Automotive Films Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

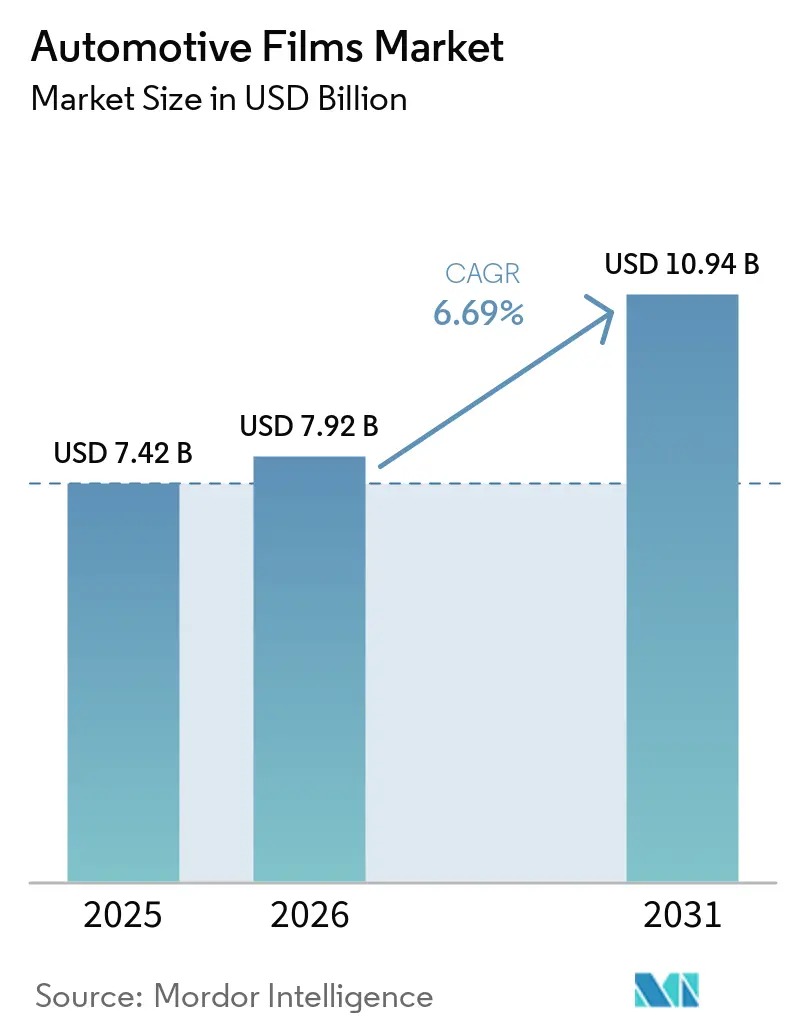

| Market Size (2026) | USD 7.92 Billion |

| Market Size (2031) | USD 10.94 Billion |

| Growth Rate (2026 - 2031) | 6.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Automotive Films Market Analysis by ���ϲ�����

The Automotive Films Market size is expected to grow from USD 7.42 billion in 2025 to USD 7.92 billion in 2026 and is forecast to reach USD 10.94 billion by 2031 at a 6.69% CAGR over 2026-2031. Thermal-management regulations, rising aesthetic expectations, and rapid material innovation are reshaping buying behavior across price tiers, while nano-ceramic formulations and electrochromic glazing allow compliance with divergent visible-light-transmission rules without sacrificing style or in-cabin comfort. Paint protection films (PPF) now sit at the intersection of asset-preservation economics and premium-vehicle customization, commanding gross margins eight to ten percentage points above the industry average as buyers treat self-healing TPU layers as a factory-equivalent safeguard. Top-tier suppliers further defend share through vertically integrated adhesive chemistries, ten-year warranties, and channel investments that independent converters rarely match. In Asia-Pacific, regulatory latitude that permits darker tints and higher infrared rejection than European or North American codes fuels accelerated adoption, while electrification raises the value of films that reduce battery-cooling loads on hot days.

Key Report Takeaways

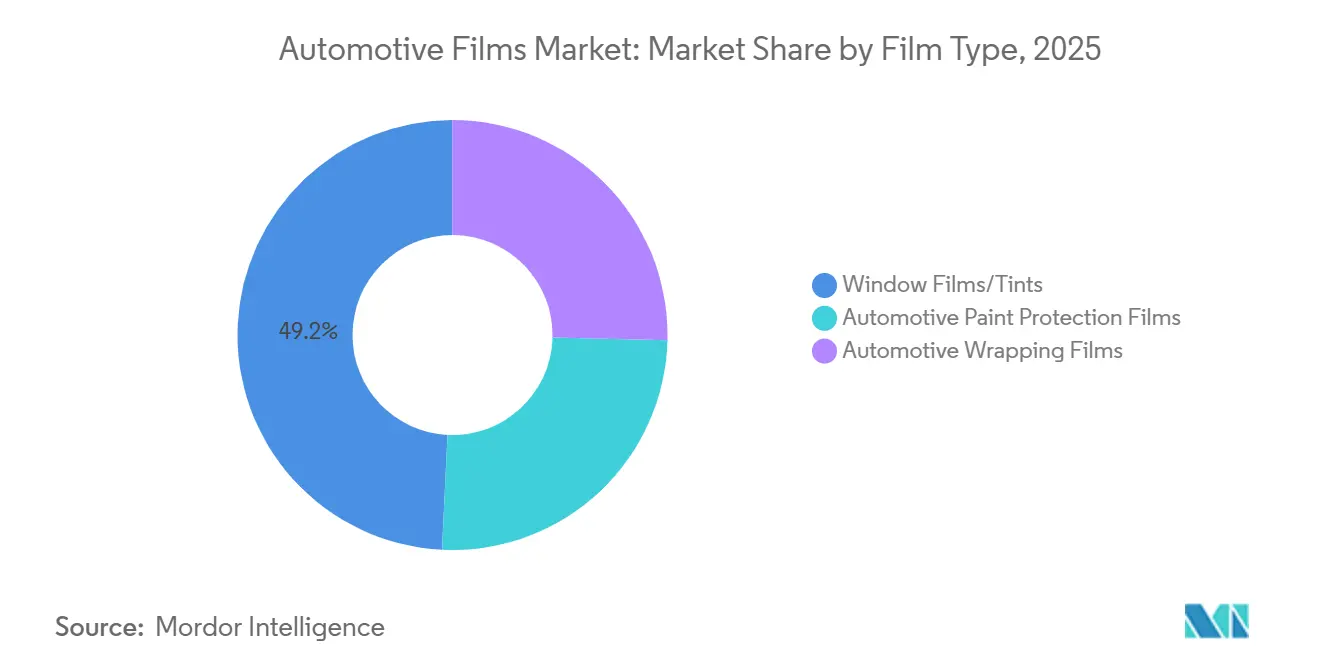

- By film type, window films and tints held 49.22% of the automotive films market share in 2025. Paint protection films are forecast to grow at a 7.12% CAGR through 2031, the fastest among all film categories.

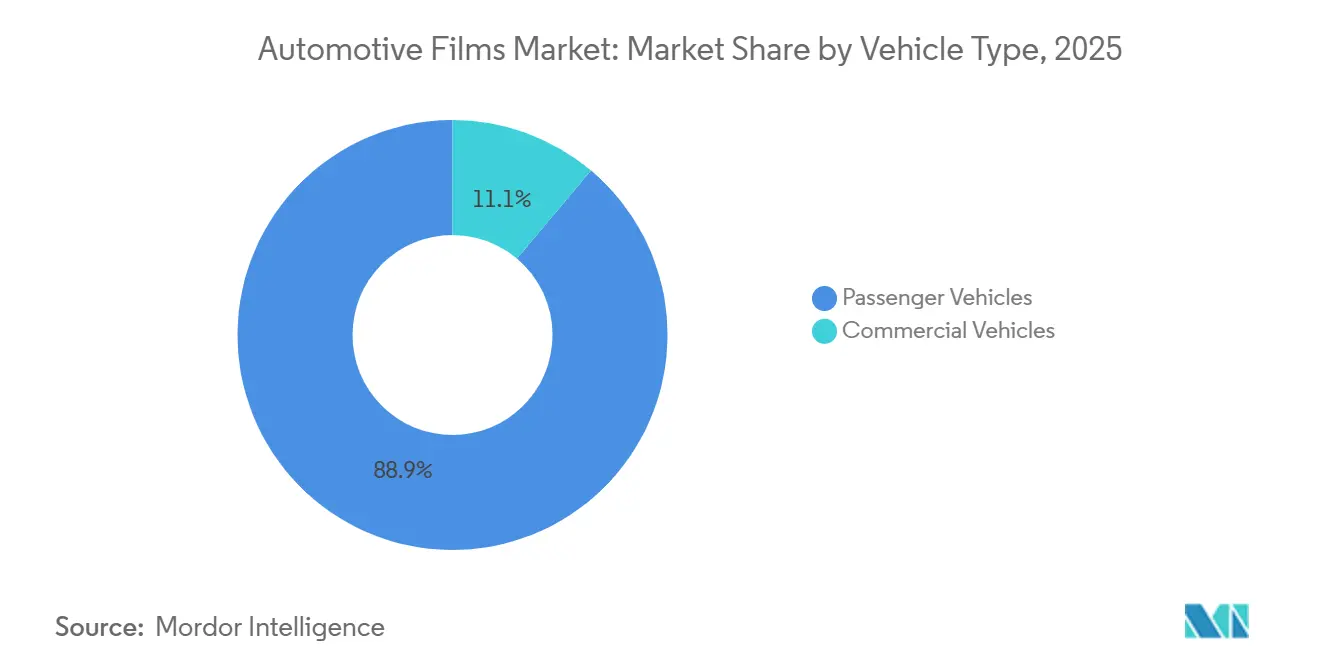

- By vehicle type, passenger cars accounted for 88.86% of the automotive films market size in 2025 and are projected to advance at a 6.98% CAGR from 2026 to 2031.

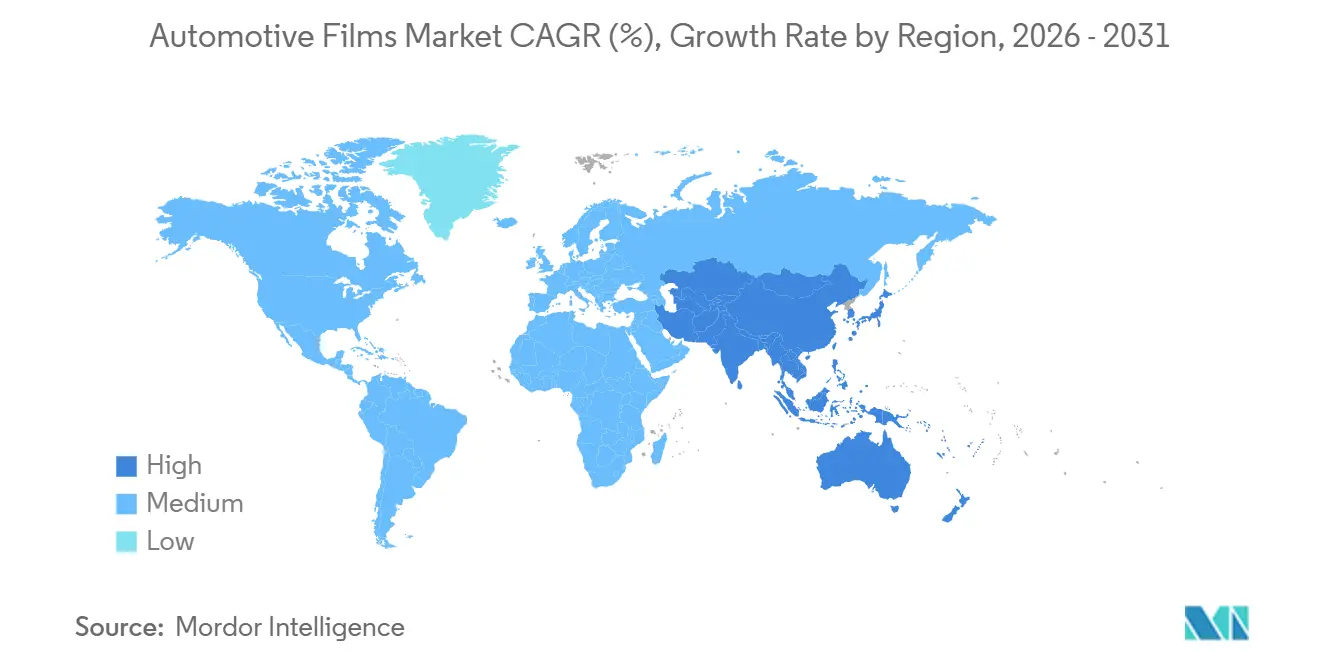

- By geography, Asia-Pacific commanded 44.43% of 2025 revenue and is poised for a 7.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Films Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for vehicle aesthetics and surface protection | +1.8% | Global, concentrated in North America and APAC | Medium term (2-4 years) |

| Stringent heat-reduction and UV regulations | +1.5% | North America and EU, emerging in Middle East | Short term (≤ 2 years) |

| Rapid vehicle-parc growth across Asia-Pacific | +2.1% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Shift from repainting to color-change wraps | +1.0% | North America and Europe, nascent in APAC | Medium term (2-4 years) |

| Commercialization of smart electrochromic window films | +0.8% | Global, led by premium segments in EU and China | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Rising Demand for Vehicle Aesthetics and Surface Protection

Owners of premium vehicles are increasingly viewing Paint Protection Film (PPF) as a safeguard against stone chips and swirl marks. They're willing to invest in full-body installations, recognizing the potential boost in resale value. In 2023, a major acquisition established an immediate distribution network spanning 200 installer hubs, propelling presence in a market where cosmetic preservation heavily influences purchasing decisions. In response, a self-healing film with a lifespan of 8 to 10 years was launched. Priced competitively, it undercuts the warranty premiums of established players, intensifying the competitive landscape in Europe. While warranty compression poses challenges for smaller converters without proprietary top coats, consumers are reaping the rewards with a wider selection and reduced price variability. As a result, the automotive films market is evolving into a barbell structure: luxury-grade and entry-grade solutions are flourishing, while mid-tier metallized variants are fading into obscurity.

Stringent Heat-Reduction and UV Regulations

The NHTSA's FMVSS 205 mandates a minimum visible light transmission (VLT) for front windshields in the U.S. This drives up the demand for nano-ceramic films, which can reject infrared radiation without darkening the glass[1]National Highway Traffic Safety Administration, “FMVSS 205 Glazing Materials,” nhtsa.gov. In Europe, enforcement of these standards is inconsistent. For instance, while Germany places a premium on infrared performance, Scandinavian countries focus on stringent VLT checks[2]European Window Film Association, “VLT Enforcement Across EU Member States,” ewfa.com. This inconsistency has led suppliers to produce jurisdiction-specific stock-keeping units (SKUs). A specific product avoids radio-frequency interference by not using metals, yet it achieves commendable rejection of total solar energy. Such market fragmentation benefits vertically integrated producers who possess both formulation flexibility and certification programs, ensuring their installers remain updated. Meanwhile, the Middle East has started tightening regulations, particularly on UV thresholds. This move indicates a burgeoning demand, especially as cities, grappling with extreme heat, aim to alleviate stress on rideshare fleets operating for extended hours.

Rapid Vehicle-Parc Growth Across Asia-Pacific

In 2024, China's vehicle count surpassed a significant milestone and is on track to grow further by decade's end. Meanwhile, India expanded its vehicle base, increasing the potential for tint and PPF applications. With new-energy vehicles gaining traction, China's demand surges, especially as cabin heat reduction can boost range on sweltering days, setting a competitive edge in EV pricing. While organized aftermarket penetration in India lingers at a low level, 3M has established numerous Car Care Studios in major cities, bolstering installer skills and boosting consumer trust. Garware's recent venture into graphene coatings caters to Indian consumers prioritizing paint-depth retention. As the Asia-Pacific region claims a substantial share of the automotive films market, economies of scale are driving down per-square-foot costs, solidifying the area's reputation for cost-effective manufacturing.

Shift From Repainting to Color-Change Wraps

Vinyl wraps have slashed downtime from weeks to mere days, all while preserving original finishes. This efficiency has led both fleets and private owners to pivot away from traditional repainting. In 2025, Avery Dennison expanded its offerings by introducing 13 new matte and chrome finishes, bringing its total palette to 83 variants. This move has invigorated custom builds, especially for influencer marketing campaigns. Certification data reveals a significant leap in installer proficiency scores after training, underscoring labor as the primary challenge for scaling. Fleet graphics in North America yield competitive rates compared to billboard CPMs in urban corridors. As a result, logistics providers can refresh seasonal branding biannually without any asset downtime. Electric vans stand to gain even more; by opting for wraps instead of repainting at de-fleet time, they safeguard their remarketing value. Collectively, these trends indicate that color-change wraps are carving out a growing niche. Rather than overshadowing window tints and PPF, they are coexisting, thereby expanding the entire automotive films market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Visible-light-transmission (VLT) regulatory limits | -0.9% | North America and EU, selective enforcement in APAC | Short term (≤ 2 years) |

| Volatile PET and TPU raw-material prices | -1.2% | Global, acute in regions lacking feedstock scale | Medium term (2-4 years) |

| Factory-fitted tinted glass reducing aftermarket demand | -0.7% | North America and EU, gradual adoption in APAC | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Visible-Light-Transmission Regulatory Limits

Installers face a complex landscape due to FMVSS 205's VLT rule and varying state regulations, risking fines and limiting the darker shades favored by many consumers. Europe faces similar hurdles; Scandinavian police actively use photometers in roadside checks to combat non-compliant films. While ceramic nano-particle films, blocking infrared radiation and transmitting visible light, offer a compliant solution, their higher cost compared to dyed alternatives stifles widespread adoption. Additionally, metallized products grapple with signal interference, diminishing their appeal in areas where e-toll and GPS reliability is paramount. As a result, while emerging regions ease regulations, mature markets see their revenue potential capped.

Volatile PET and TPU Raw-Material Prices

In 2024, spot PET prices fluctuated before rebounding in Q1 2025, aligning with steadier crude benchmarks. Meanwhile, TPU prices remained elevated, constrained by limited isocyanate capacity. Eastman’s Advanced Materials segment faced destocking pressures in early 2024, leading to margin hits, highlighting its vulnerability to feedstock price swings. While major suppliers mitigate risks through multi-year contracts or by utilizing internal resin plants, independent suppliers tend to pass these costs downstream. This practice not only inflates prices for end-users but also reduces volume elasticity. In Brazil and Turkey, currency volatility exacerbates challenges; here, dollar-denominated inputs lead to pronounced local price shocks. As a result of this sustained turbulence in raw materials, the automotive films market has seen its CAGR forecast reduced.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Film Type: Nano-Ceramic Formulations Redefine Premium Tiers

In 2025, window films and tints dominated the automotive films market, claiming a 49.22% share. Paint protection films, however, are set to outpace all categories with a projected 7.12% CAGR through 2031. This surge is driven by the innovative self-healing TPU technology, which adeptly removes micro-scratches during engine heat cycles. Ceramic window tints, while holding a significant stake in premium sales, command prices per square foot that are significantly higher than their dyed counterparts. This pricing dynamic skews revenue heavily towards these high-spec formulations. Dyed films face a dual challenge: they are overshadowed by the rise of privacy glass and their limited heat rejection capabilities. On the other hand, metallized layers are losing ground due to RF interference issues, which conflict with the growing reliance on 5G and GPS. Hybrid crystalline films, though they offer a balance of cost and performance, struggle to penetrate the market significantly. This limitation is attributed to the steeper learning curve for installers, which extends job times compared to single-layer products.

Paint protection films boast dealer ticket sizes that vary depending on coverage. These figures, coupled with their contribution margins, make them prime targets for industry giants. Carbon-infused tints strike a balance, offering moderate IR blockage at a premium over dyed films, all while sidestepping conductivity issues. Automotive wrapping films tap into the economics of brand visibility. With each delivery van racking up thousands of daily impressions, fleet roll-outs can soar to hundreds of units per operator, especially once procurement teams greenlight design templates. As nano-ceramic films gain traction, suppliers are bolstering their warranties to a decade or a specified mileage, a testament to their faith in the product's fade resistance and adhesive durability across varied climates.

By Vehicle Type: Passenger Dominance Masks Commercial Opportunity

In 2025, passenger cars dominated the revenue landscape, accounting for an 88.86% share. This dominance underscores a robust market for tint replacements and aesthetic upgrades. Projections indicate that by 2031, the market for automotive films in passenger vehicles will grow at a 6.98% CAGR. This growth is largely attributed to the rising middle-class consumers in India and Indonesia gravitating towards premium heat-rejection tiers. While commercial vehicles represent a modest portion of the market value, they paradoxically utilize two to three times more square footage per unit. Fleet wraps offer enticing returns, achieving paybacks in under 12 months when juxtaposed with billboard CPM equivalents. This financial allure is driving courier and grocery chains to adopt comprehensive van coverage strategies. The case for electric delivery vans becomes even more compelling: with ceramic tints reducing HVAC demands, these vans can enjoy an extended driving range during urban operations.

Luxury trim lines now seamlessly integrate dealer-installed PPF packages, with OEMs imposing a hefty markup on materials, all in a bid to safeguard residual values. Dealership channels contribute significantly to revenue and boast the highest gross profit per kit, thanks to the advantages of captive labor and the strategic cross-selling of ceramic coatings. The aftermarket landscape is notably fragmented: around 50,000 independent tint shops globally manage a majority of installations outside dealerships. Yet, a mere fraction of these shops possess the specialized expertise in ceramic or PPF, limiting the premium market's growth. While commercial fleets traditionally prioritize upfront costs in their procurement strategies, pilot initiatives with industry giants hint at a paradigm shift. As these corporations integrate range-extension metrics into their total-cost-of-ownership evaluations, driven by corporate ESG objectives, the market dynamics could be poised for a significant transformation.

Geography Analysis

Asia-Pacific anchors 44.43% of 2025 revenue and is forecast to post a 7.02% CAGR to 2031. This growth is driven by China, India, and Southeast Asia expanding vehicle ownership into rural areas. In 2024, China's sales of NEVs (New Energy Vehicles) are spurring a heightened demand for thermal management. This is because films that can reduce cabin temperatures potentially extend the vehicle's range on a 600-km battery pack. Currently, India's organized detailing market taps into a small fraction of its potential clientele. However, Garware's upcoming launch in February 2026, featuring graphene-ceramic multi-layer kits, aims to bridge this gap. These kits seamlessly integrate PPF, coatings, and windshield films into a singular service. Meanwhile, Japan and South Korea are honing in on OEM channels. For instance, LINTEC's integration of windshield films into factory glazing packages has bolstered its turnover, highlighting a significant shift of value towards assembly plants.

North America, contributing a substantial share to global revenue, boasts the highest per-vehicle expenditure on aftermarket PPF and ceramic tints. However, growth is tapering to a moderate pace. This slowdown is attributed to privacy glass diminishing the demand for dyed films and state VLT regulations limiting shade options. Seasonal dynamics play a role in Canada, where winter road salt boosts PPF demand on rocker panels. Concurrently, in Mexico, OEM hubs in Guanajuato are delving into factory-applied tints to align with U.S. export standards. 3M's Transportation and Electronics segment faced a dip in 2024. Yet, when excluding the impacts of PFAS exits, the segment showcases commendable organic growth, emphasizing a strategic shift towards non-fluorinated chemistries amidst tightening environmental regulations.

Europe, while contributing a notable share to the market, reveals pronounced regional disparities. Germany allows darker shades on rear windows but limits metallized layers to safeguard toll-collection sensors. In contrast, the UK mandates a specific VLT on windscreens, effectively sidelining most aftermarket tints. Eastman's 2026 investment in Ghent aims to embed film substrates during windshield lamination, serving as a buffer against potential aftermarket declines. Collectively, Brazil, Saudi Arabia, and South Africa account for a small but significant portion of global revenue. In Saudi cities like Riyadh and Jeddah, extreme heat drives demand for IR-blocking films. However, lenient inspection practices permit darker shades than those in Europe, presenting an opportunity for higher-margin nano-ceramic imports.

Competitive Landscape

The automotive films market is moderately consolidated. Three strategic levers define the emerging white space clusters: 1) OEM supply of electrochromics, 2) fleet-scale wrap initiatives for electric delivery networks, and 3) global training platforms that condense the typical 12-month skill acquisition period into just 90 days. LG Chem's partnership with Webasto highlights the OEM strategy, while Amazon's trial of reflective-silver vinyl on Rivian vans underscores the fleet's enthusiasm for wrap-centric brand updates. Central to this evolution is installer training; IWFA's membership data reveals a mere certified technicians worldwide, leaving a staggering unaccredited shops unable to fulfill ceramic or PPF warranty standards.

Automotive Films Industry Leaders

Eastman Chemical Company

3M

Saint-Gobain

Avery Dennison Corporation

Garware Suncontrol Film

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Dai Nippon Printing Co., Ltd. launched mass production of decorative film for automotive displays, combining premium design with high-visibility imaging. The decorative film integrated high-quality design elements, such as woodgrain patterns, with advanced optical performance, enabling clear display of images and icons only when needed.

- February 2025: Garware Suncontrol Film launched ceramic and graphene coating, a car-care kit, three new window-film categories, and WindShield Pro glass-protection sheets, broadening its portfolio beyond PPF and sun-control layers.

Global Automotive Films Market Report Scope

The automotive film is a thin laminate that is used on the inside and outside of a car. It gives the driver and passengers more security and privacy. Automotive can be made up of different materials, including polycarbonate, polyester, polystyrene, polyvinyl chloride, and others. These films improve the overall appearance of the vehicle and can also be used to block solar ultraviolet radiation and provide comfort by reducing glare from the sun.

The automotive films market is segmented by film type, vehicle type, and geography. By film type, the market is segmented into window films and tints, automotive paint protection films, and automotive wrapping films. By vehicle type, the market is segmented into passenger vehicles and commercial vehicles. By geography, the market is segmented into various regions. The report also covers the market size and forecasts for the automotive film market in 15 countries across major regions. For each segment, the market sizing and forecast have been done on the basis of revenue (USD).

| Window Films/Tints | Dyed Window Tint |

| Metallized Window Tint | |

| Ceramic Window Tint | |

| Carbon Window Tint | |

| Other Window Films/ Tints (Hybrid, Crystalline, etc.) | |

| Automotive Paint Protection Films | |

| Automotive Wrapping Films |

| Passenger Vehicles |

| Commercial Vehicles |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Film Type | Window Films/Tints | Dyed Window Tint |

| Metallized Window Tint | ||

| Ceramic Window Tint | ||

| Carbon Window Tint | ||

| Other Window Films/ Tints (Hybrid, Crystalline, etc.) | ||

| Automotive Paint Protection Films | ||

| Automotive Wrapping Films | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR is projected for the automotive films market between 2026 and 2031?

The sector is forecast to grow at 6.69% annually from USD 7.92 billion in 2026 to USD 10.94 billion.

Which film type is expected to see the fastest growth by 2031?

Paint protection films are projected to expand at a 7.12% CAGR through 2031.

Which region leads global revenue today?

Asia-Pacific accounts for 44.43% of 2025 revenue and remains the growth engine.

How large is the passenger-vehicle slice of spending?

Passenger cars represented 88.86% of the global value in 2025 and a 6.98% growth path.

Why are nano-ceramic films gaining share?

They deliver up to 97% infrared rejection while remaining legal under strict VLT rules and do not block RF signals.

Page last updated on: