Automotive Clutch Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 15.39 Billion |

| Market Size (2031) | USD 20.51 Billion |

| Growth Rate (2026 - 2031) | 5.91% CAGR |

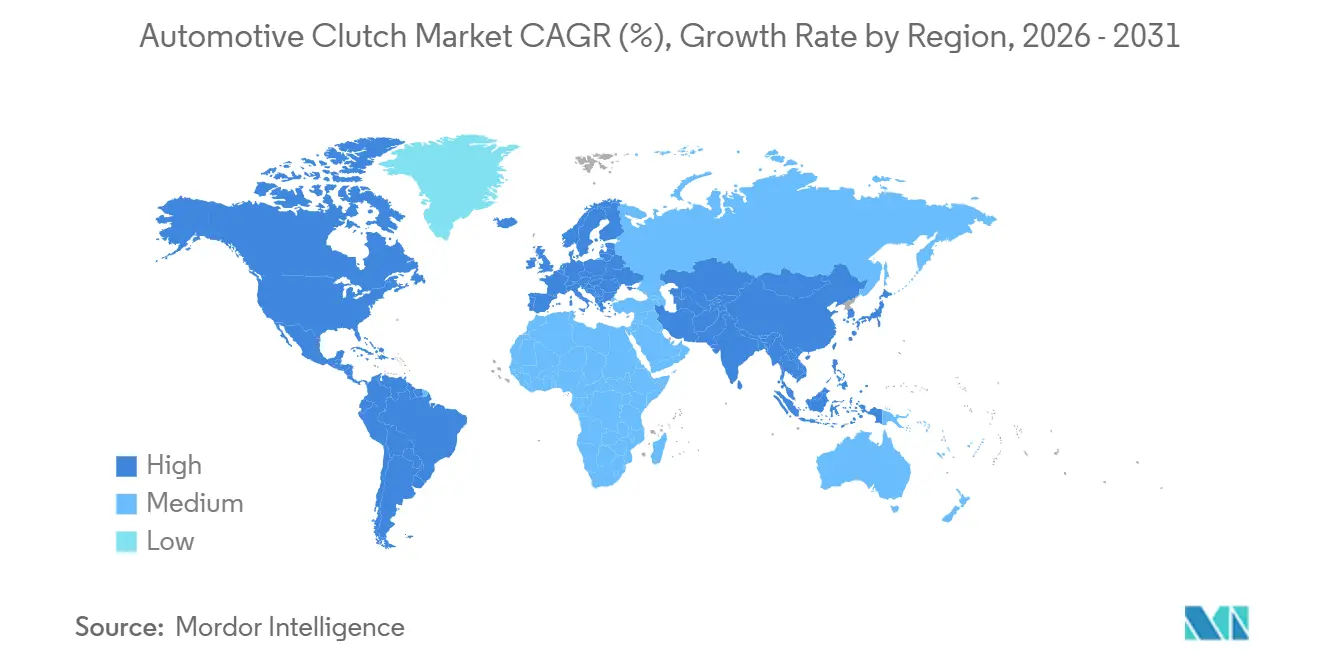

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

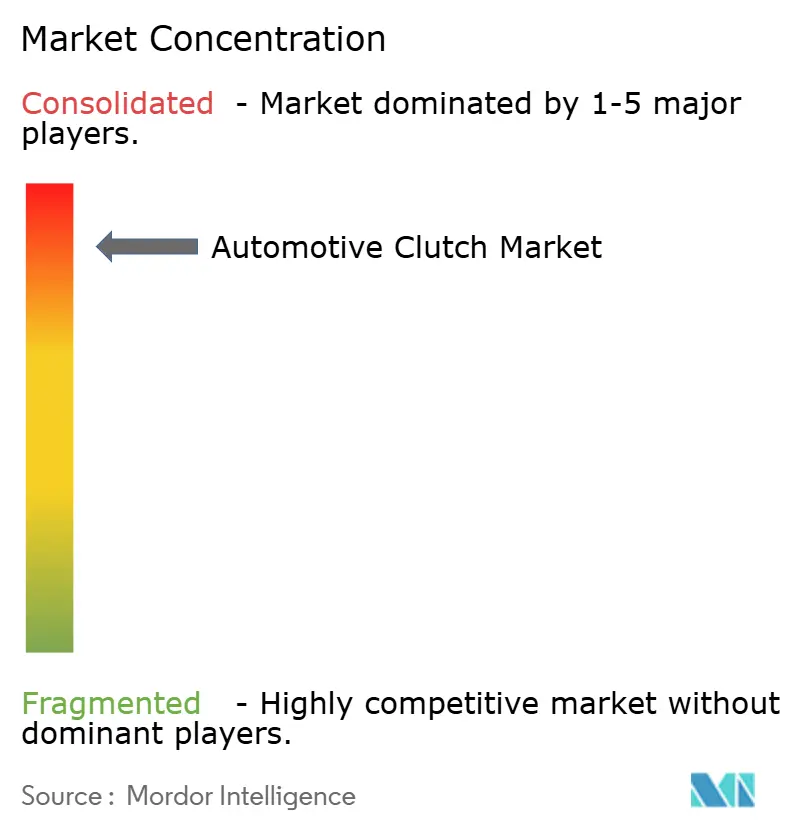

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Automotive Clutch Market Analysis by ���ϲ�����

The automotive clutch market size is valued at USD 15.39 billion in 2026 and is projected to post USD 20.51 billion by 2031, translating into a 5.91% CAGR over the forecast period (2026-2031). Demand remains anchored in cost-sensitive regions that still favor manual transmissions. Yet, dual-clutch and electro-hydraulic systems are gaining ground as automakers target lower CO₂ emissions, reduced shift times, and smoother operation in mild-hybrid vehicles.

Key Report Takeaways

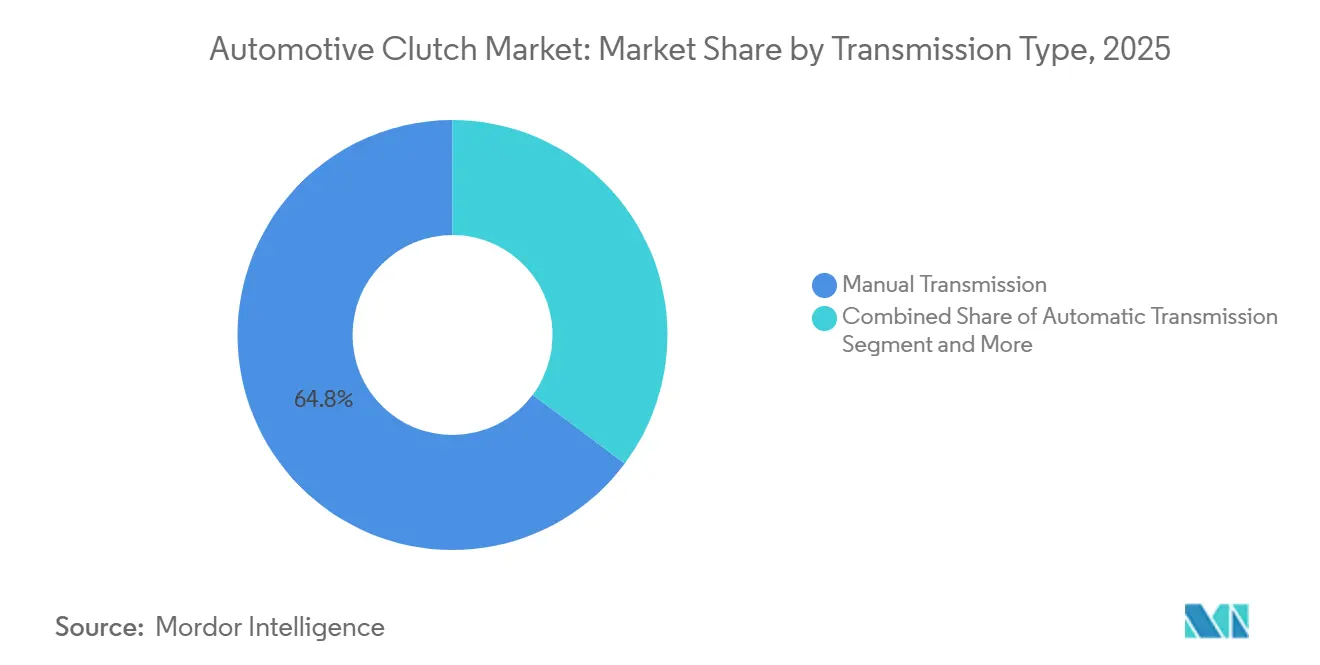

- By transmission type, manual gearboxes captured 64.79% of the automotive clutch market share in 2025, whereas wet dual-clutch systems are forecast to advance at a 9.37% CAGR to 2031.

- By vehicle type, passenger cars led with 74.23% of the automotive clutch market share in 2025, while medium and heavy commercial vehicles are projected to register the fastest growth, at 8.02% CAGR, through 2031.

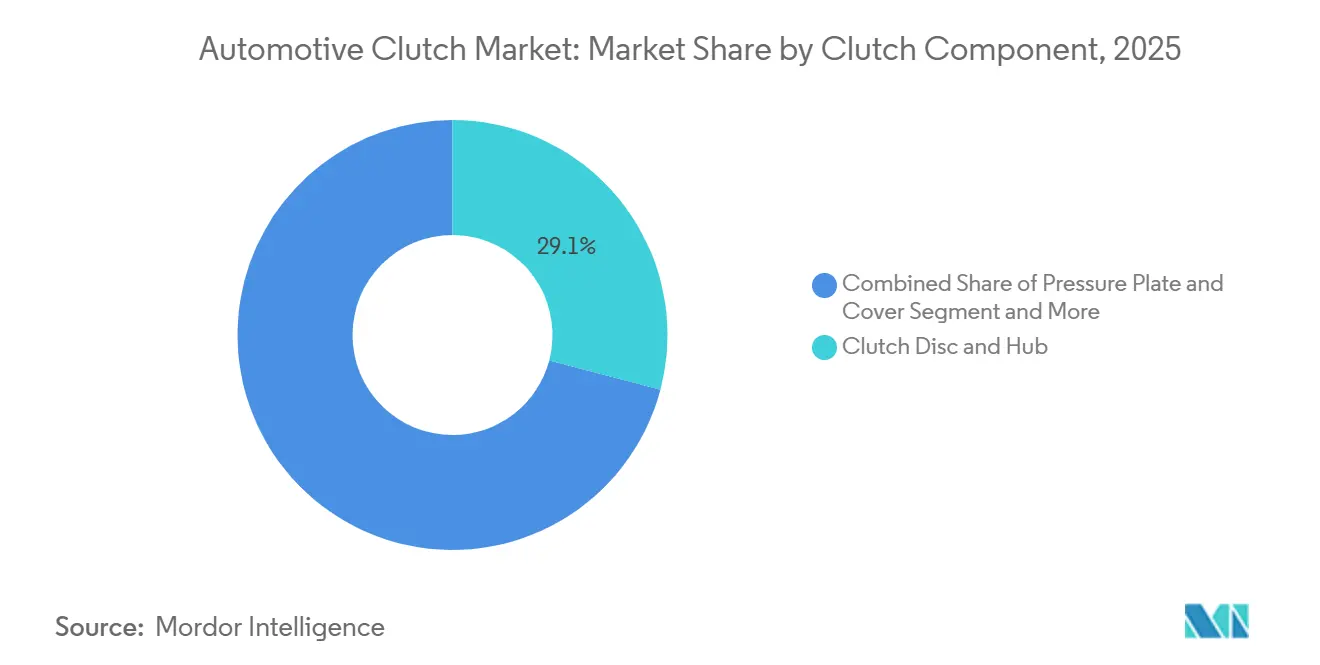

- By component, clutch disc and hub assemblies accounted for 29.08% of the automotive clutch market share in 2025; actuation systems are projected to show the strongest growth rate of 8.41% across the forecast.

- By sales channel, OEM supply accounted for 82.45% of the automotive clutch market share in 2025; however, aftermarket demand is expected to expand at a 5.79% CAGR through 2031.

- By geography, the Asia-Pacific region retained the highest 49.62% of the automotive clutch market share in 2025, and South America is expected to log the fastest 6.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Clutch Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Dual-Clutch Transmissions | +1.8% | Global, with a concentration in Europe and China | Short term (≤ 2 years) |

| Rising Light-Vehicle Production | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Stringent CO₂ Targets | +0.9% | Europe and North America, extending to Asia-Pacific | Long term (≥ 4 years) |

| 48-V E-Clutch System Adoption | +0.7% | Global, led by premium segments in developed markets | Medium term (2-4 years) |

| Lightweight Composite Friction Materials | +0.4% | North America and Europe, with adoption in Asia-Pacific | Long term (≥ 4 years) |

| Growing Retrofit Demand | +0.3% | Asia-Pacific emerging markets, selective Middle East and Africa regions | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Rapid OEM Shift Toward Dual-Clutch and Automated Transmissions

Dual-clutch penetration is rising because European and Chinese automakers favor wet-clutch designs that hit sub-95 g/km CO₂ targets without full-hybrid premiums. Volkswagen’s MQB-based models deploy electro-hydraulic DQ381 units that cut parasitic drag by 12%, while Chinese brands license DCT technology to enhance 150–250 kW plug-in hybrids. Automated manuals gain share in India’s light commercial segment, where Eaton’s AutoShift trims fuel use 8–10% on urban routes. The trend reduces single-plate dry-clutch volumes but expands demand for multi-plate wet modules and electronic actuation. Suppliers that master mechatronics capture higher unit value, reinforcing competition in premium transmission tiers. A growing base of automated and dual-clutch vehicles promises steadier aftermarket demand because replacement intervals lengthen, but repair complexity and part pricing rise.

Rising Light-Vehicle Production in Emerging Economies

India, Brazil, and key ASEAN markets are collectively forecast to expand light-vehicle production, supported by growing consumer income and favorable local assembly incentives. The output surge anchors baseline clutch volumes, counterbalancing the losses of mature-market BEVs. Emerging factories also push suppliers to co-locate stamping and friction-material plants, improving lead times and currency hedging.

Stringent CO₂ Targets Driving Demand for Fuel-Efficient Clutches

EU Regulation 2019/631[1]"Regulation (EU) 2019/631 of the European Parliament and of the Council of 17 April 2019 setting CO2 emission performance standards for new passenger cars and for new light commercial vehicles, and repealing Regulations (EC) No 443/2009 and (EU) No 510/2011 (recast) (Text with EEA relevance.)," EUR-Lex, eur-lex.europa.eu imposes EUR 95 per gram penalties above 95 g/km, compelling OEMs to cut driveline friction 5-8% between 2020 and 2025. Schaeffler’s E-Clutch saves 7 g/km by removing hydraulic drag through brushless-motor actuation. China’s CAFC cap of 4 L/100 km boosts demand for higher-load sintered-bronze facings, and California’s SULEV30 limit favors dual-mass flywheels that quell three-cylinder NVH. Together, these mandates create a near-term pull for lightweight, low-loss clutch systems that bridge ICE platforms until full electrification is achieved.

Adoption of 48-V e-Clutch Systems for Mild-Hybrid Architectures

Across the first 10 months of 2025, hybrids saw a growth of 15.6%[2], and e-clutch modules enable engine-off coasting with seamless restarts. Valeo’s iBSG recuperates 25% more urban kinetic energy, while BorgWarner’s P2.5 hybrid module allows pure-EV launch to 50 km/h without disconnecting all-wheel-drive hardware. Hyundai’s dry e-clutch reduces 1.8 kg and eliminates hydraulic fluid, signaling a shift in supplier migration from hydraulics to electromechanics. Silicon content rises in every unit, opening new revenue pools for sensor and MOSFET vendors but challenging legacy master-cylinder manufacturers.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating BEV Penetration | -1.4% | Global, led by China, Europe, and California | Long term (≥ 4 years) |

| Rising Popularity of CVT Powertrains | -0.8% | Asia-Pacific mass market, selective North America segments | Medium term (2-4 years) |

| Dual-Mass-Flywheel Reliability Issues | -0.3% | Europe and North America premium segments | Short term (≤ 2 years) |

| Upcoming Copper-Free Friction-Material Mandates | -0.5% | California, Washington, and extending globally | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Escalating BEV Penetration Eliminating Conventional Clutches

China’s approximately 25% BEV share in 2024[3]Jose Pontes, "25% of New Car Sales in China Were 100% Electric in 2024!," Clean Technica, cleantechnica.com cut 3.2 million clutch units, and Europe’s 21.7% share removed 1.8 million more. Tesla and BYD alone displaced 4.8 million assemblies, prompting Volkswagen to idle its Kassel dry-clutch line in 2025. Suppliers are redirecting R&D toward disconnect and torque-vectoring clutches for electrified drivetrains, but unit prices are 40-60% lower than those of DCT modules, thereby compressing revenue.

Rising Popularity of CVT Powertrains in Entry-Level Cars

CVT shares hit significantly in the Asia-Pacific region in 2024 as Nissan, Honda, and Subaru deployed steel-belt designs that reduce component count by 35% compared to manual transmissions. Indian automakers lifted CVT take-rates from 8% in 2020 to 22% in 2024, eroding single-plate dry-clutch volumes. CVTs favor suppliers with pulley and belt expertise, sidelining European friction-material specialists.

Segment Analysis

By Transmission Type: DCT Outpaces Manual Despite Legacy Dominance

Manual transmission retained a 64.79% share of the automotive clutch market in 2025 as buyers in India, Brazil, and Southeast Asia prized its lower ex-factory cost. Yet, wet dual-clutch systems are expected to expand at a 9.37% CAGR through 2031, driven by European and Chinese plug-in hybrids that require sub-0.2-second shifts and seamless torque overlay.

Transmission preferences illustrate a bifurcated demand curve. Cost-driven emerging markets continue to favor single-plate dry clutches, which cost USD 45–60 in the aftermarket, thereby maintaining elevated volumes even as electrification gains traction elsewhere. Premium European sedans utilize EUR 2,800 wet DCT units to achieve 12% fuel savings compared to torque-converter automatics, amid diesel prices exceeding EUR 1.80 per liter. Volvo’s I-Shift-equipped trucks eliminate pedal effort, resulting in a 14% reduction in driver injury claims in Swedish fleets. The divergence preserves high-volume manual production while giving technology leaders a margin-rich DCT runway through 2031.

Note: Segment shares of all individual segments available upon report purchase

By Vehicle Type: Commercial Vehicles Gain Momentum

Passenger cars generated a 74.23% share of the automotive clutch market in 2025. Still, medium and heavy commercial vehicles are forecast to post the fastest growth rate of 8.02% CAGR through 2031, driven by e-commerce logistics that boost mileage and regulators nudging fleets toward automated gearboxes that minimize fatigue on daily hauls of 500 km. Ford Transit and Stellantis Ducato vans utilize LuK dual-mass flywheels, which extend service intervals to 180,000 km. Meanwhile, John Deere tests wet-clutch power-shift transmissions on high-horsepower combines for in-field ratio changes.

Commercial electrification reshapes demand. Battery-electric delivery vans eliminate clutches, whereas range-extender hybrids retain disconnect units to isolate the generators. Ashok Leyland’s Boss LX uses ZF’s Traxon AMT with a dual-plate clutch rated 1,400 Nm for 49-ton gross weights, and Caterpillar dozers specify wet multi-plate clutches to dissipate 180 kW of heat during earth-moving. This mix sustains the automotive clutch market across diverse use-cases even as passenger-car BEVs proliferate.

By Clutch Component: Actuation Systems Lead Growth

Clutch disc and hub assemblies commanded a 29.08% share of the automotive clutch market in 2025; however, actuation systems advanced at an 8.41% CAGR, as 48V e-clutch modules replace hydraulics and eliminate pedal effort. Pressure plates now use diaphragm springs that cut bearing travel by 15%, and Schaeffler’s E-Clutch ball-screw actuator raises efficiency to 92%, saving 0.2 L/100 km in WLTP tests.

Electronic actuation extends into heavy trucks via pneumatic-electronic hybrids, and concentric slave cylinders reduce hydraulic lines by 60%, thereby trimming fluid volume by 40%. Aisin’s aluminum flywheel sheds 22% inertia for quicker DCT upshifts. These updates lift average unit value, positioning actuation suppliers for outsized growth within the automotive clutch market.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: Aftermarket Rises on Retrofits

OEM supply comprised an 82.45% share of the automotive clutch market in 2025; however, the aftermarket is growing at a rate of 5.79% through 2031, driven by emission upgrades in India and Brazil, which prompt taxi and ride-hail operators to replace worn friction discs with ceramic-metallic kits that can withstand the loads of turbo-diesel engines.

Different aging curves drive regional demand for services. India’s vehicle parc averages 8.2 years, with 42% of vehicles older than 10 years. In contrast, Brazil’s taxi fleet covers 180,000 km per year, quickly wearing out clutches. ZF’s Sachs Performance brand now markets sintered-bronze discs that tolerate 20% higher torque for tuners. Online availability widens reach, helping the automotive clutch market sustain aftermarket expansion despite longer OE replacement intervals on newer DCT platforms.

Geography Analysis

Asia-Pacific maintained a 49.62% share of the automotive clutch market in 2025. In China, the growing adoption of wet dual-clutch transmissions (DCTs) in plug-in hybrid SUVs is pushing up unit values. Meanwhile, in India, the dominance of manual transmissions continues to fuel a robust demand for cost-effective dry clutches. Japan sees a decline in volumes as continuously variable transmissions (CVTs) gain prominence. However, companies like EXEDY and Aisin counterbalance this dip by ramping up exports, leveraging their competitive cost structures to undercut European prices. In Southeast Asia, factories are embarking on localized initiatives, bolstered by Thailand's approval of USD 420 million in foreign direct investment (FDI) for components.

The North American automotive clutch market is primarily driven by commercial vehicles and performance cars, as the manual transmission rate in mainstream passenger models has fallen below 2%. Mexico’s premium-sedan exports sustain wet DCT volumes, and South America shows the strongest 6.82% CAGR through 2031, as Brazil’s flex-fuel hybrids pair higher-torque ethanol engines with manual gearboxes. The Middle East and Africa, with South African incentives, are drawing investment in pickup clutch assembly for sub-Saharan exports.

Competitive Landscape

The top five suppliers held a significant share of global OEM revenue in 2025, resulting in a highly concentrated profile for the automotive clutch market. Schaeffler earned 18–22% gross margins on vertically integrated dual-clutch lines, while Valeo’s merger with Vitesco expanded its 48 V e-clutch portfolio across 14 platforms. BorgWarner’s 2024 Haldex acquisition added torque-vectoring know-how, positioning the firm for electric SUV demand.

Suppliers are racing to address copper-free friction, disconnect clutches for range extenders, and torque-vectoring modules for electric crossovers. Portfolio breadth, local manufacturing, and R&D speed influence share shifts, although scale and deep OEM ties continue to favor incumbents for high-volume DCT awards.

Automotive Clutch Industry Leaders

-

Valeo SA

-

Schaeffler AG

-

EXEDY Corporation

-

Aisin Corporation

-

ZF Friedrichshafen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Schaeffler showcased an expanded lineup of motion-technology solutions at CES 2025, emphasizing its focus on BEV solutions and a commitment to a carbon-neutral roadmap.

- October 2024: Schaeffler completed its merger with Vitesco Technologies, projecting EUR 600 million EBIT synergies by 2029.

- September 2024: ZF and Foton expanded their partnership to launch the TraXon 2 Hybrid for Chinese commercial vehicles, with global production scheduled for 2026.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the automotive clutch market as the value of all factory-fitted and replacement friction, dual, and automated manual clutches, plus their core parts, disc, cover, flywheel, release bearing, and actuation modules, installed in passenger cars and commercial vehicles that still rely on internal-combustion or hybrid drivetrains.

Scope exclusion: fully battery-electric drivetrains that employ direct drive and continuously-variable transmission belt packs are kept outside the model.

Segmentation Overview

-

By Transmission Type

- Manual Transmission

- Automatic Transmission (Torque-Converter)

- Automated Manual Transmission (AMT)

- Dual-Clutch Transmission (DCT)

- Others (e-Clutch, CVT Clutch Packs, etc.)

-

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Off-Highway (Agricultural and Construction)

-

By Clutch Component

- Clutch Disc and Hub

- Pressure Plate and Cover

- Release Bearing/Slave Cylinder

- Flywheel (Single and Dual-Mass)

- Actuation Systems (Hydraulic, Electro-Hydraulic, Electronic)

-

By Sales Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts interview drivetrain engineers at Tier-1 suppliers, aftermarket distributors in Asia-Pacific, Europe, and the Americas, and fleet maintenance heads who clarify replacement intervals and dual-clutch penetration. Surveys of workshops further test assumed average selling prices, ensuring the voice of the market grounds secondary findings.

Desk Research

We begin by mining high-credibility public datasets such as OICA production tallies, UN Comtrade trade codes for clutch HS classifications, ACEA registration updates, and NHTSA recall files, which together frame the size of the global vehicle fleet and its clutch replacement rhythm. Company filings, investor decks, and respected trade journals enrich price movements and technology adoption timelines.

Complementing these are paid resources in Mordor's tool kit, Marklines for plant-level build volumes, D&B Hoovers for supplier revenue splits, and Dow Jones Factiva for real-time strategic moves, so our analysts can link physical output to monetary value.

This list is illustrative; numerous additional sources supported data capture and validation.

Market-Sizing & Forecasting

A top-down vehicle production and trade-reconstruct model provides the skeleton. Annual light-vehicle builds, average clutches per vehicle, and park-age-based replacement rates generate unit demand, which is then priced using region-specific ASP curves. Supplier roll-ups and sampled dealer invoices act as selective bottom-up cross-checks that temper any overrun. Key variables tracked include dual-clutch share of new transmissions, weighted fleet age, regional miles-driven trends, raw-material cost indices, and BEV penetration that cannibalizes friction clutches. Multivariate regression blends these inputs and projects forward to 2030, while scenario analysis stresses high-EV and mild-recession cases before a balanced outlook is locked.

Data Validation & Update Cycle

Model outputs undergo variance checks against independent shipment metrics; anomalies trigger re-contacts with previous sources, followed by a tiered analyst peer review before sign-off.

Reports refresh annually, and our team issues mid-cycle tweaks when events, such as a sudden OEM strike, materially shift supply or price dynamics.

Why Our Automotive Clutch Baseline Commands Confidence

Published estimates often diverge because firms mix drivetrain scopes, apply dissimilar average prices, or freeze assumptions for several years.

Key gap drivers center on whether hybrid clutches are counted, how aftermarket mark-ups are layered, currency conversion dates, and refresh cadence; this is where ���ϲ�����, through yearly park recalibration and live ASP tracking, secures a steadier baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.61 B (2025) | ���ϲ����� | - |

| USD 12.60 B (2024) | Global Consultancy A | Excludes heavy trucks and uses lower OEM price bands |

| USD 12.44 B (2023) | Trade Journal B | Older base year and omits dual-clutch units |

| USD 14.10 B (2022) | Industry Association C | Applies static replacement rate, no hybrid adjustment |

The comparison shows that, by selecting the right drivetrain mix, refreshing inputs yearly, and cross-verifying with field voices, we deliver a balanced, transparent figure that decision-makers can trace back to observable variables and replicate with ease.

Key Questions Answered in the Report

How large is the automotive clutch market in 2026?

The automotive clutch market size stood at USD 15.39 billion in 2026 and is expected to reach USD 20.51 billion by 2031.

Which transmission type is growing fastest?

Wet dual-clutch systems are forecast to expand at a 9.37% CAGR through 2031 as OEMs seek quick shifts and lower CO₂.

Why is aftermarket demand rising?

Retrofit programs in India, Brazil, and Southeast Asia call for emission-compliant clutch kits, pushing aftermarket revenue at a 5.79% CAGR.

Which region leads clutch consumption?

Asia-Pacific commanded 49.62% revenue in 2025 thanks to high vehicle output in China and India.

What is the main threat to clutch suppliers?

Rapid battery-electric vehicle adoption removes conventional clutch assemblies, trimming the ICE replacement base in key markets.