Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

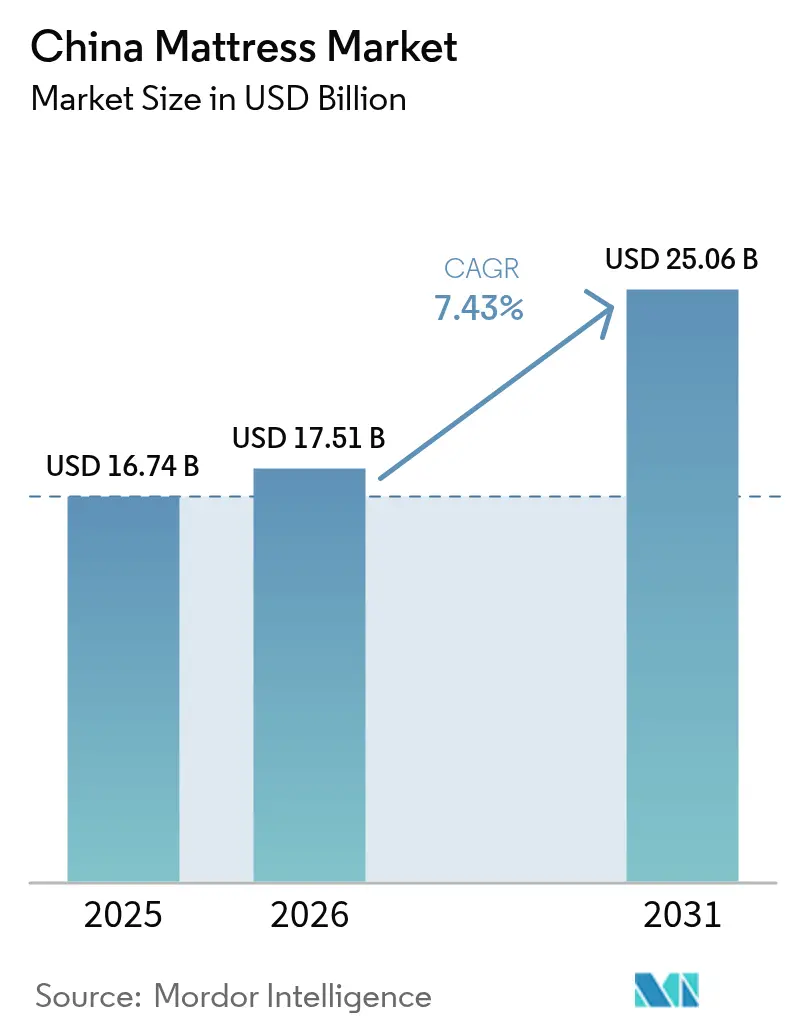

| Base Year Market Size (2025) | USD 16.74 Billion |

| Market Size (2026) | USD 17.51 Billion |

| Market Size (2031) | USD 25.06 Billion |

| Growth Rate (2026 - 2031) | 7.43% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

China Mattress Market Analysis by ���ϲ�����

The China mattress market size is projected to expand from USD 16.74 billion in 2025 and USD 17.51 billion in 2026 to USD 25.06 billion by 2031, registering a CAGR of 7.43% between 2026 and 2031. Operators track a step-up from the 2019–2025 growth arc as premiumization, sleep-health positioning, and omnichannel coverage expand the addressable base beyond new-home completions. Urban consumers in tier-two and tier-three cities lift upgrade cycles on the back of rising disposable income and stronger awareness of ergonomic support. The shift to bed-in-a-box logistics extends same-day and next-day delivery into hundreds of lower-tier cities, lowering last-mile costs and de-risking online trials. National health policy under Healthy China 2030 reframes mattress choice as a sleep-health decision and reinforces institutional adoption in eldercare and workforce wellness programs[1]Source: National Bureau of Statistics of China, “Statistical Communiqué and Real Estate Indicators,” National Bureau of Statistics of China, stats.gov.cn .

Key Report Takeaways

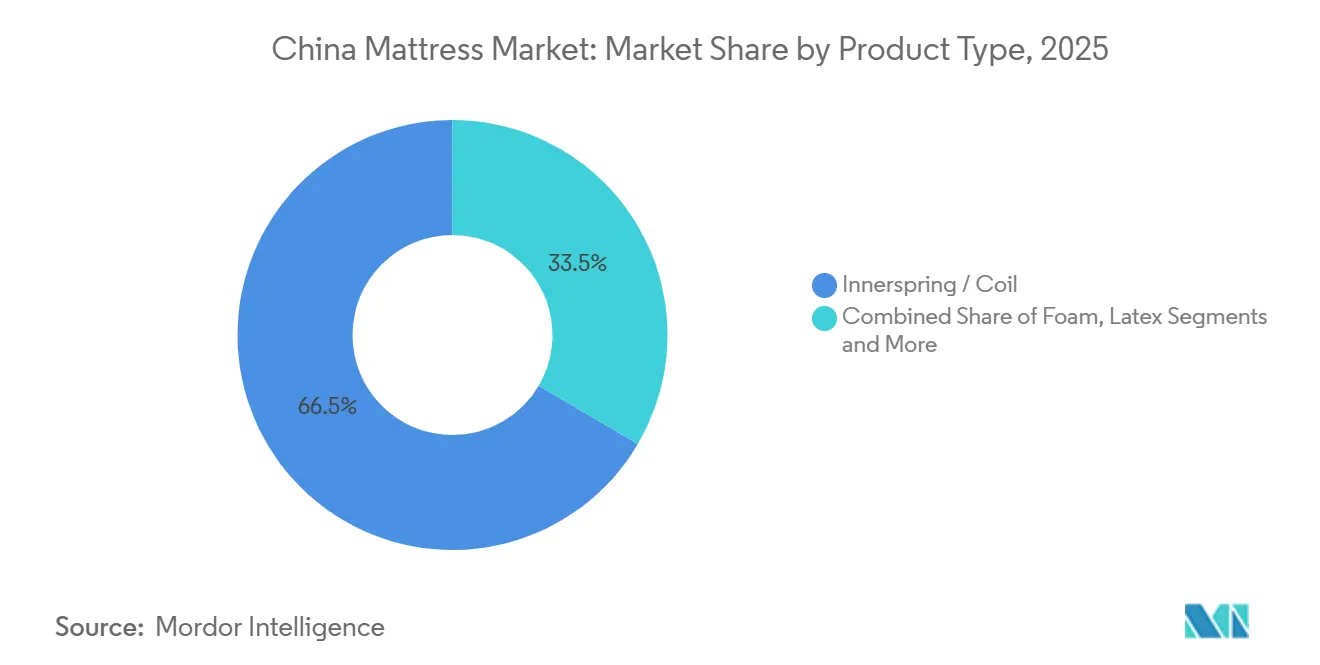

- By product type, innerspring led with 66.53% of the Chinese mattress market share in 2025, while foam is forecast to expand at an 8.22% CAGR through 2031.

- By mattress size, king-size models commanded 41.53% of the Chinese mattress market share in 2025, while queen-size variants are projected to grow at an 8.04% CAGR to 2031.

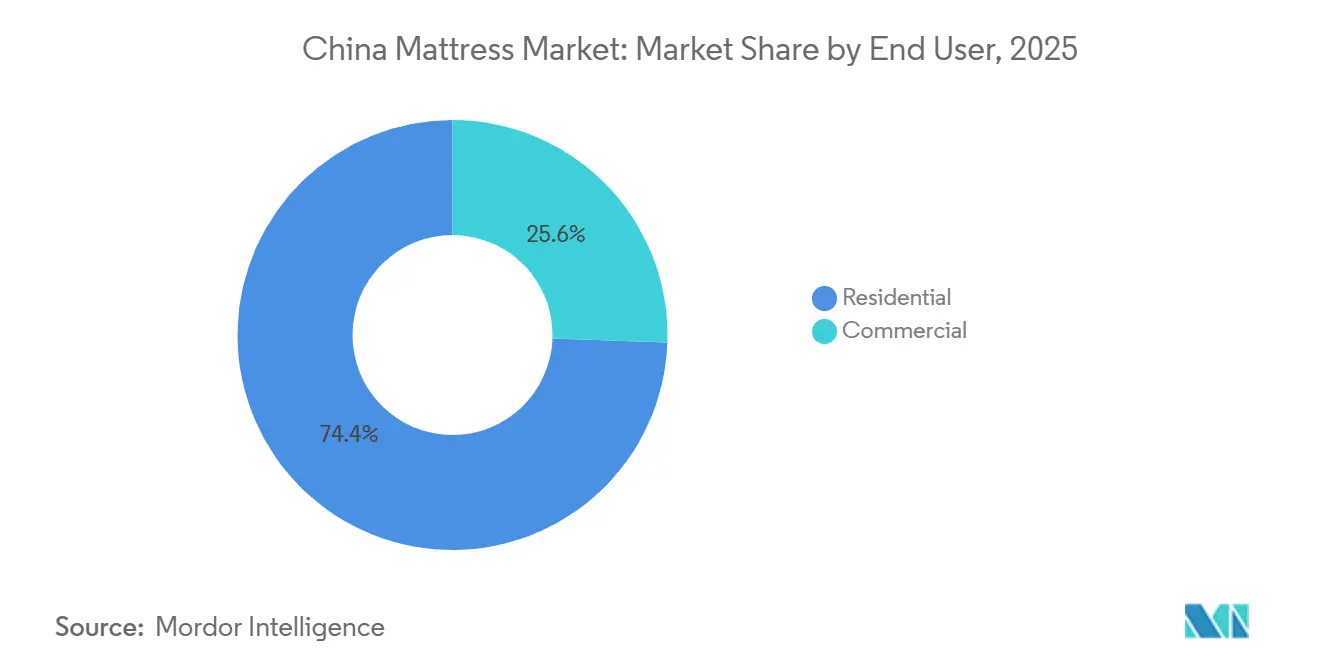

- By end user, residential accounted for 74.44% of the China mattress market share in 2025, while commercial channels are forecast to rise at an 8.40% CAGR to 2031.

- By distribution channel, the B2C segment held 75.25% of the China mattress market share in 2025, and B2C is projected to post the fastest CAGR at 9.36% through 2031.

- By geography, East China led the China mattress market with 29.12% market share in 2025, while Southwestern China is projected to record the highest CAGR of 8.63% through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and Upgrade Demand in Tier 1–3 Cities | +2.1% | East China, South Central China (strongest), North China (moderate) | Medium term (2–4 years) |

| E-Commerce and Omnichannel Expansion into Lower-Tier Cities | +1.8% | National, with the highest penetration in East and North China | Short term (≤ 2 years) |

| Sleep-Health Awareness Favoring Ergonomic, Foam, and Hybrid | +1.5% | Tier-1 and Tier-2 cities, spreading to Tier-3 | Medium term (2–4 years) |

| Hospitality Pipeline and Refurbishment Cycles Post-Pandemic | +1.2% | Southwestern China, South Central China, spill-over to North China | Medium term (2–4 years) |

| Green Labeling and Low-VOC Compliance Shaping Product Mix | +0.6% | Premium segments in South Central and East China, growing nationwide | Long term (≥ 4 years) |

| Build-To-Rent and Long-Term Rental Furnishing Programs | +0.5% | Tier-1 cities, expanding to provincial capitals | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Premiumization and Upgrade Demand in Tier 1–3 Cities

Rising disposable incomes in major urban centers support a clear shift from entry-price innerspring to better-performing foam, hybrid, and smart options that promise measurable sleep improvements and durability. Buyers in Tier 1–3 cities now prioritize certified materials and emissions safety, making CertiPUR-US for foam and STANDARD 100 by OEKO-TEX visible quality signals during product comparison. Mid to premium assortments grow faster as ergonomic zoning, gel-infused comfort, and motion isolation align with upgrade logic rather than first-time furnishing. Smart mattresses that are auto-adjust based on biometric data give brands a new basis for differentiation in affluent districts where consumers link sleep to preventive health. These preferences concentrate in East and South-Central China, then diffuse to other regions as omnichannel discovery expands awareness and access.

E-Commerce and Omnichannel Expansion into Lower-Tier Cities

Bed-in-a-box compression and courier-optimized packaging enable faster delivery and longer trial periods in lower-tier cities where physical showrooms are less dense. Platform ecosystems on Tmall, JD.com, and Douyin enable live demonstrations, authenticated reviews, and seamless customer service, reducing risk for high-ticket online purchases. Leading retailers synchronize inventory and pricing across offline stores and online flagships, enabling shoppers to research online, test comfort in-store, and complete checkout on their preferred channel. As this model scales, B2C remains the largest channel and also grows fastest through 2031, reflecting conversion gains rather than traffic cannibalization. Standardized safety and flammability labeling, aligned with GB standards, on e-commerce listings improves information quality and supports consistent expectations across regions [2]Source: International Organization for Standardization, “ISO 9001:2015 Quality Management Systems,” ISO, iso.org .

Sleep-Health Awareness Favoring Ergonomic, Foam, and Hybrid

Healthy China 2030 places sleep wellness on the national prevention agenda, raising awareness of ergonomic support, spinal alignment, and sleep quality among urban cohorts. Public health guidance and research collaborations inform procurement standards in eldercare and corporate wellness, reinforcing demand for pressure relief and motion control in mattress specifications. Brands invest in validated monitoring features and pressure-mapping demonstrations that build confidence in foam and hybrid solutions for daily health gains. As consumers connect mattress choice to back pain and recovery, willingness to pay for breathable foams, zoned coils, and temperature regulation supports premium step-ups. These health-linked preferences emerge first in Tier 1–2 cities and then spread outward through omnichannel content and in-store experience zones.

Hospitality Pipeline and Refurbishment Cycles Post-Pandemic

Hotel brands follow replacement schedules and brand-standard upgrades that keep mattress procurement on multi-year cycles, which stabilizes B2B demand even when residential sales slow. Suppliers with ISO-certified plants, short lead times, and regional warehouses are at an advantage in tenders that require consistent quality and synchronized rollouts across properties. Tourism recovery in interior hubs like Chengdu and Chongqing increases batch orders for king and queen formats that meet hygiene and durability specifications. Commercial buyers also request modular firmness and turnkey base packages to reduce out-of-service time for rooms during renovations and reflags. This B2B layer adds resilience to the China mattress market revenue mix through 2027 as refurbishment and new openings proceed on planned timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing Slowdown and Weak New-Home Completions | -1.4% | National, most acute in Tier-1 cities, moderate impact in Tier-2/3 | Medium term (2–4 years) |

| Raw Material and Latex Price Volatility | -1.1% | Manufacturing hubs in Guangdong and Zhejiang affect national pricing | Short term (≤ 2 years) |

| Compliance Costs from Tightened VOC/Flammability Standards | -0.7% | National, stricter in export-oriented coastal provinces | Long term (≥ 4 years) |

| High Reverse Logistics and Return Costs in E-Commerce | -0.6% | National, stronger impact in lower-tier cities with weaker infrastructure | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Housing Slowdown and Weak New-Home Completions

Residential property indicators weakened in 2024 and remained pressured through early 2026, reducing first-occupancy attachment for mattresses below prior norms. Policy easing helped stabilize transaction volumes but did not fully restore buyer confidence, which kept discretionary furniture purchases on a longer decision cycle. Mattress brands pivoted to replacement programs and promotions to boost demand, independent of new-home triggers, in Tier 1–3 cities. Commercial procurement from hospitality, healthcare, and rental operators partially offset residential softness during this period [3]Source: National Bureau of Statistics of China, “Real Estate Development and Sales Data 2024–2025,” National Bureau of Statistics of China, stats.gov.cn . The net effect is a slower near-term pull from new completions with greater reliance on omnichannel upgrades and institutional contracts in the China mattress market.

Raw Material and Latex Price Volatility

Polyurethane inputs such as TDI and polyols experienced notable swings through 2024 and 2025, while weather-linked yield shifts influenced natural latex supplies in Southeast Asia. Smaller assemblers with limited hedging tools faced sharper margin compression and more frequent price changes, which can increase return risk if specifications are downgraded. Integrated players mitigated volatility by locking in longer-term contracts and operating captive foam lines, which smooth quarterly costs. Input cost spikes also interact with compliance needs, since low-VOC chemistries and water-based adhesives often carry higher unit costs. This cost mix narrows promotional flexibility for mid-tier manufacturers and elevates the advantage of scale in the Chinese mattress market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Innerspring Dominates Value Share Yet Foam Captures Growth Narrative Through Smart Integration

Innerspring mattresses accounted for 66.53% of 2025 revenue, as manufacturers benefit from high-capacity coil lines and well-established supply networks in coastal clusters. The category maintains a strong presence among value seekers and legacy shoppers who equate a firmer feel with back support, helping keep entry-level demand resilient in lower-tier markets. Foam products, including memory foam, are projected to grow at an 8.22% CAGR through 2031, as gel infusions and open-cell designs address heat buildup while smart features create clear differentiation at mid- to premium price points. Latex remains a niche for hypoallergenic and sustainability-focused buyers, supported by recognized textile and foam certifications that validate low emissions and responsible sourcing. Hybrids blend pocketed-coil support with comfort foams and have become a popular step-up choice as upgrade buyers seek balanced comfort.

As connected sleep devices migrate into mainstream retail, sensor arrays and responsive air modules integrate more easily into foam layers than into coil assemblies, shifting smart adoption toward foam and hybrid SKUs. Process controls linked to emissions and fire safety standards increase testing and certification costs for foam and latex, but these hurdles also raise barriers for low-quality entrants and favor organized brands with QA systems. In coastal export hubs, compliance footprints are now routine and double as quality signals in domestic channels where buyers seek assurance on VOCs and materials safety. In this context, innerspring maintains breadth of coverage while foam and hybrids capture the innovation storyline that drives perceived value for urban consumers. This mix positions the China mattress market to sustain leadership in springs while still allocating incremental share to foam-led formats through 2031.

By Mattress Size: King Models Lead Revenue While Queen Variants Surge on Urban-Apartment Optimization

King-size mattresses accounted for 41.53% of 2025 revenue, driven by high-tier urban buyers with larger home footprints who prioritize generous sleep surfaces for couples and families. Queen-size variants are the fastest-moving format, with a projected 8.04% CAGR through 2031, as standardized hotel rooms and compact urban apartments favor layouts that conserve space without sacrificing perceived luxury. Single- and double-size units support student housing and rental units, with the remaining core at budget prices while brand upgrades focus elsewhere. Custom and specialty size niches command premiums as villa owners and eldercare settings adopt larger footprints or split-head adjustables for accessibility and caregiver convenience. Climate preferences also sway fill and cover choices by region, as humid southern provinces prioritize breathability and faster-drying materials, while colder northern provinces value thicker comfort stacks and thermal layers.

E-commerce vendors tend to optimize queen-size logistics by using parcel dimensions compatible with major couriers, which concentrate online unit volumes in that format. In-store testing remains important for king-size buyers, who often consult with sales staff on firmness, motion transfer, and partner comfort before purchasing from synchronized online channels. Standards for dimensional tolerances and labeling keep variance within acceptable ranges and require transparent disclosure so buyers can align frames and bedding with mattress selection. As brand assortments evolve, queen and king remain anchor sizes that shape inventory planning, SKU rationalization, and showroom floor layouts across provinces. This distribution aligns with the Chinese mattress market preference for family-oriented sleeping solutions while maintaining adaptability to apartment footprints in growing cities.

By End User: Residential Volumes Stabilize While Commercial Acceleration Offsets Housing Cyclicality

Residential accounted for 74.44% of the 2025 volume, reflecting the large installed base and expanding health awareness, which shorten replacement cycles in urban households. Commercial channels comprising hospitality, healthcare, eldercare, corporate dormitories, and build-to-rent are forecast to grow at an 8.40% CAGR through 2031, acting as a counterweight to soft new-home attachment. Hospitality replacements and brand rollouts support bulk orders that adhere to franchise standards for comfort, hygiene, and durability across mattress plus base packages. Long-term rental operators standardize SKUs at wholesale ranges of USD 113–169 to balance comfort, tenant turnover, and maintenance schedules. Healthcare and eldercare procure specialized pressure-relief and anti-bed-sore products that meet clinical safety and materials standards, which encourages premium features to trickle down into residential products.

Residential buyers carry over expectations from hotel stays, creating demand for a consistent feel, edge support, and temperature control that mirrors branded hospitality beds. As procurement programs emphasize safety and emissions compliance, commercial contracts reward suppliers that maintain reliable certifications and offer flexible delivery to multi-property portfolios. This activity supports steady line utilization in larger factories and distinguishes integrated players from smaller assemblers in terms of availability, specifications, and documentation. Replacement-focused promotions, including trade-ins at USD 70–141, convert legacy hard-bed users to foam comfort layers in urban rental markets without waiting for new occupancy. The result is a China mattress market that steadily broadens its demand sources while aligning product and price tiers with institutional and household priorities.

By Distribution Channel: B2C Retail Dominates Yet Posts Fastest Growth Through Omnichannel Strategies

B2C retail accounted for 75.25% of 2025 revenue and is projected to post the fastest CAGR of 9.36% through 2031, confirming that channel evolution is boosting conversion rather than cannibalizing in-store traffic. Marketplace and social-commerce platforms leverage live demonstrations, creator content, and extended trials to reduce hesitation about buying mattresses online. Specialty chains enhance the B2C journey with sleep consultations, pressure-mapping demos, and coordinated home trials that maintain experience parity across channels. B2B and project sales remain essential for hospitality, corporate, and public-sector procurement, with framework agreements that lock in volumes and timelines across multiple locations. Safety and labeling requirements for online channels, including flammability certifications under GB standards, formalize product display and reduce disputes during extended return windows.

Omnichannel sellers synchronize SKU availability and real-time inventory so shoppers can research online, test comfort in-store, and complete their purchase along the path that's most convenient for them, which raises average order values and reduces returns. Mass merchants maintain strong penetration for entry-price springs yet face price-matching pressure as marketplace sellers compress layers of distribution cost. DTC entrants fill white space with compact retail footprints in malls to provide tactile validation, while focusing on fulfillment and online promotions to preserve margins. Reverse logistics remains a cost headwind in pure e-commerce flows, which motivates sellers to strengthen in-store trials and service policies that pre-qualify buyers. These channel dynamics reinforce a China mattress market premised on discoverability, testability, and flexibility, with B2C retaining both the largest base and the fastest growth.

Geography Analysis

East China led the China mattress market with 29.12% market share in 2025, while Southwestern China is projected to record the highest CAGR of 8.63% through 2031. East China has the largest installed base for mattress production and sales, supported by the Shanghai–Jiangsu–Zhejiang corridor, where logistics density reduces delivery times and enables premium assortments. Higher per-capita disposable incomes in these provinces help brands scale smart features and advanced materials that require higher ticket sizes. The area also anchors a high proportion of compliant, export-ready plants, which have standardized quality practices that now influence domestic retail specifications. As retail footprints mature, store productivity improvements and omnichannel conversion tactics replace new store openings as the primary growth vector across coastal cities. The combination of mature demand and organized supply chains keeps the region as the largest contributor to value in the Chinese mattress market.

Southwestern China is the fastest-growing cluster as infrastructure programs lower production and distribution costs while new hospitality and tourism assets expand B2B order books. Rapid urbanization in Chengdu and Chongqing is drawing national retail brands to build balanced assortments that blend entry-level SKU coverage with premium options for new middle-class households. Regional warehousing and shorter lead times allow vendors to serve both residential replacement and project-based contracts with fewer stockouts and more timely installations. Product planning also adapts to humid, warmer conditions with breathable builds, bamboo-charcoal infusions, and antimicrobial covers, which are common differentiators in the South. This rising base positions Southwestern China to drive a larger portion of incremental growth in the Chinese mattress market through the forecast period.

North and South-Central China contribute steady demand, shaped by evolving demographics, housing stock, and institutional budgets. North China balances stable household replacement with policy-led upgrades in eldercare facilities, which adds heavier-duty specifications to procurement lists. South Central China, including Guangdong's manufacturing bases, supports national distribution but is adapting to higher wages and compliance costs that are gradually pushing some capacity inland. Northwest and Northeast participation remains lower nationally, yet plays an important role in product tailoring for colder weather, leading to localized marketing around thickness and thermal comfort. These patterns illustrate how the Chinese mattress market aligns product formats with different regional income levels, climate conditions, and infrastructure maturity to support balanced growth.

Competitive Landscape

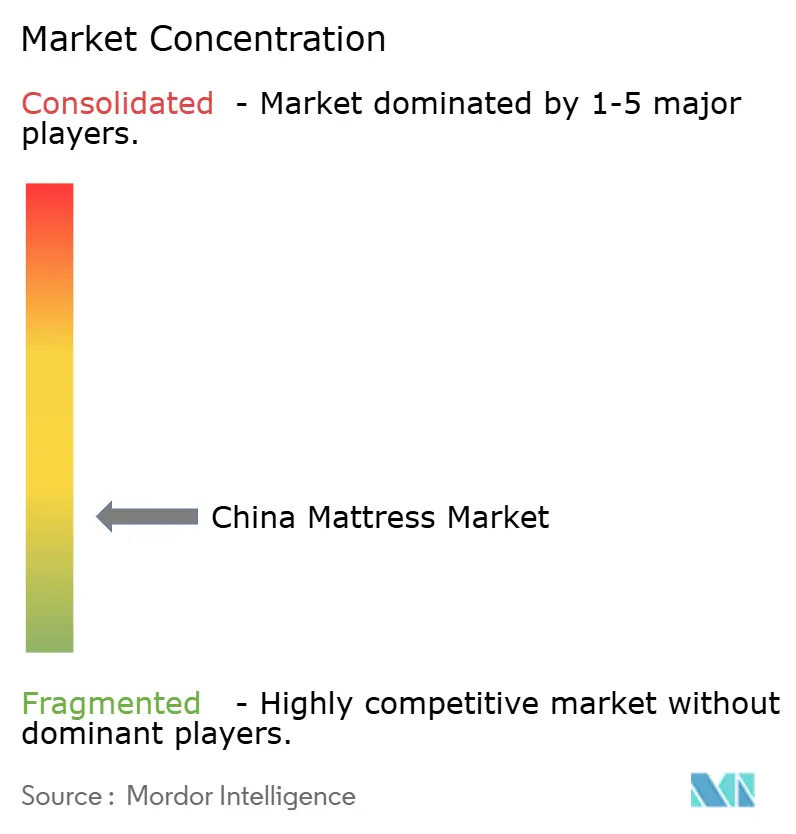

The competitive field is fragmented, and a long tail of regional brands and workshop-scale assemblers is active at entry price points. Organized brands compete on three vectors, including AI-enabled personalization, supply-chain compliance and transparency, and omnichannel mastery that compresses time from discovery to delivery. Smart-portfolio flagships, such as DeRUCCI’s T11 series, use multi-sensor arrays and adaptive air systems to make confidence-building health claims backed by trial results and clinical protocol references. In parallel, emissions and textile certifications have shifted from export prerequisites to domestic trust signals, as consumers seek low-VOC labeling and documented material provenance. Cross-border trade frictions, including anti-dumping duties on Chinese mattresses in the United States, redirect capacity to domestic channels and amplify price competition in selected city tiers.

Company strategies illustrate the range of moves used to build advantage across formats and channels. Xilinmen, rebranded as Sleemon Healthy Sleep Technology in 2026, signals a pivot to smart-sleep ecosystems while expanding joint R&D platforms with leading universities. DeRUCCI advances connected-sleep portfolios anchored in cardiopulmonary tracking and rapid firmness adjustment, positioning smart mattresses as medical-grade adjuncts for sleep health. MLILY expands entry and mid-price lines for online channels while testing in-store experience formats that funnel transactions back to e-commerce checkouts, a mix designed to preserve margin while improving discovery. International players leverage brand heritage and hospitality partnerships but face intensifying digital competition from DTC imports and domestic innovators that undercut distributor layers in lower-tier cities. These moves sustain a diverse China mattress market where both domestic champions and global brands chase premium upgrades and connected wellness demand.

Compliance and safety frameworks bring additional separation between large and small producers, shaping investment priorities and factory layouts. Stricter VOC and flammability standards push water-based adhesives, new cover chemistries, and tighter QA, formalizing practices across coastal hubs and rolling them in over staged timelines. Hazardous-chemical handling rules that took effect in 2026 increase fixed investment in safety systems and monitoring at foam processors, with heavier proportional impacts on mid-sized enterprises. As these requirements settle, larger brands with ISO credentials and captive materials capabilities earn more consistent access to institutional tenders and hotel programs. This environment encourages ongoing professionalization while still leaving ample headroom for focused disruptors in the Chinese mattress market, including smart features, modular builds, and circular-materials pilots.

China Mattress Industry Leaders

Xilinmen / Sleemon

MLILY

KUKA Home

DeRUCCI

Man Wah

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Xilinmen Furniture Co., Ltd. officially changed its name to Sleemon Healthy Sleep Technology Co., Ltd., signaling a strategic pivot toward smart-mattress ecosystems and AI-driven health platforms.

- March 2025: Xilinmen established a Joint Research Center for Great Health with Shanghai Institute for Advanced Study, Zhejiang University, focusing on cultivating new productive forces in sleep technology.

China Mattress Market Report Scope

A mattress is a soft, airtight case that is designed to be inflated and used as a bed. The report covers a complete background analysis of the Chinese mattress market, which includes an assessment of the total market, emerging trends in the segments and regional market, and significant changes in market dynamics and market overview. The report also offers qualitative and quantitative assessments by analyzing the data gathered from industry analysts and market participants across various key points in the value chain. The report covers the Chinese foam mattress market, and it is segmented by type (innerspring mattresses, memory foam mattresses, latex mattresses, and other types (gel and hybrid) and distribution channel (offline and online). The report offers market size and forecasts for the Chinese mattress market in terms of revenue (USD) for all the above segments.

By Product Type

| Innerspring / Coil |

| Foam (including memory foam) |

| Latex |

| Hybrid |

| Other Mattress Types |

By Mattress Size

| Single-size Mattress |

| Double-size Mattress |

| Queen-size Mattress |

| King-size Mattress |

| Custom & Specialty Sizes |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | |

| Online | |

| Other Distribution Channels | |

| B2B/Project |

By Geography

| East China |

| Southwestern China |

| North China |

| South Central China |

| Northeast China |

| Northwestern China |

| By Product Type | Innerspring / Coil | |

| Foam (including memory foam) | ||

| Latex | ||

| Hybrid | ||

| Other Mattress Types | ||

| By Mattress Size | Single-size Mattress | |

| Double-size Mattress | ||

| Queen-size Mattress | ||

| King-size Mattress | ||

| Custom & Specialty Sizes | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Project | ||

| By Geography | East China | |

| Southwestern China | ||

| North China | ||

| South Central China | ||

| Northeast China | ||

| Northwestern China | ||

Key Questions Answered in the Report

What is the size of the China mattress market in 2026, and what is its growth outlook to 2031?

The China mattress market size is estimated USD 17.51 billion in 2026 and is projected to reach USD 25.06 billion by 2031 at a 7.43% CAGR.

Which product category leads and which is growing fastest in China?

Innerspring led value share at 66.53% in 2025, while foam is the fastest-growing segment, with an 8.22% CAGR through 2031, driven by comfort innovation and smart integration.

How are channels evolving in the Chinese mattress market?

B2C remains dominant, accounting for 75.25% of 2025 revenue, and is also the fastest-growing through 2031 as omnichannel models link online discovery with in-store testing and rapid fulfillment.

Which regions are most important for China’s mattress demand?

East China led with 29.12% of 2025 sales, given manufacturing concentration and higher incomes, while Southwestern China is the fastest-growing region with an 8.63% projected CAGR.

What compliance standards matter most for mattresses in China?

Key standards include GB 18584 for indoor air quality, GB 20286 for flame retardancy in public places, and GB/T 26706 for dimensions and labeling, which shape materials, QA, and product display requirements.

Page last updated on: