China-Europe Rail Freight Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

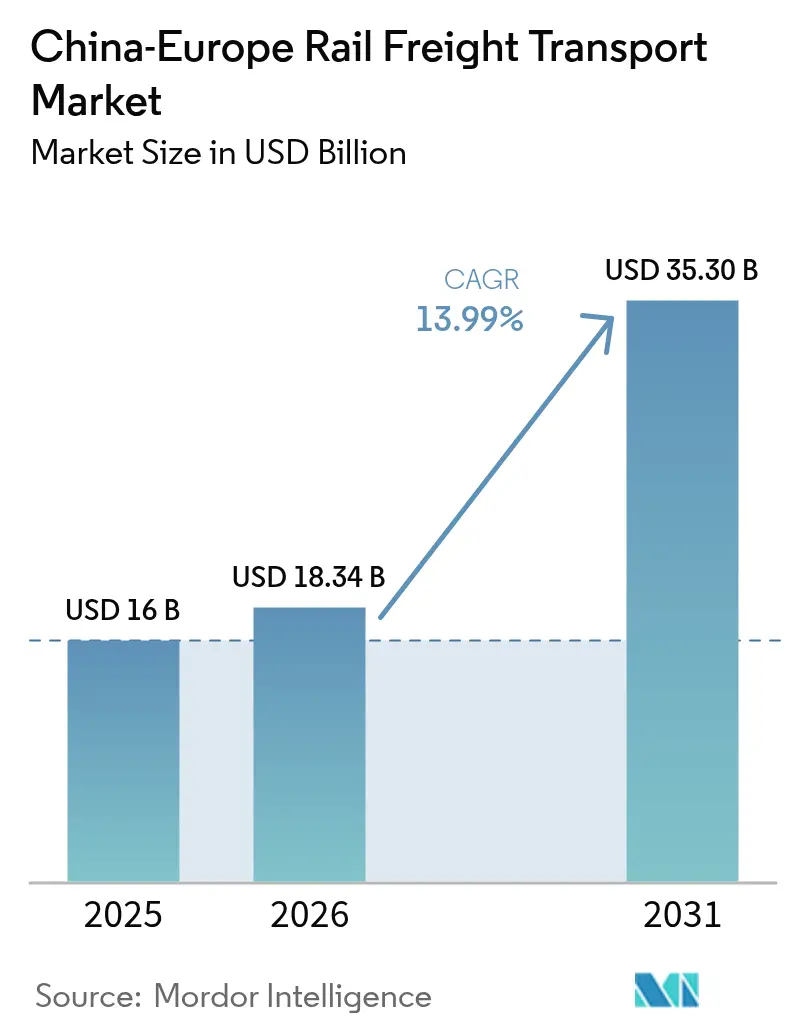

| Base Year Market Size (2025) | USD 16 Billion |

| Market Size (2026) | USD 18.34 Billion |

| Market Size (2031) | USD 35.30 Billion |

| Growth Rate (2026 - 2031) | 13.99% CAGR |

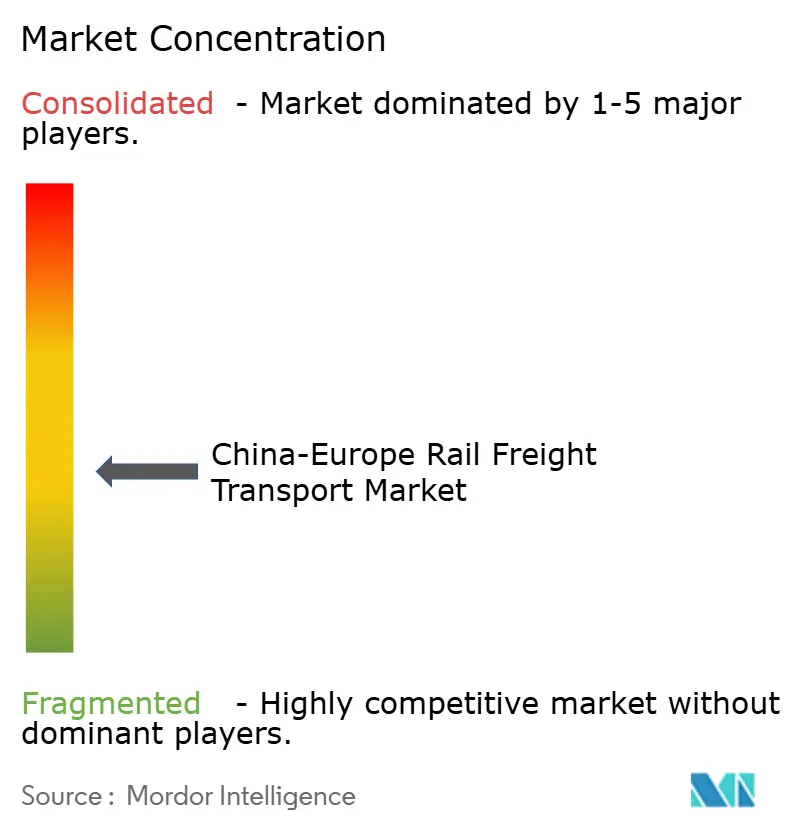

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © ���ϲ�����. Reuse requires attribution under CC BY 4.0. |

|

China-Europe Rail Freight Transport Market Analysis by ���ϲ�����

The China-Europe rail freight transport market size is projected to be USD 16.00 billion in 2025, USD 18.34 billion in 2026, and reach USD 35.30 billion by 2031, growing at a CAGR of 13.99% from 2026 to 2031.

A regulatory pivot toward zero-emission freight quotas, the scheduled commissioning of the Tehran–Van–Sofia spur, and corridor-wide artificial-intelligence deployment are driving structural demand that outpaces historic growth patterns. Transit-time variance has already fallen below 5%, transforming rail into a predictable option for high-value electronics that once moved mainly by air. Simultaneously, guaranteed agri-bulk block-train contracts stabilize eastbound volumes, improving bi-directional utilization rates that historically distorted pricing. These intertwined forces expand the customer base from cost-sensitive shippers to companies prioritizing carbon accounting, reliability, and end-to-end digital visibility.

Key Report Takeaways

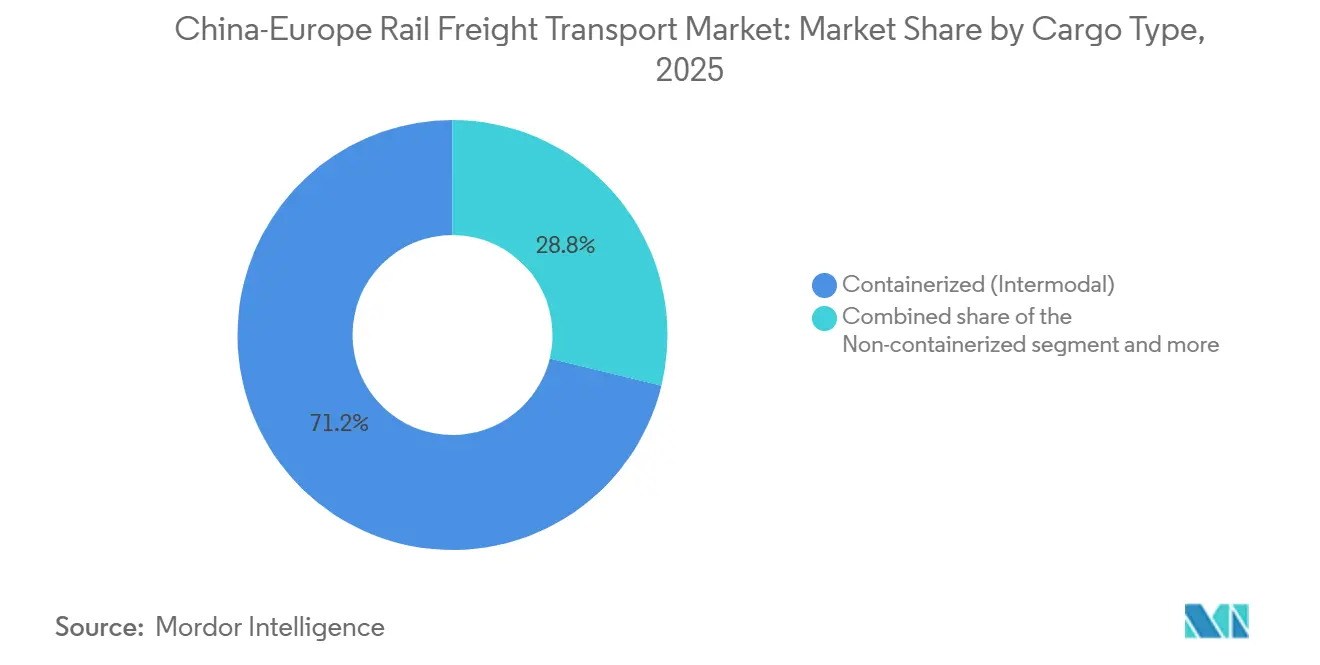

- By cargo type, containerized intermodal freight led with 71.21% of China-Europe rail freight transport market share in 2025, while non-containerized cargo is forecast to advance at a 14.23% CAGR through 2031.

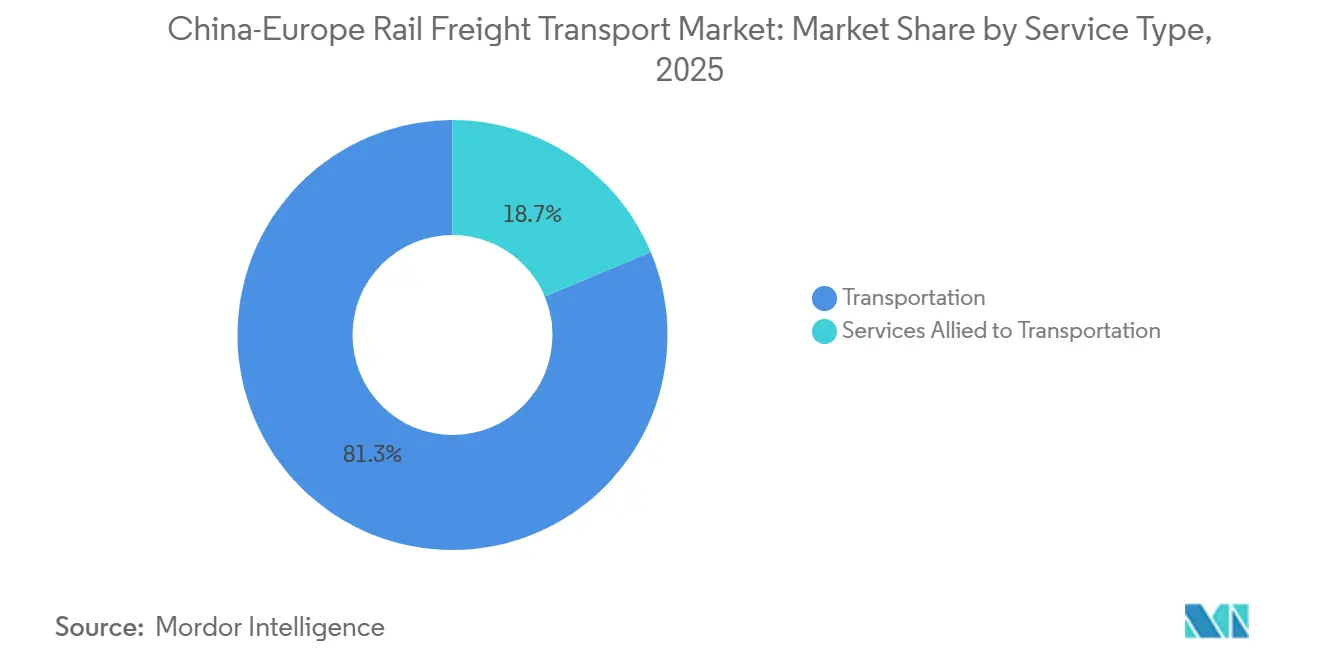

- By service type, transportation accounted for 81.3% of the China-Europe rail freight transport market size in 2025, yet services allied to transportation are projected to expand at 14.33% CAGR between 2026-2031.

- By European destination, Germany captured 29.5% share of the China-Europe rail freight transport market size in 2025, whereas Spain is set to register the fastest growth at 14.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China-Europe Rail Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU–China Zero-Emission Freight Quota (2030): Accelerating Rail Adoption | +3.1% | EU member states, extending to China coastal export hubs | Medium term (2-4 years) |

| Completion of Tehran–Van–Sofia Spur Unlocking Southern Throughput | +2.6% | Iran, Turkey, Bulgaria corridor with spillover to Central Europe | Short term (≤ 2 years) |

| AI-Optimized Network Timing Reducing Transit Variability to <5% | +2.3% | Global, concentrated in digitally advanced corridors | Medium term (2-4 years) |

| Direct Rail Access to Xi'an Semiconductor Valley Export Base | +1.9% | China Western regions, European high-tech manufacturing hubs | Long term (≥ 4 years) |

| 2026 Tri-Modal Poznań Mega-Hub Doubling EU Distribution Capacity | +1.7% | Poland, with distribution reach across Central and Eastern Europe | Short term (≤ 2 years) |

| Guaranteed COFCO Agri-Bulk Block-Train Contracts (5 Mt per year) Stabilizing Eastbound Loads | +1.4% | China agricultural import regions, European grain export zones | Long term (≥ 4 years) |

| Source: ���ϲ����� | |||

EU-China Zero-Emission Freight Quota (2030)

Mandatory carbon-reduction targets raise rail’s competitive appeal by lowering lifecycle emissions 70-80% below maritime benchmarks, aligning with China’s 2030 peak-emission pledge and the EU Corporate Sustainability Reporting Directive. Rail consequently shifts from a cost-alternatives role to a compliance imperative for multinationals disclosing Scope 3 emissions. Freight forwarders now price carbon surcharges into modal comparisons, pushing time-sensitive yet green-oriented shippers toward rail despite higher tariffs[1]“Rail Transport and Alternative Fuels for Sustainable Mobility in Europe,” European Commission, transport.ec.europa.eu.

Completion of Tehran–Van–Sofia Spur Unlocking Southern Throughput

The new link trims average transit to 14-16 days, sidesteps Northern Corridor congestion, and boosts annual capacity toward 3 million TEU by 2027. Customs digitalization and gauge-standardization investment cut border dwell times, giving shippers alternative routings that dilute geopolitical risk exposure and balance European gateway pressure[2]“Nation's Rail Network Continued to Break Records in 2024,” Government of China, english.www.gov.cn .

AI-Optimized Network Timing Reducing Transit Variability to Lesser Than 5%

China Railway’s 95306 platform applies predictive analytics on weather, congestion, and equipment maintenance to fine-tune dispatch plans, shrinking variance to levels that rival air cargo predictability. The resulting reliability unlocks premium pricing for guaranteed-delivery windows, especially in automotive electronics where inventory-carrying costs outstrip freight-rate differentials.

Direct Rail Access to Xi'an Semiconductor Valley Export Base

Dedicated tracks, temperature-controlled containers, and GPS-secured convoys let semiconductor exporters capture 40-50% freight savings versus air while meeting 16-18-day delivery commitments. Rail, therefore, carves out a share in the high-value electronics lane that once appeared irrevocably congested by aviation.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Termination of Chinese provincial rail-freight subsidies | -2.1% | China provincial export hubs, particularly inland manufacturing regions | Short term (≤ 2 years) |

| Security-insurance surcharges from Ukraine-conflict rerouting | -1.6% | Routes through Russia, Belarus, and alternative corridors | Medium term (2-4 years) |

| Locomotive shortages driven by lingering chip supply crunch | -1.3% | Global, with acute impacts on European and Chinese operators | Short term (≤ 2 years) |

| Escalating cyber-attacks on rail IT networks disrupting services | -0.9% | Digitally integrated corridors with centralized control systems | Medium term (2-4 years) |

| Source: ���ϲ����� | |||

Termination of Chinese Provincial Rail-Freight Subsidies

As subsidies phase out, landed costs rise by 8-12%, exposing genuine price disparities between ocean and rail transport. While rail transport remains a viable option for goods valued over USD 5,000 per tonne, it faces the risk of losing some marginal volumes to maritime alternatives. This shift could continue until rail operations achieve efficiencies that counterbalance the financial challenges[3]“Poland Logistics Hub Development Project,” European Investment Bank, eib.org.

Security-Insurance Surcharges from Ukraine-Conflict Rerouting

Commodity shippers, already grappling with thin margins, now face a significant challenge as war-risk premiums have surged to absorb 3-5% of total freight costs, a figure that is four times the norms established before the conflict. Adding to this strain, the Middle Corridor's capacity constraints, coupled with emerging insurance frameworks, heighten uncertainty and decelerate the pace of contract renewals[4]“Critical Information Infrastructures and Services – Rail,” European Union Agency for Cybersecurity, enisa.europa.eu.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cargo Type: Intermodal Standardization Drives Efficiency

The containerized segment controlled 71.21% of the China-Europe rail freight transport market share in 2025 as ISO standards enable automated handoffs across the 11,000-km corridor. Container pools coordinated through digital twins elevate chassis utilization, while predictive maintenance slashes idle times. Non-containerized cargo, though smaller, is forecast to outpace overall corridor growth at 14.23% CAGR, propelled by machinery, project cargo, and automotive knock-down kits requiring bespoke loading frames.

Liquid bulk remains niche, serving chemicals and refined fuels that value rail’s sealed-tanker safety record. Temperature-controlled containers now penetrate pharmaceutical and perishables lanes, their IoT telematics assuring cold-chain integrity over the 16-18-day transit. As rail hardware suppliers introduce wider-gauge adjustable wagons and faster bogie-exchange systems, oversized cargo handling hurdles ease, inviting higher-margin industrial equipment to migrate from sea to rail. The China-Europe rail freight transport market, therefore, evolves from container dominance toward a balanced portfolio that maximizes asset turns across diverse load profiles.

By Service Type: Allied Services Capture Value-Added Opportunities

Core transportation secured 81.3% of 2025 revenue, yet allied services are on track for a 14.33% CAGR through 2031, more than one percentage point above the corridor average. End-to-end visibility, automated customs brokerage, and inventory financing allow providers to capture logistics spend otherwise diffused across multiple vendors.

Digitally integrated warehousing at Duisburg and Poznań shortens order-to-delivery cycles, supporting just-in-time manufacturing partners in automotive and electronics. The 95306 platform’s API links shorten billing cycles from weeks to days, enhancing cash flow for SMEs. As customers seek single-invoice experiences, rail operators vertically integrate last-mile delivery, reverse logistics, and trade-documentation services, improving stickiness and raising average revenue per TEU. The China-Europe rail freight transport market thus rewards firms that transition from haulage to holistic supply-chain orchestration.

Geography Analysis

Germany’s leadership in 2025 derived from Duisburg’s advanced intermodal yard, 24-hour customs presence, and direct links to 90+ Chinese origins. However, capacity utilization routinely exceeded 90% during peak seasons, exposing the network to congestion risk. Poland’s Poznań hub eases that strain, doubling Central-European distribution capacity in 2026 and lowering cost-to-serve for manufacturers clustered along the Baltic-Adriatic corridor.

Spain’s ascent connects rail directly to Iberian automotive assembly plants and Mediterranean ports, cutting lead times for shipments bound for North Africa and Southern Europe. The Netherlands channels high-density consumer-goods volumes via rail-sea transshipment at Rotterdam, leveraging well-developed cold-chain capacity for pharmaceuticals. France capitalizes on high-value aerospace components that prize the corridor’s lower carbon footprint, offsetting longer transit versus air.

The extended EU transport funding of over EUR 7 billion earmarked for rail projects supports modernization across Southeastern Europe, bringing emerging markets such as Hungary and Slovakia into direct corridor access. Alternative routings through the Middle Corridor diversify geopolitical exposure, while digital customs pre-clearance harmonizes paperwork, reducing delays at external EU borders. Collectively, these developments disperse flows, lower systemic risk, and enhance service versatility for cargo owners across Europe.

Competitive Landscape

Incumbents rely on scale, cross-border agreements, and technology. China Railway Group coordinates 232 European destinations with unified scheduling, while CRRC supplies multi-system locomotives that traverse varying voltages without changeover stops. DB Cargo Eurasia integrates 18 European countries into DB’s network, capitalizing on its domestic wagon fleet for last-mile distribution.

Vertical integration accelerates: DSV absorbed DB Schenker’s rail assets, aligning Asian origin networks with European terminal density. Logistics providers bundle customs brokerage, warehousing, and supply-chain financing, monetizing data generated from IoT-equipped wagons. AI-driven network-timing tools further differentiate service reliability, enabling premium pricing on guaranteed windows.

Subsidy withdrawal in China pressures capital-weak operators, spurring consolidation. Meanwhile, cybersecurity resilience emerges as a trust metric; carriers meeting NIS Directive standards win contracts from electronics and pharma shippers wary of data leaks. The corridor’s moderate concentration favors players able to fund locomotive acquisitions despite chip shortages, sustain cybersecurity upgrades, and secure bi-directional cargo contracts.

China-Europe Rail Freight Transport Industry Leaders

-

China Railway Corporation

-

DB Cargo (Deutsche Bahn AG)

-

UTLC ERA

-

Russian Railways (RZD)

-

Rail Cargo Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: China State Railway and partner railways unveiled capacity-expansion measures and streamlined customs to improve east–west balance.

- November 2025: China State Railway Group announced the network spans 232 European and 100 Asian cities, adding seven fully timetabled routes that cut transit times 30%.

- October 2025: DB Cargo Eurasia launched a Shanghai–Hamburg round-trip, expanding access to 18 European countries.

- January 2025: China’s State Council confirmed 19,000 trips in 2024 carrying 2 million TEU, pledging further Belt and Road collaboration.

China-Europe Rail Freight Transport Market Report Scope

| Containerized (Intermodal) |

| Non-containerized |

| Liquid Bulk |

| Transportation |

| Services Allied to Transportation |

| Germany |

| Poland |

| Netherlands |

| Spain |

| France |

| United Kingdom |

| Italy |

| Rest of Europe |

| By Cargo Type (Value) | Containerized (Intermodal) |

| Non-containerized | |

| Liquid Bulk | |

| By Service Type (Value) | Transportation |

| Services Allied to Transportation | |

| By European Destination Country (Value) | Germany |

| Poland | |

| Netherlands | |

| Spain | |

| France | |

| United Kingdom | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the China-Europe rail freight transport market in 2031?

It is forecast to reach USD 35.30 billion by 2031, expanding from USD 18.34 billion in 2026 at a 13.99% CAGR.

Which cargo type leads corridor revenue?

Containerized intermodal freight commanded 71.21% market share in 2025 due to standardized handling efficiencies.

Why is Spain the fastest-growing European destination?

Automotive exports, Mediterranean port linkages, and North African market access drive Spain’s 14.7% CAGR through 2031.

How are AI tools improving corridor reliability?

Predictive scheduling on China Railway’s 95306 platform has cut transit-time variance below 5%, enabling guaranteed delivery windows.

What restraint has the greatest near-term cost impact?

The phased termination of Chinese provincial subsidies is lifting freight rates 8-12% and may trim volume 15-20% until efficiencies offset costs.

Page last updated on: