Asia-Pacific Quinoa Seeds Market Analysis by ���ϲ�����

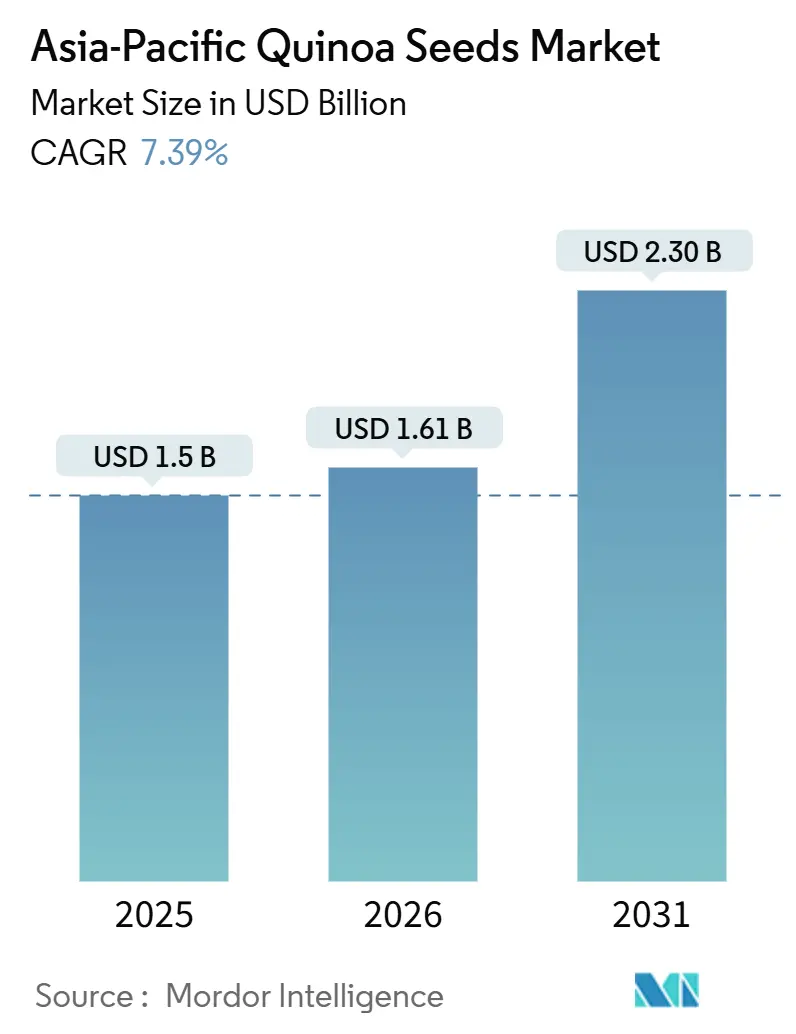

The Asia-Pacific quinoa seed market size was valued at USD 1.5 billion in 2025 and is estimated to grow from USD 1.61 billion in 2026 to USD 2.3 billion by 2031, at a CAGR of 7.39% during the forecast period (2026-2031). This market growth underscores a notable shift post-pandemic, with consumers gravitating towards gluten-free, plant-based proteins, spurred by urban buying trends and heightened institutional demand. China leads with over 100 registered enterprises, while India demonstrates the fastest growth, driven by policy-supported seed distribution and expanding e-commerce. Innovations in low-altitude, drought-resistant cultivars are not only mitigating agronomic risks but also expanding acreage in regions like Australia, northern China, and semi-arid India. Meanwhile, Japan and China are tightening residue limits through regulatory changes, increasing compliance costs but simultaneously benefiting certified organic supply chains. The competitive landscape in the downstream branded foods market is intensifying, driven by acquisitions and product innovations targeting price premiums. Meanwhile, public institutions maintain dominance in upstream breeding activities.

Key Report Takeaways

By geography, China led with 41% of the Asia-Pacific quinoa seed market share in 2025, while India is forecast to expand at a 12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using ���ϲ�����’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Quinoa Seeds Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and gluten-free diet adoption | +1.8% | China, Japan, and India (tier-1 & tier-2 cities) | Medium term (2-4 years) |

| Demand for plant-based proteins and superfoods | +1.5% | China, India, and Japan | Medium term (2-4 years) |

| Expansion of organic farming incentives | +1.2% | China (Gansu, Qinghai), India (Rajasthan, Karnataka), and Australia | Long term (≥4 years) |

| Rapid growth of e-commerce and modern retail | +1.0% | China, India, and Japan | Short term (≤2 years) |

| School nutrition programs integrating quinoa in China and India | +0.9% | China (national), India (pilot states) | Long term (≥4 years) |

| Breakthrough low-land, drought-tolerant quinoa cultivars | +1.0% | China (Shanxi, Gansu), India (Rajasthan), and Australia | Long term (≥4 years) |

| Source: ���ϲ����� | |||

Rising Health Consciousness And Gluten-Free Diet Adoption

Post-pandemic label scrutiny spurred demand for complete-protein grains, prompting a 22.2% jump in Japan’s 2024 quinoa imports and expanded shelf space in Chinese coastal supermarkets [1]Source: Ministry of Health, Labour and Welfare, “Food Sanitation Law Positive List,” jetro.go.jp . Urban Indian households, influenced by wellness influencers, replaced wheat in breakfast mixes with quinoa, reinforcing higher per-capita consumption. Provincial Chinese retailers further boosted credibility by promoting products certified under the nation’s organic logo, which mandates zero gluten contamination. Heightened consumer focus on micronutrients such as iron and magnesium keeps quinoa positioned as a premium “super grain.” Retailers across tier-1 and tier-2 cities continue to leverage gluten-free messaging to defend higher price points and margin structures [3].

Demand For Plant-Based Proteins And Superfoods

Quinoa’s 14-18% protein content and neutral flavor profile give formulators a competitive edge when designing dairy-alternative beverages. Nourish You’s millet-quinoa drink, launched in 2023 after two years of R&D with Indian institutes, illustrates technical success in creating shelf-stable, lactose-free options. Australian brand Keen Wah secured nationwide supermarket placement for quinoa granola by highlighting complete-protein credentials and low added sugars. Chinese snack makers now market puffed quinoa crisps rich in lysine, targeting parents concerned about children’s amino-acid intake. This convergence of functionality and marketing drives steady ingredient pull through the supply chain.

Expansion Of Organic Farming Incentives

China’s GB2763 residue list, extended to roughly 15,000 pesticides by 2025, raises compliance costs for conventional growers and tilts smallholders toward organic cultivation. Provincial subsidies in Gansu and Qinghai cover certification fees and soil tests, letting farmers access premium urban markets. India’s Agricultural and Processed Food Products Export Development Authority (APEDA) recorded that 52.8% of “other cereals” exports, including quinoa, headed to the United States in FY 2024, signaling lucrative returns for the United States Department of Agriculture (USDA)-aligned organic lots [3]Source: Tridge, “Asia-Pacific Quinoa Trade Dashboard,” tridge.com. Australia’s public-domain Kruso White variety generated rain-fed gross margins twice those of wheat at Geraldton, strengthening the business case for organic rotations [2]Source: Food Processing, “Australia’s Kruso White Variety Delivers Broadacre Potential,” foodprocessing.com.au. Collectively, these incentives lower entry barriers and guarantee price premiums that cushion farmers against volatility.

Rapid Growth Of E-Commerce And Modern Retail

Digital channels shrink geographic gaps, letting niche brands aggregate demand in cities lacking premium grocery stores. Bengaluru-based Healthy Buddha retails black quinoa at USD 4.05 per 500 g, a price consumers accept online due to perceived quality and convenience [3]. China’s Tmall health-food category ranks listings by origin and certification, increasing transparency and accelerating conversion among wellness shoppers. Japan’s food e-commerce penetration, while modest, is rising as seniors seek home-delivered specialty items, creating incremental volume for quinoa importers. Modern retailers complement online sales by offering private-label quinoa Stock Keeping Unit (SKU)s, often backed by supplier grants that lock in exclusive supply and assure scale.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs and yield variability outside Andes | -1.5% | Australia, China (low-altitude regions), and India | Medium term (2-4 years) |

| Supply-chain-driven price volatility | -1.2% | Asia-Pacific import-dependent markets | Short term (≤2 years) |

| Low consumer awareness beyond tier-1 metro areas | -0.8% | India (tier-3 cities, rural), inland China | Medium term (2-4 years) |

| Stringent residue and organic-audit regimes in China and Japan | -0.6% | China, Japan | Long term (≥4 years) |

| Source: ���ϲ����� | |||

High Production Costs And Yield Variability Outside Andes

Average yields in Australia hover at 1.5 metric tons/hectare, far below the 3 metric tons/hectare achieved with optimized Chilean germplasm, while Chinese trials show a spread from 0.5 metric tons/hectare to 5.1 metric tons/hectare, underscoring genotype-by-environment complexities [2]Source: Food Processing, “Australia’s Kruso White Variety Delivers Broadacre Potential,” foodprocessing.com.au. Dedicated processing lines for scarification and drying require high upfront capital, yet current regional volumes rarely fill capacity. Farmers, therefore, face compressed margins and hesitate to expand plantings. Without scale, processors cannot amortize equipment, perpetuating a cycle of under-investment. The result is a structural drag on supply growth across key Asia-Pacific agro-ecologies.

Supply-Chain-Driven Price Volatility

Peru and Bolivia still supply 72% of global exports, linking Asian prices to South American harvests and freight swings. Tridge data show 2024 spot quotes ranged from USD 2.45 to USD 6.58/kg before stabilizing near USD 6.00/kg in early 2025, a swing that complicates retailer promotions and processor costing. Japan’s 26% unit-price rise in 2024 reduced affordability despite modest volume growth. Volatility discourages long-term farmer contracts, forcing processors to rely on spot markets that may clear at unfavorable prices. This feedback loop constrains category expansion in cost-sensitive segments.

Geography Analysis

China accounted for 41% of the Asia-Pacific quinoa seed market size in 2025. China’s leadership in the Asia-Pacific quinoa seed market rests on widespread provincial cultivation, 100-plus processors, and a sophisticated e-commerce ecosystem that rapidly diffuses new health-food trends. Even so, stricter residue thresholds and labeling reforms incentivize local sourcing, compressing import needs and enhancing upstream margins for compliant domestic suppliers. Provincial subsidies for organic certification encourage a pivot toward premium positioning, buffering producers from commodity price swings.

India is the fastest-growing component of the Asia-Pacific quinoa seed market, advancing at a 12% CAGR through 2031. India’s growth trajectory depends on closing the agronomic yield gap, investing in scarification and washing infrastructure, and extending consumer education beyond top-tier metros. Seed-delivery schemes and mid-day meal pilots create grassroots awareness, while the Agricultural and Processed Food Products Export Development Authority (APEDA) streamlines export logistics to monetize diaspora demand. Trade data show a clear inflection in 2023 imports, underscoring latent consumption potential that domestic farms have yet to satisfy.

Japan exemplifies an import-dependent, regulation-intensive destination. Ageing consumers value high protein and gluten-free labels, but packaging localization and residue testing escalate landed costs. Organic Japanese Agricultural Standards-European Union (JAS-EU) equivalency reduces paperwork for Europe exporters, threatening South American incumbents lacking similar recognition. Retailers leverage quinoa in convenience formats such as salads and instant cups, aligning with on-the-go consumption patterns.

Competitive Landscape

The Asia-Pacific quinoa seed market features diversified upstream cultivation while signaling downstream consolidation. Public research institutions play a significant role in seed breeding and varietal release, maintaining an upstream environment where intellectual property largely remains in the public domain. AgriFutures Australia’s 2024–2029 plan exemplifies this approach by providing Kruso White and two additional drought-tolerant lines to growers without licensing fees, thereby reducing entry barriers for Australian farmers. Similarly, in China, state universities have screened over 300 accessions in Shanxi to identify low-altitude genotypes, while more than 100 registered processors compete for urban shelf space. Midstream fragmentation continues as most mills process washing, scarification, and drying in small batches, resulting in low switching costs and fostering regional competition.

Downstream, consolidation is accelerating as multinational food companies pursue higher margins in health-focused channels. Saco Foods' acquisition of Ancient Harvest in August 2024 provided the company with a leading quinoa brand and established distribution networks in North America, which it can utilize to expand into Asian premium retail markets. In India, Nourish You collaborated with local research institutes over two years to develop a millet-quinoa beverage line, positioning the company to scale exports as domestic processing capabilities align with growing demand. In Australia, Keen Wah leveraged a government innovation grant to introduce its Fig and Maple Quinoa Granola into national supermarket chains, highlighting the impact of public funding in expanding product availability.

Technology and regulatory compliance are shaping long-term competitive advantages in the market. Genome-wide association studies published in 2024 identified loci accounting for up to 19.2% of flowering-time variance, providing breeders with marker-assisted tools to reduce development cycles. Drone-based phenotyping trials conducted in Peru achieved yield-predictive indices exceeding 0.80, highlighting opportunities for precision agriculture services that large agribusinesses can commercialize. Olam Agri’s collaboration with 2,100 Peruvian smallholders integrates traceability software with extension support, enabling buyers to access verifiable sustainability data while securing supply chains. Additionally, regulatory measures such as Japan’s Positive List and China’s Decree 248 have increased testing and registration costs, favoring larger players with the capacity to absorb these expenses. This has resulted in moderate market concentration, with branded leaders accounting for approximately half of retail value, while raw-grain sourcing remains highly fragmented.

Recent Industry Developments

- May 2024: Bhutan officially launched the One Country One Priority Product (OCOP) initiative during the Bhutan Agrifood Trade and Investment Forum. This initiative emphasizes the promotion of quinoa, selected for its high nutritional value, potential to enhance farmers' income, and suitability for export and trade.

- December 2023: AgriFutures Australia published the Australian Quinoa Research, Development and Extension Plan 2024-2029, a strategic framework prioritizing drought-tolerant cultivar development, mechanized harvesting protocols, and value-chain coordination to transition quinoa from boutique production to broadacre commercial scale. The plan identifies Western Australia, South Australia, and Queensland as priority regions for agronomic trials and commits funding to multi-location yield testing, a critical step toward de-risking farmer investment in quinoa cultivation.

- June 2023: Nourish You, an Indian superfood company co-founded by Rakesh Kilaru, announced its ambition to transition India from net importer to net exporter of quinoa and chia seeds, supported by a product portfolio including vegan mueslis, edible seeds, and a newly launched millet milk blend developed over two years in collaboration with premier Indian research institutions. The company's focus on clean-label, fair-trade, and preservative-free products positions it to capture growing domestic demand for plant-based alternatives

Asia-Pacific Quinoa Seeds Market Report Scope

The Asia-Pacific Quinoa Seed Market Report is Segmented by Geography (China, Japan, Australia, and India). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, Regulatory Framework, Logistics and Infrastructure, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Geography

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Asia-Pacific quinoa seed market?

The market stands at USD 1.61 billion in 2026 and is forecast to reach USD 2.30 billion by 2031.

Which country holds the largest share of Asia-Pacific quinoa demand?

China leads with 41% share, supported by extensive provincial cultivation and over 100 processors.

Why is India considered the fastest-growing geography for quinoa?

Government seed programs, expanding e-commerce, and clean-label product launches underpin a 12% CAGR through 2031.

What agronomic breakthrough is accelerating quinoa adoption in Australia?

The release of the Kruso White variety, delivering profitable yields under rain-fed conditions, has doubled gross margins compared with wheat and canola rotations.