Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 13.68 Billion |

| Market Size (2031) | USD 16.62 Billion |

| Growth Rate (2026 - 2031) | 4.79% CAGR |

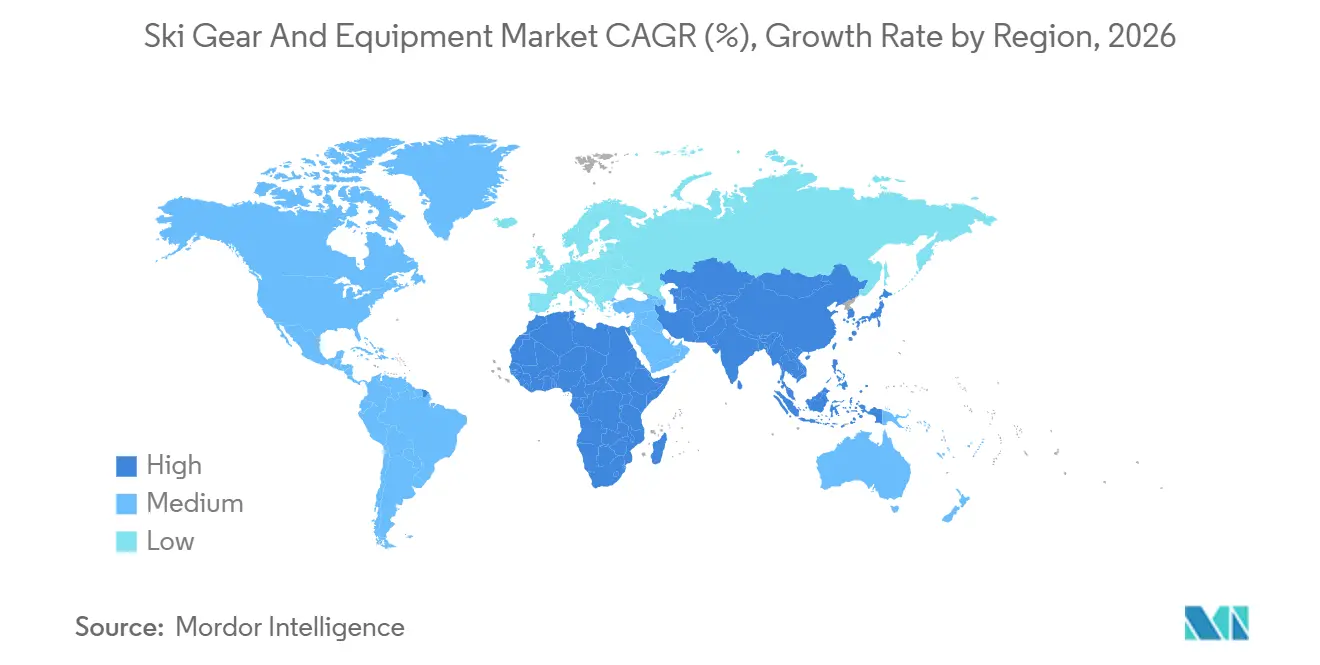

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Ski Gear And Equipment Market Analysis by ���ϲ�����

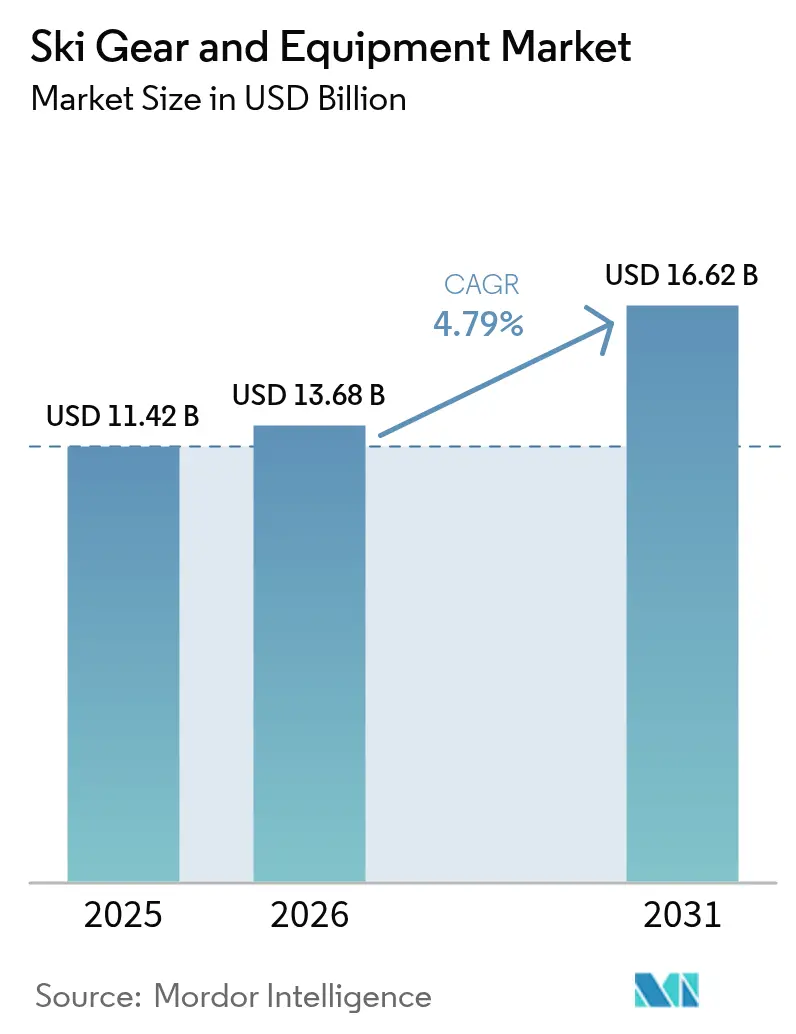

The ski gear and equipment market size is projected to expand from USD 11.42 billion in 2025 and USD 13.68 billion in 2026 to USD 16.62 billion by 2031, registering a 4.79% CAGR between 2026 and 2031. This momentum reflects a pivot from legacy European resorts toward Asia-Pacific indoor venues, ongoing digital disruption, and product‐circularity mandates that reward brands able to scale direct-to-consumer (DTC) channels and sustainable designs. Europe still accounts for 38.92% of 2025 revenue, yet China’s 313 million winter-sports participants and 60 indoor domes expanding at 20% annually signal a lasting geographic rebalancing. At the same time, mandatory safety regulations and sensor-enabled helmets, rapid DTC uptake (Amer Sports 44% 2024 DTC revenue), and algae-based ski cores illustrate how technology and eco-innovation are redefining value capture. Year-round participation, youth training subsidies, and subscription rentals further smooth seasonality, while PFAS bans and climate volatility penalize brands tethered to fossil-based materials or single-channel wholesale models.

Key Report Takeaways

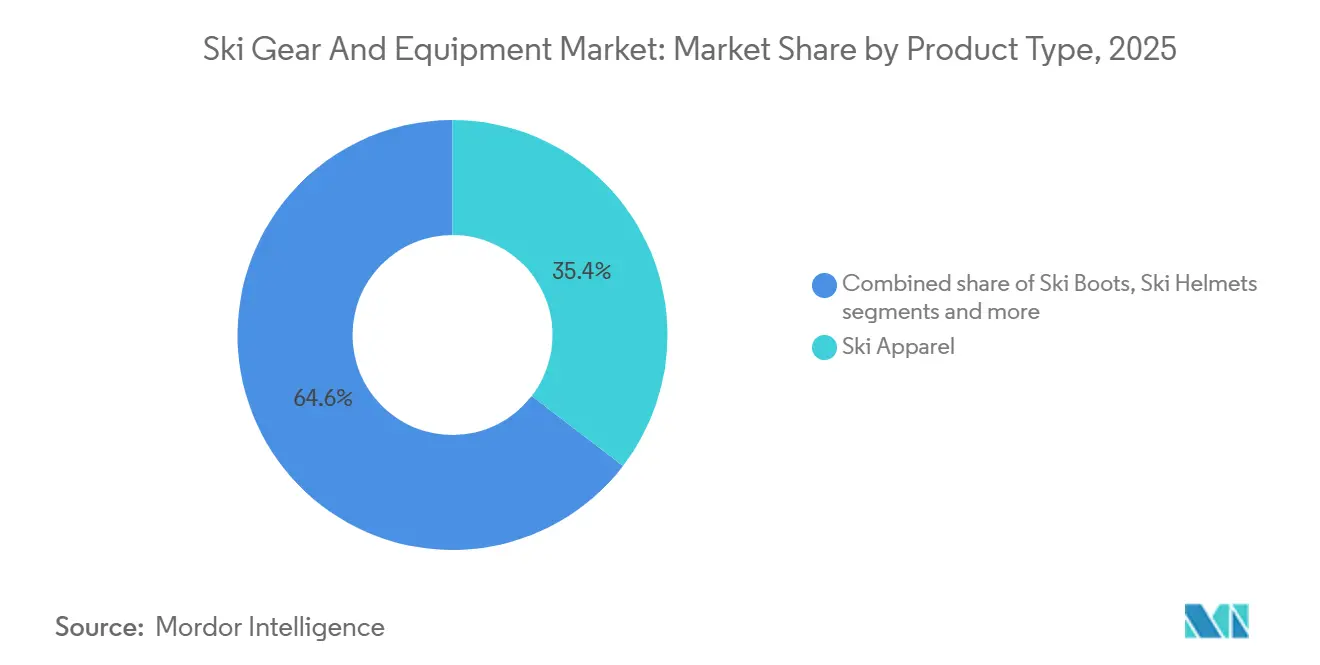

- By product type, ski apparel led with 35.42% revenue share in 2025, while helmets are advancing at a 5.45% CAGR through 2031.

- By end user, males commanded 65.25% of the 2025 demand, whereas the female segment is rising at a 6.42% CAGR to 2031.

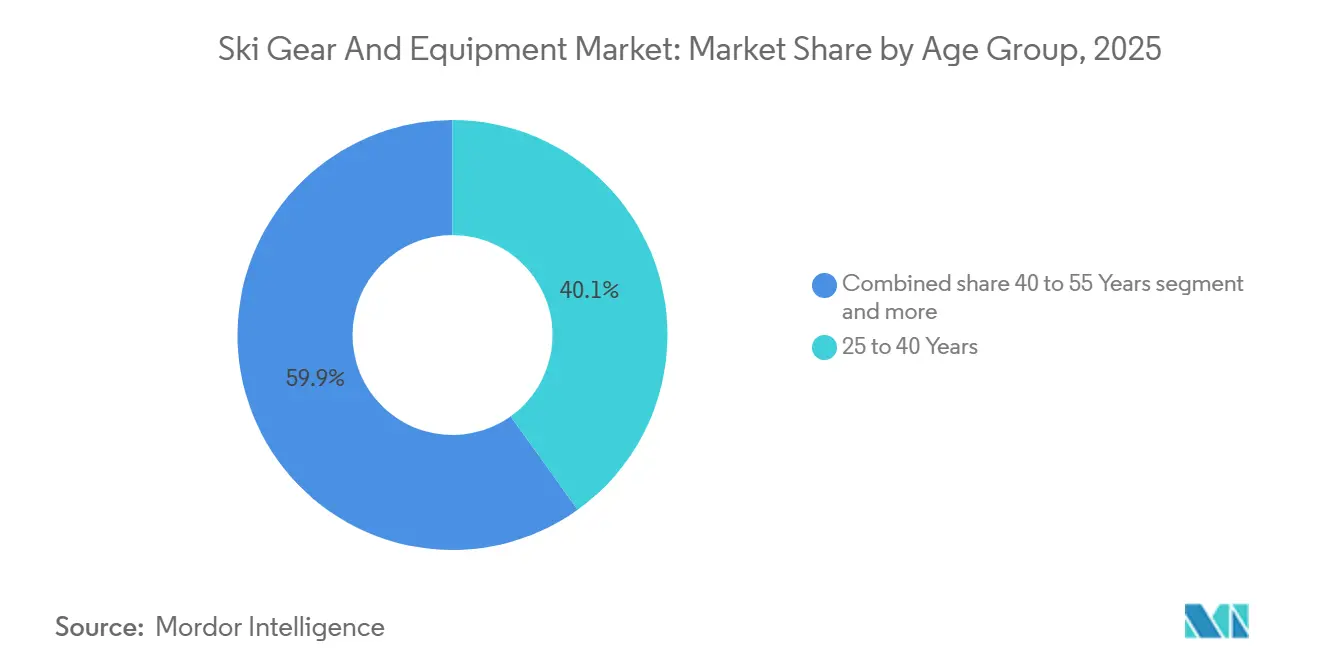

- By age group, the 25-40 cohort held 40.11% of 2025 spending; under-25 participation is growing at a 5.62% CAGR.

- By distribution channel, offline retail controlled 64.58% of 2025 revenue, but online sales are growing at a 6.28% CAGR.

- By geography, Europe captured 38.92% of the 2025 value; Asia-Pacific is expanding at a 5.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ski Gear And Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Popularity of Adventure and Outdoor Activities | +0.9% | Global, with strongest gains in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Winter Sports Tourism Expansion | +1.1% | Europe (Alps, Pyrenees), North America (Rockies, Cascades), Asia-Pacific (China, Japan, South Korea) | Long term (≥ 4 years) |

| Growth in Artificial and Indoor Skiing Facilities | +0.8% | Asia-Pacific (China, Southeast Asia), Middle East (UAE, Saudi Arabia), with spillover to urban Europe | Long term (≥ 4 years) |

| Sustainability and Eco-Friendly Gear Innovations | +0.7% | Europe (driven by EU regulations), North America (consumer-led), Asia-Pacific (emerging) | Medium term (2-4 years) |

| Rising Youth Participation and Ski Training Programs | +0.6% | North America, Europe (Alpine nations), Asia-Pacific (China youth programs) | Medium term (2-4 years) |

| Integration of Advanced Technologies | +0.8% | Global, with early adoption in North America and Europe, scaling in Asia-Pacific | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Growing Popularity of Adventure and Outdoor Activities

By 2024, mountain and nature-based tourism surged back to 87% of its pre-pandemic levels, as reported by the United Nations World Tourism Organization. Notably, segments of adventure tourism, including skiing, outpaced the general leisure travel rebound[1]Source: UNWTO, “Mountain and Nature Tourism Rebounds to 87% of Pre-Pandemic Levels,” unwto.org. This revival is not merely a trend; it is a reflection of shifting consumer priorities. The U.S. Bureau of Economic Analysis highlighted the economic weight of snow sports, pegging their contribution at a robust USD 20.8 billion in 2024. This marks a notable 6.3% year-on-year uptick, largely fueled by millennial and Gen Z consumers who now favor experiences over material possessions. Scotland's snowsports sector showcased its significance, raking in GBP 230 million (USD 291 million) in 2024. A striking 62% of its participants hailed from outside the region, emphasizing skiing's pivotal role in the local economy. For equipment manufacturers, this trend signals a shift: participation in snow sports is evolving from being weather-dependent to a lifestyle choice. This evolution paves the way for a year-round demand, not just for training gear and indoor equipment, but also for apparel that transcends seasons. Brands that market their products as essential to an adventurous identity rather than mere seasonal buys stand to gain significantly. As consumers increasingly seek multiuse, high-performance items, those that emphasize durability and versatility can command premium pricing.

Rising Winter Sports Tourism Expansion

During the 2023-24 season, China recorded 23.08 million skier visits, marking a 16.3% increase from the previous year. The following season, visits surged to 26.05 million. Notably, Harbin alone attracted 87 million tourists, raking in a staggering CNY 124.8 billion (approximately USD 17.2 billion) in revenue, a remarkable 300% increase. In France, mountain sports equipment retailers enjoyed a 6% revenue uptick in 2023-24. Rental services outpaced this growth, expanding by 8%, as short-term visitors increasingly favored the convenience of rentals over ownership. Japan's Niseko region has emerged as a prime destination for Australian snow enthusiasts. Meanwhile, South Korea's PyeongChang, bolstered by its legacy infrastructure, continues to attract a steady stream of domestic participants. A key takeaway is the growing preference for rental-optimized products in tourism-driven demand. Durable, easy-to-fit boots and skis, tailored for high-turnover environments, are eclipsing traditional consumer-grade equipment. Manufacturers focusing on modular, fleet-grade systems that promise a lower total cost of ownership stand to gain significantly. Such innovations will likely secure contracts with resort operators and rental chains, entities that account for 30 to 40% of equipment usage in bustling destinations.

Growth in Artificial and Indoor Skiing Facilities

As of 2024, China boasts 60 indoor ski resorts, expanding at an annual rate of 20%. Notable projects, such as Shanghai's L+SNOW (the globe's largest indoor facility, spanning 90,000 square meters) and Guangzhou's Huafa Snow World, showcase the year-round viability of skiing even in subtropical climates. The Middle East is mirroring this trend: Ski Dubai in Dubai and Trojena in Saudi Arabia (a segment of NEOM) are integrating indoor skiing as a luxury feature in their mixed use developments. These indoor facilities require specialized equipment, including shorter and softer skis designed for controlled settings, helmets with improved ventilation, and apparel suited for the 20 to 25°C temperatures outside the slopes. This equipment deviates from traditional alpine standards. The rise of these indoor venues also means that equipment demand is no longer tied to seasonal cycles. This shift allows manufacturers to stabilize their production schedules and mitigate inventory risks. Brands collaborating with facility operators to co-develop product lines and using real time data to enhance durability and performance are poised to create significant entry barriers. As indoor skiing transitions from a niche novelty to a mainstream activity in emerging markets, these brands stand to gain immensely.

Sustainability and Eco-Friendly Gear Innovations

In 2024, HEAD unveiled its RENEW ski line, integrating 30% recycled materials into its cores and topsheets. Meanwhile, WNDR Alpine introduced the algae based Algal Wall technology, substituting petroleum derived cores and achieving a 40% reduction in carbon footprint per ski. Salomon set an ambitious goal to cut its carbon emissions by 50% by 2030. Rossignol's Essential collection stands out by incorporating 70% recycled polyester in its apparel. These moves not only address regulatory pressures like the EU's PFAS ban impacting wax formulations and DWR coatings but also resonate with consumer sentiments. A report from SnowSports Industries America highlighted that while 79% of participants prioritize sustainability, a mere 28% opted for eco labeled products in 2024, showcasing a notable value action gap. The key opportunity lies in bridging this divide. Strategies like transparent lifecycle labeling, take back initiatives (such as Tecnica's RYB recycling program for boots), and ensuring performance parity to dispel the "green premium" notion can be pivotal. Brands securing the ISO 14001 environmental certification and showcasing concrete metrics like CO2 savings per product are poised to turn consumer intentions into actual purchases. This is especially true for the under 35 demographic, where a brand's sustainability stance significantly sways loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Premium Gear | -0.6% | Global, most acute in emerging markets (Asia-Pacific, South America) and low-income segments in developed markets | Short term (≤ 2 years) |

| Growing Popularity of Alternative Winter Sports | -0.4% | North America (snowboarding, snow tubing), Europe (cross-country skiing, snowshoeing) | Medium term (2-4 years) |

| Seasonal Dependence and Weather Variability | -0.5% | Europe (Alps, Pyrenees facing snow-deficit winters), North America (Rockies, Northeast), with indoor facilities mitigating in Asia-Pacific | Short term (≤ 2 years) |

| High Risk of Injuries | -0.3% | Global, with higher perception barriers in Asia-Pacific markets new to skiing | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

High upfront cost of premium gear

Complete ski equipment packages, including skis, bindings, boots, poles, helmet, and apparel, start at USD 800 for entry level setups and can go up to USD 3,500 for performance oriented kits. This price range creates a capital barrier, deterring price sensitive demographics from trying out skiing. In response to declining participation due to costs, Mount Washington Alpine Resort in Canada rolled out affordability initiatives in 2024, such as subsidized rentals and flexible payment plans. The rental market is evolving, with subscription models gaining traction. For instance, Vail Resorts' My Epic Gear offers an annual membership at USD 50, with daily charges of USD 55 for adults and USD 45 for children. This model allows for multi visit economics, making per use costs more economical than outright ownership. Strategically, brands are advised to split their product portfolios: one line for premium ownership and another for rentals. The rental line should be designed for over 200 cycles and standardized sizing, ensuring maximum efficiency. Brands that overlook this dual channel approach risk losing entry level customers to private label brands from rental operators.

Growing Popularity of Alternative Winter Sports

Snowboarding added 800,000 U.S. participants in 2023-24, while snow tubing and cross-country skiing captured discretionary spending from alpine skiers, particularly among families seeking lower-cost, lower-risk activities, according to Snowsports Industries America. Cross-country skiing requires minimal infrastructure and equipment costs 40-60% less than alpine setups, making it attractive in regions with inconsistent snowfall. The fragmentation of winter sports participation dilutes equipment manufacturers' addressable market unless they diversify product lines: Burton, historically snowboard-focused, has expanded into splitboarding and backcountry gear to capture multi-discipline enthusiasts. The insight is that brand loyalty is weakening as consumers adopt sport-agnostic identities, "winter athlete" rather than "skier", and expect manufacturers to offer cross-compatible gear. Companies that engineer modular systems (e.g., boots compatible with both alpine and touring bindings) will retain customers across activity shifts, while single-sport specialists face market-share erosion.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Helmets Outpace Apparel Growth

In 2025, ski apparel accounted for 35.42% of total revenue, underscoring its status as a repeat purchase category influenced by fashion trends and technical advancements. Meanwhile, ski helmets are projected to grow at a 5.45% CAGR through 2031. This surge is largely attributed to mandatory helmet laws in 23 U.S. states and Canadian provinces, transforming what was once a discretionary purchase into a compliance-driven necessity. Launched in 2024, SCOTT's Flow Pro MIPS helmet is at the forefront of this evolution, boasting features like crash detection sensors, RECCO avalanche reflectors, and twICEme NFC medical ID chips. This positions modern helmets not just as protective gear, but as advanced safety hubs. Ski boots and bindings, together, accounted for 28% of 2025's sales. The "Others" category, which includes goggles, gloves, and various accessories, captured 14.58% of the market. This segment thrives on impulse purchases and gifting occasions. The overarching insight suggests that while helmet manufacturers can harness regulatory changes and tech advancements for premium pricing, apparel brands face the challenge of balancing technical performance with aesthetic appeal to maintain growth in a saturated market.

Sustainability is becoming a cornerstone of product development across the board. Rossignol's Essential collection is leading the charge, utilizing 70% recycled polyester in its jackets. HEAD's RENEW skis are crafted with 30% recycled materials, and G3's Ion bindings are fully recyclable. Starting in 2024, the EU's General Product Safety Regulation (GPSR) will enforce digital product passports for helmets and protective gear. This regulation mandates manufacturers to transparently document material sourcing, lifecycle impacts, and disposal methods. Brands like Tecnica, with its RYB boot, take back initiative, and those achieving ISO 14001 environmental certification are poised to stand out in a landscape increasingly wary of greenwashing. The competitive landscape is evolving. It is shifting from a focus on product features to a deeper, values-based positioning. This shift is especially pronounced among consumers under 35, who are increasingly prioritizing brands that resonate with their environmental and social values.

By End User: Female Segment Drives Demographic Shift

In 2025, male consumers made up 65.25% of the demand, highlighting skiing's traditional male dominance. However, female participation is on the rise, growing at a 6.42% CAGR through 2031. This surge is fueled by targeted initiatives, gender inclusive product designs, and marketing strategies that prioritize community over competition. Data from China's 2024 25 season shows a significant shift: 71.3% of skiing enthusiasts are now female, highlighting the Asia Pacific region's pivotal role in reshaping the sport's demographic. Coalition Snow, a brand founded by women, is tapping into this shift by designing skis tailored for women, featuring specific flex patterns and shorter lengths, an area largely ignored by traditional manufacturers. In 2024, SnowSports Industries America noted a notable uptick in skiing diversity across gender, age, and ethnicity, with female participation climbing from 38% to 41% of the total skier base. This shift signals a need for brands to evolve[2]Source: SnowSports Industries America, "SnowSports Industries America: 79% Consider Sustainability Important." snowsports.org.

Instead of the outdated "shrink it and pink it" approach, brands should focus on engineering products that cater to women's unique biomechanical needs (like a lower center of gravity and narrower boot lasts) and aesthetic preferences that challenge traditional gender norms. While males still dominate in numbers, their growth is slowing, especially as participation levels off in key markets such as the U.S. and Europe. Notably, the median age of skiers in these regions hit 37 in 2024, signaling an aging demographic. Brands that invest in R&D for female-centric products and back women's ski programs stand to gain significantly in this rapidly expanding market. Conversely, those sidelining female consumers may find themselves squeezed as competition for the stagnant male segment heats up. Beyond just products, there is a strategic advantage: female skiers tend to buy apparel and accessories individually, leading to more frequent transactions and greater lifetime value. In contrast, their male counterparts often focus on spending on durable goods.

By Age Group: Youth Programs Fuel Under-25 Expansion

In 2025, the 25 to 40 age group accounted for 40.11% of total revenue, marking their peak earning years and discretionary spending power. However, the under-25 demographic is witnessing a robust growth, with a 5.62% CAGR projected through 2031. In a bid to democratize access, U.S. Ski & Snowboard rolled out its revamped Alpine Development program in February 2025, offering a 50% subsidy on costs for regional athletes aged 14 to 21. This initiative aims to dismantle the financial barriers that have traditionally confined participation to more affluent families. Data from China for the 2024 to 25 period revealed that 52% of participants were aged 24 to 30. Moreover, parent-child family groups constituted a significant 54% of the gross merchandise value, underscoring the trend where youth involvement is a catalyst for multi-generational equipment purchases. The 40 to 55 age bracket, while contributing 28% to the revenue, showcased the highest per capita spending, gravitating towards premium gear and curated experiences. In contrast, the segment above 55, accounting for 12% of the revenue, placed a premium on comfort, safety, and user friendliness over sheer performance.

Brands targeting the youth demographic should consider engineering products with adjustable features. For instance, implementing systems like the "Grow With Me" helmet sizing, which adapts to head growth over 3 to 4 years, can align product lifecycles with children's developmental milestones. This approach not only curtails the frequency of replacements but also enhances the perceived value among budget-conscious parents. On the other hand, the 40 to 55 age group emerges as a lucrative yet underserved premium market. Products that prioritize injury prevention, like knee braces and impact-absorbing boot liners alongside features emphasizing ease of use (such as Burton's Step On X step-in bindings) and comfort (including heated insoles and ergonomic boot designs) are poised to fetch higher margins compared to their performance-centric counterparts. While the 25 to 40 demographic is the largest revenue contributor, they also exhibit heightened price sensitivity and brand fluidity. This necessitates that manufacturers pivot their strategies towards digital engagement, influencer collaborations, and immersive marketing experiences, rather than relying solely on product differentiation.

By Distribution Channel: Direct-to-Consumers Reshapes Retail Economics

In 2025, offline retail stores accounted for 64.58% of distribution, supported by specialty shops offering expert fittings, immediate product availability, and trade-in programs that foster customer loyalty. Meanwhile, online channels are projected to grow at a 6.28% CAGR through 2031, driven by direct-to-consumer brands and subscription models like Amer Sports. In 2024, Amer Sports' direct-to-consumer (DTC) revenue constituted 44% of its total sales. Notably, Arc'teryx experienced a 42.8% growth in DTC sales, while Salomon's DTC sales expanded by 52.6%. These figures underscore the superior margins and customer lifetime value that digital channels offer compared to wholesale. Vail Resorts introduced its "My Epic Gear" subscription service in 2024, featuring a USD 50 annual membership alongside daily rental fees (USD 55 for adults and USD 45 for children). The service also incorporates 3D foot scanning apps to recommend boot models, leading to an 18% reduction in return rates and successfully converting renters into future buyers through personalized data insights. Deloitte forecasts that by 2027, sporting goods e-commerce will constitute 30% of total spending, a trend accelerated by the pandemic's digital shift and Gen Z's inclination towards online research and purchases.

While offline retail remains paramount for high involvement purchases like boots, where precise fitting is crucial for performance and injury prevention, digital channels have gained traction in apparel, accessories, and repeat purchases where tactile evaluation is less critical. The competitive landscape is evolving from channel conflict to integration. Brands that provide a cohesive online-to-offline experience, like online ordering with in-store pickup, virtual try-on features, and consolidated loyalty programs, are poised to outpace pure play retailers lacking these omnichannel capabilities. Starting in 2024, the EU's General Product Safety Regulation (GPSR) mandates online marketplaces to ensure product compliance and uphold digital documentation[3]. This regulation, championed by the European Commission, heightens entry barriers for smaller sellers and favors established brands with the necessary regulatory infrastructure. Consequently, while DTC growth is likely to gravitate towards large, well-capitalized brands, independent retailers are urged to carve a niche through localized services, community involvement, and curated product selections.

Geography Analysis

In 2025, Europe accounted for 38.92% of global revenue, with Alpine nations leading the charge, thanks to their deep-rooted skiing culture and well-established infrastructure. In the 2023-24 season, mountain sports equipment retailers in France saw a notable revenue uptick, buoyed by an 8% growth in rental services driven by short-term tourists prioritizing convenience. However, this growth was not uniform across the regions. Isère surged by 15%, while Jura and Vosges faced declines of 24% and 30%, respectively, hampered by inadequate snowfall at lower altitudes. Germany, Austria, and Switzerland together command 55% of Europe's demand, bolstered by affluent per capita incomes, a dense network of resorts, and government-backed youth programs. Yet, challenges loom with an aging demographic and dwindling birth rates. The key takeaway is that European brands should pivot towards premium, sustainability-driven products for better margins in a tight market and explore adjacent categories like ski touring and backcountry gear, appealing to enthusiasts seeking alternatives to bustling resorts.

Asia-Pacific is on a growth trajectory, boasting a 5.67% CAGR through 2031. China's ice and snow economy, valued at USD 133.8 billion in 2024, is set to soar to USD 206.9 billion by 2030. This surge is underscored by a 25% year-on-year jump in consumer spending, hitting USD 25.9 billion in 2024-25, as reported by the State Council of China. China's 60 indoor ski resorts, witnessing a 20% annual growth, are predominantly in southern provinces like Zhejiang and Guangdong. This strategic positioning allows for year-round skiing in subtropical climates, making demand less susceptible to seasonal weather fluctuations. Meanwhile, Japan's Niseko region continues to draw Australian powder enthusiasts, and South Korea's PyeongChang, with its legacy infrastructure, bolsters domestic participation. Manufacturers that localize, like Ninghai County in China, producing 60% of the world's ski poles, and customize products to regional tastes, such as shorter skis for indoor use and helmets with better ventilation, stand to gain as Asia-Pacific solidifies its winter sports foothold.

North America's demand is anchored by prominent resort clusters in the Rocky Mountains, Cascades, and Northeast. North American brands are increasingly adopting digital-first strategies, as seen with Vail Resorts' My Epic Gear subscription model and Amer Sports' direct-to-consumer (DTC) expansion. These brands harness e-commerce and data analytics to tailor offerings and streamline customer acquisition. While Mexico's skiing market remains in its infancy, characterized by limited infrastructure and low participation, the nation's burgeoning middle class and rising domestic tourism present a tantalizing long-term opportunity. In South America, niche segments are thriving. Chile's Andes resorts draw regional tourists, and in the Middle East, Ski Dubai in the UAE and Trojena in Saudi Arabia are elevating indoor skiing to a luxury status within mixed-use developments. This diverse landscape suggests that manufacturers should tailor their strategies. Focus on premium, sustainable products in Europe, cater to volume-driven entry-level gear in Asia-Pacific, and embrace digital-first DTC models in North America for optimal portfolio performance.

Competitive Landscape

In the ski gear and equipment market, established conglomerates like Amer Sports and VF Corporation find themselves in competition with specialized independents like Coalition Snow, WNDR Alpine, and Black Crows. The market showcases moderate fragmentation. Strategic patterns reveal a division, with large players focusing on vertical integration and expanding direct-to-consumer channels. Amer Sports' direct-to-consumer revenue increased to 44% in 2024. Meanwhile, niche brands differentiate through sustainability narratives, gender-inclusive design, and direct community engagement. VF Corporation's 2024 announcement of potential divestitures (Supreme, Vans) signals portfolio rationalization as conglomerates exit non-core categories to focus capital on high-margin outdoor segments. White space opportunities are concentrated around circular economy business models, subscription-based rental services, and technology-embedded products (e.g., crash detection helmets, 3D scanned boot fitting).

Emerging disruptors like WNDR Alpine use algae-based ski cores to reduce carbon footprints by 40 percent, appealing to sustainability-focused consumers willing to pay 15 to 20 percent premiums for verified environmental credentials. Technology adoption is reshaping competitive dynamics. The International Ski Federation's 2024 mandate for microchip-embedded racing suits to monitor aerodynamic compliance in real time demonstrates how regulatory bodies are accelerating innovation cycles, compelling manufacturers to invest in sensor integration, data analytics, and connected device ecosystems.

Anta uses Amer's brands to penetrate Western markets while Amer gains access to Anta's Asian distribution networks. Brands lacking either scale economies (to absorb direct-to-consumer infrastructure costs) or differentiated positioning (to command premium pricing) risk margin compression, as the middle market erodes between low-cost, high-volume players and high-margin, values-driven specialists. ISO 14001 environmental certification and ASTM safety standards are becoming standard requirements rather than differentiators, pushing companies to compete on intangible brand attributes such as community, authenticity, and purpose that resist commoditization.

Ski Gear And Equipment Industry Leaders

-

Amer Sports, Inc.

-

Rossignol S.A.

-

Head Sport GmbH

-

Fischer Sports GmbH

-

Tecnica Group S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Lange introduced a new line of ski boots called the Lange Concept, offering models for both men and women with flex ratings from 75 to 120. The higher-flex models incorporate a single BOA H+i1 system for lower boot closure.

- February 2025: All-new Redster skis and boots lead the 25/26 lineup, engineered to bring race-inspired performance to the piste, while goggles and helmets complete the collection with added clarity and protection.

- March 2025: J.Crew and United States Ski and Snowboard formed a three-year partnership, establishing J.Crew as the organization's official lifestyle-apparel partner. The collaboration combines J.Crew's après-ski apparel expertise with US Ski and Snowboard's objectives.

- March 2025: BWT Alpine Formula One Team collaborated with luxury skiwear and lifestyle brand Perfect Moment Ltd. to launch a special-edition capsule collection. The collection includes signature ski jackets, ski suits, performance-driven ski pants, limited-edition hoodies, T-shirts, and accessories.

Global Ski Gear And Equipment Market Report Scope

Ski Gear and Equipment refers to the equipment used by a skier, which includes Skis and snowboards, Ski Boots, Ski Apparel, Ski Protection, and others. The ski gear and equipment market is segmented based on product type, distribution channel, and geography. The scope of the global ski gear and equipment market is segmented, based on product type, into skis and poles, ski boots, and ski protective gear and accessories, based on distribution channels into online retail stores and offline retail stores. Further, the market is segmented by geography into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD Million).

By Product Type

| Skis and Poles |

| Ski Boots |

| Ski Helmets |

| Ski Apparel |

| Others |

By End-User

| Male |

| Female |

By Age Group

| Under 25 Years |

| 25 to 40 Years |

| 40 to 55 Years |

| Above 55 Years |

By Distribution Channel

| Offline Retail Stores |

| Online Retail Stores |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Netherlands | |

| Swotzerland | |

| Austria | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Skis and Poles | |

| Ski Boots | ||

| Ski Helmets | ||

| Ski Apparel | ||

| Others | ||

| By End-User | Male | |

| Female | ||

| By Age Group | Under 25 Years | |

| 25 to 40 Years | ||

| 40 to 55 Years | ||

| Above 55 Years | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Swotzerland | ||

| Austria | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large will the ski gear and equipment market be by 2031?

The ski gear and equipment market size is forecast to reach USD 16.62 billion by 2031, up from USD 13.68 billion in 2026 at a 4.79% CAGR.

Which product category is growing fastest?

Helmets are the fastest-growing category, advancing at a 5.45% CAGR through 2031 thanks to safety mandates and sensor integration.

Why is Asia-Pacific critical for future sales?

Asia-Pacific posts a 5.67% CAGR, fueled by China’s 700 resorts, 60 indoor domes, and policy support that targets a CNY 1.5 trillion ice-and-snow economy by 2031.

How are brands addressing high equipment costs?

Subscription rentals like Vail Resorts’ My Epic Gear and take-back programs lower ownership barriers while feeding data into future product designs.

Page last updated on: