Market Overview

| Study Period | 2021 - 2031 |

|---|---|

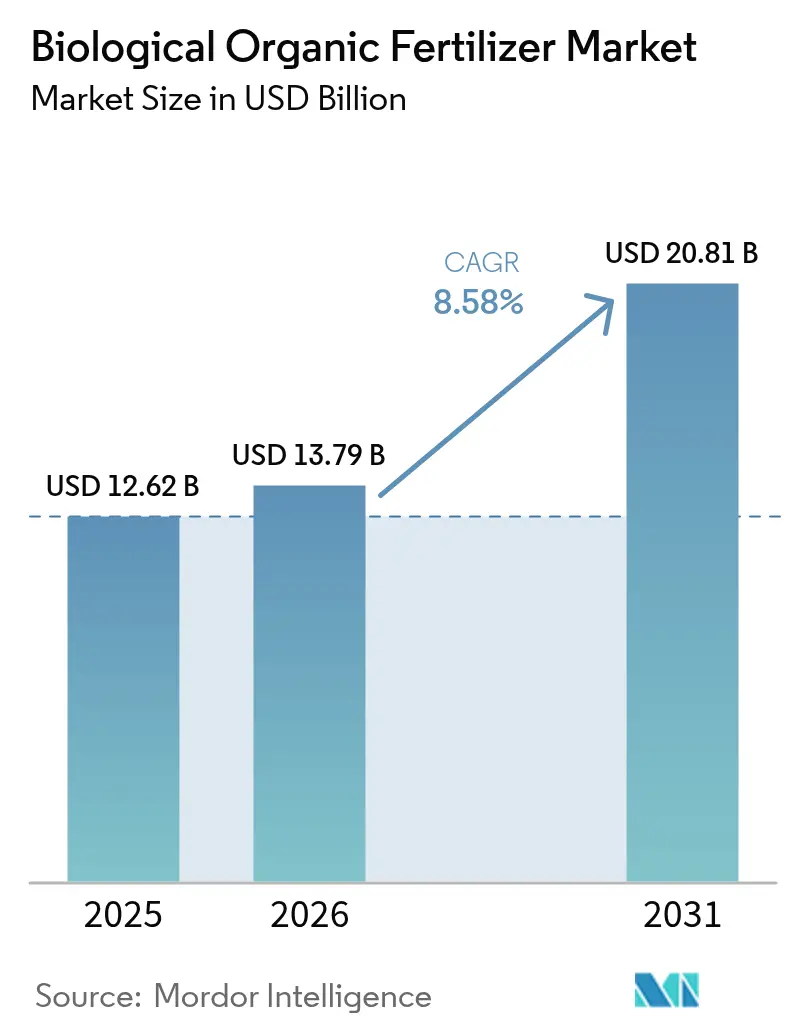

| Market Size (2026) | USD 13.79 Billion |

| Market Size (2031) | USD 20.81 Billion |

| Growth Rate (2026 - 2031) | 8.58% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Biological Organic Fertilizer Market Analysis by ���ϲ�����

The biological organic fertilizer market size is projected to grow from USD 12.62 billion in 2025 to USD 13.79 billion in 2026 and is forecast to reach USD 20.81 billion by 2031 at an 8.58% CAGR over 2026-2031. Policy-driven incentives, stricter regulations on synthetic nutrients, and cost-saving innovations at the farm level are driving the adoption of biological inputs. The United States Department of Agriculture reimburses certified biological input costs, reducing growers’ payback periods to under two years. This reimbursement program encourages farmers to transition to sustainable practices by offsetting initial investment costs. The European Union’s Farm to Fork Strategy requires a 20% reduction in synthetic fertilizer use by 2030, increasing demand for microbial alternatives. This policy aligns with broader sustainability goals and promotes environmentally friendly farming methods across the region. India’s National Mission on Natural Farming, launched in 2024, aims to bring 7.5 lakh hectares under biological inputs by 2027, boosting domestic cooperative sales. Concurrently, advancements in on-farm bioreactor platforms lower production costs, enabling localized manufacturing to become commercially viable, even for small-scale farmers. These platforms provide a cost-effective solution for producing biological inputs and support smallholders in adopting sustainable agricultural practices.

Key Report Takeaways

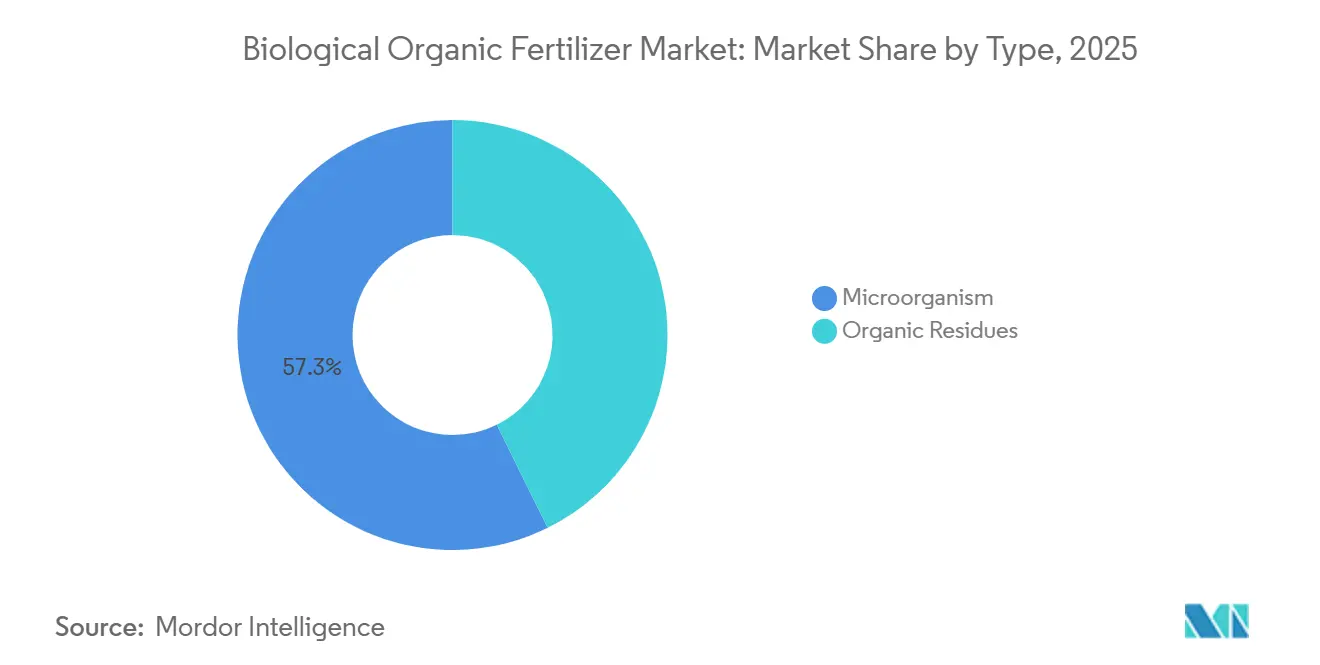

- By type, microorganism led with 57.3% of the biological organic fertilizer market share in 2025, while the same segment is projected to advance at a 10.5% CAGR through 2031.

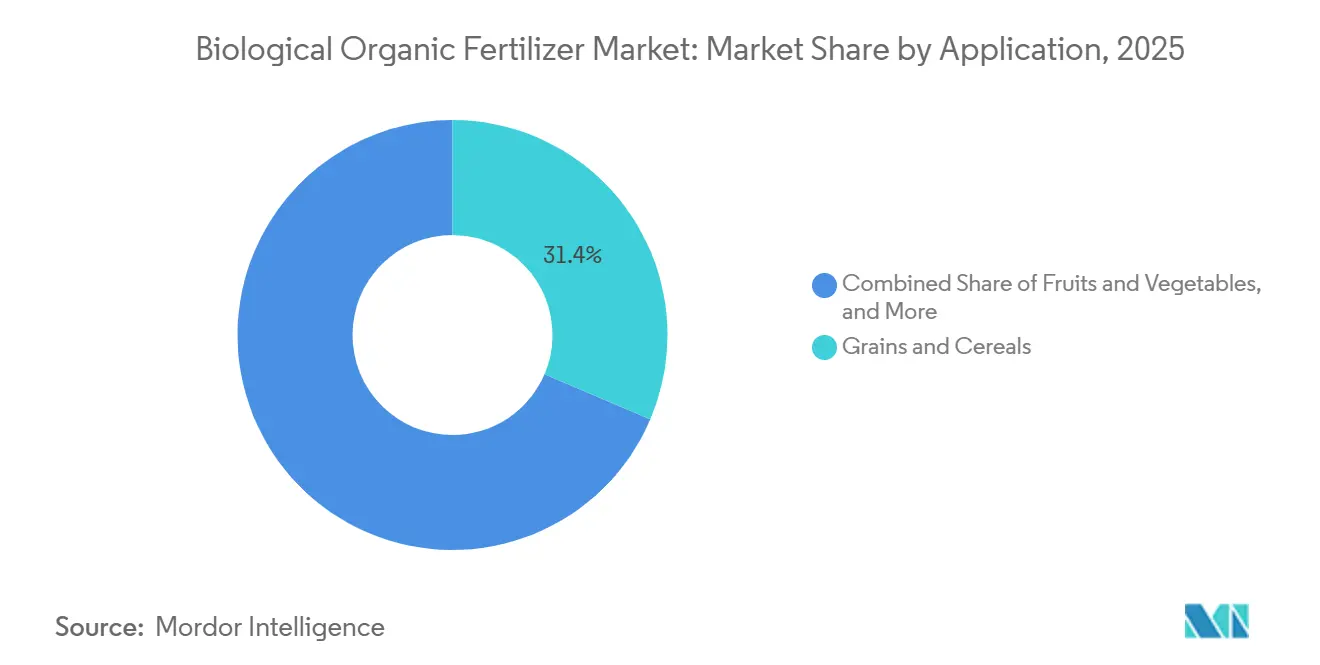

- By application, grains and cereals accounted for 31.4% of the biological organic fertilizer market size in 2025, and fruits and vegetables are forecast to expand at a 9.2% CAGR through 2031.

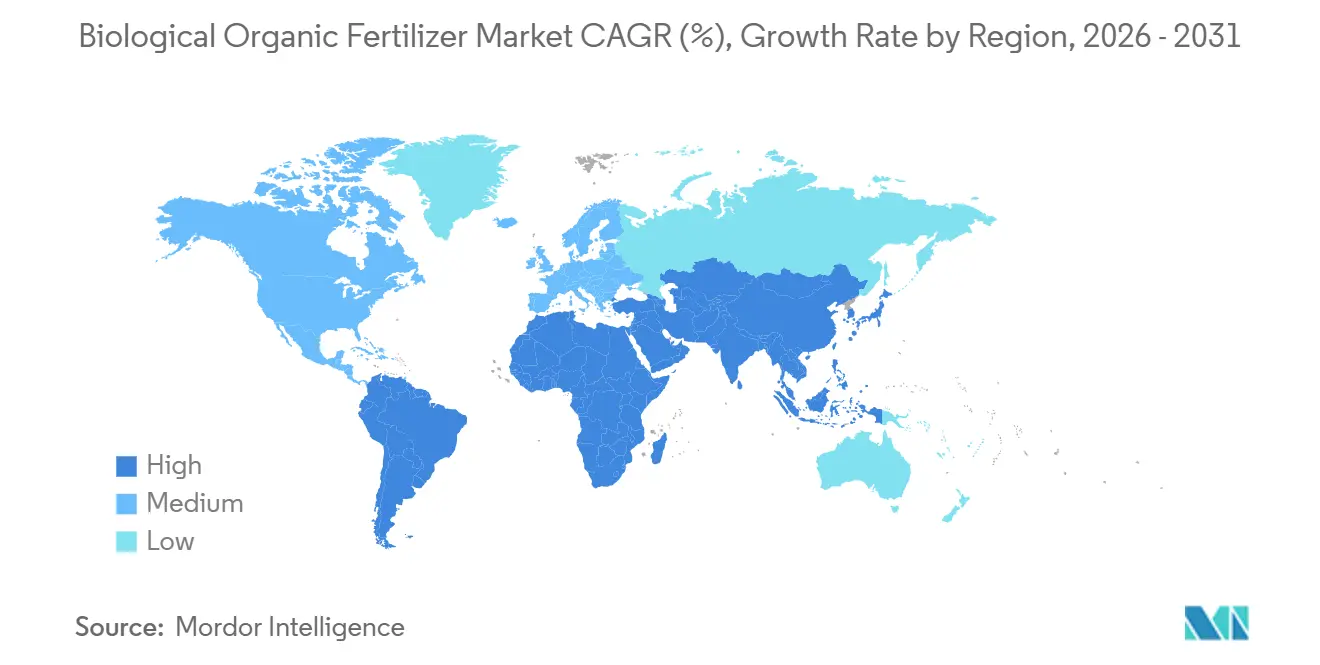

- By geography, Asia-Pacific accounted for 42.5% of the market size in 2025, whereas Africa is on track to post the fastest 8.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biological Organic Fertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal incentives for regenerative farming | +1.2% | North America, Europe, and India | Medium term (2-4 years) |

| Escalating restrictions on synthetic fertilizers | +1.0% | Global, led by Europe and India | Long term (≥ 4 years) |

| Rising demand from organic packaged-food processors | +0.8% | North America, Europe, and China | Short term (≤ 2 years) |

| Rapid adoption of microbial consortia blends | +0.9% | Global, centered in Asia-Pacific and North America | Medium term (2-4 years) |

| Farmer-led data cooperatives unlocking localized soil health insights | +0.7% | North America and Australia with spill-over to Brazil | Long term (≥ 4 years) |

| On-farm bioreactor platforms lowering production costs | +0.9% | North America, India, and Brazil | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Federal Incentives for Regenerative Farming

Across major farming regions, government programs refund a large share of biological input costs, tilting the economic calculus in favor of microbial products. In December 2025, the United States Department of Agriculture (USDA) launched a USD 700 million Regenerative Pilot Program to promote practices that enhance soil health, water quality, and biodiversity. The funding is allocated through the Natural Resources Conservation Service (NRCS), with USD 400 million provided via the Environmental Quality Incentives Program (EQIP) and USD 300 million through the Conservation Stewardship Program (CSP)[1]Source: Natural Resources Conservation Service, "Regenerative Pilot Program," nrcs.usda.gov. India encourages the use of biological fertilizers through subsidies provided under programs such as the Capital Investment Subsidy Scheme (CISS), which offers up to 100% assistance to government agencies and 25% assistance to private units for production. Farmers also benefit from financial support under the Paramparagat Krishi Vikas Yojana (PKVY) and receive incentives to reduce chemical fertilizer use through the PM-PRANAM initiative. Under the Common Agricultural Policy (CAP) 2023-2027, the European Union requires that at least 25% of the direct payments budget be dedicated to voluntary eco-schemes that support climate and environmentally sustainable practices[2]Source: European Commission, "Eco-schemes," agriculture.ec.europa.eu. Together, these incentives shorten payback periods, making biological products economically attractive even in row-crop systems.

Escalating Restrictions on Synthetic Fertilizers

Regulators worldwide are capping allowable nitrogen and phosphorus loads, creating a durable pull for the biological organic fertilizer market. The European Union is implementing restrictions on synthetic fertilizers to achieve a reduction in nutrient losses of at least 50% by 2030, as part of the "Farm to Fork" strategy. This initiative also aims to reduce overall fertilizer use by 20%. New regulations (EU 2019/1009) aim to enhance environmental standards, encourage the use of organic alternatives, and limit the use of microplastics, including polymer coatings on fertilizers, beginning in 2026[3]Source: European Commission, “Farm to Fork Strategy,” European Commission, ec.europa.eu. China enforces restrictions on chemical fertilizer use through stringent registration requirements, bans on high-toxicity products, and a national directive aimed at achieving zero growth in usage to address environmental concerns. Even fertilizer majors are repositioning. Yara International ASA increased the share of its research budget dedicated to microbes. While enforcement intensity varies by region, progressive restrictions are visible across developed and emerging markets, anchoring a structural shift toward biological inputs.

Rapid Adoption of Microbial Consortia Blends

Field research shows that multi-species inoculants outperform single-strain inoculants in both nutrient release and yield response. A 2024 Nature Microbiology study measured 35% higher nitrogen fixation from a five-species blend compared with individual strains and confirmed a 17% maize yield bump in large-plot trials. Krishak Bharati Cooperative Limited (KRIBHCO) and Novonesis Group launched ‘Kribhco Rhizosuper,’ a granular mycorrhizal biofertilizer featuring Novonesis Group's LCO Promoter Technology, in 2024. It improves nutrient and water uptake and root development in crops such as rice, wheat, and pulses, thereby enhancing yield and soil health. In 2023, Bionema Group Ltd. launched four biofertilizers containing living microbes designed to improve plant nutrition by mobilizing or increasing nutrient availability in soils and substrates. The United States Environmental Protection Agency fast-tracks dossiers containing naturally occurring organisms, cutting approval timeframes in half. Regulatory clarity and proven agronomic upside accelerate the shift to complex blends, reinforcing growth in the biological organic fertilizer market.

Farmer-Led Data Cooperatives Unlocking Localized Soil Health Insights

Grower collectives are pooling microbiome data to enhance application prescriptions, increasing effectiveness and minimizing trial-and-error expenses. Over recent years, the Soil Health Institute collaborated with a large number of farmers across the United States to develop a comprehensive soil database that significantly improved inoculant performance compared to standard off-the-shelf products. Digital agronomy platforms from companies such as Corteva Agriscience and Bioceres Crop Solutions Corp integrate this data, offering algorithm-driven blend recommendations that establish switching costs and promote repeat purchases. As the volume and depth of data continue to expand, prescription accuracy improves, enabling region-specific adoption and further broadening the demand base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short shelf-life in high-temperature climates | -1.2% | Sub-Saharan Africa, South Asia, and Middle East | Short term (≤ 2 years) |

| Fragmented, country-specific registration hurdles | -1.5% | Global, especially Europe and South America | Long term (≥ 4 years) |

| Low farmer awareness outside specialty crops | -0.8% | Africa, Southeast Asia, and Eastern Europe | Medium term (2-4 years) |

| Biocontamination risks during decentralized production | -0.6% | Global, higher incidence in India and Brazil | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Short Shelf Life in High-Temperature Climates

Microbial viability declines significantly when exposed to temperatures above 30 °C, limiting its use in tropical regions. The absence of adequate cold-chain infrastructure further intensifies this issue, as only a small proportion of rural distribution points in Africa are equipped with refrigeration facilities. This limitation results in a considerable percentage of product returns in countries with warmer climates, such as Nigeria and Kenya, during the hotter periods of the year. Although encapsulation provides some protection, it also significantly increases costs, creating financial challenges for smallholder farmers. Efforts to address this issue, such as the introduction of solar-powered village cold rooms in India, remain in the early stages, with the number of operational units still too limited to effectively reduce the risks associated with temperature sensitivity in these regions.

Low Farmer Awareness Outside Specialty Crops

Fruit and vegetable growers have readily recognized the certification advantages of biological inputs, whereas row-crop farmers remain hesitant. In regions of Southeast Asia and Eastern Europe, extension services allocate limited attention to microbial solutions, prioritizing the efficiency of synthetic inputs. This cautious approach stems from a lack of awareness and understanding of the potential benefits of biological inputs. Without extensive demonstration plots, proof-of-concept trials, and targeted educational initiatives, adoption outside premium market segments is projected to progress slowly. The limited availability of region-specific data and the absence of tailored recommendations further hinder the widespread adoption of biological inputs among row-crop farmers. Addressing these challenges through collaborative efforts between researchers, policymakers, and industry stakeholders could accelerate the integration of biological inputs into mainstream agricultural practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Microorganisms Dominate Through Precision Delivery

Microorganisms are the largest type, capturing 57.3% of the biological organic fertilizer market share in 2025 and are forecast to grow at a 10.5% CAGR through 2031, the highest among all categories. Rhizobium is anticipated to hold a significant share of the biological organic fertilizer market, as legume growers across regions such as North America and Asia increasingly adopt inoculants to reduce their reliance on synthetic nitrogen while maintaining crop productivity. Azospirillum is experiencing rapid growth, driven by its adoption in large-scale maize farming operations aiming to achieve similar reductions in nitrogen use. The use of phosphate-solubilizing bacteria and mycorrhizal fungi is also growing steadily, particularly in areas where phosphorus deficiency is prevalent or where the economic considerations of perennial crops make premium-priced solutions viable. This trend is especially notable in crops such as coffee, almonds, and avocados.

Organic residues accounted for the remaining share in 2025. Green manure leads this sub-segment but faces challenges in mechanized grain belts due to its labor-intensive nature. Fish and bone meals perform well in high-value vegetable systems, as their slow-release phosphorus complements tight irrigation schedules. Although region-specific subsidies support neem and castor oil cakes, scalability in export-oriented markets is limited by concerns over heavy-metal residues and inconsistent nutrient analysis. The adoption of organic residues is influenced by regional agricultural practices, availability of raw materials, and the cost-effectiveness of these inputs compared to synthetic alternatives. Efforts to improve nutrient consistency and address contamination concerns are critical for enhancing their adoption in global markets.

By Application: Fruits and Vegetables Surge on Organic Premiums

Grains and cereals are the largest application segment and accounting for 31.4% of the biological organic fertilizer market size in 2025, reflecting the enormous base acreage of maize, wheat, and rice. The adoption of biologicals is incremental, as they often supplement rather than replace synthetic products, resulting in a moderate growth trajectory. This gradual integration is influenced by factors such as cost considerations, compatibility with existing systems, and the need for proven efficacy. Pulses and oilseeds commonly utilize Rhizobium, a practice that has become standard due to its role in nitrogen fixation. This supports steady but modest growth, driven by consistent demand and established agricultural practices.

Fruits and vegetables, by contrast, advance at a 9.2% CAGR to 2031, the fastest among applications. Organic certification schemes and processor audits allow growers to pass through higher input costs, widening margins even after paying a premium for microbes. California lettuce acreage using microbial fertilizers nearly doubled between 2023 and 2025 as retail chains demanded residue-free produce. Turf and ornamentals have also benefited from municipal restrictions on synthetic nutrients near waterways. Florida's 2024 regulation led to a significant increase in sales of biological products to landscapers within a single season.

Geography Analysis

Asia-Pacific is the largest geography and commanded 42.5% of the biological organic fertilizer market share in 2025. India and China anchor growth via generous subsidy pools and mandatory nutrient-reduction directives. In India, the Indian Farmers Fertiliser Cooperative Limited (IFFCO) and Krishak Bharati Cooperative Limited (KRIBHCO) are prominent fertilizer cooperatives contributing to agricultural sustainability by supporting the domestic biological fertilizer market. They manufacture various eco-friendly products, including biofertilizers and compost, alongside their primary chemical fertilizer operations, securing local supply. China offers tax rebates to distributors that swap synthetic inventory for biologicals, accelerating channel penetration in Shandong and Henan provinces.

Africa records the fastest CAGR of 8.8% through 2031. Nigeria has allocated a significant budget for smallholder vouchers to support microbial products, with initial maize trials showing a notable increase in yields. In South Africa, collaborative funding for biological inputs in the Western Cape fruit-growing region has led to a significant reduction in synthetic nitrogen use. However, challenges such as gaps in cold-chain infrastructure and limitations in product shelf life continue to restrict the full potential of these initiatives. Despite these obstacles, donor-supported programs from organizations such as the United States Agency for International Development (USAID) and the Bill and Melinda Gates Foundation are steadily expanding the scope of pilot projects.

North America and Europe contributed significantly to the 2025 market revenue, with steady annual growth driven by reimbursement programs and strict nitrate regulations. In the United States, payments under the Conservation Stewardship Program led to a substantial annual increase in adoption among row-crop operators in the Midwest. Canada’s Agricultural Clean Technology Program provided substantial funding to support the co-financing of on-farm bioreactors, resulting in a significant reduction in production costs. In Europe, countries such as Germany, France, and the Netherlands showed the fastest adoption rates due to stringent nitrogen limits, while Spain and Italy experienced slower adoption but still recorded notable growth in biological sales, supported by exports of citrus and olives.

Competitive Landscape

The biological organic fertilizer market remains moderate, with the top five firms dominating, leaving room for regional specialists. Novonesis Group, established through the merger of Novozymes and Chr. Hansen in 2024 holds the world's largest microbial strain library, comprising over 50,000 isolates. The company leverages this extensive library to develop innovative solutions across industries such as agriculture, food, and health. Bioceres Crop Solutions Corp and Corteva Agriscience incorporate biologicals into digital agronomy tools that utilize soil sensors and machine learning, enabling farmers to optimize crop yields and resource use. Indian cooperatives cater to the South Asian market on a large scale but have limited international presence, focusing primarily on meeting regional agricultural demands and supporting local farmers.

Strategic activities are centered on vertical integration, geographic expansion, and the formation of partnerships with processors. There are significant opportunities in row crops outside regions such as North America and Europe, where the adoption of biological inputs remains limited compared to traditional fertilizers. Furthermore, the turf and ornamentals segment presents growth potential, driven by municipal environmental regulations that are fostering demand. However, the distribution networks in this segment are still in the early stages of development.

Regulatory preparedness is the emerging moat. ISO 17033 will require sterile handling and traceability, compliance hurdles that smaller plants may struggle to clear. Companies with established quality management systems, such as Novonesis Group and Lallemand, Inc., are better equipped to meet these requirements with minimal additional costs. In contrast, smaller producers may face challenges securing the capital investments needed for compliance. Data cooperatives are an emerging competitive factor with significant potential. For instance, growers who share soil microbiome data with platforms managed by Corteva Agriscience or the Soil Health Institute receive tailored microbial prescriptions that deliver superior results compared to generic formulations. This creates network effects that may consolidate market power among a limited number of platform operators.

Biological Organic Fertilizer Industry Leaders

-

Bioceres Crop Solutions Corp

-

Lallemand, Inc.

-

UPL Limited

-

Premier Tech Ltd. (Gestion Bernard Belanger Ltee)

-

Novonesis Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Alltech, Inc. has commenced construction on a USD 4.6 million project, a 15,000-square-foot biofertilizer production facility at its headquarters in Nicholasville, Kentucky. Supported by a USD 2.34 million grant, the facility is projected to produce over 66,000 gallons of biological fertilizers per month. The initiative aims to improve soil health, enhance crop resilience, and decrease dependence on synthetic and imported fertilizers.

- March 2025: XtalPi and Kula Bio have entered into a partnership to develop AI-driven microbial fertilizers to address desertification and soil degradation challenges in China and the Middle East. This collaboration integrates XtalPi’s AI and robotics platform with Kula Bio’s sustainable microbe technology to optimize fertilizers for arid regions and increase the availability of arable land.

- January 2025: Super Crop Safe Ltd. (SUCROSA Group), an Indian agrochemical and biotechnology company, has introduced its product, Super Gold WP+. This solution integrates inoculant mycorrhiza with essential nutrients to enhance farming practices.

Global Biological Organic Fertilizer Market Report Scope

Biological organic fertilizers are a type of fertilizer that integrates the benefits of microbial and organic components. These fertilizers are primarily derived from animal and plant residues, combined with inert organic and decomposing materials. The Biological Organic Fertilizer Market Report is Segmented by Type (Microorganism and Organic Residues), by Application (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, Commercial Crops, and Turf and Ornamentals), and by Geography (North America, Europe, Asia-Pacific, South America, the Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Type

| Microorganism | Rhizobium |

| Azotobacter | |

| Azospirillum | |

| Blue-green Algae | |

| Phosphate-Solubilizing Bacteria | |

| Mycorrhiza | |

| Other Microorganisms | |

| Organic Residues | Green Manure |

| Fish Meal | |

| Bone Meal | |

| Oil Cakes | |

| Others |

By Application

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Commercial Crops |

| Turf and Ornamentals |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Type | Microorganism | Rhizobium |

| Azotobacter | ||

| Azospirillum | ||

| Blue-green Algae | ||

| Phosphate-Solubilizing Bacteria | ||

| Mycorrhiza | ||

| Other Microorganisms | ||

| Organic Residues | Green Manure | |

| Fish Meal | ||

| Bone Meal | ||

| Oil Cakes | ||

| Others | ||

| By Application | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Commercial Crops | ||

| Turf and Ornamentals | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the biological organic fertilizer market be by 2031?

It is forecast to reach USD 20.81 billion by 2031, expanding at an 8.58% CAGR from 2026-2031.

Which product type leads revenue?

Microorganism-based formulations held 57.3% of 2025 revenue, making them the largest segment.

What is the fastest-growing crop application?

Fruits and vegetables are projected to grow at a 9.2% CAGR through 2031, the quickest among all applications.

Which region will grow the quickest?

Africa shows the highest regional CAGR at 8.8% over 2026-2031, although from a smaller base.

How will ISO 17033 affect suppliers?

The new standard mandates sterile handling and traceability, favoring firms that already run pharmaceutical-grade quality systems.

Page last updated on: