growth areas. While traditional Alpine markets defend their value share through experience and premium pricing, the market landscape is increasingly influenced by growth in peripheral regions with rising participation and infrastructure development.

Competitive Landscape

The European ski equipment market exhibits moderate concentration, with several established manufacturers holding significant market shares. Key players in the market include Amer Sports, Inc., Skis Rossignol S.A., Fischer Sports GmbH, Tecnica Group S.p.A., and Head Sport GmbH. These companies leverage their strong brand recognition and diverse product portfolios to cater to various consumer segments. Their established market presence is further supported by extensive distribution networks and partnerships with ski resorts and retailers, enabling them to maintain competitive positions. The market also witnesses consistent merger, acquisition, and collaboration activities aimed at geographical expansion and technological advancements.

The primary competitive focus among key players revolves around technological differentiation. Manufacturers invest in proprietary innovations to enhance performance, comfort, and safety features, thereby distinguishing their products in this mature market. For instance, HEAD's EMC (Energy Management Circuit) electronic dampening system exemplifies advanced technology that improves ski stability and reduces vibrations. Additionally, companies are focusing on lightweight composite materials, integrated sensors, and smart connectivity features to cater to the demands of technology-oriented consumers. These innovations not only enhance the user experience but also serve as effective tools for building brand loyalty and supporting premium pricing strategies.

The European ski equipment market offers several growth opportunities. One significant area of potential lies in adaptive equipment designed for older demographics, addressing the needs of the region's aging yet active population seeking comfortable, safe, and high-performance gear. Furthermore, the development of sustainable products using recyclable and biodegradable materials provides manufacturers with an opportunity to differentiate their offerings while complying with environmental regulations. Additionally, the integration of digital services, such as equipment tracking, maintenance notifications, and connectivity with ski resort operations, presents opportunities to enhance customer engagement and create new revenue streams.

Europe Ski Gear And Equipment Industry Leaders

-

Amer Sports, Inc.

-

Skis Rossignol S.A.

-

Fischer Sports GmbH

-

Tecnica Group S.p.A.

-

Head Sport GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BWT Alpine Formula One Team partnered with luxury skiwear and lifestyle brand Perfect Moment Ltd. to introduce a special-edition capsule collection. This collection includes ski jackets, ski suits, performance-oriented ski pants, limited-edition hoodies, T-shirts, and accessories.

- January 2025: Armada launched its first ski boot model, the AR ONE, which incorporates Hybrid Cabrio Construction. This design combines a 3-piece cabrio structure with enhanced performance features. The product range offers boots with flex options of 90, 100, and 120.

- December 2024: Perfect Moment established its first seasonal store in Europe at the Kitzbuhel ski resort in Tirol, Austria. The store will host special in-store events tailored to the Alpine setting.

- November 2024: Blackcrows unveiled the latest version of its Corvus ski for the 2024-25 season. The ski is designed for big terrain and freeriding, featuring a 110mm waist, a 25m turning radius, and a progressive rocker profile.

Europe Ski Gear And Equipment Market Report Scope

Ski gear and equipment are the equipment or special clothing used by skiers for a particular activity.

The Europe ski gear & equipment market is segmented into product type, end-user, distribution channel, and geography. Based on product type, the market is segmented into skis & poles, ski helmets, ski boots, and other protective gear and accessories. Based on end-user, the market is divided into men, women, and children. Based on the distribution channel, the market is segmented into specialty stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into United Kingdom, Germany, Spain, France, Italy, Russia, and the Rest of Europe.

The report offers market size and forecasts for Europe ski gear & equipment market in value (USD million) for all the above segments.

By Product Type

| Skis and Poles |

| Ski Boots |

| Ski Helmets |

| Ski Apparel |

| Others |

By End-User

| Male |

| Female |

By Age Group

| Under 25 Years |

| 25 to 40 Years |

| 40 to 55 Years |

| Above 55 Years |

By Distribution Channel

| Offline Retail Stores |

| Online Retail Stores |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Switzerland |

| Austria |

| Sweden |

| Rest of Europe |

| By Product Type | Skis and Poles |

| Ski Boots | |

| Ski Helmets | |

| Ski Apparel | |

| Others | |

| By End-User | Male |

| Female | |

| By Age Group | Under 25 Years |

| 25 to 40 Years | |

| 40 to 55 Years | |

| Above 55 Years | |

| By Distribution Channel | Offline Retail Stores |

| Online Retail Stores | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Switzerland | |

| Austria | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe ski gear and equipment market in 2026 and where is it headed?

It stands at USD 5.01 billion in 2026 and is projected to reach USD 5.76 billion by 2031, advancing at a 2.83% CAGR.

Which product category generates the most revenue?

Ski apparel holds the largest slice, contributing 37.17% of 2025 sales thanks to rapid style-driven replacement cycles.

What is driving helmet demand across Europe?

Austria and Italy introduced universal helmet laws in 2024-25, lifting adoption and pushing helmets toward a 3.38% CAGR through 2031.

Why is Spain considered the fastest-growing national market?

EUR 85 million in Pyrenean and Sierra Nevada upgrades extend seasons and are lifting Spain’s segment at a 4.76% CAGR.

Page last updated on: