Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 18.65 Billion |

| Market Size (2026) | USD 19.57 Billion |

| Market Size (2031) | USD 24.92 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

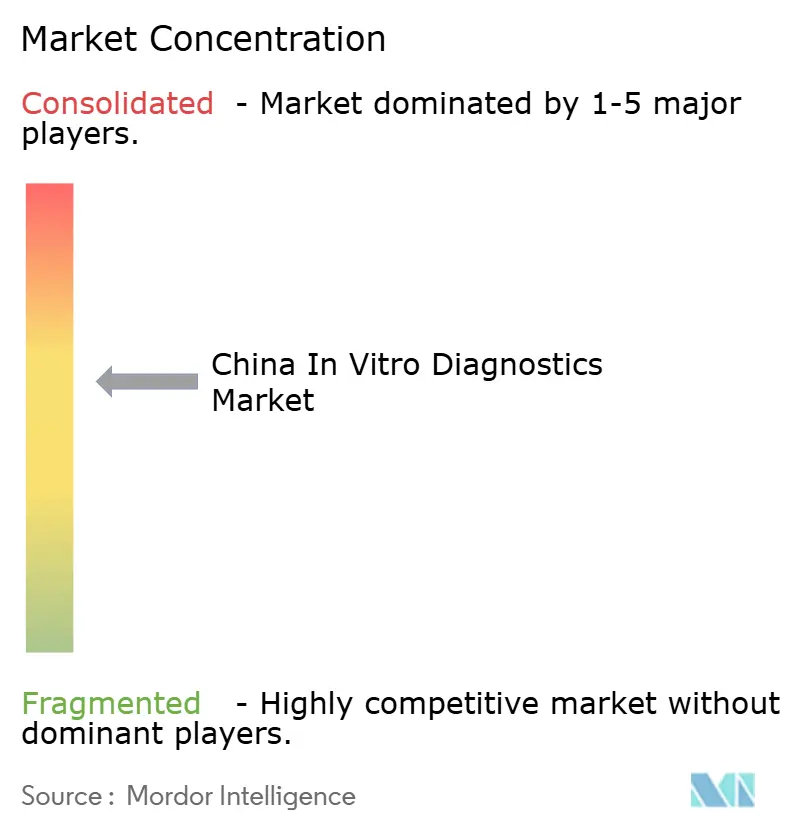

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

China In-Vitro Diagnostics Market Analysis by ���ϲ�����

The China In-Vitro Diagnostics Market size is projected to be USD 18.65 billion in 2025, USD 19.57 billion in 2026, and reach USD 24.92 billion by 2031, growing at a CAGR of 4.95% from 2026 to 2031.

With 297 million citizens aged 60 and above and 118 million to 148 million adults living with diabetes, clinical demand remains robust. However, aggressive volume-based procurement reforms have driven reagent prices in provincial tenders down by up to 90%. Consolidation pressures are compelling both multinational and domestic suppliers to localize production, automate quality systems, and transition from commodity assays to software-enabled, high-complexity testing that aligns with Diagnosis-Related Group payment incentives. Simultaneously, the National Medical Products Administration's updated GMP standards, effective November 1, 2026, mandate stricter traceability and post-market surveillance requirements. While these regulations increase compliance costs, they also elevate competitive standards. Together, these factors moderate topline growth while accelerating the industry's structural shift toward integrated reagent-instrument-software business models.

Key Report Takeaways

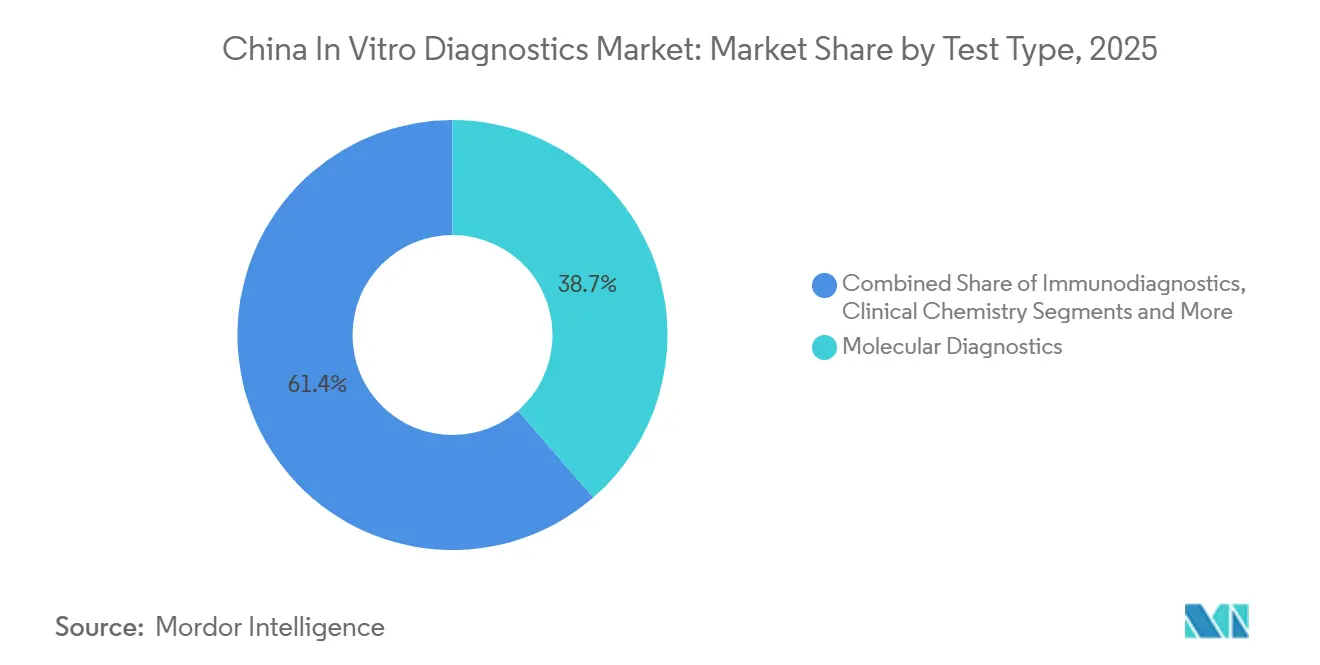

- By test type, molecular diagnostics led with a 38.65% share of the China in-vitro diagnostics market size in 2025, while immunodiagnostics is advancing at a 6.87% CAGR through 2031.

- By product, reagents and kits accounted for 61.43% of revenue in the China in-vitro diagnostics market in 2025; software and services are forecast to grow fastest at a 6.67% CAGR through 2031.

- By usability, disposable devices accounted for 68.65% of the China in-vitro diagnostics market share in 2025, whereas reusable equipment is projected to expand at a 7.84% CAGR to 2031.

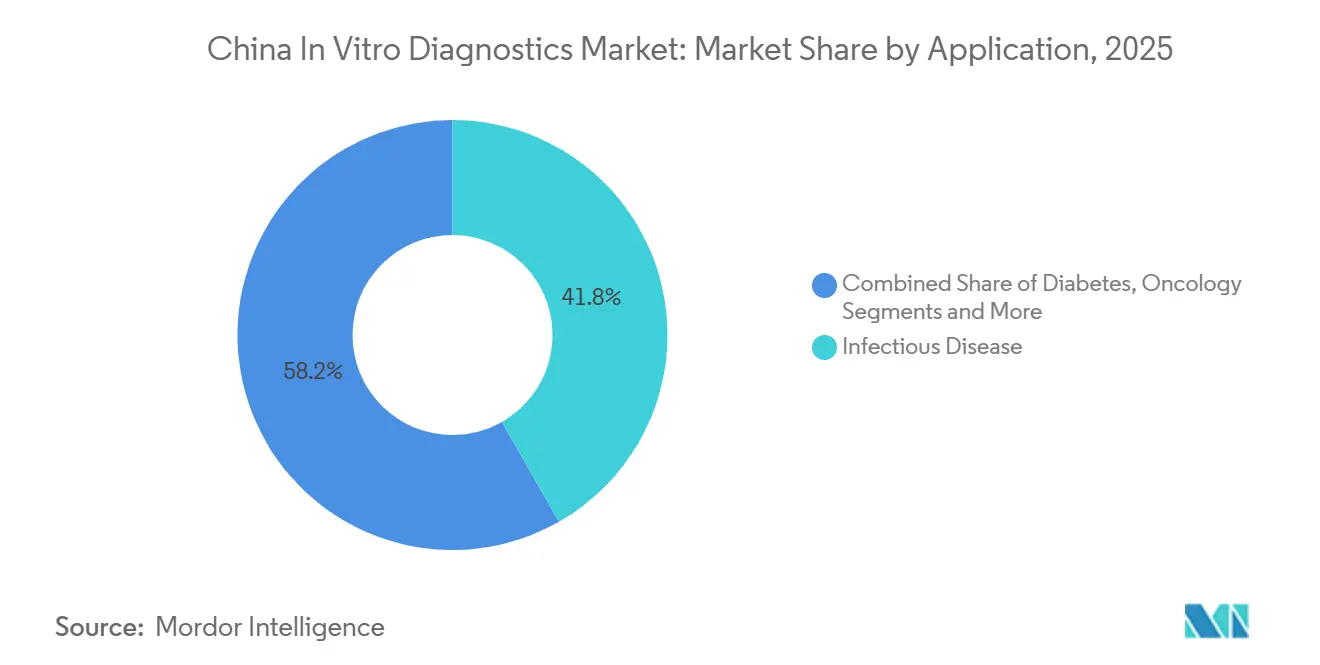

- By application, infectious disease testing dominated with a 41.76% revenue share in 2025, but oncology diagnostics is set to grow at a 7.43% CAGR through 2031.

- By end user, hospital laboratories captured 52.65% of spending in 2025; home-care and self-testing users are growing at a 5.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic And Infectious Disease Burden | +1.2% | National, higher intensity in Beijing, Shanghai, Guangzhou, Liaoning, Jiangsu, Sichuan | Long term (≥ 4 years) |

| Rapidly Ageing Population | +1.0% | Northeastern and coastal provinces (Liaoning, Jilin, Heilongjiang, Jiangsu, Zhejiang, Shanghai) | Long term (≥ 4 years) |

| Government Healthcare Reform And Insurance Expansion | +0.8% | Nationwide rollout, fastest in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Technological Advancements In Molecular And Point-Of-Care Testing | +1.1% | Early adoption in tier-1 hospitals and tertiary cancer centers | Medium term (2-4 years) |

| Local Manufacturing Expansion And Import Substitution | +0.7% | Shenzhen, Wuhan, Suzhou, Chengdu manufacturing corridors | Medium term (2-4 years) |

| Digital Health Integration And Real-Time Data Connectivity | +0.6% | Pilot programs in Zhejiang, Jiangsu, Guangdong | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rising Chronic and Infectious Disease Burden

Diabetes affected 148 million adults in 2024, and cardiovascular disease caused 40% of deaths, driving sustained demand for HbA1c, lipid panels, and cardiac biomarkers. The National Cancer Center recorded 4.82 million new cancer cases in 2024, spurring adoption of tumor-marker panels and next-generation sequencing companion diagnostics for therapies such as EGFR inhibitors. Mandatory HIV, hepatitis B, and syphilis screening for pregnant women expanded the addressable immunoassay market. Rapid pathogen response capability was demonstrated when Daan Gene secured approval for a monkeypox nucleic acid test kit in August 2024. Although mutual recognition of test results lowers duplicate routine panels, specialty assay volumes continue to rise.

Rapidly Ageing Population

The 60-plus cohort reached 297 million in 2024 and is projected to reach 400 million by 2035, escalating the use of coagulation, hematology, and renal-function assays. Community elder-care centers now deploy point-of-care devices for glucose, lipid, and uric acid monitoring under a 2025 pilot spanning 10,000 sites in Jiangsu, Zhejiang, and Sichuan. Mindray released a compact chemiluminescence analyzer in 2025, tailored for primary care, that integrates WeChat-based result delivery to offset staffing shortages in rural clinics. Regulatory fast-tracking led to NMPA clearance for 12 self-testing devices in 2024-2025, underscoring policy support for at-home monitoring.

Rapid Decentralisation to Point-of-Care Settings

Portable systems such as iPonatic deliver 30-minute infectious-disease panels from fingertip samples[2]Jun-Feng Li, “Streamlined POCT Solution for Rapid Infectious-Disease Detection,” Nature Scientific Reports, nature.com. Emergency departments adopting “point-of-careology” report materially shorter therapeutic turnaround times. Rural pilots covering 2,700 village clinics showcase scalable pathways for nationwide deployment. Connectivity and cloud dashboards enable remote supervision, plugging urban–rural gaps.

Technological Advancements in Molecular and Point-of-Care Testing

MGI Tech’s DNBSEQ-T20 platform doubled national next-generation sequencing throughput, pushing per-genome cost to USD 100 by 2026. The NMPA cleared eight companion diagnostics between 2024-2025, including BRCA1/2 and KRAS assays, underlining official support for precision oncology. Wondfo’s 15-minute troponin-I cartridge broadened emergency-department testing beyond glucose strips. Mindray embedded DeepSeek’s large language model into hematology analyzers, reducing manual differentials by 30% in a pilot. Software-centric capabilities are redefining competitive advantage away from price toward workflow productivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Erosion From Volume-Based Procurement | -1.8% | Provinces with centralized tenders (Anhui, Jiangxi, Hubei, Shandong) | Short term (≤ 2 years) |

| Stringent And Evolving Regulatory Requirements | -0.9% | National—affects all manufacturers seeking NMPA registration and GMP compliance | Medium term (2-4 years) |

| Regional Disparities In Laboratory Infrastructure | -0.6% | Western and rural provinces where Healthy China 2030 upgrades are still ramping up | Long term (≥ 4 years) |

| Data Privacy And Cybersecurity Compliance Costs | -0.4% | National—intensified enforcement of Personal Information Protection Law across all regions | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Price Erosion from Volume-Based Procurement

Provincial tenders in 2024-2025 slashed immunoassay reagent prices to CNY 3-5 per test from CNY 15-20, wiping 30 percentage points off gross margins and prompting Roche and Siemens to exit unprofitable SKUs. Jiangxi’s 2025 biochemical-reagent round cut average selling prices by 72%, driving smaller firms to shutter niche assay lines below 1 million annual tests. Mutual recognition of results across 31 provinces trimmed routine-panel volumes 15-20%[2]Jun-Feng Li, “Streamlined POCT Solution for Rapid Infectious-Disease Detection,” Nature Scientific Reports, nature.com. Manufacturers are countering by bundling instruments at cost and focusing R&D on premium assays that remain outside tender scope, though specialty validation cycles are delaying revenue recovery.

Stringent and Evolving Regulatory Requirements

The NMPA’s 2025 GMP revision, effective November 2026, mandates ISO 13485 alignment and raw-material traceability, adding CNY 20 million-50 million compliance costs per facility[3]National Healthcare Security Administration, “2023 Healthcare Security Statistical Bulletin,” NHSA, nhsa.gov.cn. Unique device identification rules require an investment of up to CNY 5 million in each manufacturer's barcode infrastructure. Class III approval timelines have lengthened to 18-24 months, stalling product launches. Data-privacy fines totaling CNY 120 million were levied on eight LIS vendors in 2024, intensifying cybersecurity spending needs.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Diagnostics Lead, Immunoassays Accelerate

Molecular diagnostics accounted for 38.65% of the market in 2025, underpinned by next-generation sequencing and infectious-disease panels. Immunodiagnostics is on track for the fastest 6.87% CAGR through 2031 as domestic chemiluminescence systems displace imports in provincial tenders. The China in-vitro diagnostics market size for molecular platforms is expected to rise alongside companion-diagnostic uptake, yet reimbursement exclusions for 12 liquid-biopsy assays in 2025 temper short-term growth. Clinical-chemistry volumes dropped by 15-20% in Jiangsu and Zhejiang due to mutual recognition policies that reduced duplicate lipid and liver-function tests. Hematology benefited from ISO 15189-driven replacement of legacy 3-part analyzers, with Mindray and Sysmex offering automated slide-making modules that captured 60% combined share.

In 2025, BGI Genomics launched a CNY 500 whole-exome panel and won reimbursement in eight provinces, illustrating how falling sequencing costs are broadening access. YHLO’s iFlash 3000, priced 45% below Abbott’s Alinity, penetrated 700 tier-2 hospitals within its first year. Although molecular diagnostics remains the largest revenue pool, continued price cuts necessitate workflow innovation and clinical-value demonstration to sustain margins in the China in-vitro diagnostics market.

By Product: Reagents Dominate, Software Gains Traction

Reagents and kits generated 61.43% of product revenue in 2025, yet software and services are growing at 6.67% CAGR as laboratories digitize. Instruments face lengthening replacement cycles under DRG budgets, but vendors offset this by bundling zero-margin analyzers with multi-year reagent contracts. Mindray’s Wuhan complex embodies this shift, securing consumable deals worth up to CNY 1 billion per hospital chain.

Real-time data mandates from the National Health Commission bolster middleware demand. Mindray-Alibaba AI modules cut troponin false positives by 12%, helping hospitals avoid readmission penalties. Zhejiang’s blockchain repository demonstrated CNY 800 million in annual cost savings, propelling adoption of the HL7 FHIR standard. With reagent gross margins compressed to 40%, after-sales service, cloud subscriptions, and quality-control consulting now account for 8-12% of leading firms’ sales, a ratio expected to rise within the China in-vitro diagnostics market.

By Usability: Disposables Lead, Re-Usable Equipment Surges

Disposable cartridges, strips, and microfluidic chips commanded 68.65% share in 2025, fueled by expanding OTC approvals for glucose and cholesterol tests. However, reusable equipment is expected to grow at a 7.84% CAGR through 2031 as hospitals replace aging analyzers to meet ISO 15189 standards. The China in-vitro diagnostics market share of re-usable analyzers will climb to about 40% of hematology systems installed before 2015 that hit end-of-life in 2026.

Product design increasingly emphasizes connectivity. Mindray’s BS-2000M chemistry analyzer streams QC data to cloud dashboards, lowering calibration errors by 18%. Wondfo’s disposable 15-minute troponin cartridge exemplifies cross-pollination, bringing lab-grade sensitivity to emergency settings and intensifying format blurring within the China in-vitro diagnostics market.

By Application: Infectious Diseases Largest, Oncology Fastest

Infectious-disease assays made up 41.76% of 2025 revenue, driven by mandatory HIV, hepatitis B/C, syphilis, and TB screening. Oncology tests are forecast to expand at 7.43% CAGR due to National Cancer Center screening pilots for lung, colorectal, and gastric tumors. Diabetes monitoring remains a core demand pillar, though continuous glucose monitoring has trimmed lab-based HbA1c volumes by roughly 9%.

Eight NMPA-approved companion diagnostics between 2024-2025, covering BRCA1/2, EGFR, and KRAS, are pushing sequencing into mainstream oncology workflows. Infectious-disease volumes declined after COVID-19 mandates lapsed, but routine hepatitis and HIV screening remains stable. As value-based care advances, high-specificity oncology panels are positioned to capture oversized profit pools in the China in-vitro diagnostics market.

By End User: Hospitals Dominate, Homecare Expands

Hospital laboratories absorbed 52.65% of spending in 2025, processing up to 1,000 daily samples with automated hematology and chemiluminescence lines. Stand-alone reference labs gained share as hospitals outsourced complex assays, with Adicon and KingMed holding 40% together. Home-care and self-testing users will rise at 5.64% CAGR, propelled by 12 NMPA-approved OTC devices and the Ministry of Civil Affairs’ elder-care strategy.

Andon Health’s USD 45.9 million iHealth stake taps rising demand for Bluetooth-enabled glucose and ECG devices integrated into WeChat mini-programs. Hospitals, facing procurement cost ceilings, are consolidating purchasing; the top 10 networks already represent 25% of IVD expenditure, intensifying key-account dynamics in the China in-vitro diagnostics market.

Competitive Landscape

In 2025, the top five suppliers—Mindray, Roche, Abbott, Danaher, and Siemens—accounted for approximately 30% of the market's combined revenue, indicating a moderately concentrated market structure. Domestic players reinforced their market positions, with Mindray integrating AI into hematology workflows and offering bundled instruments at competitive prices to secure long-term reagent contracts. Similarly, YHLO disrupted the market by pricing its chemiluminescence systems 45% lower than imported alternatives. In response, multinational companies localized production, exemplified by Roche’s Suzhou hub, which generated an additional RMB 360 million in revenue within 12 months of obtaining NMPA registration.

Private equity activity intensified, highlighted by Andon Health’s investment in iHealth and Tellgen’s acquisition of Wuhan HealthCare Biotech. Specialty segments continued to attract interest, as demonstrated by Beckman Coulter’s November 2025 collaboration with Eisai China to co-develop Alzheimer’s biomarkers, targeting the country’s 15 million dementia patients. Emerging disruptors such as AI-powered pathology provider Infervision and 30-minute PCR innovator Sansure Biotech are leveraging software-driven differentiation to gain a competitive edge in China’s in vitro diagnostics market.

Technological competition is accelerating, particularly in sequencing throughput and AI-driven analytics. BGI Genomics’ DNBSEQ-T20 reduced genome sequencing costs to USD 100, pressuring Illumina’s pricing strategy. The partnership between Mindray and Alibaba Cloud on a quality-control SaaS solution highlights the industry’s shift toward recurring revenue models. Furthermore, volume-based procurement initiatives and stringent GMP upgrades are driving mergers and acquisitions, favoring large-scale players capable of funding compliance and digital transformation efforts.

China In-Vitro Diagnostics Industry Leaders

F Hoffmann-la Roche Ltd

Thermo Fisher Scientific Inc

Abbott Laboratories

Shenzhen Mindray Bio-Medical Electronics Co. Ltd

Danaher Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The National Medical Products Administration (NMPA) in China approved the OncoMate Microsatellite Instability (MSI) Detection Kit as a Class III in vitro diagnostic device. It is intended as a companion diagnostic to identify patients with MSI-high (MSI-H) solid tumors for treatment with KEYTRUDA® (pembrolizumab), the anti-PD-1 therapy from Merck & Co., Inc., Rahway, NJ, USA. This is Promega’s first companion diagnostic to receive approval from the NMPA.

- October 2025: The IMQ Group strengthened its presence in the Asian market with the opening of IMQ Lab Suzhou Co. Ltd., an ISO/IEC 17025-accredited laboratory dedicated to testing medical devices, in vitro diagnostics (IVD), small household appliances, and lighting equipment. The new facility aims to provide manufacturers and global operators with a qualified reference point for verifying compliance with major international and European standards, ensuring the safety and quality of products made in China and destined for global markets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines China's in-vitro diagnostics (IVD) market as the total annual revenue generated inside China from clinical-use instruments, reagents and consumables, and diagnostic software/services that enable ex-vivo detection or monitoring of physiological status across all healthcare settings. Tests covered range from high-throughput core-lab chemistry to rapid point-of-care assays and home self-tests.

Scope exclusion: veterinary diagnostics and life-science research-only assay kits are kept out of scope.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Immuno-Diagnostics

- Molecular Diagnostics

- Hematology

- Coagulation

- Microbiology

- Other Test Types

- By Product

- Instruments

- Reagents & Kits

- Software & Services

- By Usability

- Disposable IVD Devices

- Re-Usable Equipment

- By Application

- Infectious Diseases

- Diabetes

- Oncology

- Cardiology

- Auto-Immune Disorders

- Nephrology

- Other Applications

- By End User

- Stand-Alone Laboratories

- Hospital-Based Laboratories

- Point-Of-Care Settings

- Home-Care & Self-Testing Users

Detailed Research Methodology and Data Validation

Primary Research

To close data gaps, we interviewed laboratory directors, procurement managers at tier-3 hospitals, domestic reagent manufacturers, and regional distributors across seven provinces. Their perspectives on average selling prices, menu expansion, and volume-based procurement impacts helped us validate model assumptions and fine-tune growth drivers.

Desk Research

Mordor analysts first mapped the sector using publicly available cornerstones such as NMPA product approval lists, National Health Commission hospital statistics, China Association of IVD (CAIVD) industry bulletins, UN Comtrade reagent trade codes, peer-reviewed journals (e.g. Chinese Journal of Laboratory Medicine), and provincial tender catalogs. Company 10-Ks, IPO prospectuses, and investor decks enriched price-band and installed-base insights, which were then cross-referenced against paid databases, D&B Hoovers for local player financials and Dow Jones Factiva for deal flow. These sources illustrate but do not exhaust the references consulted.

Market-Sizing & Forecasting

We applied a top-down demand-pool build starting with China's annual diagnostic test throughput, segmented by modality, and multiplied each cohort by province-weighted average selling prices. Selected bottom-up roll-ups, such as PCR analyzer shipments and reagent import data, served as plausibility checks. Key variables modeled include:

hospital bed additions and lab automation penetration,

chronic disease prevalence (diabetes, cancer, hepatitis),

reagent price resets under national volume-based procurement,

instrument replacement cycles, and

point-of-care kit adoption in primary care centers.

A multivariate regression with lagged macro and epidemiological indicators generated the forecast, and scenario analysis gauged policy shocks. Any residual data voids were bridged through ratio estimates anchored to verified regional benchmarks.

Data Validation & Update Cycle

Outputs undergo three-layer variance checks, senior analyst sign-off, and reconciliation against independent trade and utilization signals. We refresh every twelve months, with mid-cycle revisions triggered by material events such as nationwide tender rounds.

Why Our China In Vitro Diagnostics Baseline Commands Reliability

Published estimates often diverge because firms select differing product baskets, pricing bases, or refresh cadences.

Key gap drivers include whether instruments and software are counted alongside reagents, treatment of direct-to-consumer self-tests, and how price-volume procurement cuts are baked into projections. Mordor's model captures full system revenue, applies rolling FX adjustments, and is refreshed annually, whereas some peers freeze ASPs for multiple years or exclude low-margin domestic reagents.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.65 B (2025) | ���ϲ����� | - |

| USD 6.20 B (2025) | Global Consultancy A | Reagents-only scope; hospital instruments excluded |

| USD 5.70 B (2024) | Regional Consultancy B | Uses list prices, omits VBP price cuts and self-testing kits |

| USD 12.00 B (2024) | Trade Journal C | Stops at tier-2 cities; limited primary checks on gray-market imports |

Taken together, the comparison shows how Mordor's disciplined variable selection, yearly refresh, and dual-path validation deliver a balanced, transparent baseline that decision-makers can confidently rely on.

Key Questions Answered in the Report

How large will the China in-vitro diagnostics market be in 2031?

It is forecast to reach USD 24.92 billion by 2031, expanding at a 4.95% CAGR from 2026.

Which test category is growing fastest?

Immunodiagnostics is projected to post the highest 6.87% CAGR owing to rapid uptake of domestic chemiluminescence platforms.

What drives hospital demand for re-usable analyzers?

ISO 15189 accreditation and the replacement of pre-2015 hematology instruments are spurring a 7.84% CAGR in re-usable equipment.

How are price cuts affecting suppliers?

Provincial tenders have reduced reagent prices by up to 90%, pushing vendors to bundle instruments at cost and focus R&D on specialty assays.

Which regions lead in advanced diagnostics adoption?

Tier-1 cities such as Beijing and Shanghai adopt next-generation sequencing earliest, while Jiangsu and Zhejiang drive mutual-recognition initiatives that free budgets for specialty tests.

Why are software and services gaining share?

Real-time data-sharing mandates and AI-driven quality control are elevating middleware and subscription revenues, which are set to grow at a 6.67% CAGR.

Page last updated on: