Automotive Brake Pad Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 4.57 Billion |

| Market Size (2031) | USD 5.87 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

Automotive Brake Pad Market Analysis by ���ϲ�����

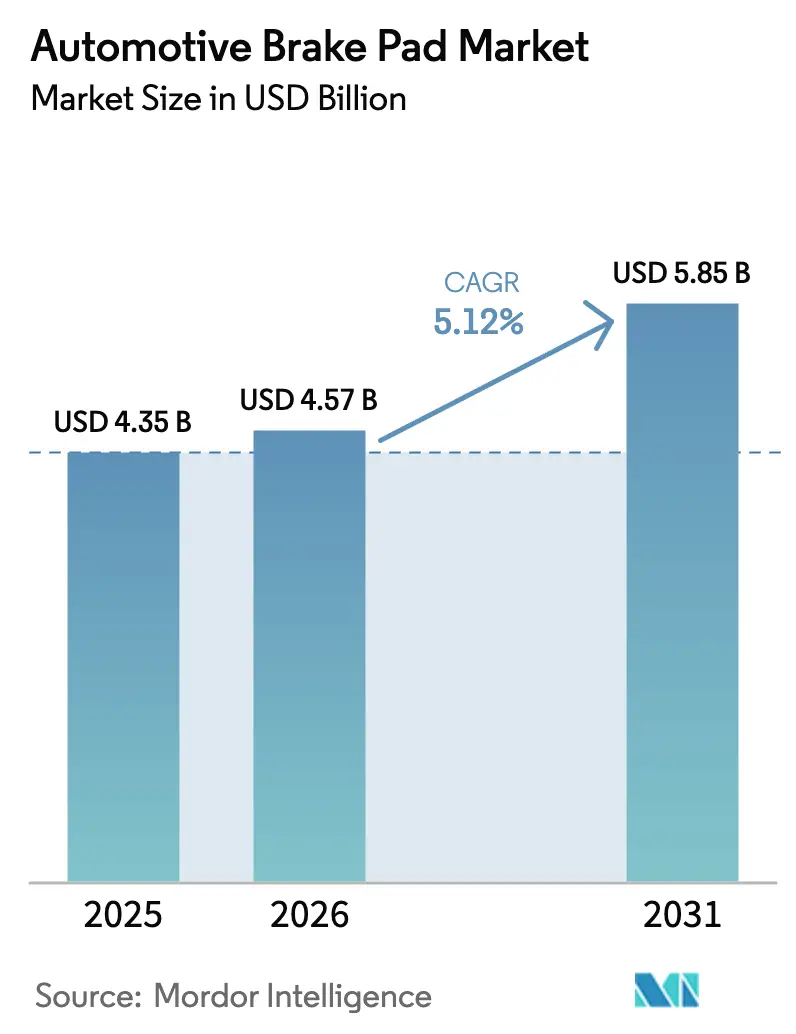

The Automotive brake pads market size is expected to grow from USD 4.35 billion in 2025 to USD 4.57 billion in 2026 and is forecast to reach USD 5.87 billion by 2031 at 5.12% CAGR over 2026-2031. Stronger particulate-matter limits under Euro 7 and China 7, rapid copper-free material substitution, and the proliferation of e-commerce across replacement parts are together rewriting product-development timelines and channel economics in the Automotive brake pads market. Ceramic formulations are advancing fastest because premium and battery-electric platforms demand low-dust, low-noise pads, while semi-metallic products remain dominant on cost-sensitive internal-combustion vehicles. Asia-Pacific commands almost half of current revenue thanks to China’s record vehicle production and India’s surging two-wheeler electrification; the region also represents the fastest geographic expansion trajectory. Competitive differentiation is tilting toward digital R&D assets, with leading suppliers compressing homologation cycles by integrating neural-network models and connected-vehicle telemetry into virtual test loops.

Key Report Takeaways

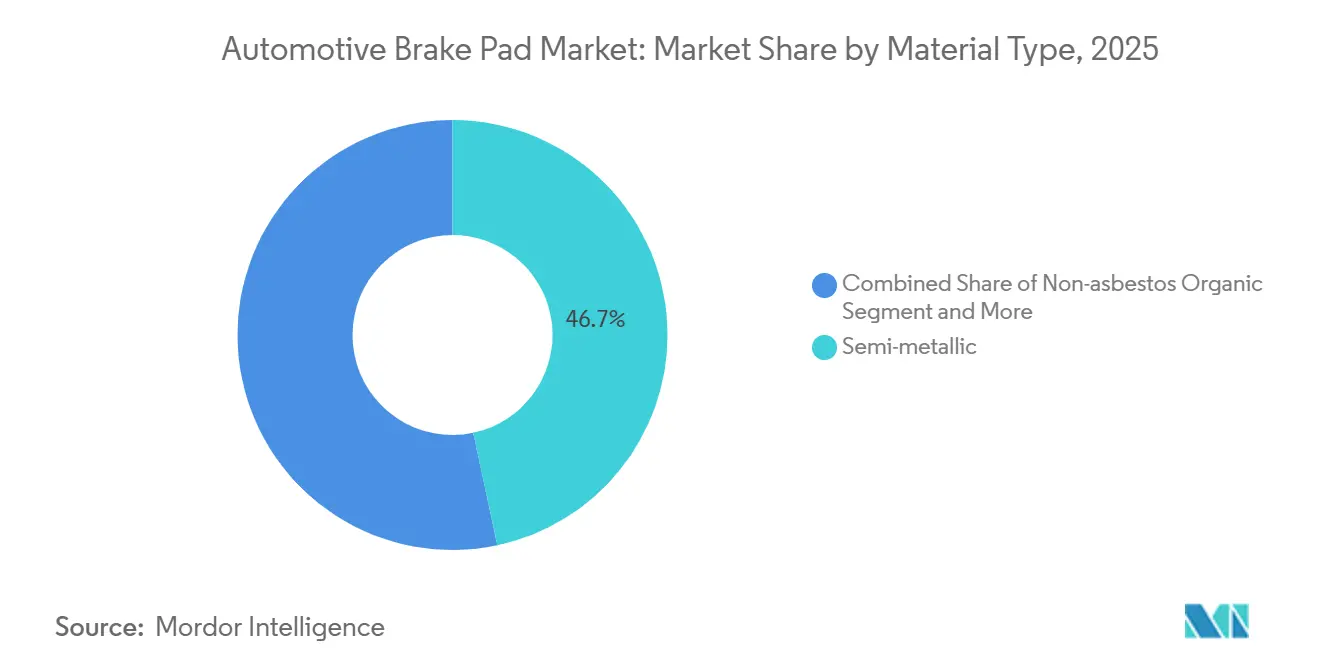

- By material type, semi-metallic pads held the largest 46.67% share of 2025 revenue, while ceramic pads are projected to register the fastest 5.92% CAGR through 2031.

- By position, front-axle pads commanded 64.73% of 2025 sales, whereas rear pads are forecast to grow at a 6.15% CAGR to 2031.

- By sales channel, the aftermarket captured 65.23% of 2025 revenue and is also the fastest-growing segment with a 6.19% CAGR over 2026-2031.

- By propulsion type, internal-combustion vehicles accounted for 84.28% of 2025 revenue; battery-electric vehicles led growth with a 7.81% CAGR through 2031.

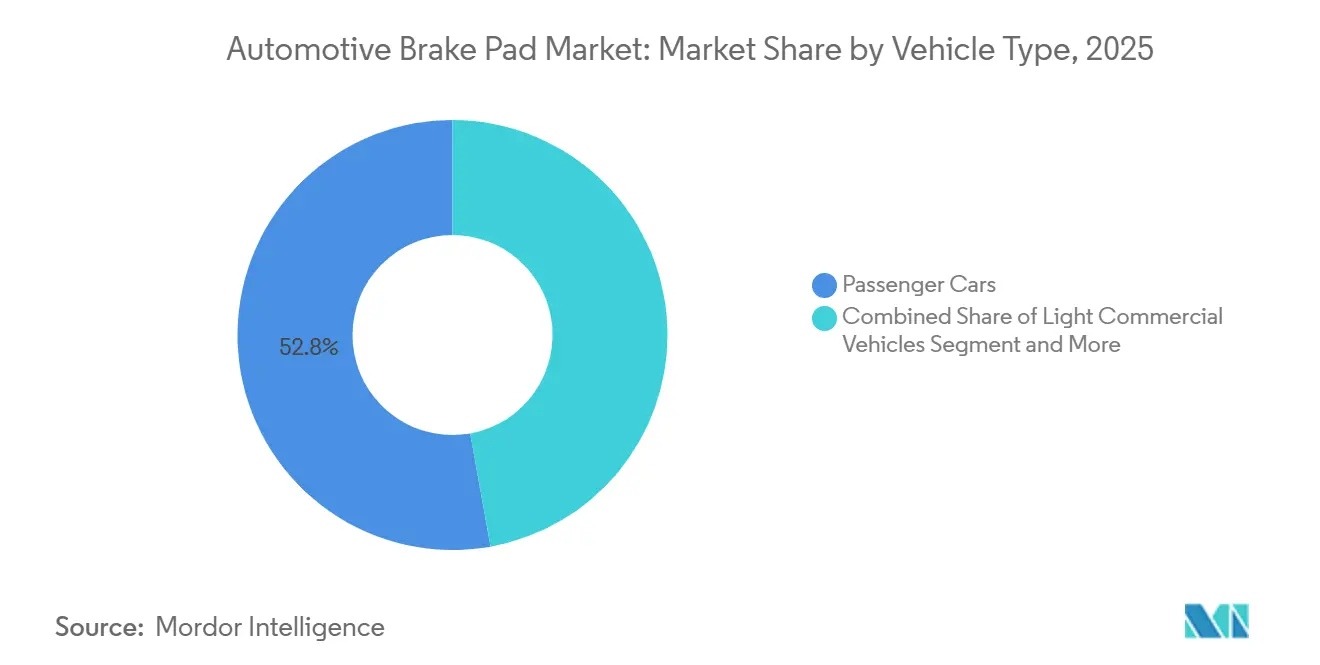

- By vehicle type, passenger cars accounted for 52.82% of 2025 sales, while two-wheelers posted the quickest 6.32% CAGR over the forecast horizon.

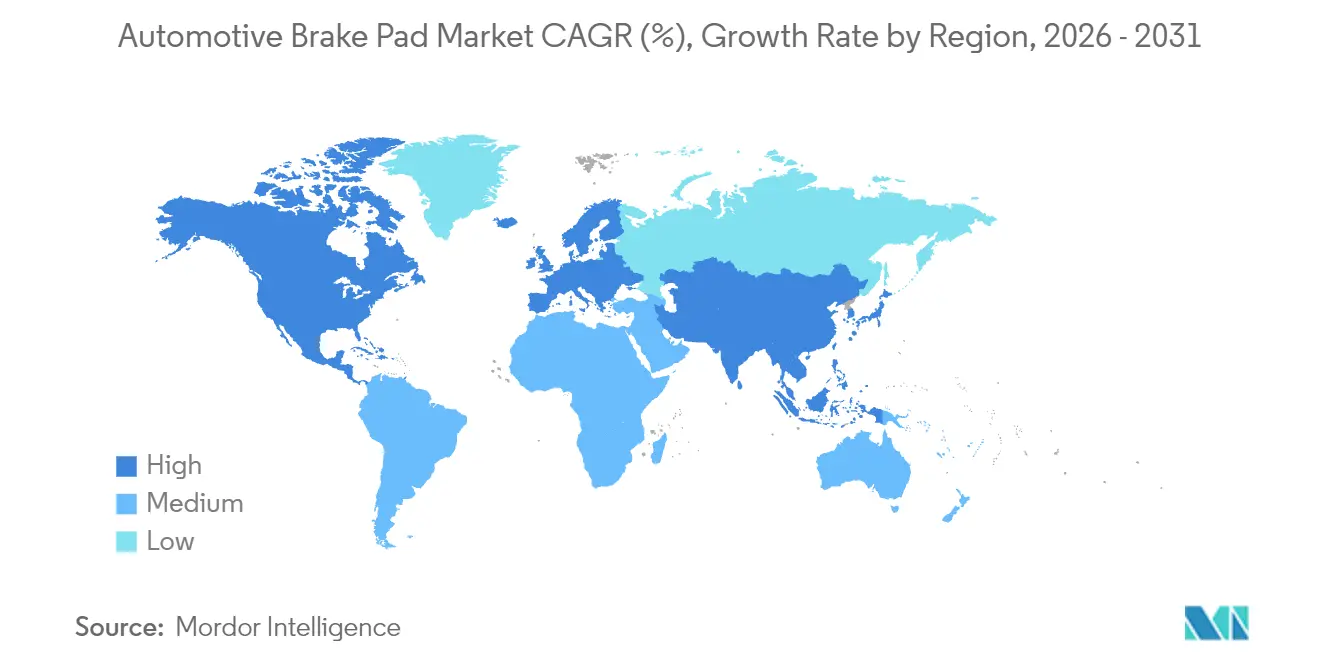

- By region, Asia-Pacific dominated with a 48.31% revenue share in 2025 and is projected to expand at the highest Cto 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Brake Pad Market Trends and Insights

Drivers Impact Analysis Table

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Safety Regulations (Euro 7, China 7) | +1.4% | Europe, China, with spillover to ASEAN and Latin America | Medium term (2-4 years) |

| Shift to Copper-Free, Low-Emission Brake Pads | +1.2% | Global, led by North America (California Prop 65) and EU | Short term (≤ 2 years) |

| New NVH and Corrosion Standards for EVs | +1.1% | Global, concentrated in China, Europe, North America EV hubs | Medium term (2-4 years) |

| Surge in Aftermarket E-Commerce for Brake Parts | +0.8% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| AI Optimizes Pad Formulation and Testing | +0.6% | Global, early adoption in Europe and Japan | Long term (≥ 4 years) |

| Rising Demand for Brake Pad Sensors | +0.5% | Europe, North America premium segments, China NEV platforms | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Surging Safety-Regulation Stringency (Euro 7, China 7)

Euro 7 rules cap brake particulate emissions at 7 mg/km from 2025 and force copper content below 0.5% by weight, making legacy phenolic-copper blends obsolete [1]“Euro 7 Emission Standards,”, European Commission, ec.europa.eu. Beginning in late 2026, China 7 will enforce real-world emission testing, effectively outlawing copper-rich pads. Suppliers holding the UN GTR No. 24 certification can expedite their approval cycles by up to 9 months, resulting in nearly a 20% reduction in engineering costs. Tier-1 companies, equipped with their own particle labs, benefit from priority access to new vehicle programs. In contrast, remanufacturers face hurdles due to high testing fees. Such regulatory pressures are fueling consolidation within the automotive brake pads market.

Rapid Copper-Free and Low-Emission Pad Material Adoption

California's zero-copper mandate has set off a chain reaction across the nation [2]“Brake Friction Materials Restrictions,”, California Department of Toxic Substances Control, dtsc.ca.gov. In response, OEMs are streamlining their SKUs and pivoting towards stainless-steel and ceramic blends. Akebono's patent describes an SS316-andalusite matrix that achieves a consistent friction coefficient across a wide temperature range. While ceramic pads command a significant price premium, they're in high demand among luxury and electric vehicle (EV) buyers who prioritize pristine wheels. With andalusite supplies predominantly sourced from South Africa and China, any export restrictions could push raw material costs substantially higher. Such supply chain intricacies underscore the elevated status of copper-free pads in the automotive brake pad market.

Electrified-Vehicle NVH and Corrosion Design Requirements

Battery-electric cars utilize regenerative braking for most of their deceleration. This extended use leaves brake pads idle, making them susceptible to moisture corrosion on their backing plates[3]"Quantifying the Deceleration of Various Electric Vehicles", SAE INTERNATIONAL, sae.org. Continental recommends using galvanized steel plates for brake pads. While this addition increases costs slightly per pad set, it significantly extends the pad's lifespan. The silent operation of electric engines has heightened the prominence of squeals, leading to stricter NVH (Noise, Vibration, and Harshness) specifications. These now favor features like chamfered edges, multilayer shims, and damping coatings. Brembo's SENSIFY suite, a brake-by-wire system, incorporates advanced algorithms for pad wear. These algorithms smartly distribute the responsibility for stopping between electric motors and hydraulic systems, resulting in a notable reduction in pad consumption. Suppliers adept in both corrosion prevention and acoustic enhancement are poised to dominate the automotive brake pads market.

Aftermarket E-Commerce Penetration in Brake Parts

Digital channels are gaining prominence in North America's automotive aftermarket. A notable number of brake pad orders, whether for professional installation or DIY, are now being placed through online marketplaces and specialized portals. This trend reflects increasing consumer confidence in e-commerce and the convenience of digital platforms for routine vehicle maintenance. The use of ACES/PIES catalog standards, combined with natural-language search, reduces fitment errors, minimizing costly returns for small shops. Predictive-maintenance apps leverage connected-vehicle telematics to forecast pad life, send consumer alerts, and automatically queue replacement kits. Small distributors utilize drop-ship tools to lower on-hand inventory, freeing up cash while meeting delivery targets. These structural efficiencies accelerate product launches, as catalog updates are instant and no longer constrained by print cycles.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regenerative Braking Reduces Replacements | -1.2% | China, Europe, North America EV-adoption leaders | Medium term (2-4 years) |

| Raw Material Volatility Raises Prices | -0.7% | Global, most severe in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Limited Copper-Free Supply Chain Capacity | -0.5% | Global, bottlenecks in South Africa and China andalusite supply | Medium term (2-4 years) |

| Recall Risk from Thermal Cracking | -0.3% | Global, acute in North America litigation environment | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

Regenerative Braking Reducing Replacement Frequency

Battery-electric cars are setting new standards, often surpassing significant mileage thresholds before their first brake pad change. This marks a substantial improvement compared to traditional internal combustion vehicles. Service data revealed that specific electric vehicle models had median brake pad replacements at much higher mileage, leading to a considerable reduction in lifetime pad demand. While aftermarket distributors face reduced revenue density, they are expanding their portfolios to include products such as fluids and wipers. Meanwhile, OEM suppliers are mitigating losses by offering sensor-embedded pads, which command significant premiums. However, this adoption is predominantly observed in the premium vehicle segment. The extended interval for brake pad changes poses a considerable challenge for the automotive brake pads market, a challenge projected to persist over the long term.

Price Pressure from Raw-Material Volatility

Steel backing plates fluctuated between USD 800 and USD 900 per metric ton as energy-price instability affected mills. Phenolic resin, closely tied to crude oil, experienced price swings in response to fluctuations in Brent crude. Akebono's report highlighted materials inflation as a key factor behind a significant margin squeeze in North America. In response, major suppliers are vertically integrating into the resin business, while smaller remanufacturers face shrinking profit margins. This volatility has strengthened the bargaining power of well-capitalized players in the automotive brake pads market.

Segment Analysis

By Material: Ceramic Ascendancy on Premium and EV Platforms

Semi-metallic pads still account for 46.67% of 2025 revenue because they cost USD 25–40 per axle, compared with USD 50–70 for ceramics, yet copper phase-outs force expensive stainless-steel substitution. Ceramic pads will grow at 5.92% CAGR as OEMs target low dust and quiet cabins. In Asian and Latin American aftermarkets, non-asbestos organic products are favored for their rotor-friendly composition. However, fluctuations in resin prices are impacting profitability. Low-metallic NAO mixes, which blend organic fibers with steel, ensure particle compliance. Akebono’s patent introduces an andalusite-reinforced variant that aligns with Euro standards. Today, OEMs prioritize total system economics—encompassing pad, rotor, and warranty—over the upfront unit cost alone. This shift is bolstering ceramics' momentum in the automotive brake pads market, especially for material upgrades. a

Sustainability is becoming a key focus in the materials portfolio. A forthcoming European regulation mandates recycled content in friction materials. This move benefits suppliers who can swiftly integrate scrap steel fibers. In Japan, bio-based phenolic resins, boasting plant content and maintaining mechanical integrity, have entered pilot production. Such green innovations are carving out a larger share of the automotive brake pads market while ensuring top-notch performance.

Note: Segment shares of all individual segments available upon report purchase

By Position: Front Dominance with Growing Rear Engagement

Front pads captured 64.73% of 2025 sales because 60–70% of vehicle mass shifts forward under braking. Electronic brake-force distribution on hybrids and EVs shifts incremental load rearward to harvest energy, lifting rear-pad growth to a 6.15% CAGR. Conventional internal-combustion vehicles typically replace front pads more frequently than rear pads. However, regenerative vehicles are reducing overall activation, thereby narrowing the wear gap. Brembo has recommended using semi-metallic blends for the front and ceramic blends for the rear on new hybrids. Toyota has already adopted this specification for its upcoming models. In India, regulations mandating rear discs on motorcycles above a specific engine capacity are set to boost demand for rear pads, thereby increasing the market share of automotive brake pads for rear applications.

Trends in load balancing are introducing design complexities. While rear pads are subjected to lower temperatures, they are also more prone to corrosion. To combat this, suppliers are turning to coated backing plates and water-resistant shims. With the surge in EV sales, there's a noticeable uptick in rear-axle utilization, poised to influence the product mix and revenue distribution in the automotive brake pads market.

By Sales Channel: Digital Disruption Redraws Aftermarket Maps

The aftermarket generated 65.23% of revenue during 2025 and expanded at a 6.19% CAGR, underpinned by online ordering, fitment algorithms, and rapid last-mile delivery. Amazon, RockAuto, and AutoZone collectively deliver over one-third of aftermarket pad units in North America, leveraging data to cross-sell rotors and sensors. OEM channels, while growing more slowly, leverage higher price points through bundled telematics and extended warranties. For instance, Continental’s wireless pad-wear sensor, designed for Volkswagen’s MEB platform, showcases data-rich OEM kits commanding significantly higher prices than their aftermarket counterparts. However, as regenerative braking reduces replacement frequency—especially in electric fleets—digital retailers are responding by adding fluids, filters, and tires to their offerings, ensuring they capture a larger share of the wallet within the Automotive brake pads market.

Regional differences are evident: European consumers tend to install products themselves more than their Asian counterparts, who favor click-and-collect models. Meanwhile, in Latin America, corner workshops thrive on cash sales. Yet, the global trend leans towards fewer intermediaries and increased pricing transparency.

By Vehicle Type: Two-Wheeler Urbanization Drives Growth

Passenger cars remain the most significant slice at 52.82% of revenue, but growth in mature markets is slowing. Two-wheelers expand at a 6.32% CAGR through 2031 as India, Indonesia, and Vietnam shift to electric scooters with disc brakes instead of drums. As e-commerce surges, European parcel vans experience a notable shift: their payload life now averages significantly less due to the stop-and-go demands. Heavy-duty trucks, on the other hand, are turning to sintered-metal pads that withstand incredibly high temperatures. Meritor is capitalizing on this trend, promoting long-lasting sets tailored for Class 8 tractors. In India, the AIS-155 legislation is making waves, introducing a substantial number of disc-equipped bikes each year. This surge is sending ripples through the Automotive brake pads market, especially influencing OEM supply dynamics in South and Southeast Asia.

While emerging economies have traditionally leaned towards budget-friendly semi-metallic pads, escalating safety standards are nudging them towards premium options. As a result, there's a gradual shift towards ceramic and copper-free alternatives. This diverse vehicle landscape ensures that no single sub-segment dominates, paving the way for sustained growth in the Automotive brake pads market.

Note: Segment shares of all individual segments available upon report purchase

By Propulsion Type: Electrification Creates Specialized Demands

Internal-combustion platforms still account for 84.28% of 2025 revenue, sustaining bulk volume for several more years as the global ICE parc exceeds 1 billion units. Battery-electric vehicles post the fastest 7.81% CAGR, thanks to policy-driven adoption in China and Europe. Regenerative stopping extends pad life significantly, dampening per-vehicle demand. Hybrids, with their transitional architecture, experience intermittent loading patterns that subject pads to wider temperature swings. Research from Bosch indicates that hybrid duty cycles produce greater thermal variance than BEVs or ICEs. This variance prompts a shift towards resin chemistries that boast broader glass-transition windows. Consequently, the evolving propulsion mix delineates distinct material priorities in the automotive brake pads market: hybrids prioritize fade resistance, BEVs focus on corrosion control, and ICEs emphasize cost optimization.

National policies dictate the pace and composition of these trends. China has cemented its status as a global leader in new-energy vehicle production. Meanwhile, North America's lagging BEV growth extends the aftermarket replacement cycle for ICE models. The strategic equilibrium among these propulsion types will be pivotal for revenue stability among pad manufacturers in the coming decade.

Geography Analysis

In 2025, the Asia-Pacific region dominated the automotive brake pad market, accounting for 48.31% and projected to grow at a CAGR of 5.97% through 2031. This growth is fueled by surging vehicle outputs in China, India, and ASEAN nations, bolstered by dense supplier clusters. China's shift from Euro 6 to Euro 7 standards is catalyzing swift transitions to copper-free pads, presenting both hurdles and prospects for local manufacturers. Meanwhile, India's booming two-wheeler market is benefiting homegrown champions, who are consolidating foundries and compound kitchens to lessen import dependencies. Furthermore, Japanese and Korean companies are pioneering advancements in ceramic and aramid fiber technologies, subsequently sharing these innovations with regional partners.

North America presents a seasoned replacement market, buoyed by an aging vehicle demographic that ensures steady aftermarket revenues. Proactive investments by suppliers, spurred by state-level copper bans in California and Washington, are now reaping rewards nationwide. Thanks to USMCA tariff incentives favoring regional content, Mexico's burgeoning vehicle assembly lines are increasingly sourcing parts locally. Additionally, Canada's harsh winters and similar conditions in northern U.S. states heighten the demand for specialized, corrosion-resistant backplates and low-temperature binders that combat salt-induced delamination.

Europe, setting the global benchmark with its Euro 7 particulate limits, sees premium German brands championing ceramic adoption. At the same time, Italian and Spanish suppliers carve out niches in the motorcycle and performance segments. While currency fluctuations and energy price volatility raise production costs, the unity within the EU mitigates cross-border regulatory challenges, ensuring seamless intra-EU freight movement from Poland to Portugal. Moreover, Eastern European facilities are clinching more pad contracts, thanks to their competitive labor costs and adherence to EU quality standards.

Competitive Landscape

Industry leadership concentrates in a handful of multinational groups like Brembo, Bosch, Continental, Nisshinbo, and Aisin that combine OEM pedigree with strong aftermarket branding. Continental integrates IoT sensors into pads, enabling fleet-scale wear analytics that unlock subscription revenue. Bosch leverages its diagnostics tool portfolio to bundle pad sales with workshop software updates, deepening installer stickiness.

Mid-tier specialists thrive by owning niches—ASK Automotive dominates Indian two-wheelers, while Tenneco’s Ferodo line targets performance enthusiasts. Private-label programs offered by global distributors create price ceilings that force majors to differentiate via features, not just cost. Rising R&D spend on copper-free blends, NVH coatings, and AI simulation favors scale players.

Digital retail reshuffles channel power: marketplaces directly court installers, squeezing traditional wholesalers. Some incumbents respond with same-day delivery fleets and inventory-as-a-service platforms for garages that cannot stock every SKU. Smaller local formulators find it increasingly challenging to meet the hefty financial demands of Euro 7 certification, often running into costs of several million dollars for each compound family. Consequently, this has heightened the likelihood of industry consolidation, as larger players are more likely to shoulder these regulatory expenses. Specialist firms may pivot to contract manufacturing under big-brand labels or exit altogether.

Automotive Brake Pad Industry Leaders

-

Tenneco Inc.

-

Nisshinbo Holdings Inc.,

-

Akebono Brake Industry Co., Ltd.

-

Robert Bosch GmbH

-

Brembo N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Brembo S.p.A. (Brembo) joined the RE-BREATH project to reduce non-exhaust particulate emissions in urban fleets. Supported by the European Commission’s LIFE Programme, Brembo developed a low-emission braking system for heavy-duty vehicles, meeting Euro 7 standards with low-wear cast iron discs and copper-free pads.

- January 2025: ASK Automotive Limited, through its subsidiary ASK Automobiles Private Limited, started production at its 18th facility in Karnataka. This third ASK Automobiles facility serves OEM customers in southern India. ASK Automotive produces advanced braking systems, including brake panel assemblies, brake shoes, and disc brake pads.

Global Automotive Brake Pad Market Report Scope

The automotive brake pad market report is segmented by material type (semi-metallic, non-asbestos organic, low-metallic nao, and ceramic), position (front and rear), sales channel (OEM and aftermarket), vehicle type (passenger cars, light commercial vehicles, heavy commercial vehicles, and two-wheelers), propulsion type (ICE, hybrid electric vehicles, and battery electric vehicles), and geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Semi-metallic |

| Non-asbestos Organic (NAO) |

| Low-metallic NAO |

| Ceramic |

| Front |

| Rear |

| Original Equipment Manufacturers (OEM) |

| Aftermarket |

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Heavy Commercial Vehicles (HCV) |

| Two-Wheelers |

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery-Electric Vehicles |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Qatar | |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Semi-metallic | |

| Non-asbestos Organic (NAO) | ||

| Low-metallic NAO | ||

| Ceramic | ||

| By Position | Front | |

| Rear | ||

| By Sales Channel | Original Equipment Manufacturers (OEM) | |

| Aftermarket | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Heavy Commercial Vehicles (HCV) | ||

| Two-Wheelers | ||

| By Propulsion Type | Internal-Combustion Engine Vehicles | |

| Hybrid Electric Vehicles | ||

| Battery-Electric Vehicles | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Qatar | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Automotive brake pads market in 2031?

It is forecast to reach USD 5.87 billion by 2031, rising at a 5.12% CAGR between 2026 and 2031.

Which material segment leads revenue today, and which grows fastest?

Semi-metallic pads hold the largest 46.67% share, while ceramic pads expand the quickest at 5.92% CAGR through 2031.

Which region contributes the most revenue to pad suppliers?

Asia-Pacific generated 48.31% of global sales in 2025 and remains the fastest-growing geography at a 5.97% CAGR.

How are raw-material price swings managed by major suppliers?

Leading players increasingly integrate upstream, such as Brembo securing resin supply through equity stakes, insulating margins from steel and resin volatility.

How will regenerative braking influence replacement demand?

BEV regenerative systems extend pad life beyond 100,000 miles, lowering aftermarket replacement frequency by roughly two-thirds versus ICE vehicles.