In-Vitro Diagnostics Quality Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 1.85 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

In-Vitro Diagnostics Quality Control Market Analysis by ���ϲ�����

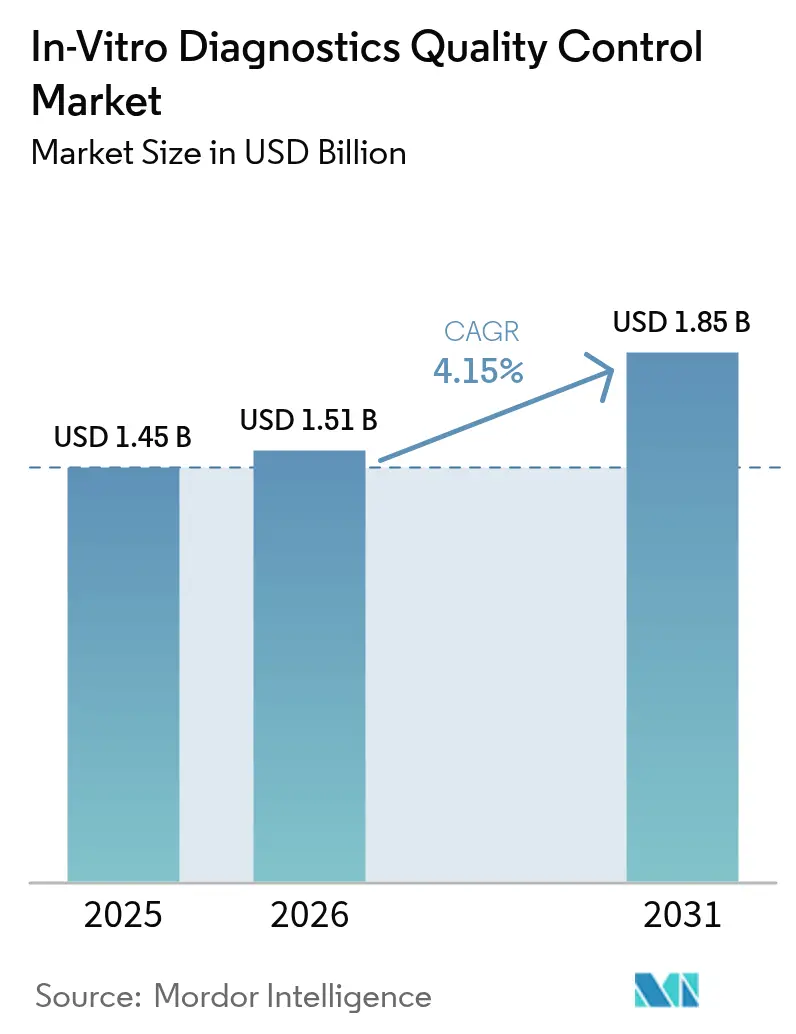

The In-Vitro Diagnostics Quality Control Market size was valued at USD 1.45 billion in 2025 and is estimated to grow from USD 1.51 billion in 2026 to reach USD 1.85 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031).

The industry is transitioning from a focus on reagent volume to data-driven quality ecosystems that integrate hardware, software, and services. Molecular diagnostics is leading this growth, fueled by the increasing adoption of liquid biopsies and NGS panels, which require advanced multi-analyte reference materials that traditional controls cannot support. Stricter regulatory frameworks under the EU IVDR and U.S. CLIA are tying reimbursement to measurable quality performance, pushing laboratories to implement ISO-traceable controls. Additionally, middleware solutions that integrate control data into electronic health records have proven effective, reducing reportable errors by 22% in hospital pilot programs conducted in 2025.

Key Report Takeaways

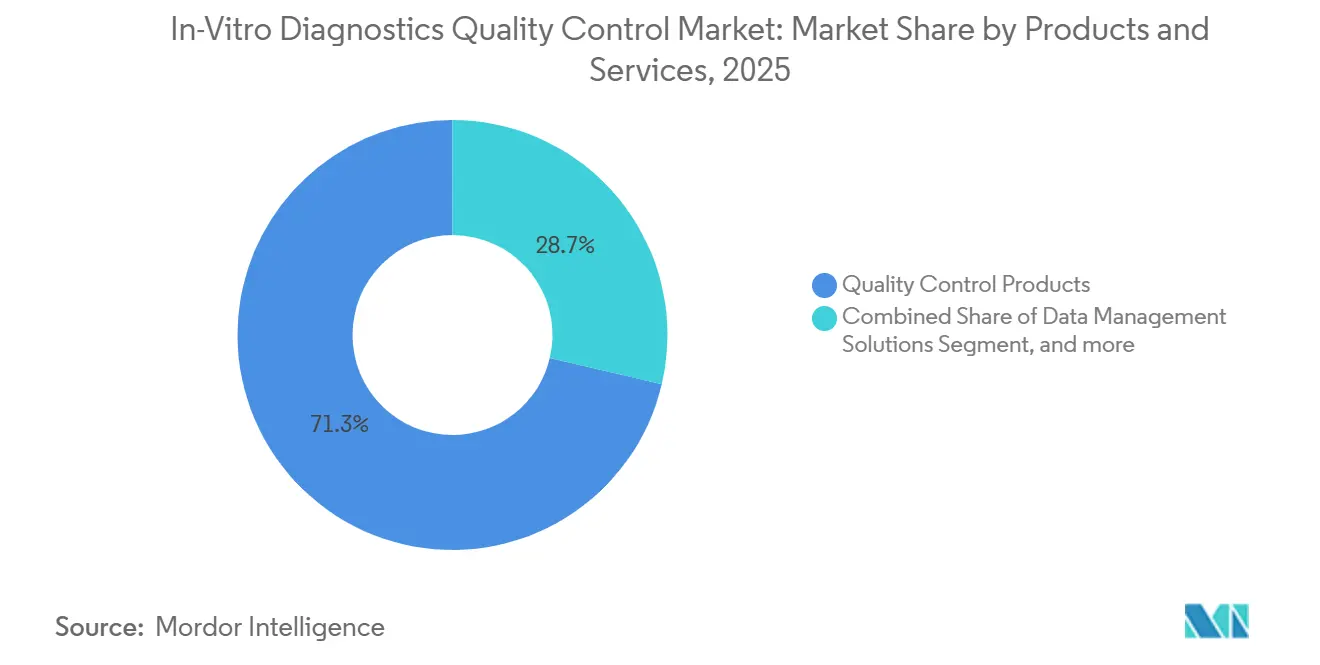

- By products and services, quality control products led with 71.32% revenue share in 2025; data management solutions are projected to expand at a 6.75% CAGR through 2031.

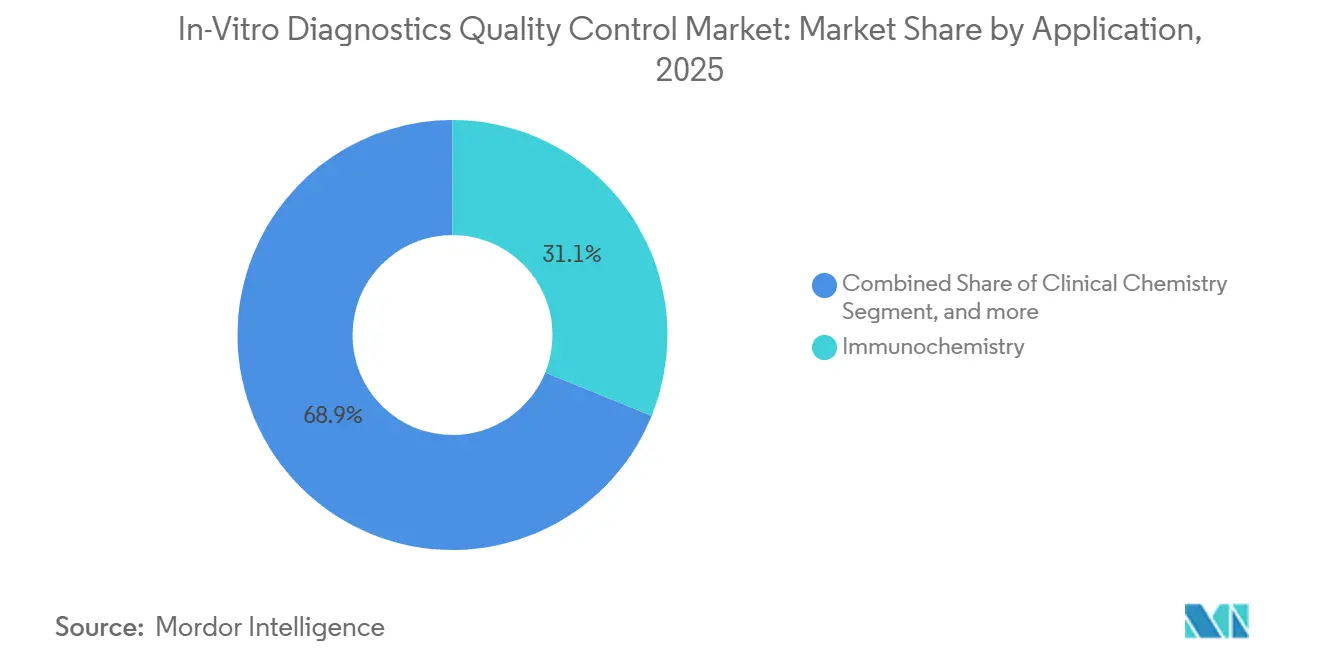

- By application, immunochemistry accounted for 31.12% of the in-vitro diagnostics quality control market share in 2025, while molecular diagnostics is expected to advance at a 6.87% CAGR to 2031.

- By end user, independent clinical laboratories accounted for 44.55% of 2025 revenue, and IVD manufacturers and contract research organizations are growing at a 7.86% CAGR.

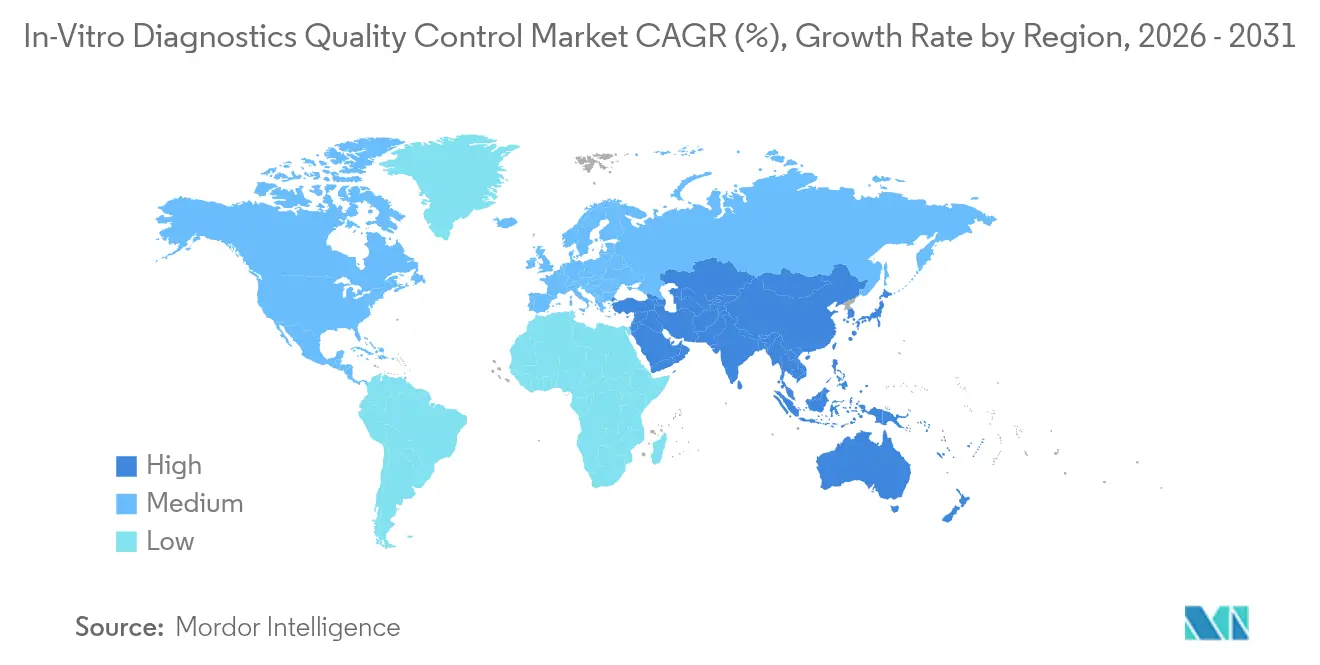

- By geography, North America accounted for 44.12% of revenue in 2025, whereas Asia-Pacific is expected to grow at a 5.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global In-Vitro Diagnostics Quality Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global Disease Burden | +0.9% | Global with acute pressure in APAC and MEA | Long term (≥ 4 years) |

| Expansion of Accredited Clinical Laboratories | +0.8% | North America and EU core, spill-over to APAC | Medium term (2-4 years) |

| Technological Advancements in IVD Platforms | +0.7% | Global led by North America and Western Europe | Medium term (2-4 years) |

| Shift Toward Decentralized and Point-of-Care Testing | +0.6% | North America, EU, and urban APAC | Short term (≤ 2 years) |

| Increasing Regulatory Focus on Diagnostic Accuracy | +0.5% | North America, EU, and Australia | Short term (≤ 2 years) |

| Digital Transformation and Data Integration in Laboratories | +0.6% | North America, EU, and select APAC markets | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Growing Global Disease Burden

Chronic and infectious diseases are expanding test volumes that need daily quality oversight, driving direct growth in the in-vitro diagnostics quality control market. Non-communicable ailments accounted for 74% of global deaths in 2024, and rising diabetes prevalence boosts demand for glycated hemoglobin controls that laboratories must run at multiple levels each day. Oncology laboratories increased liquid biopsy volumes by 28% in 2025, yet fewer than 40% stock circulating tumor DNA materials with defined allele frequencies, leaving a compliance gap regulators have begun to question[1]U.S. National Cancer Institute, “Liquid Biopsy Market Trends 2025,” National Cancer Institute, cancer.gov. Public health facilities in Brazil and Thailand tripled molecular control inventories during 2024-2025 outbreaks, underscoring how epidemiological swings escalate per-test quality costs. Quality spending now aligns more with disease volatility than routine growth, favoring vendors that can scale multi-analyte reference kits quickly. This trend will keep upward pressure on consumable demand even as laboratories adopt data platforms.

Expansion of Accredited Clinical Laboratories

Accreditation has shifted quality control from optional to mandatory spending, enlarging the in-vitro diagnostics quality control market across mature regions. The College of American Pathologists counted 8,200 accredited U.S. labs by December 2025, a 6% rise since 2023, after Medicare tied reimbursement eligibility to deemed-status recognition. ISO 15189 became a prerequisite for public procurement in Germany and France, prompting 1,400 private labs to launch compliance programs that require documented controls on every platform. China ordered all tertiary hospitals to secure ISO 15189 status by 2027, influencing roughly 3,000 facilities and fueling short-term spikes in bulk control purchases. Accreditation also pushes buyers toward suppliers that can provide certificates traceable to international reference methods, consolidating share among multinational vendors. Laboratories now treat control documentation as a credential for payer negotiations and public tenders.

Technological Advancements in IVD Platforms

High-throughput systems such as Roche cobas pro process up to 300 samples per hour and require controls with proven commutability with fresh human serum, a feature that only a few third-party suppliers offer today. Abbott Alinity flagged 12% of generic controls as out of linearity during 2025 validations, pressuring labs to adopt proprietary materials or finance costly bridging studies. In molecular diagnostics, next-generation sequencing panels require synthetic DNA references with single-nucleotide precision, yet fewer than eight suppliers hold FDA clearance for BRCA1 or EGFR materials. Specialty firms now develop modular kits that laboratories can tailor for custom gene lists, opening new revenue lanes. Platform vendors have begun bundling exclusive controls within reagent-rental contracts to lock in service revenue. This technical escalator elevates entry barriers and steers demand toward integrated ecosystems.

Shift Toward Decentralized and Point-of-Care Testing

Point-of-care expansion fragments oversight and exposes quality gaps, affecting near-term growth of the in-vitro diagnostics quality control market. The FDA cleared 47 new POCT devices in 2025, but only 18% included stability data for tropical field conditions, leaving clinics uncertain about control frequency. A 2024 CLIA audit found that 34% of physician office labs skipped external control runs due to cost and workflow concerns. Suppliers responded with single-use ambient-stable formats that remove refrigeration needs and cut waste in low-volume sites. Device makers are also embedding electronic algorithms that validate performance using patient result patterns, a shift that could erode up to 20% of traditional control demand by 2030 if regulators approve the method. The tension between convenience and traceability will determine adoption curves.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unfavorable Reimbursement Landscape | -0.5% | North America, secondary effects in EU | Short term (≤ 2 years) |

| Limited Laboratory Infrastructure in Emerging Regions | -0.4% | Sub-Saharan Africa, Southeast Asia, rural Latin America | Long term (≥ 4 years) |

| High Compliance and Validation Costs | -0.3% | North America and EU | Medium term (2-4 years) |

| Supply Chain Vulnerabilities and Material Shortages | -0.2% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Unfavorable Reimbursement Landscape

Payment cuts force laboratories to ration control use, weighing on near-term growth of the in-vitro diagnostics quality control market. Medicare’s schedule has reduced test fees by a cumulative 8.5% since 2021 and more reductions are scheduled through 2027, prompting 42% of U.S. hospital labs to move from twice-daily to once-daily runs for stable analytes in 2025 surveys. Commercial insurers introduced prior authorization on molecular tests, shrinking volumes by 18% and delaying purchases of high-cost next-generation sequencing controls. German statutory payers negotiated a 3.2% tariff cut in 2025 that hit small independent labs hardest, as they lack the volume discounts enjoyed by national chains[2]GKV-Spitzenverband, “Laboratory Tariff Agreement 2025,” GKV-Spitzenverband, gkv-spitzenverband.de. Consolidation accelerated, with 127 U.S. independents acquired in 2025 because shrinking margins made standalone quality programs unsustainable. Suppliers face pressure to lower per-test costs or risk being replaced by in-house electronic quality schemes.

Limited Laboratory Infrastructure in Emerging Regions

Power outages and weak cold-chain capacity limit product viability and sales potential in many low-income markets, restraining the long-term trajectory of the in-vitro diagnostics quality control market. Only 29% of sub-Saharan African labs reported uninterrupted electricity in a 2024 WHO audit, and fewer than 15% possessed functional refrigeration for temperature-sensitive controls. A 2025 survey in India found that 61% of district labs lacked staff trained to interpret Westgard rules, leading to undetected systematic errors. Import tariffs ranging from 12% in Vietnam to 28% in Nigeria inflate control costs by up to 50%, pushing buyers toward uncertified local products with erratic lot performance[3]World Bank, “Customs Tariffs on Medical Reagents Database 2025,” World Bank, worldbank.org. Regulatory bodies in fewer than 20 African and Southeast Asian countries mandate external quality assessment, removing incentives to invest in premium controls. Until multilateral funding improves infrastructure, growth in these regions will lag the global average.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products & Services: Data Platforms Reshape Value Capture

Quality control products accounted for 71.32% of 2025 revenue, equal to about two-thirds of the in-vitro diagnostics quality control market, reflecting laboratories’ continuing need for multi-level liquid and lyophilized reagents for daily instrument checks. Data management solutions, although still a smaller slice, are expanding at a 6.75% CAGR as laboratories adopt cloud platforms that automate Westgard rule application and flag instrument drift in real time. Roche’s navify Quality Control Management demonstrated a 19% cut in unplanned downtime across 34 hospitals by triaging service calls before errors reached patients. Bio-Rad broadened its Liquichek line to 42 analytes per vial, lowering inventory complexity and sustaining reagent demand. At the same time, subscription analytics generate recurring revenue that offsets slowing vial growth.

Laboratories now evaluate suppliers on the combined value of reagents, middleware, and proficiency testing programs, a shift that re-orders procurement criteria toward end-to-end ecosystems. As a result, data platforms win share even when offered at premium prices because they quantify cost avoidance from prevented errors. The in-vitro diagnostics quality control market share for pure-play software is poised to rise as younger lab directors prioritize workflow efficiency over per-vial cost. Suppliers that cannot complement reagents with predictive analytics risk being relegated to second-tier status. Demand therefore tilts toward companies owning ISO-17025 plants plus software development teams, giving multinationals a scale edge.

By Application: Molecular Diagnostics Outpaces Legacy Segments

Immunochemistry retained 31.12% of 2025 demand, benefiting from thyroid, cardiac, and tumor marker panels that require daily multi-level controls. Yet molecular diagnostics is growing at 6.87% as oncology companion tests and infectious-disease panels migrate to multi-gene workflows that need synthetic DNA references traceable to WHO standards. Coagulation is another bright spot because direct oral anticoagulants force laboratories to validate anti-Xa assays with chromogenic substrates, raising control spend per test by about 12% since 2024. Clinical chemistry and hematology remain mature but stable, underpinned by high-volume metabolic panels.

The in-vitro diagnostics quality control market for molecular assays will grow as next-generation sequencing panels expand from single-gene panels to 500-plus-gene oncology portfolios. Fewer than eight vendors now hold FDA clearance for BRCA or EGFR reference materials, creating scarcity pricing and high gross margins. Point-of-care testing controls are also rising because the U.S. FDA draft guidance now expects stability data under worst-case tropical environments, spurring adoption of ambient-stable lyophilized kits. Suppliers that tailor modular kits enabling laboratories to customize mutation mixes stand to capture incremental share. Those lacking nucleic-acid manufacturing capacity face a steep entry barrier, reinforcing consolidation trends in advanced applications.

By End User: IVD Manufacturers Internalize Quality Functions

Independent clinical laboratories generated 44.55% of 2025 revenue, reflecting routine chemistry, immunoassay, and hematology workloads that depend on twice-daily control runs. Hospitals follow, but their growth is tempered as group purchasing organizations negotiate multi-year contracts that cap price increases at 2-3% annually. IVD manufacturers and contract research organizations, though smaller, are expanding at a 7.86% CAGR by conducting in-house validation to shorten regulatory timelines and secure design-history files before product launch. Academic centers buy specialized controls for translational research, driven by the U.S. NIH rigor guidelines that require assay validation evidence in every omics grant.

The in-vitro diagnostics quality control market share for manufacturer-run labs will climb as platform vendors vertically integrate lot-release testing and proficiency programs. Ambulatory and physician-office laboratories lag because 34% failed to meet recommended control frequencies during the 2025 CLIA reviews, citing workflow disruptions. Suppliers responded with single-use vials that cut handling time by 60%, narrowing the compliance gap. Over the forecast period, purchasing power will continue to shift toward multinational IVD companies and consolidated hospital networks, nudging smaller independent labs either to merge or to outsource quality functions.

Geography Analysis

North America captured 44.12% of 2025 revenue, underpinned by stringent CAP accreditation and CMS payment rules that reward documented quality, but growth now moderates as reimbursement cuts pressure laboratories to reduce daily control frequency. The United States alone accounts for more than three-quarters of regional spending, yet its cost-containment climate is pushing suppliers to offer value-based contracts that tie price to instrument uptime. Canada shows steadier momentum because provincial health plans have ring-fenced laboratory budgets through 2028.

Europe is the second-largest region, driven by Germany, France, and the United Kingdom, which together contributed roughly 62% of 2025 sales after the EU IVDR mandated lot-to-lot surveillance for every control shipment. Laboratories fast-tracked ISO 15189 certification to qualify for public tenders, adding about 1,400 new accredited sites in 2024-2025. Southern Europe lags due to fragmented payer systems, but convergence toward Northern standards is expected by 2028. The in-vitro diagnostics quality control market size tied to European public hospitals will likely edge higher as digital quality records become compulsory.

Asia-Pacific advances at a 5.65% CAGR through 2031, led by China’s mandate that all tertiary hospitals secure ISO 15189 status by 2027, a move that touches about 3,000 institutions. India’s private chains continue rolling out tier-2 city labs, broadening reach where facility density is under one lab per 100,000 people. Japan and South Korea remain mature but demand premium multi-level controls as ministries enforce daily QC logs. Emerging ASEAN markets wrestle with refrigeration gaps, so ambient-stable kits dominate orders. The Middle East and Africa still represent a small share, yet Gulf Cooperation Council spending on reference labs positions the region for mid-single-digit growth. South America’s outlook hinges on Brazil and Argentina, where currency swings hinder capital equipment buys but keep consumable purchases resilient, anchoring a baseline for the in-vitro diagnostics quality control market share in the region.

Competitive Landscape

Roche, Bio-Rad Laboratories, Siemens Healthineers, Abbott, and Danaher’s Beckman Coulter collectively controlled 58% of 2025 global revenue, giving the in-vitro diagnostics quality control market a moderately concentrated profile. Leading firms anchor strategy on platform integration; Roche bundles cobas controls and navify software within reagent‐rental agreements that lock customers into multiyear consumable streams. Siemens Healthineers deploys Atellica Quality Control Management on Microsoft Azure, offering laboratories peer-benchmarking dashboards that justify premium pricing. Abbott strengthens defensibility by restricting third-party controls on Alinity instruments after 2025 validation mismatches and now promotes an FDA-cleared respiratory pathogen kit to keep consumables in-house.

Mid-tier players carve niches through formulation innovation. Randox Laboratories and Technopath Clinical Diagnostics supply lyophilized vials with 24-month ambient stability, reducing cold-chain logistics costs by about 30% in regions lacking reliable refrigeration. ZeptoMetrix and SeraCare target molecular assays with customizable synthetic DNA references that laboratories can tailor to any multi-gene oncology panel, winning orders from independent oncology labs. Streck focuses on point-of-care by launching room-temperature platelet and hematology controls that cut handling time in busy clinics.

Competitive dynamics now reward suppliers that couple ISO-17025 manufacturing, deep regulatory affairs, and cloud analytics. Patent filings underscore the shift: Bio-Rad lodged seven patents on lyophilized immunoassay matrices during 2024-2025, while Roche secured intellectual property for multi-site quality dashboards at the U.S. Patent and Trademark Office. Mergers and acquisitions accelerate capability stacking: Bio-Rad purchased Quantum Analytics for USD 340 million to embed predictive algorithms into Liquichek programs, and Thermo Fisher acquired CorEvitas to broaden real-world evidence and external assessment services. As electronic algorithms for “virtual” controls gain regulatory traction, incumbents race to demonstrate software superiority before quality schemes that eschew hardware erode the reagent base. The net effect is a tilt toward vendors able to sell integrated ecosystems rather than stand-alone vials, reinforcing the current share hierarchy while leaving white-space for agile specialists in molecular diagnostics.

In-Vitro Diagnostics Quality Control Industry Leaders

Abbott Laboratories

Thermo Fisher Scientific Inc.

F. Hoffmann-La Roche AG

Siemens Healthineers AG

Bio-Rad Laboratories Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: bioMérieux, one of the world's leaders in the field of in vitro diagnostics, acquired Accellix, a US company specializing in rapid, automated flow cytometry solutions for cell and gene therapy quality control. With this strategic transaction, bioMérieux strengthens its Pharmaceutical Quality Control activity and invests in innovative solutions that will support the growing advanced therapy market and improve patient outcomes worldwide.

- August 2025: bioMérieux, one of the world's leaders in the field of in vitro diagnostics, launched GENE-UP PRO HRM—the first DNA-based test commercially developed to detect heat-resistant molds at the molecular level.

Global In-Vitro Diagnostics Quality Control Market Report Scope

As per the scope of the report, in-vitro diagnostic quality controls are used to evaluate the performance of in-vitro diagnostic tests, such as in vitro nucleic acid testing procedures for pathogen detection, healthcare-associated infections (HAIs) like pneumonia, and urinary tract infections. These products majorly focus on the detection of defects, quality control, and validation panels, such as the Human Papillomavirus (HPV) Control Panel and Blood Culture (BCID) Control Panel, to support the implementation and monitoring of the performance of clinical and research laboratories, blood diagnostic centers, and IVD manufacturers.

The in-vitro diagnostics quality control market is segmented by products & services, application, end user, and geography. By products & services, the market is segmented into quality control products, data management solutions, and quality assurance services. By application, includes immunochemistry, clinical chemistry, hematology, molecular diagnostics, coagulation / hemostasis, microbiology & infectious disease, and point-of-care testing. By end user, the market is segmented into hospitals, independent clinical laboratories, IVD manufacturers & CROs, academic & research institutes, and ambulatory & physician office labs. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Quality Control Products |

| Data Management Solutions |

| Quality Assurance Services |

| Immunochemistry |

| Clinical Chemistry |

| Hematology |

| Molecular Diagnostics |

| Coagulation / Hemostasis |

| Microbiology & Infectious Disease |

| Point-Of-Care Testing |

| Hospitals |

| Independent Clinical Laboratories |

| IVD Manufacturers & CROs |

| Academic & Research Institutes |

| Ambulatory & Physician Office Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Products & Services | Quality Control Products | |

| Data Management Solutions | ||

| Quality Assurance Services | ||

| By Application | Immunochemistry | |

| Clinical Chemistry | ||

| Hematology | ||

| Molecular Diagnostics | ||

| Coagulation / Hemostasis | ||

| Microbiology & Infectious Disease | ||

| Point-Of-Care Testing | ||

| By End User | Hospitals | |

| Independent Clinical Laboratories | ||

| IVD Manufacturers & CROs | ||

| Academic & Research Institutes | ||

| Ambulatory & Physician Office Labs | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the in-vitro diagnostics quality control market in 2031?

The market is forecast to reach USD 1.85 billion by 2031.

Which application category is growing fastest within quality control?

Molecular diagnostics leads with a projected 6.87% CAGR through 2031.

Why are data management platforms gaining traction among laboratories?

Cloud middleware predicts control failures, cuts reportable errors by 22%, and reduces analyzer downtime, delivering measurable cost savings.

How concentrated is supplier power in this space?

The five largest vendors control 58% of 2025 revenue, reflecting moderate concentration.

What geographic region shows the highest growth rate?

Asia-Pacific advances at a 5.65% CAGR, propelled by China's ISO 15189 mandate and expanding private diagnostic networks.

How are reimbursement cuts affecting laboratory quality programs?

U.S. Medicare fee reductions prompt many labs to lower control run frequency, pressuring suppliers to offer

Page last updated on: