Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

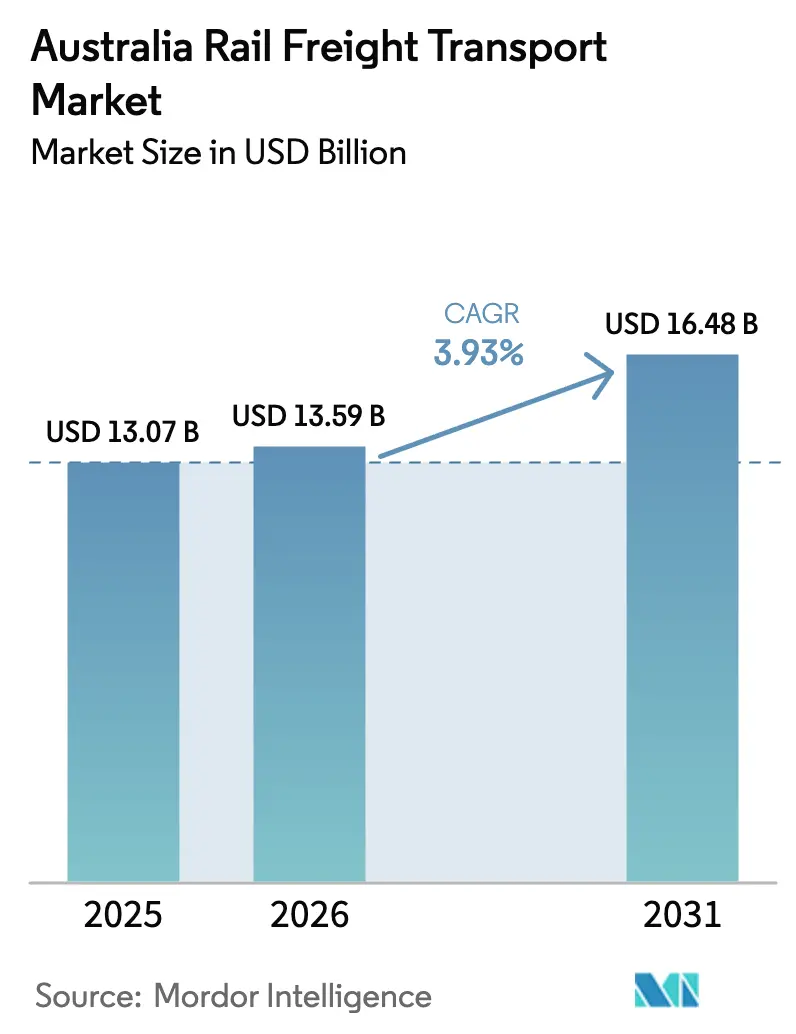

| Base Year Market Size (2025) | USD 13.07 Billion |

| Market Size (2026) | USD 13.59 Billion |

| Market Size (2031) | USD 16.48 Billion |

| Growth Rate (2026 - 2031) | 3.93% CAGR |

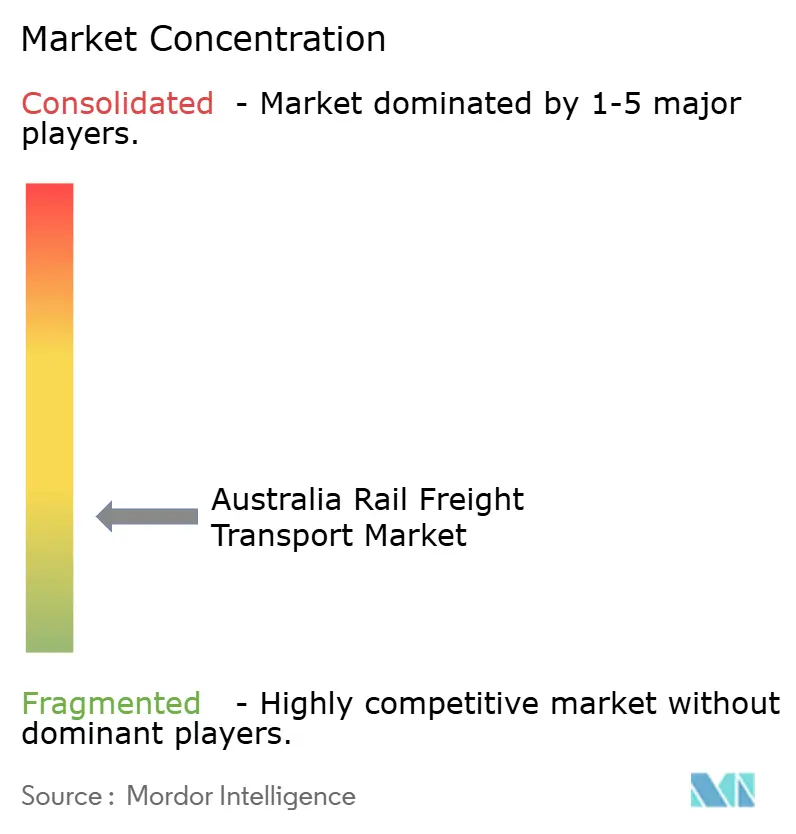

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. | |

Australia Rail Freight Transport Market Analysis by ���ϲ�����

The Australia Rail Freight Transport Market size is expected to grow from USD 13.07 billion in 2025 to USD 13.59 billion in 2026 and is forecast to reach USD 16.48 billion by 2031 at a 3.93% CAGR over 2026-2031.

Rising battery-mineral exports, decisive federal access reform, and technology-enabled service models are widening the revenue base of the Australia rail freight transport market. Regulatory changes that lower below-rail charges are improving modal economics, while strong long-term haulage contracts signed by miners shield operators from commodity price swings. Cost overruns on Inland Rail and climate-related insurance pressure remain material headwinds; however, distributed intermodal precincts and 24/7 metro freight windows are unlocking fresh volume pools. Competitive intensity is shifting toward data-rich, integrated logistics offerings that embed rail within door-to-door solutions rather than stand-alone haulage.

Key Report Takeaways

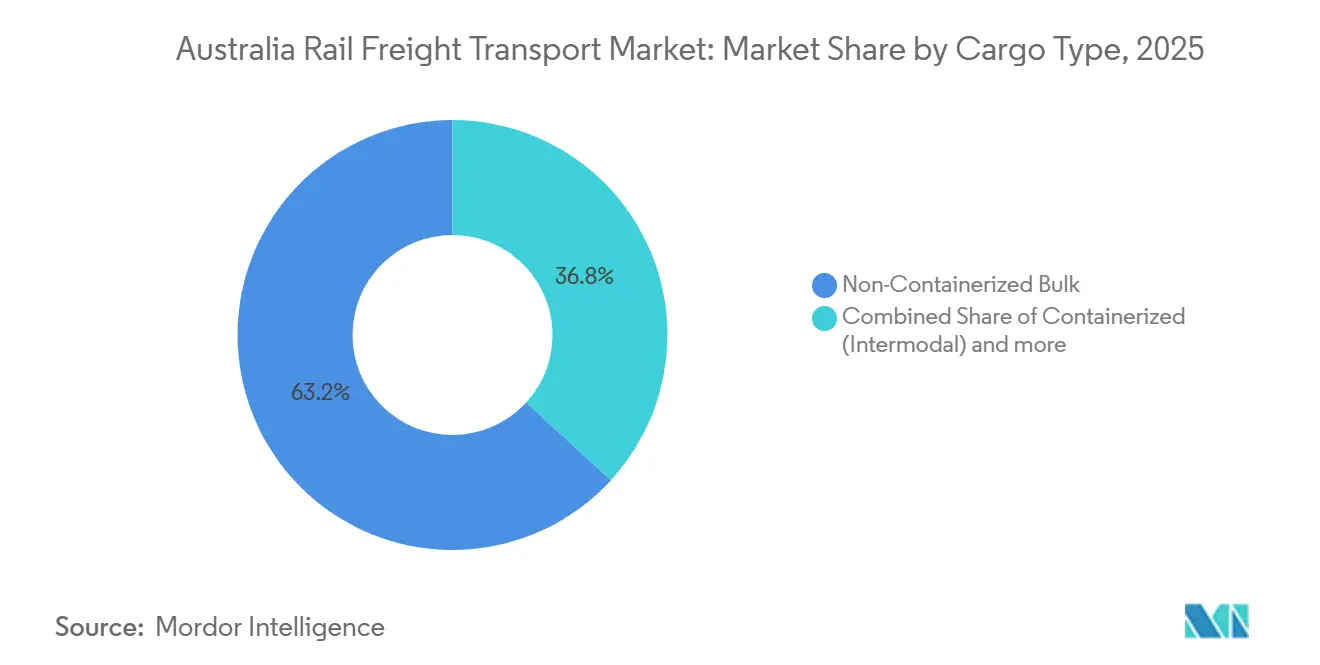

- By cargo type, non-containerized bulk held 63.2% of Australia rail freight transport market share in 2025, while containerized intermodal is forecast to expand at 4.26% CAGR to 2031.

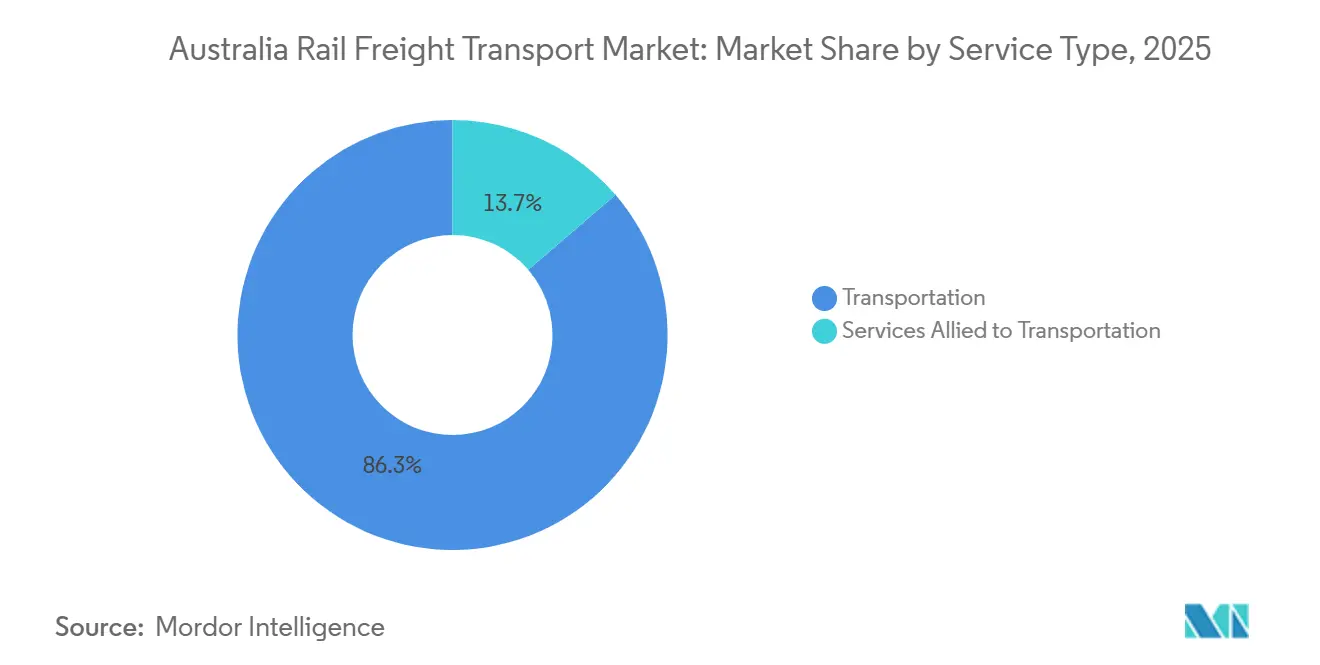

- By service type, transportation services commanded 86.3% share of the Australia rail freight transport market size in 2025 and services allied to transportation are advancing at a 4.60% CAGR through 2031.

- By operational scope, interstate freight corridors accounted for 81.5% share in 2025, whereas port-linked import movements show the fastest growth at 4.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Rail Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth in battery-minerals exports | +1.1% | Western Australia, Queensland, Northern Territory | Medium term (2-4 years) |

| Federal rail access reform lowering charges | +0.7% | National interstate corridors | Short term (≤ 2 years) |

| 24/7 urban freight window | +0.4% | Sydney, Melbourne, Brisbane metro areas | Medium term (2-4 years) |

| Supply-chain resilience funding for hubs | +0.6% | Regional NSW, Queensland, Victoria | Long term (≥ 4 years) |

| Take-or-pay haulage contracts | +0.8% | Queensland, Western Australia, Hunter Valley NSW | Medium term (2-4 years) |

| Blockchain cargo-visibility platforms | +0.3% | National, containerized freight focus | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

Explosive Growth in Battery-Minerals Exports

Australia produced 88,000 tonnes of lithium carbonate equivalent in 2023-24, equal to 47% of global supply, and this surge is redirecting train paths from iron ore toward battery-grade minerals. Rail operators secure multiyear lithium haulage contracts that lock in volumes well beyond 600-kilometer thresholds where road loses cost advantage. The Critical Minerals Strategy names rail as essential infrastructure, channeling capital toward new spurs in the Goldfields and North West Minerals Province. Diversification into rare earths reduces dependence on coal, anchors fresh revenue streams, and lengthens asset life cycles for the Australia rail freight transport market[1]“Resources and Energy Quarterly: March 2024,” Department of Industry, INDUSTRY.GOV.AU .

Federal Rail Access Reform Lowering Charges

The 2024 Interstate Access Undertaking supervised by the ACCC aims to trim below-rail fees by up to 20%, addressing cost opacity that historically skewed freight toward road. Transparency boosts investor confidence and encourages private upgrades on the Australian Rail Track Corporation spine. A parallel draft undertaking in Queensland signals state alignment, reinforcing national consistency on pricing. Lower access costs raise profit margins and bolster the competitive stance of the Australia rail freight transport market on east-west and north-south lanes[2]“Interstate Rail Network Access Undertaking,” Australian Competition and Consumer Commission, ACCC.GOV.AU.

24/7 Urban Freight Window

Noise-mitigation technology drops emissions by 10-15 decibels, unlocking overnight rail slots into dense metro zones that historically enforced curfews. The Port of Melbourne moves only 5.8% of its 3.4 million containers by rail, in part due to time restrictions. Extended windows allow rail to capture e-commerce and perishables that demand flexible schedules, increasing wagon turns and network utilisation across the Australia rail freight transport market.

Supply-Chain Resilience Funding for Hubs

The federal Supply-Chain Resilience initiative channels USD 50 million into Wagga Wagga’s 95-hectare intermodal precinct, creating inland consolidation points that relieve metropolitan terminals. Moorebank’s 240-hectare site is projected to remove 3,000 truck trips a day from Sydney roads, providing USD 11 billion of long-run economic gains. Distributed hubs shorten dray distances, cut empty repositioning, and broaden the service reach of the Australia rail freight transport market into regional catchments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inland Rail schedule blow-outs | -0.8% | Queensland, NSW, Victoria corridor | Long term (≥ 4 years) |

| Rising rolling-stock insurance premiums | -0.4% | National, bushfire-exposed corridors | Short term (≤ 2 years) |

| Port Botany and Kwinana slot congestion | -0.6% | Sydney, Perth metro areas | Medium term (2-4 years) |

| Electric B-double road trains on 600 km hauls | -0.5% | National, short-haul routes | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Inland Rail Schedule Blow-Outs

Inland Rail's budget surged to USD 31.4 billion, and ongoing legal challenges are pushing its substantial completion date past 2031. These delays threaten to hand over growth opportunities to trucks and undermine investor confidence in Australia's ambitious rail freight expansion. The increasing costs and extended timelines highlight significant challenges in executing large-scale infrastructure projects within the Australia rail freight transport market. Additionally, the prolonged uncertainty could impact the competitive positioning of rail freight against other modes of transport, further complicating the market dynamics[3]“Critical Minerals Strategy 2023-2030,” Department of Industry, INDUSTRY.GOV.AU .

Rising Rolling-Stock Insurance Premiums

As bushfire risks surge, cover costs have risen by 20-30%. This shift compels operators to shoulder higher deductibles through self-insurance, diverting capital from growth initiatives. The increased financial burden is particularly challenging for smaller carriers, who often lack the resources to absorb such costs. This strain may lead to a reduction in their operational capacity or force them to exit the market entirely. Consequently, the Australia rail freight transport market could witness accelerated consolidation, as larger players acquire smaller, struggling operators to expand their market share and strengthen their competitive position[4]“Freight Projects – Port Rail Shuttle,” Victoria State Government, VIC.GOV.AU.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Allied Services Move Up the Value Chain

Transportation services captured 86.3% of the Australia rail freight transport market size in 2025. Core haulage remains essential, but operators increasingly bundle maintenance, customs, and warehousing into single contracts. Pacific National’s USD 594 million locomotive maintenance agreement with UGL reflects vertical integration that deepens client stickiness.

Services allied to transportation are growing at a 4.60% CAGR through 2031, fuelled by Qube’s AUD 600 million bond that funds port logistics and intermodal terminals. Integrated offerings capture a greater wallet share and protect margins, marking a structural pivot in the Australia rail freight transport market toward solution-based competition.

By Cargo Type: Bulk Dominance Meets Container Expansion

Non-containerized bulk generated 63.2% of Australia rail freight transport market share in 2025 as iron ore, coal, and grain remain the backbone of long-haul operations. Bulk flow resilience is anchored by take-or-pay contracts, with Rio Tinto’s Pilbara system lifting volumes quickly after cyclone disruptions.

Containerized intermodal freight is advancing at a 4.26% CAGR, supported by e-commerce growth and digitised supply chains. Rail currently carries just 5.8% of Melbourne’s container flow, yet the Port Rail Shuttle Network aims to triple the modal share through 24/7 access and inland hubs. Blockchain visibility and faster metro slots will position rail to absorb rising import volumes, signalling that container services will be the next profit frontier for the Australia rail freight transport market.

By Operational Scope: Port Connectivity Sets the Pace

Interstate corridors provided 81.5% of the 2025 value, driven by east-west mineral flows and the Brisbane-Sydney-Melbourne consumer axis. The Australia rail freight transport market size for interstate moves is forecast to rise steadily as battery minerals add fresh tonnage.

Port-linked import movements record the fastest 4.1% CAGR, encouraged by on-dock rail investments at Port Botany and Fremantle that trim truck kilometres. Accelerated port connectivity improves container dwell times, providing a competitive wedge for the Australia rail freight transport market against road on coastal supply chains.

Intrastate corridors remain vital for agricultural and construction materials, yet face stiff road competition on shorter hauls. Enhanced high-capacity signalling in Perth lifts intrastate efficiency, partially offsetting the truck advantage.

Geography Analysis

Western Australia dominates bulk rail due to Pilbara iron ore and rising lithium exports. DP World will invest USD 600 million across four Australian terminals by 2028, including a USD 10.5 million rail interchange at Fremantle that removes 15,000 truck trips each year. A USD 1.1 billion signalling upgrade expands Perth network capacity by 40% and benefits bulk as well as container flows, reinforcing the strategic weight of Western Australia in the Australia rail freight transport market.

Queensland leverages USD 22.9 billion of fiscal 2024-25 infrastructure spending that covers the Direct Sunshine Coast Rail Line and new rolling-stock manufacturing. Coal remains pivotal, yet rare earth and agricultural exports diversify volumes. Inland Rail delays restrain potential, but alternative Toowoomba-to-Gladstone links aim to secure port access for regional shippers.

New South Wales acts as the critical junction in the Australia rail freight transport market. The Moorebank terminal removes 3,000 daily truck runs and underpins a new logistics ecosystem for Sydney. However, Port Botany rail bottlenecks limit immediate scale-up. Victoria focuses on the Port of Melbourne, where container throughput hit 3.4 million units in 2025, yet rail modal share remains below 6% as suburban shuttle projects lag.

South Australia and Northern Territory provide essential north-south connectivity, while Tasmania relies on sea links but still benefits from rail for forestry and agriculture. The Trans-Australian Railway will receive more than USD 1 billion in weatherproofing to avert USD 320 million disruption losses observed in 2022. Regional hubs such as Wagga Wagga anchor future inland connectivity, rounding out the spatial picture of the Australia rail freight transport market.

Competitive Landscape

Aurizon Holdings and Pacific National together control about 70% of above-rail volume, giving the Australia rail freight transport market a moderate concentration structure. Aurizon’s proposed acquisition of Flinders Logistics has drawn regulator attention for potential foreclosure in South Australia. Pacific National pursues fleet modernisation through its USD 594 million locomotive service deal that lengthens asset life and boosts reliability.

Second-tier specialists, including SCT Logistics and Qube, focus on intermodal and port drayage niches. Qube’s AUD 600 million bond finances terminal expansion and technology upgrades that improve end-to-end visibility. Digital transformation is the new battleground; Western Australia’s high-capacity signalling shows how tech investment lifts throughput without extra track.

Sustainability positions influence bids for new contracts. Aurizon pilots battery-electric locomotives under a USD 6.3 million ARENA grant, seeking to lock in low-carbon haulage deals. Toll Group’s electric truck rollout threatens rail on short hauls, signalling that rail carriers must pair decarbonisation with service flexibility to defend share in the Australia rail freight transport market.

Australia Rail Freight Transport Industry Leaders

Aurizon Holdings Limited

Pacific National Holdings Pty Ltd

Southern Shorthaul Railroad

SCT Logistic

KTI Transport

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: SCT Logistics gained funding to link its Altona site to the shuttle network.

- January 2025: NSW Ports commenced Stage Two of its On-Dock Rail Investment Program at Port Botany to lift rail’s share of container moves.

- January 2025: DP World and NSW Ports invested AUD 400 million (USD 281 million) to expand the Port Botany rail terminal, doubling rail container capacity and enhancing freight throughput.

- December 2024: Qube issued AUD 600 million unsecured notes to fund logistics growth.

Australia Rail Freight Transport Market Report Scope

By Service Type (Value, USD)

| Transportation |

| Services Allied to Transportation |

By Cargo Type (Value, USD)

| Containerized (Intermodal) | 20-foot TEU |

| 40-foot TEU | |

| Non-Containerized Bulk | Iron Ore |

| Coal | |

| Grain | |

| Other Minerals and Commodities | |

| Liquid Bulk | Petroleum and Fuel |

| Chemicals | |

| Other Liquids |

By Operational Scope (Value, USD)

| Intrastate and Interstate Freight Corridors | Interstate Corridors |

| Intrastate Movements | |

| Port-Linked Freight Movements | Export to Port |

| Import from Port |

| By Service Type (Value, USD) | Transportation | |

| Services Allied to Transportation | ||

| By Cargo Type (Value, USD) | Containerized (Intermodal) | 20-foot TEU |

| 40-foot TEU | ||

| Non-Containerized Bulk | Iron Ore | |

| Coal | ||

| Grain | ||

| Other Minerals and Commodities | ||

| Liquid Bulk | Petroleum and Fuel | |

| Chemicals | ||

| Other Liquids | ||

| By Operational Scope (Value, USD) | Intrastate and Interstate Freight Corridors | Interstate Corridors |

| Intrastate Movements | ||

| Port-Linked Freight Movements | Export to Port | |

| Import from Port | ||

Key Questions Answered in the Report

What is the current value of the Australia rail freight transport market?

The market is valued at USD 13.59 billion in 2026 and is on track to reach USD 16.48 billion by 2031.

Which cargo type contributes most to Australian rail freight revenue?

Non-containerized bulk such as iron ore, coal, grain, and lithium provides 63.2% of 2025 revenue.

How fast is containerized rail freight growing in Australia?

Containerized intermodal services are expanding at 4.26% CAGR through 2031, outpacing bulk growth.

What regulatory change most benefits rail operators right now?

The ACCC-supervised Interstate Access Undertaking is lowering below-rail charges and improving pricing transparency.

How will Inland Rail delays affect freight flows?

Schedule overruns shift near-term growth toward coastal corridors, but completion will eventually shorten Melbourne–Brisbane transit times to under 24 hours.

Page last updated on: