Market Overview

| Study Period | 2020 - 2031 |

|---|---|

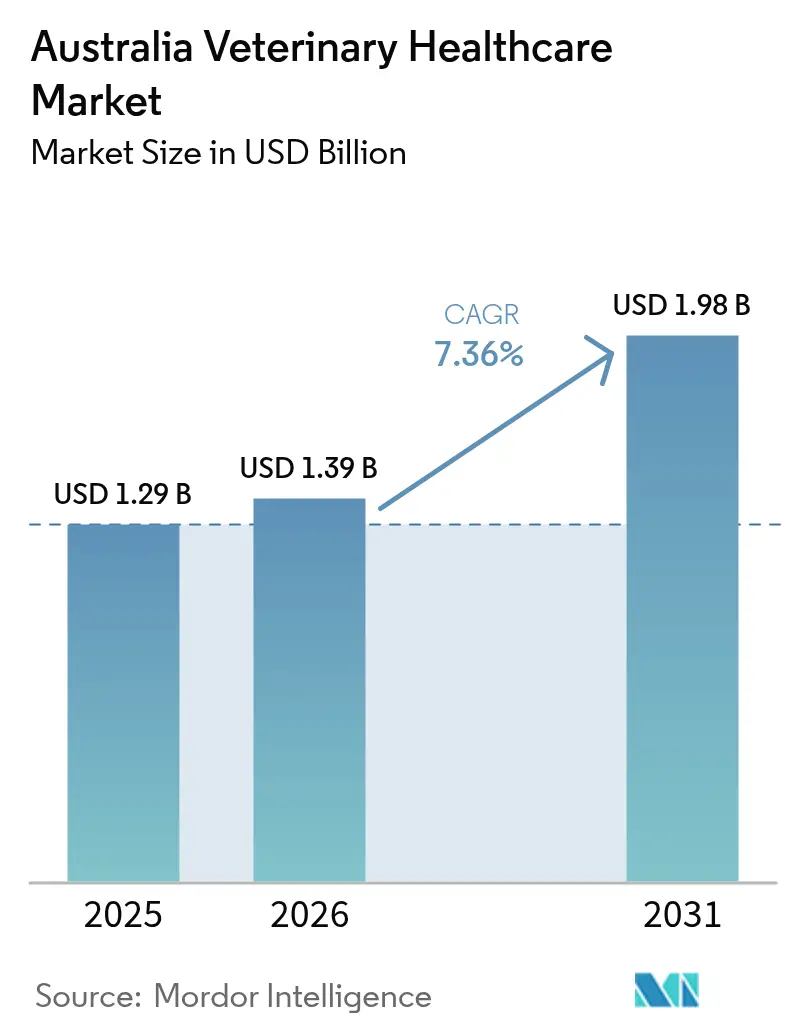

| Base Year Market Size (2025) | USD 1.29 Billion |

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.98 Billion |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Australia Veterinary Healthcare Market Analysis by ���ϲ�����

The Australia veterinary healthcare market size is expected to grow from USD 1.29 billion in 2025 to USD 1.39 billion in 2026 and is forecast to reach USD 1.98 billion by 2031 at 7.36% CAGR over 2026-2031. Demand is pivoting around mandatory livestock traceability, fast-tracked biologic approvals, and rising companion-animal spending. Electronic identification for sheep and goats couples disease surveillance with data analytics revenue, while point-of-care diagnostics shorten decision cycles and capture margin that once flowed to external laboratories[1].Integrity Systems Company, “NLIS Database Uplift Project,” integritysystems.com.au Private-equity roll-ups equip newly acquired clinics with proprietary analyzers to boost earnings, and sovereign vaccine manufacturing investments protect supply chains from geopolitical disruptions. Workforce shortages in rural areas and price-sensitive pet owners temper growth, yet pet insurance uptake and subscription wellness plans cushion out-of-pocket shocks.

Key Report Takeaways

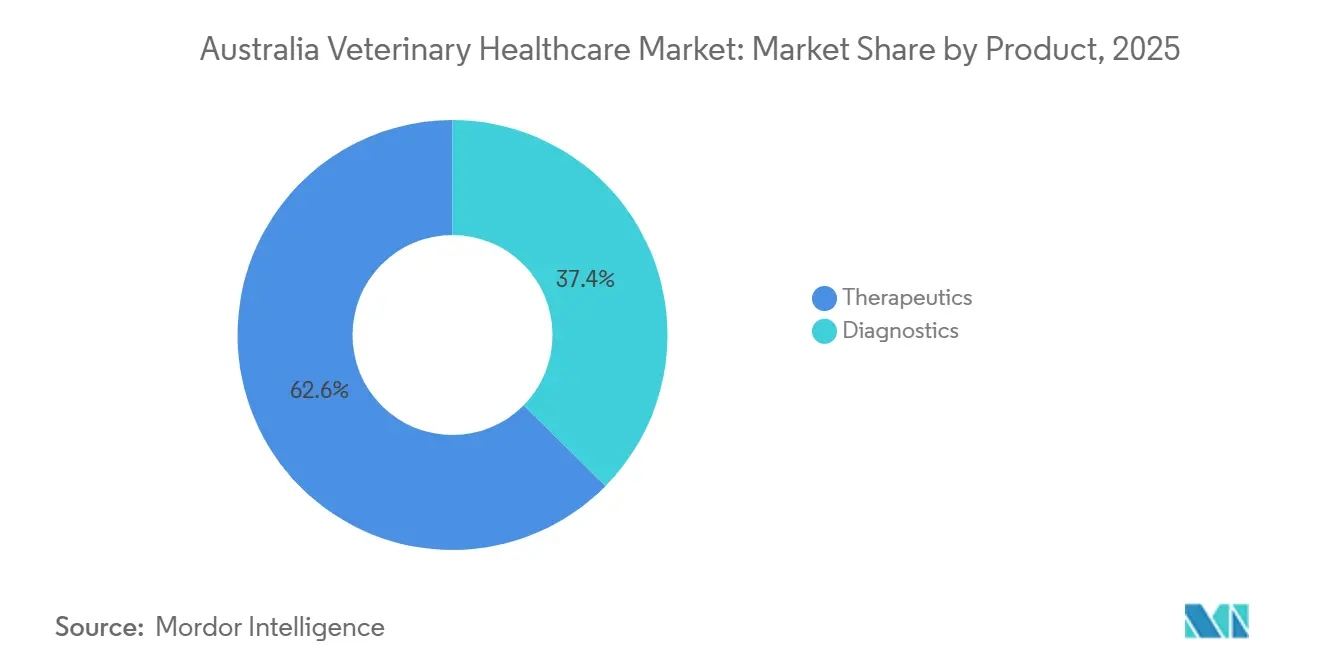

- By product, therapeutics led with 62.55% of the Australian veterinary healthcare market share in 2025. Diagnostics are projected to expand at a 9.85% CAGR through 2031, the fastest rate among all categories.

- By animal type, dogs and cats generated 45.53% revenue in 2025, while poultry is advancing at an 8.75% CAGR to 2031.

- By route of administration, parenteral products held a 47.15% share in 2025; oral formulations will expand at an 8.82% CAGR during the forecast period.

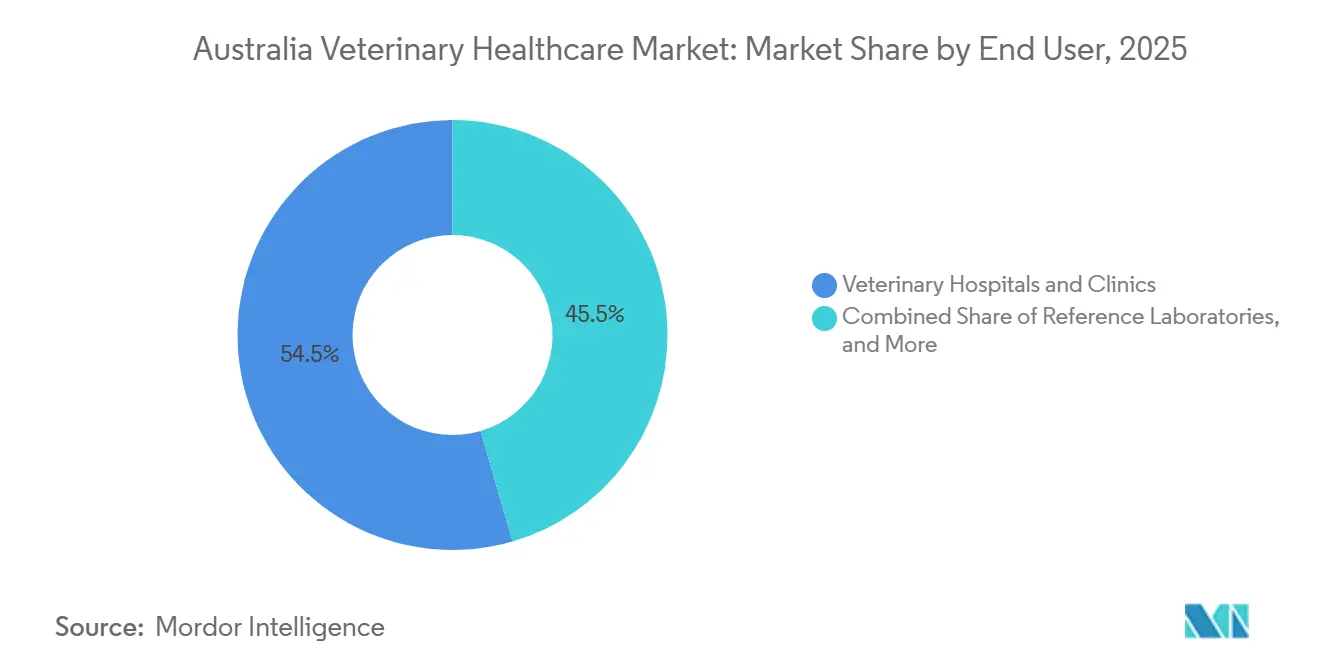

- By end user, veterinary hospitals and clinics accounted for 54.52% of spending in 2025, whereas point-of-care testing settings are rising at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Veterinary Healthcare Market Trends and Insights

Driver Impact Analysis*

| Driver | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Animal-Health Expenditure Among Pet Owners | +1.5% | Major metropolitan areas | Medium term (2-4 years) |

| Expansion of Livestock Export Volumes And Values | +1.3% | QLD, NSW, VIC | Long term (≥ 4 years) |

| Uptake of Advanced Diagnostics | +1.8% | National | Short term (≤ 2 years) |

| Growth in Pet-Insurance Penetration | +0.8% | National | Medium term (2-4 years) |

| APVMA Fast-Track Pathway for Biologics | +0.6% | National | Medium term (2-4 years) |

| Traceability-Linked Demand for eID Health Tech | +1.0% | Sheep-producing states | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Rising Animal-Health Expenditure Among Pet Owners

Households spend between AUD 1,500 and AUD 3,000 (USD 975 to USD 1,950) per pet per year, with veterinary care accounting for up to 20% of those outlays[2]Australian Veterinary Association, “Veterinary Workforce Survey 2024,” ava.com.au. Insurance penetration climbed by double digits in 2024-2025 and now covers nearly one in five animals, enabling costly interventions such as orthopedic surgery and oncology to proceed without liquidity constraints[3]Australian Veterinary Association, “Veterinary Workforce Survey 2024,” ava.com.au. Telehealth reimbursement lowers barriers to early diagnosis, and corporate wellness subscriptions lock in repeat visits by spreading fees across the year. These mechanisms stabilize clinic revenue and fund investments in diagnostics that reinforce the growth trajectory of the Australian veterinary healthcare market.

Expansion of Livestock Export Volumes and Values

Australia shipped 766,044 head of cattle and 433,078 sheep in 2024, underpinned by livestock product value of AUD 38.6 billion (USD 25.1 billion)[4]ABARES, “Agricultural Commodities Forecasts 2024-25,” agriculture.gov.au . Disease-free status is critical for market access, prompting producers to intensify vaccination and parasite-control programs. Climate volatility heightens parasite load, steering demand toward long-acting injectables and multivalent vaccines that align with extensive grazing practices. China’s reopening to additional Australian plants and Indonesia’s appetite for feeder cattle are expected to boost therapeutics consumption, reinforcing the Australian veterinary healthcare market outlook.

Uptake of Advanced Diagnostics

The April 2024 launch of IDEXX Catalyst One delivers 17-chemistry panels in 10 minutes, eliminating reference-lab delays. Zoetis followed with its AI-driven Vetscan OptiCell hematology platform in December 2024. Faster results improve care quality and allow clinics to capture revenue that would otherwise be ceded to external labs. Corporate chains standardize these analyzers across networks to optimize reagent procurement and technician training, thereby strengthening the profitability of the Australian veterinary healthcare market.

Traceability-Linked Demand for eID-Enabled Health Tech

Electronic identification became compulsory for sheep and goats born after 1 January 2025, with full-flock compliance due by 2027. The National Livestock Identification System database migration to Amazon Web Services supports real-time linkage between movement data and veterinary interventions. Federal and state subsidies covering tag and reader costs spur adoption, while software overlays convert compliance into predictive health analytics, an emerging revenue stream inside the Australian veterinary healthcare market.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Veterinary Services And Pharmaceuticals | –0.8% | National | Short term (≤ 2 years) |

| Stringent, Evolving Regulatory Processes | –0.4% | National | Long term (≥ 4 years) |

| Rural Workforce Shortages | –0.6% | Regional and remote areas | Long term (≥ 4 years) |

| Counterfeit and Grey-Market Medicines Online | –0.3% | National | Short term (≤ 2 years) |

| Source: ���ϲ����� | |||

High Cost of Veterinary Services and Pharmaceuticals

Consultation fees rose by 91% in 2024, pushing routine visits to AUD 80-150 (USD 52-98) and emergency care to AUD 200-500 (USD 130-325). Complex surgeries now exceed AUD 5,000 (USD 3,250), deterring price-sensitive owners and delaying care. Unregulated online channels market discounted, often unregistered drugs, siphoning revenue from legitimate suppliers and creating compliance risks. These pressures moderate near-term expansion of the Australian veterinary healthcare market.

Rural Workforce Shortages Limiting Service Access

One in three veterinary roles outside metropolitan areas remained vacant in 2025. Government incentives totaling AUD 10.6 million (USD 6.9 million) address relocation and loan forgiveness, yet professional isolation and limited career paths persist. Telemedicine offers triage support but cannot replace hands-on procedures, keeping service gaps wide and capping growth potential in livestock-intensive regions that otherwise would enlarge the Australian veterinary healthcare market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Diagnostics Capture Fastest Upside

Diagnostics started from a smaller base yet are growing at a 9.85% CAGR, outpacing therapeutics, which held 62.55% of the Australian veterinary healthcare market share in 2025. Point-of-care chemistry and hematology systems shorten turnaround to minutes and keep revenue in-house, lifting clinic profitability. Vaccines dominate therapeutics, with combination shots reducing visits and enhancing compliance. Parasiticides gain from tick range expansion, while antimicrobial stewardship tempers anti-infective use.

Diagnostic imaging remains capital-intensive, yet corporate chains deploy radiography and ultrasound to differentiate their services. Molecular PCR panels gained poultry traction amid avian-influenza vigilance, compressing detection from 48 hours to 4 hours and reinforcing demand across the Australia veterinary healthcare market.

By Animal Type: Poultry Leads Growth Curve

Dogs and cats accounted for 45.53% of 2025 revenue, reflecting high pet ownership, but poultry is forecast to grow at an 8.75% CAGR as biosecurity investments scale. Mandatory surveillance and hatchery vaccination protect a sector that produces 1.3 million tonnes of meat annually, anchoring the uptake of therapeutics and diagnostics. Equine and swine remain niche yet high-value, while sheep and goats benefit from electronic identification that tightens residue compliance, broadening opportunities across the Australia veterinary healthcare market size for these subsegments

By Route of Administration: Oral Formulations Gain Traction

Parenteral formats held 47.15% share in 2025, but oral products are rising at 8.82% CAGR as taste-masked chewables boost adherence. Long-acting injectables remain essential for large-scale cattle operations that require documented dosing for export certification. Spot-on topicals face scrutiny over environmental runoff, prompting label reviews. Continued improvements in palatability will increase oral uptake and diversify revenue in the Australian veterinary healthcare market.

By End User: Point-of-Care Testing Accelerates

Hospitals and clinics captured 54.52% spending in 2025, yet in-house testing sites are scaling at an 8.12% CAGR as analyzers replicate reference-lab menus at lower cost. Corporate consolidators standardize workflows to leverage reagent purchasing power, while academic centers focus on surveillance and research. Reference labs retain complex assays but must retool services to defend share amid the in-practice migration reshaping the Australia veterinary healthcare market.

Competitive Landscape

The Australia veterinary healthcare market reports moderate consolidation as private equity inflows chase scale economies and brand leverage. EQT’s acquisition of VetPartners in January 2025 created a 267-clinic network employing more than 1,300 veterinarians, intensifying bargaining power with suppliers and accelerating protocol standardization. Greencross, valued at USD 3.75 billion, evaluates an ASX relisting to unlock capital for digital initiatives and clinic refurbishments. U.K.-based CVS Group invested USD 82.5 million to secure 28 Australian sites, signaling continued cross-border interest in local assets.

Pharmaceutical manufacturers expand production footprints to secure supply sovereignty. Zoetis purchased a 21-acre plant in Melbourne in August 2024, doubling its vaccine output and aligning with government calls for domestic vaccine production. Technology vendors differentiate practices: 30% of clinicians now rely on AI diagnostics to shorten wait times and elevate accuracy, appealing to quality-conscious owners. Practice management software providers integrate compliance modules that ease APVMA documentation, lowering administrative burdens and sharpening competitive positioning.

White-space remains in remote service delivery. Telehealth triage, mobile surgical units, and subscription wellness plans aim to bridge clinician gaps in the outback while generating recurring revenue. Workforce initiatives focus on retention bonuses and mental health support to curb attrition. As consolidation continues, the Australia veterinary healthcare market will likely reach an equilibrium where a handful of corporate groups coexist with high-touch independents that command localized loyalty.

Australia Veterinary Healthcare Industry Leaders

Zoetis Inc

Merck Co. Inc.

Elanco Animal Health

Boehringer Ingelheim Animal Health

Virbac

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Regulator approved a first-in-class vaccine protecting koalas from chlamydia infections.

- February 2025: MiDOG Animal Diagnostics entered Australia with Exotic Vet Support to deploy its All-in-One Microbial Test for exotic and wildlife species.

Australia Veterinary Healthcare Market Report Scope

As per the scope of this report, the Australia veterinary healthcare market is growing, and it comprises therapeutic and diagnostic products and solutions for companion and farm animals. Companion animals can be tamed or adopted for companionship or as house/office guards, and farm animals are raised for meat and milk-related products. Companion animals include canines, felines, and equines. Farm animals include bovine, poultry, and porcine.

The Australia veterinary healthcare market segmentation includes product, animal type, route of administration, and end user. By product, the market is segmented into therapeutics (vaccines, parasiticides, anti-infectives, medical feed additives, and other therapeutics) and diagnostics (point-of-care testing devices, clinical chemistry, diagnostic imaging, molecular diagnostics, and immunodiagnostic tests). By animal type, the market is segmented into dogs and cats, horses, swine, poultry, and others. By route of administration, the market is segmented into oral, parenteral, topical, and others. By end user, the market is segmented into veterinary hospitals & clinics, reference laboratories, point-of-care / in-house testing settings, and academic & research institutes. The report offers the value (in USD) for the above segments.

By Product

| Therapeutics | Vaccines |

| Parasiticides | |

| Anti-Infectives | |

| Medical Feed Additives | |

| Other Therapeutics | |

| Diagnostics | Immunodiagnostic Tests |

| Molecular Diagnostics | |

| Diagnostic Imaging | |

| Clinical Chemistry | |

| Point-of-Care Testing Devices |

By Animal Type

| Dogs and Cats |

| Horses |

| Swine |

| Poultry |

| Other Animal Types |

By Route of Administration

| Oral |

| Parenteral |

| Topical |

| Others |

By End User

| Veterinary Hospitals & Clinics |

| Reference Laboratories |

| Point-of-Care / In-House Testing Settings |

| Academic & Research Institutes |

| By Product | Therapeutics | Vaccines |

| Parasiticides | ||

| Anti-Infectives | ||

| Medical Feed Additives | ||

| Other Therapeutics | ||

| Diagnostics | Immunodiagnostic Tests | |

| Molecular Diagnostics | ||

| Diagnostic Imaging | ||

| Clinical Chemistry | ||

| Point-of-Care Testing Devices | ||

| By Animal Type | Dogs and Cats | |

| Horses | ||

| Swine | ||

| Poultry | ||

| Other Animal Types | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| Others | ||

| By End User | Veterinary Hospitals & Clinics | |

| Reference Laboratories | ||

| Point-of-Care / In-House Testing Settings | ||

| Academic & Research Institutes | ||

Key Questions Answered in the Report

How fast is the Australia veterinary healthcare market growing?

The market is expanding at 7.36% CAGR between 2026 and 2031, moving from USD 1.39 billion in 2026 to USD 1.98 billion by 2031.

Which product category is expanding the quickest?

Diagnostics are projected to grow at 9.85% CAGR through 2031, driven by point-of-care analyzers and molecular tests.

What animal segment shows the highest future growth?

Poultry health solutions are forecast to increase at 8.75% CAGR due to heightened biosecurity and surveillance spending.

Why are oral formulations gaining share?

Palatability innovations in chewable parasiticides improve adherence, pushing oral products toward an 8.82% CAGR.

How does traceability affect livestock health investment?

Mandatory electronic identification links movement data with treatment history, boosting demand for data analytics and compliance-driven therapeutics.

Which companies are leading consolidation of veterinary clinics?

CVS Group and VetPartners, backed by private equity, are the most active consolidators, collectively controlling hundreds of practices nationwide.

Page last updated on: