United States Mattress Bases Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

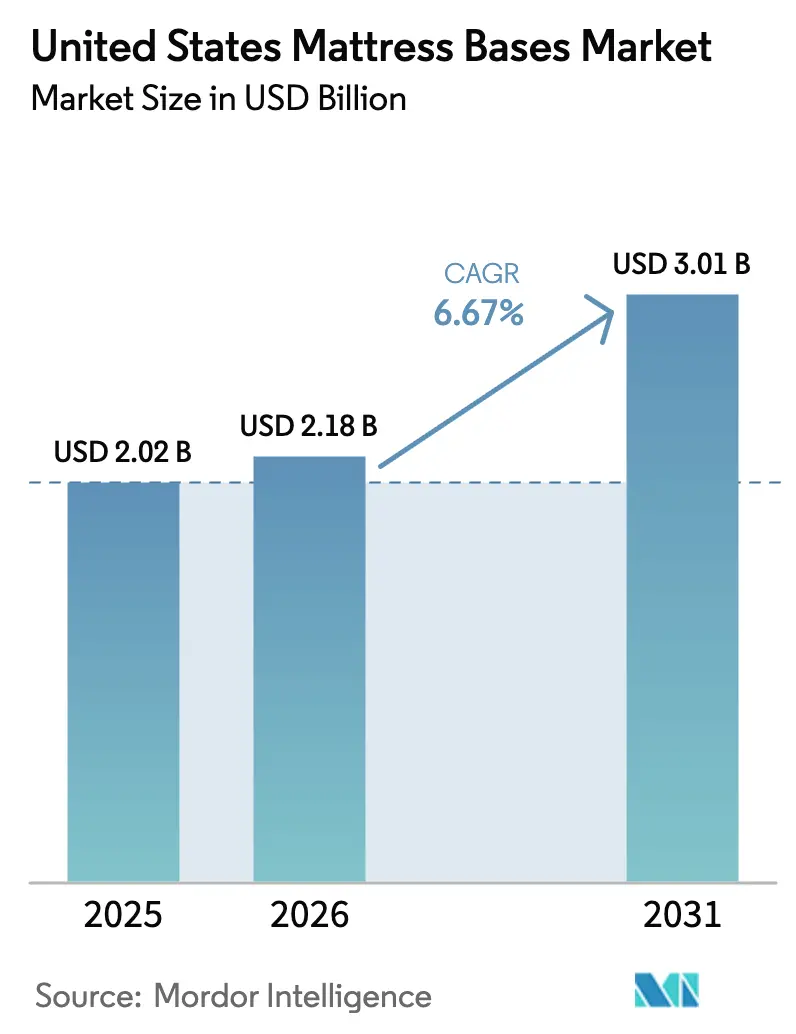

| Base Year Market Size (2025) | USD 2.02 Billion |

| Market Size (2026) | USD 2.18 Billion |

| Market Size (2031) | USD 3.01 Billion |

| Growth Rate (2026 - 2031) | 6.67% CAGR |

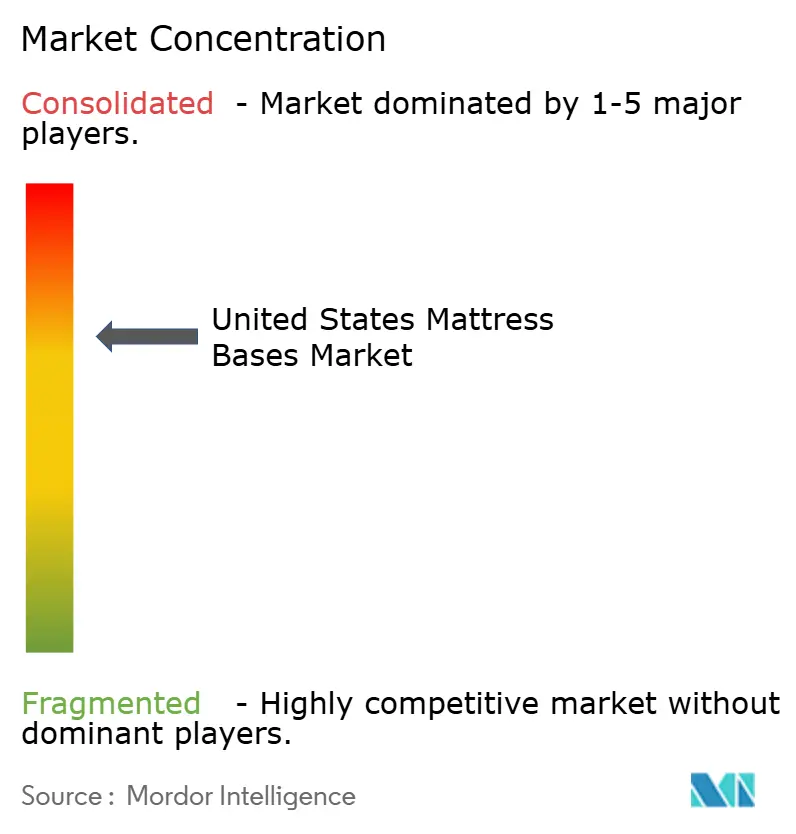

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

United States Mattress Bases Market Analysis by ���ϲ�����

The United States mattress bases market size stood at USD 2.18 billion in 2026, up from USD 2.02 billion in 2025, and is projected to reach USD 3.01 billion by 2031 at a 6.67% CAGR. Growth remains anchored in the rapid adoption of adjustable bases, which lead by volume and are outpacing legacy platforms, box springs, and slats through 2031. The South remains the largest regional buyer in 2026, while the West posts the fastest expansion as omnichannel and direct-to-consumer retailers bundle bases with mattresses and financing to lift attachment rates. A consolidated supply side led by Leggett & Platt and Ergomotion supports private-label programs for national and regional retailers, while Tempur Sealy and Sleep Number focus on software-enabled ecosystems that raise average ticket prices and stickiness across their store networks. Input-cost headwinds from tariffs and electronics components remain in the near term, although leading companies continue to optimize footprints and product mixes to protect margins as demand normalizes through 2026[1]International Sleep Products Association, “Tariff Effects,” International Sleep Products Association, sleepproducts.org.

Key Report Takeaways

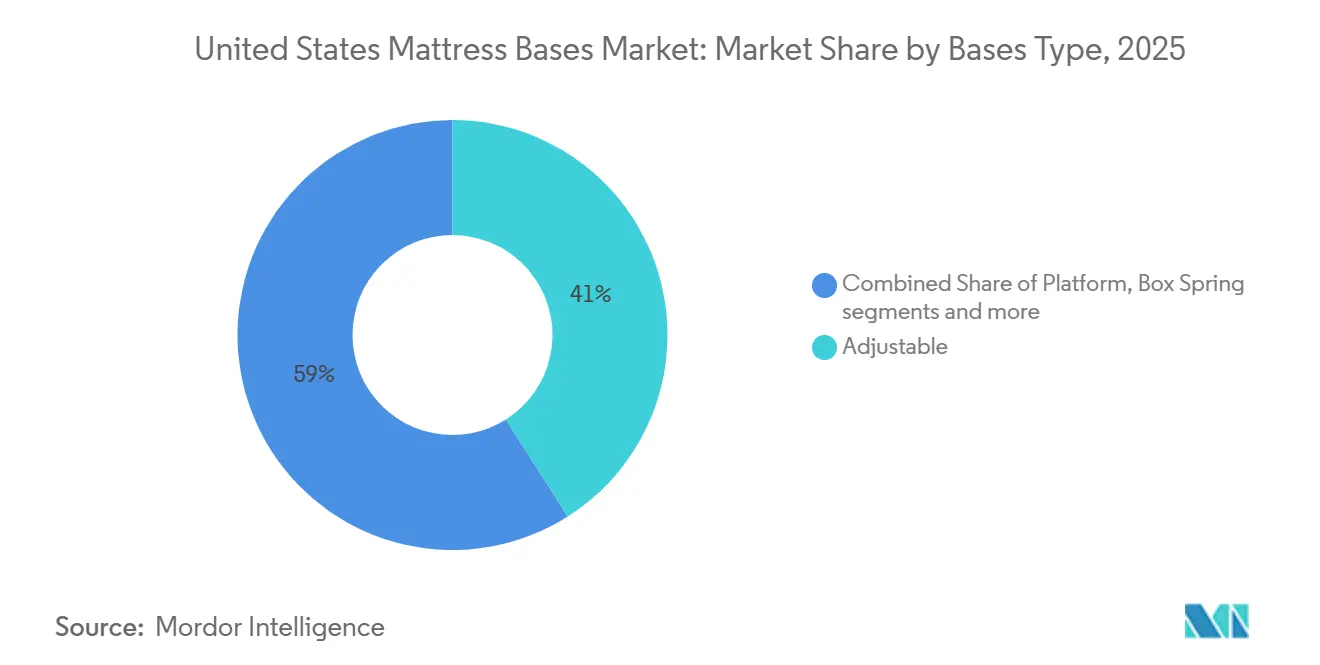

- By base type, adjustable bases led with 41.00% of the United States mattress bases market share in 2025 and are projected to expand at a 7.38% CAGR through 2031.

- By material, wood accounted for 60.74% of the United States mattress base market share in 2025, while metal is the fastest-growing, with a 6.93% CAGR through 2031.

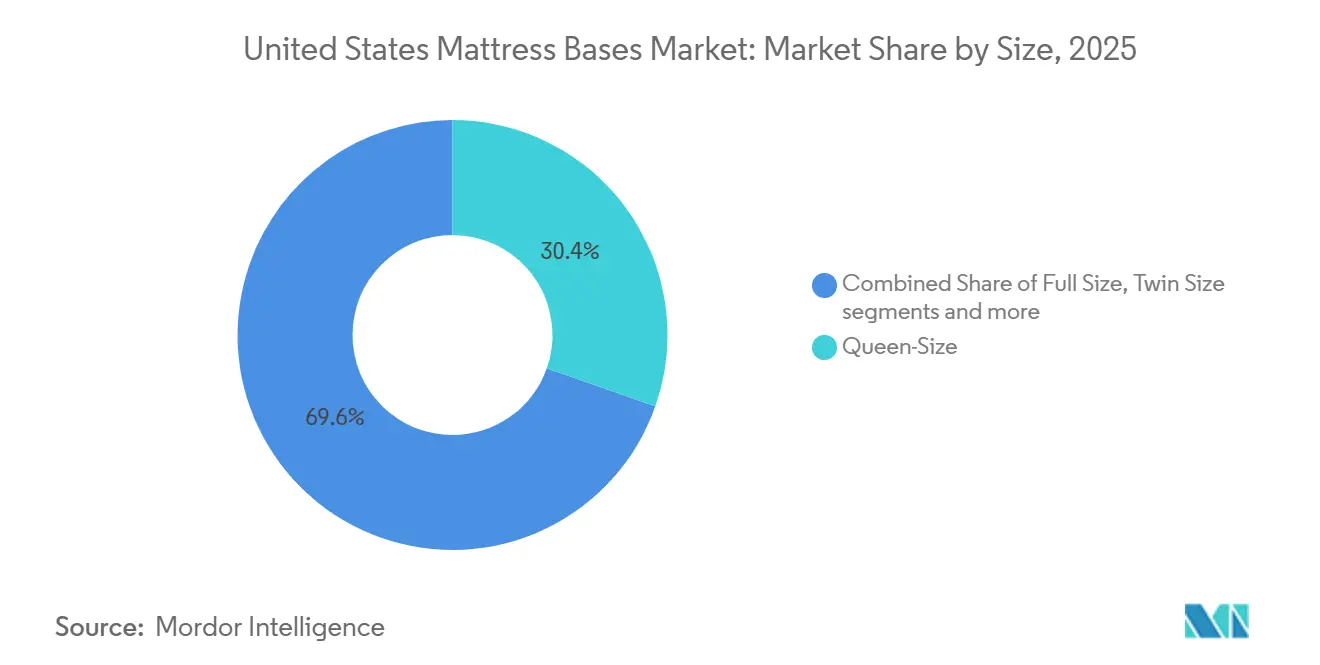

- By size, queen held 30.38% of the United States mattress bases market share in 2025, and Twin-XL is the fastest-growing at 7.23% CAGR through 2031.

- By end user, residential accounted for 74.18% of the United States mattress bases market share in 2025 and is advancing at a 6.78% CAGR through 2031.

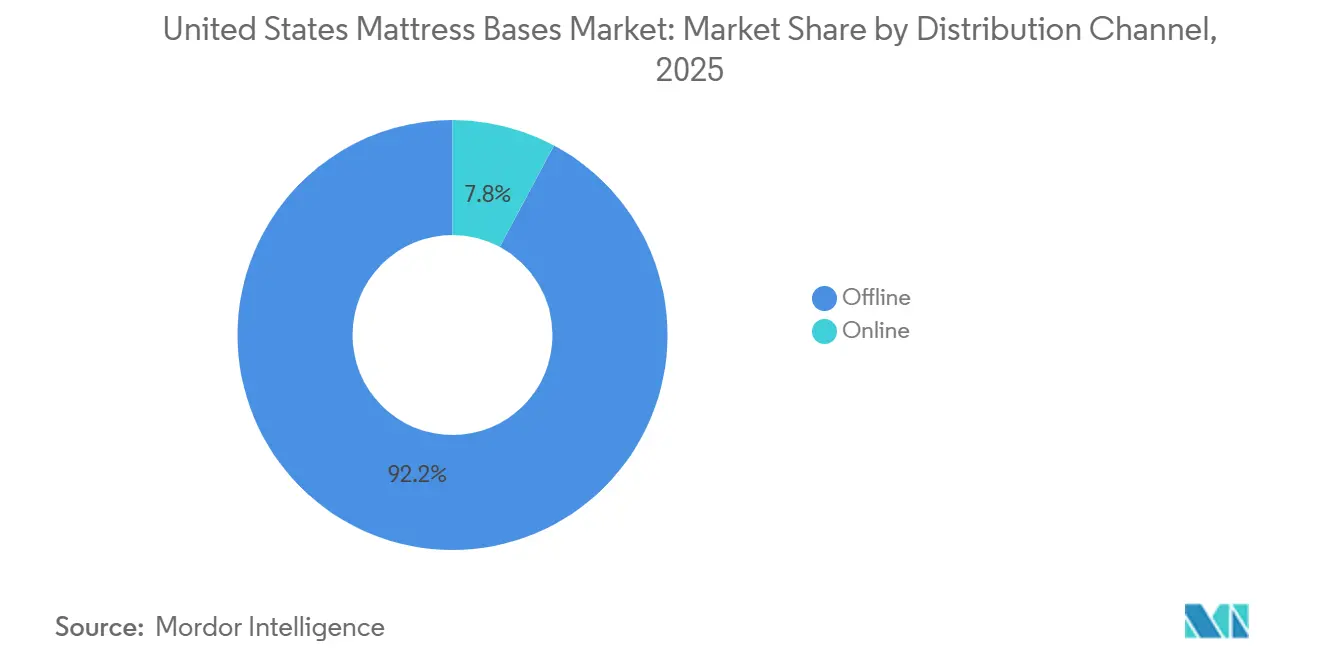

- By distribution channel, offline commanded 92.17% of the United States mattress bases market share in 2025, and online is the fastest-growing channel, with a 9.52% CAGR through 2031.

- By geography, the South led the United States mattress bases market with 34.00% market share in 2025, while the West is the fastest-growing region, with a 8.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Mattress Bases Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adjustable-Base Attach Rates at Retail | +1.2% | National, strongest in the South and West regions | Medium term (2-4 years) |

| Aging Population and Sleep-Health Use Cases | +1.5% | National, concentrated in Florida, Arizona, and California | Long term (≥ 4 years) |

| Smart Features and App-Integrated Bases Boosting Spend | +1.0% | Urban markets in the Northeast and the West | Short term (≤ 2 years) |

| DTC Bundling, Promotions, and Financing Expand Access | +0.8% | National e-commerce, stronger on the West Coast | Medium term (2-4 years) |

| Split-King Adoption and Twin-XL Pair Growth | +0.7% | National, strongest among couples upgrading primary bedrooms | Medium term (2-4 years) |

| Zero-Clearance and Retrofit Capability Lifting Adoption | +0.6% | Urban and suburban households with existing frames | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rising Adjustable-Base Attach Rates at Retail

Retailers continue to prioritize attachment of adjustable bases to premium mattresses, aided by in-store demonstrations and structured financing that reduce upfront friction for households in upgrade cycles. Tempur Sealy reports consistent gains in attachment as smart bases become a core part of the company’s ecosystem pitch, with software features marketed to improve comfort and reduce snoring across mainstream price tiers. Leggett & Platt underpins private-label breadth across the Top 25 bedding retailers, helping regional chains carry feature-rich adjustable models at accessible price points in metros. Tempur-Pedic and Sleep Number each reinforce store-level conversion with app-enabled demonstrations that show anti-snore, head-lift, and zero-gravity presets linked to their branded ecosystems. This pattern supports steady gains for the United States mattress bases market as retailers align training and promotions to emphasize wellness use cases and ease-of-use controls that resonate with mid-income households.

Aging Population and Sleep-Health Use Cases

The 65-plus cohort continues to expand in 2026, and by 2030, older adults will represent a much larger share of the United States population, which sustains interest in adjustable bases that can elevate the head or legs for reflux relief, circulation support, and comfort around chronic conditions[2]U.S. Census Bureau, “Aging Population,” U.S. Census Bureau, census.gov. Flexabed’s hi-low adjustable platforms, which raise and lower the entire sleep surface for easier entry and transfers, reflect the product design focus for aging-in-place and assisted-living settings. Monarch Sleep Systems offers assisted-care models with integrated support and convenience features that help facilities improve residents' independence while reducing caregiver strain. Brands now frame these purchases as wellness solutions tied to sleep quality, symptom relief, and ergonomic positioning rather than as medical equipment, a shift that broadens appeal to households in their 50s and 60s. This demographic tailwind continues to support the United States mattress bases market through product roadmaps that blend therapeutic positioning with familiar lifestyle presets and app guidance.

Smart Features and App-Integrated Bases Boosting Spend

Connectivity and software continue to lift spending in premium tiers, where voice control, snore detection, lumbar support, and app-guided positions enhance perceived value in showrooms and online channels. Sleep Number integrates its FlexFit bases with the SleepIQ platform to monitor biosignals and coordinate adjustments, anchoring a closed-loop system that encourages long-term engagement and higher attachment on replacement cycles. Tempur Sealy’s smart base portfolio incorporates Sleeptracker-AI for automatic anti-snore head elevation and ecosystem features, which the company positions as differentiators in its premium configurations[3]Tempur Sealy International, “Form 8-K Current Report Filed 2024-01-26,” U.S. Securities and Exchange Commission, secdatabase.com. Ergomotion’s new Sleep Assist app, previewed at CES 2026, signals continued R&D toward software-defined comfort that can inform positioning based on user inputs and streamline adjustments throughout the sleep session. With core features moving down the price ladder, this functionality raises average selling prices while maintaining affordability bands that keep the United States mattress bases market accessible to larger customer segments.

DTC Bundling, Promotions, and Financing Expand Access

Large bedding brands have accelerated omnichannel strategies that pair premium mattresses with adjustable bases to lift average order value and manage pricing across owned stores and e-commerce. The completion of the Mattress Firm acquisition broadened Tempur Sealy’s control over point-of-sale execution, where feature demonstrations and promotional financing can drive step-ups into power bases. Sleep Number reports that digital channels complement its store network and support ecosystem messaging for FlexFit bases, which connects app data and comfort modes to measurable outcomes that customers can track over time. These programs highlight the role of financing and bundling in shifting buyer perception from accessory to integral part of the sleep system, a change that sustains attach rates across cohorts with different price sensitivities. The net effect is a rising share of premium configurations in 2026, supporting value growth in the United States mattress bases market, even as volume normalizes across the category.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Average Selling Prices and Return Restrictions | -0.9% | National, stronger in the Midwest and rural markets | Medium term (2-4 years) |

| Tariffs and Component Supply Constraints Raise Costs | -1.1% | National, import-reliant brands are most exposed | Short term (≤ 2 years) |

| Electronics Warranty and Service Burdens | -0.7% | National, where service center capacity is limited | Short term (≤ 2 years) |

| Macroeconomic Softness and Replacement Deferrals | -0.8% | National, more pronounced in price-sensitive regions | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

High Average Selling Prices and Return Restrictions

Entry adjustable bases in 2026 typically start near the lower mid-hundreds and scale into the premium range as features add massage, lumbar, and smart automation, which can stretch household budgets in slower macro cycles. Sleep Number noted margin pressure tied to electronics and warranty costs in recent disclosures, which reinforces the sensitivity of complex base components to after-sale service overhead. Return policies are another friction point, as many retailers and brands treat adjustable bases as non-returnable or final sale items due to electrical components and hygiene considerations, which dampens trial-based conversion for first-time buyers. Sealy explicitly states that its Ease Power Base is non-returnable, signaling industry-wide constraints that differ from mattress-trial practices and require greater confidence at purchase. These factors slow upgrade cycles for value-focused households and weigh modestly on the United States mattress bases market until financing and demonstration-driven selling address perceived risk and affordability concerns.

Tariffs and Component Supply Constraints Raise Costs

In 2025, tariff layers increased duties on key components and finished goods from several trade partners, raising input costs for actuators, control boxes, steel substructures, and related electronics across the adjustable base supply chain. Leggett & Platt outlined footprint-consolidation steps to improve cost competitiveness, including production shifts that leverage USMCA-compliant manufacturing to preserve duty-free access while reducing labor and logistics costs for complex assemblies. Brands also face component availability constraints that can extend lead times or compress feature sets, affecting promotional cadence and assortment depth during peak selling periods. Industry associations have cautioned that tariffs can raise average ticket prices, a trend that concentrates demand in mid-tier price bands and lengthens replacement intervals when households defer big-ticket purchases. These pressures remain a short-term drag on expansion but do not alter the long-term appeal of smart adjustable bases that deliver visible comfort and wellness benefits in the United States mattress bases market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Base Type: Adjustable Bases, Command Share, and Velocity

Adjustable bases captured 41.00% of the market in 2025 and are projected to advance at a 7.38% CAGR through 2031, solidifying their lead over traditional platforms, box springs, and slats in the United States mattress bases market. The United States mattress bases market for adjustable bases is supported by rapid feature migration into mid-tier price points, where entry models add quiet motors, anti-snore programs, and memory presets, boosting consumer willingness to pay. Beautyrest’s Baselogic line illustrates this diffusion, with the Baselogic Silver offering head and foot articulation, zero-clearance design, and underbed lighting in widely carried SKUs. Retailers that demonstrate Zero Gravity and head-lift presets during mattress trials improve attach rates by linking perceived wellness benefits to daily routines, and comfort needs across couples and solo sleepers. Software-enabled automation ties these features to snore response and comfort coaching, which differentiates adjustable configurations from static support systems and sustains upgrade intent through 2031.

Traditional platforms, slats, and box springs continue to serve budget-conscious segments and minimalist aesthetics, although they do not capture the same wellness halo that drives premium adjustable adoption in the United States mattress bases market. Price ladders within OEM programs allow retailers to private-label adjustable bases with consistent feature steps, which helps explain the breadth of selection now present across regional chains and national banners. Product integration strategies at Tempur Sealy and Sleep Number also reinforce the role of adjustable bases as part of complete sleep systems tied to apps and sensors, which extend brand ecosystems over multi-year ownership cycles. As supply chain pressures ease, feature sets continue to improve at accessible price points, creating a stronger funnel for upgrades from stationary foundations through 2026. In this context, the United States mattress base industry is clearly pivoting toward multifunctional platforms that blend motion, comfort, and connected services to defend market share against static alternatives.

By Material: Wood Leads, But Metal Gains on Adjustable Demand

Wood-based foundations accounted for 60.74% of the United States mattress base market share in 2025, reflecting dominance in platforms, slats, and legacy box spring constructions that emphasize structural rigidity and finish options. The United States mattress bases market for metal frames is growing faster, with the metal segment advancing at a 6.93% CAGR through 2031, as adjustable bases rely on steel substructures to handle lift cycles and higher dynamic loads. Leggett & Platt’s adjustable bed platforms are engineered on a steel chassis and long-life components that support repeated head and foot articulation with minimal deflection, giving retailers confidence in long-term performance claims. Metal also enables zero-clearance designs that allow bases to sit within existing bedroom furniture, which supports retrofit projects that preserve room layouts and storage solutions. As software features extend into lower price points, the material implication is a steady shift from wood-heavy constructions to metal-centric frames in articulated categories that value durability and mounting flexibility.

Tariff-driven costs on steel and electronics in 2025 increased sourcing complexity for import-reliant assemblers, which in turn encouraged footprint and supplier diversification across North America. Leggett & Platt described actions that align production with tariff frameworks to preserve duty-free access where possible, a move that stabilizes bill-of-materials costs for bases built around steel tubes and welded brackets. Wooden platforms continue to appeal to consumers who do not prioritize motion or app integration, but the relative value proposition of steel rises as adjustable features become the norm in family bedrooms and primary suites. Retailers have responded by simplifying assortments, steering budget shoppers toward metal-reinforced SKUs when buyers express interest in upgrade flexibility over the next few years. This rebalancing supports durable growth in articulated categories that rely on metal to deliver reliable motion and lower service interventions across ownership cycles.

By Size: Queen Dominates, Twin-XL Surges on Split Configs

Queen-size foundations held a 30.38% share in 2025, aligning with household bedroom layouts where a 60-inch width suits couples and delivers strong value in the United States mattress bases market. Twin-XL is the fastest-growing size, with a 7.23% CAGR through 2031, driven by split-king configurations that let couples adjust head and foot angles independently without compromising individual comfort. Juna Sleep Systems’ H-Bed introduces bridging foam to reduce the center gap issue common in split setups, addressing a known pain point for couples who prefer a unified surface while preserving motion customization. Split configurations also match the rise of app-enabled anti-snore and TV positions that differ between partners, since settings persist per side and streamline nightly routines. The size mix, therefore, shifts demand for accessories and linens while encouraging retailers to bundle compatible bases and mattresses to simplify the path to purchase for households upgrading beyond queen.

Full and standard twin sizes remain relevant for kids’ rooms and guest spaces, where buyers prioritize cost and simplicity, but velocity is concentrated in queen and split-king sizes for primary bedrooms in the United States mattress bases market. Retailers address compatibility concerns in split builds by featuring quick demos that show how two Twin-XL foundations sit within existing frames and by explaining sheet and blanket configurations that keep the setup tidy. Premium tiers add pillow-tilt and lumbar features that appeal to readers and side sleepers, with accessories designed to address cable management and device charging on both sides of the bed[4]Tempur-Pedic, “Shop Tempur-Pedic Power Bases,” Tempur-Pedic, tempurpedic.com. In 2026, this sizing trend aligns with the broader shift to smart features and couples’ customization, reinforcing the role of Twin-XL pairs as the engine of growth in adjustable categories. Taken together, the size mix complements feature adoption and helps retailers rationalize floor space by focusing on demonstration-ready queen and split configurations that convert efficiently at the point of sale.

By End User: Residential Anchors Demand, Commercial Gains Momentum

Residential accounted for 74.18% of the market in 2025 and is advancing at a 6.78% CAGR through 2031, which reflects the category’s core position in home bedroom upgrades across income bands in the United States mattress bases market. Store networks and brand-owned showrooms remain central to consumer education on adjustable features, while app integrations show prospective buyers how snore response and comfort presets fit into nightly routines. Financing offers and omnichannel content help households compare configurations and preserve upgrade intent even when macro headwinds slow discretionary purchases. Residential buyers show steady interest in zero-clearance designs that fit existing furniture, which lowers installation complexity and supports adoption in apartments and primary homes alike. These elements keep the United States mattress bases market aligned with consumer comfort and wellness needs while minimizing barriers to trial across price tiers in 2026.

Commercial adoption is expanding within senior living, where hi-lo bases reduce caregiver strain and ease transfers, aligning with safety mandates and fall-prevention priorities in assisted-care environments. Facilities also prefer modular designs that simplify maintenance and service, keeping rooms available and lowering the total cost of ownership across multi-year contracts. Compliance culture remains important for institutional buyers, as illustrated by recurring CPSC enforcement updates that underscore adherence to standards for related bedroom products and accessories sold online. Hotels and wellness-focused properties continue to test smart comfort features to differentiate guest experiences, which sustains a steady pipeline for premium adjustable bases when projects align with brand standards and ROI thresholds. Over time, commercial specifications inform residential expectations, reinforcing the premiumization path for the United States mattress base industry as features like anti-snore and head-lift become familiar across contexts.

By Distribution Channel: Offline Reigns, Online Accelerates

Offline channels commanded a 92.17% share in 2025 because shoppers prefer in-store demonstrations to evaluate motor sound, motion profiles, and upholstery quality before committing to a purchase, which often has stricter return conditions in the United States mattress bases market. Specialty bedding chains, brand-owned stores, and regional independents rely on trained sales associates who can explain snore response, Zero Gravity, and lumbar features in practical terms that link benefits to daily life. Tempur Sealy’s 2025 acquisition of Mattress Firm expanded the company’s reach to more than 2,200 retail locations, allowing it to merchandise smart bases alongside branded mattresses in a controlled point-of-sale environment. Retailers that include delivery, setup, and haul-away in the ticket help close sales by removing friction, particularly for heavier split configurations that require careful installation. These dynamics steady conversion and keep the United States mattress bases market anchored in offline engagement while digital channels scale around it over the forecast period.

Online channels have a smaller base but are growing at a 9.52% CAGR through 2031 as brands improve content, offer guided selection tools, and connect app ecosystems to reduce post-purchase uncertainty. Supplier initiatives such as Logicdata and Dreamotion’s domestic inventory program shorten lead times for retailers and e-commerce operators, which allows faster replenishment and more aggressive promotional calendars. Safety oversight also matters online, with the CPSC spotlighting product compliance and issuing recalls or warnings when required, reinforcing the importance of transparent specifications and certifications in digital listings. As omnichannel matures, more shoppers research online, test in-store, and complete checkout at home, a pattern that keeps the United States mattress bases market adaptable to buyer preferences and helps brands serve customers consistently across touchpoints. The result is steady normalization of the online share that complements, rather than replaces, offline showrooms in this tactile product category through 2031.

Geography Analysis

The South led the United States mattress bases market with 34.00% in 2025, supported by dense retail coverage and strong replacement activity across large states like Texas and Florida, where aging demographics are driving interest in therapeutic positioning. Florida’s above-average concentration of seniors reinforces the appeal of adjustable platforms that can raise the head or legs to address reflux, snoring, and circulatory comfort, which supports premium attachment rates in coastal and retirement communities. Texas continues to generate high absolute volume due to population scale, and regional chains leverage private-label adjustable programs to address family households with budget sensitivity and wellness needs in tandem. Store networks across the South also offer multi-brand exposure in a single trip, helping couples efficiently compare feature sets and price ladders when planning upgrades in primary bedrooms. This region remains foundational for the United States mattress bases market as retailers refine demonstrations to link software features with everyday comfort outcomes across diverse households.

The West is the fastest-growing region, with an 8.44% CAGR through 2031, driven by early adoption of smart home technologies and robust DTC activity that bundles adjustable bases with financing and app ecosystems. California’s large addressable base and appetite for connected devices amplify trials of anti-snore automation, voice control, and temperature-coordinated comfort settings that differentiate premium setups in metropolitan markets. Arizona’s retiree inflows add a second demand vector for therapeutic bases that favor hi-low functionality, and head-lift presets to ease nighttime breathing and entry or exit comfort. Retail assortments in the West typically feature a deep range of adjustable configurations, paired with content that explains compatibility with existing frames and the value of zero-clearance designs in bedrooms with built-ins or storage beds. This combination of innovation appetite and demographic fit lifts the region’s share of premium sales and supports momentum for the United States mattress bases market through 2031.

The Northeast and Midwest show balanced demand tied to housing stock and household budgets, with conversion hinging on clear demonstrations and financing options that de-risk adoption for first-time buyers of adjustable bases. Older housing in parts of the Northeast constrains king sizes, which tilts premium adoption toward queen and split-king in rooms that can accommodate independent motion presets for couples. Midwest shoppers respond to private-label metal-frame adjustable bases that hit mid-tier price points while delivering the core feature set, sourced through OEMs with established service coverage by regional retailers. Safety and regulatory compliance are nationally uniform, though individual states, such as California, maintain additional flammability labeling standards that shape product disclosures and testing practices. Across both regions, omnichannel research with in-store trials keeps conversion rates steady, supporting a broad geographic foundation for the United States mattress bases market as supply chains stabilize and promotional calendars normalize in 2026.

Competitive Landscape

Competition in the United States mattress bases market features two large OEM anchors and two dominant branded ecosystems that shape distribution, product roadmaps, and attachment strategies through 2026. Ergomotion positions as the world’s largest adjustable base manufacturer with more than 10 million units sold, providing OEM platforms for leading brands and maintaining North American warehousing to support retailers with short lead times and broad assortments. Leggett & Platt leverages longstanding relationships with Top 25 bedding retailers and emphasizes customization for private-label programs across price ladders, which raises floor coverage for adjustable features in showrooms nationwide. This OEM backbone delivers consistent quality and service levels, helping retailers meet warranty and white-glove delivery expectations for heavier articulated models. The result is a supply environment that supports rapid feature diffusion and cost discipline, benefiting the United States mattress bases market in 2026.

At the branded tier, Tempur Sealy and Sleep Number compete on software-enabled comfort, data integration, and network control over the point of sale. Following the 2025 completion of the Mattress Firm acquisition, Tempur Sealy can merchandise TEMPUR-Ergo smart bases across a large store footprint and coordinate messaging with mattresses and apps that highlight snore response and guided positions. Sleep Number’s FlexFit line integrates with SleepIQ to monitor biosignals and adjust settings, a strategy that underpins premium pricing and encourages ecosystem attachment among couples and solo sleepers. Serta Simmons and Beautyrest complement this with tiered lines such as Baselogic that democratize key features and offer clear step-ups for shoppers comparing value and premium models. These strategies align the United States mattress bases market around smart features, vertical distribution, and private-label breadth, maintaining a competitive balance across channels.

Strategic moves highlight the emphasis on software, inventory placement, and footprint optimization in 2025 and 2026. Ergomotion launched its Sleep Assist app path at CES 2026 to extend automation and guidance that can synchronize with modern wellness ecosystems, a move that deepens software differentiation in its OEM offer. Logicdata and Dreamotion introduced a domestic inventory program to shorten United States lead times and reduce retailer risk, supporting omnichannel speed-to-market and in-season promotional agility. Leggett & Platt implemented footprint changes to align with tariff frameworks and cost-structure needs, indicating a measured approach to component sourcing and final assembly across North America. Collectively, these steps reinforce a competitive environment in which OEM capacity, software features, and store control shape outcomes for the United States mattress bases market through 2031.

United States Mattress Bases Industry Leaders

Leggett & Platt, Inc.

Tempur Sealy International

Serta Simmons Bedding

Sleep Number Corporation

Ergomotion Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Ergomotion opened a new Design Showroom and celebrated its 20th Anniversary, commemorating two decades since the company's founding and its evolution from a startup actuator supplier to the world's largest adjustable base manufacturer.

- September 2025: Leggett & Platt announced the consolidation of its Georgetown Adjustable Bed manufacturing plant in Kentucky into its Mexico operation by year-end 2025, a move impacting 122 jobs and driven by what the company described as difficult business conditions.

- August 2025: Juna Sleep Systems introduced the Juna H-Bed gapless adjustable mattress system, a modular solution designed to eliminate the center gap inherent in traditional split-king adjustable bed configurations.

- January 2025: Serta Simmons Bedding launched a new line of adjustable bed bases under the Baselogic brand, featuring four distinct models designed to complement both Beautyrest and Serta product lines.

United States Mattress Bases Market Report Scope

Mattress bases, also called bed bases, help to support and extend the life of a mattress. They also add height and structural integrity to the bed. Box springs and Foundations exist among the most popular bed bases in the market, providing longevity and firm support to the beds.

The United States mattress bases market is segmented by type (box spring, slatted bases & bed frames, ottoman, platform, bunky boards, and other types), by distribution channel (specialty stores, departmental stores, hypermarkets or supermarkets, online channel), by end-user (residential, hospitals, hotels, and other end-users).

The report offers market size and forecasts in value (USD) for all the above segments.

| Platform |

| Box Spring |

| Slats |

| Adjustable |

| Other Bases |

| Wood |

| Metal |

| Other Materials |

| Full Size |

| Twin Size |

| Twin-XL Size |

| Queen Size |

| King Size |

| Special Size (California King) |

| Residential |

| Commercial |

| Offline | Home Centers |

| Specialty Stores | |

| Other Distribution Channels | |

| Online |

| Northeast |

| Midwest |

| South |

| West |

| By Base Type | Platform | |

| Box Spring | ||

| Slats | ||

| Adjustable | ||

| Other Bases | ||

| By Material | Wood | |

| Metal | ||

| Other Materials | ||

| By Size | Full Size | |

| Twin Size | ||

| Twin-XL Size | ||

| Queen Size | ||

| King Size | ||

| Special Size (California King) | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | Offline | Home Centers |

| Specialty Stores | ||

| Other Distribution Channels | ||

| Online | ||

| By Region | Northeast | |

| Midwest | ||

| South | ||

| West | ||

Key Questions Answered in the Report

What is the 2026 value and long-term growth outlook for the United States mattress bases market?

The United States mattress bases market size is USD 2.18 billion in 2026 and is projected to reach USD 3.01 billion by 2031 at a 6.67% CAGR, reflecting steady value growth anchored in smart adjustable bases.

Which base type leads and which grows fastest in the United States mattress bases market?

Adjustable bases lead with a 41.00% share in 2025 and are also the fastest-growing through 2031, with a 7.38% CAGR, driven by app-enabled features and retail demonstrations that drive attach rates.

Which region is expanding the quickest in the United States mattress bases market?

The West is the fastest growing at 8.44% CAGR through 2031, supported by early adoption of connected features and active omnichannel bundling of bases with mattresses.

What materials are gaining share in the United States mattress bases market?

Wood remains in the lead, but metal frames are growing faster, with a 6.93% CAGR, because adjustable bases rely on steel chassis to meet motion and durability requirements.

How do tariffs and supply challenges affect the United States mattress bases market in 2026?

Tariff layers added in 2025 increased input costs for steel and electronics, encouraging footprint shifts to USMCA-compliant sites and modestly weighing on near-term growth until supply chains rebalance.

Page last updated on: